Finance Case Study: Time Value of Money, Risk, and Return Analysis

VerifiedAdded on 2020/10/05

|9

|2102

|119

Case Study

AI Summary

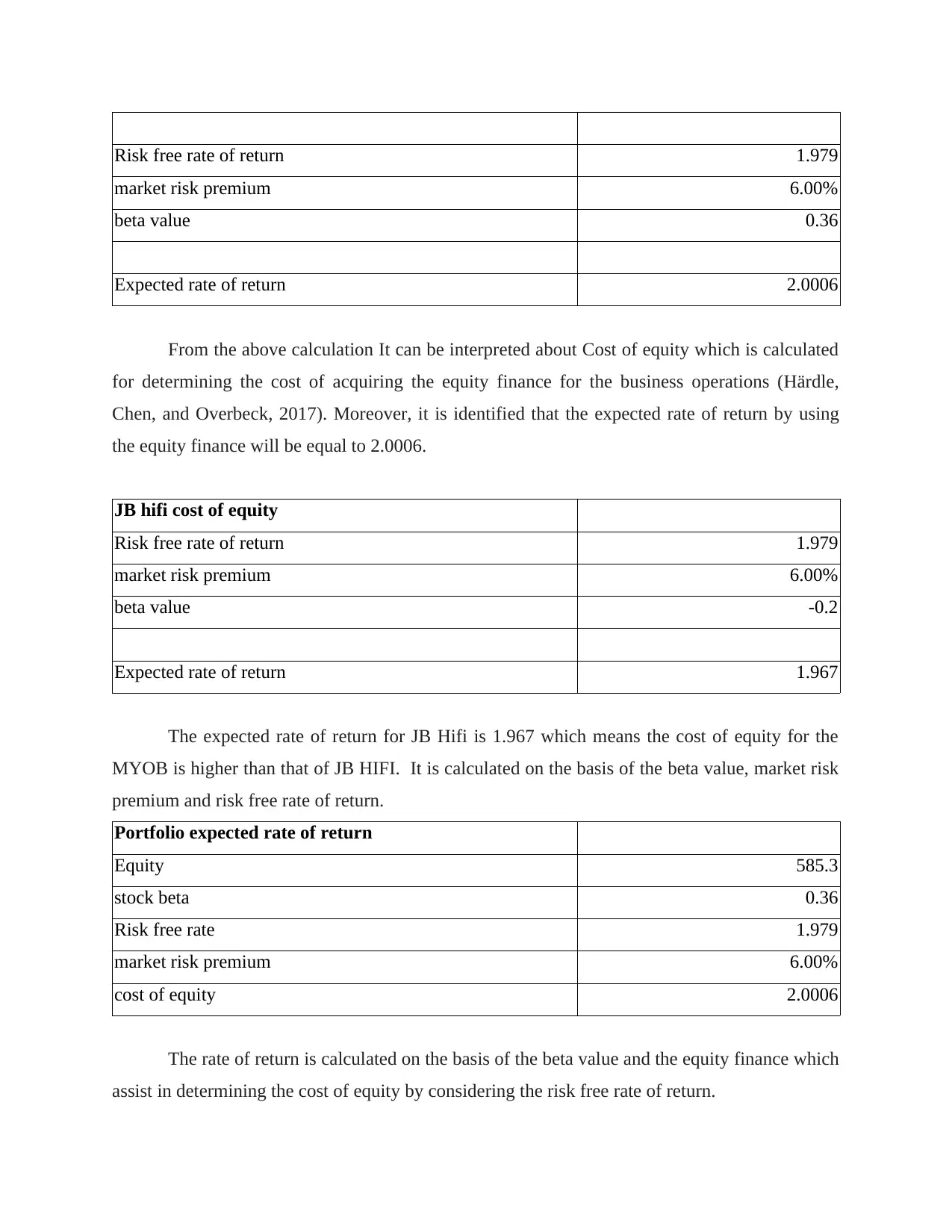

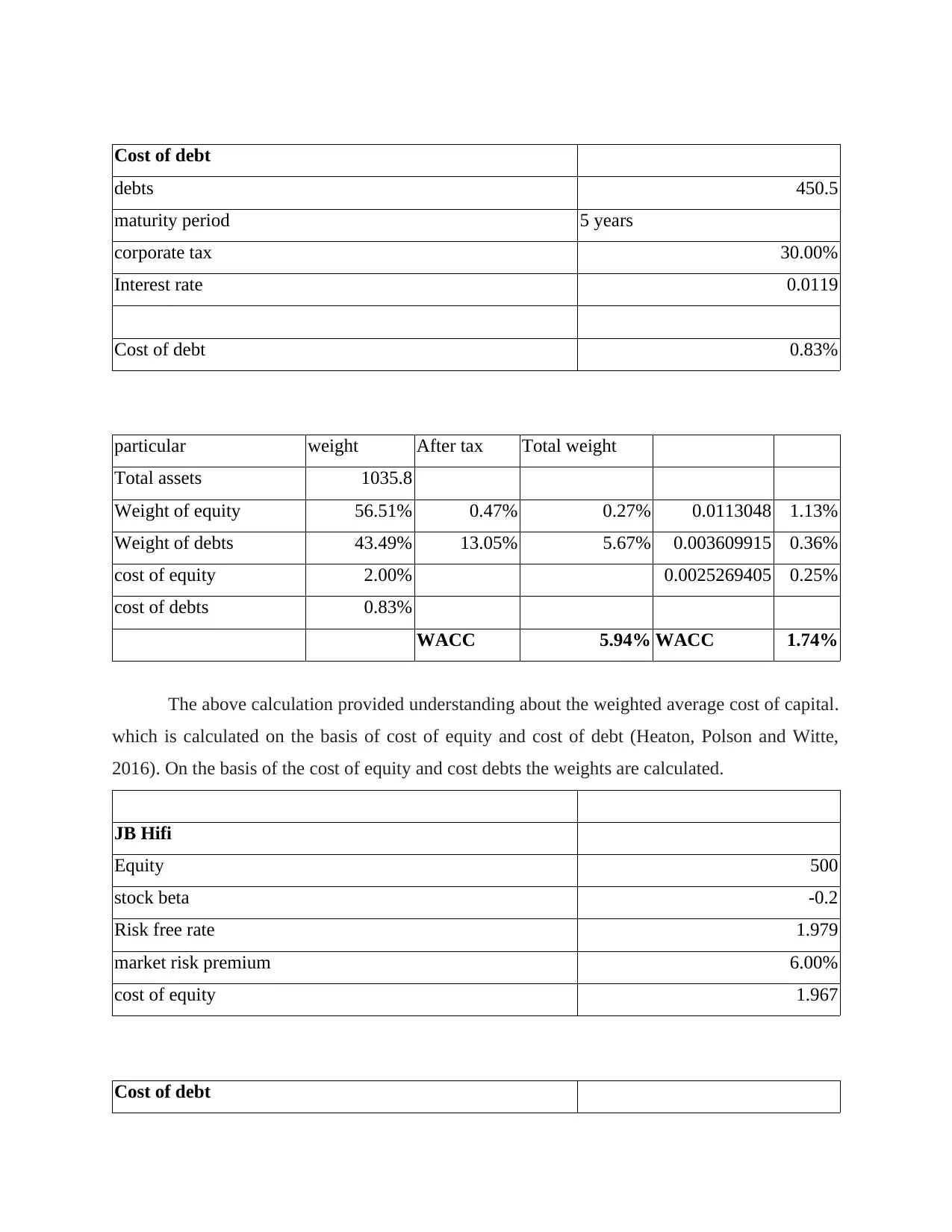

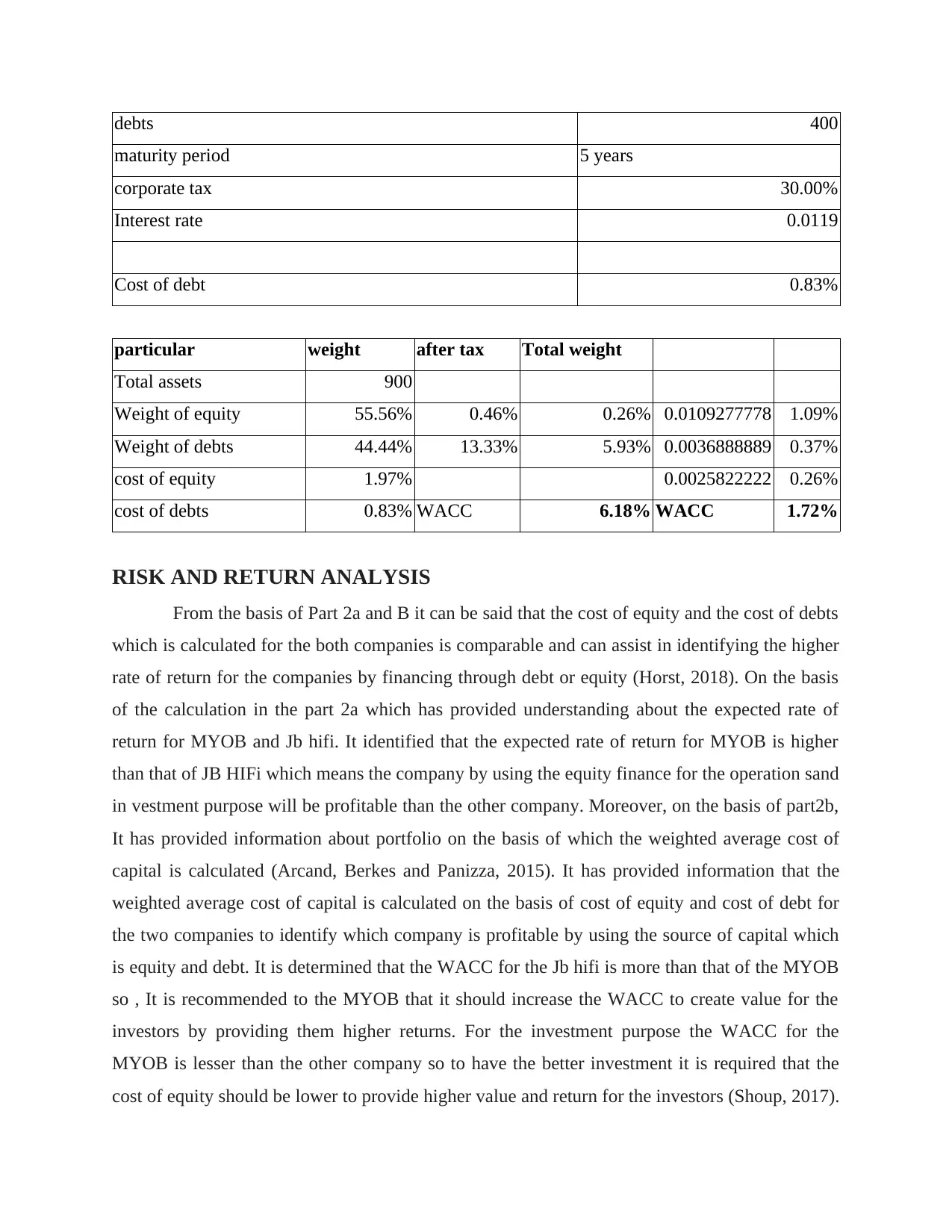

This finance case study analyzes various financial aspects, including time value of money (TVM) and bond valuation, for companies like MYOB and JB Hi-Fi. The assignment delves into calculating cash flows, annual operating revenue, effective annual rates (EAR) of loan options, and quarterly payments. It also determines the yield to maturity of bonds and coupon payments. Furthermore, the case study estimates and analyzes risk and return, calculating the cost of equity, expected rates of return, and weighted average cost of capital (WACC) for both companies. The analysis compares the financial performance of MYOB and JB Hi-Fi, offering insights into their investment potential and the importance of WACC in creating value for investors. The report concludes with a summary of the key findings and recommendations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.