Finance Homework: Project Evaluation and Portfolio Analysis

VerifiedAdded on 2022/10/11

|4

|442

|76

Homework Assignment

AI Summary

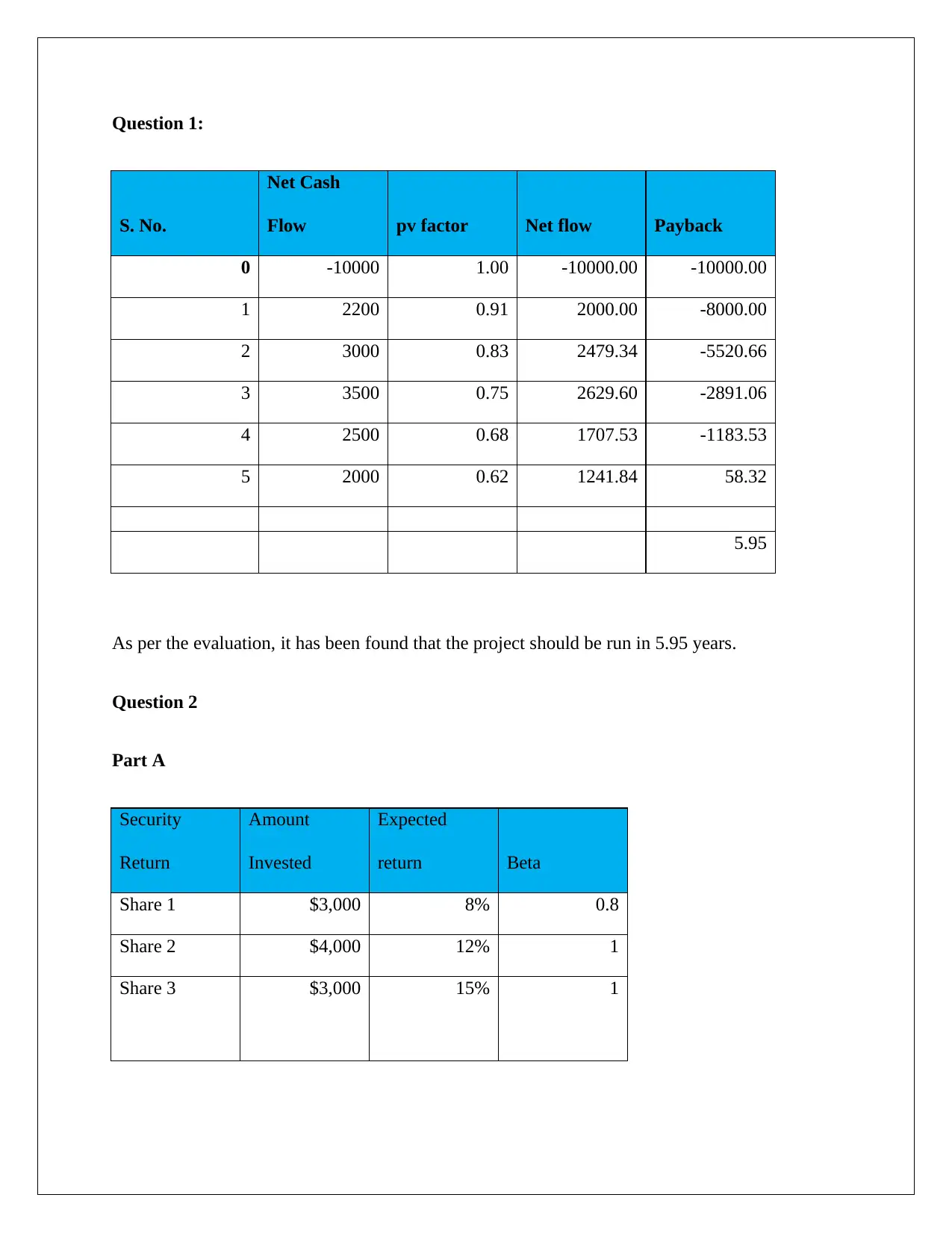

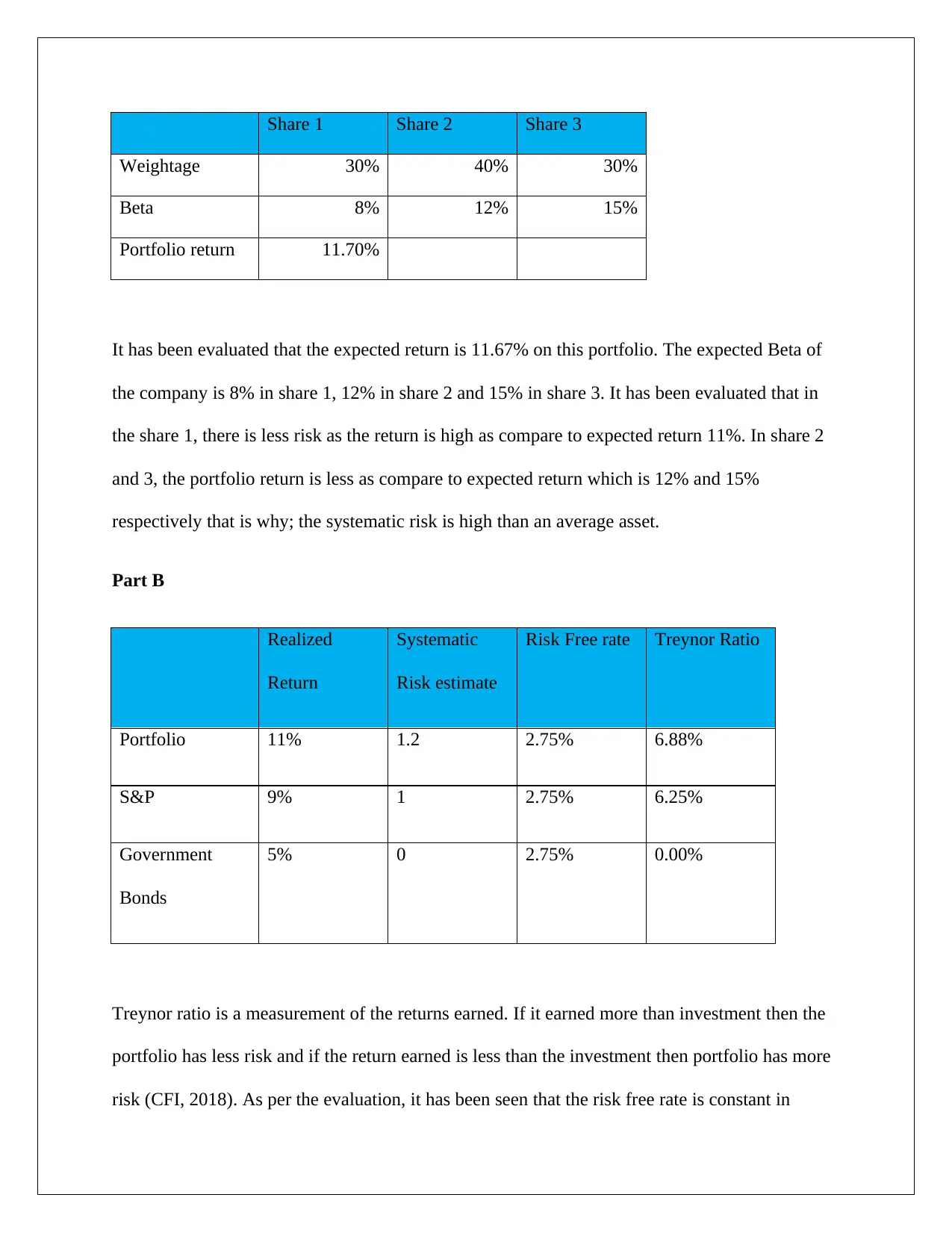

This document presents a detailed solution to a finance homework assignment, encompassing two key questions. The first question focuses on project evaluation, calculating the payback period using net cash flow and present value factors. The analysis determines the project's viability based on a 5.95-year payback period. The second question delves into portfolio analysis, examining the returns and risks associated with a diversified portfolio. Part A calculates the expected return of the portfolio, considering the amount invested, expected return, and beta for each security. Part B assesses the portfolio's performance using the Treynor ratio, comparing the realized return, systematic risk, and risk-free rate to evaluate risk-adjusted returns against market benchmarks like S&P and government bonds. The solution provides insights into the risk and return characteristics of the portfolio, demonstrating how to evaluate investment performance.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.