Finance Assignment: Analysis of Risk and Return for CSL and Portfolio

VerifiedAdded on 2021/06/18

|4

|674

|45

Report

AI Summary

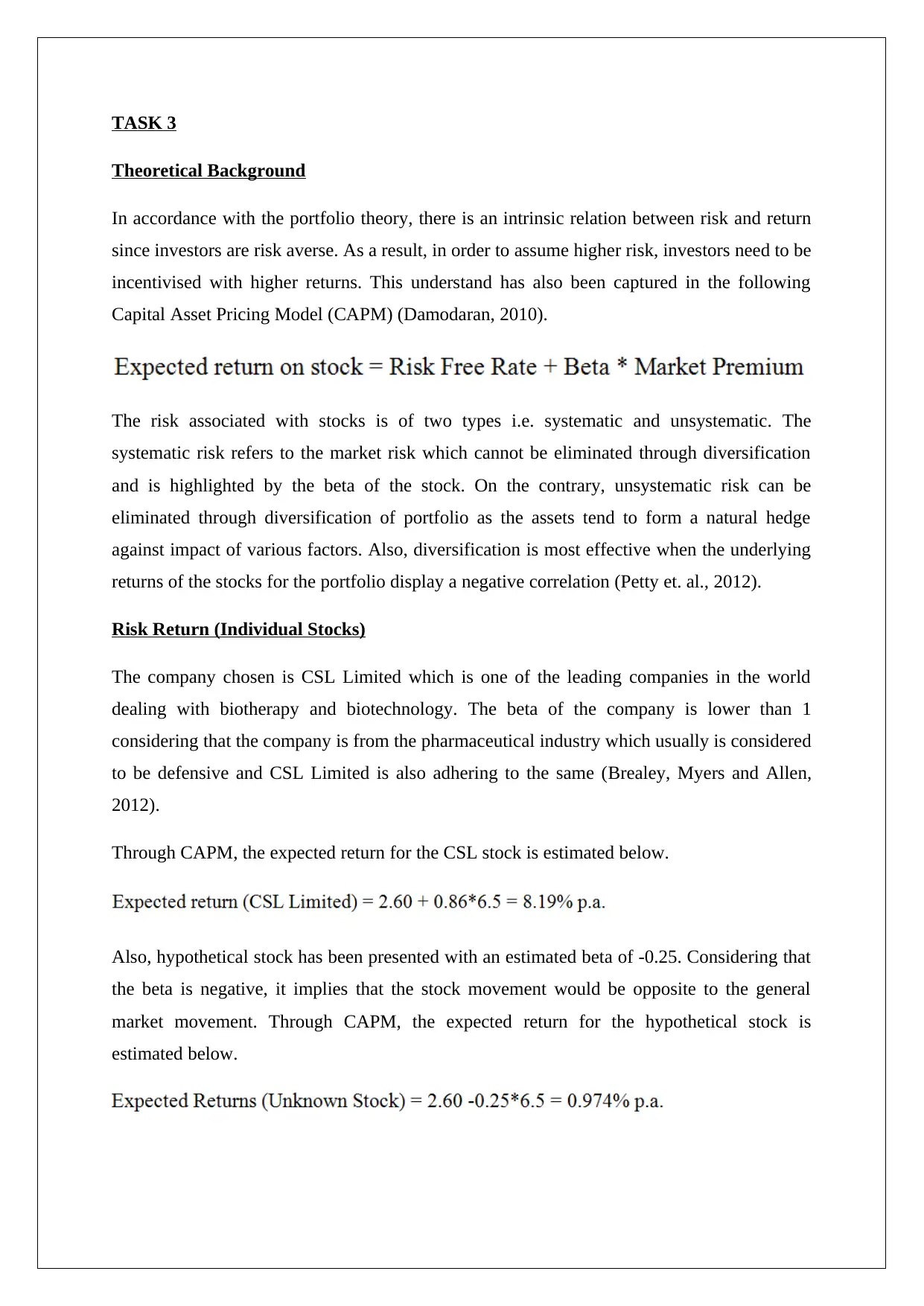

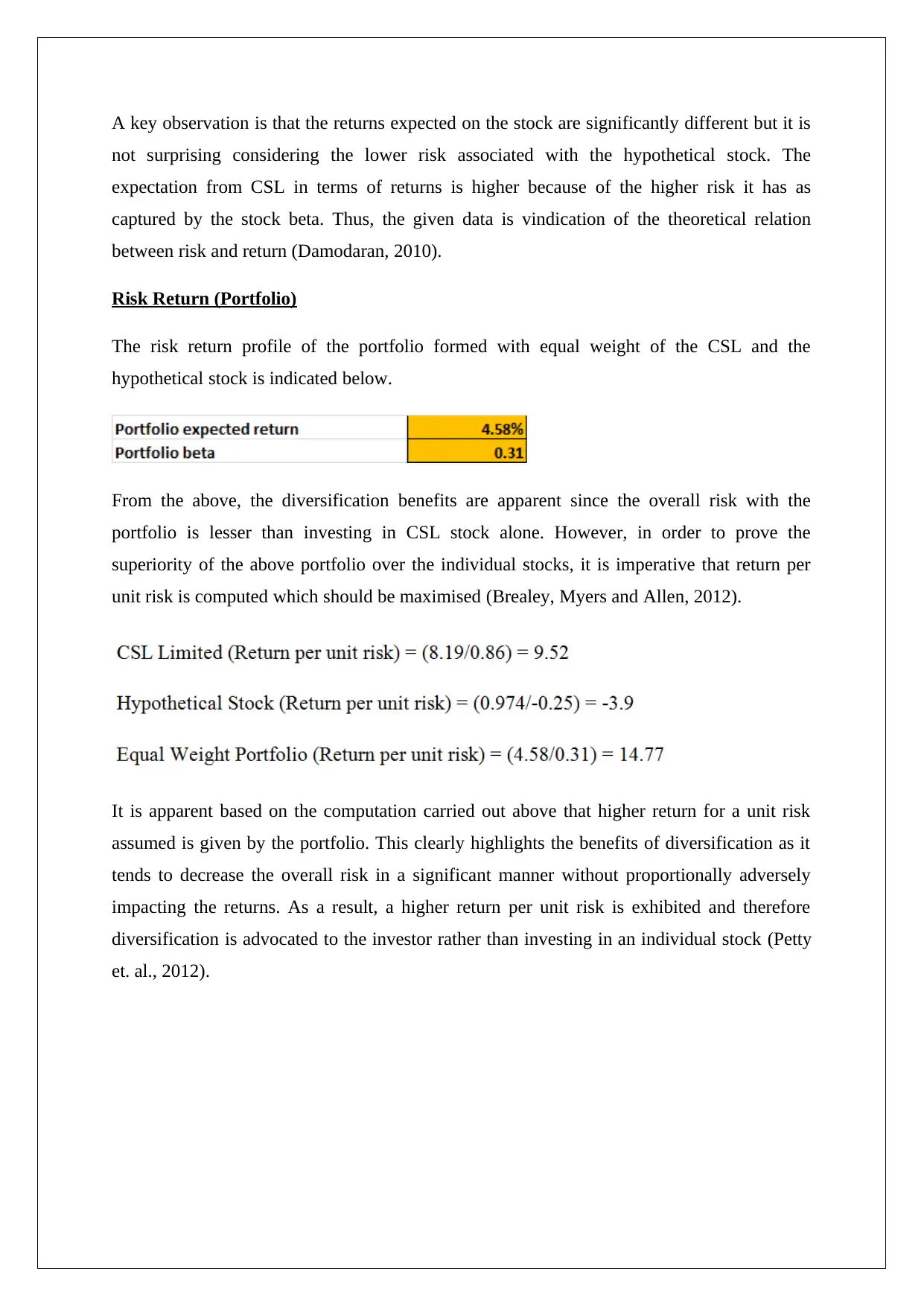

This report analyzes the relationship between risk and return in finance, focusing on the Capital Asset Pricing Model (CAPM) and portfolio construction. It examines how diversification can reduce risk without significantly impacting returns. The report uses the example of a real company (CSL) and a hypothetical stock to illustrate these concepts. The report highlights the benefits of diversification through the analysis of a portfolio that includes CSL and a hypothetical stock, and the importance of considering the return per unit of risk. The analysis demonstrates how a well-diversified portfolio can improve risk-adjusted returns, making it a valuable tool for investors. The document also includes a list of references used for the analysis.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.