BUS-FP3062 - Fundamentals of Finance: Risk and Return Assessment

VerifiedAdded on 2022/08/22

|6

|789

|20

Homework Assignment

AI Summary

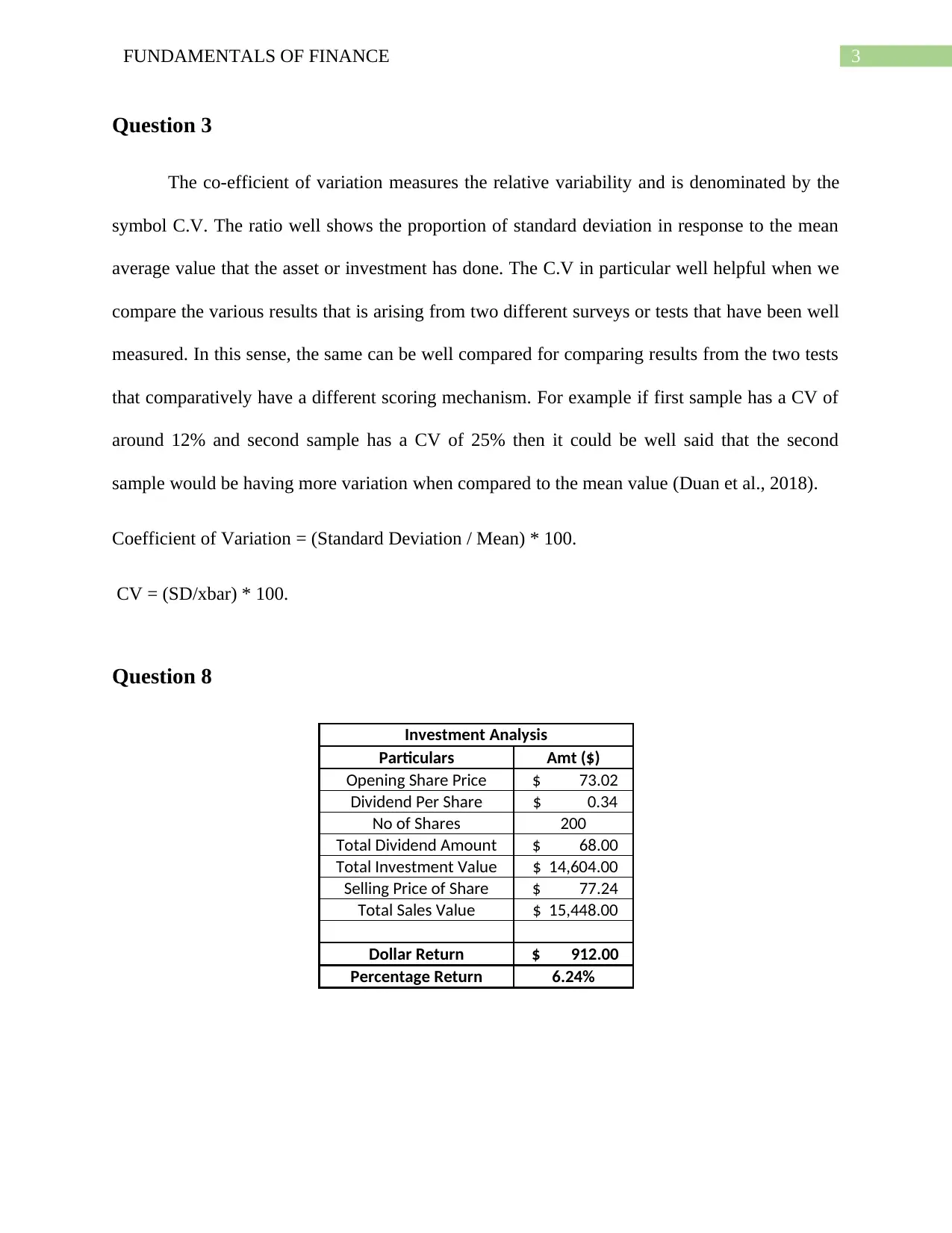

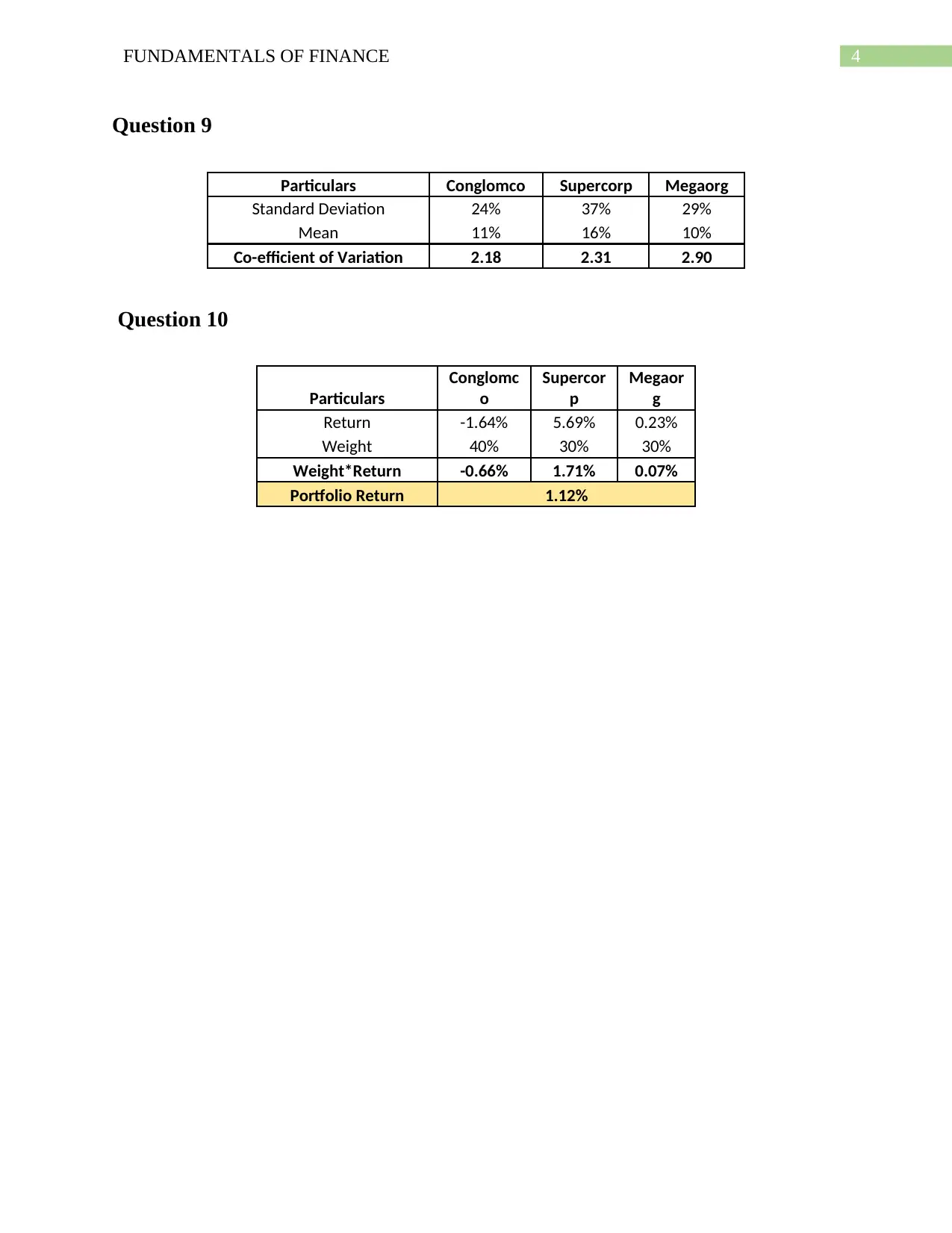

This assignment, completed for a Fundamentals of Finance course, addresses key concepts in financial risk and return. It begins by defining risk and its measurement through volatility, explaining the difference between actual and expected returns. The assignment then distinguishes between market risk and firm-specific risk, emphasizing how they affect investments. The coefficient of variation is explained as a measure of relative variability, with examples illustrating its application in comparing investment results. The solution includes calculations for dollar and percentage return on an investment, and the assignment concludes with a comparative analysis of risk and return for different companies (Conglomco, Supercorp, and Megaorg), calculating the coefficient of variation for each and determining portfolio return based on weighted returns.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.