In-depth Report on Corporate Finance: SML, CML, MVP and CAPM Analysis

VerifiedAdded on 2023/06/08

|12

|2984

|83

Report

AI Summary

This report provides a detailed analysis of key corporate finance concepts including the Security Market Line (SML), Capital Market Line (CML), Minimum Variance Portfolio (MVP), and Capital Asset Pricing Model (CAPM). It elucidates the differences between SML and CML in terms of risk consideration, investment analysis methods, and result interpretation, highlighting the strengths of CML in analyzing portfolio risk. The significance of MVP in identifying low-risk portfolios and shielding investors from market volatility is explored. Furthermore, the report discusses the application of CAPM in determining the required rate of return for investors, weighing its ease of use against its limitations related to assumptions. The report concludes by emphasizing the importance of these models in informing investment decisions and managing risk.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

1

Table of Contents

Introduction:...............................................................................................................................2

Exploring the difference between security market line (SML) and capital market line (CML):

....................................................................................................................................................2

Exploring the significance of Minimum Variance Portfolio (MVP):........................................5

Exploring why CAPM calculation is used for identifying the required rate of return by

investors:....................................................................................................................................7

Conclusion:................................................................................................................................9

References and Bibliography:..................................................................................................10

1

Table of Contents

Introduction:...............................................................................................................................2

Exploring the difference between security market line (SML) and capital market line (CML):

....................................................................................................................................................2

Exploring the significance of Minimum Variance Portfolio (MVP):........................................5

Exploring why CAPM calculation is used for identifying the required rate of return by

investors:....................................................................................................................................7

Conclusion:................................................................................................................................9

References and Bibliography:..................................................................................................10

CORPORATE FINANCE

2

Introduction:

The assessment evaluates the significance of Security market line, capital market line,

minimum variance portfolio and Capital Asset pricing model. In addition, the investors

intends to formulate the portfolio, which has returns and low risk from investment. The

assessment sheds light on the difference between the security market line and capital market

line, which is used for understanding the risk and return attributes of an investment.

Minimum variance portfolio is considered to be one of the viable approaches, which is used

by investors for contemplating the future returns and risk associated with investment.

Furthermore, the belief of investors on CAPM Model is relatively high, as the technique has

allowed the investors to detect the minimum returns that should be provided by investment in

comparison to its risk attribute.

Exploring the difference between security market line (SML) and capital market line

(CML):

Figure 1: Security Market Line (SML) Graph

(Source: Brooks and Mukherjee 2013)

2

Introduction:

The assessment evaluates the significance of Security market line, capital market line,

minimum variance portfolio and Capital Asset pricing model. In addition, the investors

intends to formulate the portfolio, which has returns and low risk from investment. The

assessment sheds light on the difference between the security market line and capital market

line, which is used for understanding the risk and return attributes of an investment.

Minimum variance portfolio is considered to be one of the viable approaches, which is used

by investors for contemplating the future returns and risk associated with investment.

Furthermore, the belief of investors on CAPM Model is relatively high, as the technique has

allowed the investors to detect the minimum returns that should be provided by investment in

comparison to its risk attribute.

Exploring the difference between security market line (SML) and capital market line

(CML):

Figure 1: Security Market Line (SML) Graph

(Source: Brooks and Mukherjee 2013)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

3

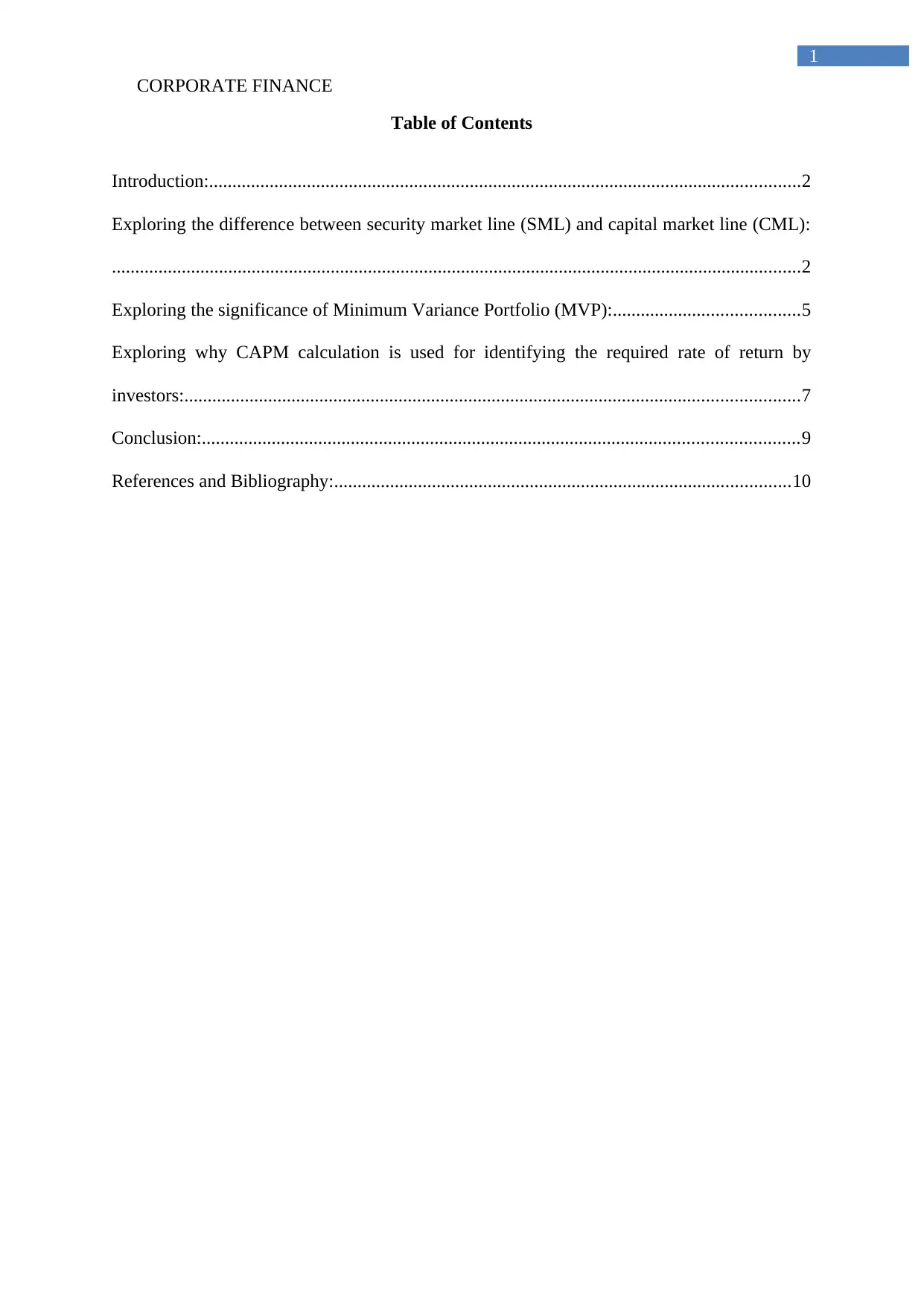

Figure 2: Capital Market Line (CML) Graph

(Source: Christensen, Hail and Leuz 2016)

The above figure 1 and 2 relatively depict the SML and CML graph, which could be

used by investor for analyzing the current trajectory of the stocks and determine its return and

risk attribute. Furthermore, the graph adequately indicates that with the help of security

market line the investors are able to understand the level of relationship between the

systematic risk and return from investment. This is mainly contemplated by using the

expected return and beta of the stock to determine the minimum returns that it needs to

provide during the investment phase. On the other hand, figure 2 depict the curve, which is

created by using different portfolio weights that helps in detecting the minimum risk that

could be generated from a particular portfolio. The further differences between the capital

SML and CML are elaborated as follows.

Difference is risk consideration:

There are different risk attributes associated with the capital market line and security

market line, which is detected in the calculation of risk and reward section of the

investment. This alteration in the risk consideration directly alters the way which an investor

3

Figure 2: Capital Market Line (CML) Graph

(Source: Christensen, Hail and Leuz 2016)

The above figure 1 and 2 relatively depict the SML and CML graph, which could be

used by investor for analyzing the current trajectory of the stocks and determine its return and

risk attribute. Furthermore, the graph adequately indicates that with the help of security

market line the investors are able to understand the level of relationship between the

systematic risk and return from investment. This is mainly contemplated by using the

expected return and beta of the stock to determine the minimum returns that it needs to

provide during the investment phase. On the other hand, figure 2 depict the curve, which is

created by using different portfolio weights that helps in detecting the minimum risk that

could be generated from a particular portfolio. The further differences between the capital

SML and CML are elaborated as follows.

Difference is risk consideration:

There are different risk attributes associated with the capital market line and security

market line, which is detected in the calculation of risk and reward section of the

investment. This alteration in the risk consideration directly alters the way which an investor

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

4

can understand the systematic and unsystematic risk of an investment. The evaluation

directly indicates that capital market line uses standard deviation method for determining the

risk of an investment. On the other hand, security market line directly used as beta, as the risk

attribute for a particular investment. Therefore, with the help of Beta adequate this attribute

of a particular stock is calculated by security market line, while the standard deviation of

capital market line is used to detect the risk attribute of the portfolio (Epstein and Zin 2013).

Method of analyzing the investment:

The method of analyzing an investment is relatively different for both capital market

line and security market, which adequately helps the investor to detect the risk and return

attribute. Furthermore, the measures used by capital market line used to evaluate and analyze

different strokes, which combined in a particular portfolio. The risk and return attributes of

the portfolio is considered, which adequately allows the investors to detect a curve indicating

risk and return attributes of the portfolio. Nevertheless, SML analysis only one stock and

detect the return and risk attributes of the investment. Therefore, it can be understood that

investors looking for portfolio investment can use capital market line, while security market

line would help in choosing the return capability of a particular stock.

Alternating results:

The calculations conducted by capital market line relatively help in detecting an

efficient Frontier curve, which can help investors to understand the implication of different

weight class that can be used to formulate the portfolio. Capital market line eventually allows

the investors to create an adequate portfolio, which can generate higher returns while

engulfing low risk from investment. Nevertheless, SML eventually allows the investor to

understand the risk and return attributes of a particular stock by evaluating risk free rate and

market returns (Gagliardini and Gourieroux 2013).

Superiority in analyzing risk factors:

4

can understand the systematic and unsystematic risk of an investment. The evaluation

directly indicates that capital market line uses standard deviation method for determining the

risk of an investment. On the other hand, security market line directly used as beta, as the risk

attribute for a particular investment. Therefore, with the help of Beta adequate this attribute

of a particular stock is calculated by security market line, while the standard deviation of

capital market line is used to detect the risk attribute of the portfolio (Epstein and Zin 2013).

Method of analyzing the investment:

The method of analyzing an investment is relatively different for both capital market

line and security market, which adequately helps the investor to detect the risk and return

attribute. Furthermore, the measures used by capital market line used to evaluate and analyze

different strokes, which combined in a particular portfolio. The risk and return attributes of

the portfolio is considered, which adequately allows the investors to detect a curve indicating

risk and return attributes of the portfolio. Nevertheless, SML analysis only one stock and

detect the return and risk attributes of the investment. Therefore, it can be understood that

investors looking for portfolio investment can use capital market line, while security market

line would help in choosing the return capability of a particular stock.

Alternating results:

The calculations conducted by capital market line relatively help in detecting an

efficient Frontier curve, which can help investors to understand the implication of different

weight class that can be used to formulate the portfolio. Capital market line eventually allows

the investors to create an adequate portfolio, which can generate higher returns while

engulfing low risk from investment. Nevertheless, SML eventually allows the investor to

understand the risk and return attributes of a particular stock by evaluating risk free rate and

market returns (Gagliardini and Gourieroux 2013).

Superiority in analyzing risk factors:

CORPORATE FINANCE

5

Furthermore, capital market line has a security in analyzing the risk factor in

comparison to security market line, as it helps in drafting an adequate weightage, which could

be used for investment purposes. The security market line only evaluates the risk factors and

returns for the particular stock, which does not help in diversifying the disk attributes of the

investor. On the other hand, capital market line adequately evaluates different stocks to detect

the risk attribute of the total portfolio, which might allow the investor to detect the actual risk

factors affecting its investment.

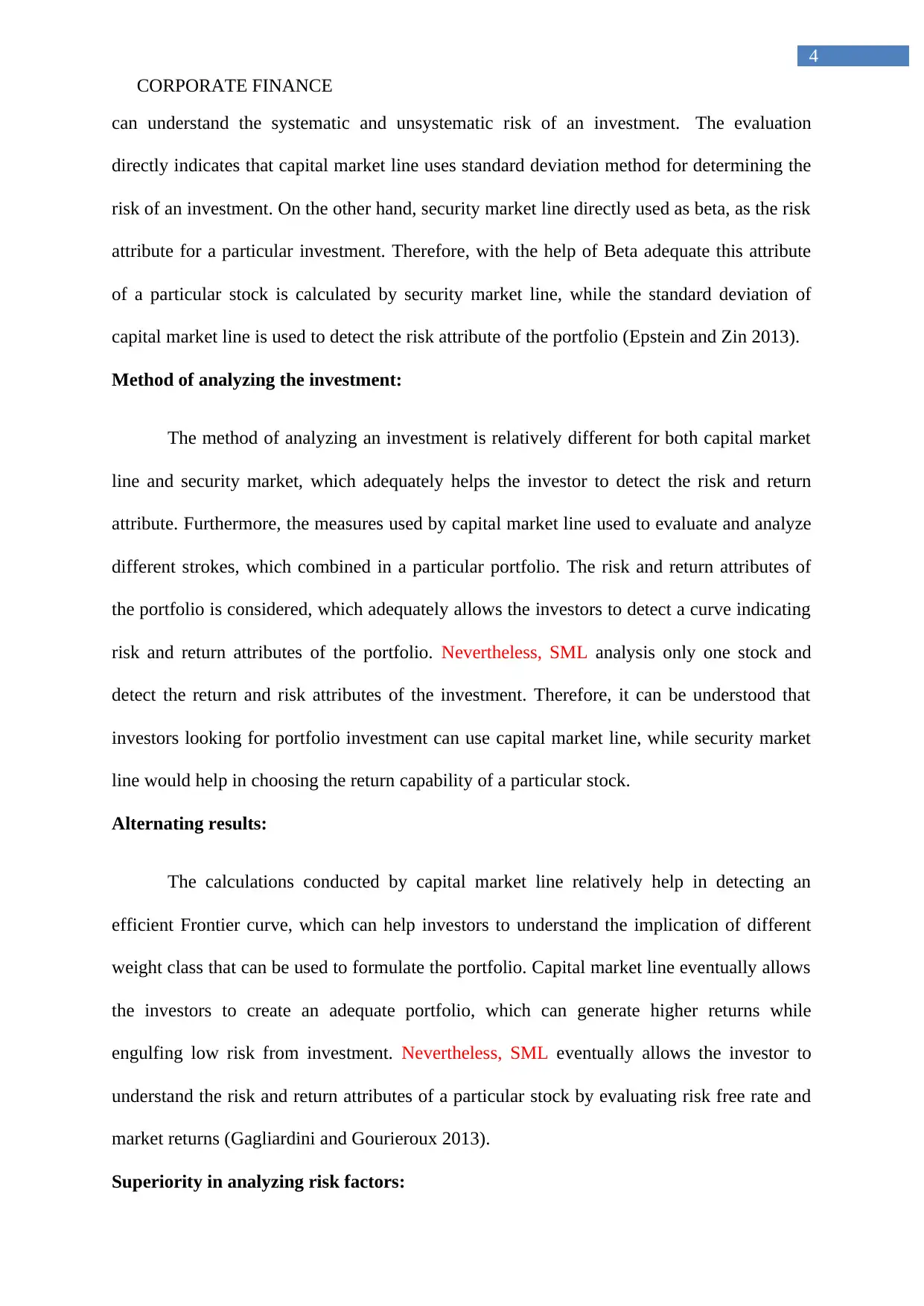

Exploring the significance of Minimum Variance Portfolio (MVP):

Figure 3: Minimum variance portfolio (MVP) graph

(Source: Xing, Hu and Yang 2014)

The minimum variance portfolio graph is adequate be detected in the above figure,

which relatively indicates the minimum risk that the portfolio can contemplate. Minimum

variance portfolio illuminates the investor to detect the overall weight of the stocks, which

might provide the highest return possible with the lowest risk affecting the investment. Bjork,

Murgoci and Zhou (2014) mentioned that investors using the minimum variance portfolio and

not able to maximize the returns from investment, as higher risk tends to generate high level

5

Furthermore, capital market line has a security in analyzing the risk factor in

comparison to security market line, as it helps in drafting an adequate weightage, which could

be used for investment purposes. The security market line only evaluates the risk factors and

returns for the particular stock, which does not help in diversifying the disk attributes of the

investor. On the other hand, capital market line adequately evaluates different stocks to detect

the risk attribute of the total portfolio, which might allow the investor to detect the actual risk

factors affecting its investment.

Exploring the significance of Minimum Variance Portfolio (MVP):

Figure 3: Minimum variance portfolio (MVP) graph

(Source: Xing, Hu and Yang 2014)

The minimum variance portfolio graph is adequate be detected in the above figure,

which relatively indicates the minimum risk that the portfolio can contemplate. Minimum

variance portfolio illuminates the investor to detect the overall weight of the stocks, which

might provide the highest return possible with the lowest risk affecting the investment. Bjork,

Murgoci and Zhou (2014) mentioned that investors using the minimum variance portfolio and

not able to maximize the returns from investment, as higher risk tends to generate high level

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

6

of returns. On the other hand, Yang et al. (2015) mentioned that minimum variance portfolio

is used by investors having a conservative investment attitude, as it comes in reducing the

risk level of investment, which does not let the investor to generate higher returns from

investment.

The significance of minimum variance portfolio is depicted as follows.

Identifying the lowest risk-generating portfolio:

The minimum variance portfolio adequately allows the investor to detect the low risk-

generating portfolio, which eventually helps in securing the overall investment capital. The

minimum variance portfolio directly values the different conditions in which an investment

can be conducted for reducing the total risk of the portfolio and maximizes its returns.

Moreover, the method directly uses a combination of different weights to improve returns

that could be generated from an investment. Consequently, investors with the conservative

outlook can use the minimum variance portfolio for securing the investment and maximizing

the level of returns, which could be generated from the particular risk exposure.

Minimizes the risk attributes of investment:

Furthermore, investors using the minimum variance portfolio are able to reduce the

level of risk attributes from the investment by combining different level of stocks. This

combination eventually supports the conservative investors to maximize the returns on a

given level of risk. The calculations conducted in the minimum variance portfolio directly

combine the stocks with different weights, where the investors are able to generate the lowest

risk from their investment by using the above method. Lehutova, Krizanova and Kliestik

(2013) argued that minimum variance portfolio loses its friction and value when an economic

crisis occurs, as the whole capital market is negatively affected.

Shielding investors from volatile capital market fluctuations:

6

of returns. On the other hand, Yang et al. (2015) mentioned that minimum variance portfolio

is used by investors having a conservative investment attitude, as it comes in reducing the

risk level of investment, which does not let the investor to generate higher returns from

investment.

The significance of minimum variance portfolio is depicted as follows.

Identifying the lowest risk-generating portfolio:

The minimum variance portfolio adequately allows the investor to detect the low risk-

generating portfolio, which eventually helps in securing the overall investment capital. The

minimum variance portfolio directly values the different conditions in which an investment

can be conducted for reducing the total risk of the portfolio and maximizes its returns.

Moreover, the method directly uses a combination of different weights to improve returns

that could be generated from an investment. Consequently, investors with the conservative

outlook can use the minimum variance portfolio for securing the investment and maximizing

the level of returns, which could be generated from the particular risk exposure.

Minimizes the risk attributes of investment:

Furthermore, investors using the minimum variance portfolio are able to reduce the

level of risk attributes from the investment by combining different level of stocks. This

combination eventually supports the conservative investors to maximize the returns on a

given level of risk. The calculations conducted in the minimum variance portfolio directly

combine the stocks with different weights, where the investors are able to generate the lowest

risk from their investment by using the above method. Lehutova, Krizanova and Kliestik

(2013) argued that minimum variance portfolio loses its friction and value when an economic

crisis occurs, as the whole capital market is negatively affected.

Shielding investors from volatile capital market fluctuations:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

7

Moreover, minimum variance portfolio also Shields the investors from volatile capital

market fluctuations, which occur frequently due to the presence of continuous demand and

supply. The fluctuations in capital market directly respond to the improvements and the

growth obtained by organizations, which are listed in the index. The changes in value

eventually fluctuates the prices of a particular stock and hampers the investment scope.

Therefore, implementation of MVP investors are able to diversify the investment, which

reduces the level of negative impact that capital market can have on the portfolio returns.

Hence, it could be identified that minimum variance portfolio acts as an insurance for the

investors, which allows them to generate high returns from investment.

Combining both low risk and high-risk stocks:

The major significance of the minimum variance portfolio is its capability to combine

both lowest and highest stock in a particular investment portfolio to generate high returns.

The calculations conducted in the minimum variance portfolio directly allow the investor to

understand the level of risk attribute that is affecting their Investments. Hence, the

combination of both lowest and highest stocks directly helps in improving the level of returns

valued using the risk attributes from investment.

Exploring why CAPM calculation is used for identifying the required rate of return by

investors:

Figure 4: Capital Asset Pricing Model (CAPM)

(Source: Bao, Diks and Li 2018)

7

Moreover, minimum variance portfolio also Shields the investors from volatile capital

market fluctuations, which occur frequently due to the presence of continuous demand and

supply. The fluctuations in capital market directly respond to the improvements and the

growth obtained by organizations, which are listed in the index. The changes in value

eventually fluctuates the prices of a particular stock and hampers the investment scope.

Therefore, implementation of MVP investors are able to diversify the investment, which

reduces the level of negative impact that capital market can have on the portfolio returns.

Hence, it could be identified that minimum variance portfolio acts as an insurance for the

investors, which allows them to generate high returns from investment.

Combining both low risk and high-risk stocks:

The major significance of the minimum variance portfolio is its capability to combine

both lowest and highest stock in a particular investment portfolio to generate high returns.

The calculations conducted in the minimum variance portfolio directly allow the investor to

understand the level of risk attribute that is affecting their Investments. Hence, the

combination of both lowest and highest stocks directly helps in improving the level of returns

valued using the risk attributes from investment.

Exploring why CAPM calculation is used for identifying the required rate of return by

investors:

Figure 4: Capital Asset Pricing Model (CAPM)

(Source: Bao, Diks and Li 2018)

CORPORATE FINANCE

8

The formula for CAPM is adequately depicted in the above figure, which is used by

investors to identify the level of expected returns from and investment. Moreover, the

calculation also depicts that the expected return and the identified as cost of equity for

deriving the overall value of WACC (Weighted Average Cost of Capital) of the organization.

WACC is one of the measures that CAPM allows the investors to identify and detect the level

of investments that needs to be conducted in a particular stock. Furthermore, the assumptions

made by the Capital Asset pricing model such as risk free rate and market premium directly

allows the investor to detect the level of expected returns, which needs to be provided by the

company. On the other hand, Bornholt (2013) argued that CAPM only allows the investor to

analyze only one stock and does not increase its reach in evaluating the whole portfolio.

There are other models which has been used by investors for identifying the return

and risk capability of a particular stock. Model such as Fama French Three Factor Model and

Modified Fama French model are used in the absence of Capital Asset pricing model. These

measures are relatively used for improving enhancing the output result, which is not possible

by the simple Capital Asset pricing model method. However, different theories and methods

used for calculating the expected return needs high-end calculations and statistical data,

which is not used in the simple Capital Asset pricing model. The simplicity of the model

relatively makes it more attractive for investors to analyze the level of risk and return

attributes of a particular stock (Dempsey 2013).

The simplicity relatively makes the Capital Asset pricing model to be one of the

adequate methods, which can be used by investors to understand the expected returns from a

particular stock. However, there are certain advantages and disadvantages towards the use of

Capital Asset pricing model, which can increase or reduce the problems of an investor.

Ease of use (Significance):

8

The formula for CAPM is adequately depicted in the above figure, which is used by

investors to identify the level of expected returns from and investment. Moreover, the

calculation also depicts that the expected return and the identified as cost of equity for

deriving the overall value of WACC (Weighted Average Cost of Capital) of the organization.

WACC is one of the measures that CAPM allows the investors to identify and detect the level

of investments that needs to be conducted in a particular stock. Furthermore, the assumptions

made by the Capital Asset pricing model such as risk free rate and market premium directly

allows the investor to detect the level of expected returns, which needs to be provided by the

company. On the other hand, Bornholt (2013) argued that CAPM only allows the investor to

analyze only one stock and does not increase its reach in evaluating the whole portfolio.

There are other models which has been used by investors for identifying the return

and risk capability of a particular stock. Model such as Fama French Three Factor Model and

Modified Fama French model are used in the absence of Capital Asset pricing model. These

measures are relatively used for improving enhancing the output result, which is not possible

by the simple Capital Asset pricing model method. However, different theories and methods

used for calculating the expected return needs high-end calculations and statistical data,

which is not used in the simple Capital Asset pricing model. The simplicity of the model

relatively makes it more attractive for investors to analyze the level of risk and return

attributes of a particular stock (Dempsey 2013).

The simplicity relatively makes the Capital Asset pricing model to be one of the

adequate methods, which can be used by investors to understand the expected returns from a

particular stock. However, there are certain advantages and disadvantages towards the use of

Capital Asset pricing model, which can increase or reduce the problems of an investor.

Ease of use (Significance):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

9

Capital Asset pricing model is an adequate measure, which allows investor to use

three different factors to detect the expected returns from investment. The method is

relatively simple and can be used by investors without the need for statistical calculations.

The simplicity of the Capital Asset pricing model actually appeals to the investors and allows

them to detect the level of returns, which could be generated from a stock at a certain beta.

Wide range of assumptions (Limitations):

However, there are certain limitations to the Capital Asset pricing model, which are is

used by investors while calculating the returns. The calculation adequately assumes the level

of market returns and risk free rate, which is used for calculating the expected return of the

stock. The investors can ignore the identified limitations, as it provides an adequate gist of

the total returns that a stock should provide from investment (Dzaja and Aljinovic 2013).

Conclusion:

The evaluation of minimum variance portfolio, capital market line, security market

line, and Capital Asset pricing model has helped in depicting the level of measures that needs

to be taken by the investors creating their portfolio. Investors to improve their investment

scope and reduce the level of risk from investment relatively use the above-depicted theories.

The difference between security market line and capital market line has illuminated the

significance of an adequate portfolio creation method. The minimum variance portfolio

actually depicts the level of risk attribute an investor can provide while creating a portfolio.

Lastly, the everlasting presence of Capital Asset pricing model has allowed the investors to

analyze the stock for investment and detect the level of returns, which it should provide in

future. Therefore, understanding the level of measures that is considered by the above

theories, it can be detected that formulating an adequate portfolio for investment is a viable

option, which could allow investors to maximize their returns.

9

Capital Asset pricing model is an adequate measure, which allows investor to use

three different factors to detect the expected returns from investment. The method is

relatively simple and can be used by investors without the need for statistical calculations.

The simplicity of the Capital Asset pricing model actually appeals to the investors and allows

them to detect the level of returns, which could be generated from a stock at a certain beta.

Wide range of assumptions (Limitations):

However, there are certain limitations to the Capital Asset pricing model, which are is

used by investors while calculating the returns. The calculation adequately assumes the level

of market returns and risk free rate, which is used for calculating the expected return of the

stock. The investors can ignore the identified limitations, as it provides an adequate gist of

the total returns that a stock should provide from investment (Dzaja and Aljinovic 2013).

Conclusion:

The evaluation of minimum variance portfolio, capital market line, security market

line, and Capital Asset pricing model has helped in depicting the level of measures that needs

to be taken by the investors creating their portfolio. Investors to improve their investment

scope and reduce the level of risk from investment relatively use the above-depicted theories.

The difference between security market line and capital market line has illuminated the

significance of an adequate portfolio creation method. The minimum variance portfolio

actually depicts the level of risk attribute an investor can provide while creating a portfolio.

Lastly, the everlasting presence of Capital Asset pricing model has allowed the investors to

analyze the stock for investment and detect the level of returns, which it should provide in

future. Therefore, understanding the level of measures that is considered by the above

theories, it can be detected that formulating an adequate portfolio for investment is a viable

option, which could allow investors to maximize their returns.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

10

References and Bibliography:

Bao, T., Diks, C. and Li, H., 2018. A generalized CAPM model with asymmetric power

distributed errors with an application to portfolio construction. Economic Modelling, 68,

pp.611-621.

Björk, T., Murgoci, A. and Zhou, X.Y., 2014. Mean–variance portfolio optimization with

state‐dependent risk aversion. Mathematical Finance: An International Journal of

Mathematics, Statistics and Financial Economics, 24(1), pp.1-24.

Bornholt, G., 2013. The failure of the Capital Asset Pricing Model (CAPM): An update and

discussion. Abacus, 49, pp.36-43.

Brooks, R. and Mukherjee, A.K., 2013. Financial management: core concepts. Pearson.

Christensen, H.B., Hail, L. and Leuz, C., 2016. Capital-market effects of securities

regulation: Prior conditions, implementation, and enforcement. The Review of Financial

Studies, 29(11), pp.2885-2924.

Dempsey, M., 2013. The capital asset pricing model (CAPM): the history of a failed

revolutionary idea in finance?. Abacus, 49, pp.7-23.

Džaja, J. and Aljinović, Z., 2013. Testing CAPM model on the emerging markets of the

Central and Southeastern Europe. Croatian Operational Research Review, 4(1), pp.164-175.

Epstein, L.G. and Zin, S.E., 2013. Substitution, risk aversion and the temporal behavior of

consumption and asset returns: A theoretical framework. In Handbook Of The Fundamentals

Of Financial Decision Making: Part I(pp. 207-239).

Gagliardini, P. and Gouriéroux, C., 2013. Granularity adjustment for risk measures:

Systematic vs unsystematic risks. Int. J. Approx. Reasoning, 54(6), pp.717-747.

10

References and Bibliography:

Bao, T., Diks, C. and Li, H., 2018. A generalized CAPM model with asymmetric power

distributed errors with an application to portfolio construction. Economic Modelling, 68,

pp.611-621.

Björk, T., Murgoci, A. and Zhou, X.Y., 2014. Mean–variance portfolio optimization with

state‐dependent risk aversion. Mathematical Finance: An International Journal of

Mathematics, Statistics and Financial Economics, 24(1), pp.1-24.

Bornholt, G., 2013. The failure of the Capital Asset Pricing Model (CAPM): An update and

discussion. Abacus, 49, pp.36-43.

Brooks, R. and Mukherjee, A.K., 2013. Financial management: core concepts. Pearson.

Christensen, H.B., Hail, L. and Leuz, C., 2016. Capital-market effects of securities

regulation: Prior conditions, implementation, and enforcement. The Review of Financial

Studies, 29(11), pp.2885-2924.

Dempsey, M., 2013. The capital asset pricing model (CAPM): the history of a failed

revolutionary idea in finance?. Abacus, 49, pp.7-23.

Džaja, J. and Aljinović, Z., 2013. Testing CAPM model on the emerging markets of the

Central and Southeastern Europe. Croatian Operational Research Review, 4(1), pp.164-175.

Epstein, L.G. and Zin, S.E., 2013. Substitution, risk aversion and the temporal behavior of

consumption and asset returns: A theoretical framework. In Handbook Of The Fundamentals

Of Financial Decision Making: Part I(pp. 207-239).

Gagliardini, P. and Gouriéroux, C., 2013. Granularity adjustment for risk measures:

Systematic vs unsystematic risks. Int. J. Approx. Reasoning, 54(6), pp.717-747.

CORPORATE FINANCE

11

Horváthová, J. and Mokrišová, M., 2014. Determination of Cost of Equity for Selected

Enterprises of the Energy Industry Applying the CAPM Model and its Comparison with the

Model with Gradual Counting Risk Premium. Journal of Management and Business:

Research and Practice, 6(1), pp.43-54.

Hur, S.K. and Chung, C.Y., 2017. Revisiting CAPM betas in an incomplete market: Evidence

from the Korean stock market. Finance Research Letters, 21, pp.241-248.

Lal, I., Mubeen, M., Hussain, A. and Zubair, M., 2016. An empirical analysis of higher

moment capital asset pricing model for Karachi stock exchange (KSE). Open Journal of

Social Sciences, 4(06), p.53.

Lehutova, K., Krizanova, A. and Kliestik, T., 2013. Quantification of equity and debt capital

costs in the specific conditions of transport enterprises. In 17th International Conference on

Transport Means, Transport Means., Kaunas Univ Technol, Kaunas, Lithuania (pp. 258-

261).

Nasiri, M., Alishah, A.Y., Sayyahmelli, S.A.S. and Karimi, A., 2017. Estimating Expected

Return based on Capital Asset Pricing Model compared with Stock Interest Rate at Tehran

Stock Exchange. HELIX, 7(2), pp.1406-1415.

Xing, X., Hu, J. and Yang, Y., 2014. Robust minimum variance portfolio with L-infinity

constraints. Journal of Banking & Finance, 46, pp.107-117.

Yang, L., Couillet, R. and McKay, M.R., 2015. A robust statistics approach to minimum

variance portfolio optimization. IEEE Transactions on Signal Processing, 63(24), pp.6684-

6697.

11

Horváthová, J. and Mokrišová, M., 2014. Determination of Cost of Equity for Selected

Enterprises of the Energy Industry Applying the CAPM Model and its Comparison with the

Model with Gradual Counting Risk Premium. Journal of Management and Business:

Research and Practice, 6(1), pp.43-54.

Hur, S.K. and Chung, C.Y., 2017. Revisiting CAPM betas in an incomplete market: Evidence

from the Korean stock market. Finance Research Letters, 21, pp.241-248.

Lal, I., Mubeen, M., Hussain, A. and Zubair, M., 2016. An empirical analysis of higher

moment capital asset pricing model for Karachi stock exchange (KSE). Open Journal of

Social Sciences, 4(06), p.53.

Lehutova, K., Krizanova, A. and Kliestik, T., 2013. Quantification of equity and debt capital

costs in the specific conditions of transport enterprises. In 17th International Conference on

Transport Means, Transport Means., Kaunas Univ Technol, Kaunas, Lithuania (pp. 258-

261).

Nasiri, M., Alishah, A.Y., Sayyahmelli, S.A.S. and Karimi, A., 2017. Estimating Expected

Return based on Capital Asset Pricing Model compared with Stock Interest Rate at Tehran

Stock Exchange. HELIX, 7(2), pp.1406-1415.

Xing, X., Hu, J. and Yang, Y., 2014. Robust minimum variance portfolio with L-infinity

constraints. Journal of Banking & Finance, 46, pp.107-117.

Yang, L., Couillet, R. and McKay, M.R., 2015. A robust statistics approach to minimum

variance portfolio optimization. IEEE Transactions on Signal Processing, 63(24), pp.6684-

6697.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.