Finance Assignment Solution: Budgeting, Costing, Overhead Analysis

VerifiedAdded on 2020/04/01

|6

|1494

|74

Homework Assignment

AI Summary

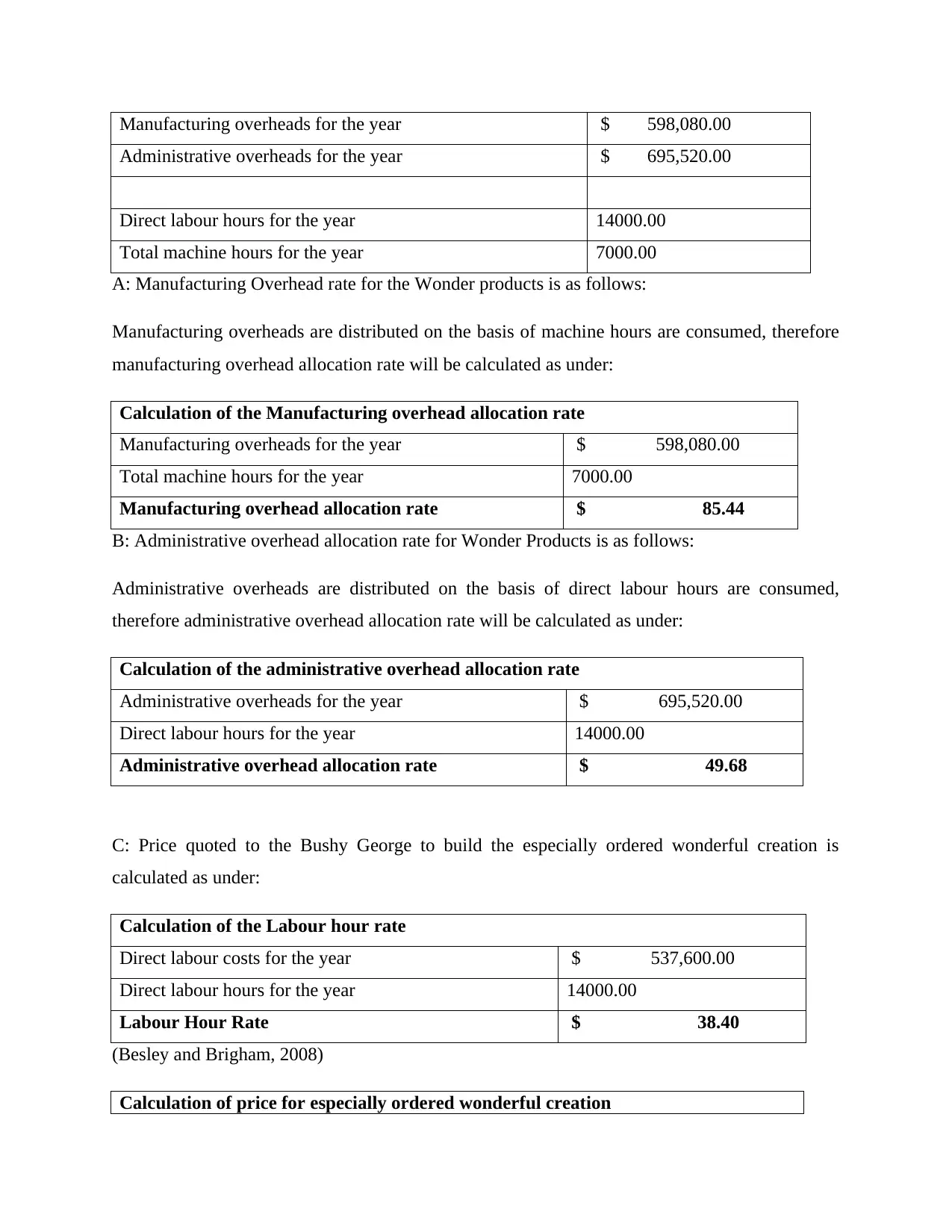

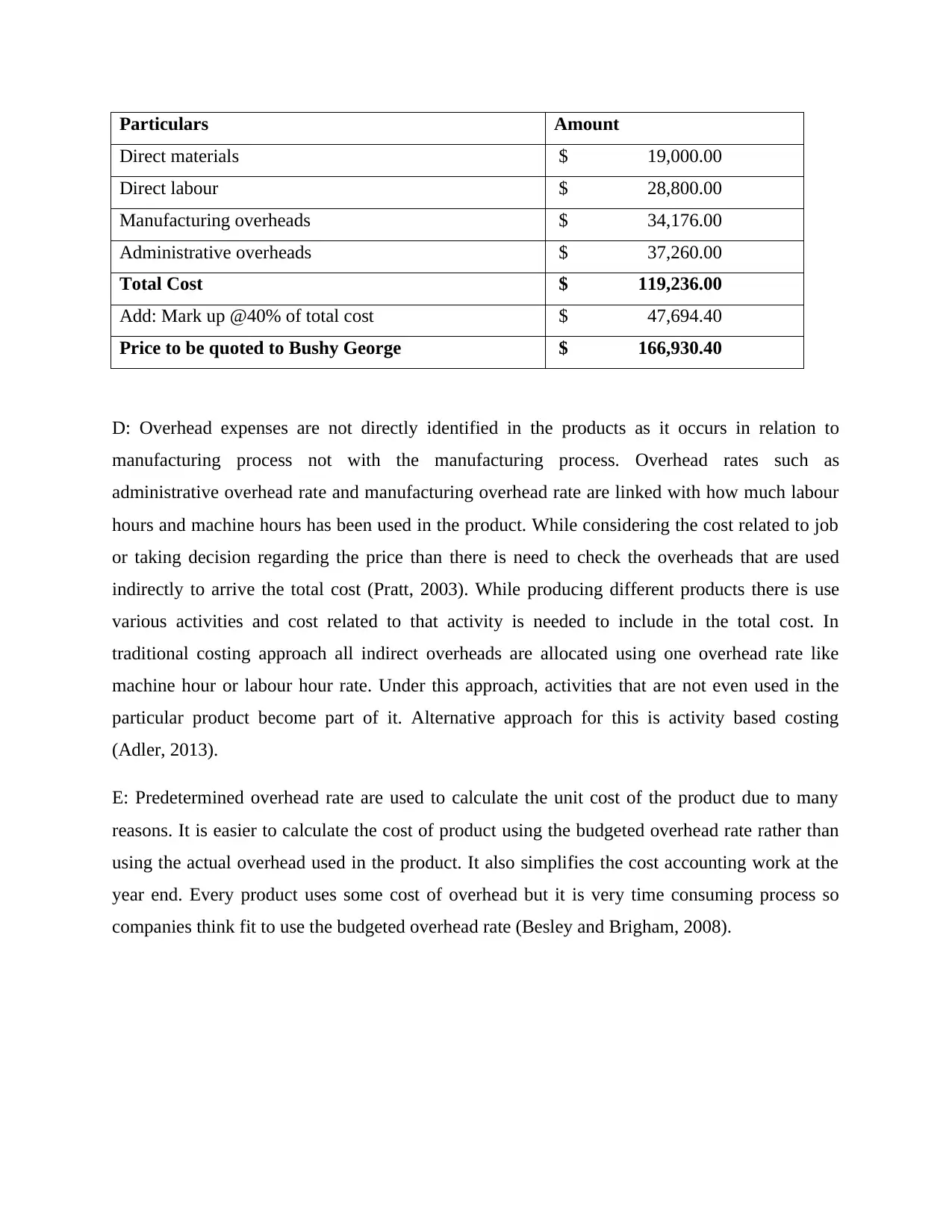

This document presents a comprehensive solution to a finance assignment, delving into key financial concepts. It begins by explaining flexible budgets, their role in determining variable costs at different expenditure levels, and their importance in evaluating past organizational performance. The solution then moves on to cash budgets, detailing their purpose in managing cash flows and their dependence on sales, purchase, and profit/loss budgets. The concept of the operating cycle is explained, contrasting it with the cash cycle and highlighting its significance for business cash receipts. The assignment also addresses the differences between governmental and non-profit organizations' accounting practices. Furthermore, the solution explores cost accounting, covering various costing processes like activity-based costing, and traditional costing. The second part of the solution provides a detailed calculation of manufacturing and administrative overhead rates. It also includes a pricing strategy for a specific project, considering direct materials, labor, overhead, and markup. The document concludes by explaining the use of predetermined overhead rates in calculating product costs and their practical advantages.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.