Finance Sources for British Airways

VerifiedAdded on 2020/02/05

|16

|4399

|47

Report

AI Summary

This report analyzes the financial sources available to British Airways, including internal and external options, implications of these sources, and the importance of financial planning. It also evaluates the company's budget, investment techniques, and financial statements to assess its overall financial health and strategies for expansion.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Sources of finance available to the company........................................................................3

1.2 Implications of different sources of finance..........................................................................4

1.3 Appropriate sources of finance which can aid the company to raise its capital....................4

2.1 Cost of sources of finance identified.....................................................................................5

2.2 Importance of financial planning..........................................................................................5

2.3 Information needed by internal and external decision makers. ............................................6

2.4 Appearance of various sources identified in the profit and loss account and balance sheet.7

Task 2...............................................................................................................................................7

3.1 Analyze of companies budget...............................................................................................7

3.3 Calculation of various investment techniques in order to find out the best project..............8

Task 3.............................................................................................................................................10

4.1 The main purpose of financial statements and its uses. .....................................................10

4.2 Financial statements prepared by various business organization........................................11

4.3 Calculation of company various ratio.................................................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Appendix........................................................................................................................................13

INTRODUCTION ..........................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Sources of finance available to the company........................................................................3

1.2 Implications of different sources of finance..........................................................................4

1.3 Appropriate sources of finance which can aid the company to raise its capital....................4

2.1 Cost of sources of finance identified.....................................................................................5

2.2 Importance of financial planning..........................................................................................5

2.3 Information needed by internal and external decision makers. ............................................6

2.4 Appearance of various sources identified in the profit and loss account and balance sheet.7

Task 2...............................................................................................................................................7

3.1 Analyze of companies budget...............................................................................................7

3.3 Calculation of various investment techniques in order to find out the best project..............8

Task 3.............................................................................................................................................10

4.1 The main purpose of financial statements and its uses. .....................................................10

4.2 Financial statements prepared by various business organization........................................11

4.3 Calculation of company various ratio.................................................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Appendix........................................................................................................................................13

INTRODUCTION

Finance is the management of large amount of cash that take place both the inside and

outside of the organization. In order words, it can be said that finance is the science that defines

the management of banking and investment as well as assets and liabilities. British airways are

the airline company headquartered in Waterside, Harmondsworth, England. It is one of the

largest airline companies operating its business in UK. The present report depicts about the

various internal and external sources of finance and at the same time it shows how these sources

of finance are beneficial for company to raise its funds. In this report, importance of finance

planning is discussed and per unit cost of company will be identified in order to make various

pricing decisions. At last, various financial statements are studied in order to calculate the

various ratios.

Task 1

1.1 Sources of finance available to the company.

There are various types of sources of finance through which company is available to raise

its funds. Some of them are internal sources of finance and some are external sources of finance.

Internal sources of finance

Sales of assets: - Company can raise its funds by selling its own property or assets.

Company often sales its unwanted stock in order to meet its requirement of short term finance

(Ageba and Amha, 2006). This is one of the simplest methods through which company can

quickly meets its short term requirement of cash.

Retained profit: - Retained profit is an amount of profit which company earns at the end

of financial year. A small amount of profit is kept by company as a reserve in order to meet any

sudden requirement of short term finance.

External sources of finance

Issue of shares: - By issuing shares to the general public, company is able to meet its

long term requirement of funds. Equity shares are also is issued to the existing shareholders

(Beaver, McNichols and Rhie, 2005). This method is generally used by company to expand its

business or to purchase new machinery.

Hire purchase: - It is a method which aids company to purchase assets without paying the

completed amount. It is a method which is used by company to meet its long term requirement of

Finance is the management of large amount of cash that take place both the inside and

outside of the organization. In order words, it can be said that finance is the science that defines

the management of banking and investment as well as assets and liabilities. British airways are

the airline company headquartered in Waterside, Harmondsworth, England. It is one of the

largest airline companies operating its business in UK. The present report depicts about the

various internal and external sources of finance and at the same time it shows how these sources

of finance are beneficial for company to raise its funds. In this report, importance of finance

planning is discussed and per unit cost of company will be identified in order to make various

pricing decisions. At last, various financial statements are studied in order to calculate the

various ratios.

Task 1

1.1 Sources of finance available to the company.

There are various types of sources of finance through which company is available to raise

its funds. Some of them are internal sources of finance and some are external sources of finance.

Internal sources of finance

Sales of assets: - Company can raise its funds by selling its own property or assets.

Company often sales its unwanted stock in order to meet its requirement of short term finance

(Ageba and Amha, 2006). This is one of the simplest methods through which company can

quickly meets its short term requirement of cash.

Retained profit: - Retained profit is an amount of profit which company earns at the end

of financial year. A small amount of profit is kept by company as a reserve in order to meet any

sudden requirement of short term finance.

External sources of finance

Issue of shares: - By issuing shares to the general public, company is able to meet its

long term requirement of funds. Equity shares are also is issued to the existing shareholders

(Beaver, McNichols and Rhie, 2005). This method is generally used by company to expand its

business or to purchase new machinery.

Hire purchase: - It is a method which aids company to purchase assets without paying the

completed amount. It is a method which is used by company to meet its long term requirement of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the fund. In this, company rents some of its required equipment or property for some year as

company can bear expenses in terms of hiring equipment instead of purchasing it.

1.2 Implications of different sources of finance.

Source Advantages Disadvantages Suitability

Sale of assets Rate of deprecation will be

reduced and at the same

time cost of the assets can

get back.

Reduces the assets of the

company.

To pay dividend

and interest to the

shareholders.

Retained profit Aid the company to meet

its short term requirement

without paying anything

(Cetorelli and Strahan,

2006).

Reserves of the company

are reduced and at the

same time shareholders

may not be happy to

forego its profit ratio.

To make payment

to the suppliers.

Issue of shares Funds collected from the

shareholders need not to be

paid back.

Dividend and the voting

rights need to be given.

For expanding its

business or

purchase of heavy

machinery.

Hire purchase Company can avail benefits

of using the assets without

purchasing it.

Total rental installment

cost became more as

compared to its original

cost.

For using assets for

some time period

without purchasing

it (Paramasivan and

Subramanian, n.d).

1.3 Appropriate sources of finance which can aid the company to raise its capital.

British airways want to expand its business to other countries in order to beat the sales

rate of Tesco and to become the number one leading retailer company in the UK as well as all

over the world. Therefore, in order to raise its capital for the achievement of its objectives,

company can sale its least usable asset to meet short term requirement and at the same time,

company can bear expenses in terms of hiring equipment instead of purchasing it.

1.2 Implications of different sources of finance.

Source Advantages Disadvantages Suitability

Sale of assets Rate of deprecation will be

reduced and at the same

time cost of the assets can

get back.

Reduces the assets of the

company.

To pay dividend

and interest to the

shareholders.

Retained profit Aid the company to meet

its short term requirement

without paying anything

(Cetorelli and Strahan,

2006).

Reserves of the company

are reduced and at the

same time shareholders

may not be happy to

forego its profit ratio.

To make payment

to the suppliers.

Issue of shares Funds collected from the

shareholders need not to be

paid back.

Dividend and the voting

rights need to be given.

For expanding its

business or

purchase of heavy

machinery.

Hire purchase Company can avail benefits

of using the assets without

purchasing it.

Total rental installment

cost became more as

compared to its original

cost.

For using assets for

some time period

without purchasing

it (Paramasivan and

Subramanian, n.d).

1.3 Appropriate sources of finance which can aid the company to raise its capital.

British airways want to expand its business to other countries in order to beat the sales

rate of Tesco and to become the number one leading retailer company in the UK as well as all

over the world. Therefore, in order to raise its capital for the achievement of its objectives,

company can sale its least usable asset to meet short term requirement and at the same time,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company can issue large number of shares in the market in order to meet long term requirement

of the fund.

Sale of assets: - Through selling its assets, British airways can able to meet its short term

requirement of cash that arises at the time of expansion of the business. This method can also be

used by company to pay interest and dividend to the existing and new shareholders (Chandra,

2011). This method can also be used by the company to pay its liabilities.

Issue of shares: - British airways can issue its shares to new and existing shareholders in

order to expand its business. Issue of shares will aid company to create more awareness about the

business. This method can also be used to purchase new assets.

2.1 Cost of sources of finance identified.

Sales of assets: - This method is used by company to meet its short term requirement of

the cash. This method is normally used to make payment to the suppliers or interest to the

shareholders. But at the same time, it reduces the cost of company’s assets. Many times,

company is not able to get the actual cost of assets at the time of sale. They need it to be sold at

loss which in turn reduces the profit margin of the company.

Retained profit: - This method is used by company to meet its short term requirement of

the funds. Normally, company uses retained profit to pay interest and dividend to its shareholders

at the time of loss when company is not left with funds to pay to its shareholders. This retained

profit is also used by business in order to expand its business at the small level.

Issue of shares: - This method is used by company to meet its long term requirement of

the funds. They issue shares to general public for which they need to pay dividend to them

(DRURY, 2013). This in turn increases the cost and expenses of the company. Management is

not able to avail any tax benefit on the dividend paid to the shareholders.

Hire purchase: - It is a method which is used by company to meet its requirement of

property, machinery and vehicles for some period of time without purchasing it (Sullivan, 2009).

But at the same time, this method increases the expenses of the company. Organization has to

provide payment through half-yearly and yearly installments to the owner of the assets which in

turn increases the cost of company. Normally, cost of total installment paid is more than the

actual cost of the asset.

of the fund.

Sale of assets: - Through selling its assets, British airways can able to meet its short term

requirement of cash that arises at the time of expansion of the business. This method can also be

used by company to pay interest and dividend to the existing and new shareholders (Chandra,

2011). This method can also be used by the company to pay its liabilities.

Issue of shares: - British airways can issue its shares to new and existing shareholders in

order to expand its business. Issue of shares will aid company to create more awareness about the

business. This method can also be used to purchase new assets.

2.1 Cost of sources of finance identified.

Sales of assets: - This method is used by company to meet its short term requirement of

the cash. This method is normally used to make payment to the suppliers or interest to the

shareholders. But at the same time, it reduces the cost of company’s assets. Many times,

company is not able to get the actual cost of assets at the time of sale. They need it to be sold at

loss which in turn reduces the profit margin of the company.

Retained profit: - This method is used by company to meet its short term requirement of

the funds. Normally, company uses retained profit to pay interest and dividend to its shareholders

at the time of loss when company is not left with funds to pay to its shareholders. This retained

profit is also used by business in order to expand its business at the small level.

Issue of shares: - This method is used by company to meet its long term requirement of

the funds. They issue shares to general public for which they need to pay dividend to them

(DRURY, 2013). This in turn increases the cost and expenses of the company. Management is

not able to avail any tax benefit on the dividend paid to the shareholders.

Hire purchase: - It is a method which is used by company to meet its requirement of

property, machinery and vehicles for some period of time without purchasing it (Sullivan, 2009).

But at the same time, this method increases the expenses of the company. Organization has to

provide payment through half-yearly and yearly installments to the owner of the assets which in

turn increases the cost of company. Normally, cost of total installment paid is more than the

actual cost of the asset.

2.2 Importance of financial planning.

Financial planning of all the activities assists company to easily achieve the desired target.

Therefore, some of the importance of financial planning is as follows:-

Maintain the flow of cash from within and outside the organization: - Planning of all

the financial activities in advance aids management to maintain the flow of funds properly in the

organization to achieve the desired target.

Fully utilize the available resources: - Planning of all the activities will also assist British

airways to fully utilize the available resources in an effective manner in order to achieve the

goals and objectives of the company (Alamosa, Kaminker and Johnstone, 2011).

Reduces uncertainty: - Financial planning of all the activities aids company to reduce the

level of uncertainty that may take place within the business unit. Reduce level of uncertainty

Helps Company to generate more profit by reducing its expenses.

Distribute the finance properly to each and every department: - Planning of all the

financial activities in advance assists company to know about that how much fund is required in

each and every department. This in turn aids company to distribute funds accordingly in order to

fully utilize the available finance.

2.3 Information needed by internal and external decision makers.

There are different types of information which decision maker requires taking decisions

on the various aspects. But the most important information which is needed by both internal and

external decision maker is as follows:-

Internal decision maker: - Internal decision makers are the persons who generally work

for the betterment of company. Internal decision maker can be employees, board members and

manager (Revsine and et.al, 2005). These all require income statements and different types of

financial statements (i.e. trading and profit & loss account, balance sheet, cash flow statements).

They need these statements to take various necessary decisions like preparing various strategies,

knowing the company growth rate, understanding the flow of funds and gaining knowledge

about the profit earned.

External decision maker: - These decision makers affect company from the outside.

External decision makers are shareholders, government, suppliers and many more. They require

both the financial statements of the company and its audit report (Lennard, 2007). Shareholders

want these statements to decide whether they should invest or not. Likewise government uses

Financial planning of all the activities assists company to easily achieve the desired target.

Therefore, some of the importance of financial planning is as follows:-

Maintain the flow of cash from within and outside the organization: - Planning of all

the financial activities in advance aids management to maintain the flow of funds properly in the

organization to achieve the desired target.

Fully utilize the available resources: - Planning of all the activities will also assist British

airways to fully utilize the available resources in an effective manner in order to achieve the

goals and objectives of the company (Alamosa, Kaminker and Johnstone, 2011).

Reduces uncertainty: - Financial planning of all the activities aids company to reduce the

level of uncertainty that may take place within the business unit. Reduce level of uncertainty

Helps Company to generate more profit by reducing its expenses.

Distribute the finance properly to each and every department: - Planning of all the

financial activities in advance assists company to know about that how much fund is required in

each and every department. This in turn aids company to distribute funds accordingly in order to

fully utilize the available finance.

2.3 Information needed by internal and external decision makers.

There are different types of information which decision maker requires taking decisions

on the various aspects. But the most important information which is needed by both internal and

external decision maker is as follows:-

Internal decision maker: - Internal decision makers are the persons who generally work

for the betterment of company. Internal decision maker can be employees, board members and

manager (Revsine and et.al, 2005). These all require income statements and different types of

financial statements (i.e. trading and profit & loss account, balance sheet, cash flow statements).

They need these statements to take various necessary decisions like preparing various strategies,

knowing the company growth rate, understanding the flow of funds and gaining knowledge

about the profit earned.

External decision maker: - These decision makers affect company from the outside.

External decision makers are shareholders, government, suppliers and many more. They require

both the financial statements of the company and its audit report (Lennard, 2007). Shareholders

want these statements to decide whether they should invest or not. Likewise government uses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial statements and audit report in order to calculate the amount of tax that needs to be paid

by company and evaluate whether company is making any fraud or not. Similarly, suppliers use

these statements to decide whether company is able to pay for the raw material purchased by

them or not.

Therefore, main documents which are required by company to take various necessary decisions

are income statements, financial statements and company audit report.

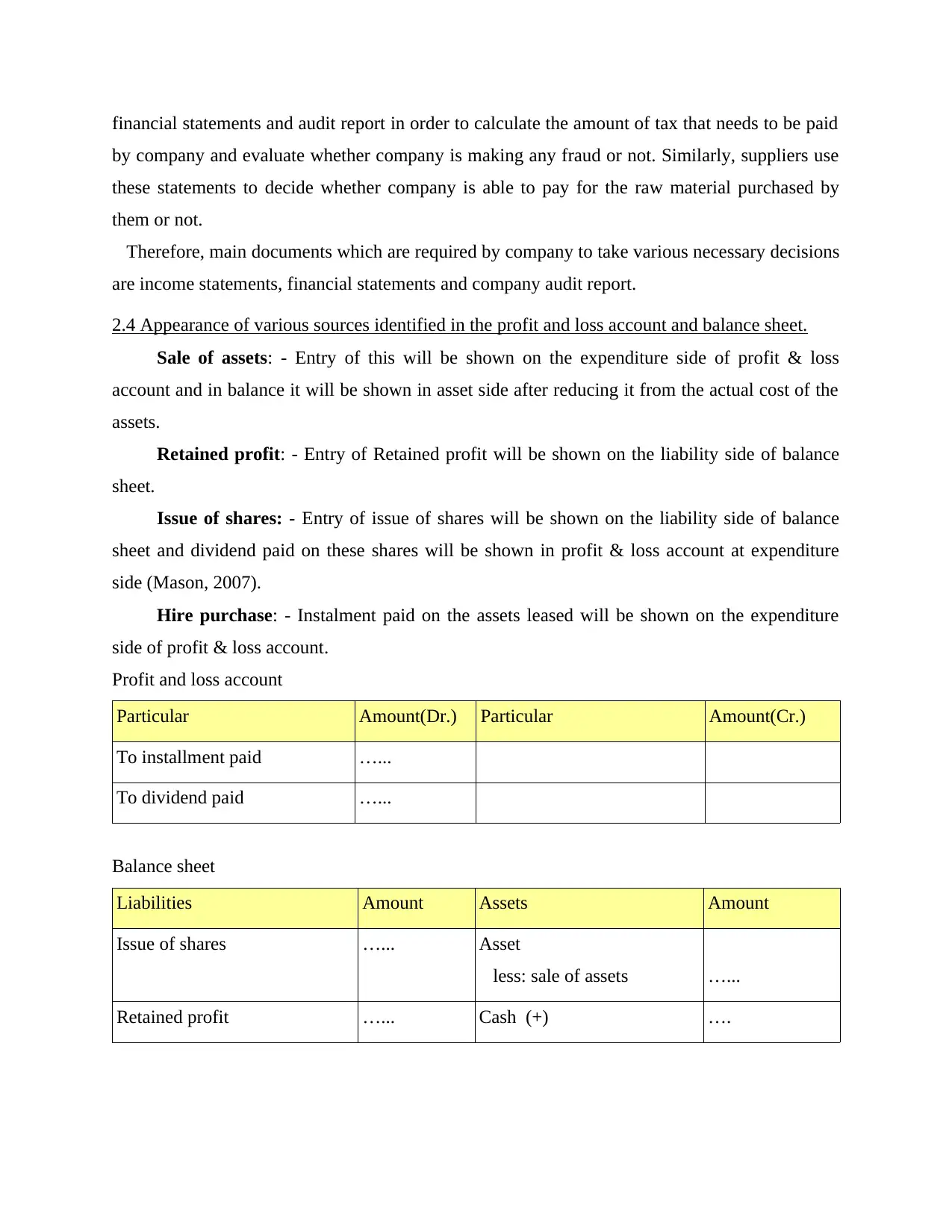

2.4 Appearance of various sources identified in the profit and loss account and balance sheet.

Sale of assets: - Entry of this will be shown on the expenditure side of profit & loss

account and in balance it will be shown in asset side after reducing it from the actual cost of the

assets.

Retained profit: - Entry of Retained profit will be shown on the liability side of balance

sheet.

Issue of shares: - Entry of issue of shares will be shown on the liability side of balance

sheet and dividend paid on these shares will be shown in profit & loss account at expenditure

side (Mason, 2007).

Hire purchase: - Instalment paid on the assets leased will be shown on the expenditure

side of profit & loss account.

Profit and loss account

Particular Amount(Dr.) Particular Amount(Cr.)

To installment paid …...

To dividend paid …...

Balance sheet

Liabilities Amount Assets Amount

Issue of shares …... Asset

less: sale of assets …...

Retained profit …... Cash (+) ….

by company and evaluate whether company is making any fraud or not. Similarly, suppliers use

these statements to decide whether company is able to pay for the raw material purchased by

them or not.

Therefore, main documents which are required by company to take various necessary decisions

are income statements, financial statements and company audit report.

2.4 Appearance of various sources identified in the profit and loss account and balance sheet.

Sale of assets: - Entry of this will be shown on the expenditure side of profit & loss

account and in balance it will be shown in asset side after reducing it from the actual cost of the

assets.

Retained profit: - Entry of Retained profit will be shown on the liability side of balance

sheet.

Issue of shares: - Entry of issue of shares will be shown on the liability side of balance

sheet and dividend paid on these shares will be shown in profit & loss account at expenditure

side (Mason, 2007).

Hire purchase: - Instalment paid on the assets leased will be shown on the expenditure

side of profit & loss account.

Profit and loss account

Particular Amount(Dr.) Particular Amount(Cr.)

To installment paid …...

To dividend paid …...

Balance sheet

Liabilities Amount Assets Amount

Issue of shares …... Asset

less: sale of assets …...

Retained profit …... Cash (+) ….

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 2

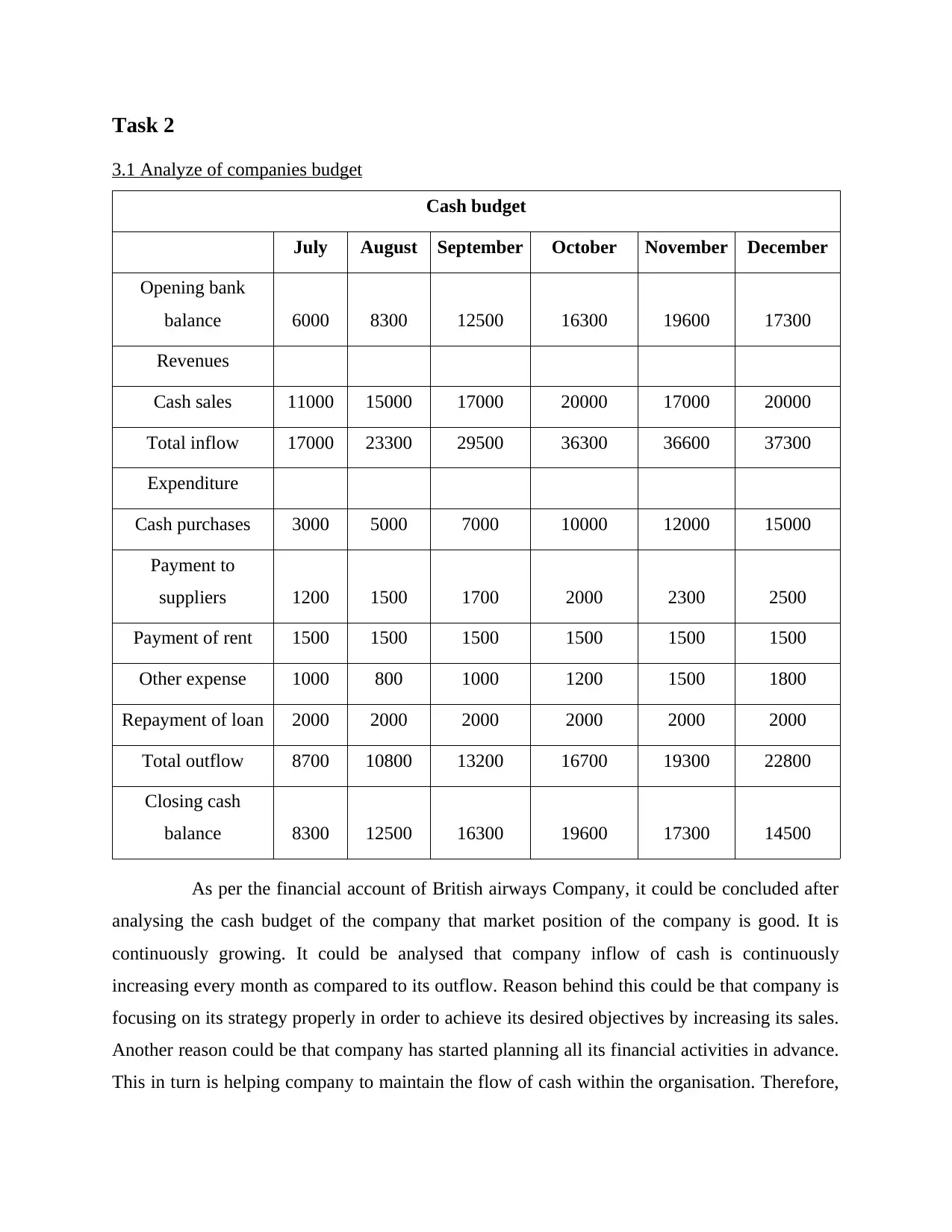

3.1 Analyze of companies budget

Cash budget

July August September October November December

Opening bank

balance 6000 8300 12500 16300 19600 17300

Revenues

Cash sales 11000 15000 17000 20000 17000 20000

Total inflow 17000 23300 29500 36300 36600 37300

Expenditure

Cash purchases 3000 5000 7000 10000 12000 15000

Payment to

suppliers 1200 1500 1700 2000 2300 2500

Payment of rent 1500 1500 1500 1500 1500 1500

Other expense 1000 800 1000 1200 1500 1800

Repayment of loan 2000 2000 2000 2000 2000 2000

Total outflow 8700 10800 13200 16700 19300 22800

Closing cash

balance 8300 12500 16300 19600 17300 14500

As per the financial account of British airways Company, it could be concluded after

analysing the cash budget of the company that market position of the company is good. It is

continuously growing. It could be analysed that company inflow of cash is continuously

increasing every month as compared to its outflow. Reason behind this could be that company is

focusing on its strategy properly in order to achieve its desired objectives by increasing its sales.

Another reason could be that company has started planning all its financial activities in advance.

This in turn is helping company to maintain the flow of cash within the organisation. Therefore,

3.1 Analyze of companies budget

Cash budget

July August September October November December

Opening bank

balance 6000 8300 12500 16300 19600 17300

Revenues

Cash sales 11000 15000 17000 20000 17000 20000

Total inflow 17000 23300 29500 36300 36600 37300

Expenditure

Cash purchases 3000 5000 7000 10000 12000 15000

Payment to

suppliers 1200 1500 1700 2000 2300 2500

Payment of rent 1500 1500 1500 1500 1500 1500

Other expense 1000 800 1000 1200 1500 1800

Repayment of loan 2000 2000 2000 2000 2000 2000

Total outflow 8700 10800 13200 16700 19300 22800

Closing cash

balance 8300 12500 16300 19600 17300 14500

As per the financial account of British airways Company, it could be concluded after

analysing the cash budget of the company that market position of the company is good. It is

continuously growing. It could be analysed that company inflow of cash is continuously

increasing every month as compared to its outflow. Reason behind this could be that company is

focusing on its strategy properly in order to achieve its desired objectives by increasing its sales.

Another reason could be that company has started planning all its financial activities in advance.

This in turn is helping company to maintain the flow of cash within the organisation. Therefore,

company should make efforts to increase the inflow of cash as compared to outflow by fully

utilizing the available resources.

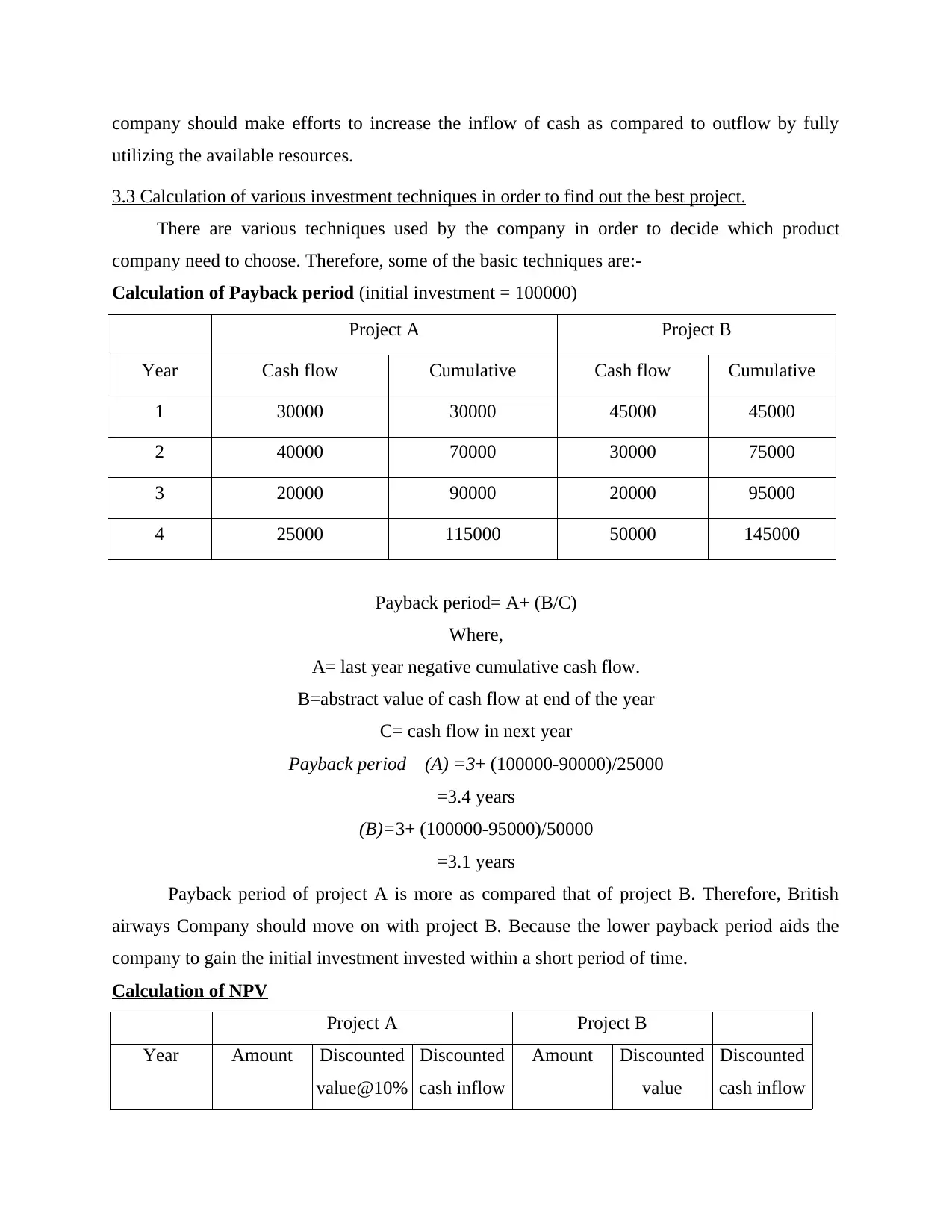

3.3 Calculation of various investment techniques in order to find out the best project.

There are various techniques used by the company in order to decide which product

company need to choose. Therefore, some of the basic techniques are:-

Calculation of Payback period (initial investment = 100000)

Project A Project B

Year Cash flow Cumulative Cash flow Cumulative

1 30000 30000 45000 45000

2 40000 70000 30000 75000

3 20000 90000 20000 95000

4 25000 115000 50000 145000

Payback period= A+ (B/C)

Where,

A= last year negative cumulative cash flow.

B=abstract value of cash flow at end of the year

C= cash flow in next year

Payback period (A) =3+ (100000-90000)/25000

=3.4 years

(B)=3+ (100000-95000)/50000

=3.1 years

Payback period of project A is more as compared that of project B. Therefore, British

airways Company should move on with project B. Because the lower payback period aids the

company to gain the initial investment invested within a short period of time.

Calculation of NPV

Project A Project B

Year Amount Discounted

value@10%

Discounted

cash inflow

Amount Discounted

value

Discounted

cash inflow

utilizing the available resources.

3.3 Calculation of various investment techniques in order to find out the best project.

There are various techniques used by the company in order to decide which product

company need to choose. Therefore, some of the basic techniques are:-

Calculation of Payback period (initial investment = 100000)

Project A Project B

Year Cash flow Cumulative Cash flow Cumulative

1 30000 30000 45000 45000

2 40000 70000 30000 75000

3 20000 90000 20000 95000

4 25000 115000 50000 145000

Payback period= A+ (B/C)

Where,

A= last year negative cumulative cash flow.

B=abstract value of cash flow at end of the year

C= cash flow in next year

Payback period (A) =3+ (100000-90000)/25000

=3.4 years

(B)=3+ (100000-95000)/50000

=3.1 years

Payback period of project A is more as compared that of project B. Therefore, British

airways Company should move on with project B. Because the lower payback period aids the

company to gain the initial investment invested within a short period of time.

Calculation of NPV

Project A Project B

Year Amount Discounted

value@10%

Discounted

cash inflow

Amount Discounted

value

Discounted

cash inflow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

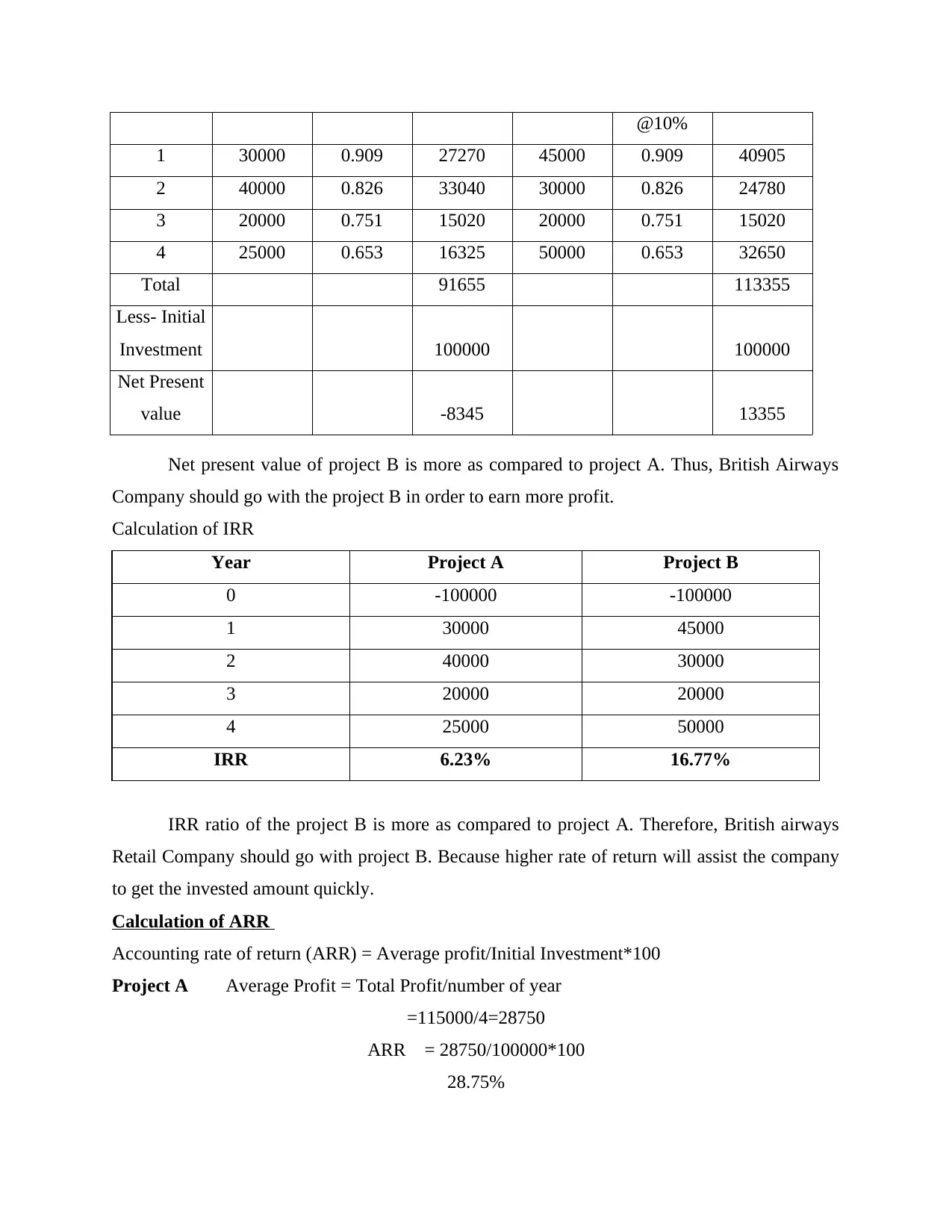

@10%

1 30000 0.909 27270 45000 0.909 40905

2 40000 0.826 33040 30000 0.826 24780

3 20000 0.751 15020 20000 0.751 15020

4 25000 0.653 16325 50000 0.653 32650

Total 91655 113355

Less- Initial

Investment 100000 100000

Net Present

value -8345 13355

Net present value of project B is more as compared to project A. Thus, British Airways

Company should go with the project B in order to earn more profit.

Calculation of IRR

Year Project A Project B

0 -100000 -100000

1 30000 45000

2 40000 30000

3 20000 20000

4 25000 50000

IRR 6.23% 16.77%

IRR ratio of the project B is more as compared to project A. Therefore, British airways

Retail Company should go with project B. Because higher rate of return will assist the company

to get the invested amount quickly.

Calculation of ARR

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A Average Profit = Total Profit/number of year

=115000/4=28750

ARR = 28750/100000*100

28.75%

1 30000 0.909 27270 45000 0.909 40905

2 40000 0.826 33040 30000 0.826 24780

3 20000 0.751 15020 20000 0.751 15020

4 25000 0.653 16325 50000 0.653 32650

Total 91655 113355

Less- Initial

Investment 100000 100000

Net Present

value -8345 13355

Net present value of project B is more as compared to project A. Thus, British Airways

Company should go with the project B in order to earn more profit.

Calculation of IRR

Year Project A Project B

0 -100000 -100000

1 30000 45000

2 40000 30000

3 20000 20000

4 25000 50000

IRR 6.23% 16.77%

IRR ratio of the project B is more as compared to project A. Therefore, British airways

Retail Company should go with project B. Because higher rate of return will assist the company

to get the invested amount quickly.

Calculation of ARR

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A Average Profit = Total Profit/number of year

=115000/4=28750

ARR = 28750/100000*100

28.75%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Project B

Average Profit = 145000/4

=36250

ARR =36250/100000

=36.25%

Average rate of return of project B is more as compared to project A. Therefore, British

Airways Company should go with project B. Because higher average return of return will assist

the company to increase its level of profitability.

Therefore, at last it can be concluded that British Airways Company should go with project

B in order to gain the profit and quick recover the amount invested.

Task 3

4.1 The main purpose of financial statements and its uses.

Income statements: - Income statements are prepared by the company in order to find out

the income generated and expenses made by the company at the end of every financial year

(Mayer, Schoors and Yafeh, 2005). This statement also said the company to find out the profit

earned by the company at the end of the year. At the same time it assists the company to

conclude the amount of dividend and tax company need to pay to its shareholders and to the

government. These statements are normally considered by the finance manager in order to plan

various activities.

Balance Sheet: - Balance sheet is prepared by the company in order to calculate the assets

and liabilities available with the company at the end of every financial year. This statement is

used by the manager, shareholders and government in order to find out the growth rate of the

company.

Cash flow statements: - Cash flow statements are prepared by the company in order to

find out the amount of cash invested while performing various activities at the end of every

financial year (Melis, A., 2007). These statements are generally used by manager of the company

in order to fully utilize the available the finance. This statement is made up three activities (i.e.

operating, investing and financing activities).

Average Profit = 145000/4

=36250

ARR =36250/100000

=36.25%

Average rate of return of project B is more as compared to project A. Therefore, British

Airways Company should go with project B. Because higher average return of return will assist

the company to increase its level of profitability.

Therefore, at last it can be concluded that British Airways Company should go with project

B in order to gain the profit and quick recover the amount invested.

Task 3

4.1 The main purpose of financial statements and its uses.

Income statements: - Income statements are prepared by the company in order to find out

the income generated and expenses made by the company at the end of every financial year

(Mayer, Schoors and Yafeh, 2005). This statement also said the company to find out the profit

earned by the company at the end of the year. At the same time it assists the company to

conclude the amount of dividend and tax company need to pay to its shareholders and to the

government. These statements are normally considered by the finance manager in order to plan

various activities.

Balance Sheet: - Balance sheet is prepared by the company in order to calculate the assets

and liabilities available with the company at the end of every financial year. This statement is

used by the manager, shareholders and government in order to find out the growth rate of the

company.

Cash flow statements: - Cash flow statements are prepared by the company in order to

find out the amount of cash invested while performing various activities at the end of every

financial year (Melis, A., 2007). These statements are generally used by manager of the company

in order to fully utilize the available the finance. This statement is made up three activities (i.e.

operating, investing and financing activities).

4.2 Financial statements prepared by various business organizations.

Sole traders: - Sole traders are the one who invest this own capital in order to start its

business. These sole traders only prepare journals, ledger and receipt & payment accounts in

order to record all the transaction made by him.

Partnership: - Partnership firm is the firm which is operated by two or more partners.

These type of organization are only required to prepare the income and expenditure account in

order to calculate the amount of profit earned by them at the end of the financial year (Penman

and Penman, 2007).

Public and private ltd. Companies: - Public and private ltd. Company need to prepare all

type of financial statements (i.e. income statement, balance sheet, cash flow statements). This

helps the company to find out its growth rate and profit earned by them at the end of the year.

4.3 Calculation of company various ratio.

After analysing and calculating the various ratios it can be find out that company position

is good. Its profitability, liquidity and Activities ratio are increasing at the low rate. It is also

found out that its ratios have been declined in the year 2013 as compared to 2012. The reason

behind this could be that the number of competitors has been increased or company is not able to

maintain the balance between inflow and outflow of the cash properly (Persons, 2011). But on

the other hand it seen out that its growth rate has started increasing as compared to that of year

2013. But its liquidity ratio is continuously increasing every year. The reason behind this could

be that company has started focusing on formation of various strategies in order to maintain the

flow of funds and beat its competitors. Thus, at last it can be conclude that overall position of the

company is fairly good.

Conclusion

The following report emphasis on various sources of finance through which company can

raise its finance. In this report unit cost of the company is also calculated by considering the

fixed and variable cost. In this report cash budget is prepared and analyse in order to find out

companies position. At last financial accounts of the company are taken into consideration in

order to calculate various ratios of the British airways company.

Sole traders: - Sole traders are the one who invest this own capital in order to start its

business. These sole traders only prepare journals, ledger and receipt & payment accounts in

order to record all the transaction made by him.

Partnership: - Partnership firm is the firm which is operated by two or more partners.

These type of organization are only required to prepare the income and expenditure account in

order to calculate the amount of profit earned by them at the end of the financial year (Penman

and Penman, 2007).

Public and private ltd. Companies: - Public and private ltd. Company need to prepare all

type of financial statements (i.e. income statement, balance sheet, cash flow statements). This

helps the company to find out its growth rate and profit earned by them at the end of the year.

4.3 Calculation of company various ratio.

After analysing and calculating the various ratios it can be find out that company position

is good. Its profitability, liquidity and Activities ratio are increasing at the low rate. It is also

found out that its ratios have been declined in the year 2013 as compared to 2012. The reason

behind this could be that the number of competitors has been increased or company is not able to

maintain the balance between inflow and outflow of the cash properly (Persons, 2011). But on

the other hand it seen out that its growth rate has started increasing as compared to that of year

2013. But its liquidity ratio is continuously increasing every year. The reason behind this could

be that company has started focusing on formation of various strategies in order to maintain the

flow of funds and beat its competitors. Thus, at last it can be conclude that overall position of the

company is fairly good.

Conclusion

The following report emphasis on various sources of finance through which company can

raise its finance. In this report unit cost of the company is also calculated by considering the

fixed and variable cost. In this report cash budget is prepared and analyse in order to find out

companies position. At last financial accounts of the company are taken into consideration in

order to calculate various ratios of the British airways company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.