RM Ltd. Finance Assignment: Income Statement and Balance Sheet

VerifiedAdded on 2022/11/24

|10

|2020

|413

Homework Assignment

AI Summary

This finance assignment solution addresses key concepts in financial accounting and management. It begins with the preparation of an income statement and statement of financial position for RM Ltd., incorporating adjustments for inventory valuation, accruals, depreciation, and taxation. The solution then delves into project appraisal, calculating payback periods and net present values for two projects, followed by a discussion of project ranking and additional factors influencing investment decisions. Finally, the assignment concludes with a breakeven analysis, calculating contribution margins, breakeven points, and margins of safety, while also addressing the limitations of breakeven analysis.

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question: 1.......................................................................................................................................3

SECTION- B...................................................................................................................................5

QUESTION- 2.................................................................................................................................5

Question: 4.......................................................................................................................................8

REFERENCES..............................................................................................................................10

Question: 1.......................................................................................................................................3

SECTION- B...................................................................................................................................5

QUESTION- 2.................................................................................................................................5

Question: 4.......................................................................................................................................8

REFERENCES..............................................................................................................................10

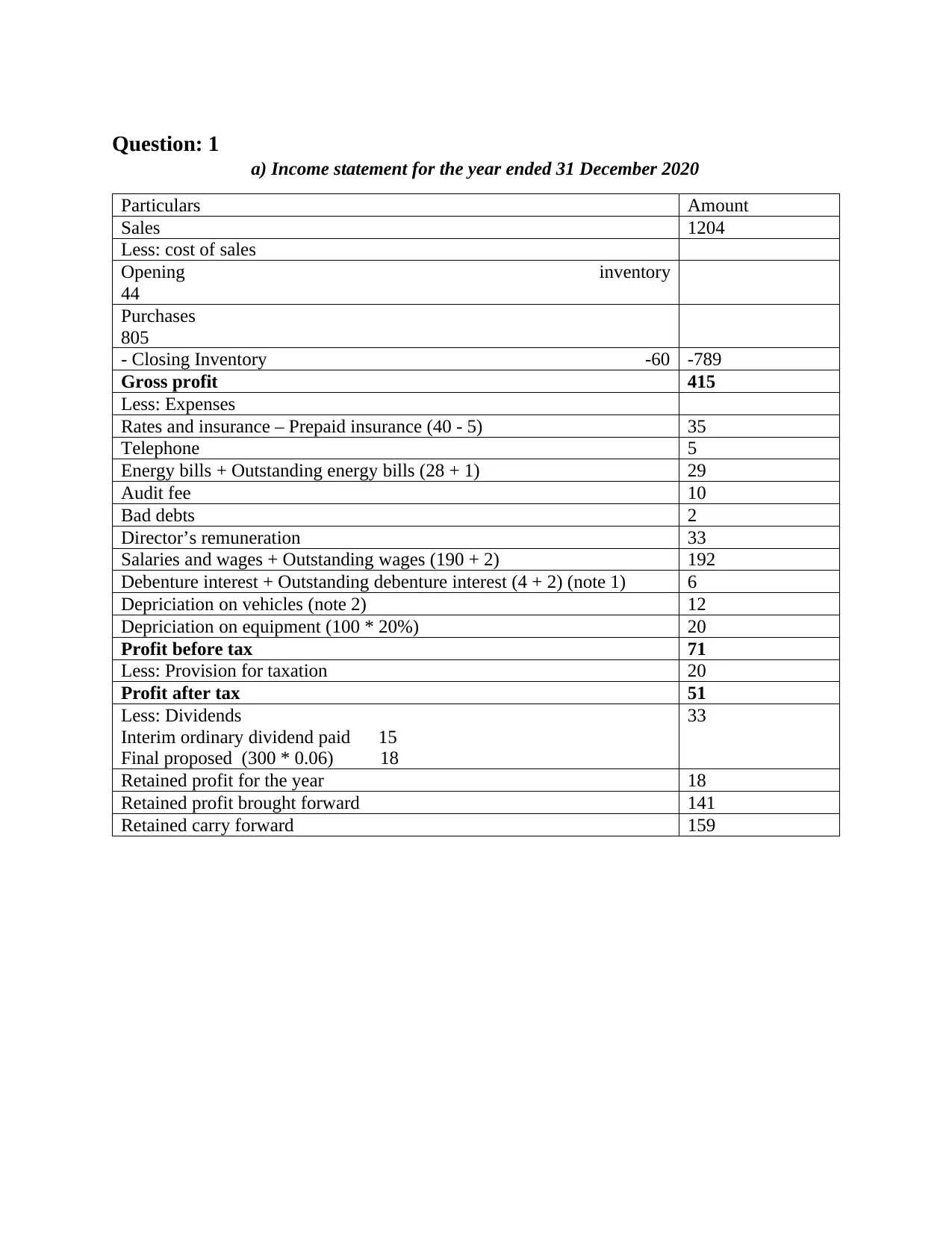

Question: 1

a) Income statement for the year ended 31 December 2020

Particulars Amount

Sales 1204

Less: cost of sales

Opening inventory

44

Purchases

805

- Closing Inventory -60 -789

Gross profit 415

Less: Expenses

Rates and insurance – Prepaid insurance (40 - 5) 35

Telephone 5

Energy bills + Outstanding energy bills (28 + 1) 29

Audit fee 10

Bad debts 2

Director’s remuneration 33

Salaries and wages + Outstanding wages (190 + 2) 192

Debenture interest + Outstanding debenture interest (4 + 2) (note 1) 6

Depriciation on vehicles (note 2) 12

Depriciation on equipment (100 * 20%) 20

Profit before tax 71

Less: Provision for taxation 20

Profit after tax 51

Less: Dividends

Interim ordinary dividend paid 15

Final proposed (300 * 0.06) 18

33

Retained profit for the year 18

Retained profit brought forward 141

Retained carry forward 159

a) Income statement for the year ended 31 December 2020

Particulars Amount

Sales 1204

Less: cost of sales

Opening inventory

44

Purchases

805

- Closing Inventory -60 -789

Gross profit 415

Less: Expenses

Rates and insurance – Prepaid insurance (40 - 5) 35

Telephone 5

Energy bills + Outstanding energy bills (28 + 1) 29

Audit fee 10

Bad debts 2

Director’s remuneration 33

Salaries and wages + Outstanding wages (190 + 2) 192

Debenture interest + Outstanding debenture interest (4 + 2) (note 1) 6

Depriciation on vehicles (note 2) 12

Depriciation on equipment (100 * 20%) 20

Profit before tax 71

Less: Provision for taxation 20

Profit after tax 51

Less: Dividends

Interim ordinary dividend paid 15

Final proposed (300 * 0.06) 18

33

Retained profit for the year 18

Retained profit brought forward 141

Retained carry forward 159

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Statement of Financial Position as at 31st December 2020

Particulars Amount

ASSETS

Non – current Assets

Land and building 550

Equipment (cost less accumulated

Depriciation) (100 – 20 – 20)

60

Vehicles (cost less accumulated Depriciation)

(90 – 30 - 12 )

48

Current assets

Inventory 60

Receivables 81

Prepaid insurance 5

Bank 2

Cash 1

TOTAL 807

£1 Ordinary share capital 300

Reserves

Share premium 160

Retained profits 159

Shareholder’s fund 619

Non-current liabilities

6% debentures 100

Current liabilities

Payables 45

Accruals (2 + 2 + 1) 5

Provision for taxation 20

Dividend proposed 18

TOTAL 807

Working notes:

1. The Debenture interest due for the year /incurred for the year is: 6% on £100,000 (6%

Debenture of £100,000) is £6,000.

From the trial balance, the debenture interest paid is £4,000.

This requires an accruals adjustment of £2,000; so the amount to charge as

Debenture interest is £6,000 (£4,000 + £2,000)

2. Depriciation on vehicle – reduced balance of vehicle * 20%

Particulars Amount

ASSETS

Non – current Assets

Land and building 550

Equipment (cost less accumulated

Depriciation) (100 – 20 – 20)

60

Vehicles (cost less accumulated Depriciation)

(90 – 30 - 12 )

48

Current assets

Inventory 60

Receivables 81

Prepaid insurance 5

Bank 2

Cash 1

TOTAL 807

£1 Ordinary share capital 300

Reserves

Share premium 160

Retained profits 159

Shareholder’s fund 619

Non-current liabilities

6% debentures 100

Current liabilities

Payables 45

Accruals (2 + 2 + 1) 5

Provision for taxation 20

Dividend proposed 18

TOTAL 807

Working notes:

1. The Debenture interest due for the year /incurred for the year is: 6% on £100,000 (6%

Debenture of £100,000) is £6,000.

From the trial balance, the debenture interest paid is £4,000.

This requires an accruals adjustment of £2,000; so the amount to charge as

Debenture interest is £6,000 (£4,000 + £2,000)

2. Depriciation on vehicle – reduced balance of vehicle * 20%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reduced balance of vehicle = cost of vehicle – Accumulated Depriciation of vehicle

= 90 – 30 = 60

Therefore, Depriciation for the year on vehicle will be 60 * 20% = 12

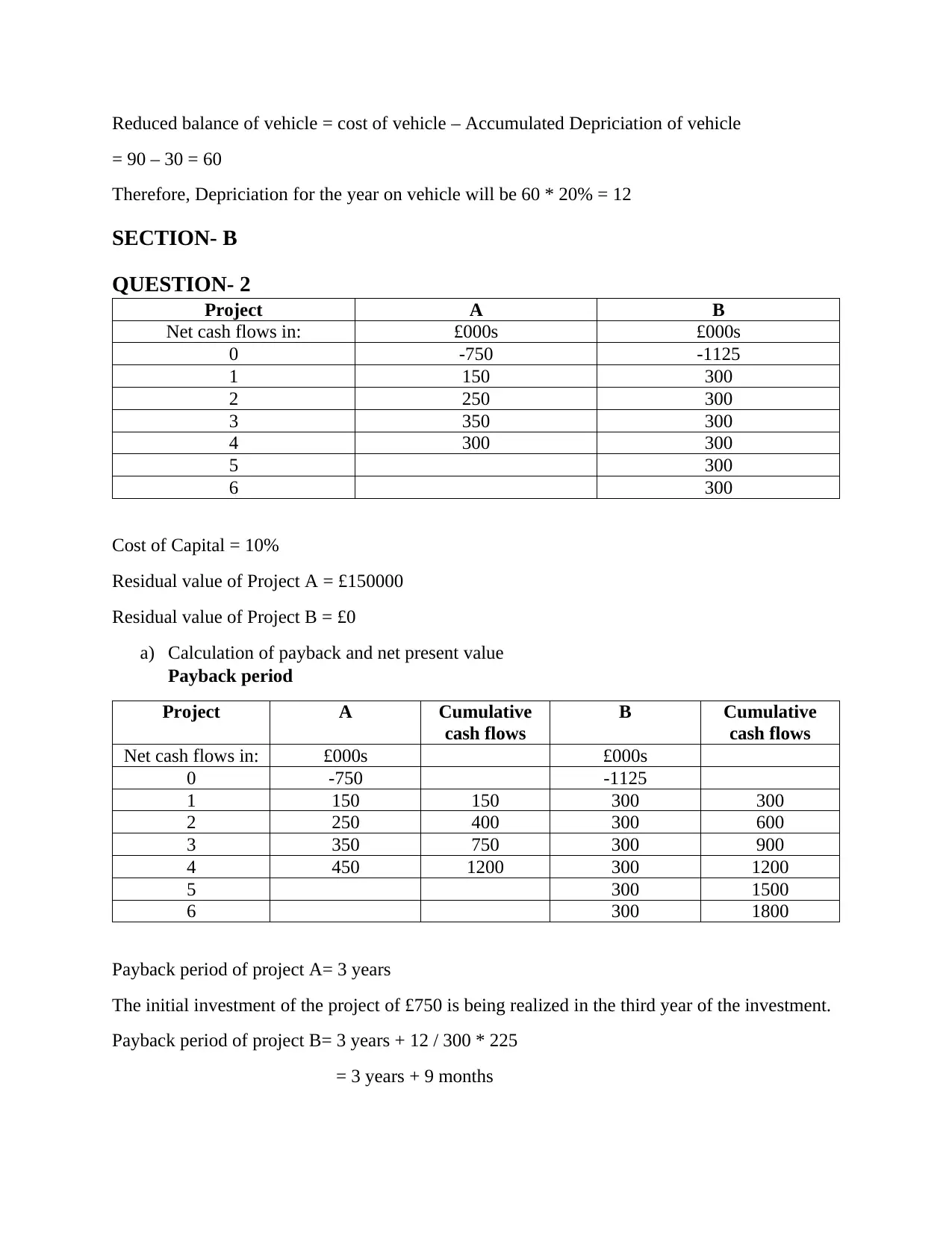

SECTION- B

QUESTION- 2

Project A B

Net cash flows in: £000s £000s

0 -750 -1125

1 150 300

2 250 300

3 350 300

4 300 300

5 300

6 300

Cost of Capital = 10%

Residual value of Project A = £150000

Residual value of Project B = £0

a) Calculation of payback and net present value

Payback period

Project A Cumulative

cash flows

B Cumulative

cash flows

Net cash flows in: £000s £000s

0 -750 -1125

1 150 150 300 300

2 250 400 300 600

3 350 750 300 900

4 450 1200 300 1200

5 300 1500

6 300 1800

Payback period of project A= 3 years

The initial investment of the project of £750 is being realized in the third year of the investment.

Payback period of project B= 3 years + 12 / 300 * 225

= 3 years + 9 months

= 90 – 30 = 60

Therefore, Depriciation for the year on vehicle will be 60 * 20% = 12

SECTION- B

QUESTION- 2

Project A B

Net cash flows in: £000s £000s

0 -750 -1125

1 150 300

2 250 300

3 350 300

4 300 300

5 300

6 300

Cost of Capital = 10%

Residual value of Project A = £150000

Residual value of Project B = £0

a) Calculation of payback and net present value

Payback period

Project A Cumulative

cash flows

B Cumulative

cash flows

Net cash flows in: £000s £000s

0 -750 -1125

1 150 150 300 300

2 250 400 300 600

3 350 750 300 900

4 450 1200 300 1200

5 300 1500

6 300 1800

Payback period of project A= 3 years

The initial investment of the project of £750 is being realized in the third year of the investment.

Payback period of project B= 3 years + 12 / 300 * 225

= 3 years + 9 months

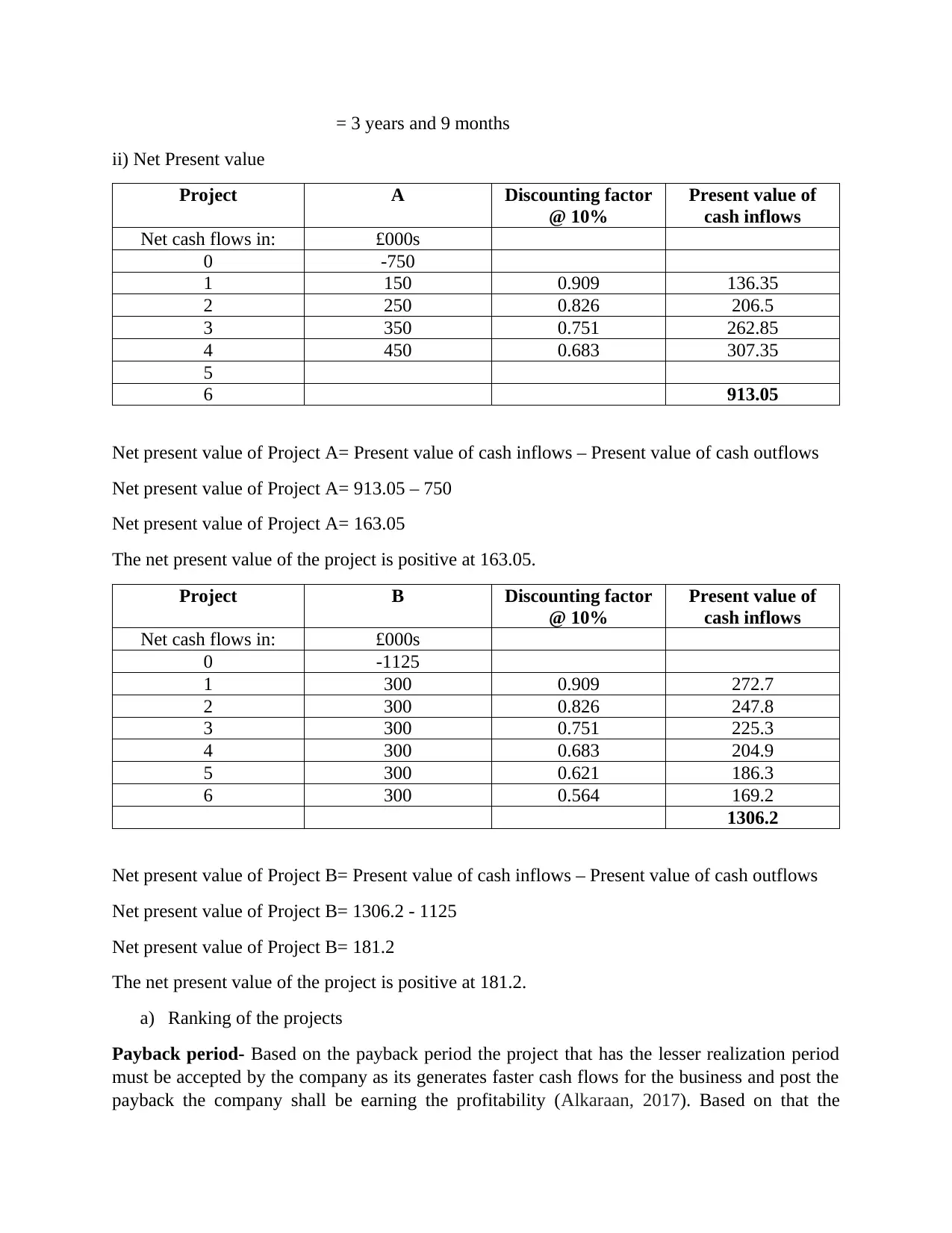

= 3 years and 9 months

ii) Net Present value

Project A Discounting factor

@ 10%

Present value of

cash inflows

Net cash flows in: £000s

0 -750

1 150 0.909 136.35

2 250 0.826 206.5

3 350 0.751 262.85

4 450 0.683 307.35

5

6 913.05

Net present value of Project A= Present value of cash inflows – Present value of cash outflows

Net present value of Project A= 913.05 – 750

Net present value of Project A= 163.05

The net present value of the project is positive at 163.05.

Project B Discounting factor

@ 10%

Present value of

cash inflows

Net cash flows in: £000s

0 -1125

1 300 0.909 272.7

2 300 0.826 247.8

3 300 0.751 225.3

4 300 0.683 204.9

5 300 0.621 186.3

6 300 0.564 169.2

1306.2

Net present value of Project B= Present value of cash inflows – Present value of cash outflows

Net present value of Project B= 1306.2 - 1125

Net present value of Project B= 181.2

The net present value of the project is positive at 181.2.

a) Ranking of the projects

Payback period- Based on the payback period the project that has the lesser realization period

must be accepted by the company as its generates faster cash flows for the business and post the

payback the company shall be earning the profitability (Alkaraan, 2017). Based on that the

ii) Net Present value

Project A Discounting factor

@ 10%

Present value of

cash inflows

Net cash flows in: £000s

0 -750

1 150 0.909 136.35

2 250 0.826 206.5

3 350 0.751 262.85

4 450 0.683 307.35

5

6 913.05

Net present value of Project A= Present value of cash inflows – Present value of cash outflows

Net present value of Project A= 913.05 – 750

Net present value of Project A= 163.05

The net present value of the project is positive at 163.05.

Project B Discounting factor

@ 10%

Present value of

cash inflows

Net cash flows in: £000s

0 -1125

1 300 0.909 272.7

2 300 0.826 247.8

3 300 0.751 225.3

4 300 0.683 204.9

5 300 0.621 186.3

6 300 0.564 169.2

1306.2

Net present value of Project B= Present value of cash inflows – Present value of cash outflows

Net present value of Project B= 1306.2 - 1125

Net present value of Project B= 181.2

The net present value of the project is positive at 181.2.

a) Ranking of the projects

Payback period- Based on the payback period the project that has the lesser realization period

must be accepted by the company as its generates faster cash flows for the business and post the

payback the company shall be earning the profitability (Alkaraan, 2017). Based on that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company shall be accepting the Project A that has the payback period of 3 years which is early in

comparison to the Project B. Also the company requires payback less than 3.5 years so this

condition is also acceptable in case of Project A.

Net Present Value- In case of net present value the project that shall be having the higher net

present value shall be selected by the company. In this scenario Project B shall be selected which

has the positive NPV of 181.2 which is higher than that of Project B.

b) The investment appraisal technique of Payback period can be used in this scenario as one

of the demerits of Net present value technique is that it cannot be applied to the mutually

exclusive projects whose life is not similar. If the net present value is not used then the

decisions shall be made based on the payback period method (Pawlak, Rapacewicz and

Zarzecki, 2020). In that case it can be assessed that Project A must be selected because it

has the lower payback period of 3 years as compared to Project B which has the payback

of 3 years and 9 months.

So it can be recommended that the Project A must be accepted so that the investments are

profitable in the long run for the company.

c) There can be other factors that can be considered by the company for the final decision of

the investments appraisal:-

The one factor is that whether the company has the funds to finance the

investment and what shall be the cost of acquisition of these funds. Apart from

that whether regular returns are being generated for the smooth working capital

cycle.

The internal rate of return for the company has to be identified so that it can be

assessed that how much is the project profitable for the company. The higher is

the IRR than the cost of capital the better it shall be for the company (Nnamani,

2017).

The technological capacity and the qualification of the employees to operate with

the project are some of the factors that has to be considered before the

investments are made by the company.

The consistency of the generation of the cash flows is one of the factors that needs

to be assured by the business, as regular cash flows are required for the operations

to be carried out smooth by the company.

comparison to the Project B. Also the company requires payback less than 3.5 years so this

condition is also acceptable in case of Project A.

Net Present Value- In case of net present value the project that shall be having the higher net

present value shall be selected by the company. In this scenario Project B shall be selected which

has the positive NPV of 181.2 which is higher than that of Project B.

b) The investment appraisal technique of Payback period can be used in this scenario as one

of the demerits of Net present value technique is that it cannot be applied to the mutually

exclusive projects whose life is not similar. If the net present value is not used then the

decisions shall be made based on the payback period method (Pawlak, Rapacewicz and

Zarzecki, 2020). In that case it can be assessed that Project A must be selected because it

has the lower payback period of 3 years as compared to Project B which has the payback

of 3 years and 9 months.

So it can be recommended that the Project A must be accepted so that the investments are

profitable in the long run for the company.

c) There can be other factors that can be considered by the company for the final decision of

the investments appraisal:-

The one factor is that whether the company has the funds to finance the

investment and what shall be the cost of acquisition of these funds. Apart from

that whether regular returns are being generated for the smooth working capital

cycle.

The internal rate of return for the company has to be identified so that it can be

assessed that how much is the project profitable for the company. The higher is

the IRR than the cost of capital the better it shall be for the company (Nnamani,

2017).

The technological capacity and the qualification of the employees to operate with

the project are some of the factors that has to be considered before the

investments are made by the company.

The consistency of the generation of the cash flows is one of the factors that needs

to be assured by the business, as regular cash flows are required for the operations

to be carried out smooth by the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

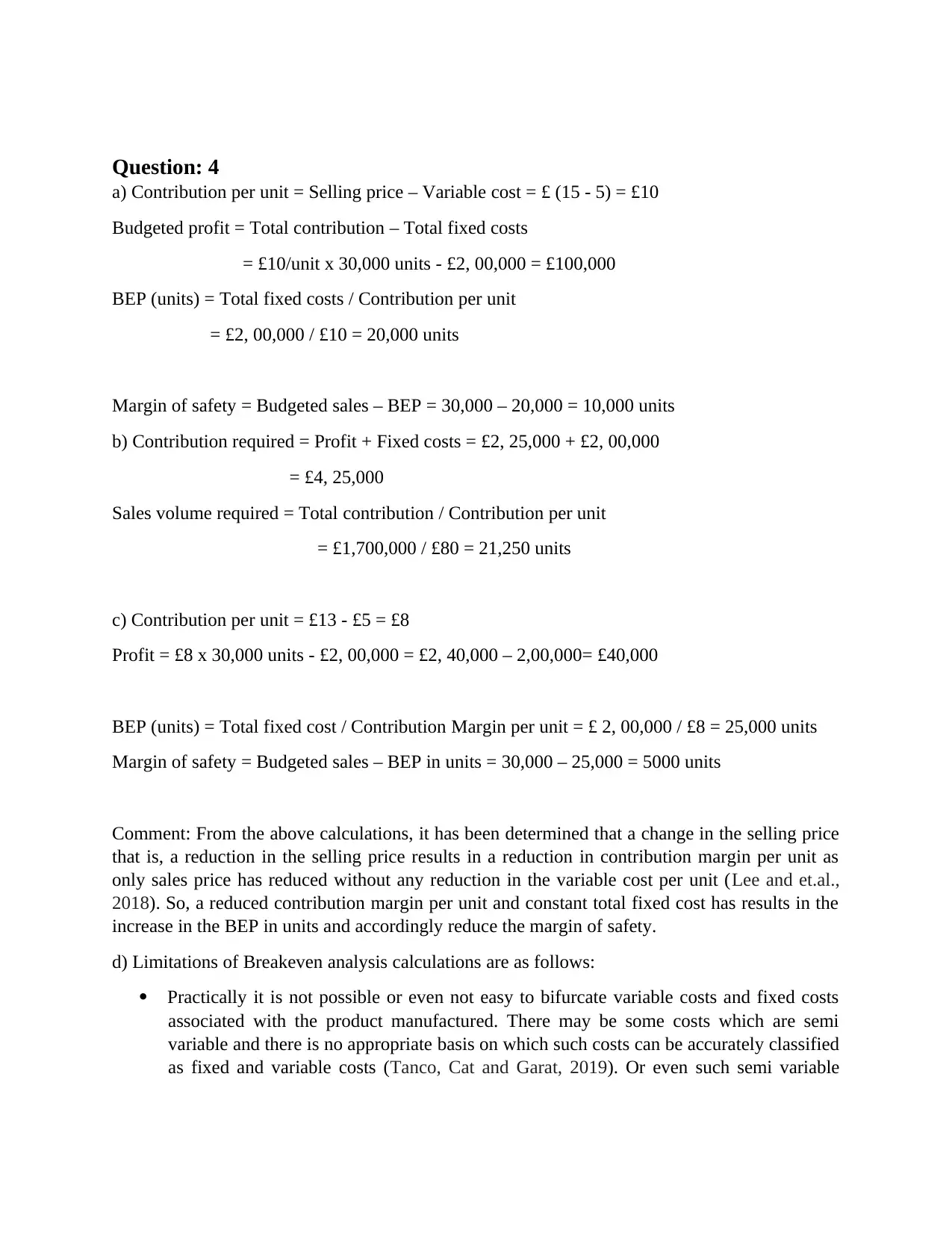

Question: 4

a) Contribution per unit = Selling price – Variable cost = £ (15 - 5) = £10

Budgeted profit = Total contribution – Total fixed costs

= £10/unit x 30,000 units - £2, 00,000 = £100,000

BEP (units) = Total fixed costs / Contribution per unit

= £2, 00,000 / £10 = 20,000 units

Margin of safety = Budgeted sales – BEP = 30,000 – 20,000 = 10,000 units

b) Contribution required = Profit + Fixed costs = £2, 25,000 + £2, 00,000

= £4, 25,000

Sales volume required = Total contribution / Contribution per unit

= £1,700,000 / £80 = 21,250 units

c) Contribution per unit = £13 - £5 = £8

Profit = £8 x 30,000 units - £2, 00,000 = £2, 40,000 – 2,00,000= £40,000

BEP (units) = Total fixed cost / Contribution Margin per unit = £ 2, 00,000 / £8 = 25,000 units

Margin of safety = Budgeted sales – BEP in units = 30,000 – 25,000 = 5000 units

Comment: From the above calculations, it has been determined that a change in the selling price

that is, a reduction in the selling price results in a reduction in contribution margin per unit as

only sales price has reduced without any reduction in the variable cost per unit (Lee and et.al.,

2018). So, a reduced contribution margin per unit and constant total fixed cost has results in the

increase in the BEP in units and accordingly reduce the margin of safety.

d) Limitations of Breakeven analysis calculations are as follows:

Practically it is not possible or even not easy to bifurcate variable costs and fixed costs

associated with the product manufactured. There may be some costs which are semi

variable and there is no appropriate basis on which such costs can be accurately classified

as fixed and variable costs (Tanco, Cat and Garat, 2019). Or even such semi variable

a) Contribution per unit = Selling price – Variable cost = £ (15 - 5) = £10

Budgeted profit = Total contribution – Total fixed costs

= £10/unit x 30,000 units - £2, 00,000 = £100,000

BEP (units) = Total fixed costs / Contribution per unit

= £2, 00,000 / £10 = 20,000 units

Margin of safety = Budgeted sales – BEP = 30,000 – 20,000 = 10,000 units

b) Contribution required = Profit + Fixed costs = £2, 25,000 + £2, 00,000

= £4, 25,000

Sales volume required = Total contribution / Contribution per unit

= £1,700,000 / £80 = 21,250 units

c) Contribution per unit = £13 - £5 = £8

Profit = £8 x 30,000 units - £2, 00,000 = £2, 40,000 – 2,00,000= £40,000

BEP (units) = Total fixed cost / Contribution Margin per unit = £ 2, 00,000 / £8 = 25,000 units

Margin of safety = Budgeted sales – BEP in units = 30,000 – 25,000 = 5000 units

Comment: From the above calculations, it has been determined that a change in the selling price

that is, a reduction in the selling price results in a reduction in contribution margin per unit as

only sales price has reduced without any reduction in the variable cost per unit (Lee and et.al.,

2018). So, a reduced contribution margin per unit and constant total fixed cost has results in the

increase in the BEP in units and accordingly reduce the margin of safety.

d) Limitations of Breakeven analysis calculations are as follows:

Practically it is not possible or even not easy to bifurcate variable costs and fixed costs

associated with the product manufactured. There may be some costs which are semi

variable and there is no appropriate basis on which such costs can be accurately classified

as fixed and variable costs (Tanco, Cat and Garat, 2019). Or even such semi variable

costs are ignored sometimes during breakeven analysis making this technique or resulting

calculations quite inaccurate.

In reality sales revenue and cost which are variable do not increase in the same

proportions with the increase in the output volume as assumed in this analysis. At the

time, when the production is at very higher level, there seems to be less proportionality

between these factors due to the provision of discounts and economies of scale.

Comparison of the contribution associated with two different periods is not that possible

where there the time period involved is long as costs are considered to be change over a

long period of time.

Also, comparison cannot be possible on the basis of contribution between the two firms

when the amount of fixed costs associated with these firms differ. If even comparison is

done, it would be misleading and would never be accurate.

Marginal costing results in undervaluation of closing stock and accordingly this would

lead to under estimation in the final accounts as well (Calabrò, 2017). Such an under

estimation will lead to comparatively poor profitability and also distorted financial

position of the business.

calculations quite inaccurate.

In reality sales revenue and cost which are variable do not increase in the same

proportions with the increase in the output volume as assumed in this analysis. At the

time, when the production is at very higher level, there seems to be less proportionality

between these factors due to the provision of discounts and economies of scale.

Comparison of the contribution associated with two different periods is not that possible

where there the time period involved is long as costs are considered to be change over a

long period of time.

Also, comparison cannot be possible on the basis of contribution between the two firms

when the amount of fixed costs associated with these firms differ. If even comparison is

done, it would be misleading and would never be accurate.

Marginal costing results in undervaluation of closing stock and accordingly this would

lead to under estimation in the final accounts as well (Calabrò, 2017). Such an under

estimation will lead to comparatively poor profitability and also distorted financial

position of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Alkaraan, F., 2017. Strategic investment appraisal: multidisciplinary perspectives. In Advances

in Mergers and Acquisitions. Emerald Publishing Limited.

Pawlak, M., Rapacewicz, A. and Zarzecki, D., 2020. Investment Appraisal Practice in the

Biggest Companies in Poland. European Research Studies. 23(2). pp.137-147.

Nnamani, O. C., 2017. Application of Quantitative Risk Assessment Techniques in Property

Investment Appraisal in Enugu Urban, Nigeria. Journal of Land Management and

Appraisal. 5(1). pp.23-41.

Calabrò, F., 2017, July. Local communities and management of cultural heritage of the inner

areas. An application of break-even analysis. In International Conference on Computational

Science and Its Applications (pp. 516-531). Springer, Cham.

Tanco, M., Cat, L. and Garat, S., 2019. A break-even analysis for battery electric trucks in Latin

America. Journal of Cleaner Production. 228. pp.1354-1367.

Lee, M., and et.al., 2018. A break-even analysis and impact analysis of residential solar

photovoltaic systems considering state solar incentives. Technological and Economic

Development of Economy. 24(2). pp.358-382.

Alkaraan, F., 2017. Strategic investment appraisal: multidisciplinary perspectives. In Advances

in Mergers and Acquisitions. Emerald Publishing Limited.

Pawlak, M., Rapacewicz, A. and Zarzecki, D., 2020. Investment Appraisal Practice in the

Biggest Companies in Poland. European Research Studies. 23(2). pp.137-147.

Nnamani, O. C., 2017. Application of Quantitative Risk Assessment Techniques in Property

Investment Appraisal in Enugu Urban, Nigeria. Journal of Land Management and

Appraisal. 5(1). pp.23-41.

Calabrò, F., 2017, July. Local communities and management of cultural heritage of the inner

areas. An application of break-even analysis. In International Conference on Computational

Science and Its Applications (pp. 516-531). Springer, Cham.

Tanco, M., Cat, L. and Garat, S., 2019. A break-even analysis for battery electric trucks in Latin

America. Journal of Cleaner Production. 228. pp.1354-1367.

Lee, M., and et.al., 2018. A break-even analysis and impact analysis of residential solar

photovoltaic systems considering state solar incentives. Technological and Economic

Development of Economy. 24(2). pp.358-382.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.