Finance Assignment: Bogota plc Financial Analysis, MBA 03, Sem 1

VerifiedAdded on 2023/01/10

|9

|1168

|84

Homework Assignment

AI Summary

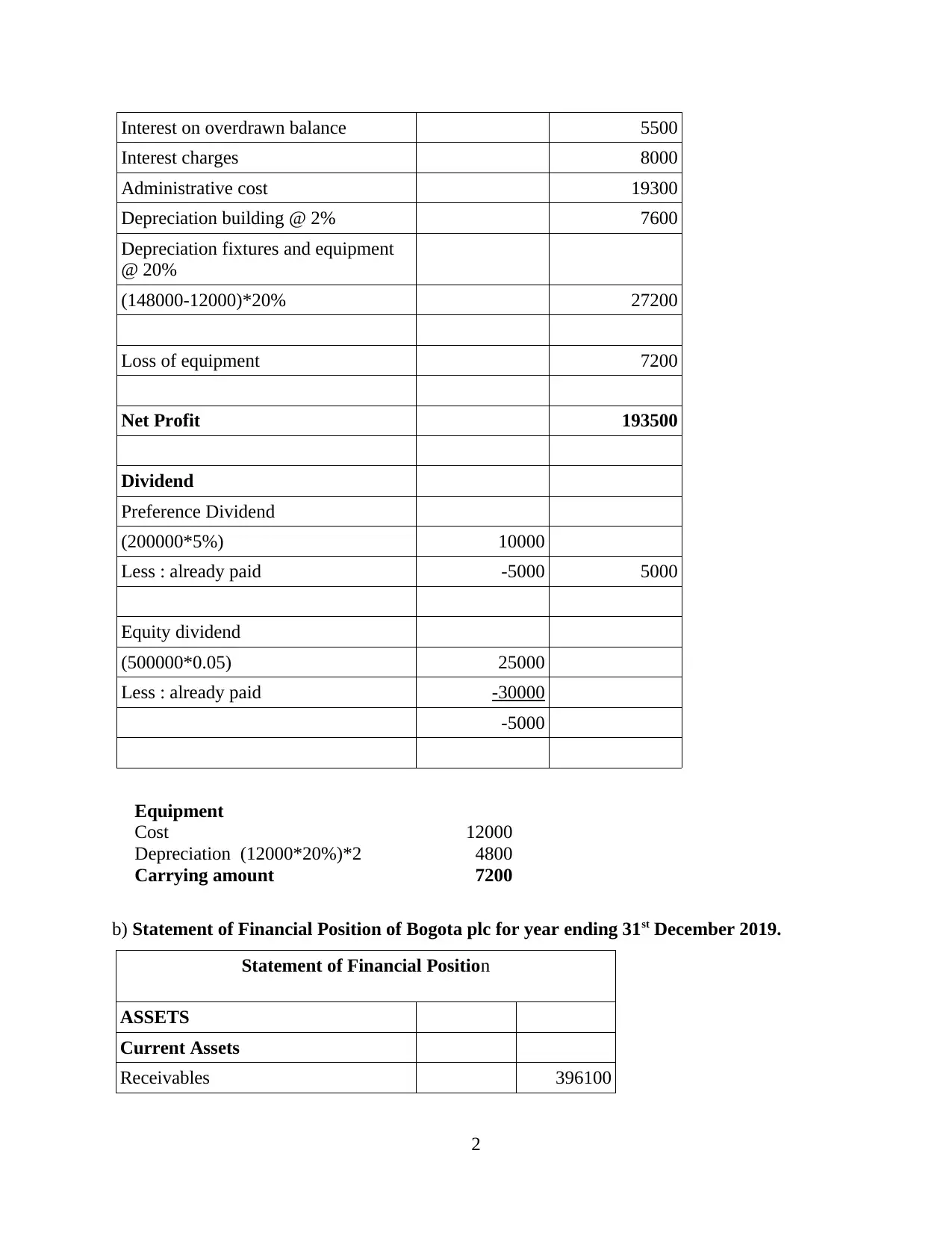

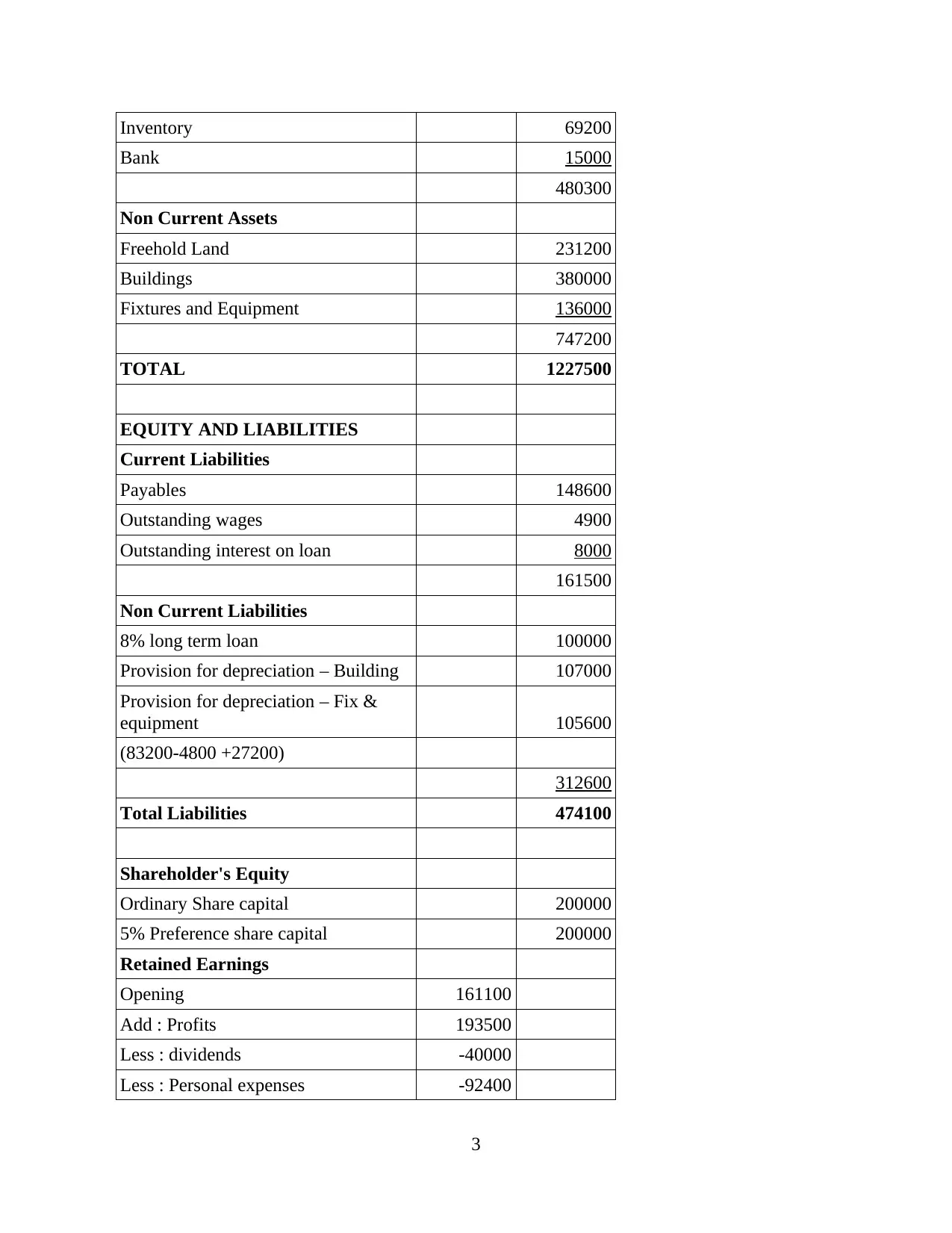

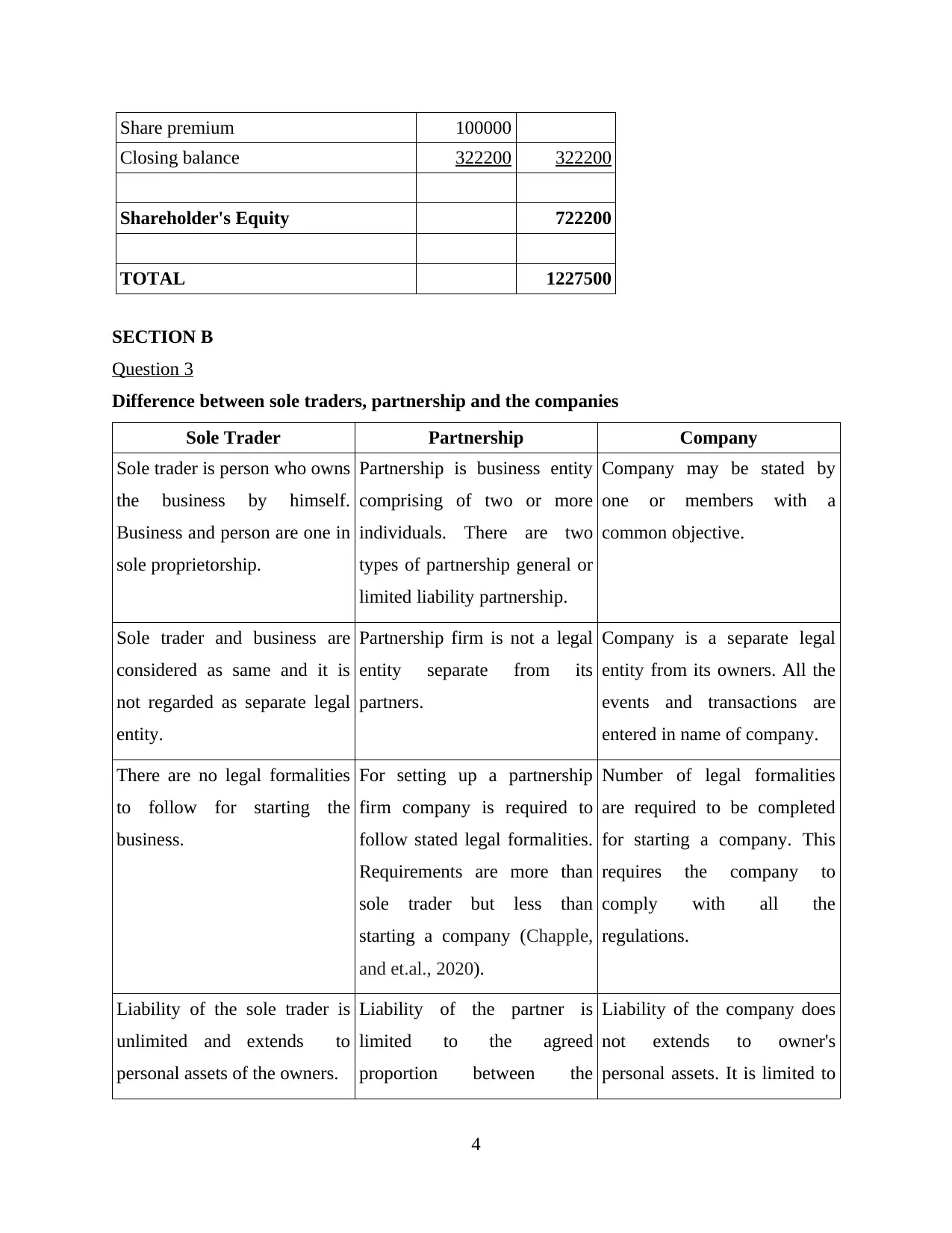

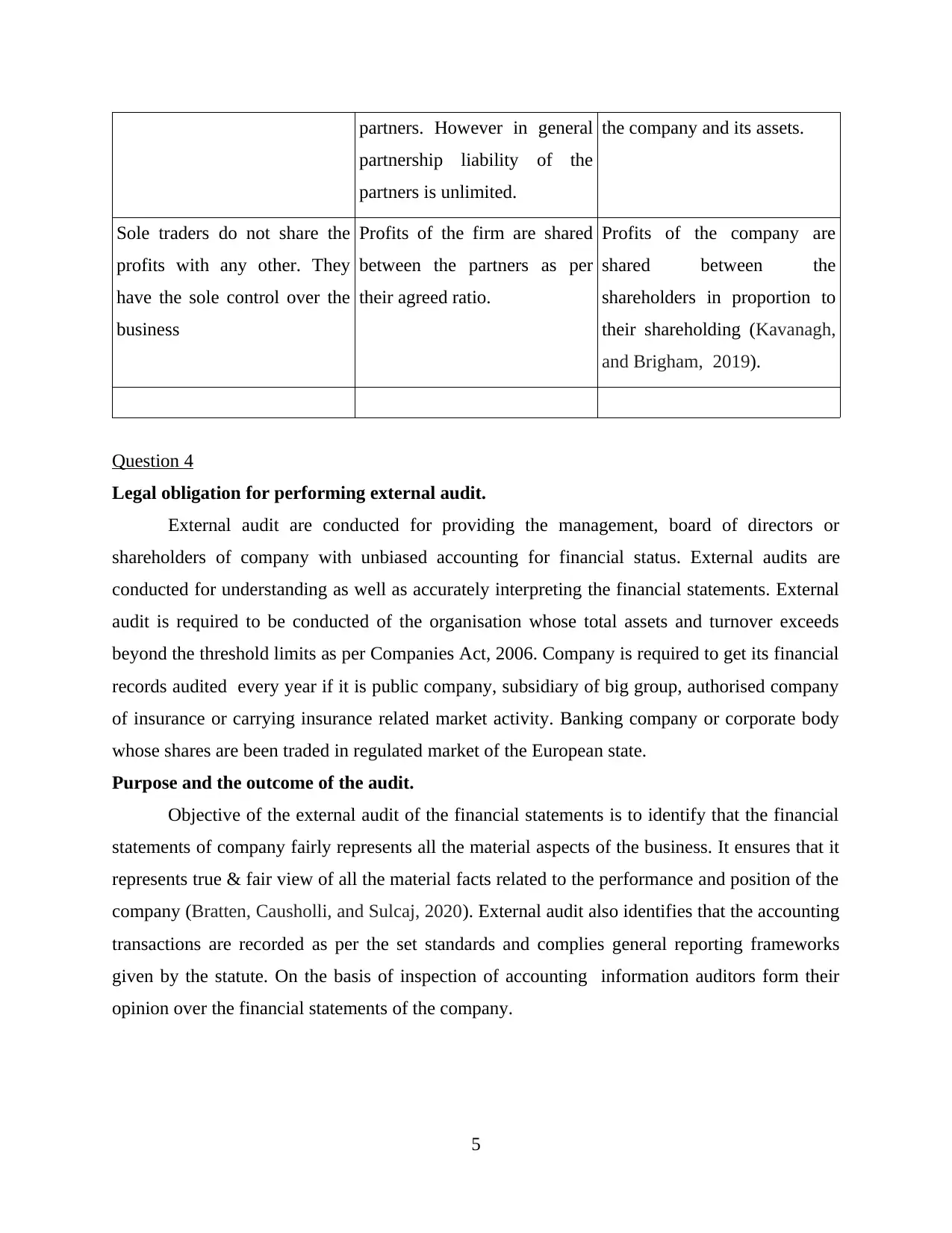

This assignment presents a comprehensive analysis of accountancy and finance principles. Section A focuses on the financial statements of Bogota plc, including the Statement of Profit or Loss and the Statement of Financial Position, with detailed workings. Section B delves into the differences between sole traders, partnerships, and companies, providing a comparative analysis of their characteristics, liabilities, and profit distribution. The assignment further explores the legal obligations related to external audits, outlining their purpose, outcomes, and requirements based on the Companies Act 2006. References to relevant academic resources are included to support the analysis and findings.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.