BA301 Finance Report: Stock Selection and Corporate Governance

VerifiedAdded on 2022/08/26

|28

|5348

|30

Report

AI Summary

This report, prepared for an Introduction to Finance course, delves into the critical aspects of stock selection and corporate governance. It analyzes the financial performance and corporate governance structures of two Australian companies, BHP and Wesfarmers. The report investigates the relationship between corporate governance practices and investment returns, emphasizing the significance of strong governance for company performance. Stock valuation is performed using the Gordon growth model to assess the relative value of the stocks, and the analysis also includes the dividend discount model. The report compares executive compensation with financial performance, and offers recommendations on stock selection and valuation methodologies. The research utilizes secondary data, including annual reports and academic journals, to support its findings and conclusions. The report aims to provide insights into making informed investment decisions and understanding the dynamics of financial management.

Running head: INTRODUCTION TO FINANCE

Introduction to finance

Name of the student

Name of the university

Student ID

Author note

Introduction to finance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

INTRODUCTION TO FINANCE

Executive Summary

Many authors have highlighted the importance of the study of finance in their respective

journal. Concerning about the financial study it is also important to know how the financial

management work. It helps to understand the project viability, stock valuation, firm valuation the

key analysis of financial ratios. The paper is all about the understanding of finance in terms of

stock selection to invest. It researches the annual report of BHP and Wesfarmers and articulates

that to select the proper stock, clarity in corporate governance is very important. It has a positive

impact on the company performance. To choose the correct stock to invest this report takes

“Gordon growth model” and after evaluating the stock by the growth model, research suggests

that both the stock value is overpriced. It has been detected that there is a proportionate

relationship between executive remuneration and company’s financial performance. The paper

also concludes which stock is better to invest and which model has to adopt to do the valuation

of stock.

INTRODUCTION TO FINANCE

Executive Summary

Many authors have highlighted the importance of the study of finance in their respective

journal. Concerning about the financial study it is also important to know how the financial

management work. It helps to understand the project viability, stock valuation, firm valuation the

key analysis of financial ratios. The paper is all about the understanding of finance in terms of

stock selection to invest. It researches the annual report of BHP and Wesfarmers and articulates

that to select the proper stock, clarity in corporate governance is very important. It has a positive

impact on the company performance. To choose the correct stock to invest this report takes

“Gordon growth model” and after evaluating the stock by the growth model, research suggests

that both the stock value is overpriced. It has been detected that there is a proportionate

relationship between executive remuneration and company’s financial performance. The paper

also concludes which stock is better to invest and which model has to adopt to do the valuation

of stock.

2

INTRODUCTION TO FINANCE

Table of Contents

Introduction......................................................................................................................................4

Literature review..............................................................................................................................5

Methodology....................................................................................................................................6

Corporate governance......................................................................................................................6

1. Corporate governance structure of BHP and Wesfarmers.......................................................6

BHP..................................................................................................................................................6

Wesfarmers......................................................................................................................................9

Responsibility of the Board.............................................................................................................9

Functions of Board........................................................................................................................10

Independent Directors....................................................................................................................10

The pragmatic relation between corporate governance and firms performance............................12

CEO- Leadership...........................................................................................................................12

Capital Budgeting..........................................................................................................................12

Compensation................................................................................................................................13

Communication..............................................................................................................................13

Competition...................................................................................................................................13

Analysis.........................................................................................................................................13

INTRODUCTION TO FINANCE

Table of Contents

Introduction......................................................................................................................................4

Literature review..............................................................................................................................5

Methodology....................................................................................................................................6

Corporate governance......................................................................................................................6

1. Corporate governance structure of BHP and Wesfarmers.......................................................6

BHP..................................................................................................................................................6

Wesfarmers......................................................................................................................................9

Responsibility of the Board.............................................................................................................9

Functions of Board........................................................................................................................10

Independent Directors....................................................................................................................10

The pragmatic relation between corporate governance and firms performance............................12

CEO- Leadership...........................................................................................................................12

Capital Budgeting..........................................................................................................................12

Compensation................................................................................................................................13

Communication..............................................................................................................................13

Competition...................................................................................................................................13

Analysis.........................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

INTRODUCTION TO FINANCE

2. Comparison between compensation and company performance...........................................14

3. Share valuation.......................................................................................................................15

Constant growth valuation model..................................................................................................15

BHP’s stock valuation under constant growth model....................................................................16

Wesfarmers’s stock valuation under constant growth model........................................................16

Zero growth valuation model.........................................................................................................16

BHP’s stock valuation under zero growth model..........................................................................17

Wesfarmers’s stock valuation under zero growth model..............................................................17

Variable Growth Valuation Model................................................................................................17

BHP vs. Wesfarmers- stocks comparison......................................................................................20

Popular stock valuation model.......................................................................................................22

Dividend discount model (DDM)..................................................................................................22

Discounted cash flow model..........................................................................................................23

Recommendations..........................................................................................................................23

Conclusion.....................................................................................................................................23

Reference.......................................................................................................................................24

INTRODUCTION TO FINANCE

2. Comparison between compensation and company performance...........................................14

3. Share valuation.......................................................................................................................15

Constant growth valuation model..................................................................................................15

BHP’s stock valuation under constant growth model....................................................................16

Wesfarmers’s stock valuation under constant growth model........................................................16

Zero growth valuation model.........................................................................................................16

BHP’s stock valuation under zero growth model..........................................................................17

Wesfarmers’s stock valuation under zero growth model..............................................................17

Variable Growth Valuation Model................................................................................................17

BHP vs. Wesfarmers- stocks comparison......................................................................................20

Popular stock valuation model.......................................................................................................22

Dividend discount model (DDM)..................................................................................................22

Discounted cash flow model..........................................................................................................23

Recommendations..........................................................................................................................23

Conclusion.....................................................................................................................................23

Reference.......................................................................................................................................24

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

INTRODUCTION TO FINANCE

Introduction

In the recent global competitive world, the business entity always intends to expand their

project. They need to produce at a large scale to meet the global demand as a result the company

needs to invest more. One of the most popular ways to raise money to invest is from public

through the issue of shares. The interest of the investors is always look upon the performance of

the stock, return of the stock, growth of the stock so all these depends on how well the company

perform (Revelli and Viviani 2015) The performance of the company will depend on some key

factors like company’s management, service, financial performance, corporate governance

structure. This report is critically analyze two Australian based mining company BHP and

Australian conglomerate Wesfarmers suggest which types of corporate governance should adopt

by them and for strong corporate governance and weak corporate governance what will be the

impact of the returns of investment. This report also highlights valuation techniques of the stock.

To select the right stock to invest an individual should always calculate the trend of the stock.

Therefore, valuation of the stock is necessary in the case of investment. The study researches all

the financial data of the selected two companies in terms of calculate the stock and therefore

suggests which company’s stock will best for investment. Analysis of financial ratio is also

included in this report to suggest the significance and interpretation of those particular ratios in

the selected company. The aim of this report is to provide legitimate research on stock selection

to invest. To make the healthy investment this study analyses various key financial and non-

financials path like corporate governance, this report asks about any correlation between good

corporate governance practice and impact of this on the return on investment. The report also

recommends how to evaluate the stock on depending on the Gordon Growth Model. Introduction

to finance may require acknowledging the financial management sometime (Ruppert 2014), so it

INTRODUCTION TO FINANCE

Introduction

In the recent global competitive world, the business entity always intends to expand their

project. They need to produce at a large scale to meet the global demand as a result the company

needs to invest more. One of the most popular ways to raise money to invest is from public

through the issue of shares. The interest of the investors is always look upon the performance of

the stock, return of the stock, growth of the stock so all these depends on how well the company

perform (Revelli and Viviani 2015) The performance of the company will depend on some key

factors like company’s management, service, financial performance, corporate governance

structure. This report is critically analyze two Australian based mining company BHP and

Australian conglomerate Wesfarmers suggest which types of corporate governance should adopt

by them and for strong corporate governance and weak corporate governance what will be the

impact of the returns of investment. This report also highlights valuation techniques of the stock.

To select the right stock to invest an individual should always calculate the trend of the stock.

Therefore, valuation of the stock is necessary in the case of investment. The study researches all

the financial data of the selected two companies in terms of calculate the stock and therefore

suggests which company’s stock will best for investment. Analysis of financial ratio is also

included in this report to suggest the significance and interpretation of those particular ratios in

the selected company. The aim of this report is to provide legitimate research on stock selection

to invest. To make the healthy investment this study analyses various key financial and non-

financials path like corporate governance, this report asks about any correlation between good

corporate governance practice and impact of this on the return on investment. The report also

recommends how to evaluate the stock on depending on the Gordon Growth Model. Introduction

to finance may require acknowledging the financial management sometime (Ruppert 2014), so it

5

INTRODUCTION TO FINANCE

is very essential that financial decisions look after the shareholders interest. After going through

the study, it was noted that there is some limitations such as dependency on the historical cost,

specific period based; there is some effects on inflation (Velte and Stawinoga 2017).

By doing the research of this financial study, report faced some issues these are:

The financial statement is prepared on a certain time gap. It usually prepared on a

quarterly basis or half-yearly basis so to extract the accurate financial data is very hard to

get while analyze the stock.

Ad- hoc transaction usually included in the financial statements, though it will not repeat

in the future.

It has been observed that in the financial report, closing balances may not match the

economic reality.

Literature review

According to the Ruppert (2014), much of finance is concerned to measure and manage the

financial risk. The return of an investment is its earning revenue as a fraction of the initial

investment. In case of all investments, future returns are cannot be evaluated exactly. Thus, it is a

random variable.

According to the Davies (2016), corporate governance is a strategic approach. Examines

the corporate governance from a philosophical and big picture standpoint. Here the authors

explore a number of key themes.

INTRODUCTION TO FINANCE

is very essential that financial decisions look after the shareholders interest. After going through

the study, it was noted that there is some limitations such as dependency on the historical cost,

specific period based; there is some effects on inflation (Velte and Stawinoga 2017).

By doing the research of this financial study, report faced some issues these are:

The financial statement is prepared on a certain time gap. It usually prepared on a

quarterly basis or half-yearly basis so to extract the accurate financial data is very hard to

get while analyze the stock.

Ad- hoc transaction usually included in the financial statements, though it will not repeat

in the future.

It has been observed that in the financial report, closing balances may not match the

economic reality.

Literature review

According to the Ruppert (2014), much of finance is concerned to measure and manage the

financial risk. The return of an investment is its earning revenue as a fraction of the initial

investment. In case of all investments, future returns are cannot be evaluated exactly. Thus, it is a

random variable.

According to the Davies (2016), corporate governance is a strategic approach. Examines

the corporate governance from a philosophical and big picture standpoint. Here the authors

explore a number of key themes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

INTRODUCTION TO FINANCE

Methodology

This research takes all the secondary data of the selected companies. To calculate the

stock valuation this study critically analyzes the company’s annual report and several journal. To

proof the theory of positive relativity of remuneration and the company’s performance this study

has adopted some theoretical part of hypothesis. To calculate the stock price, theory of “Gordon

model” has been implemented.

Corporate governance

Corporate governance is a business practice, which follows certain rules, regulations and

principles by which the organization is regulated. It involves the interest of the shareholders.

Since the corporate governance draws, a framework to achieve the organization’s goal it follows

the management’s actions plan and internal controls of measurement (Tricker and Tricker 2015).

1. Corporate governance structure of BHP and Wesfarmers

BHP

BHP’s governance philosophy, believes extraordinary core value, which creates a long-term

worth creation. Put the good governance in good business, is the primary mechanism is to adopt

the best governance standards in Australia. As per the company’s report good governance is also

the responsibility of the management executives and it is embedded within the group. By

practicing the good governance, the group’s board and management are guided by the company’s

charter values (bhp.com, 2020).

Such corporate governance rules the entity how they deal with their business on a regular

basis, expand them to perform very productively and leading in a very sustainable growth

INTRODUCTION TO FINANCE

Methodology

This research takes all the secondary data of the selected companies. To calculate the

stock valuation this study critically analyzes the company’s annual report and several journal. To

proof the theory of positive relativity of remuneration and the company’s performance this study

has adopted some theoretical part of hypothesis. To calculate the stock price, theory of “Gordon

model” has been implemented.

Corporate governance

Corporate governance is a business practice, which follows certain rules, regulations and

principles by which the organization is regulated. It involves the interest of the shareholders.

Since the corporate governance draws, a framework to achieve the organization’s goal it follows

the management’s actions plan and internal controls of measurement (Tricker and Tricker 2015).

1. Corporate governance structure of BHP and Wesfarmers

BHP

BHP’s governance philosophy, believes extraordinary core value, which creates a long-term

worth creation. Put the good governance in good business, is the primary mechanism is to adopt

the best governance standards in Australia. As per the company’s report good governance is also

the responsibility of the management executives and it is embedded within the group. By

practicing the good governance, the group’s board and management are guided by the company’s

charter values (bhp.com, 2020).

Such corporate governance rules the entity how they deal with their business on a regular

basis, expand them to perform very productively and leading in a very sustainable growth

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

INTRODUCTION TO FINANCE

strategy. By adopting the corporate governance, management play a vital role in risk inaccuracy,

engagement of public policy and the commitment to the environment and sustainability.

Practicing good governance in the entity, BHP’s Executives superintends the Principal Executive

professional and senior management and assures that suitable procedures and controls are in

place casing management activities in working the company on the basis business principles

(McAlister and Ferrell 2016).

Among the corporate governance of the company, some examples are highlighted below:

The framework of BHP’s governance describes the interaction between their shareholders

and the board and CEO as well. It also depicts the flow of delegation of the stockholders.

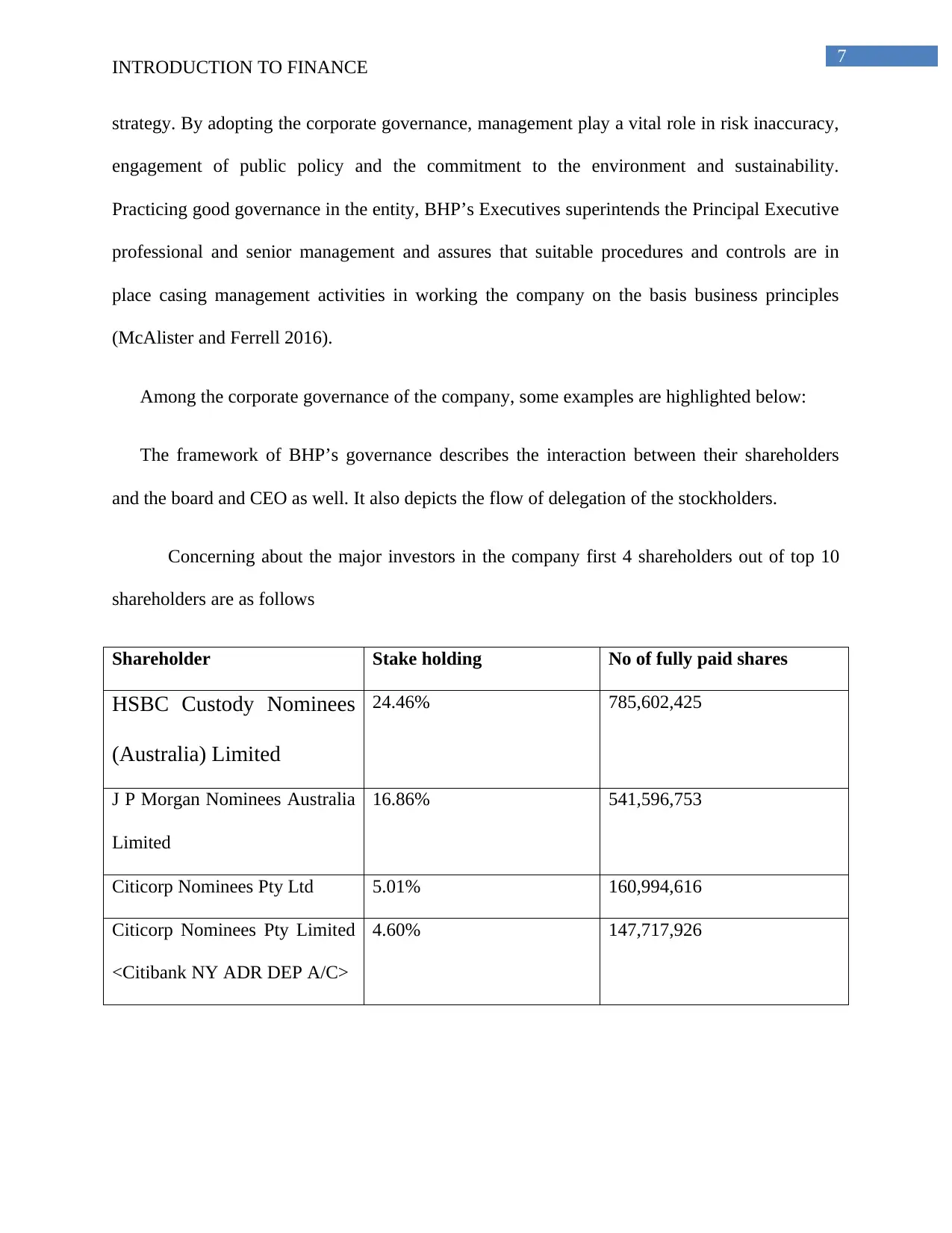

Concerning about the major investors in the company first 4 shareholders out of top 10

shareholders are as follows

Shareholder Stake holding No of fully paid shares

HSBC Custody Nominees

(Australia) Limited

24.46% 785,602,425

J P Morgan Nominees Australia

Limited

16.86% 541,596,753

Citicorp Nominees Pty Ltd 5.01% 160,994,616

Citicorp Nominees Pty Limited

<Citibank NY ADR DEP A/C>

4.60% 147,717,926

INTRODUCTION TO FINANCE

strategy. By adopting the corporate governance, management play a vital role in risk inaccuracy,

engagement of public policy and the commitment to the environment and sustainability.

Practicing good governance in the entity, BHP’s Executives superintends the Principal Executive

professional and senior management and assures that suitable procedures and controls are in

place casing management activities in working the company on the basis business principles

(McAlister and Ferrell 2016).

Among the corporate governance of the company, some examples are highlighted below:

The framework of BHP’s governance describes the interaction between their shareholders

and the board and CEO as well. It also depicts the flow of delegation of the stockholders.

Concerning about the major investors in the company first 4 shareholders out of top 10

shareholders are as follows

Shareholder Stake holding No of fully paid shares

HSBC Custody Nominees

(Australia) Limited

24.46% 785,602,425

J P Morgan Nominees Australia

Limited

16.86% 541,596,753

Citicorp Nominees Pty Ltd 5.01% 160,994,616

Citicorp Nominees Pty Limited

<Citibank NY ADR DEP A/C>

4.60% 147,717,926

8

INTRODUCTION TO FINANCE

The above table shows, major shareholders in BHP, among this HSBC is holding largest part of

the company as 24.46 percent stake, but not control the entity. The controlling power still lays in

hand of BHP.

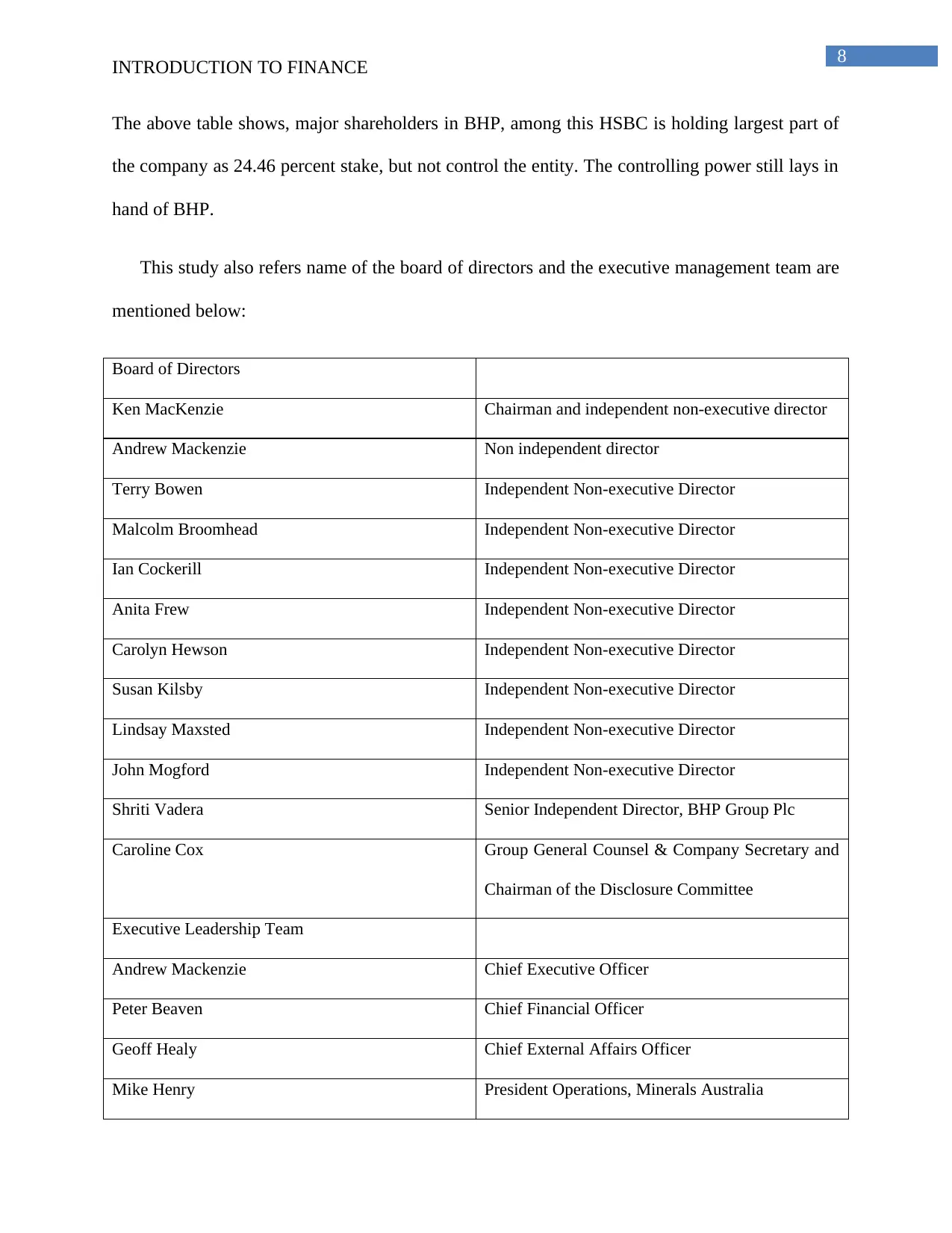

This study also refers name of the board of directors and the executive management team are

mentioned below:

Board of Directors

Ken MacKenzie Chairman and independent non-executive director

Andrew Mackenzie Non independent director

Terry Bowen Independent Non-executive Director

Malcolm Broomhead Independent Non-executive Director

Ian Cockerill Independent Non-executive Director

Anita Frew Independent Non-executive Director

Carolyn Hewson Independent Non-executive Director

Susan Kilsby Independent Non-executive Director

Lindsay Maxsted Independent Non-executive Director

John Mogford Independent Non-executive Director

Shriti Vadera Senior Independent Director, BHP Group Plc

Caroline Cox Group General Counsel & Company Secretary and

Chairman of the Disclosure Committee

Executive Leadership Team

Andrew Mackenzie Chief Executive Officer

Peter Beaven Chief Financial Officer

Geoff Healy Chief External Affairs Officer

Mike Henry President Operations, Minerals Australia

INTRODUCTION TO FINANCE

The above table shows, major shareholders in BHP, among this HSBC is holding largest part of

the company as 24.46 percent stake, but not control the entity. The controlling power still lays in

hand of BHP.

This study also refers name of the board of directors and the executive management team are

mentioned below:

Board of Directors

Ken MacKenzie Chairman and independent non-executive director

Andrew Mackenzie Non independent director

Terry Bowen Independent Non-executive Director

Malcolm Broomhead Independent Non-executive Director

Ian Cockerill Independent Non-executive Director

Anita Frew Independent Non-executive Director

Carolyn Hewson Independent Non-executive Director

Susan Kilsby Independent Non-executive Director

Lindsay Maxsted Independent Non-executive Director

John Mogford Independent Non-executive Director

Shriti Vadera Senior Independent Director, BHP Group Plc

Caroline Cox Group General Counsel & Company Secretary and

Chairman of the Disclosure Committee

Executive Leadership Team

Andrew Mackenzie Chief Executive Officer

Peter Beaven Chief Financial Officer

Geoff Healy Chief External Affairs Officer

Mike Henry President Operations, Minerals Australia

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

INTRODUCTION TO FINANCE

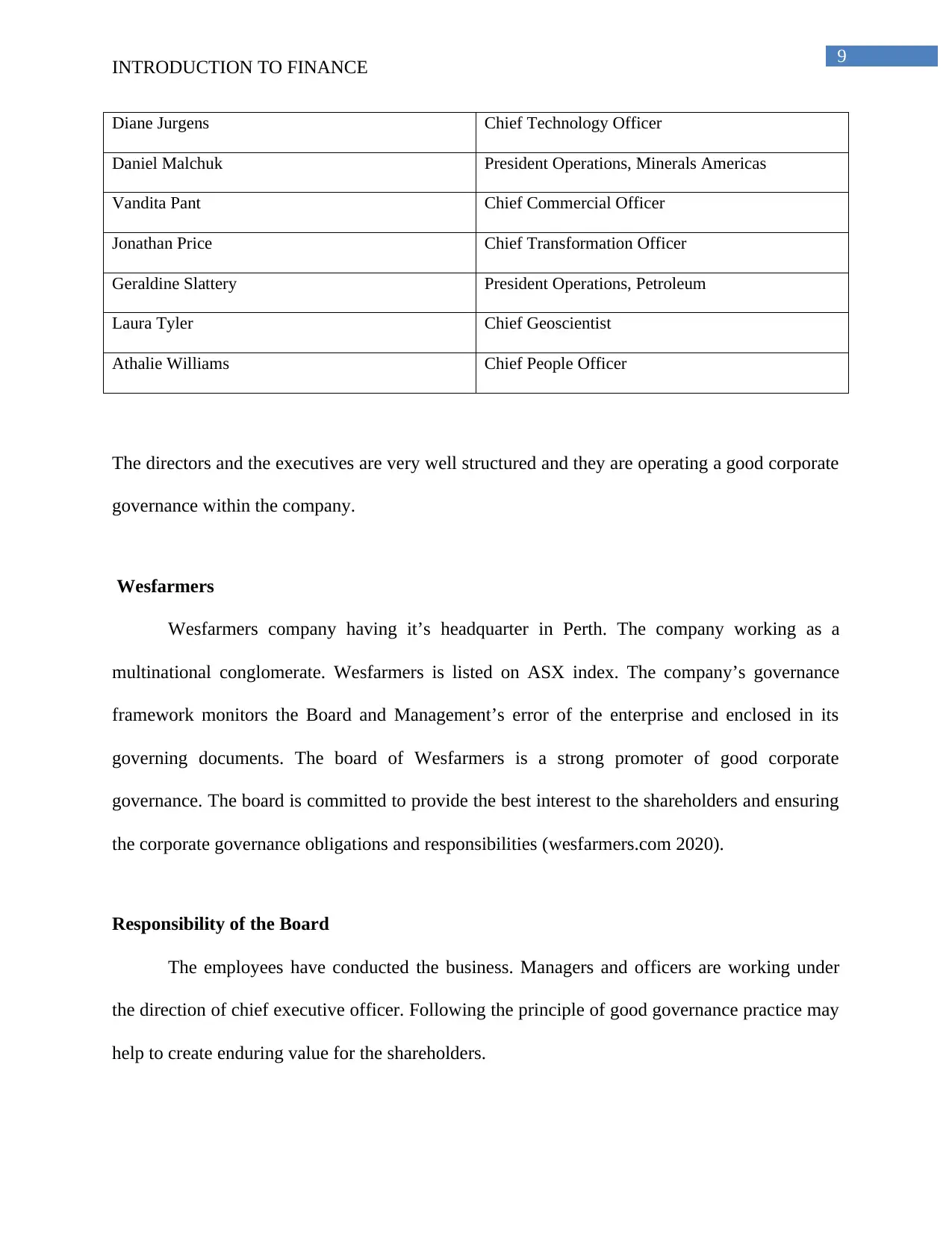

Diane Jurgens Chief Technology Officer

Daniel Malchuk President Operations, Minerals Americas

Vandita Pant Chief Commercial Officer

Jonathan Price Chief Transformation Officer

Geraldine Slattery President Operations, Petroleum

Laura Tyler Chief Geoscientist

Athalie Williams Chief People Officer

The directors and the executives are very well structured and they are operating a good corporate

governance within the company.

Wesfarmers

Wesfarmers company having it’s headquarter in Perth. The company working as a

multinational conglomerate. Wesfarmers is listed on ASX index. The company’s governance

framework monitors the Board and Management’s error of the enterprise and enclosed in its

governing documents. The board of Wesfarmers is a strong promoter of good corporate

governance. The board is committed to provide the best interest to the shareholders and ensuring

the corporate governance obligations and responsibilities (wesfarmers.com 2020).

Responsibility of the Board

The employees have conducted the business. Managers and officers are working under

the direction of chief executive officer. Following the principle of good governance practice may

help to create enduring value for the shareholders.

INTRODUCTION TO FINANCE

Diane Jurgens Chief Technology Officer

Daniel Malchuk President Operations, Minerals Americas

Vandita Pant Chief Commercial Officer

Jonathan Price Chief Transformation Officer

Geraldine Slattery President Operations, Petroleum

Laura Tyler Chief Geoscientist

Athalie Williams Chief People Officer

The directors and the executives are very well structured and they are operating a good corporate

governance within the company.

Wesfarmers

Wesfarmers company having it’s headquarter in Perth. The company working as a

multinational conglomerate. Wesfarmers is listed on ASX index. The company’s governance

framework monitors the Board and Management’s error of the enterprise and enclosed in its

governing documents. The board of Wesfarmers is a strong promoter of good corporate

governance. The board is committed to provide the best interest to the shareholders and ensuring

the corporate governance obligations and responsibilities (wesfarmers.com 2020).

Responsibility of the Board

The employees have conducted the business. Managers and officers are working under

the direction of chief executive officer. Following the principle of good governance practice may

help to create enduring value for the shareholders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

INTRODUCTION TO FINANCE

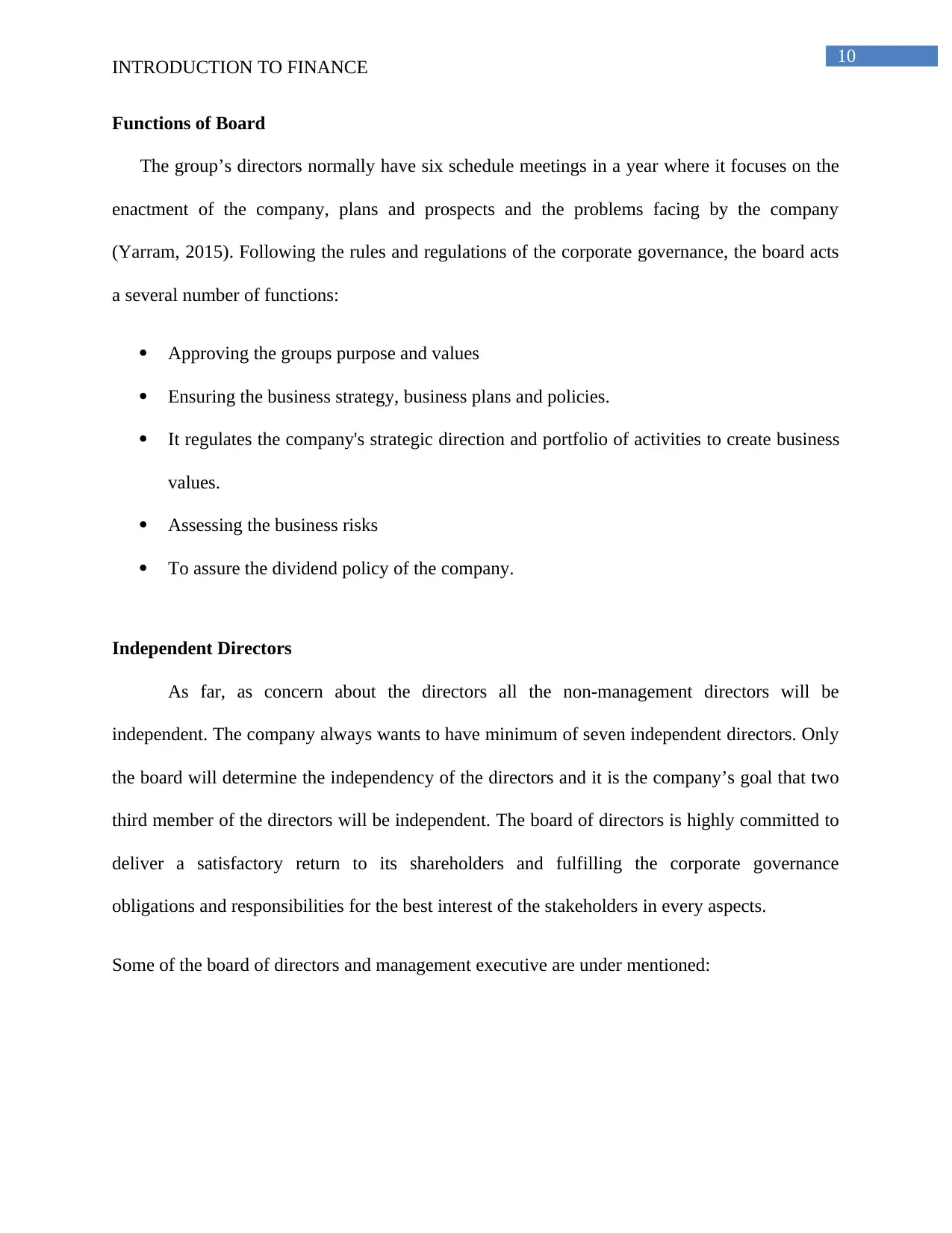

Functions of Board

The group’s directors normally have six schedule meetings in a year where it focuses on the

enactment of the company, plans and prospects and the problems facing by the company

(Yarram, 2015). Following the rules and regulations of the corporate governance, the board acts

a several number of functions:

Approving the groups purpose and values

Ensuring the business strategy, business plans and policies.

It regulates the company's strategic direction and portfolio of activities to create business

values.

Assessing the business risks

To assure the dividend policy of the company.

Independent Directors

As far, as concern about the directors all the non-management directors will be

independent. The company always wants to have minimum of seven independent directors. Only

the board will determine the independency of the directors and it is the company’s goal that two

third member of the directors will be independent. The board of directors is highly committed to

deliver a satisfactory return to its shareholders and fulfilling the corporate governance

obligations and responsibilities for the best interest of the stakeholders in every aspects.

Some of the board of directors and management executive are under mentioned:

INTRODUCTION TO FINANCE

Functions of Board

The group’s directors normally have six schedule meetings in a year where it focuses on the

enactment of the company, plans and prospects and the problems facing by the company

(Yarram, 2015). Following the rules and regulations of the corporate governance, the board acts

a several number of functions:

Approving the groups purpose and values

Ensuring the business strategy, business plans and policies.

It regulates the company's strategic direction and portfolio of activities to create business

values.

Assessing the business risks

To assure the dividend policy of the company.

Independent Directors

As far, as concern about the directors all the non-management directors will be

independent. The company always wants to have minimum of seven independent directors. Only

the board will determine the independency of the directors and it is the company’s goal that two

third member of the directors will be independent. The board of directors is highly committed to

deliver a satisfactory return to its shareholders and fulfilling the corporate governance

obligations and responsibilities for the best interest of the stakeholders in every aspects.

Some of the board of directors and management executive are under mentioned:

11

INTRODUCTION TO FINANCE

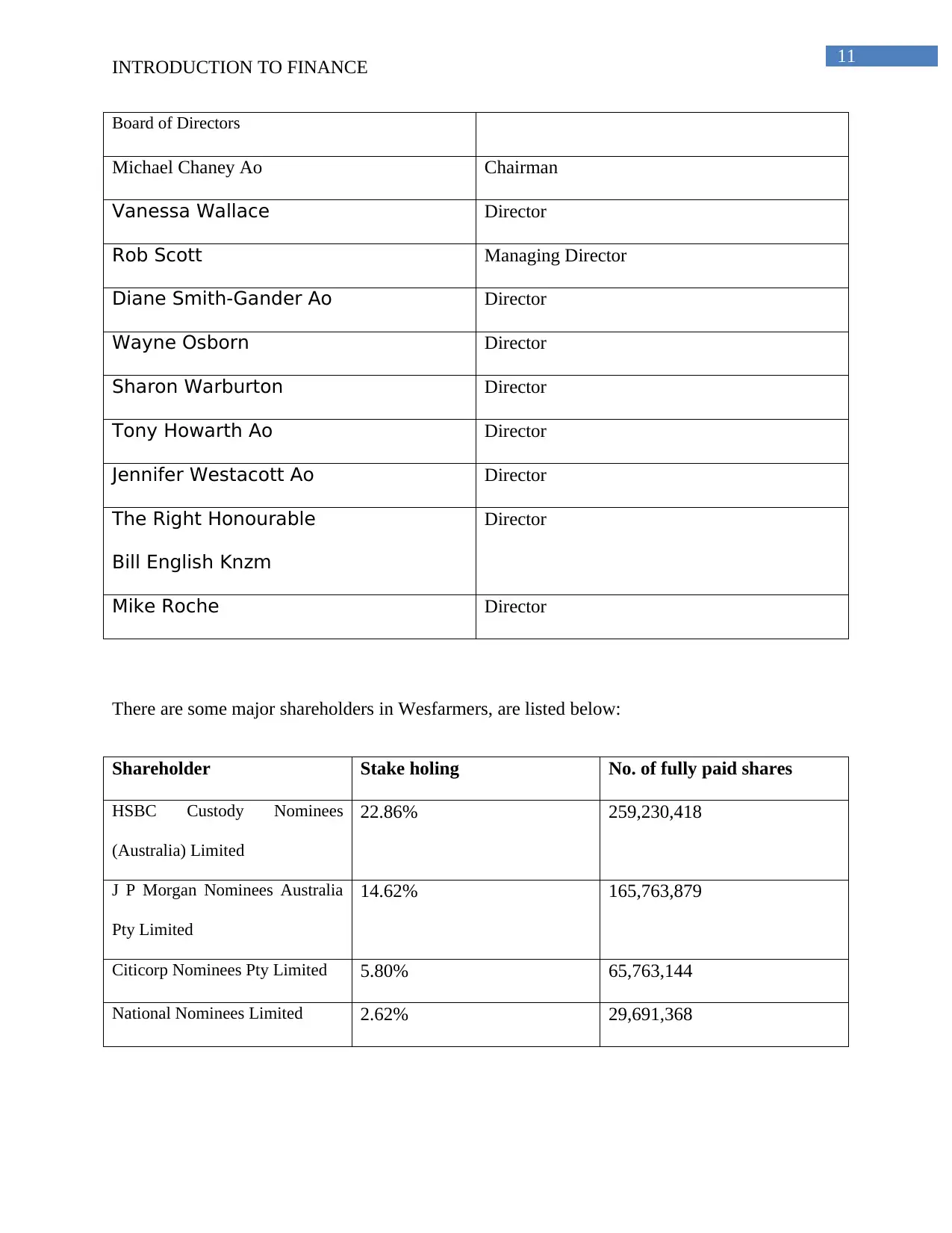

Board of Directors

Michael Chaney Ao Chairman

Vanessa Wallace Director

Rob Scott Managing Director

Diane Smith-Gander Ao Director

Wayne Osborn Director

Sharon Warburton Director

Tony Howarth Ao Director

Jennifer Westacott Ao Director

The Right Honourable

Bill English Knzm

Director

Mike Roche Director

There are some major shareholders in Wesfarmers, are listed below:

Shareholder Stake holing No. of fully paid shares

HSBC Custody Nominees

(Australia) Limited

22.86% 259,230,418

J P Morgan Nominees Australia

Pty Limited

14.62% 165,763,879

Citicorp Nominees Pty Limited 5.80% 65,763,144

National Nominees Limited 2.62% 29,691,368

INTRODUCTION TO FINANCE

Board of Directors

Michael Chaney Ao Chairman

Vanessa Wallace Director

Rob Scott Managing Director

Diane Smith-Gander Ao Director

Wayne Osborn Director

Sharon Warburton Director

Tony Howarth Ao Director

Jennifer Westacott Ao Director

The Right Honourable

Bill English Knzm

Director

Mike Roche Director

There are some major shareholders in Wesfarmers, are listed below:

Shareholder Stake holing No. of fully paid shares

HSBC Custody Nominees

(Australia) Limited

22.86% 259,230,418

J P Morgan Nominees Australia

Pty Limited

14.62% 165,763,879

Citicorp Nominees Pty Limited 5.80% 65,763,144

National Nominees Limited 2.62% 29,691,368

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.