Finance in Hospitality: Analysis of Costs, Ratios, and Decisions

VerifiedAdded on 2019/12/03

|18

|5008

|356

Report

AI Summary

This report provides a comprehensive analysis of financial management within the hospitality industry. It begins by identifying various sources of funding available to a hypothetical business, including bank loans, leasing, and equity financing. The report then delves into strategies for income generation, such as hiring commission agents and leveraging sponsorships, while also examining cost elements, gross profit calculations, and pricing strategies. Furthermore, it explores methods for controlling stock and cash flow, including techniques like Just-In-Time inventory and internal audits. The report also covers the structure and purpose of trial balances and budgetary control, providing a detailed breakdown of financial statements and variance analysis. Finally, it includes a ratio analysis to assess financial performance and recommend future management strategies.

Finance in Hospitality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

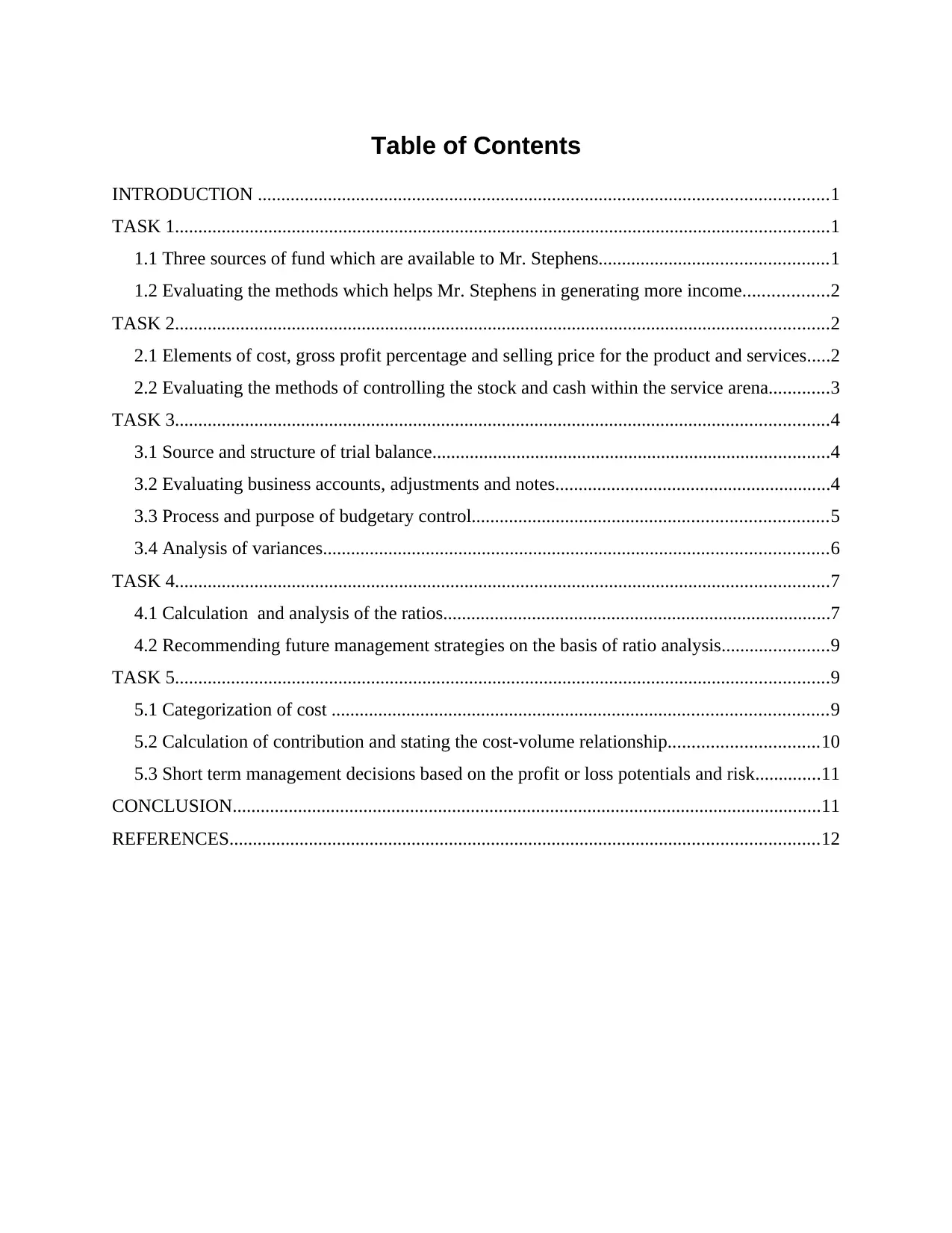

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Three sources of fund which are available to Mr. Stephens.................................................1

1.2 Evaluating the methods which helps Mr. Stephens in generating more income..................2

TASK 2............................................................................................................................................2

2.1 Elements of cost, gross profit percentage and selling price for the product and services.....2

2.2 Evaluating the methods of controlling the stock and cash within the service arena.............3

TASK 3............................................................................................................................................4

3.1 Source and structure of trial balance.....................................................................................4

3.2 Evaluating business accounts, adjustments and notes...........................................................4

3.3 Process and purpose of budgetary control............................................................................5

3.4 Analysis of variances............................................................................................................6

TASK 4............................................................................................................................................7

4.1 Calculation and analysis of the ratios...................................................................................7

4.2 Recommending future management strategies on the basis of ratio analysis.......................9

TASK 5............................................................................................................................................9

5.1 Categorization of cost ..........................................................................................................9

5.2 Calculation of contribution and stating the cost-volume relationship................................10

5.3 Short term management decisions based on the profit or loss potentials and risk..............11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Three sources of fund which are available to Mr. Stephens.................................................1

1.2 Evaluating the methods which helps Mr. Stephens in generating more income..................2

TASK 2............................................................................................................................................2

2.1 Elements of cost, gross profit percentage and selling price for the product and services.....2

2.2 Evaluating the methods of controlling the stock and cash within the service arena.............3

TASK 3............................................................................................................................................4

3.1 Source and structure of trial balance.....................................................................................4

3.2 Evaluating business accounts, adjustments and notes...........................................................4

3.3 Process and purpose of budgetary control............................................................................5

3.4 Analysis of variances............................................................................................................6

TASK 4............................................................................................................................................7

4.1 Calculation and analysis of the ratios...................................................................................7

4.2 Recommending future management strategies on the basis of ratio analysis.......................9

TASK 5............................................................................................................................................9

5.1 Categorization of cost ..........................................................................................................9

5.2 Calculation of contribution and stating the cost-volume relationship................................10

5.3 Short term management decisions based on the profit or loss potentials and risk..............11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Finance is one of the main resource without which no one can survive in the dynamic

business environment. Growth and development of hospitality industry highly depends upon the

uniqueness of product and services which are introduced by an organization (Hales, 2005.). For

this, organization needs to undertake research and development activity which imposes cost in

front of them. In this, finance manager of an organization play a vital in making effective

strategies which facilitates optimum utilization of finance (Baker and English, 2009). This

project report is based on the scenario which depicts sources through which Mr. Stephens can

raise finance and thereby meet their requirements. Besides this, it will develop understanding

about the elements of cost, gross profit percentage and selling price for the product and services.

The present report will also discuss about the ratio analysis techniques to assess financial

performance. It also states the process and purpose of budgetary control in functioning of the

business organization.

TASK 1

1.1 Three sources of fund which are available to Mr. Stephens

There are mainly three sources of finance which are available to Mr. Stephens through

which they can raise to meet their financial requirements for the new business. Sources of

finance include bank loan, leasing, issue of share and debentures and venture capital which helps

him in meeting their financial needs.

Short term sources of finance-

S.No

.

Source Feature Advantages Disadvantages

1 Bank loan Bank loan is one of the simplest

methods of raising the funds

from the bank. Bank lends

money to the company by

charging the interest (Baker and

Powell, 2009).

This loan can easily

be procured and the

interest paid on this is

tax deductible.

Banks charges high

rate of interest

from the borrowers

2 Leasing Leasing is an agreement Mr. Stephens can use Lessee who

1

Finance is one of the main resource without which no one can survive in the dynamic

business environment. Growth and development of hospitality industry highly depends upon the

uniqueness of product and services which are introduced by an organization (Hales, 2005.). For

this, organization needs to undertake research and development activity which imposes cost in

front of them. In this, finance manager of an organization play a vital in making effective

strategies which facilitates optimum utilization of finance (Baker and English, 2009). This

project report is based on the scenario which depicts sources through which Mr. Stephens can

raise finance and thereby meet their requirements. Besides this, it will develop understanding

about the elements of cost, gross profit percentage and selling price for the product and services.

The present report will also discuss about the ratio analysis techniques to assess financial

performance. It also states the process and purpose of budgetary control in functioning of the

business organization.

TASK 1

1.1 Three sources of fund which are available to Mr. Stephens

There are mainly three sources of finance which are available to Mr. Stephens through

which they can raise to meet their financial requirements for the new business. Sources of

finance include bank loan, leasing, issue of share and debentures and venture capital which helps

him in meeting their financial needs.

Short term sources of finance-

S.No

.

Source Feature Advantages Disadvantages

1 Bank loan Bank loan is one of the simplest

methods of raising the funds

from the bank. Bank lends

money to the company by

charging the interest (Baker and

Powell, 2009).

This loan can easily

be procured and the

interest paid on this is

tax deductible.

Banks charges high

rate of interest

from the borrowers

2 Leasing Leasing is an agreement Mr. Stephens can use Lessee who

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

between two people in order to

buy the asset for use for some

period of type.

asset without making

huge investment in

purchasing it.

purchases the

assets has to pay

rental charges to

the lesser on a

regular basis.

Long term sources of finance-

S.No

.

Source Meaning Advantages Disadvantages

1 Issue of

shares

Issue of shares is one of the

easiest methods to raise long

term finance. Company issue

shares to the general public in

order to raise the funds.

Different types of shares are

issued by the company to raise

the funds (Brigham and

Ehrhardt, 2013).

No fixed rate of

interest need to be

paid to the equity

shares holders.

Dividend paid to

the shareholder is

not tax deductible

expenditure.

2 Issue of

debentures

Mr. Stephen can also raise

funds by issuing the debentures

to the general public.

Debentures can easily be

redeemed after a specific

period of time. Debentures

holder does not have any

voting rights.

Interest paid to the

debenture holders is

tax deductible

expenditure which

Mr. Stephen can

easily recover at the

time of paying

income tax.

A fixed rate of

interest need to be

paid to the

debenture holders

even in the

condition of losses.

3 Retained

earning

Retained earnings are the part

of profit which is kept by the

company in advance in order

to meet its sudden requirement

It is one of the

cheaper sources of

raising finance.

It does not allow

the company to

utilize the company

actual earning to

2

buy the asset for use for some

period of type.

asset without making

huge investment in

purchasing it.

purchases the

assets has to pay

rental charges to

the lesser on a

regular basis.

Long term sources of finance-

S.No

.

Source Meaning Advantages Disadvantages

1 Issue of

shares

Issue of shares is one of the

easiest methods to raise long

term finance. Company issue

shares to the general public in

order to raise the funds.

Different types of shares are

issued by the company to raise

the funds (Brigham and

Ehrhardt, 2013).

No fixed rate of

interest need to be

paid to the equity

shares holders.

Dividend paid to

the shareholder is

not tax deductible

expenditure.

2 Issue of

debentures

Mr. Stephen can also raise

funds by issuing the debentures

to the general public.

Debentures can easily be

redeemed after a specific

period of time. Debentures

holder does not have any

voting rights.

Interest paid to the

debenture holders is

tax deductible

expenditure which

Mr. Stephen can

easily recover at the

time of paying

income tax.

A fixed rate of

interest need to be

paid to the

debenture holders

even in the

condition of losses.

3 Retained

earning

Retained earnings are the part

of profit which is kept by the

company in advance in order

to meet its sudden requirement

It is one of the

cheaper sources of

raising finance.

It does not allow

the company to

utilize the company

actual earning to

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of the fund. the full extent.

Stephen should approach for the bank loan to meet their financial requirements for

meeting short term requirement of the fund in order to starting up new business. By giving

financial security to bank, Stephen can easily meet his financial needs. Similarly, in order to

meet it long term requirement of the funds in order to start a new business Mr. Stephen can raise

funds through venture capital (Brigham and Ehrhardt, 2013).

1.2 Evaluating the methods which helps Mr. Stephens in generating more income

There are several methods through which Mr. Stephen can generate more income and

thereby helps in achieving success in the competitive business arena. In order to maximize sales

as well profit of the business, Stephens can hire commission agent which will help him in

attracting more customers. By appoint a commission agent Stephen will be able to increase the

sales of its products and services. This is turn will create brand awareness in the mind of the

customers. By taking into consideration the direct selling method an agent will also be able to

take the feedback from the customers who in turn will assist the Stephen to prepare various

strategies in order to increase its sales and beat its competitors. However, it is to be critically

evaluated that if Stephens hire commission agent then he needs to pay commission to the agent.

On other hand, in sponsorship he enjoys financial support from the reputed organization. It

provides benefit to him in terms of high sales revenue. Besides this, by taking sponsorship from

the well-known brand he can build awareness about the product and services which they

introduce in the market. It provides opportunity to Stephen to present their offering as unique

against its competitors (Drake and Fabozzi, 2012). Through this, he is able to increase his brand

image and market share.

TASK 2

2.1 Elements of cost, gross profit percentage and selling price for the product and services

There are mainly two types of cost such as direct and indirect cost which are enumerated

below: Direct cost: It is also termed as prime cost because it is directly related to the production

of a product and it is directly accountable to a cost object. It consists of cost of material,

3

Stephen should approach for the bank loan to meet their financial requirements for

meeting short term requirement of the fund in order to starting up new business. By giving

financial security to bank, Stephen can easily meet his financial needs. Similarly, in order to

meet it long term requirement of the funds in order to start a new business Mr. Stephen can raise

funds through venture capital (Brigham and Ehrhardt, 2013).

1.2 Evaluating the methods which helps Mr. Stephens in generating more income

There are several methods through which Mr. Stephen can generate more income and

thereby helps in achieving success in the competitive business arena. In order to maximize sales

as well profit of the business, Stephens can hire commission agent which will help him in

attracting more customers. By appoint a commission agent Stephen will be able to increase the

sales of its products and services. This is turn will create brand awareness in the mind of the

customers. By taking into consideration the direct selling method an agent will also be able to

take the feedback from the customers who in turn will assist the Stephen to prepare various

strategies in order to increase its sales and beat its competitors. However, it is to be critically

evaluated that if Stephens hire commission agent then he needs to pay commission to the agent.

On other hand, in sponsorship he enjoys financial support from the reputed organization. It

provides benefit to him in terms of high sales revenue. Besides this, by taking sponsorship from

the well-known brand he can build awareness about the product and services which they

introduce in the market. It provides opportunity to Stephen to present their offering as unique

against its competitors (Drake and Fabozzi, 2012). Through this, he is able to increase his brand

image and market share.

TASK 2

2.1 Elements of cost, gross profit percentage and selling price for the product and services

There are mainly two types of cost such as direct and indirect cost which are enumerated

below: Direct cost: It is also termed as prime cost because it is directly related to the production

of a product and it is directly accountable to a cost object. It consists of cost of material,

3

labor and other expenses which are incurred by an organization in relation to production

of a product.

◦ Direct material-Direct material cost is the cost which can easily be identify at the

time of production. For example-cost of the glass, cost of the bulb and so on.

◦ Direct labor- Direct labor cost is the cost associated with the manufacture of the

product. It involved in the production process not in administration, maintenance or

any other services

◦ Direct expenses-Direct expenses are the expenses which are incurred with the

purchase of goods. For example- freight, carriage, wages and so on.

Indirect cost: Indirect costs are those which are not directly attributable to a particular

project and function. It may be either fixed or variable cost depending upon the nature of

the expenses (Batta, Ganguly and Rosett, 2014). Fixed costs are those which remain fixed

irrespective of the changes which take place in the level of output such as salary etc.

Whereas variable costs are those which changes according to the change in the level of

output.

Selling price: It is the summation of cost and gross profit percentage. Costs are those

which is incurred by an organization to produce a per unit product. Whereas gross profit

percentage entails the margin which organization wishes to earn by selling per unit of

product.

Relationship between cost, gross profit and selling price are as follows:

Selling price = cost + cost *profit%

For instance: Per unit cost of the product= 300

Gross profit% = 10%

Selling price = 300+300*10%

=300+30=330

If Stephens wishes to earn 10% profit margin then he needs to sell his product @330each.

2.2 Evaluating the methods of controlling the stock and cash within the service arena

In order to control the stock Stephen can use just in time and economic order quantity

which facilitates effective use and management of stock. In just in time technique, company

make order of stock only when they are needed which reduces wastage and holding cost.

However, it is to be critically evaluated that this technique may cause of the delay in the

4

of a product.

◦ Direct material-Direct material cost is the cost which can easily be identify at the

time of production. For example-cost of the glass, cost of the bulb and so on.

◦ Direct labor- Direct labor cost is the cost associated with the manufacture of the

product. It involved in the production process not in administration, maintenance or

any other services

◦ Direct expenses-Direct expenses are the expenses which are incurred with the

purchase of goods. For example- freight, carriage, wages and so on.

Indirect cost: Indirect costs are those which are not directly attributable to a particular

project and function. It may be either fixed or variable cost depending upon the nature of

the expenses (Batta, Ganguly and Rosett, 2014). Fixed costs are those which remain fixed

irrespective of the changes which take place in the level of output such as salary etc.

Whereas variable costs are those which changes according to the change in the level of

output.

Selling price: It is the summation of cost and gross profit percentage. Costs are those

which is incurred by an organization to produce a per unit product. Whereas gross profit

percentage entails the margin which organization wishes to earn by selling per unit of

product.

Relationship between cost, gross profit and selling price are as follows:

Selling price = cost + cost *profit%

For instance: Per unit cost of the product= 300

Gross profit% = 10%

Selling price = 300+300*10%

=300+30=330

If Stephens wishes to earn 10% profit margin then he needs to sell his product @330each.

2.2 Evaluating the methods of controlling the stock and cash within the service arena

In order to control the stock Stephen can use just in time and economic order quantity

which facilitates effective use and management of stock. In just in time technique, company

make order of stock only when they are needed which reduces wastage and holding cost.

However, it is to be critically evaluated that this technique may cause of the delay in the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

production. Moreover, company makes order on the basis of their requirements which hampers

the smooth production of business activities (Dagiliene, 2015). In contrary to this, economic

order quantity is to most effective technique through which company is able to reduce carrying

and ordering cost. In this, company assesses the need of the stock which they require for the

smooth production. Further, it is to be critically evaluated that to assess EOQ Company requires

highly developed and updated software which imposer high cost in front of the company.

In addition to this, to manage cash related activities more effectively and efficiently

Stephens needs to undertake internal audit. Through this, he is able to assess the areas where they

need to make control over the expenses. It enables him to manage cash effectively and invest the

fund in the research and development activity to build customer satisfaction and loyalty.

S.no Basis Inventory control Cash control

1 Meaning Inventory control is the activity

of checking the shop's stock. It

can also be said as the software

which helps in managing the

stock.

Cash control is the mode of

monitoring the credit, cash allocation

and disbursement of various policies.

2 Objective It is used by the company to

manage the stock of the company

in order to utilize the resources to

the full extent.

It is used by the company to manage

the cash and to catch the various

fraudulent activities being performed

in the organization.

TASK 3

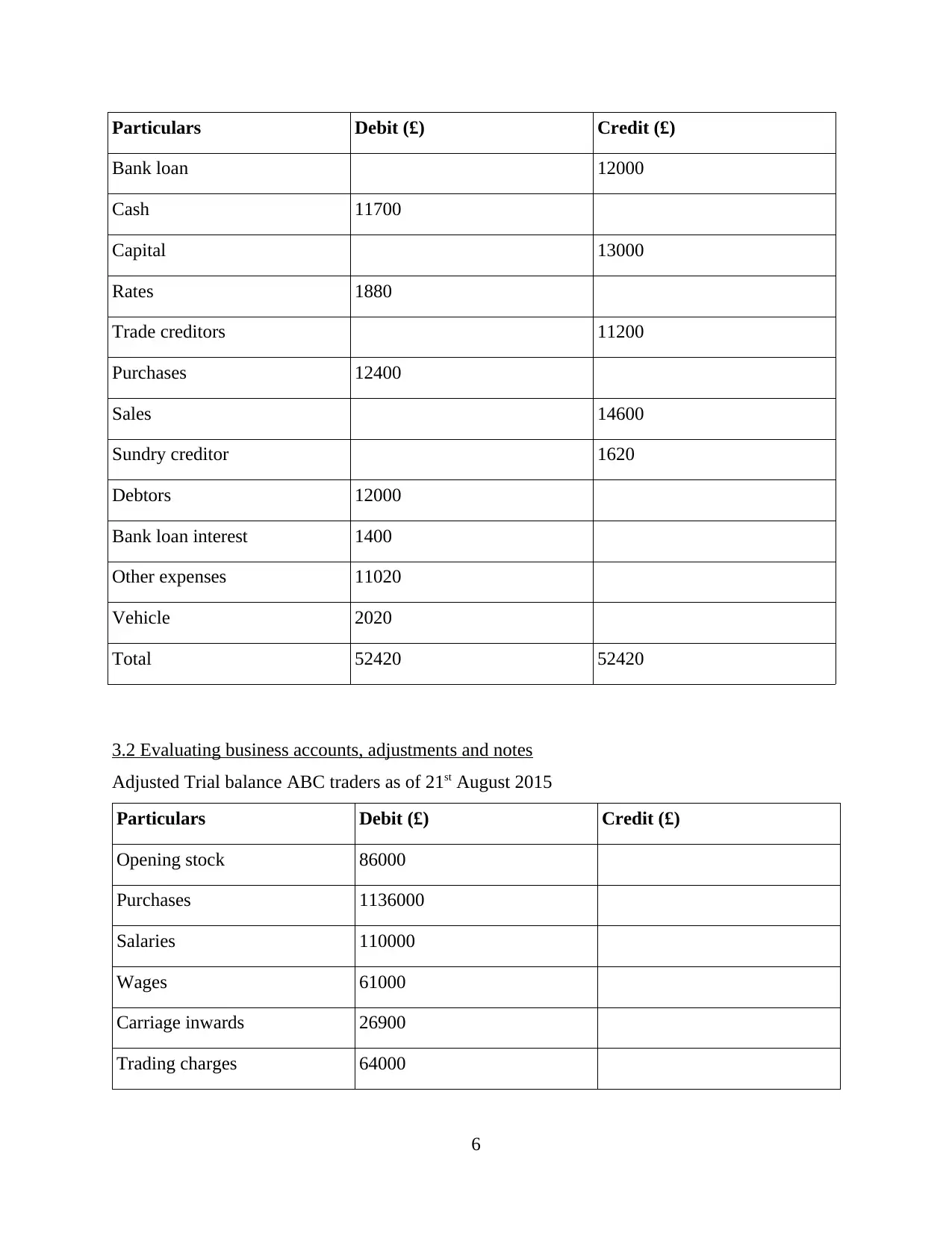

3.1 Source and structure of trial balance

Trial balance is the first step of preparing financial statement which summarizes all the

debit and credit balance of ledger accounts. One of the main sources of trial balance is ledger

account which is prepared by the organization for their each and every transaction (Chen, Kim

and Chen, 2007). It is prepared by the organization at the end of the financial year which

provides deeper insight to an organization about their transactions. Therefore, trial balance is

prepared below considering the given data.

Trial balance:

5

the smooth production of business activities (Dagiliene, 2015). In contrary to this, economic

order quantity is to most effective technique through which company is able to reduce carrying

and ordering cost. In this, company assesses the need of the stock which they require for the

smooth production. Further, it is to be critically evaluated that to assess EOQ Company requires

highly developed and updated software which imposer high cost in front of the company.

In addition to this, to manage cash related activities more effectively and efficiently

Stephens needs to undertake internal audit. Through this, he is able to assess the areas where they

need to make control over the expenses. It enables him to manage cash effectively and invest the

fund in the research and development activity to build customer satisfaction and loyalty.

S.no Basis Inventory control Cash control

1 Meaning Inventory control is the activity

of checking the shop's stock. It

can also be said as the software

which helps in managing the

stock.

Cash control is the mode of

monitoring the credit, cash allocation

and disbursement of various policies.

2 Objective It is used by the company to

manage the stock of the company

in order to utilize the resources to

the full extent.

It is used by the company to manage

the cash and to catch the various

fraudulent activities being performed

in the organization.

TASK 3

3.1 Source and structure of trial balance

Trial balance is the first step of preparing financial statement which summarizes all the

debit and credit balance of ledger accounts. One of the main sources of trial balance is ledger

account which is prepared by the organization for their each and every transaction (Chen, Kim

and Chen, 2007). It is prepared by the organization at the end of the financial year which

provides deeper insight to an organization about their transactions. Therefore, trial balance is

prepared below considering the given data.

Trial balance:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Debit (£) Credit (£)

Bank loan 12000

Cash 11700

Capital 13000

Rates 1880

Trade creditors 11200

Purchases 12400

Sales 14600

Sundry creditor 1620

Debtors 12000

Bank loan interest 1400

Other expenses 11020

Vehicle 2020

Total 52420 52420

3.2 Evaluating business accounts, adjustments and notes

Adjusted Trial balance ABC traders as of 21st August 2015

Particulars Debit (£) Credit (£)

Opening stock 86000

Purchases 1136000

Salaries 110000

Wages 61000

Carriage inwards 26900

Trading charges 64000

6

Bank loan 12000

Cash 11700

Capital 13000

Rates 1880

Trade creditors 11200

Purchases 12400

Sales 14600

Sundry creditor 1620

Debtors 12000

Bank loan interest 1400

Other expenses 11020

Vehicle 2020

Total 52420 52420

3.2 Evaluating business accounts, adjustments and notes

Adjusted Trial balance ABC traders as of 21st August 2015

Particulars Debit (£) Credit (£)

Opening stock 86000

Purchases 1136000

Salaries 110000

Wages 61000

Carriage inwards 26900

Trading charges 64000

6

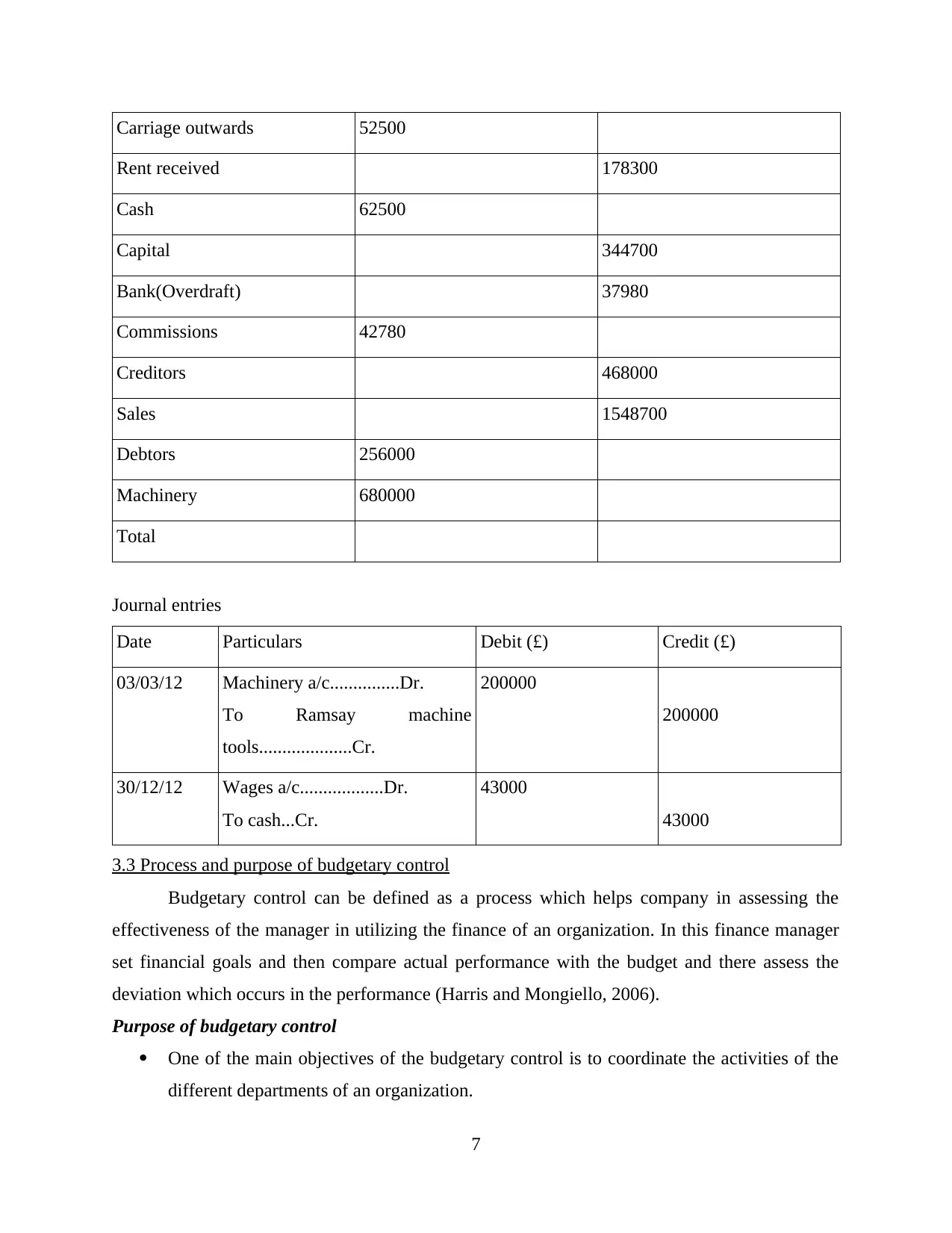

Carriage outwards 52500

Rent received 178300

Cash 62500

Capital 344700

Bank(Overdraft) 37980

Commissions 42780

Creditors 468000

Sales 1548700

Debtors 256000

Machinery 680000

Total

Journal entries

Date Particulars Debit (£) Credit (£)

03/03/12 Machinery a/c...............Dr.

To Ramsay machine

tools....................Cr.

200000

200000

30/12/12 Wages a/c..................Dr.

To cash...Cr.

43000

43000

3.3 Process and purpose of budgetary control

Budgetary control can be defined as a process which helps company in assessing the

effectiveness of the manager in utilizing the finance of an organization. In this finance manager

set financial goals and then compare actual performance with the budget and there assess the

deviation which occurs in the performance (Harris and Mongiello, 2006).

Purpose of budgetary control

One of the main objectives of the budgetary control is to coordinate the activities of the

different departments of an organization.

7

Rent received 178300

Cash 62500

Capital 344700

Bank(Overdraft) 37980

Commissions 42780

Creditors 468000

Sales 1548700

Debtors 256000

Machinery 680000

Total

Journal entries

Date Particulars Debit (£) Credit (£)

03/03/12 Machinery a/c...............Dr.

To Ramsay machine

tools....................Cr.

200000

200000

30/12/12 Wages a/c..................Dr.

To cash...Cr.

43000

43000

3.3 Process and purpose of budgetary control

Budgetary control can be defined as a process which helps company in assessing the

effectiveness of the manager in utilizing the finance of an organization. In this finance manager

set financial goals and then compare actual performance with the budget and there assess the

deviation which occurs in the performance (Harris and Mongiello, 2006).

Purpose of budgetary control

One of the main objectives of the budgetary control is to coordinate the activities of the

different departments of an organization.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further, another objective of budgetary control process is to make control over the

unnecessary expenditures which act as a barrier in the organizational growth and

development. Besides this, regulation of the activities and functions of employees are also the main

objective of budgetary control. Through this, organization is able to build and sustain

competitive advantage.

Process of budgetary control

In the very first step finance manager of an organization forecast the expenses or money

which is required to accomplish the activities. Besides this, they also forecast the income

which they generate over a period of time. Finance manager also compare their budget

with the previous year which helps them in setting appropriate budget.

Once budget have set by the manager then after they needs to take approval from the

higher authority of an organization.

Thereafter, manager of an organization compare actual performance with the budgeted

amount and find out the deviations which occurs in the performance (Hein and Riegel,

2011).

One deviation of the performance have identified then after manager makes effort to

assess the causes due to which deficiencies occurred in the performance.

In the last step of budgetary control manager take corrective measures by taking into

consideration the causes due to which variances occurs in the performance.

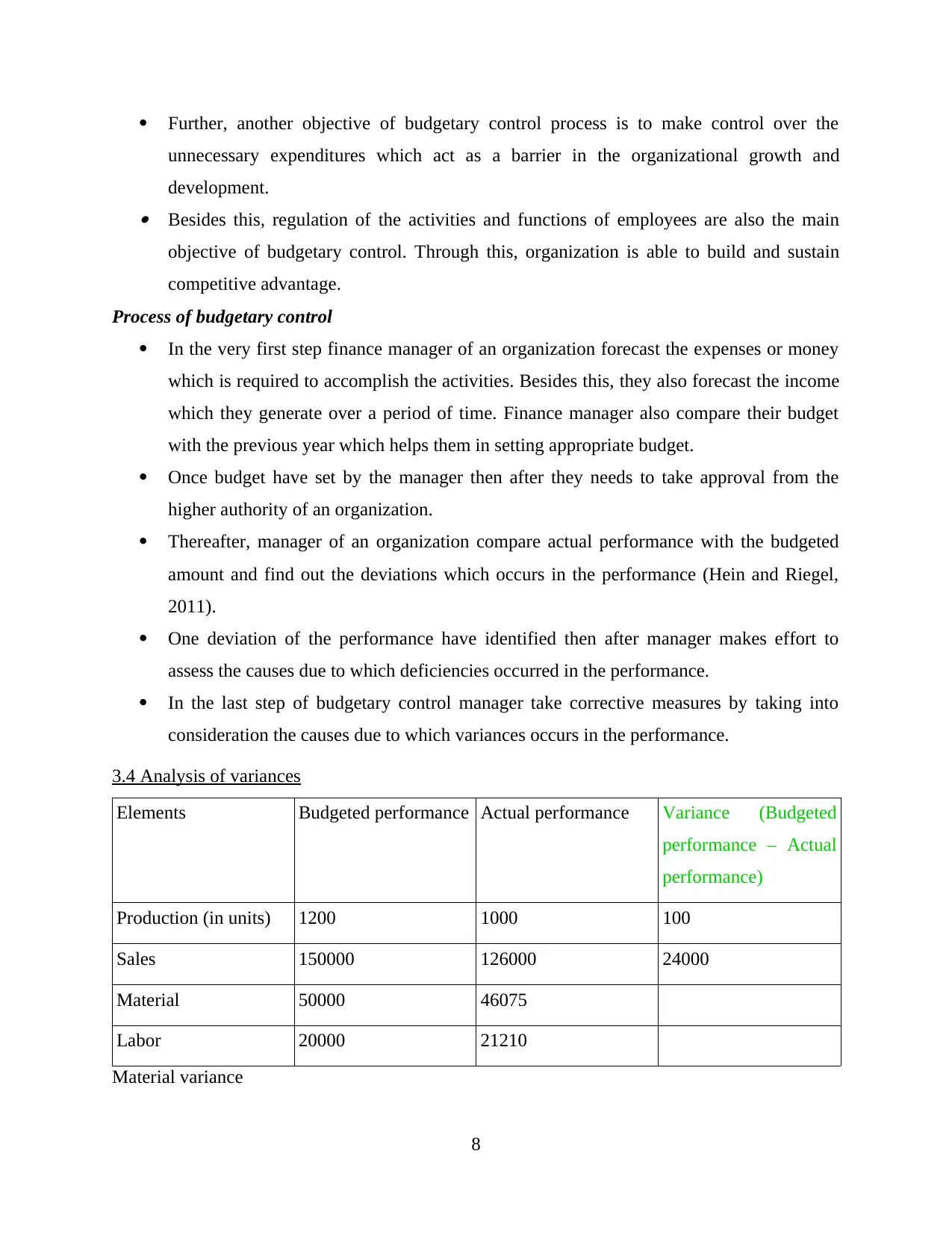

3.4 Analysis of variances

Elements Budgeted performance Actual performance Variance (Budgeted

performance – Actual

performance)

Production (in units) 1200 1000 100

Sales 150000 126000 24000

Material 50000 46075

Labor 20000 21210

Material variance

8

unnecessary expenditures which act as a barrier in the organizational growth and

development. Besides this, regulation of the activities and functions of employees are also the main

objective of budgetary control. Through this, organization is able to build and sustain

competitive advantage.

Process of budgetary control

In the very first step finance manager of an organization forecast the expenses or money

which is required to accomplish the activities. Besides this, they also forecast the income

which they generate over a period of time. Finance manager also compare their budget

with the previous year which helps them in setting appropriate budget.

Once budget have set by the manager then after they needs to take approval from the

higher authority of an organization.

Thereafter, manager of an organization compare actual performance with the budgeted

amount and find out the deviations which occurs in the performance (Hein and Riegel,

2011).

One deviation of the performance have identified then after manager makes effort to

assess the causes due to which deficiencies occurred in the performance.

In the last step of budgetary control manager take corrective measures by taking into

consideration the causes due to which variances occurs in the performance.

3.4 Analysis of variances

Elements Budgeted performance Actual performance Variance (Budgeted

performance – Actual

performance)

Production (in units) 1200 1000 100

Sales 150000 126000 24000

Material 50000 46075

Labor 20000 21210

Material variance

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Elements Budgeted performance Actual performance Variance

Material usage

variance

5000 4850 150

Material price variance 10 9.5 0.5

Material total variance 50000 46075 3925

Labor variances

Elements Budgeted performance Actual performance Variance

Labor efficiency

variance (in hours)

4000 4200 -200

Labor rate variance 5 5.05 -0.05

Direct labor total

variance

20000 21210 -1210

Overhead variances

Elements Budgeted performance Actual performance Variance

Fixed overhead 24000 25000 -1000

Variable overhead 8000 9450 -1450

On the basis of the above figures it has been analyzed that organization has made

optimum utilization of material in order to produce the product or services. On the basis of this it

can be stated that company reduces the wastage and have undertaken effective technique to

control the stock. In contrary to this, company fails to utilize the human resource of an

organization to the full extent. Thus, they need to encourage their workforce to make their best

efforts for the benefit of an organization (Ivankovič, Jerman and Jankovič, 2009). In addition to

this, as compared to budgeted amount actual overhead expenses of an organization is high which

is not fruitful for the organization. Thus, company needs to frame effective policies and

strategies which make contribution in achievement of organizational goals and objectives.

9

Material usage

variance

5000 4850 150

Material price variance 10 9.5 0.5

Material total variance 50000 46075 3925

Labor variances

Elements Budgeted performance Actual performance Variance

Labor efficiency

variance (in hours)

4000 4200 -200

Labor rate variance 5 5.05 -0.05

Direct labor total

variance

20000 21210 -1210

Overhead variances

Elements Budgeted performance Actual performance Variance

Fixed overhead 24000 25000 -1000

Variable overhead 8000 9450 -1450

On the basis of the above figures it has been analyzed that organization has made

optimum utilization of material in order to produce the product or services. On the basis of this it

can be stated that company reduces the wastage and have undertaken effective technique to

control the stock. In contrary to this, company fails to utilize the human resource of an

organization to the full extent. Thus, they need to encourage their workforce to make their best

efforts for the benefit of an organization (Ivankovič, Jerman and Jankovič, 2009). In addition to

this, as compared to budgeted amount actual overhead expenses of an organization is high which

is not fruitful for the organization. Thus, company needs to frame effective policies and

strategies which make contribution in achievement of organizational goals and objectives.

9

TASK 4

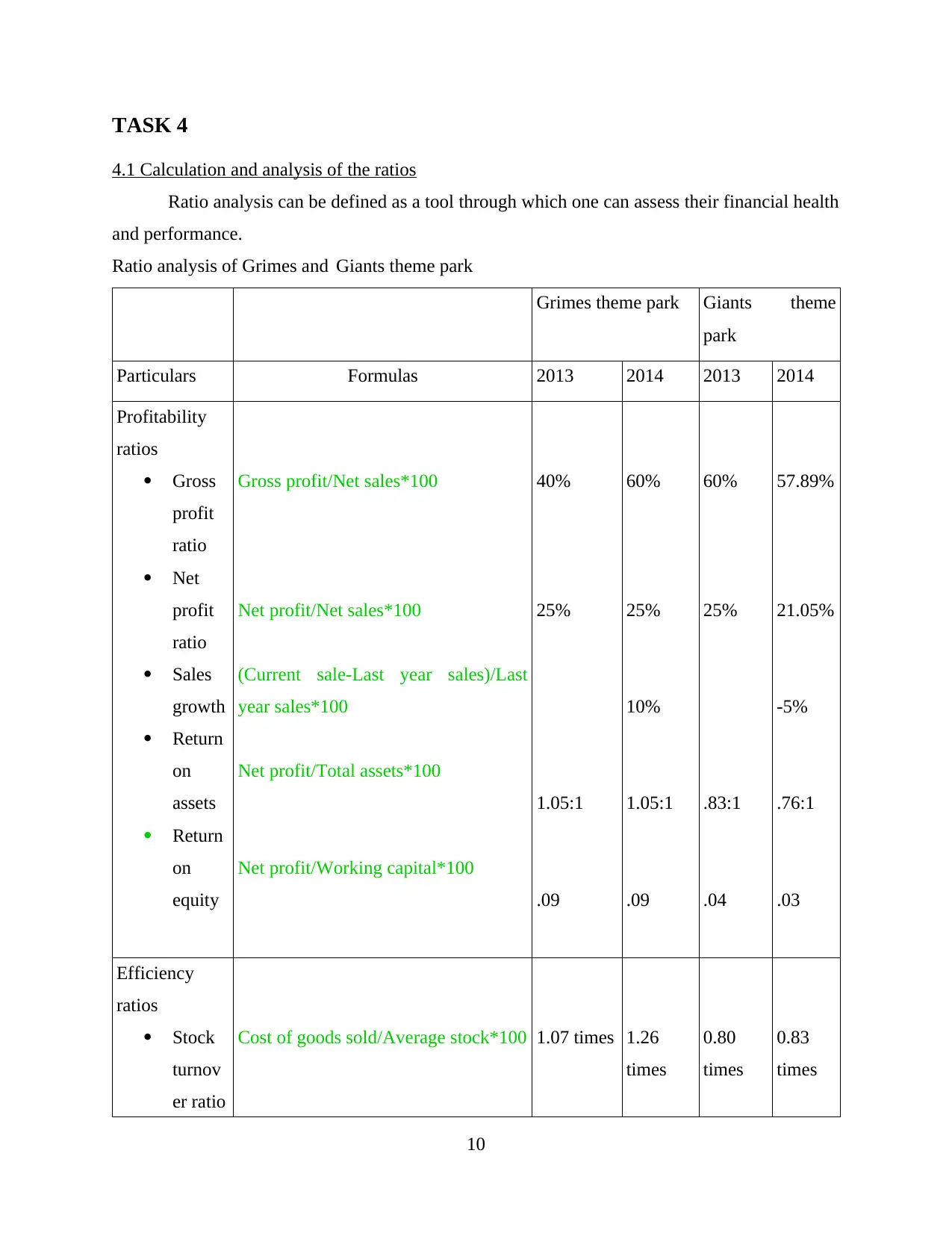

4.1 Calculation and analysis of the ratios

Ratio analysis can be defined as a tool through which one can assess their financial health

and performance.

Ratio analysis of Grimes and Giants theme park

Grimes theme park Giants theme

park

Particulars Formulas 2013 2014 2013 2014

Profitability

ratios

Gross

profit

ratio

Net

profit

ratio

Sales

growth

Return

on

assets

Return

on

equity

Gross profit/Net sales*100

Net profit/Net sales*100

(Current sale-Last year sales)/Last

year sales*100

Net profit/Total assets*100

Net profit/Working capital*100

40%

25%

1.05:1

.09

60%

25%

10%

1.05:1

.09

60%

25%

.83:1

.04

57.89%

21.05%

-5%

.76:1

.03

Efficiency

ratios

Stock

turnov

er ratio

Cost of goods sold/Average stock*100 1.07 times 1.26

times

0.80

times

0.83

times

10

4.1 Calculation and analysis of the ratios

Ratio analysis can be defined as a tool through which one can assess their financial health

and performance.

Ratio analysis of Grimes and Giants theme park

Grimes theme park Giants theme

park

Particulars Formulas 2013 2014 2013 2014

Profitability

ratios

Gross

profit

ratio

Net

profit

ratio

Sales

growth

Return

on

assets

Return

on

equity

Gross profit/Net sales*100

Net profit/Net sales*100

(Current sale-Last year sales)/Last

year sales*100

Net profit/Total assets*100

Net profit/Working capital*100

40%

25%

1.05:1

.09

60%

25%

10%

1.05:1

.09

60%

25%

.83:1

.04

57.89%

21.05%

-5%

.76:1

.03

Efficiency

ratios

Stock

turnov

er ratio

Cost of goods sold/Average stock*100 1.07 times 1.26

times

0.80

times

0.83

times

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.