Finance Assignment: Application of Accounting Standards and Principles

VerifiedAdded on 2021/02/19

|13

|3355

|34

Homework Assignment

AI Summary

This finance assignment addresses several key accounting concepts and principles. Question 1 presents journal entries related to various financial transactions, including losses from cloud service disruptions, asset revaluations, fraudulent activities, and share value declines. Question 2 focuses on share transactions, detailing journal entries for share applications, underwriting commissions, share allotments, and calls, including forfeitures and reissuance. Question 3 delves into current and deferred tax calculations, providing worksheets and journal entries to illustrate the process. The assignment also covers the revaluation model, explaining its application to fixed assets, specifically trucks, with accompanying journal entries to reflect changes in asset values. This assignment provides a detailed exploration of financial accounting practices, offering valuable insights into real-world financial scenarios and the application of accounting standards.

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2 ..................................................................................................................................2

QUESTION 3...................................................................................................................................4

QUESTION 4...................................................................................................................................6

QUESTION 5...................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2 ..................................................................................................................................2

QUESTION 3...................................................................................................................................4

QUESTION 4...................................................................................................................................6

QUESTION 5...................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financing is the major source of funding which help the business to run their operational

activities in order to fulfil their financial needs. There are various financial institutes available

which provide funding such as banks, investors and other non commercial institutes for source of

funding (Finance for organization, 2019). It help the organization to purchase product, further

investments etc. This report is all about generating funds with the help of various activities. It

includes different methods of techniques which help the organization to generate money which is

beneficial for the businessman to smoothly run their business and further invest for for more

profit. This report cover various practice questions which required to solve with the help of

various accounting standards and principles.

MAIN BODY

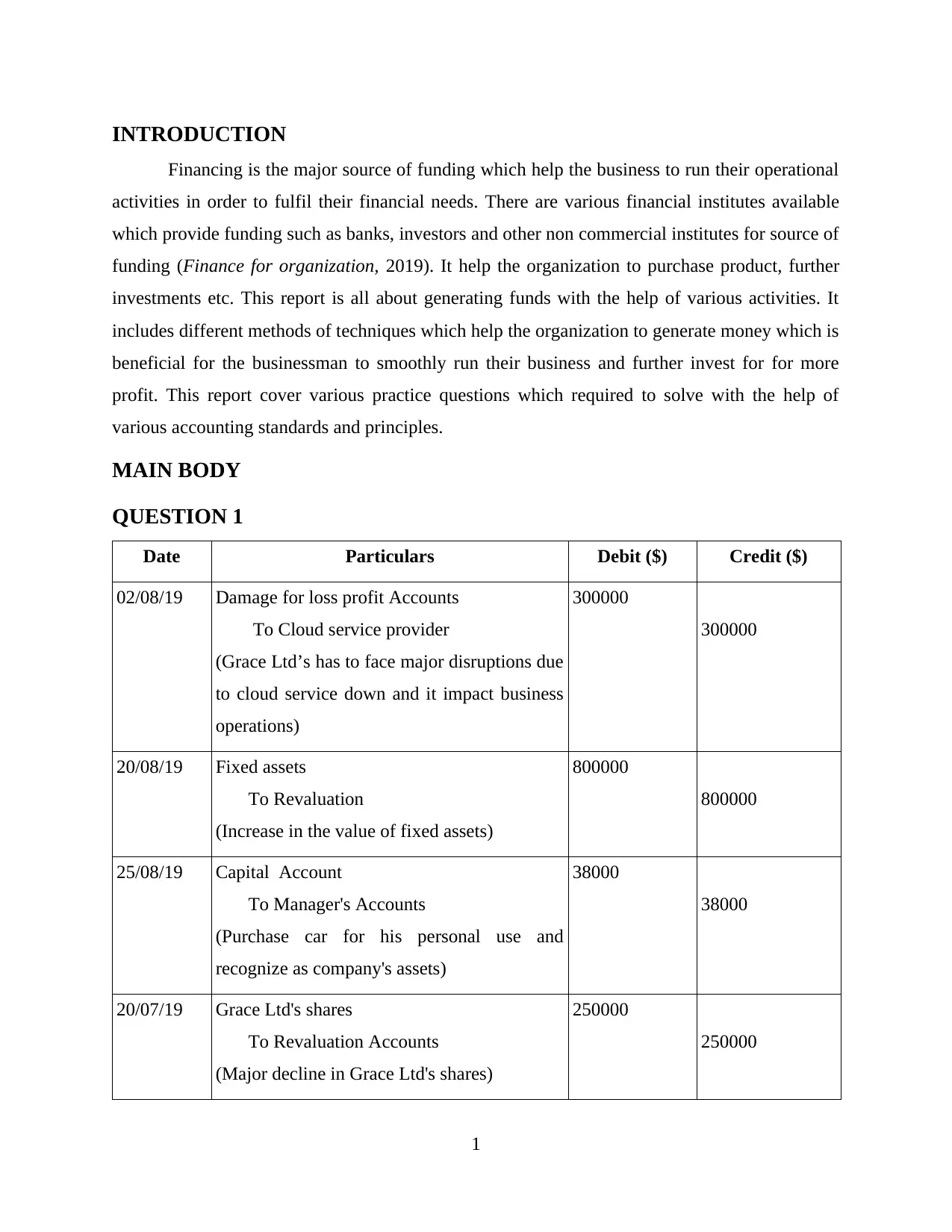

QUESTION 1

Date Particulars Debit ($) Credit ($)

02/08/19 Damage for loss profit Accounts

To Cloud service provider

(Grace Ltd’s has to face major disruptions due

to cloud service down and it impact business

operations)

300000

300000

20/08/19 Fixed assets

To Revaluation

(Increase in the value of fixed assets)

800000

800000

25/08/19 Capital Account

To Manager's Accounts

(Purchase car for his personal use and

recognize as company's assets)

38000

38000

20/07/19 Grace Ltd's shares

To Revaluation Accounts

(Major decline in Grace Ltd's shares)

250000

250000

1

Financing is the major source of funding which help the business to run their operational

activities in order to fulfil their financial needs. There are various financial institutes available

which provide funding such as banks, investors and other non commercial institutes for source of

funding (Finance for organization, 2019). It help the organization to purchase product, further

investments etc. This report is all about generating funds with the help of various activities. It

includes different methods of techniques which help the organization to generate money which is

beneficial for the businessman to smoothly run their business and further invest for for more

profit. This report cover various practice questions which required to solve with the help of

various accounting standards and principles.

MAIN BODY

QUESTION 1

Date Particulars Debit ($) Credit ($)

02/08/19 Damage for loss profit Accounts

To Cloud service provider

(Grace Ltd’s has to face major disruptions due

to cloud service down and it impact business

operations)

300000

300000

20/08/19 Fixed assets

To Revaluation

(Increase in the value of fixed assets)

800000

800000

25/08/19 Capital Account

To Manager's Accounts

(Purchase car for his personal use and

recognize as company's assets)

38000

38000

20/07/19 Grace Ltd's shares

To Revaluation Accounts

(Major decline in Grace Ltd's shares)

250000

250000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total 1388000 1388000

a. Company bear the loss because of cloud service provider and its services down for the 14 days

in the month of July 2019. It majorly impact the business operation of Grace Ltd and they take

legal action against cloud service provider. Company seeking $ 300000 for lost profit due to

damage. Here company follow their legal rights where business can claim for their damages to

the another party.

b. Grace Ltd was planing to subdivide the area into residential block or airport for landing or

take off (Darrough, Guler and Wang, 2014). Company revise the and value on 20 August 2019

but after government announcement land was valued at $ 800000. it will be less than the amount

which listed in financial statement on 30th June, 2019.

c. On 25th August 2019, At the time of auditing company find the fraudulent activity where

manager use $ 38000 amount from company's fund. It will be used for personal purpose and this

car recognise as business assets in the financial statement of the company. Director of the

company met with manager and said to repay $ 38000 amount by 30th September 2019.

d. Grace Ltd owns shares of public listed company which had a market value of $ 500,000 on 30

June 2019 and will decline $ 250,000 on 20 July 2019. It will be recorded in the financial

statement of the company.

QUESTION 2

Date Particulars Debit ($) Credit ($)

01/02/19 Bank account

(200000 * 3)

To Share application account

(200000 * 3)

(Being share application amount received)

600000

600000

01/02/19 Cost of issue account

To Commission account

(Being underwritten commission of $ 12000 )

12000

12000

2

a. Company bear the loss because of cloud service provider and its services down for the 14 days

in the month of July 2019. It majorly impact the business operation of Grace Ltd and they take

legal action against cloud service provider. Company seeking $ 300000 for lost profit due to

damage. Here company follow their legal rights where business can claim for their damages to

the another party.

b. Grace Ltd was planing to subdivide the area into residential block or airport for landing or

take off (Darrough, Guler and Wang, 2014). Company revise the and value on 20 August 2019

but after government announcement land was valued at $ 800000. it will be less than the amount

which listed in financial statement on 30th June, 2019.

c. On 25th August 2019, At the time of auditing company find the fraudulent activity where

manager use $ 38000 amount from company's fund. It will be used for personal purpose and this

car recognise as business assets in the financial statement of the company. Director of the

company met with manager and said to repay $ 38000 amount by 30th September 2019.

d. Grace Ltd owns shares of public listed company which had a market value of $ 500,000 on 30

June 2019 and will decline $ 250,000 on 20 July 2019. It will be recorded in the financial

statement of the company.

QUESTION 2

Date Particulars Debit ($) Credit ($)

01/02/19 Bank account

(200000 * 3)

To Share application account

(200000 * 3)

(Being share application amount received)

600000

600000

01/02/19 Cost of issue account

To Commission account

(Being underwritten commission of $ 12000 )

12000

12000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

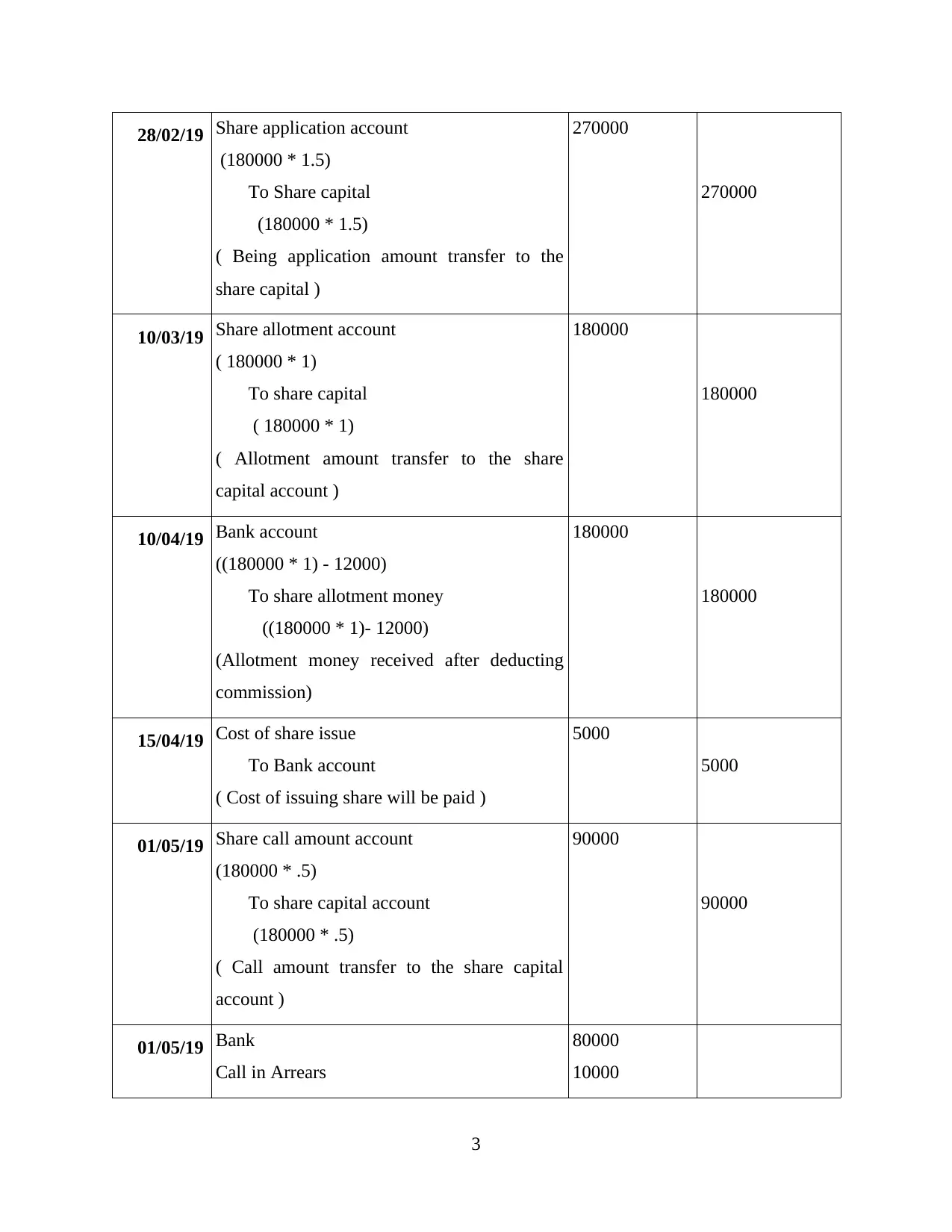

28/02/19 Share application account

(180000 * 1.5)

To Share capital

(180000 * 1.5)

( Being application amount transfer to the

share capital )

270000

270000

10/03/19 Share allotment account

( 180000 * 1)

To share capital

( 180000 * 1)

( Allotment amount transfer to the share

capital account )

180000

180000

10/04/19 Bank account

((180000 * 1) - 12000)

To share allotment money

((180000 * 1)- 12000)

(Allotment money received after deducting

commission)

180000

180000

15/04/19 Cost of share issue

To Bank account

( Cost of issuing share will be paid )

5000

5000

01/05/19 Share call amount account

(180000 * .5)

To share capital account

(180000 * .5)

( Call amount transfer to the share capital

account )

90000

90000

01/05/19 Bank

Call in Arrears

80000

10000

3

(180000 * 1.5)

To Share capital

(180000 * 1.5)

( Being application amount transfer to the

share capital )

270000

270000

10/03/19 Share allotment account

( 180000 * 1)

To share capital

( 180000 * 1)

( Allotment amount transfer to the share

capital account )

180000

180000

10/04/19 Bank account

((180000 * 1) - 12000)

To share allotment money

((180000 * 1)- 12000)

(Allotment money received after deducting

commission)

180000

180000

15/04/19 Cost of share issue

To Bank account

( Cost of issuing share will be paid )

5000

5000

01/05/19 Share call amount account

(180000 * .5)

To share capital account

(180000 * .5)

( Call amount transfer to the share capital

account )

90000

90000

01/05/19 Bank

Call in Arrears

80000

10000

3

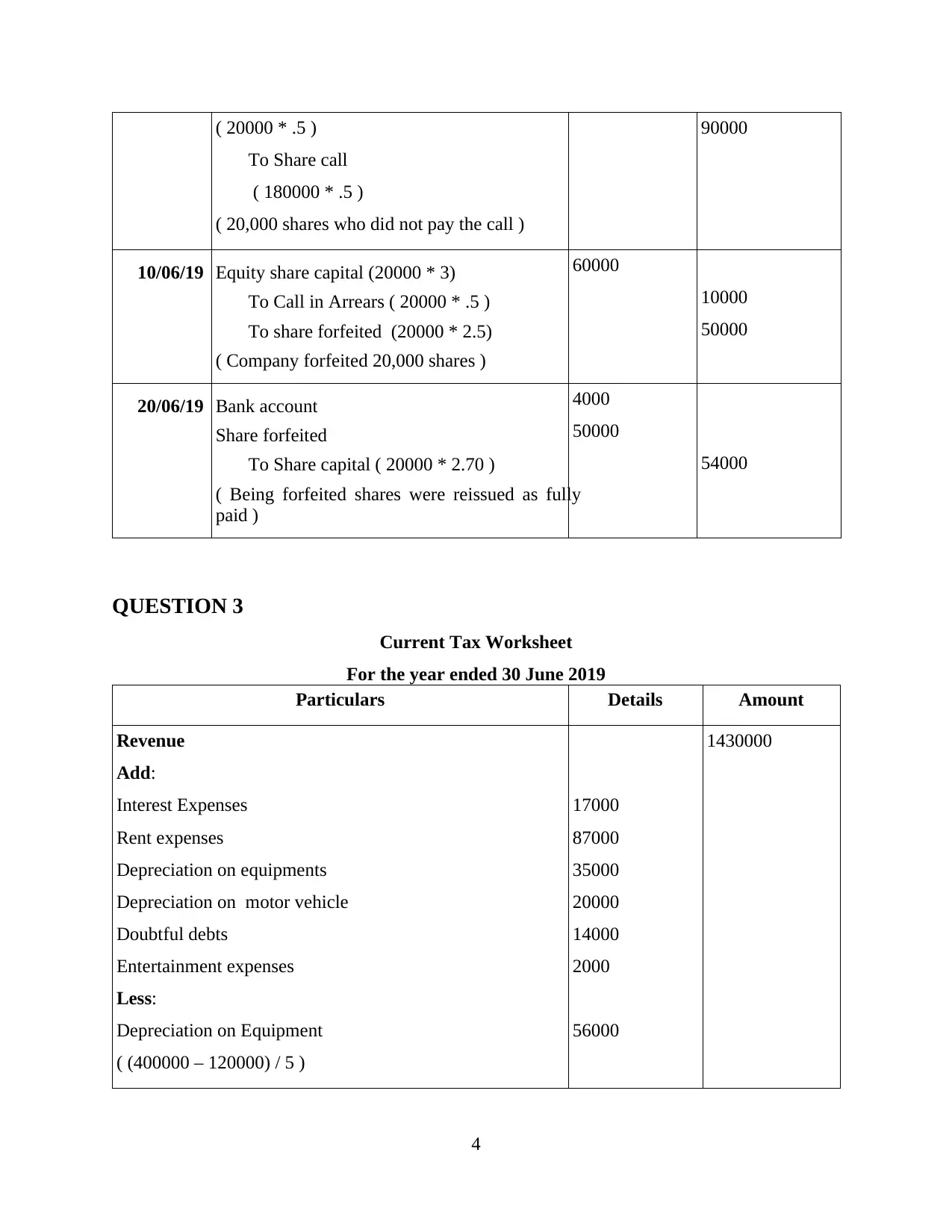

( 20000 * .5 )

To Share call

( 180000 * .5 )

( 20,000 shares who did not pay the call )

90000

10/06/19 Equity share capital (20000 * 3)

To Call in Arrears ( 20000 * .5 )

To share forfeited (20000 * 2.5)

( Company forfeited 20,000 shares )

60000

10000

50000

20/06/19 Bank account

Share forfeited

To Share capital ( 20000 * 2.70 )

( Being forfeited shares were reissued as fully

paid )

4000

50000

54000

QUESTION 3

Current Tax Worksheet

For the year ended 30 June 2019

Particulars Details Amount

Revenue

Add:

Interest Expenses

Rent expenses

Depreciation on equipments

Depreciation on motor vehicle

Doubtful debts

Entertainment expenses

Less:

Depreciation on Equipment

( (400000 – 120000) / 5 )

17000

87000

35000

20000

14000

2000

56000

1430000

4

To Share call

( 180000 * .5 )

( 20,000 shares who did not pay the call )

90000

10/06/19 Equity share capital (20000 * 3)

To Call in Arrears ( 20000 * .5 )

To share forfeited (20000 * 2.5)

( Company forfeited 20,000 shares )

60000

10000

50000

20/06/19 Bank account

Share forfeited

To Share capital ( 20000 * 2.70 )

( Being forfeited shares were reissued as fully

paid )

4000

50000

54000

QUESTION 3

Current Tax Worksheet

For the year ended 30 June 2019

Particulars Details Amount

Revenue

Add:

Interest Expenses

Rent expenses

Depreciation on equipments

Depreciation on motor vehicle

Doubtful debts

Entertainment expenses

Less:

Depreciation on Equipment

( (400000 – 120000) / 5 )

17000

87000

35000

20000

14000

2000

56000

1430000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

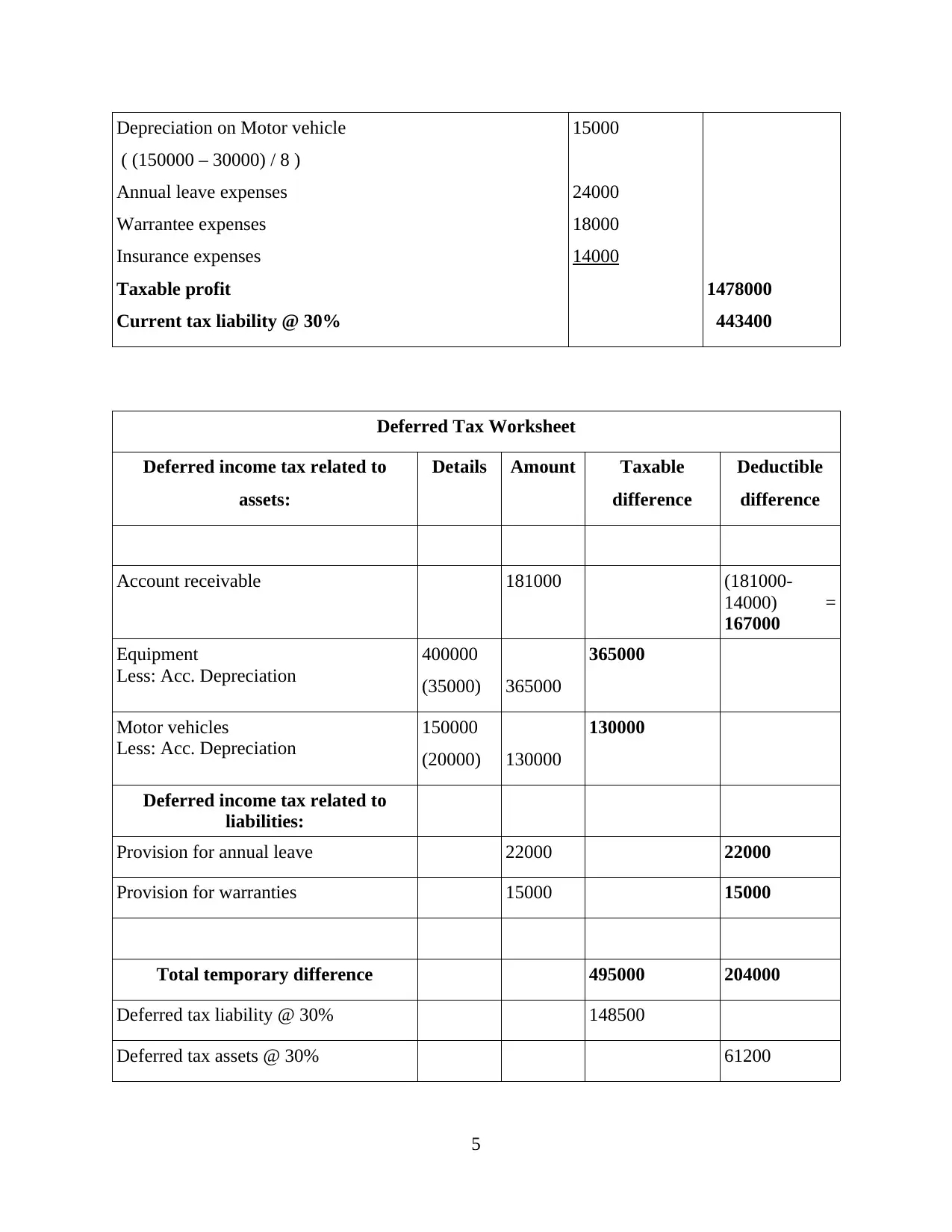

Depreciation on Motor vehicle

( (150000 – 30000) / 8 )

Annual leave expenses

Warrantee expenses

Insurance expenses

Taxable profit

Current tax liability @ 30%

15000

24000

18000

14000

1478000

443400

Deferred Tax Worksheet

Deferred income tax related to

assets:

Details Amount Taxable

difference

Deductible

difference

Account receivable 181000 (181000-

14000) =

167000

Equipment

Less: Acc. Depreciation

400000

(35000) 365000

365000

Motor vehicles

Less: Acc. Depreciation

150000

(20000) 130000

130000

Deferred income tax related to

liabilities:

Provision for annual leave 22000 22000

Provision for warranties 15000 15000

Total temporary difference 495000 204000

Deferred tax liability @ 30% 148500

Deferred tax assets @ 30% 61200

5

( (150000 – 30000) / 8 )

Annual leave expenses

Warrantee expenses

Insurance expenses

Taxable profit

Current tax liability @ 30%

15000

24000

18000

14000

1478000

443400

Deferred Tax Worksheet

Deferred income tax related to

assets:

Details Amount Taxable

difference

Deductible

difference

Account receivable 181000 (181000-

14000) =

167000

Equipment

Less: Acc. Depreciation

400000

(35000) 365000

365000

Motor vehicles

Less: Acc. Depreciation

150000

(20000) 130000

130000

Deferred income tax related to

liabilities:

Provision for annual leave 22000 22000

Provision for warranties 15000 15000

Total temporary difference 495000 204000

Deferred tax liability @ 30% 148500

Deferred tax assets @ 30% 61200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

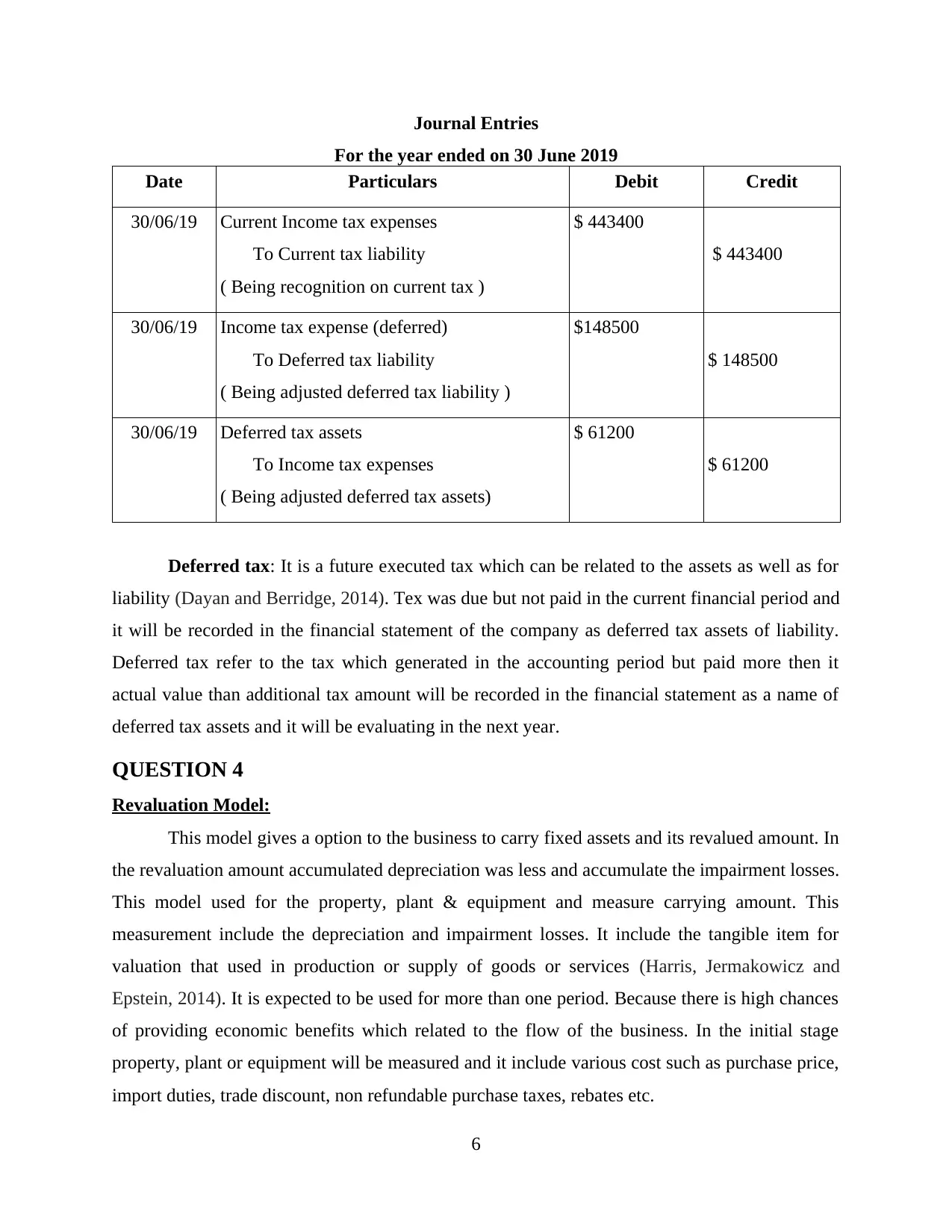

Journal Entries

For the year ended on 30 June 2019

Date Particulars Debit Credit

30/06/19 Current Income tax expenses

To Current tax liability

( Being recognition on current tax )

$ 443400

$ 443400

30/06/19 Income tax expense (deferred)

To Deferred tax liability

( Being adjusted deferred tax liability )

$148500

$ 148500

30/06/19 Deferred tax assets

To Income tax expenses

( Being adjusted deferred tax assets)

$ 61200

$ 61200

Deferred tax: It is a future executed tax which can be related to the assets as well as for

liability (Dayan and Berridge, 2014). Tex was due but not paid in the current financial period and

it will be recorded in the financial statement of the company as deferred tax assets of liability.

Deferred tax refer to the tax which generated in the accounting period but paid more then it

actual value than additional tax amount will be recorded in the financial statement as a name of

deferred tax assets and it will be evaluating in the next year.

QUESTION 4

Revaluation Model:

This model gives a option to the business to carry fixed assets and its revalued amount. In

the revaluation amount accumulated depreciation was less and accumulate the impairment losses.

This model used for the property, plant & equipment and measure carrying amount. This

measurement include the depreciation and impairment losses. It include the tangible item for

valuation that used in production or supply of goods or services (Harris, Jermakowicz and

Epstein, 2014). It is expected to be used for more than one period. Because there is high chances

of providing economic benefits which related to the flow of the business. In the initial stage

property, plant or equipment will be measured and it include various cost such as purchase price,

import duties, trade discount, non refundable purchase taxes, rebates etc.

6

For the year ended on 30 June 2019

Date Particulars Debit Credit

30/06/19 Current Income tax expenses

To Current tax liability

( Being recognition on current tax )

$ 443400

$ 443400

30/06/19 Income tax expense (deferred)

To Deferred tax liability

( Being adjusted deferred tax liability )

$148500

$ 148500

30/06/19 Deferred tax assets

To Income tax expenses

( Being adjusted deferred tax assets)

$ 61200

$ 61200

Deferred tax: It is a future executed tax which can be related to the assets as well as for

liability (Dayan and Berridge, 2014). Tex was due but not paid in the current financial period and

it will be recorded in the financial statement of the company as deferred tax assets of liability.

Deferred tax refer to the tax which generated in the accounting period but paid more then it

actual value than additional tax amount will be recorded in the financial statement as a name of

deferred tax assets and it will be evaluating in the next year.

QUESTION 4

Revaluation Model:

This model gives a option to the business to carry fixed assets and its revalued amount. In

the revaluation amount accumulated depreciation was less and accumulate the impairment losses.

This model used for the property, plant & equipment and measure carrying amount. This

measurement include the depreciation and impairment losses. It include the tangible item for

valuation that used in production or supply of goods or services (Harris, Jermakowicz and

Epstein, 2014). It is expected to be used for more than one period. Because there is high chances

of providing economic benefits which related to the flow of the business. In the initial stage

property, plant or equipment will be measured and it include various cost such as purchase price,

import duties, trade discount, non refundable purchase taxes, rebates etc.

6

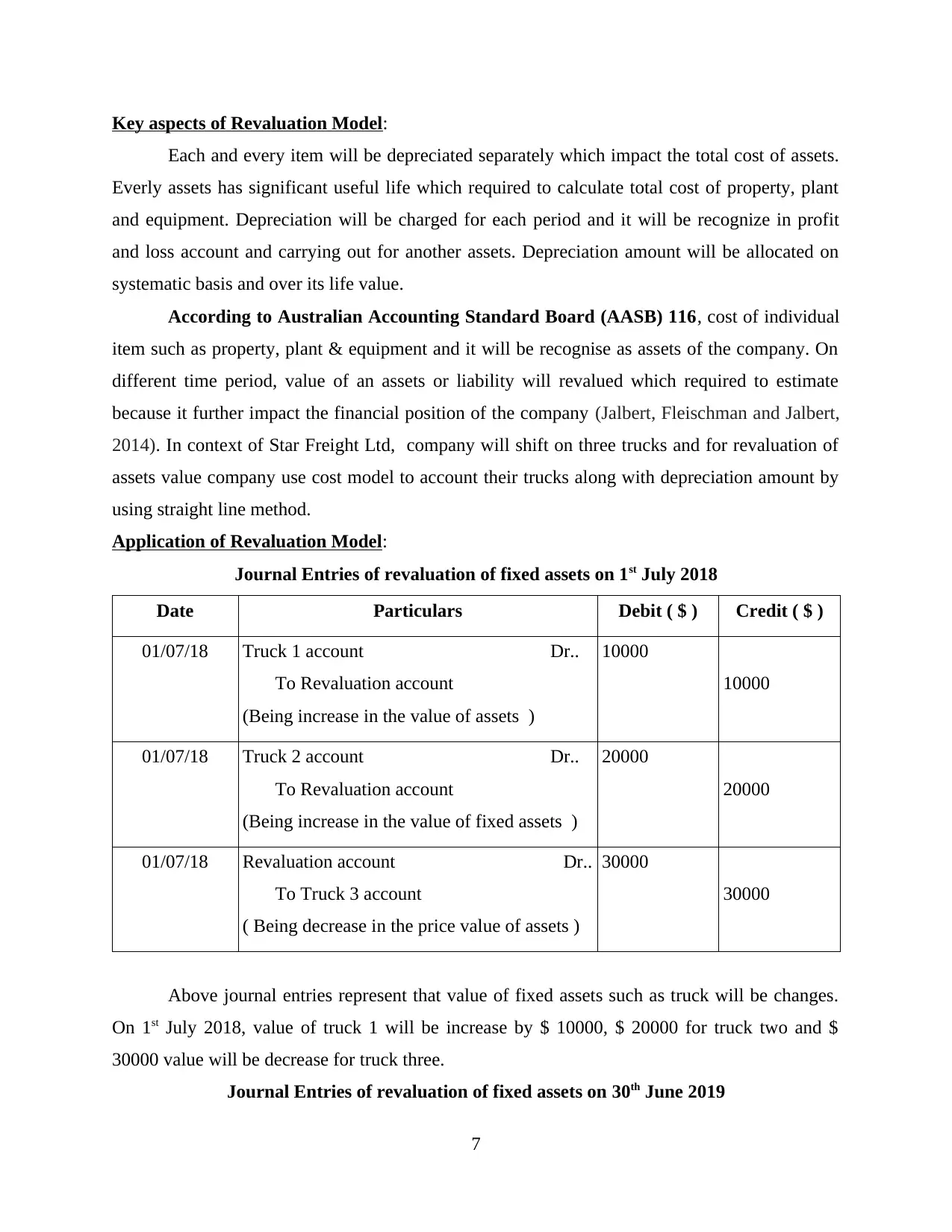

Key aspects of Revaluation Model:

Each and every item will be depreciated separately which impact the total cost of assets.

Everly assets has significant useful life which required to calculate total cost of property, plant

and equipment. Depreciation will be charged for each period and it will be recognize in profit

and loss account and carrying out for another assets. Depreciation amount will be allocated on

systematic basis and over its life value.

According to Australian Accounting Standard Board (AASB) 116, cost of individual

item such as property, plant & equipment and it will be recognise as assets of the company. On

different time period, value of an assets or liability will revalued which required to estimate

because it further impact the financial position of the company (Jalbert, Fleischman and Jalbert,

2014). In context of Star Freight Ltd, company will shift on three trucks and for revaluation of

assets value company use cost model to account their trucks along with depreciation amount by

using straight line method.

Application of Revaluation Model:

Journal Entries of revaluation of fixed assets on 1st July 2018

Date Particulars Debit ( $ ) Credit ( $ )

01/07/18 Truck 1 account Dr..

To Revaluation account

(Being increase in the value of assets )

10000

10000

01/07/18 Truck 2 account Dr..

To Revaluation account

(Being increase in the value of fixed assets )

20000

20000

01/07/18 Revaluation account Dr..

To Truck 3 account

( Being decrease in the price value of assets )

30000

30000

Above journal entries represent that value of fixed assets such as truck will be changes.

On 1st July 2018, value of truck 1 will be increase by $ 10000, $ 20000 for truck two and $

30000 value will be decrease for truck three.

Journal Entries of revaluation of fixed assets on 30th June 2019

7

Each and every item will be depreciated separately which impact the total cost of assets.

Everly assets has significant useful life which required to calculate total cost of property, plant

and equipment. Depreciation will be charged for each period and it will be recognize in profit

and loss account and carrying out for another assets. Depreciation amount will be allocated on

systematic basis and over its life value.

According to Australian Accounting Standard Board (AASB) 116, cost of individual

item such as property, plant & equipment and it will be recognise as assets of the company. On

different time period, value of an assets or liability will revalued which required to estimate

because it further impact the financial position of the company (Jalbert, Fleischman and Jalbert,

2014). In context of Star Freight Ltd, company will shift on three trucks and for revaluation of

assets value company use cost model to account their trucks along with depreciation amount by

using straight line method.

Application of Revaluation Model:

Journal Entries of revaluation of fixed assets on 1st July 2018

Date Particulars Debit ( $ ) Credit ( $ )

01/07/18 Truck 1 account Dr..

To Revaluation account

(Being increase in the value of assets )

10000

10000

01/07/18 Truck 2 account Dr..

To Revaluation account

(Being increase in the value of fixed assets )

20000

20000

01/07/18 Revaluation account Dr..

To Truck 3 account

( Being decrease in the price value of assets )

30000

30000

Above journal entries represent that value of fixed assets such as truck will be changes.

On 1st July 2018, value of truck 1 will be increase by $ 10000, $ 20000 for truck two and $

30000 value will be decrease for truck three.

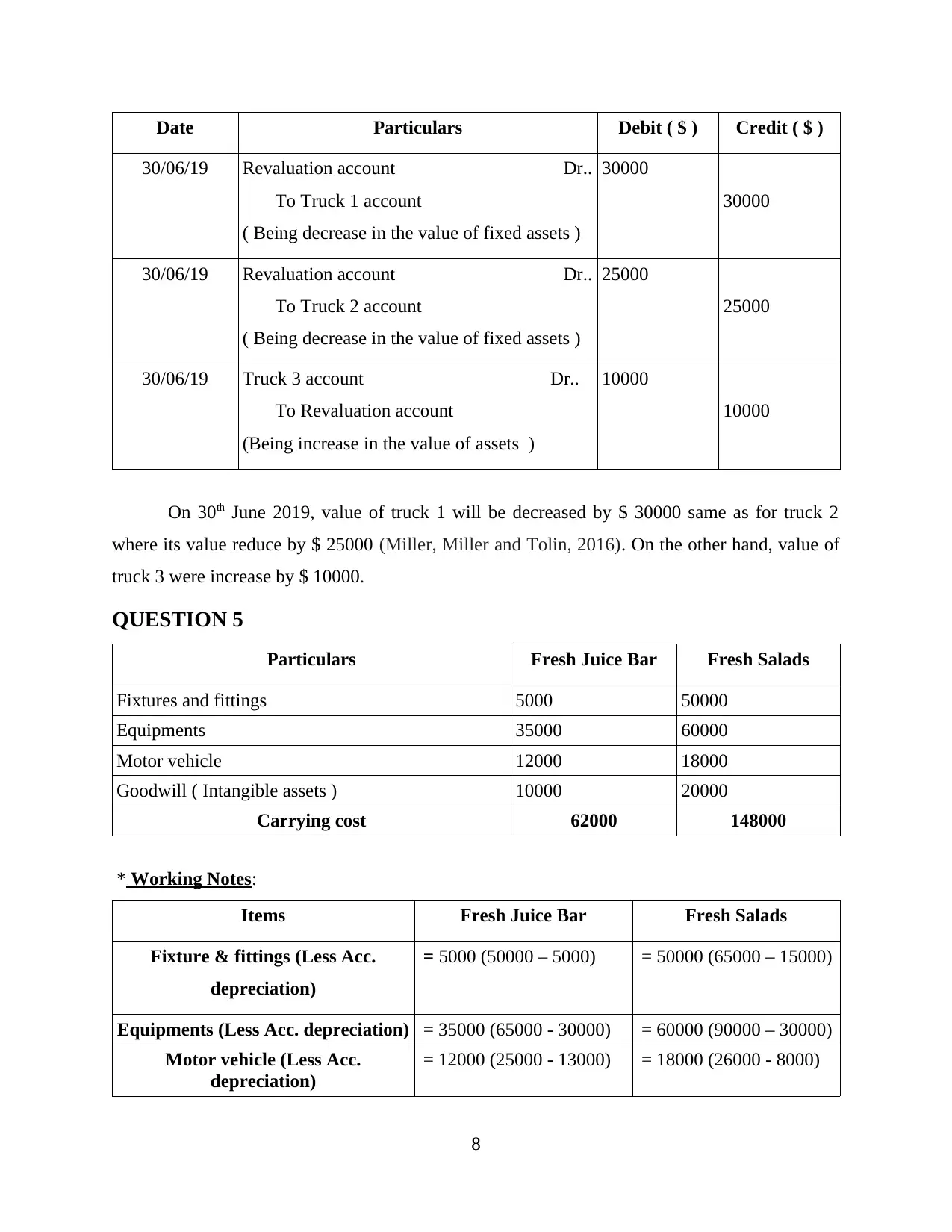

Journal Entries of revaluation of fixed assets on 30th June 2019

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Date Particulars Debit ( $ ) Credit ( $ )

30/06/19 Revaluation account Dr..

To Truck 1 account

( Being decrease in the value of fixed assets )

30000

30000

30/06/19 Revaluation account Dr..

To Truck 2 account

( Being decrease in the value of fixed assets )

25000

25000

30/06/19 Truck 3 account Dr..

To Revaluation account

(Being increase in the value of assets )

10000

10000

On 30th June 2019, value of truck 1 will be decreased by $ 30000 same as for truck 2

where its value reduce by $ 25000 (Miller, Miller and Tolin, 2016). On the other hand, value of

truck 3 were increase by $ 10000.

QUESTION 5

Particulars Fresh Juice Bar Fresh Salads

Fixtures and fittings 5000 50000

Equipments 35000 60000

Motor vehicle 12000 18000

Goodwill ( Intangible assets ) 10000 20000

Carrying cost 62000 148000

* Working Notes:

Items Fresh Juice Bar Fresh Salads

Fixture & fittings (Less Acc.

depreciation)

= 5000 (50000 – 5000) = 50000 (65000 – 15000)

Equipments (Less Acc. depreciation) = 35000 (65000 - 30000) = 60000 (90000 – 30000)

Motor vehicle (Less Acc.

depreciation)

= 12000 (25000 - 13000) = 18000 (26000 - 8000)

8

30/06/19 Revaluation account Dr..

To Truck 1 account

( Being decrease in the value of fixed assets )

30000

30000

30/06/19 Revaluation account Dr..

To Truck 2 account

( Being decrease in the value of fixed assets )

25000

25000

30/06/19 Truck 3 account Dr..

To Revaluation account

(Being increase in the value of assets )

10000

10000

On 30th June 2019, value of truck 1 will be decreased by $ 30000 same as for truck 2

where its value reduce by $ 25000 (Miller, Miller and Tolin, 2016). On the other hand, value of

truck 3 were increase by $ 10000.

QUESTION 5

Particulars Fresh Juice Bar Fresh Salads

Fixtures and fittings 5000 50000

Equipments 35000 60000

Motor vehicle 12000 18000

Goodwill ( Intangible assets ) 10000 20000

Carrying cost 62000 148000

* Working Notes:

Items Fresh Juice Bar Fresh Salads

Fixture & fittings (Less Acc.

depreciation)

= 5000 (50000 – 5000) = 50000 (65000 – 15000)

Equipments (Less Acc. depreciation) = 35000 (65000 - 30000) = 60000 (90000 – 30000)

Motor vehicle (Less Acc.

depreciation)

= 12000 (25000 - 13000) = 18000 (26000 - 8000)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

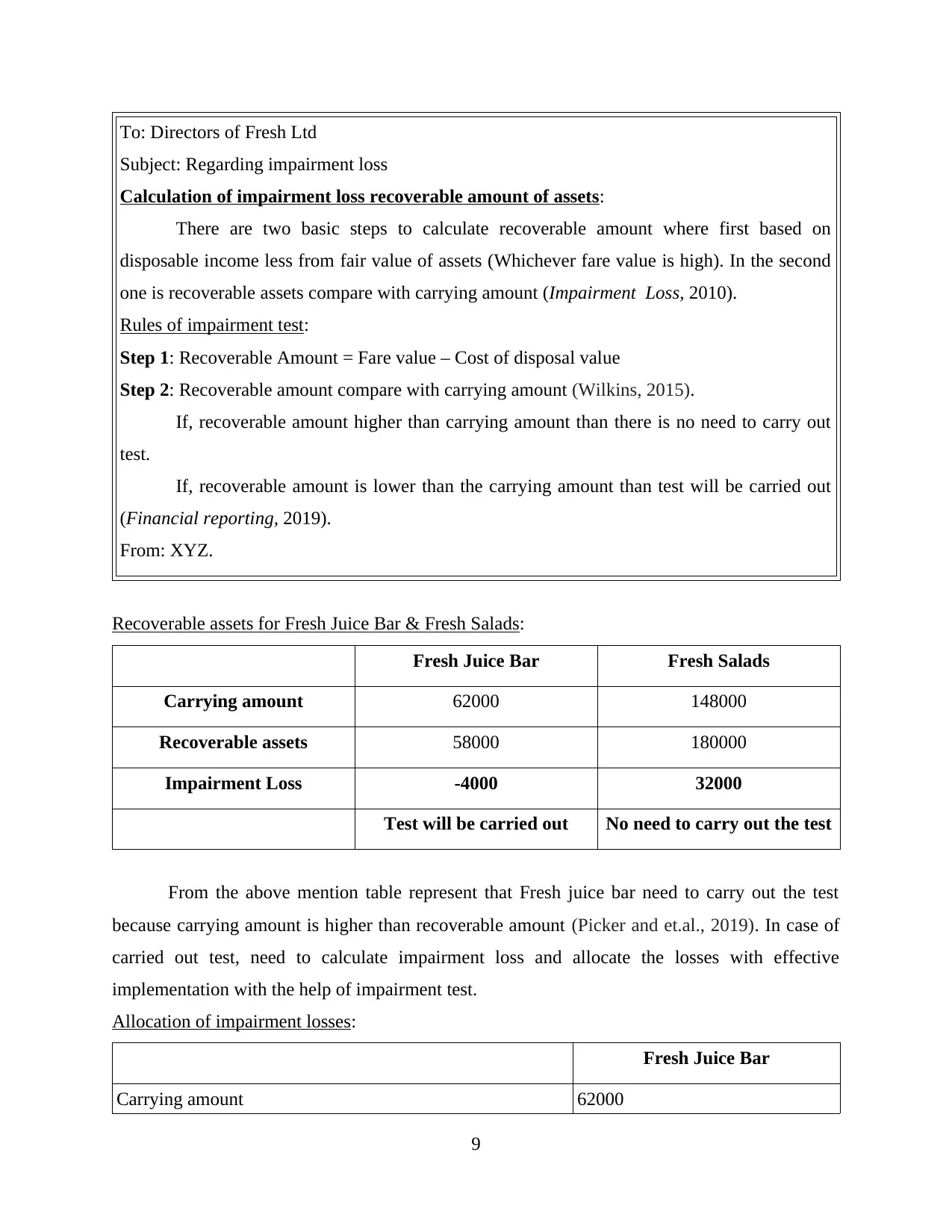

To: Directors of Fresh Ltd

Subject: Regarding impairment loss

Calculation of impairment loss recoverable amount of assets:

There are two basic steps to calculate recoverable amount where first based on

disposable income less from fair value of assets (Whichever fare value is high). In the second

one is recoverable assets compare with carrying amount (Impairment Loss, 2010).

Rules of impairment test:

Step 1: Recoverable Amount = Fare value – Cost of disposal value

Step 2: Recoverable amount compare with carrying amount (Wilkins, 2015).

If, recoverable amount higher than carrying amount than there is no need to carry out

test.

If, recoverable amount is lower than the carrying amount than test will be carried out

(Financial reporting, 2019).

From: XYZ.

Recoverable assets for Fresh Juice Bar & Fresh Salads:

Fresh Juice Bar Fresh Salads

Carrying amount 62000 148000

Recoverable assets 58000 180000

Impairment Loss -4000 32000

Test will be carried out No need to carry out the test

From the above mention table represent that Fresh juice bar need to carry out the test

because carrying amount is higher than recoverable amount (Picker and et.al., 2019). In case of

carried out test, need to calculate impairment loss and allocate the losses with effective

implementation with the help of impairment test.

Allocation of impairment losses:

Fresh Juice Bar

Carrying amount 62000

9

Subject: Regarding impairment loss

Calculation of impairment loss recoverable amount of assets:

There are two basic steps to calculate recoverable amount where first based on

disposable income less from fair value of assets (Whichever fare value is high). In the second

one is recoverable assets compare with carrying amount (Impairment Loss, 2010).

Rules of impairment test:

Step 1: Recoverable Amount = Fare value – Cost of disposal value

Step 2: Recoverable amount compare with carrying amount (Wilkins, 2015).

If, recoverable amount higher than carrying amount than there is no need to carry out

test.

If, recoverable amount is lower than the carrying amount than test will be carried out

(Financial reporting, 2019).

From: XYZ.

Recoverable assets for Fresh Juice Bar & Fresh Salads:

Fresh Juice Bar Fresh Salads

Carrying amount 62000 148000

Recoverable assets 58000 180000

Impairment Loss -4000 32000

Test will be carried out No need to carry out the test

From the above mention table represent that Fresh juice bar need to carry out the test

because carrying amount is higher than recoverable amount (Picker and et.al., 2019). In case of

carried out test, need to calculate impairment loss and allocate the losses with effective

implementation with the help of impairment test.

Allocation of impairment losses:

Fresh Juice Bar

Carrying amount 62000

9

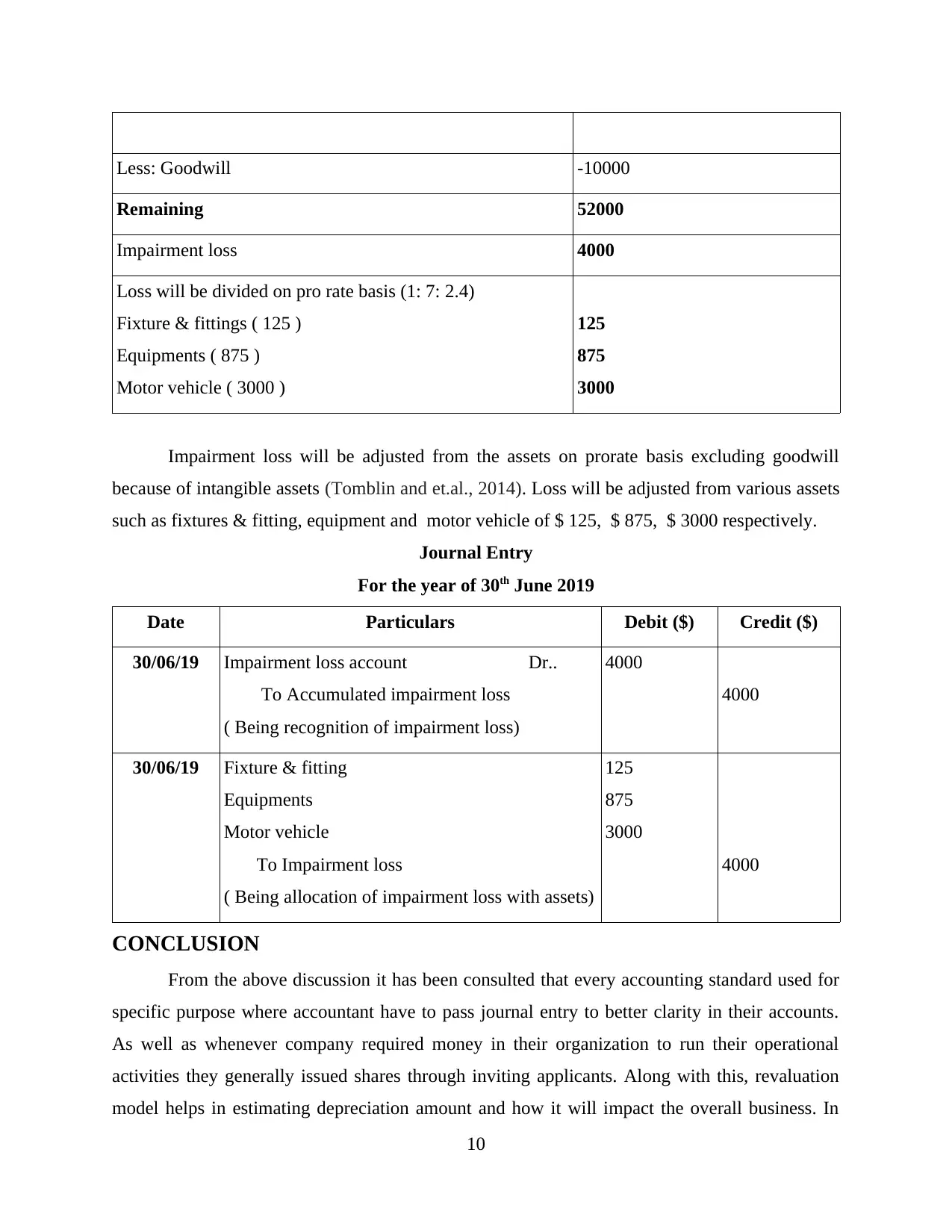

Less: Goodwill -10000

Remaining 52000

Impairment loss 4000

Loss will be divided on pro rate basis (1: 7: 2.4)

Fixture & fittings ( 125 )

Equipments ( 875 )

Motor vehicle ( 3000 )

125

875

3000

Impairment loss will be adjusted from the assets on prorate basis excluding goodwill

because of intangible assets (Tomblin and et.al., 2014). Loss will be adjusted from various assets

such as fixtures & fitting, equipment and motor vehicle of $ 125, $ 875, $ 3000 respectively.

Journal Entry

For the year of 30th June 2019

Date Particulars Debit ($) Credit ($)

30/06/19 Impairment loss account Dr..

To Accumulated impairment loss

( Being recognition of impairment loss)

4000

4000

30/06/19 Fixture & fitting

Equipments

Motor vehicle

To Impairment loss

( Being allocation of impairment loss with assets)

125

875

3000

4000

CONCLUSION

From the above discussion it has been consulted that every accounting standard used for

specific purpose where accountant have to pass journal entry to better clarity in their accounts.

As well as whenever company required money in their organization to run their operational

activities they generally issued shares through inviting applicants. Along with this, revaluation

model helps in estimating depreciation amount and how it will impact the overall business. In

10

Remaining 52000

Impairment loss 4000

Loss will be divided on pro rate basis (1: 7: 2.4)

Fixture & fittings ( 125 )

Equipments ( 875 )

Motor vehicle ( 3000 )

125

875

3000

Impairment loss will be adjusted from the assets on prorate basis excluding goodwill

because of intangible assets (Tomblin and et.al., 2014). Loss will be adjusted from various assets

such as fixtures & fitting, equipment and motor vehicle of $ 125, $ 875, $ 3000 respectively.

Journal Entry

For the year of 30th June 2019

Date Particulars Debit ($) Credit ($)

30/06/19 Impairment loss account Dr..

To Accumulated impairment loss

( Being recognition of impairment loss)

4000

4000

30/06/19 Fixture & fitting

Equipments

Motor vehicle

To Impairment loss

( Being allocation of impairment loss with assets)

125

875

3000

4000

CONCLUSION

From the above discussion it has been consulted that every accounting standard used for

specific purpose where accountant have to pass journal entry to better clarity in their accounts.

As well as whenever company required money in their organization to run their operational

activities they generally issued shares through inviting applicants. Along with this, revaluation

model helps in estimating depreciation amount and how it will impact the overall business. In

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.