Detailed Analysis of Taxation Theory Assignment - Finance Module

VerifiedAdded on 2019/10/30

|8

|2525

|81

Homework Assignment

AI Summary

This assignment provides a detailed analysis of taxation theory through five distinct scenarios. The first answer examines capital gains tax, calculating net capital gain or loss on assets held for different periods and for personal use, collectibles, and investments. The second answer addresses loan fringe benefits, calculating the taxable value of a loan with a below-market interest rate, and determining tax-deductible interest. The third scenario explores the tax implications of a rental property agreement, outlining how profits and losses are divided between partners and the responsibility for tax treatment. The fourth answer discusses the legal principle of tax avoidance and the rights of individuals to manage their accounts to minimize tax liability. The final answer investigates the tax treatment of timber receipts, differentiating between recurring and non-recurring payments and their implications for tax categorization.

TAXATION THEORY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation theory

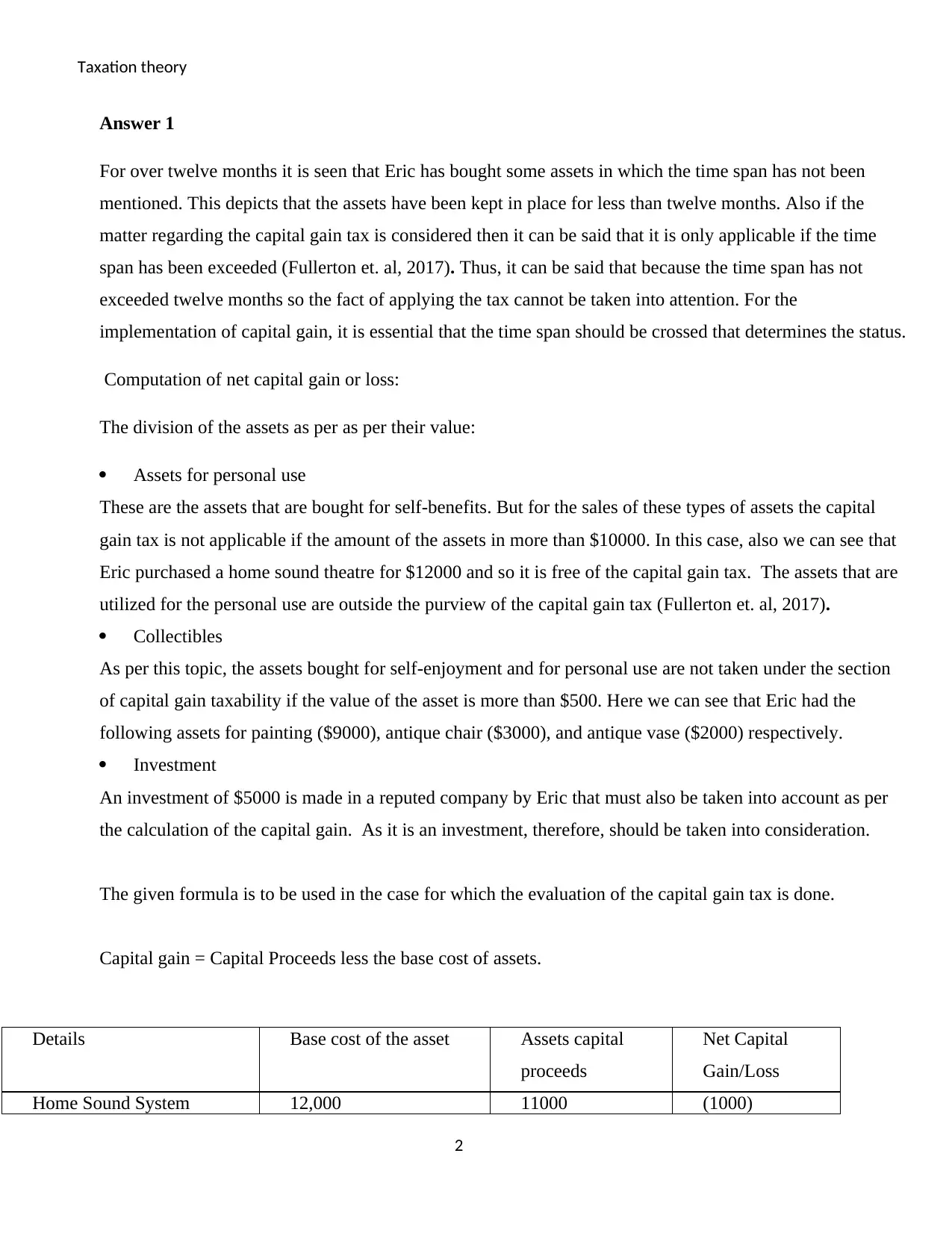

Answer 1

For over twelve months it is seen that Eric has bought some assets in which the time span has not been

mentioned. This depicts that the assets have been kept in place for less than twelve months. Also if the

matter regarding the capital gain tax is considered then it can be said that it is only applicable if the time

span has been exceeded (Fullerton et. al, 2017). Thus, it can be said that because the time span has not

exceeded twelve months so the fact of applying the tax cannot be taken into attention. For the

implementation of capital gain, it is essential that the time span should be crossed that determines the status.

Computation of net capital gain or loss:

The division of the assets as per as per their value:

Assets for personal use

These are the assets that are bought for self-benefits. But for the sales of these types of assets the capital

gain tax is not applicable if the amount of the assets in more than $10000. In this case, also we can see that

Eric purchased a home sound theatre for $12000 and so it is free of the capital gain tax. The assets that are

utilized for the personal use are outside the purview of the capital gain tax (Fullerton et. al, 2017).

Collectibles

As per this topic, the assets bought for self-enjoyment and for personal use are not taken under the section

of capital gain taxability if the value of the asset is more than $500. Here we can see that Eric had the

following assets for painting ($9000), antique chair ($3000), and antique vase ($2000) respectively.

Investment

An investment of $5000 is made in a reputed company by Eric that must also be taken into account as per

the calculation of the capital gain. As it is an investment, therefore, should be taken into consideration.

The given formula is to be used in the case for which the evaluation of the capital gain tax is done.

Capital gain = Capital Proceeds less the base cost of assets.

Details Base cost of the asset Assets capital

proceeds

Net Capital

Gain/Loss

Home Sound System 12,000 11000 (1000)

2

Answer 1

For over twelve months it is seen that Eric has bought some assets in which the time span has not been

mentioned. This depicts that the assets have been kept in place for less than twelve months. Also if the

matter regarding the capital gain tax is considered then it can be said that it is only applicable if the time

span has been exceeded (Fullerton et. al, 2017). Thus, it can be said that because the time span has not

exceeded twelve months so the fact of applying the tax cannot be taken into attention. For the

implementation of capital gain, it is essential that the time span should be crossed that determines the status.

Computation of net capital gain or loss:

The division of the assets as per as per their value:

Assets for personal use

These are the assets that are bought for self-benefits. But for the sales of these types of assets the capital

gain tax is not applicable if the amount of the assets in more than $10000. In this case, also we can see that

Eric purchased a home sound theatre for $12000 and so it is free of the capital gain tax. The assets that are

utilized for the personal use are outside the purview of the capital gain tax (Fullerton et. al, 2017).

Collectibles

As per this topic, the assets bought for self-enjoyment and for personal use are not taken under the section

of capital gain taxability if the value of the asset is more than $500. Here we can see that Eric had the

following assets for painting ($9000), antique chair ($3000), and antique vase ($2000) respectively.

Investment

An investment of $5000 is made in a reputed company by Eric that must also be taken into account as per

the calculation of the capital gain. As it is an investment, therefore, should be taken into consideration.

The given formula is to be used in the case for which the evaluation of the capital gain tax is done.

Capital gain = Capital Proceeds less the base cost of assets.

Details Base cost of the asset Assets capital

proceeds

Net Capital

Gain/Loss

Home Sound System 12,000 11000 (1000)

2

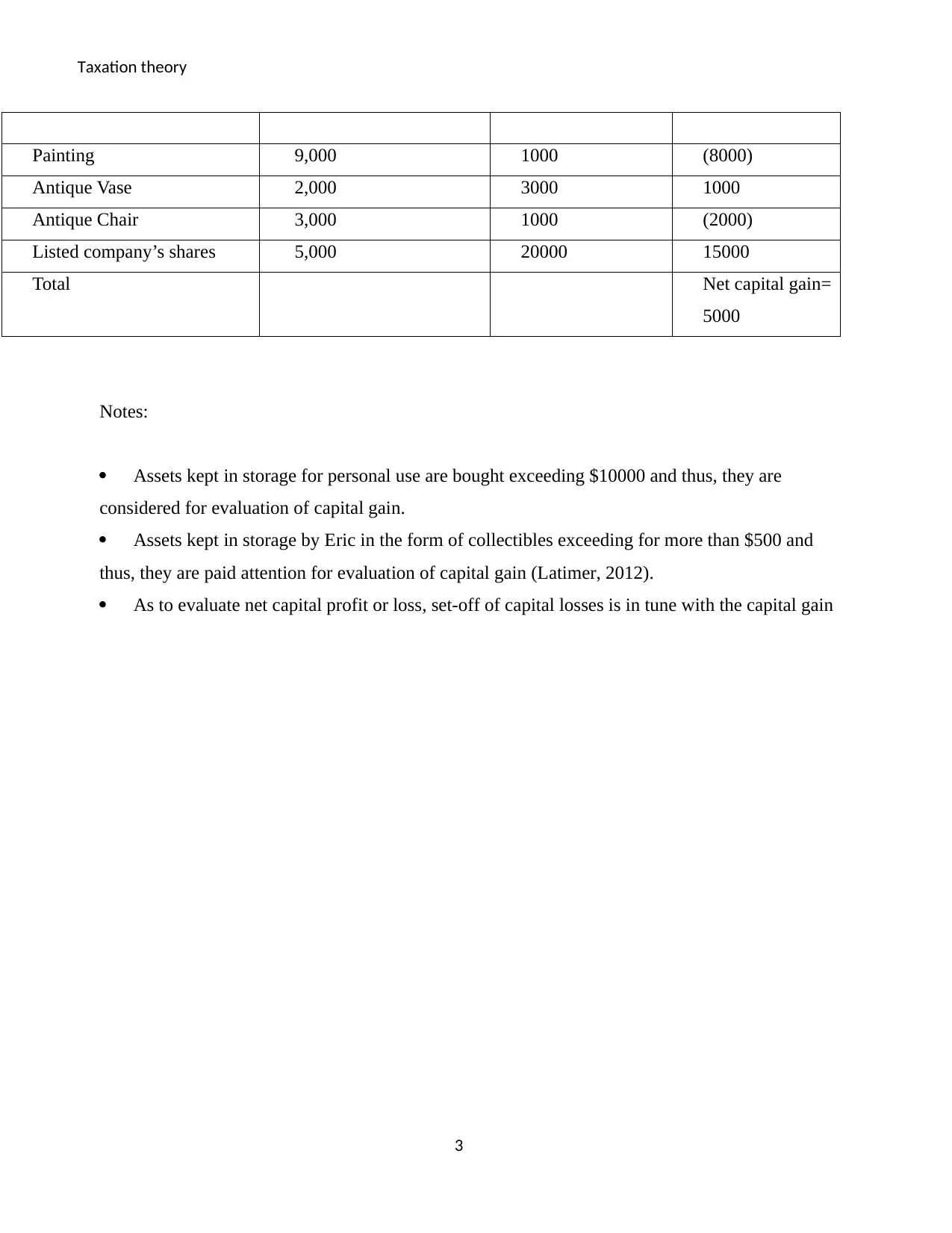

Taxation theory

Painting 9,000 1000 (8000)

Antique Vase 2,000 3000 1000

Antique Chair 3,000 1000 (2000)

Listed company’s shares 5,000 20000 15000

Total Net capital gain=

5000

Notes:

Assets kept in storage for personal use are bought exceeding $10000 and thus, they are

considered for evaluation of capital gain.

Assets kept in storage by Eric in the form of collectibles exceeding for more than $500 and

thus, they are paid attention for evaluation of capital gain (Latimer, 2012).

As to evaluate net capital profit or loss, set-off of capital losses is in tune with the capital gain

3

Painting 9,000 1000 (8000)

Antique Vase 2,000 3000 1000

Antique Chair 3,000 1000 (2000)

Listed company’s shares 5,000 20000 15000

Total Net capital gain=

5000

Notes:

Assets kept in storage for personal use are bought exceeding $10000 and thus, they are

considered for evaluation of capital gain.

Assets kept in storage by Eric in the form of collectibles exceeding for more than $500 and

thus, they are paid attention for evaluation of capital gain (Latimer, 2012).

As to evaluate net capital profit or loss, set-off of capital losses is in tune with the capital gain

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation theory

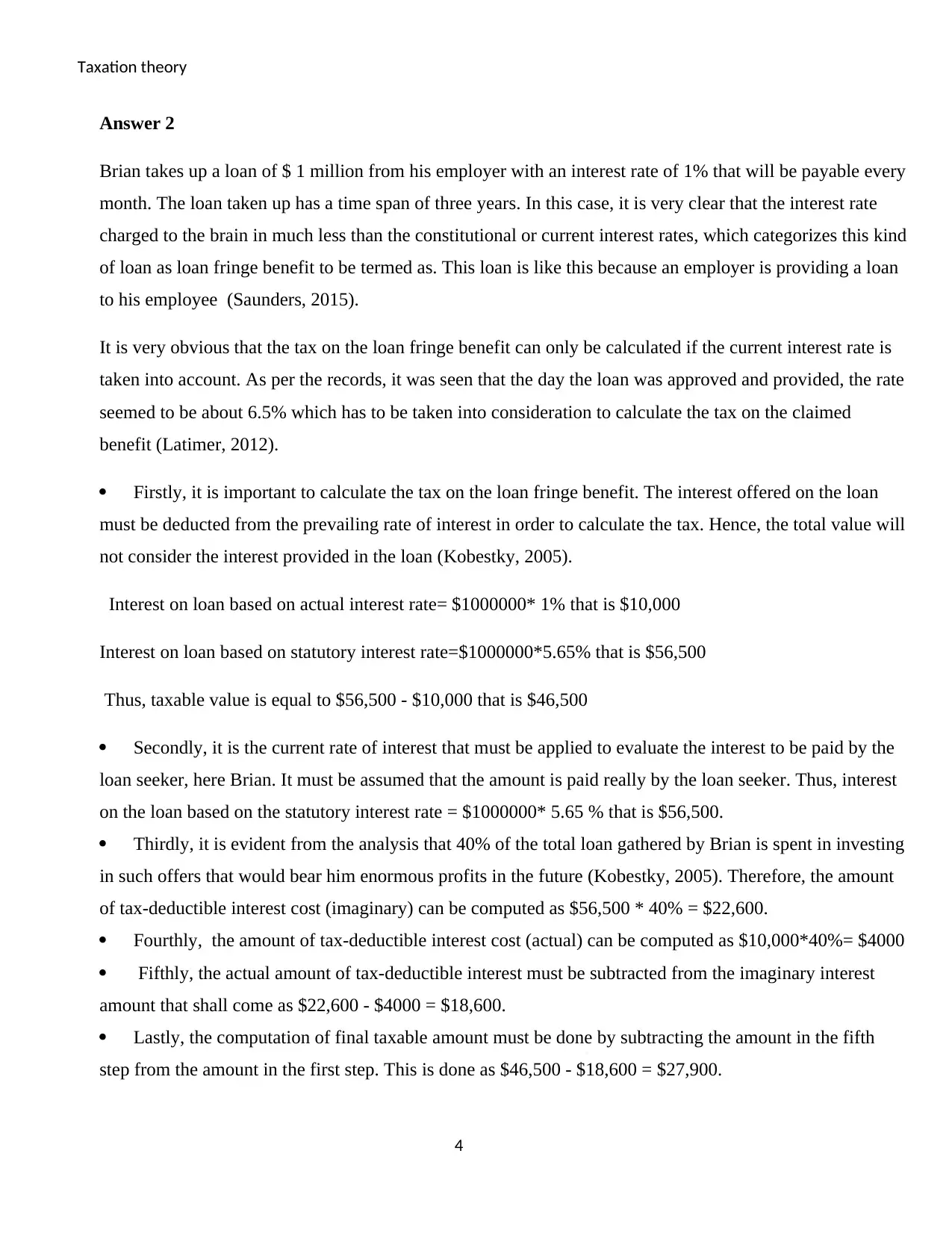

Answer 2

Brian takes up a loan of $ 1 million from his employer with an interest rate of 1% that will be payable every

month. The loan taken up has a time span of three years. In this case, it is very clear that the interest rate

charged to the brain in much less than the constitutional or current interest rates, which categorizes this kind

of loan as loan fringe benefit to be termed as. This loan is like this because an employer is providing a loan

to his employee (Saunders, 2015).

It is very obvious that the tax on the loan fringe benefit can only be calculated if the current interest rate is

taken into account. As per the records, it was seen that the day the loan was approved and provided, the rate

seemed to be about 6.5% which has to be taken into consideration to calculate the tax on the claimed

benefit (Latimer, 2012).

Firstly, it is important to calculate the tax on the loan fringe benefit. The interest offered on the loan

must be deducted from the prevailing rate of interest in order to calculate the tax. Hence, the total value will

not consider the interest provided in the loan (Kobestky, 2005).

Interest on loan based on actual interest rate= $1000000* 1% that is $10,000

Interest on loan based on statutory interest rate=$1000000*5.65% that is $56,500

Thus, taxable value is equal to $56,500 - $10,000 that is $46,500

Secondly, it is the current rate of interest that must be applied to evaluate the interest to be paid by the

loan seeker, here Brian. It must be assumed that the amount is paid really by the loan seeker. Thus, interest

on the loan based on the statutory interest rate = $1000000* 5.65 % that is $56,500.

Thirdly, it is evident from the analysis that 40% of the total loan gathered by Brian is spent in investing

in such offers that would bear him enormous profits in the future (Kobestky, 2005). Therefore, the amount

of tax-deductible interest cost (imaginary) can be computed as $56,500 * 40% = $22,600.

Fourthly, the amount of tax-deductible interest cost (actual) can be computed as $10,000*40%= $4000

Fifthly, the actual amount of tax-deductible interest must be subtracted from the imaginary interest

amount that shall come as $22,600 - $4000 = $18,600.

Lastly, the computation of final taxable amount must be done by subtracting the amount in the fifth

step from the amount in the first step. This is done as $46,500 - $18,600 = $27,900.

4

Answer 2

Brian takes up a loan of $ 1 million from his employer with an interest rate of 1% that will be payable every

month. The loan taken up has a time span of three years. In this case, it is very clear that the interest rate

charged to the brain in much less than the constitutional or current interest rates, which categorizes this kind

of loan as loan fringe benefit to be termed as. This loan is like this because an employer is providing a loan

to his employee (Saunders, 2015).

It is very obvious that the tax on the loan fringe benefit can only be calculated if the current interest rate is

taken into account. As per the records, it was seen that the day the loan was approved and provided, the rate

seemed to be about 6.5% which has to be taken into consideration to calculate the tax on the claimed

benefit (Latimer, 2012).

Firstly, it is important to calculate the tax on the loan fringe benefit. The interest offered on the loan

must be deducted from the prevailing rate of interest in order to calculate the tax. Hence, the total value will

not consider the interest provided in the loan (Kobestky, 2005).

Interest on loan based on actual interest rate= $1000000* 1% that is $10,000

Interest on loan based on statutory interest rate=$1000000*5.65% that is $56,500

Thus, taxable value is equal to $56,500 - $10,000 that is $46,500

Secondly, it is the current rate of interest that must be applied to evaluate the interest to be paid by the

loan seeker, here Brian. It must be assumed that the amount is paid really by the loan seeker. Thus, interest

on the loan based on the statutory interest rate = $1000000* 5.65 % that is $56,500.

Thirdly, it is evident from the analysis that 40% of the total loan gathered by Brian is spent in investing

in such offers that would bear him enormous profits in the future (Kobestky, 2005). Therefore, the amount

of tax-deductible interest cost (imaginary) can be computed as $56,500 * 40% = $22,600.

Fourthly, the amount of tax-deductible interest cost (actual) can be computed as $10,000*40%= $4000

Fifthly, the actual amount of tax-deductible interest must be subtracted from the imaginary interest

amount that shall come as $22,600 - $4000 = $18,600.

Lastly, the computation of final taxable amount must be done by subtracting the amount in the fifth

step from the amount in the first step. This is done as $46,500 - $18,600 = $27,900.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation theory

Nevertheless, if the loan fringe benefit interest is paid after the time span of the loan and not in

monthly installments, then the actual tenure of the loan would be counted from the time span till

the date when the interest becomes billed. Furthermore, if Brian is set free by the bank for paying

off the interest on the loan, then the evaluations will be done in the way as stated before (Woellner

et. al, 2017). The one difference which will exist is that the defined interest rate will not be paid

any attention to.

Answer 3

Jack and Jill took up an agreement in which to grab a rented property tell will be entitled to obtain funds.

The agreement clearly says that both Jack and his wife Jill will be tenants, but the profits made by them in

relation to the property will be divided in a way resulting in Jack receiving only 10% of them will Jill

grabbing 90% profits. It was also clearly stated that if the acquired property suffers any losses then it is Jack

who will have to bear them fully. It was clearly prescribed in the written document and hence, the major

responsibility is to Jack.

As per the given case it is seen that a massive loss of $10000 had struck the previous year and as per the

rules of the agreement, it is Jack who will be fully responsible for paying off for the losses. It is seen that

the loss amount is added up to the income of Jack in order to reduce his income and tax. The agreement

also allows Jack to carry forward the loss amount if he has no source of income (Sadiq et. al, 2017).

Two cases can be put up in front of Jack and Jill is they reach the conclusion to sell the property. The cases

are either profit or loss. As per the rules of the agreement, if they earn a profit then, first of all, the profit

will be divided in accordance with their respective percentages. Also, it must be noticed that if there is

profit than the loss of $10000 in the previous year will be deducted from Jack’s profit. But, if they suffer a

loss then the whole should be paid by Jack alone. Jack is allowed to carry forward the final loss amount if

he has no source of income otherwise the loss amount will be compensated from his incomes. So the loss

would be taken on by Jack in any case and so it is clear that the pressure of tax treatment will not affect

Jack though he is paying off for the losses.

Answer 4

In accordance with the case of IRC v Duke of Westminster [1936] AC 1 it is said that it is the right of a

person or individual to manage his account in a way that the payable tax on the amount is set on a minimum

5

Nevertheless, if the loan fringe benefit interest is paid after the time span of the loan and not in

monthly installments, then the actual tenure of the loan would be counted from the time span till

the date when the interest becomes billed. Furthermore, if Brian is set free by the bank for paying

off the interest on the loan, then the evaluations will be done in the way as stated before (Woellner

et. al, 2017). The one difference which will exist is that the defined interest rate will not be paid

any attention to.

Answer 3

Jack and Jill took up an agreement in which to grab a rented property tell will be entitled to obtain funds.

The agreement clearly says that both Jack and his wife Jill will be tenants, but the profits made by them in

relation to the property will be divided in a way resulting in Jack receiving only 10% of them will Jill

grabbing 90% profits. It was also clearly stated that if the acquired property suffers any losses then it is Jack

who will have to bear them fully. It was clearly prescribed in the written document and hence, the major

responsibility is to Jack.

As per the given case it is seen that a massive loss of $10000 had struck the previous year and as per the

rules of the agreement, it is Jack who will be fully responsible for paying off for the losses. It is seen that

the loss amount is added up to the income of Jack in order to reduce his income and tax. The agreement

also allows Jack to carry forward the loss amount if he has no source of income (Sadiq et. al, 2017).

Two cases can be put up in front of Jack and Jill is they reach the conclusion to sell the property. The cases

are either profit or loss. As per the rules of the agreement, if they earn a profit then, first of all, the profit

will be divided in accordance with their respective percentages. Also, it must be noticed that if there is

profit than the loss of $10000 in the previous year will be deducted from Jack’s profit. But, if they suffer a

loss then the whole should be paid by Jack alone. Jack is allowed to carry forward the final loss amount if

he has no source of income otherwise the loss amount will be compensated from his incomes. So the loss

would be taken on by Jack in any case and so it is clear that the pressure of tax treatment will not affect

Jack though he is paying off for the losses.

Answer 4

In accordance with the case of IRC v Duke of Westminster [1936] AC 1 it is said that it is the right of a

person or individual to manage his account in a way that the payable tax on the amount is set on a minimum

5

Taxation theory

scale. But the steps followed in order to achieve the above-mentioned case one should always remember

that not to follow any unauthorized or manipulative means that can prove to be a danger to the individual in

the future. As per the case it can be said that the authorities is not allowed to interfere in any of the methods

followed by the person if he is able to produce valid documents for such actions and the court cannot just

pass judgment on the basis of underlying documents (Pratt & Kulsrud, 2013).

The records mentioned as per the case shows that the following concerns are comprised in it:

Every individual has a right to check their accounts in such a way that it decreases their tax

amount which is to be given to the authorities. It clearly implies that the individual can check the

overall accounts so as to provide the correct amount.

If any clever unauthorized or manipulative steps, then additional tax is approved to be applied

to the account which will increase the tax amount upon the individual.

If the transactions are genuine in nature and the individual has authenticated documents to

prove the same, then no authority can question the validity of the transactions based on the

submitted substances documents (Nethercott et. al, 2013).

With the passage of time, it is seen that new laws have been implemented with a decrease in value of the

above-mentioned law. In today’s world, such laws have been put up that it not easy to manipulate the

transactions. It is also seen that a business suffering insolvency is approved to manipulate its balance sheets

which are only valid if the assets of the company are written off. Thus from the above explanations, it is

clear that any means adopted by the business which is legally correct cannot rise to any set of the question

by any authority (Kenny, 2016). They can be followed whenever needed.

Answer 5

Bill owns a massive land full of pine trees on a large scale. He has an idea to start grazing sheep on that

massive area for which the whole area must be swept off the pine trees. An amount of $1000 will also be

rewarded to bill for sweeping off every thousand meters of timber. The risen question is that whether a tax

on the payment receipts will be earned by Bill or not, as the net value of the receipts of timber clearing is

not acknowledged (Kenny, 2016). But despite all this the receipts are put into the category of revenue and

thus no credits will be approved to be earned.

6

scale. But the steps followed in order to achieve the above-mentioned case one should always remember

that not to follow any unauthorized or manipulative means that can prove to be a danger to the individual in

the future. As per the case it can be said that the authorities is not allowed to interfere in any of the methods

followed by the person if he is able to produce valid documents for such actions and the court cannot just

pass judgment on the basis of underlying documents (Pratt & Kulsrud, 2013).

The records mentioned as per the case shows that the following concerns are comprised in it:

Every individual has a right to check their accounts in such a way that it decreases their tax

amount which is to be given to the authorities. It clearly implies that the individual can check the

overall accounts so as to provide the correct amount.

If any clever unauthorized or manipulative steps, then additional tax is approved to be applied

to the account which will increase the tax amount upon the individual.

If the transactions are genuine in nature and the individual has authenticated documents to

prove the same, then no authority can question the validity of the transactions based on the

submitted substances documents (Nethercott et. al, 2013).

With the passage of time, it is seen that new laws have been implemented with a decrease in value of the

above-mentioned law. In today’s world, such laws have been put up that it not easy to manipulate the

transactions. It is also seen that a business suffering insolvency is approved to manipulate its balance sheets

which are only valid if the assets of the company are written off. Thus from the above explanations, it is

clear that any means adopted by the business which is legally correct cannot rise to any set of the question

by any authority (Kenny, 2016). They can be followed whenever needed.

Answer 5

Bill owns a massive land full of pine trees on a large scale. He has an idea to start grazing sheep on that

massive area for which the whole area must be swept off the pine trees. An amount of $1000 will also be

rewarded to bill for sweeping off every thousand meters of timber. The risen question is that whether a tax

on the payment receipts will be earned by Bill or not, as the net value of the receipts of timber clearing is

not acknowledged (Kenny, 2016). But despite all this the receipts are put into the category of revenue and

thus no credits will be approved to be earned.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation theory

In case a single payment of $50000 is made by the logging company to Bill, so as to deforest as many

timber trees from the land in accordance with the demand, means that Bill has sold his right on the timber

of his land and the same is categorized as non-recurring and capital in nature as well as single which

happened due to the selling of rights. All this corresponds to the receipt which is capital in nature.

Taking into utter consideration both the above cases, if Bill chooses the first technique in which a small

amount of $1000 will be paid from time to time then, only normal taxes will be applied on the receipt. It

can be commented that the rule will determine the status of the transaction. Since consideration is provided

to the first method thereby attraction of normal taxes will be done (Hopewell, 2012). But if Bill follows the

second technique than a single large payment of $50000 is made against the rights to cut timber, and due to

the massiveness of the amount, the capital gain tax will be a part of it. Since the transaction has happened it

has attracted capital gain tax.

7

In case a single payment of $50000 is made by the logging company to Bill, so as to deforest as many

timber trees from the land in accordance with the demand, means that Bill has sold his right on the timber

of his land and the same is categorized as non-recurring and capital in nature as well as single which

happened due to the selling of rights. All this corresponds to the receipt which is capital in nature.

Taking into utter consideration both the above cases, if Bill chooses the first technique in which a small

amount of $1000 will be paid from time to time then, only normal taxes will be applied on the receipt. It

can be commented that the rule will determine the status of the transaction. Since consideration is provided

to the first method thereby attraction of normal taxes will be done (Hopewell, 2012). But if Bill follows the

second technique than a single large payment of $50000 is made against the rights to cut timber, and due to

the massiveness of the amount, the capital gain tax will be a part of it. Since the transaction has happened it

has attracted capital gain tax.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation theory

References

Fullerton, I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters: Australia

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Kenny, P, Blissenden, M, & Villios, S 2017, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation Press

Latimer, P 2012, Australian Business Law 2012, 31st ed, Sydney, NSW: CCH Australia Limited.

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 15 September 2017,

www.zdnet.com.au.

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Woellner, R, Barkoczy, S, Murphy, S, Evans, C & Pinto, D 2017, Australian taxation law 2017,

Oxford University Press Australia

8

References

Fullerton, I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters: Australia

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Kenny, P, Blissenden, M, & Villios, S 2017, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation Press

Latimer, P 2012, Australian Business Law 2012, 31st ed, Sydney, NSW: CCH Australia Limited.

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 15 September 2017,

www.zdnet.com.au.

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Woellner, R, Barkoczy, S, Murphy, S, Evans, C & Pinto, D 2017, Australian taxation law 2017,

Oxford University Press Australia

8

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.