Detailed Analysis of Finance and Funding in Travel and Tourism Sector

VerifiedAdded on 2020/01/21

|18

|4804

|46

Report

AI Summary

This report provides a detailed analysis of finance and funding within the travel and tourism sector. It begins with an introduction to the importance of finance in the industry, followed by an in-depth exploration of Cost-Volume-Profit (CVP) analysis and its application. The report then examines various pricing methods, including competitive, geographical, cost-plus margin, and penetration pricing policies. It also discusses factors influencing profits, such as costs, volume, and price. Furthermore, the report delves into management accounting information, including budgeting, cost accounting, and ratio analysis, and how these tools are utilized in decision-making. Investment appraisal techniques, such as payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR), are also analyzed. The report includes an interpretation of financial statements from Thomas Cook Group PLC, focusing on profitability, liquidity, and investment ratios. Finally, it explores various sources of finance available to the tourism industry, including both internal and external options, providing a comprehensive overview of financial strategies and their practical application within the sector.

Finance and Funding in the Travel and Tourism Sector

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ...............................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 Importance of CVP Analysis.....................................................................................................4

CVP Anlysis : .........................................................................................................................4

Importance of CVP anlaysis in Tourism Industry...................................................................5

1.2 Analysis of Pricing methods for Travel and Tourism Sector.....................................................5

Competitive pricing policy .....................................................................................................5

Geographical Pricing ..............................................................................................................5

Cost plus Margin ....................................................................................................................6

Penetration Pricing Policy ......................................................................................................6

1.3 Factors influencing Profits for Travel and Tourism...................................................................6

TASK 2 ................................................................................................................................................7

2.1 Types Of Management Accounting Information applied in Decision Making..........................7

Budgeting ...............................................................................................................................7

Cost accounting and Variance analysis .................................................................................8

Ratio Analysis ........................................................................................................................8

2.2 Use of investment Appraisal Techniques in decision making...................................................8

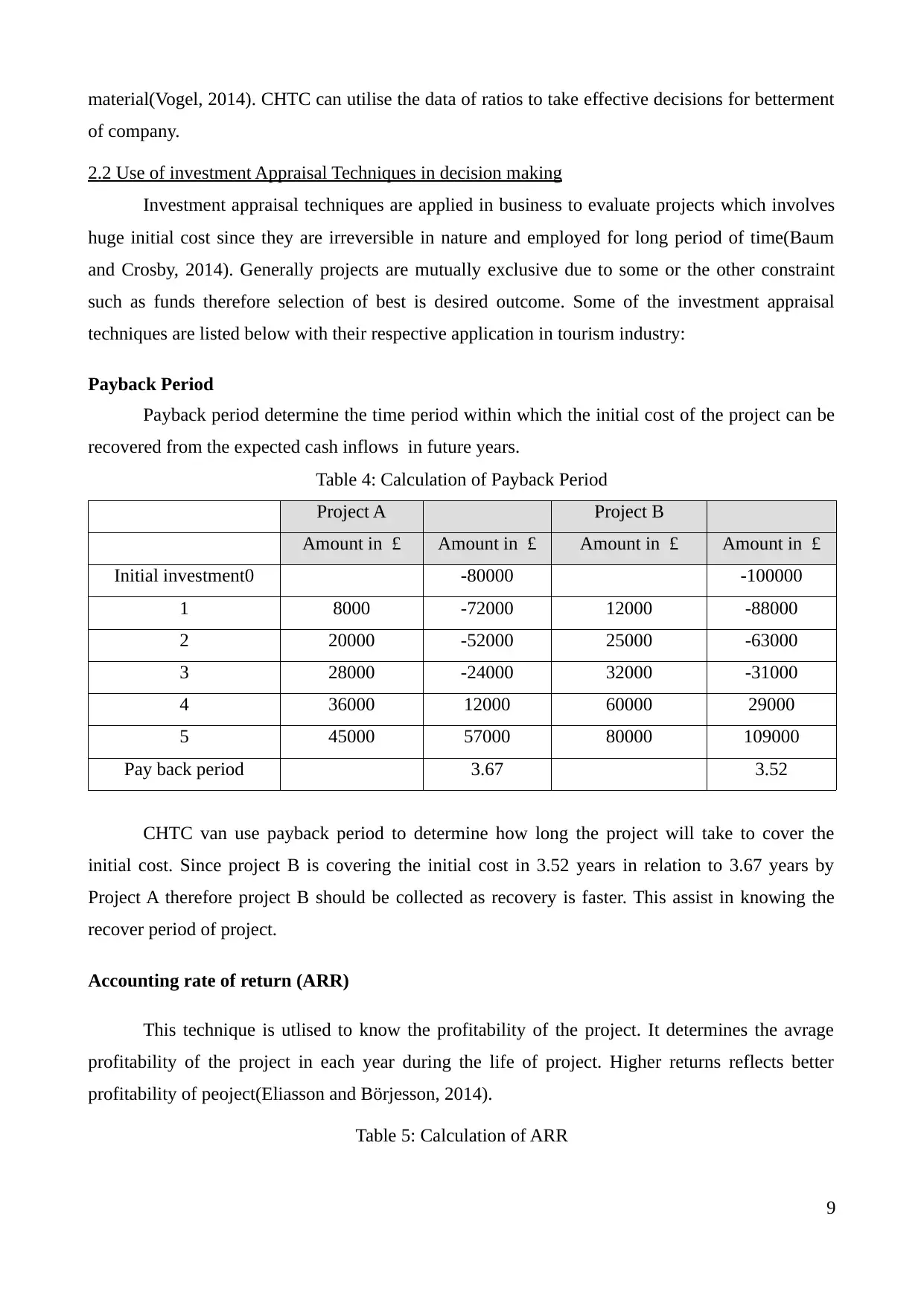

Payback Period........................................................................................................................8

Accounting rate of return (ARR)............................................................................................9

Net Present Value (NPV).........................................................................................................9

Internal Rate of Return (IRR)................................................................................................10

TASK 3 ..............................................................................................................................................10

3.1 Interpretation of Financial Statements of Thomas Cook Group PLC......................................10

Profitability Ratios................................................................................................................10

Liquidity Ratios.....................................................................................................................11

Investment Ratios.................................................................................................................12

TASK 4...............................................................................................................................................13

4.1 Sources of Finance for Tourism Industry.................................................................................13

Internal Source......................................................................................................................14

External Sources ...................................................................................................................14

CONCLUSION .................................................................................................................................15

REFERENCES...................................................................................................................................17

Index of Tables

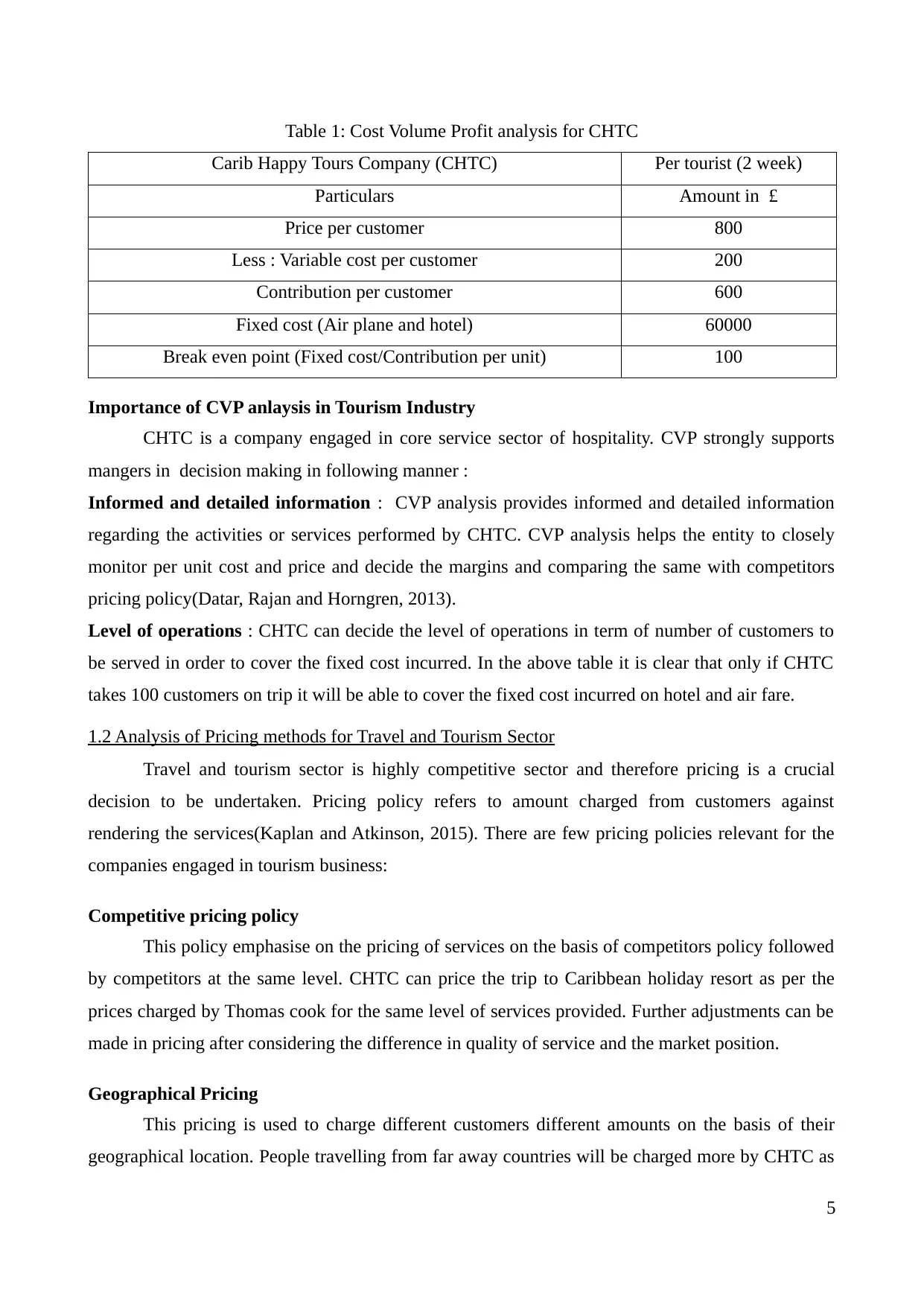

Table 1: Cost Volume Profit analysis for CHTC..................................................................................5

Table 2: Factors influencing the profits................................................................................................6

Table 3: Calculation for profits when 90 tourist registers....................................................................7

Table 4: Calculation of Payback Period...............................................................................................8

Table 5: Calculation of ARR................................................................................................................9

Table 6: Calculation of NPV................................................................................................................9

Table 7: Calculation of IRR................................................................................................................10

Table 8: Ratio analysis on the basis of Profitability ratios of Thomas Cook Group PLC..................10

2

INTRODUCTION ...............................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 Importance of CVP Analysis.....................................................................................................4

CVP Anlysis : .........................................................................................................................4

Importance of CVP anlaysis in Tourism Industry...................................................................5

1.2 Analysis of Pricing methods for Travel and Tourism Sector.....................................................5

Competitive pricing policy .....................................................................................................5

Geographical Pricing ..............................................................................................................5

Cost plus Margin ....................................................................................................................6

Penetration Pricing Policy ......................................................................................................6

1.3 Factors influencing Profits for Travel and Tourism...................................................................6

TASK 2 ................................................................................................................................................7

2.1 Types Of Management Accounting Information applied in Decision Making..........................7

Budgeting ...............................................................................................................................7

Cost accounting and Variance analysis .................................................................................8

Ratio Analysis ........................................................................................................................8

2.2 Use of investment Appraisal Techniques in decision making...................................................8

Payback Period........................................................................................................................8

Accounting rate of return (ARR)............................................................................................9

Net Present Value (NPV).........................................................................................................9

Internal Rate of Return (IRR)................................................................................................10

TASK 3 ..............................................................................................................................................10

3.1 Interpretation of Financial Statements of Thomas Cook Group PLC......................................10

Profitability Ratios................................................................................................................10

Liquidity Ratios.....................................................................................................................11

Investment Ratios.................................................................................................................12

TASK 4...............................................................................................................................................13

4.1 Sources of Finance for Tourism Industry.................................................................................13

Internal Source......................................................................................................................14

External Sources ...................................................................................................................14

CONCLUSION .................................................................................................................................15

REFERENCES...................................................................................................................................17

Index of Tables

Table 1: Cost Volume Profit analysis for CHTC..................................................................................5

Table 2: Factors influencing the profits................................................................................................6

Table 3: Calculation for profits when 90 tourist registers....................................................................7

Table 4: Calculation of Payback Period...............................................................................................8

Table 5: Calculation of ARR................................................................................................................9

Table 6: Calculation of NPV................................................................................................................9

Table 7: Calculation of IRR................................................................................................................10

Table 8: Ratio analysis on the basis of Profitability ratios of Thomas Cook Group PLC..................10

2

Table 9: Ratio analysis on the basis of Liquidity ratios of Thomas Cook Group PLC......................11

Table 10: Ratio analysis on the basis of Investment ratios of Thomas Cook Group PLC.................12

Table 11: Analysis of Internal Sources of Finance.............................................................................14

Table 12: Analysis of External Sources of Finance............................................................................14

Illustration Index

Illustration 1: Cost Volume Profit (CVP) analysis ..............................................................................4

Illustration 2: Management Accounting information functions...........................................................7

Illustration 3: Profitability ratios of Thomas Cook Group PLC.........................................................11

Illustration 4: Liquidity ratios of Thomas Cook Group PLC.............................................................12

Illustration 5: Investment ratios of Thomas Cook Group PLC..........................................................13

3

Table 10: Ratio analysis on the basis of Investment ratios of Thomas Cook Group PLC.................12

Table 11: Analysis of Internal Sources of Finance.............................................................................14

Table 12: Analysis of External Sources of Finance............................................................................14

Illustration Index

Illustration 1: Cost Volume Profit (CVP) analysis ..............................................................................4

Illustration 2: Management Accounting information functions...........................................................7

Illustration 3: Profitability ratios of Thomas Cook Group PLC.........................................................11

Illustration 4: Liquidity ratios of Thomas Cook Group PLC.............................................................12

Illustration 5: Investment ratios of Thomas Cook Group PLC..........................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is a pillar of success and growth for business in every sector and Travel and tourism

is no exception. Carib Happy Tours Company(CHTC) is a company engaged in arranging tours

across the globe. This report reflects the application of CVP analysis and its importance in addition

to evaluation of factors influencing profits of the CHTC. Although management decisions are based

on the intuitions and market conditions but information regarding management accounting plays

vital role in the same. Further this report displays investment appraisal techniques and its use in

decision making. Moreover Thomas Cook Group PLC is selected for performance measurement

under the financial microscope. Finance being major function, this report described the sources of

finance available for the expansion projects of travel and tourism companies.

TASK 1

1.1 Importance of CVP Analysis

CVP Anlysis :

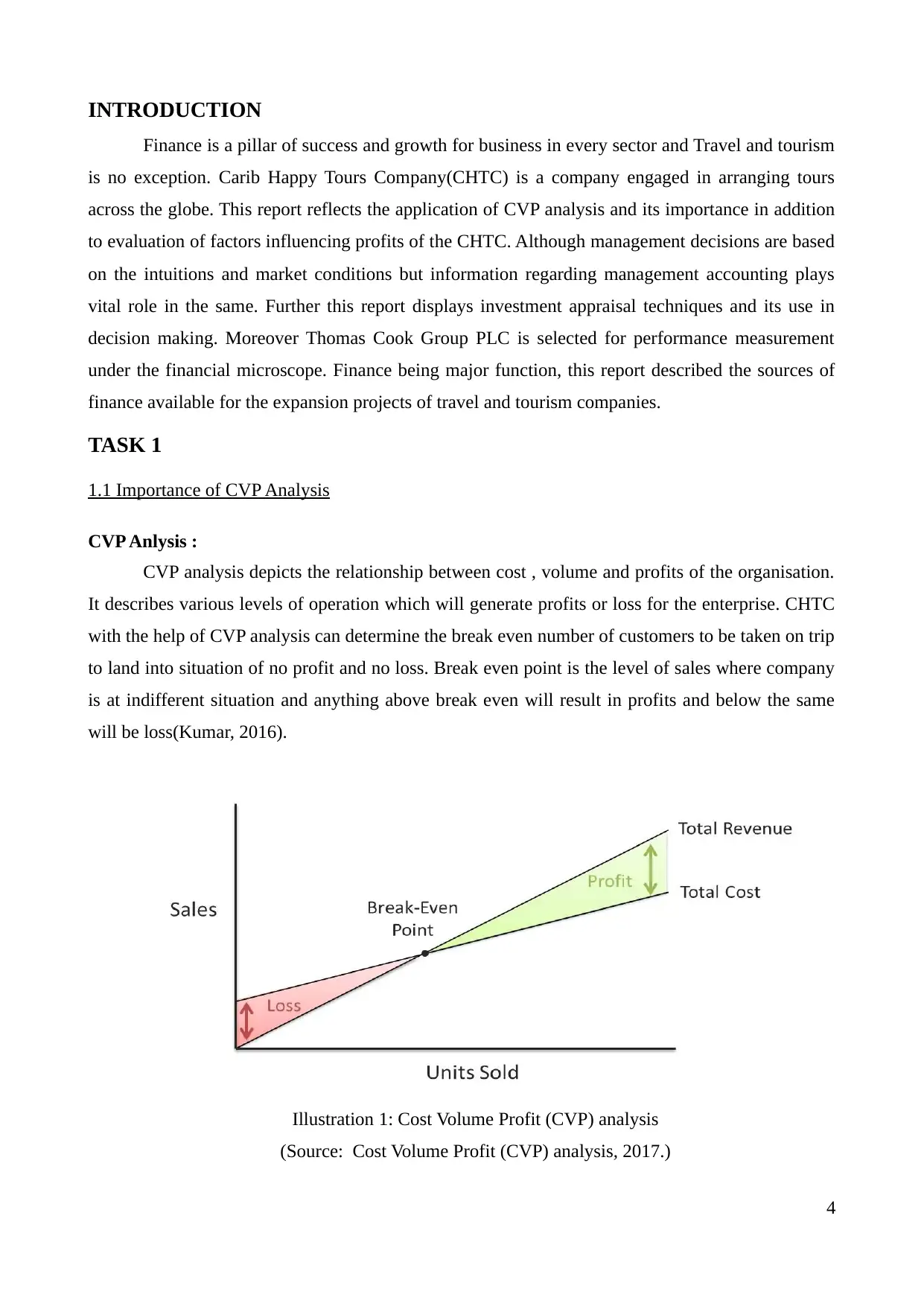

CVP analysis depicts the relationship between cost , volume and profits of the organisation.

It describes various levels of operation which will generate profits or loss for the enterprise. CHTC

with the help of CVP analysis can determine the break even number of customers to be taken on trip

to land into situation of no profit and no loss. Break even point is the level of sales where company

is at indifferent situation and anything above break even will result in profits and below the same

will be loss(Kumar, 2016).

4

Illustration 1: Cost Volume Profit (CVP) analysis

(Source: Cost Volume Profit (CVP) analysis, 2017.)

Finance is a pillar of success and growth for business in every sector and Travel and tourism

is no exception. Carib Happy Tours Company(CHTC) is a company engaged in arranging tours

across the globe. This report reflects the application of CVP analysis and its importance in addition

to evaluation of factors influencing profits of the CHTC. Although management decisions are based

on the intuitions and market conditions but information regarding management accounting plays

vital role in the same. Further this report displays investment appraisal techniques and its use in

decision making. Moreover Thomas Cook Group PLC is selected for performance measurement

under the financial microscope. Finance being major function, this report described the sources of

finance available for the expansion projects of travel and tourism companies.

TASK 1

1.1 Importance of CVP Analysis

CVP Anlysis :

CVP analysis depicts the relationship between cost , volume and profits of the organisation.

It describes various levels of operation which will generate profits or loss for the enterprise. CHTC

with the help of CVP analysis can determine the break even number of customers to be taken on trip

to land into situation of no profit and no loss. Break even point is the level of sales where company

is at indifferent situation and anything above break even will result in profits and below the same

will be loss(Kumar, 2016).

4

Illustration 1: Cost Volume Profit (CVP) analysis

(Source: Cost Volume Profit (CVP) analysis, 2017.)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 1: Cost Volume Profit analysis for CHTC

Carib Happy Tours Company (CHTC) Per tourist (2 week)

Particulars Amount in £

Price per customer 800

Less : Variable cost per customer 200

Contribution per customer 600

Fixed cost (Air plane and hotel) 60000

Break even point (Fixed cost/Contribution per unit) 100

Importance of CVP anlaysis in Tourism Industry

CHTC is a company engaged in core service sector of hospitality. CVP strongly supports

mangers in decision making in following manner :

Informed and detailed information : CVP analysis provides informed and detailed information

regarding the activities or services performed by CHTC. CVP analysis helps the entity to closely

monitor per unit cost and price and decide the margins and comparing the same with competitors

pricing policy(Datar, Rajan and Horngren, 2013).

Level of operations : CHTC can decide the level of operations in term of number of customers to

be served in order to cover the fixed cost incurred. In the above table it is clear that only if CHTC

takes 100 customers on trip it will be able to cover the fixed cost incurred on hotel and air fare.

1.2 Analysis of Pricing methods for Travel and Tourism Sector

Travel and tourism sector is highly competitive sector and therefore pricing is a crucial

decision to be undertaken. Pricing policy refers to amount charged from customers against

rendering the services(Kaplan and Atkinson, 2015). There are few pricing policies relevant for the

companies engaged in tourism business:

Competitive pricing policy

This policy emphasise on the pricing of services on the basis of competitors policy followed

by competitors at the same level. CHTC can price the trip to Caribbean holiday resort as per the

prices charged by Thomas cook for the same level of services provided. Further adjustments can be

made in pricing after considering the difference in quality of service and the market position.

Geographical Pricing

This pricing is used to charge different customers different amounts on the basis of their

geographical location. People travelling from far away countries will be charged more by CHTC as

5

Carib Happy Tours Company (CHTC) Per tourist (2 week)

Particulars Amount in £

Price per customer 800

Less : Variable cost per customer 200

Contribution per customer 600

Fixed cost (Air plane and hotel) 60000

Break even point (Fixed cost/Contribution per unit) 100

Importance of CVP anlaysis in Tourism Industry

CHTC is a company engaged in core service sector of hospitality. CVP strongly supports

mangers in decision making in following manner :

Informed and detailed information : CVP analysis provides informed and detailed information

regarding the activities or services performed by CHTC. CVP analysis helps the entity to closely

monitor per unit cost and price and decide the margins and comparing the same with competitors

pricing policy(Datar, Rajan and Horngren, 2013).

Level of operations : CHTC can decide the level of operations in term of number of customers to

be served in order to cover the fixed cost incurred. In the above table it is clear that only if CHTC

takes 100 customers on trip it will be able to cover the fixed cost incurred on hotel and air fare.

1.2 Analysis of Pricing methods for Travel and Tourism Sector

Travel and tourism sector is highly competitive sector and therefore pricing is a crucial

decision to be undertaken. Pricing policy refers to amount charged from customers against

rendering the services(Kaplan and Atkinson, 2015). There are few pricing policies relevant for the

companies engaged in tourism business:

Competitive pricing policy

This policy emphasise on the pricing of services on the basis of competitors policy followed

by competitors at the same level. CHTC can price the trip to Caribbean holiday resort as per the

prices charged by Thomas cook for the same level of services provided. Further adjustments can be

made in pricing after considering the difference in quality of service and the market position.

Geographical Pricing

This pricing is used to charge different customers different amounts on the basis of their

geographical location. People travelling from far away countries will be charged more by CHTC as

5

compared to North America as the flight charges for later would be less due to minimal

geographical distance.

Cost plus Margin

This is the best pricing policy to be adopted to ascertain minimum profits in the form of margin

over cost. As per thsi pricing policy CHTC should prefer this policy for lareadyt established tour

packages as the cosyt is already known and only desired margin is to be sadded. However this

cannot be applied on new tour packages as exact costs are not clearly defined .

Penetration Pricing Policy

Penetration pricing policy is adopted when demand is elastic with prices and company wants

to act as entry barrier for the new entrants. Penetration policy emphasise on keeping the prices

lower at the initial stage of launching the service to gain the market share(Zadek, Evans and Pruzan,

2013). CHTC can launch the summer holiday trip to Caribbean at lower prices in comparison to

competitors and gain on volumes.

1.3 Factors influencing Profits for Travel and Tourism

Profits are the function of several factors affecting directly or indirectly. However cost, price

and volume affects the profits directly. Further changes in consumer taste and preferences or market

conditions will affect the volume and cost respectively.

Table 2: Factors influencing the profits

Factors Meaning Influence on profits

Cost Cost refers to the expense incurred for

making the services deliverable for the

client. It includes all the direct and

indirect cost. For example: air fare, hotel

rent, food, commission to agents etc.

Cost is in inverse relation with profits. If

the cost of CHTC increase the profits

will decline as the spread between price

and cost will reduce.

Volume Volume refers to number of customers

served. Volume is elastic to the price

charged.

This is in direct relation with profits. If

the number of customers increase the

profitability of CHTC will increase

automatically.

Price Price is the amount charged from

customer for the services. Price drives

Price is directly in relation with profits. If

the price of the services increases the

6

geographical distance.

Cost plus Margin

This is the best pricing policy to be adopted to ascertain minimum profits in the form of margin

over cost. As per thsi pricing policy CHTC should prefer this policy for lareadyt established tour

packages as the cosyt is already known and only desired margin is to be sadded. However this

cannot be applied on new tour packages as exact costs are not clearly defined .

Penetration Pricing Policy

Penetration pricing policy is adopted when demand is elastic with prices and company wants

to act as entry barrier for the new entrants. Penetration policy emphasise on keeping the prices

lower at the initial stage of launching the service to gain the market share(Zadek, Evans and Pruzan,

2013). CHTC can launch the summer holiday trip to Caribbean at lower prices in comparison to

competitors and gain on volumes.

1.3 Factors influencing Profits for Travel and Tourism

Profits are the function of several factors affecting directly or indirectly. However cost, price

and volume affects the profits directly. Further changes in consumer taste and preferences or market

conditions will affect the volume and cost respectively.

Table 2: Factors influencing the profits

Factors Meaning Influence on profits

Cost Cost refers to the expense incurred for

making the services deliverable for the

client. It includes all the direct and

indirect cost. For example: air fare, hotel

rent, food, commission to agents etc.

Cost is in inverse relation with profits. If

the cost of CHTC increase the profits

will decline as the spread between price

and cost will reduce.

Volume Volume refers to number of customers

served. Volume is elastic to the price

charged.

This is in direct relation with profits. If

the number of customers increase the

profitability of CHTC will increase

automatically.

Price Price is the amount charged from

customer for the services. Price drives

Price is directly in relation with profits. If

the price of the services increases the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the customer preference and ratings to

the company.

profits will increase for CHTC as the

difference between cost and price

increases.

Table 3: Calculation for profits when 90 tourist registers

Carib Happy Tours Company Per tourist (2 weeks) 90 Tourist (2 weeks) 117 customers(2 weeks)

Particulars Amount in £ Amount in £ Amount in £

Price per customer 800 72000 93600

Less : Variable cost per

customer 200 18000 23400

Contribution per customer 600 54000 70200

Fixed cost (Air plane and hotel) 60000 60000

Net Profit -6000 10200

TASK 2

2.1 Types Of Management Accounting Information applied in Decision Making

Management Accounting information is crucial part of decision making. It provides

technical evidence to the decision and forms basis for the same. Further quality of decision depends

on the data or information from management accounting(Leary and Roberts, 2014). Some of the

major management accounting informations are demonstrated below:

7

the company.

profits will increase for CHTC as the

difference between cost and price

increases.

Table 3: Calculation for profits when 90 tourist registers

Carib Happy Tours Company Per tourist (2 weeks) 90 Tourist (2 weeks) 117 customers(2 weeks)

Particulars Amount in £ Amount in £ Amount in £

Price per customer 800 72000 93600

Less : Variable cost per

customer 200 18000 23400

Contribution per customer 600 54000 70200

Fixed cost (Air plane and hotel) 60000 60000

Net Profit -6000 10200

TASK 2

2.1 Types Of Management Accounting Information applied in Decision Making

Management Accounting information is crucial part of decision making. It provides

technical evidence to the decision and forms basis for the same. Further quality of decision depends

on the data or information from management accounting(Leary and Roberts, 2014). Some of the

major management accounting informations are demonstrated below:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

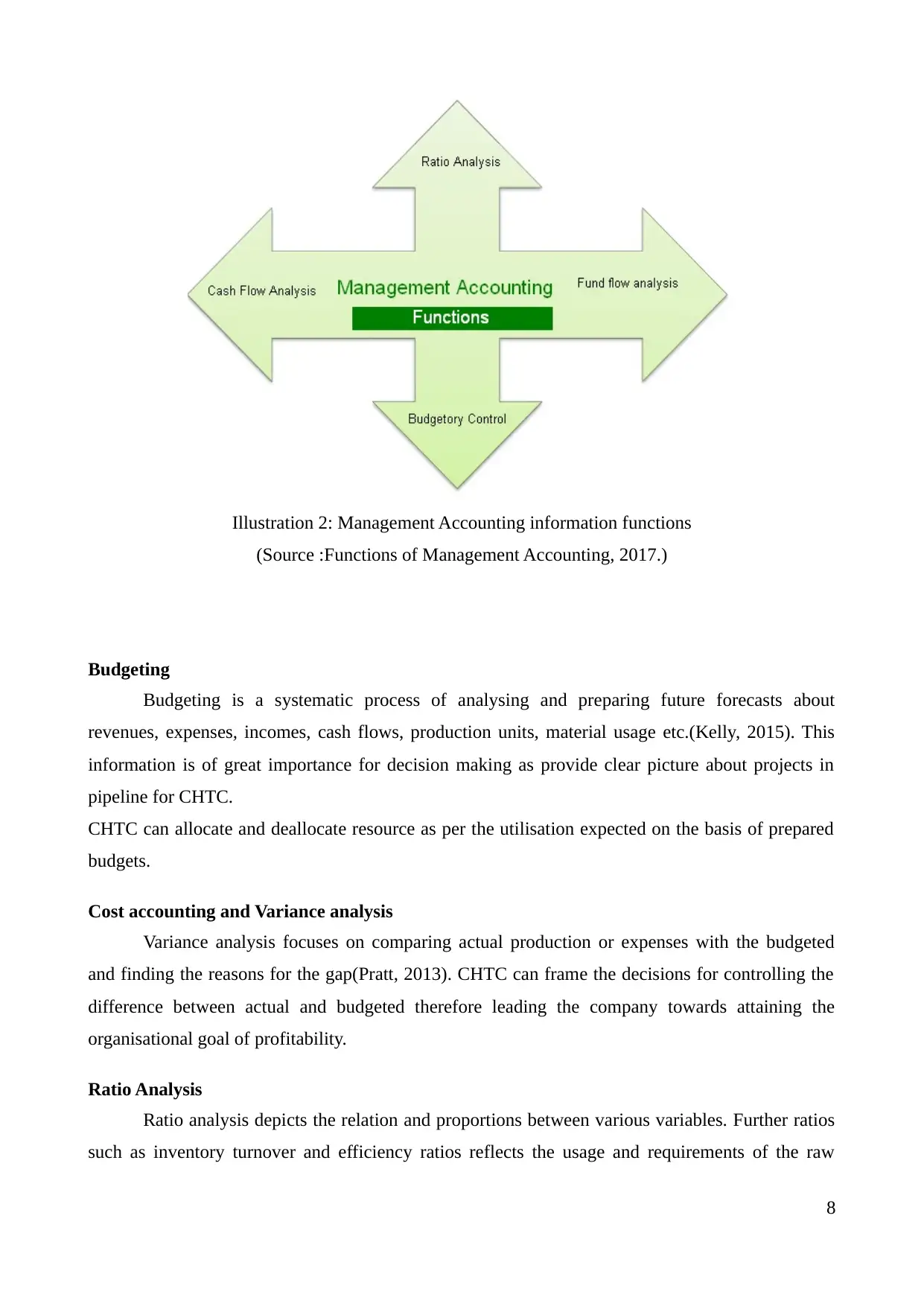

Budgeting

Budgeting is a systematic process of analysing and preparing future forecasts about

revenues, expenses, incomes, cash flows, production units, material usage etc.(Kelly, 2015). This

information is of great importance for decision making as provide clear picture about projects in

pipeline for CHTC.

CHTC can allocate and deallocate resource as per the utilisation expected on the basis of prepared

budgets.

Cost accounting and Variance analysis

Variance analysis focuses on comparing actual production or expenses with the budgeted

and finding the reasons for the gap(Pratt, 2013). CHTC can frame the decisions for controlling the

difference between actual and budgeted therefore leading the company towards attaining the

organisational goal of profitability.

Ratio Analysis

Ratio analysis depicts the relation and proportions between various variables. Further ratios

such as inventory turnover and efficiency ratios reflects the usage and requirements of the raw

8

Illustration 2: Management Accounting information functions

(Source :Functions of Management Accounting, 2017.)

Budgeting is a systematic process of analysing and preparing future forecasts about

revenues, expenses, incomes, cash flows, production units, material usage etc.(Kelly, 2015). This

information is of great importance for decision making as provide clear picture about projects in

pipeline for CHTC.

CHTC can allocate and deallocate resource as per the utilisation expected on the basis of prepared

budgets.

Cost accounting and Variance analysis

Variance analysis focuses on comparing actual production or expenses with the budgeted

and finding the reasons for the gap(Pratt, 2013). CHTC can frame the decisions for controlling the

difference between actual and budgeted therefore leading the company towards attaining the

organisational goal of profitability.

Ratio Analysis

Ratio analysis depicts the relation and proportions between various variables. Further ratios

such as inventory turnover and efficiency ratios reflects the usage and requirements of the raw

8

Illustration 2: Management Accounting information functions

(Source :Functions of Management Accounting, 2017.)

material(Vogel, 2014). CHTC can utilise the data of ratios to take effective decisions for betterment

of company.

2.2 Use of investment Appraisal Techniques in decision making

Investment appraisal techniques are applied in business to evaluate projects which involves

huge initial cost since they are irreversible in nature and employed for long period of time(Baum

and Crosby, 2014). Generally projects are mutually exclusive due to some or the other constraint

such as funds therefore selection of best is desired outcome. Some of the investment appraisal

techniques are listed below with their respective application in tourism industry:

Payback Period

Payback period determine the time period within which the initial cost of the project can be

recovered from the expected cash inflows in future years.

Table 4: Calculation of Payback Period

Project A Project B

Amount in £ Amount in £ Amount in £ Amount in £

Initial investment0 -80000 -100000

1 8000 -72000 12000 -88000

2 20000 -52000 25000 -63000

3 28000 -24000 32000 -31000

4 36000 12000 60000 29000

5 45000 57000 80000 109000

Pay back period 3.67 3.52

CHTC van use payback period to determine how long the project will take to cover the

initial cost. Since project B is covering the initial cost in 3.52 years in relation to 3.67 years by

Project A therefore project B should be collected as recovery is faster. This assist in knowing the

recover period of project.

Accounting rate of return (ARR)

This technique is utlised to know the profitability of the project. It determines the avrage

profitability of the project in each year during the life of project. Higher returns reflects better

profitability of peoject(Eliasson and Börjesson, 2014).

Table 5: Calculation of ARR

9

of company.

2.2 Use of investment Appraisal Techniques in decision making

Investment appraisal techniques are applied in business to evaluate projects which involves

huge initial cost since they are irreversible in nature and employed for long period of time(Baum

and Crosby, 2014). Generally projects are mutually exclusive due to some or the other constraint

such as funds therefore selection of best is desired outcome. Some of the investment appraisal

techniques are listed below with their respective application in tourism industry:

Payback Period

Payback period determine the time period within which the initial cost of the project can be

recovered from the expected cash inflows in future years.

Table 4: Calculation of Payback Period

Project A Project B

Amount in £ Amount in £ Amount in £ Amount in £

Initial investment0 -80000 -100000

1 8000 -72000 12000 -88000

2 20000 -52000 25000 -63000

3 28000 -24000 32000 -31000

4 36000 12000 60000 29000

5 45000 57000 80000 109000

Pay back period 3.67 3.52

CHTC van use payback period to determine how long the project will take to cover the

initial cost. Since project B is covering the initial cost in 3.52 years in relation to 3.67 years by

Project A therefore project B should be collected as recovery is faster. This assist in knowing the

recover period of project.

Accounting rate of return (ARR)

This technique is utlised to know the profitability of the project. It determines the avrage

profitability of the project in each year during the life of project. Higher returns reflects better

profitability of peoject(Eliasson and Börjesson, 2014).

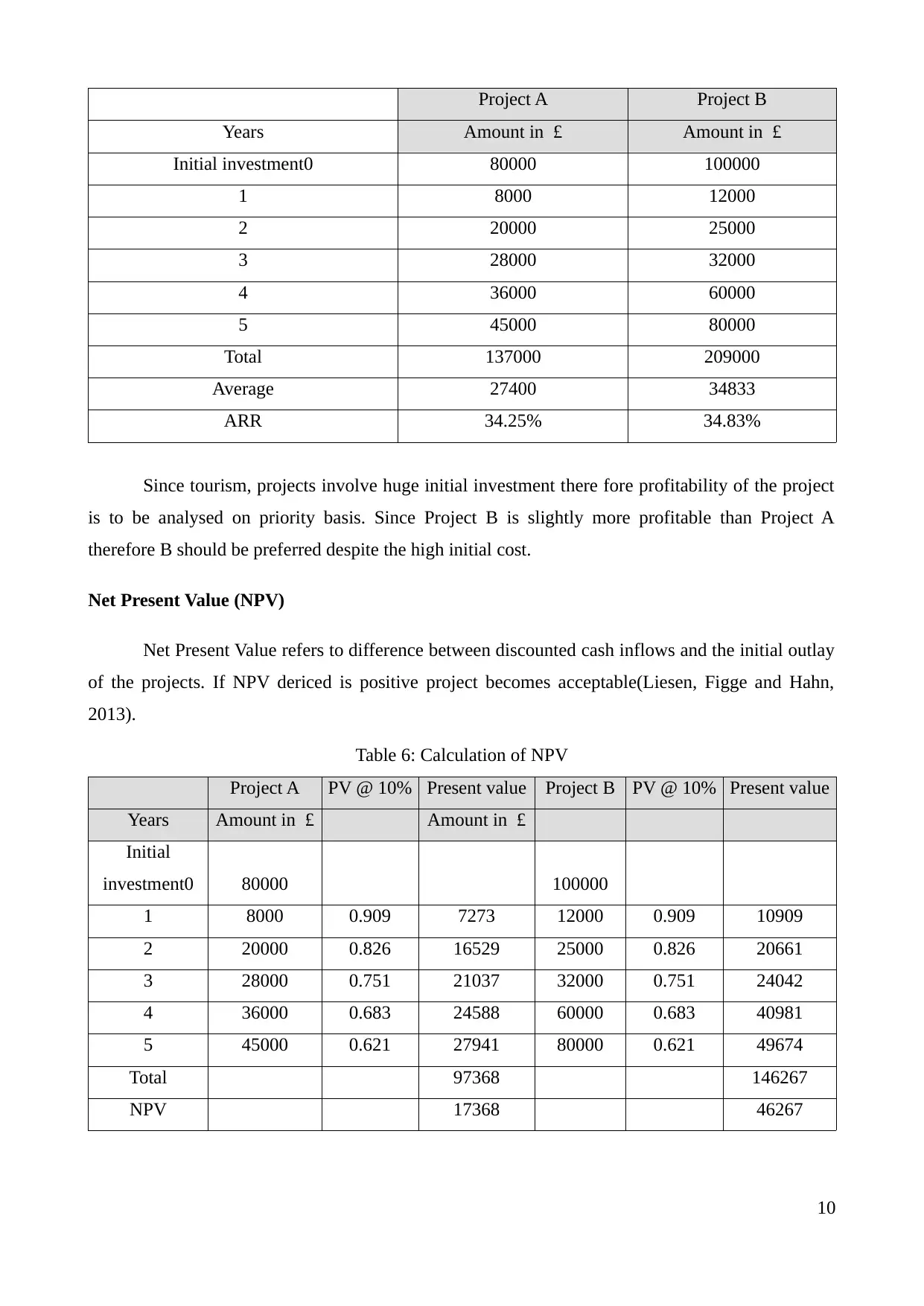

Table 5: Calculation of ARR

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Project A Project B

Years Amount in £ Amount in £

Initial investment0 80000 100000

1 8000 12000

2 20000 25000

3 28000 32000

4 36000 60000

5 45000 80000

Total 137000 209000

Average 27400 34833

ARR 34.25% 34.83%

Since tourism, projects involve huge initial investment there fore profitability of the project

is to be analysed on priority basis. Since Project B is slightly more profitable than Project A

therefore B should be preferred despite the high initial cost.

Net Present Value (NPV)

Net Present Value refers to difference between discounted cash inflows and the initial outlay

of the projects. If NPV dericed is positive project becomes acceptable(Liesen, Figge and Hahn,

2013).

Table 6: Calculation of NPV

Project A PV @ 10% Present value Project B PV @ 10% Present value

Years Amount in £ Amount in £

Initial

investment0 80000 100000

1 8000 0.909 7273 12000 0.909 10909

2 20000 0.826 16529 25000 0.826 20661

3 28000 0.751 21037 32000 0.751 24042

4 36000 0.683 24588 60000 0.683 40981

5 45000 0.621 27941 80000 0.621 49674

Total 97368 146267

NPV 17368 46267

10

Years Amount in £ Amount in £

Initial investment0 80000 100000

1 8000 12000

2 20000 25000

3 28000 32000

4 36000 60000

5 45000 80000

Total 137000 209000

Average 27400 34833

ARR 34.25% 34.83%

Since tourism, projects involve huge initial investment there fore profitability of the project

is to be analysed on priority basis. Since Project B is slightly more profitable than Project A

therefore B should be preferred despite the high initial cost.

Net Present Value (NPV)

Net Present Value refers to difference between discounted cash inflows and the initial outlay

of the projects. If NPV dericed is positive project becomes acceptable(Liesen, Figge and Hahn,

2013).

Table 6: Calculation of NPV

Project A PV @ 10% Present value Project B PV @ 10% Present value

Years Amount in £ Amount in £

Initial

investment0 80000 100000

1 8000 0.909 7273 12000 0.909 10909

2 20000 0.826 16529 25000 0.826 20661

3 28000 0.751 21037 32000 0.751 24042

4 36000 0.683 24588 60000 0.683 40981

5 45000 0.621 27941 80000 0.621 49674

Total 97368 146267

NPV 17368 46267

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is most suitable tool of capital budgeting as it considers time value of money. Further

since the projects are mutually exclusive project B should be adopted with higher NPV generated.

NPV calculates the value added to CHTC with the acceptance of project.

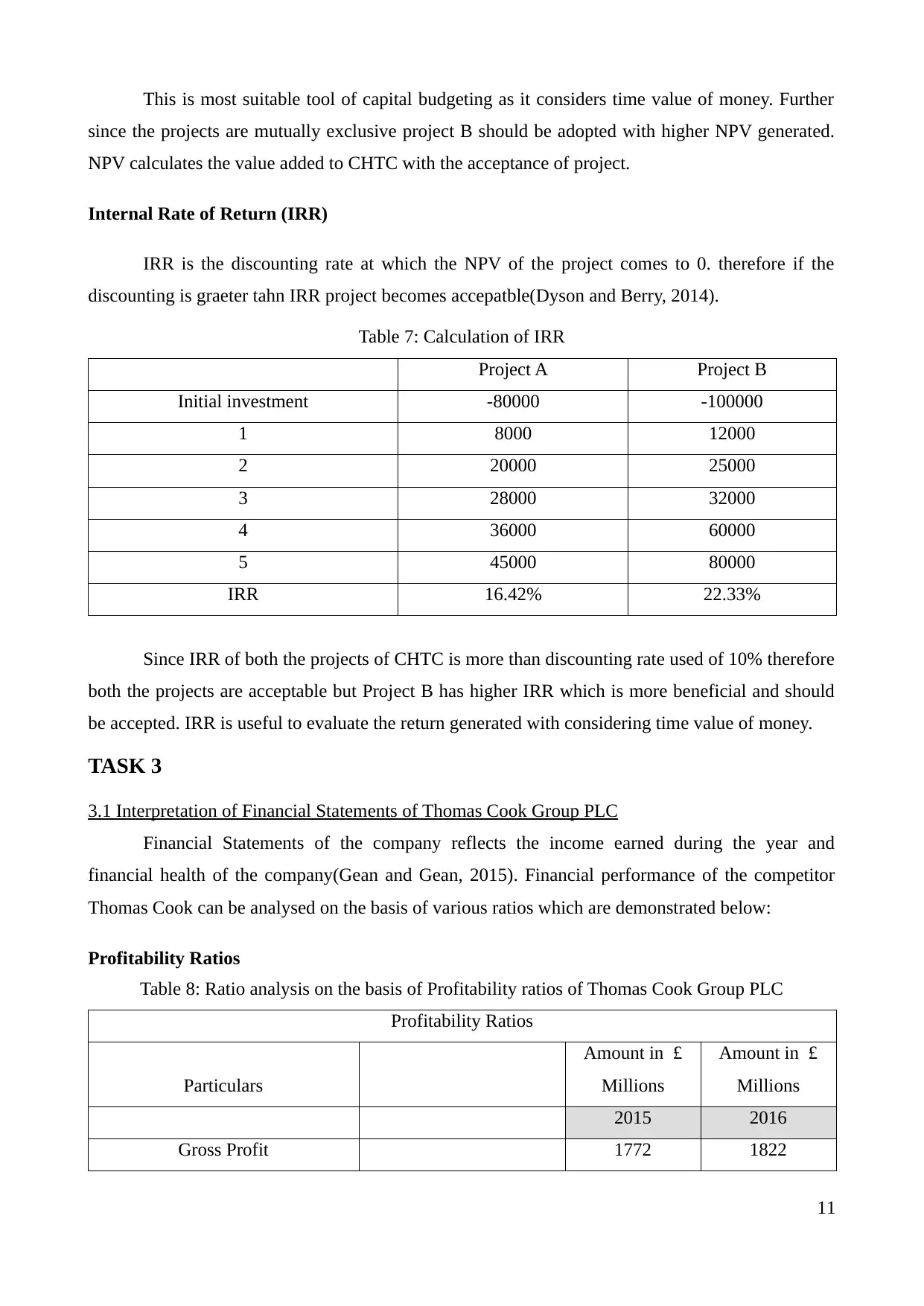

Internal Rate of Return (IRR)

IRR is the discounting rate at which the NPV of the project comes to 0. therefore if the

discounting is graeter tahn IRR project becomes accepatble(Dyson and Berry, 2014).

Table 7: Calculation of IRR

Project A Project B

Initial investment -80000 -100000

1 8000 12000

2 20000 25000

3 28000 32000

4 36000 60000

5 45000 80000

IRR 16.42% 22.33%

Since IRR of both the projects of CHTC is more than discounting rate used of 10% therefore

both the projects are acceptable but Project B has higher IRR which is more beneficial and should

be accepted. IRR is useful to evaluate the return generated with considering time value of money.

TASK 3

3.1 Interpretation of Financial Statements of Thomas Cook Group PLC

Financial Statements of the company reflects the income earned during the year and

financial health of the company(Gean and Gean, 2015). Financial performance of the competitor

Thomas Cook can be analysed on the basis of various ratios which are demonstrated below:

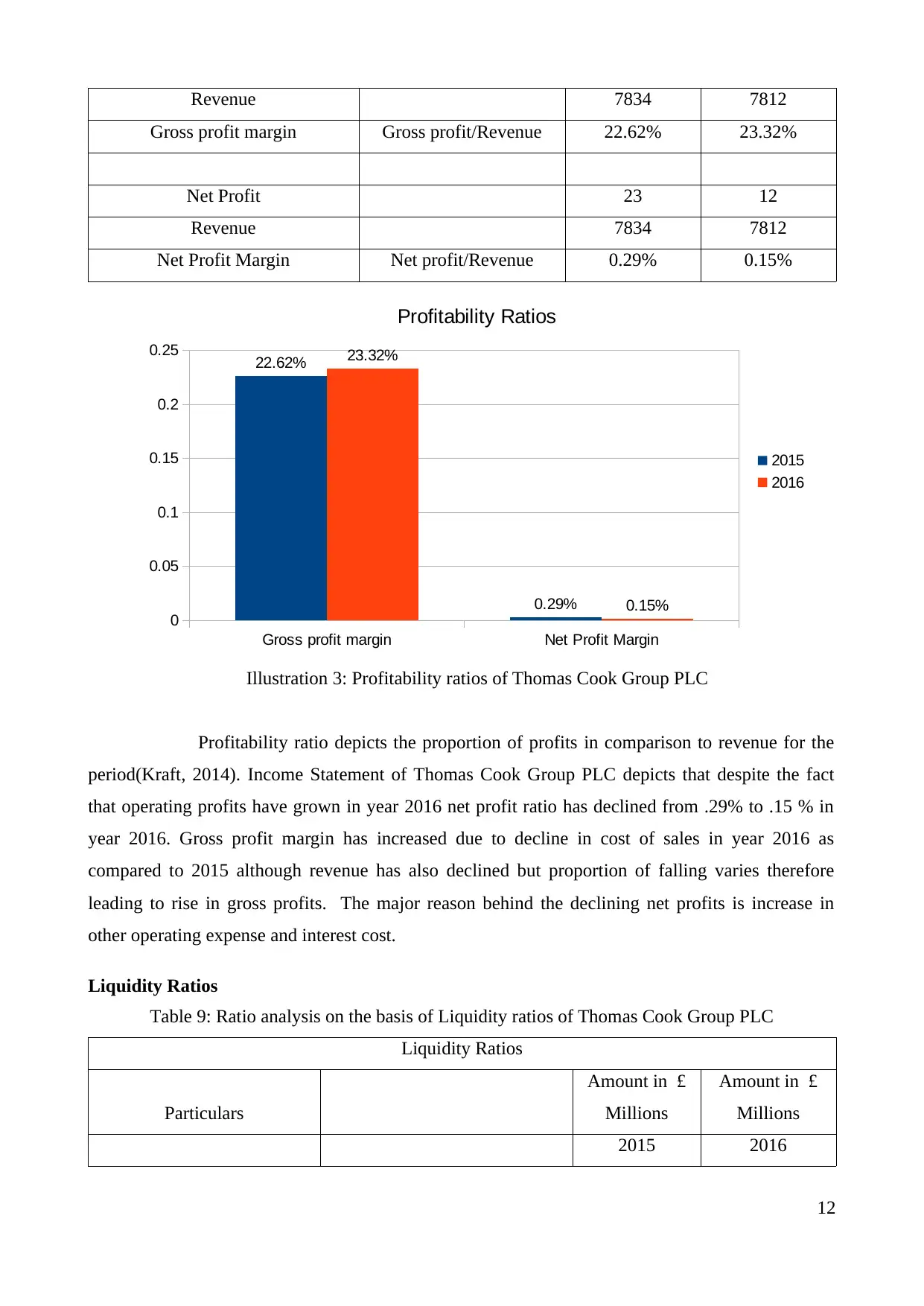

Profitability Ratios

Table 8: Ratio analysis on the basis of Profitability ratios of Thomas Cook Group PLC

Profitability Ratios

Particulars

Amount in £

Millions

Amount in £

Millions

2015 2016

Gross Profit 1772 1822

11

since the projects are mutually exclusive project B should be adopted with higher NPV generated.

NPV calculates the value added to CHTC with the acceptance of project.

Internal Rate of Return (IRR)

IRR is the discounting rate at which the NPV of the project comes to 0. therefore if the

discounting is graeter tahn IRR project becomes accepatble(Dyson and Berry, 2014).

Table 7: Calculation of IRR

Project A Project B

Initial investment -80000 -100000

1 8000 12000

2 20000 25000

3 28000 32000

4 36000 60000

5 45000 80000

IRR 16.42% 22.33%

Since IRR of both the projects of CHTC is more than discounting rate used of 10% therefore

both the projects are acceptable but Project B has higher IRR which is more beneficial and should

be accepted. IRR is useful to evaluate the return generated with considering time value of money.

TASK 3

3.1 Interpretation of Financial Statements of Thomas Cook Group PLC

Financial Statements of the company reflects the income earned during the year and

financial health of the company(Gean and Gean, 2015). Financial performance of the competitor

Thomas Cook can be analysed on the basis of various ratios which are demonstrated below:

Profitability Ratios

Table 8: Ratio analysis on the basis of Profitability ratios of Thomas Cook Group PLC

Profitability Ratios

Particulars

Amount in £

Millions

Amount in £

Millions

2015 2016

Gross Profit 1772 1822

11

Revenue 7834 7812

Gross profit margin Gross profit/Revenue 22.62% 23.32%

Net Profit 23 12

Revenue 7834 7812

Net Profit Margin Net profit/Revenue 0.29% 0.15%

Profitability ratio depicts the proportion of profits in comparison to revenue for the

period(Kraft, 2014). Income Statement of Thomas Cook Group PLC depicts that despite the fact

that operating profits have grown in year 2016 net profit ratio has declined from .29% to .15 % in

year 2016. Gross profit margin has increased due to decline in cost of sales in year 2016 as

compared to 2015 although revenue has also declined but proportion of falling varies therefore

leading to rise in gross profits. The major reason behind the declining net profits is increase in

other operating expense and interest cost.

Liquidity Ratios

Table 9: Ratio analysis on the basis of Liquidity ratios of Thomas Cook Group PLC

Liquidity Ratios

Particulars

Amount in £

Millions

Amount in £

Millions

2015 2016

12

Gross profit margin Net Profit Margin

0

0.05

0.1

0.15

0.2

0.25 22.62%

0.29%

23.32%

0.15%

Profitability Ratios

2015

2016

Illustration 3: Profitability ratios of Thomas Cook Group PLC

Gross profit margin Gross profit/Revenue 22.62% 23.32%

Net Profit 23 12

Revenue 7834 7812

Net Profit Margin Net profit/Revenue 0.29% 0.15%

Profitability ratio depicts the proportion of profits in comparison to revenue for the

period(Kraft, 2014). Income Statement of Thomas Cook Group PLC depicts that despite the fact

that operating profits have grown in year 2016 net profit ratio has declined from .29% to .15 % in

year 2016. Gross profit margin has increased due to decline in cost of sales in year 2016 as

compared to 2015 although revenue has also declined but proportion of falling varies therefore

leading to rise in gross profits. The major reason behind the declining net profits is increase in

other operating expense and interest cost.

Liquidity Ratios

Table 9: Ratio analysis on the basis of Liquidity ratios of Thomas Cook Group PLC

Liquidity Ratios

Particulars

Amount in £

Millions

Amount in £

Millions

2015 2016

12

Gross profit margin Net Profit Margin

0

0.05

0.1

0.15

0.2

0.25 22.62%

0.29%

23.32%

0.15%

Profitability Ratios

2015

2016

Illustration 3: Profitability ratios of Thomas Cook Group PLC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.