Finance and Funding in the Travel and Tourism Sector Report

VerifiedAdded on 2019/12/17

|13

|4190

|165

Report

AI Summary

This report provides a comprehensive analysis of finance and funding within the travel and tourism sector. It begins with an introduction to financial management, emphasizing the importance of costs and volume. The report delves into cost-volume-profit analysis, pricing methods (cost-plus, demand, and competition-based pricing), and factors influencing profitability, such as selling price, costs, sales volume, and market fluctuations. The report further interprets financial statements to assess the financial health of The Restaurant Group (TRG), utilizing ratio analysis as a key tool. Moreover, it explores the sources of finance relevant to the travel and tourism industry, concluding with an overview of the key financial considerations for businesses in this sector. The report uses Merlin Entertainment Plc and The Restaurant Group (TRG) as case studies to illustrate key concepts.

Finance and Funding in the Travel

and Tourism Sector

1

and Tourism Sector

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Importance of costs and volume in financial management of travel and tourism business ..3

1.2 Analysis of pricing methods used in travel and tourism sector ............................................4

1.3 Analysis of factors influencing profit for travel and tourism business .................................5

TASK 2............................................................................................................................................7

TASK 3 ...........................................................................................................................................7

3.1 Interpretation of Financial Statements...................................................................................7

TASK 4..........................................................................................................................................10

4.1 Analysis of Sources of Finance...........................................................................................10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Importance of costs and volume in financial management of travel and tourism business ..3

1.2 Analysis of pricing methods used in travel and tourism sector ............................................4

1.3 Analysis of factors influencing profit for travel and tourism business .................................5

TASK 2............................................................................................................................................7

TASK 3 ...........................................................................................................................................7

3.1 Interpretation of Financial Statements...................................................................................7

TASK 4..........................................................................................................................................10

4.1 Analysis of Sources of Finance...........................................................................................10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION

Finance is at root of every business and growth of business depends on how effectively

the roots are managed. Merlin Entertainments Plc being one of the leading company in leisure

industry with foot prints across major continents. Tourism industry is one of the modern and

highly competitive industry with wide scope of innovation its pattern of providing services. This

report demonstrates the CVP analysis in the tourism industry and its applications. Further

management informations systems are explained with their roles in the decision making process.

Moreover this report lays focus on the sources of finance and their application in the tourism

industry (WisCombe and et.al., 2016). Performance evaluation of one of the leading restaurant

group of UK, The Restaurant Group (TRG) is conducted to assess the financial health of the

company.

TASK 1

1.1 Importance of costs and volume in financial management of travel and tourism business

The major concern of the owner of management is towards determination of the cost that

would be borne in future course of time. Such is required to be predicted on prior basis in order

to cut down the costs. There is presence of several types of costs that are being borne within the

organization of travel and tourism sector (Stewart, 2014). This has been enumerated in the

manner as below:

Variable cost: It is regarded as the cost which is borne by the firm and this changes with the

increase or decrease in the sales volume in the firm such as Merlin Entertainment. It is

considered as one of the essential segment that is being utilized in firm like commission paid to

all the travel agents appointed for the sake of selling all services related with travel. The variable

nature of the services that are being offered would be liable to offer commission to all the agents

who are specifically being appointed for such purpose. The services relating with advertising and

marketing would be incurred by this business so as to attract greater number of customers

towards firm that is Merlin Entertainment as it is faces tough competition from its rivalries in the

market (Ciplet, Roberts and Khan, 2013).

Fixed cost: The rigid expenses are borne within the organization which are not influenced with

the sales volume that is prevailing in the firm. The expenses such as rent space taken on rent for

3

Finance is at root of every business and growth of business depends on how effectively

the roots are managed. Merlin Entertainments Plc being one of the leading company in leisure

industry with foot prints across major continents. Tourism industry is one of the modern and

highly competitive industry with wide scope of innovation its pattern of providing services. This

report demonstrates the CVP analysis in the tourism industry and its applications. Further

management informations systems are explained with their roles in the decision making process.

Moreover this report lays focus on the sources of finance and their application in the tourism

industry (WisCombe and et.al., 2016). Performance evaluation of one of the leading restaurant

group of UK, The Restaurant Group (TRG) is conducted to assess the financial health of the

company.

TASK 1

1.1 Importance of costs and volume in financial management of travel and tourism business

The major concern of the owner of management is towards determination of the cost that

would be borne in future course of time. Such is required to be predicted on prior basis in order

to cut down the costs. There is presence of several types of costs that are being borne within the

organization of travel and tourism sector (Stewart, 2014). This has been enumerated in the

manner as below:

Variable cost: It is regarded as the cost which is borne by the firm and this changes with the

increase or decrease in the sales volume in the firm such as Merlin Entertainment. It is

considered as one of the essential segment that is being utilized in firm like commission paid to

all the travel agents appointed for the sake of selling all services related with travel. The variable

nature of the services that are being offered would be liable to offer commission to all the agents

who are specifically being appointed for such purpose. The services relating with advertising and

marketing would be incurred by this business so as to attract greater number of customers

towards firm that is Merlin Entertainment as it is faces tough competition from its rivalries in the

market (Ciplet, Roberts and Khan, 2013).

Fixed cost: The rigid expenses are borne within the organization which are not influenced with

the sales volume that is prevailing in the firm. The expenses such as rent space taken on rent for

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

establishment of the office is considered as fixed cost that is considered as fixed cots. This is

required to be paid every month whether it is being taken into utilization or it is left idle. The

cost of licensing is also fixed for the business that has to be repaid at specific duration of time

without seeking for the profitability that is earned by business.

Cost volume profit analysis is considered as most common tool that is being used in

management accounting. It has major role in determination of the cost that is borne by the firm in

bringing out the internal potential of the firm through assistance of breakeven point as well as

margin of safety (Huff and Rogers, 2015). The CVP analysis is useful for the management as

such it offers an understanding regarding the effects as well as interrelationship factors that

influence the profitability of the organization. The association among the cost, volume as well as

profit makes up the structure of profit of the business. Thus CVP relationship becomes important

for the budgeting as well as planning of the profitability. Cost volume profit analysis is one that

Merlin Entertainment can use towards figuring out the manner in which changes in the cost as

well as profit affects the operating income and net income. It works through comparison of

varied association like cost of operating as well as production of goods, the amount of goods sold

as well as profit that is being generated from the sales of those products (Inderst, 2013).

1.2 Analysis of pricing methods used in travel and tourism sector

The role of travel and tourism sector has enhanced with the external difficulties

increasing in the external business environment. It is considered as one of the integral parts of

the entire hospitality sector as there is increase in the global exposure of this sector that is

increasing the level of the specific travel and tourism sector. The firm is required to meet varied

quality assurance tools for the purpose of making delivery of quality relates services to all kinds

of customers (Bennett, Naylor and Mellor, 2015). The price sensitiveness can dominate the entire

market through affecting the business in terms of reducing the prices to attract higher customer

base for the product that is being offered by them. The development of varied tour packages is

important for the purpose of adding up extra features so as to lure varied variety of customers.

Pricing is considered as important segment of the standard marketing mix that enhances the

significance of pricing. As such just designing as well as manufacturing of the product is not

adequate until it is being sold to the final target market. The different pricing methods that are

being used by travel and tourism sector are enumerated in the manner stated as under:

4

required to be paid every month whether it is being taken into utilization or it is left idle. The

cost of licensing is also fixed for the business that has to be repaid at specific duration of time

without seeking for the profitability that is earned by business.

Cost volume profit analysis is considered as most common tool that is being used in

management accounting. It has major role in determination of the cost that is borne by the firm in

bringing out the internal potential of the firm through assistance of breakeven point as well as

margin of safety (Huff and Rogers, 2015). The CVP analysis is useful for the management as

such it offers an understanding regarding the effects as well as interrelationship factors that

influence the profitability of the organization. The association among the cost, volume as well as

profit makes up the structure of profit of the business. Thus CVP relationship becomes important

for the budgeting as well as planning of the profitability. Cost volume profit analysis is one that

Merlin Entertainment can use towards figuring out the manner in which changes in the cost as

well as profit affects the operating income and net income. It works through comparison of

varied association like cost of operating as well as production of goods, the amount of goods sold

as well as profit that is being generated from the sales of those products (Inderst, 2013).

1.2 Analysis of pricing methods used in travel and tourism sector

The role of travel and tourism sector has enhanced with the external difficulties

increasing in the external business environment. It is considered as one of the integral parts of

the entire hospitality sector as there is increase in the global exposure of this sector that is

increasing the level of the specific travel and tourism sector. The firm is required to meet varied

quality assurance tools for the purpose of making delivery of quality relates services to all kinds

of customers (Bennett, Naylor and Mellor, 2015). The price sensitiveness can dominate the entire

market through affecting the business in terms of reducing the prices to attract higher customer

base for the product that is being offered by them. The development of varied tour packages is

important for the purpose of adding up extra features so as to lure varied variety of customers.

Pricing is considered as important segment of the standard marketing mix that enhances the

significance of pricing. As such just designing as well as manufacturing of the product is not

adequate until it is being sold to the final target market. The different pricing methods that are

being used by travel and tourism sector are enumerated in the manner stated as under:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost plus profit pricing: It is one of the widely used concept that assists in promoting the

primary aim of the firm that is towards attainment of profit while carrying out the

business operations in fair as well as ethical manner. Under this method a certain

percentage of profit margin is added to the overall cost of product or service. The cost

that is being includes in this is related with cost of designing, cost of rent, visa cost,

accommodation, cost of packaging and eating cost(Minsky, 2015). The tour package is

comprised of varied components that are being joint together. This increases the cost and

thereby affect the selling price of the product and service to a greater extent.

Demand pricing: It is considered as another pricing method wherein the price of product

is being finalized in accordance with the demand. In case demand of the product is higher

an organization can prefer to set higher prices of the product for the purpose of gaining

huge profitability. However in case the demand of the product is less is lower less prices

is being charged for attracting the customers. The success of the demand based pricing is

dependent on the potential of the marketers towards making analysis of the demand. Such

kind of pricing is popular in case of travel industry (Audretsch and et.al., 2016). For

instance, airlines while the period of lower demand charge lesser rates in comparison

with higher demand. Demand based pricing assist the business to earn greater

profitability in case the customers make acceptance of the product at the price more than

its cost.

Competition based pricing: It is considered as another method in which firm takes into

account the prices of the competitors product so as to set the prices of own products. The

firm can charge higher, lower or equal prices in comparison with the prices of

competitors. The aviation industry is regarded as the best example of the competition

based pricing wherein airlines charge the similar or fewer prices of the same routes as it

is being charged by their competitors (Eyckmans, Fankhauser and Kverndokk, 2016).

1.3 Analysis of factors influencing profit for travel and tourism business

The factors that dominates the whole market in beating varied kind of customers who are

influenced towards the reduction in the cost related activities of the business. It acts as an aid in

increasing the business through upliftment of the present status towards the higher position

within the market. Such achievement can be earned by means of making important changes

5

primary aim of the firm that is towards attainment of profit while carrying out the

business operations in fair as well as ethical manner. Under this method a certain

percentage of profit margin is added to the overall cost of product or service. The cost

that is being includes in this is related with cost of designing, cost of rent, visa cost,

accommodation, cost of packaging and eating cost(Minsky, 2015). The tour package is

comprised of varied components that are being joint together. This increases the cost and

thereby affect the selling price of the product and service to a greater extent.

Demand pricing: It is considered as another pricing method wherein the price of product

is being finalized in accordance with the demand. In case demand of the product is higher

an organization can prefer to set higher prices of the product for the purpose of gaining

huge profitability. However in case the demand of the product is less is lower less prices

is being charged for attracting the customers. The success of the demand based pricing is

dependent on the potential of the marketers towards making analysis of the demand. Such

kind of pricing is popular in case of travel industry (Audretsch and et.al., 2016). For

instance, airlines while the period of lower demand charge lesser rates in comparison

with higher demand. Demand based pricing assist the business to earn greater

profitability in case the customers make acceptance of the product at the price more than

its cost.

Competition based pricing: It is considered as another method in which firm takes into

account the prices of the competitors product so as to set the prices of own products. The

firm can charge higher, lower or equal prices in comparison with the prices of

competitors. The aviation industry is regarded as the best example of the competition

based pricing wherein airlines charge the similar or fewer prices of the same routes as it

is being charged by their competitors (Eyckmans, Fankhauser and Kverndokk, 2016).

1.3 Analysis of factors influencing profit for travel and tourism business

The factors that dominates the whole market in beating varied kind of customers who are

influenced towards the reduction in the cost related activities of the business. It acts as an aid in

increasing the business through upliftment of the present status towards the higher position

within the market. Such achievement can be earned by means of making important changes

5

within the external market that is combination of varied factors that are influencing the present

performance of the organization. The firm is required to take into account several factors that

would act as an aid for the organization in enhancing their present financial situation. There is

presence of numerous factors that affects the business yield in positive or negative manner. The

factor that would affect the profit for travel and tourism business are enumerated in the manner

stated as under: Selling price: Merlin Entertainment Plc is able to generation of revenues by means of

delivering accommodation, hotel, meal and other entertainment such as rides, shows to

the target market. Therefore selling price is considered most important component that is

influencing the profitability as higher selling price is contributing towards grown

revenues or vice versa (Clark and Das, 2015). At the similar point of time it is required to

be emphasized that higher prices affects the profitability in negative aspect specifically in

situation when Merlin Entertainment's competition are offers services a cheaper rates.

Therefore it can be stated that keeping other factors as constant higher prices results in

decreasing the total sales of the business and vice versa. Cost of goods as well as services: Profit is being assessed through subtraction of the total

cost from the organization's turnover. Therefore cost is regarded as another essential

element that has greater impact on Merlin Entertainment Plc. Greater is the cost of the

product it result in decreasing the net earning. However in case the company is able to

keep control over its expenses then it can effectively maximize its profitability in long

run course of time (Staveren, 2013). Therefore it is being suggested to Merlin

Entertainment Plc to decrease its operational spendings by means of monitoring on

regular basis by the means of budget and this leads to enhancing the return position to a

significant level. In this regard greater output assist in decreasing the cost per unit

because of the economies of scale. This leads to increasing the earnings of the firm in an

effective manner. Volume of sales: Higher the number of sales units, keeping other factors as constant it

would assist Merlin Entertainment Plc in maximizing the net profitability. The reason

beside this is that in case Merlin Entertainment is able towards attracting greater number

of visitors and make delivery of services in greater quantity then it would be able to make

6

performance of the organization. The firm is required to take into account several factors that

would act as an aid for the organization in enhancing their present financial situation. There is

presence of numerous factors that affects the business yield in positive or negative manner. The

factor that would affect the profit for travel and tourism business are enumerated in the manner

stated as under: Selling price: Merlin Entertainment Plc is able to generation of revenues by means of

delivering accommodation, hotel, meal and other entertainment such as rides, shows to

the target market. Therefore selling price is considered most important component that is

influencing the profitability as higher selling price is contributing towards grown

revenues or vice versa (Clark and Das, 2015). At the similar point of time it is required to

be emphasized that higher prices affects the profitability in negative aspect specifically in

situation when Merlin Entertainment's competition are offers services a cheaper rates.

Therefore it can be stated that keeping other factors as constant higher prices results in

decreasing the total sales of the business and vice versa. Cost of goods as well as services: Profit is being assessed through subtraction of the total

cost from the organization's turnover. Therefore cost is regarded as another essential

element that has greater impact on Merlin Entertainment Plc. Greater is the cost of the

product it result in decreasing the net earning. However in case the company is able to

keep control over its expenses then it can effectively maximize its profitability in long

run course of time (Staveren, 2013). Therefore it is being suggested to Merlin

Entertainment Plc to decrease its operational spendings by means of monitoring on

regular basis by the means of budget and this leads to enhancing the return position to a

significant level. In this regard greater output assist in decreasing the cost per unit

because of the economies of scale. This leads to increasing the earnings of the firm in an

effective manner. Volume of sales: Higher the number of sales units, keeping other factors as constant it

would assist Merlin Entertainment Plc in maximizing the net profitability. The reason

beside this is that in case Merlin Entertainment is able towards attracting greater number

of visitors and make delivery of services in greater quantity then it would be able to make

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

generation greater revenue at the similar level of the cost. Thus it acts as an aid in

increasing the profitability.

Market fluctuations: The hospitality industry success to a greater extent is based on the

level of the customer satisfaction. While within the market wider range of fluctuations

can be viewed with respect to customer taste, preferences as well as attitude. Therefore

Merlin Entertainment would be influenced by the seasonal variations as well as

alterations in the social preferences. Further the alterations within the political rules as

well as regulations and the economic condition influence the profitability of organization

to a significant level (McCann, 2014).

Therefore after taking into consideration all the components it can be suggested that

manager of Merlin Entertainment Plc needs to increase the sales and selling price upto a level

that is accepted. Further it is required to keep track on their routine expenses in order to

minimize the cost as well as increase the profitability to a significant level.

TASK 2

Covered in PPT

TASK 3

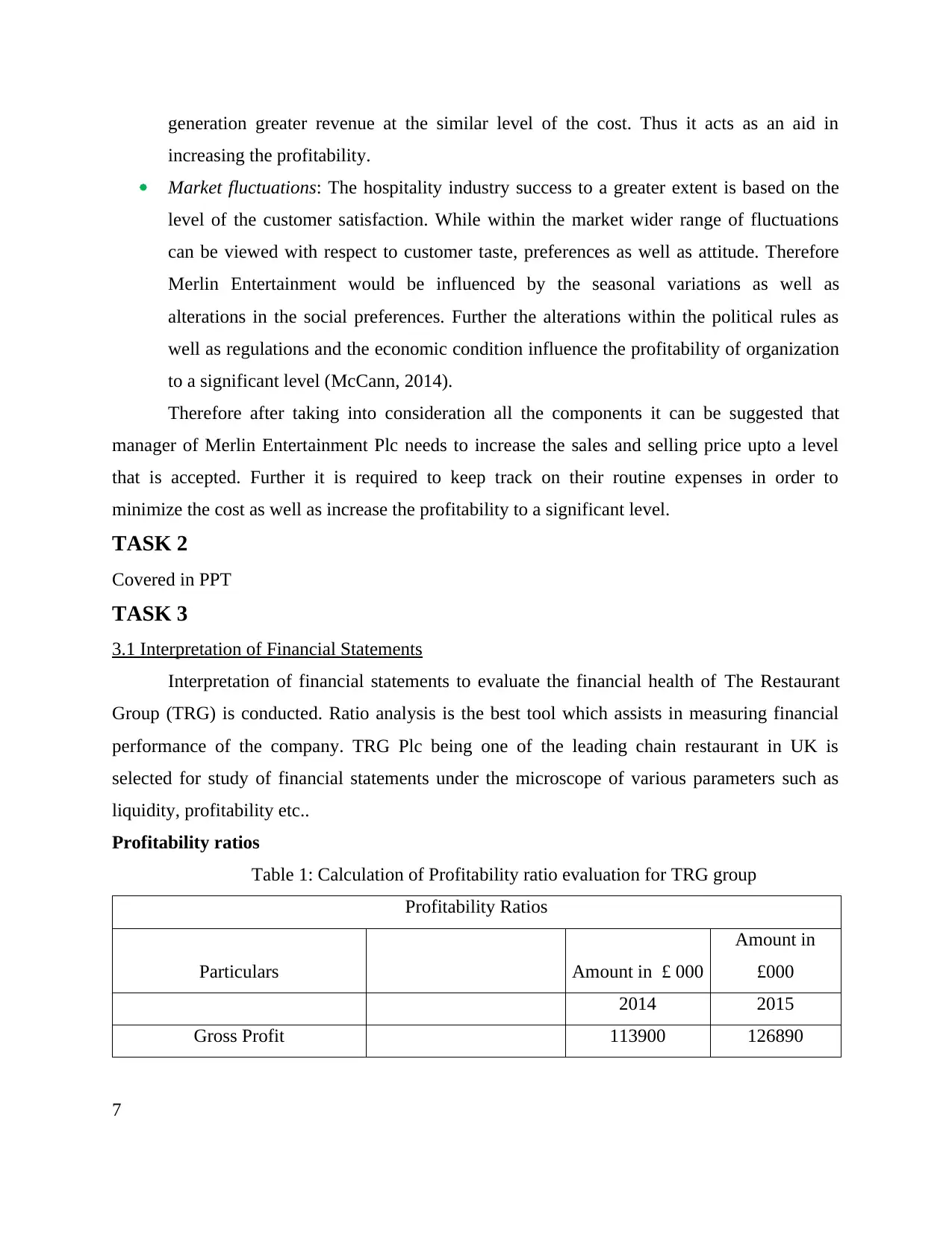

3.1 Interpretation of Financial Statements

Interpretation of financial statements to evaluate the financial health of The Restaurant

Group (TRG) is conducted. Ratio analysis is the best tool which assists in measuring financial

performance of the company. TRG Plc being one of the leading chain restaurant in UK is

selected for study of financial statements under the microscope of various parameters such as

liquidity, profitability etc..

Profitability ratios

Table 1: Calculation of Profitability ratio evaluation for TRG group

Profitability Ratios

Particulars Amount in £ 000

Amount in

£000

2014 2015

Gross Profit 113900 126890

7

increasing the profitability.

Market fluctuations: The hospitality industry success to a greater extent is based on the

level of the customer satisfaction. While within the market wider range of fluctuations

can be viewed with respect to customer taste, preferences as well as attitude. Therefore

Merlin Entertainment would be influenced by the seasonal variations as well as

alterations in the social preferences. Further the alterations within the political rules as

well as regulations and the economic condition influence the profitability of organization

to a significant level (McCann, 2014).

Therefore after taking into consideration all the components it can be suggested that

manager of Merlin Entertainment Plc needs to increase the sales and selling price upto a level

that is accepted. Further it is required to keep track on their routine expenses in order to

minimize the cost as well as increase the profitability to a significant level.

TASK 2

Covered in PPT

TASK 3

3.1 Interpretation of Financial Statements

Interpretation of financial statements to evaluate the financial health of The Restaurant

Group (TRG) is conducted. Ratio analysis is the best tool which assists in measuring financial

performance of the company. TRG Plc being one of the leading chain restaurant in UK is

selected for study of financial statements under the microscope of various parameters such as

liquidity, profitability etc..

Profitability ratios

Table 1: Calculation of Profitability ratio evaluation for TRG group

Profitability Ratios

Particulars Amount in £ 000

Amount in

£000

2014 2015

Gross Profit 113900 126890

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue 635225 685381

Gross profit margin Gross profit/Revenue 17.93% 18.51%

Net Profit 66999 68886

Revenue 635225 685381

Net Profit Margin Net profit/Revenue 10.55% 10.05%

Profitability ratio depicts the proportion of profits to the total revenue of the company

from operations. Gross profit ratio has increased for TRG group as both the gross profits and

revenues have raised in year 2015 as compared to year 2014. Net profit ratio depicts proportion

between the total profits generated after considering interest and taxes and the revenues

generated by the business (Vazquez and Federico, 2015). Despite increase in revenue net profit

has declined due to significant increase in depreciation. As Property, plant and equipments have

increased thereby hiking depreciation which in turn reduced net profits for year 2015.

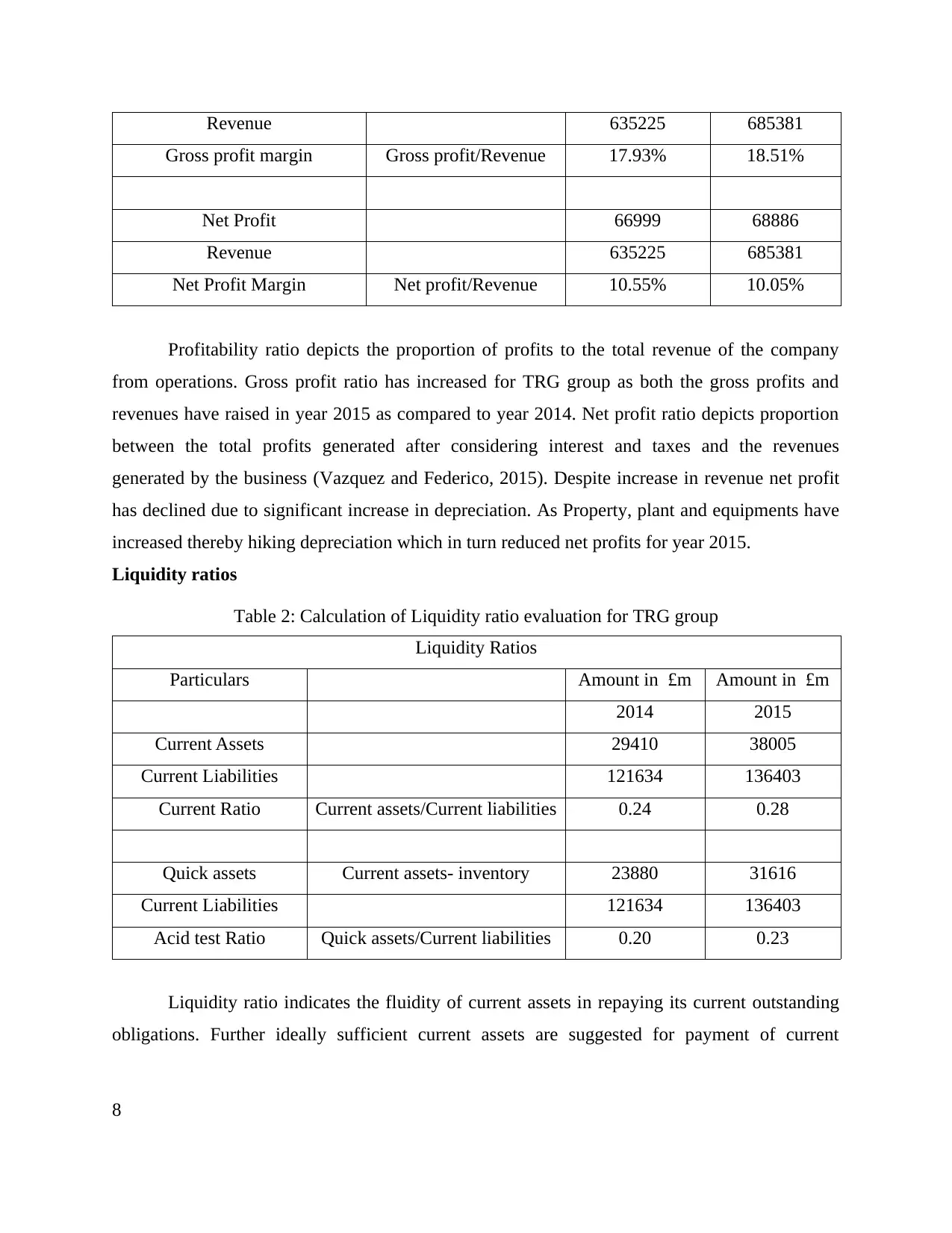

Liquidity ratios

Table 2: Calculation of Liquidity ratio evaluation for TRG group

Liquidity Ratios

Particulars Amount in £m Amount in £m

2014 2015

Current Assets 29410 38005

Current Liabilities 121634 136403

Current Ratio Current assets/Current liabilities 0.24 0.28

Quick assets Current assets- inventory 23880 31616

Current Liabilities 121634 136403

Acid test Ratio Quick assets/Current liabilities 0.20 0.23

Liquidity ratio indicates the fluidity of current assets in repaying its current outstanding

obligations. Further ideally sufficient current assets are suggested for payment of current

8

Gross profit margin Gross profit/Revenue 17.93% 18.51%

Net Profit 66999 68886

Revenue 635225 685381

Net Profit Margin Net profit/Revenue 10.55% 10.05%

Profitability ratio depicts the proportion of profits to the total revenue of the company

from operations. Gross profit ratio has increased for TRG group as both the gross profits and

revenues have raised in year 2015 as compared to year 2014. Net profit ratio depicts proportion

between the total profits generated after considering interest and taxes and the revenues

generated by the business (Vazquez and Federico, 2015). Despite increase in revenue net profit

has declined due to significant increase in depreciation. As Property, plant and equipments have

increased thereby hiking depreciation which in turn reduced net profits for year 2015.

Liquidity ratios

Table 2: Calculation of Liquidity ratio evaluation for TRG group

Liquidity Ratios

Particulars Amount in £m Amount in £m

2014 2015

Current Assets 29410 38005

Current Liabilities 121634 136403

Current Ratio Current assets/Current liabilities 0.24 0.28

Quick assets Current assets- inventory 23880 31616

Current Liabilities 121634 136403

Acid test Ratio Quick assets/Current liabilities 0.20 0.23

Liquidity ratio indicates the fluidity of current assets in repaying its current outstanding

obligations. Further ideally sufficient current assets are suggested for payment of current

8

liabilities which is not present in TRG Group. TRG group lacks the current assets in comparison

to current liabilities. In year 2015 situation has improved but corrective measures should be

taken to reduce the current liabilities and remarkable increase in current assets to bring fluidity

into business. Quick ratio shows the adequacy of quick assets to repay immediate liabilities

however inventory is excluded from current assets because it takes considerable time to convert

itself into cash (Damodaran, 2015).

Gearing ratios

Table 3: Calculation of Leverage ratios for TRG group

Leverage Ratios

Particulars Amount in £m Amount in £m

2014 2015

Long term debt 39458 30527

Equity 244524 283560

Debt Equity Ratio Long term debt/Equity 0.16 0.11

Earnings before interest and tax

(EBIT) 87415 88973

interest cost 2488 2128

Interest coverage ratio EBIT/ Interest cost 35.13 41.81

Gearing ratio measures the combination of equity and long term funds to finance the long

term assets of business. Equity capital has increased in year 2015 therefore improving the ratio.

However more debt can be raised as debt is cheaper than equity. Interest coverage ratio depicts

the adequacy of the earnings of the firm to cover the interest expense on the financial loans

acquired (Ufen and Mietzner, 2015). With the increase in loans interest expense will increase.

TRG has repaid loans therefore decreasing the interest liability and resulting into better interest

coverage ratio in year 2015.

Investment ratios

9

to current liabilities. In year 2015 situation has improved but corrective measures should be

taken to reduce the current liabilities and remarkable increase in current assets to bring fluidity

into business. Quick ratio shows the adequacy of quick assets to repay immediate liabilities

however inventory is excluded from current assets because it takes considerable time to convert

itself into cash (Damodaran, 2015).

Gearing ratios

Table 3: Calculation of Leverage ratios for TRG group

Leverage Ratios

Particulars Amount in £m Amount in £m

2014 2015

Long term debt 39458 30527

Equity 244524 283560

Debt Equity Ratio Long term debt/Equity 0.16 0.11

Earnings before interest and tax

(EBIT) 87415 88973

interest cost 2488 2128

Interest coverage ratio EBIT/ Interest cost 35.13 41.81

Gearing ratio measures the combination of equity and long term funds to finance the long

term assets of business. Equity capital has increased in year 2015 therefore improving the ratio.

However more debt can be raised as debt is cheaper than equity. Interest coverage ratio depicts

the adequacy of the earnings of the firm to cover the interest expense on the financial loans

acquired (Ufen and Mietzner, 2015). With the increase in loans interest expense will increase.

TRG has repaid loans therefore decreasing the interest liability and resulting into better interest

coverage ratio in year 2015.

Investment ratios

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Table 4: Calculation of Investment ratios for TRG group

Investment Ratios

Particulars Amount in £m Amount in £m

2014 2015

Earnings available for equity

shareholders 66999 68886

No of equity shares 200648821 200950672

Earnings Per Share

Earnings for equity

shareholders/No. of equity

shares 0.33 0.34

Dividends per share 0.18 0.16

EPS 0.33 0.34

Dividend Payout ratios Dividends/EPS 0.54 0.47

Investment ratios are calculated by existing and potential investor for decision making.

These ratios will help investor to decide whether to buy, sell or hold shares of the company. EPS

ratio depicts return earned by each shareholder on the money invested in the company. EPS is

showing growing trend which is beneficial for shareholders. Besides the increase in Earnings per

share dividend is reduced due to some investment projects in pipeline therefore declining the

dividend payout ratio (Steinitz and Field, 2014). Dividend payout ratio depicts that out of total

earnings for the shareholders how much potion is distributed as dividends and how much is

retained into business.

Turnover ratios

Table 5: Calculation of Turnover Ratios for TRG group

Turnover Ratios

Particulars Amount in £m Amount in £m

2014 2015

Revenue 635225 685381

10

Investment Ratios

Particulars Amount in £m Amount in £m

2014 2015

Earnings available for equity

shareholders 66999 68886

No of equity shares 200648821 200950672

Earnings Per Share

Earnings for equity

shareholders/No. of equity

shares 0.33 0.34

Dividends per share 0.18 0.16

EPS 0.33 0.34

Dividend Payout ratios Dividends/EPS 0.54 0.47

Investment ratios are calculated by existing and potential investor for decision making.

These ratios will help investor to decide whether to buy, sell or hold shares of the company. EPS

ratio depicts return earned by each shareholder on the money invested in the company. EPS is

showing growing trend which is beneficial for shareholders. Besides the increase in Earnings per

share dividend is reduced due to some investment projects in pipeline therefore declining the

dividend payout ratio (Steinitz and Field, 2014). Dividend payout ratio depicts that out of total

earnings for the shareholders how much potion is distributed as dividends and how much is

retained into business.

Turnover ratios

Table 5: Calculation of Turnover Ratios for TRG group

Turnover Ratios

Particulars Amount in £m Amount in £m

2014 2015

Revenue 635225 685381

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total assets 424419.00 468078.00

Asset turnover Ratio Revenue/Average total assets 1.50 1.46

Turnover ratio demonstrates the efficiency of assets employed in the business to generate

the revenues. Revenues have increased however increase in investments in total assets is greater

than rise in revenue thereby declining the asset turnover ratio. This implies that revenues

generated are 1.46 times of total assets employed in the TRG group.

TASK 4

4.1 Analysis of Sources of Finance

Tourism industry is most challenging industry as the customer needs are the prime focus.

Customer is god as they are the ultimate consumers of the service provided (Crépey, Brigo and

Bielecki, 2013). Further Merlin Plc is a company with high growth perspective and therefore is

expanding on regular basis. Huge financial funds are required for financing the capital projects

and decisions. Some of the major financial sources are listed below:

Debt Funds : Debt funds refers to loans or financial assistance from financial

institutions, non conventional lenders, credit unions or private funding companies.

However various factors are to be considered before accepting debt as sources of finance.

Merlin's top management should pay great emphasis towards tax and interest

implications of borrowed funds(Knoeppel and Della Sala, 2015). Debt funds have

scheduled repayments which affects the liquidity of the firm. Moreover interest has tax

benefits attached with it. Debt is cheaper source of finance but has high financial risk.

Equity Funds : Merlin finance can raise funds to finance the huge capital projects with

the help of issuing equity in the public. Further equity has risk of dilution of control and

caries high cost of capital(Gatti, 2013). Equity funds have share in profits in the form of

dividends. However equity has no implications or conditions regarding repayment

therefore good source of finance. However company can even utilise retained earnings to

generate further income by investing the money into new ventures.

Government Grants : Government grants can be in form of loans or tax holidays or

granting of funds for supporting the industry. Government supports tourism industry

widely as it is highly profitable and opens new ventures inviting foreign direct

11

Asset turnover Ratio Revenue/Average total assets 1.50 1.46

Turnover ratio demonstrates the efficiency of assets employed in the business to generate

the revenues. Revenues have increased however increase in investments in total assets is greater

than rise in revenue thereby declining the asset turnover ratio. This implies that revenues

generated are 1.46 times of total assets employed in the TRG group.

TASK 4

4.1 Analysis of Sources of Finance

Tourism industry is most challenging industry as the customer needs are the prime focus.

Customer is god as they are the ultimate consumers of the service provided (Crépey, Brigo and

Bielecki, 2013). Further Merlin Plc is a company with high growth perspective and therefore is

expanding on regular basis. Huge financial funds are required for financing the capital projects

and decisions. Some of the major financial sources are listed below:

Debt Funds : Debt funds refers to loans or financial assistance from financial

institutions, non conventional lenders, credit unions or private funding companies.

However various factors are to be considered before accepting debt as sources of finance.

Merlin's top management should pay great emphasis towards tax and interest

implications of borrowed funds(Knoeppel and Della Sala, 2015). Debt funds have

scheduled repayments which affects the liquidity of the firm. Moreover interest has tax

benefits attached with it. Debt is cheaper source of finance but has high financial risk.

Equity Funds : Merlin finance can raise funds to finance the huge capital projects with

the help of issuing equity in the public. Further equity has risk of dilution of control and

caries high cost of capital(Gatti, 2013). Equity funds have share in profits in the form of

dividends. However equity has no implications or conditions regarding repayment

therefore good source of finance. However company can even utilise retained earnings to

generate further income by investing the money into new ventures.

Government Grants : Government grants can be in form of loans or tax holidays or

granting of funds for supporting the industry. Government supports tourism industry

widely as it is highly profitable and opens new ventures inviting foreign direct

11

investments. However most of the government programs have entry and exit dates and

regulations attached which needs to be followed strictly. To enjoy the government grants

Merlin Plc should apply and present the exact and clear picture of the company and put

great efforts to gain the advantage under government schemes (Binks and Ennew, 2016).

CONCLUSION

As per the detailed analysis of Tourism industry under financial microscope it can be

concluded that CVP plays major role in setting the prices and controlling the cost. Further it can

be inferred from the report that management information tools present in the company provide

major assistance to Merlin Plc in finalising various decision regarding expansion and future

growth. Moreover debt can be treated as cheaper source of funds for funding thee expansion

project . However affecting the liquidity in business. Moreover financial performance of leading

restaurant group in UK is appreciable, despite the liquidity crunch faced by it although it is

growing in terms of magnitude in serving number of customers and profits.

12

regulations attached which needs to be followed strictly. To enjoy the government grants

Merlin Plc should apply and present the exact and clear picture of the company and put

great efforts to gain the advantage under government schemes (Binks and Ennew, 2016).

CONCLUSION

As per the detailed analysis of Tourism industry under financial microscope it can be

concluded that CVP plays major role in setting the prices and controlling the cost. Further it can

be inferred from the report that management information tools present in the company provide

major assistance to Merlin Plc in finalising various decision regarding expansion and future

growth. Moreover debt can be treated as cheaper source of funds for funding thee expansion

project . However affecting the liquidity in business. Moreover financial performance of leading

restaurant group in UK is appreciable, despite the liquidity crunch faced by it although it is

growing in terms of magnitude in serving number of customers and profits.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.