Finance and Funding in the Travel and Tourism Sector: Report Analysis

VerifiedAdded on 2020/07/23

|19

|5600

|28

Report

AI Summary

This report examines the crucial role of finance in the travel and tourism sector, focusing on Eurocarib Tours, a London-based tour operator. It delves into Cost-Volume-Profit (CVP) analysis, exploring its importance in decision-making, including contribution margin, operating income, desired sales volume, and break-even points. The report also analyzes various pricing methods such as cost-centered, competitive, demand-based, target return, seasonal, and going-rate pricing. Furthermore, it identifies factors affecting the travel and tourism business, including seasonal variations, economic and political environments, social factors, and staffing. The report also assesses management accounting tools like budgeting and investment appraisal. Finally, it analyzes financial statements and potential funding sources for business development, including detailed financial ratio analysis and recommendations for improved financial performance. The report concludes by evaluating various funding options that a firm can obtain for developing a new hotel.

Finance and Funding in the Travel and

Tourism Sector

Tourism Sector

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................................1

TASK 1..........................................................................................................................................................1

A. Examine the concept of CVP analysis and its importance...................................................................1

B. Pricing methods...................................................................................................................................3

1.3 Analysis of factors affecting travel and tourism business..................................................................4

2.1 Different type of management accounting information that can be used in the business...................5

2.2 Assessing the use of investment appraisal techniques as a decision making tool.............................7

TASK 3..........................................................................................................................................................8

Analyzing financial statements of Thomas Cook.....................................................................................8

TASK 4........................................................................................................................................................13

Analyzing sources of funding that can be obtained by firm for developing new hotel..........................13

CONCLUSION.............................................................................................................................................15

REFERENCES..............................................................................................................................................16

INTRODUCTION...........................................................................................................................................1

TASK 1..........................................................................................................................................................1

A. Examine the concept of CVP analysis and its importance...................................................................1

B. Pricing methods...................................................................................................................................3

1.3 Analysis of factors affecting travel and tourism business..................................................................4

2.1 Different type of management accounting information that can be used in the business...................5

2.2 Assessing the use of investment appraisal techniques as a decision making tool.............................7

TASK 3..........................................................................................................................................................8

Analyzing financial statements of Thomas Cook.....................................................................................8

TASK 4........................................................................................................................................................13

Analyzing sources of funding that can be obtained by firm for developing new hotel..........................13

CONCLUSION.............................................................................................................................................15

REFERENCES..............................................................................................................................................16

INTRODUCTION

Finance is the crucial and highly important requirement of every business because none

of the enterprise can operate in tough market with lack of access to sufficient fund. Not only the

fund collection is sufficient but also needs to be managed, supervised and administrated strongly

to achieve set financial goals. EUROCARIB TOURS is a London-based tour operator that

launches various trips and tours at the attractive tourist destinations all over the world. Company

provide luxury facilities to all the visitors to provide them a wonderful travelling experience. The

current research study aims at examining the key aspects of business success including pricing

and factors that affect business profitability. Moreover, it will examine the key managerial tools

like cost-volume-profit analysis, investment appraisal and other methods of management

accounting which cited organization can use for growth. Despite this, in order to examine

financial success or health of the organization, a number of quantitative ratios including

liquidity, solvency and profitability will be compute and accordingly, firm will be suggest to use

new tactics to improve their financial performance. Lastly, various sources from where tour

operator can generate funds will be critically evaluated.

TASK 1

1.1 Examine the concept of CVP analysis and its importance

Cost-Volume-Profit-Analysis (CVP) is an important tool of cost accounting that gains

crucial importance for the short-term management decisions. The method is used by the

companies to assess that how changes in various costs elements, selling prices and sales volume

will influence bottom line of the business. The method believes that various costs of the

company can be classified into fixed or variable cost elements including manufacturing,

administrative, marketing and others (Choo and Tan, 2011). As per the case, a major tour

operator in London, named EUROCARIB TOURS is keen to invest in a summer holiday trip at

Caribbean Holiday Resort lasting 4-week. In order to serve customers with the luxury facilities,

it book hotel and airplane for the users. Here, CVP analysis is helpful for the company to

perform sensitivity analysis means how its net profitability will be influenced by number of

1

Finance is the crucial and highly important requirement of every business because none

of the enterprise can operate in tough market with lack of access to sufficient fund. Not only the

fund collection is sufficient but also needs to be managed, supervised and administrated strongly

to achieve set financial goals. EUROCARIB TOURS is a London-based tour operator that

launches various trips and tours at the attractive tourist destinations all over the world. Company

provide luxury facilities to all the visitors to provide them a wonderful travelling experience. The

current research study aims at examining the key aspects of business success including pricing

and factors that affect business profitability. Moreover, it will examine the key managerial tools

like cost-volume-profit analysis, investment appraisal and other methods of management

accounting which cited organization can use for growth. Despite this, in order to examine

financial success or health of the organization, a number of quantitative ratios including

liquidity, solvency and profitability will be compute and accordingly, firm will be suggest to use

new tactics to improve their financial performance. Lastly, various sources from where tour

operator can generate funds will be critically evaluated.

TASK 1

1.1 Examine the concept of CVP analysis and its importance

Cost-Volume-Profit-Analysis (CVP) is an important tool of cost accounting that gains

crucial importance for the short-term management decisions. The method is used by the

companies to assess that how changes in various costs elements, selling prices and sales volume

will influence bottom line of the business. The method believes that various costs of the

company can be classified into fixed or variable cost elements including manufacturing,

administrative, marketing and others (Choo and Tan, 2011). As per the case, a major tour

operator in London, named EUROCARIB TOURS is keen to invest in a summer holiday trip at

Caribbean Holiday Resort lasting 4-week. In order to serve customers with the luxury facilities,

it book hotel and airplane for the users. Here, CVP analysis is helpful for the company to

perform sensitivity analysis means how its net profitability will be influenced by number of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

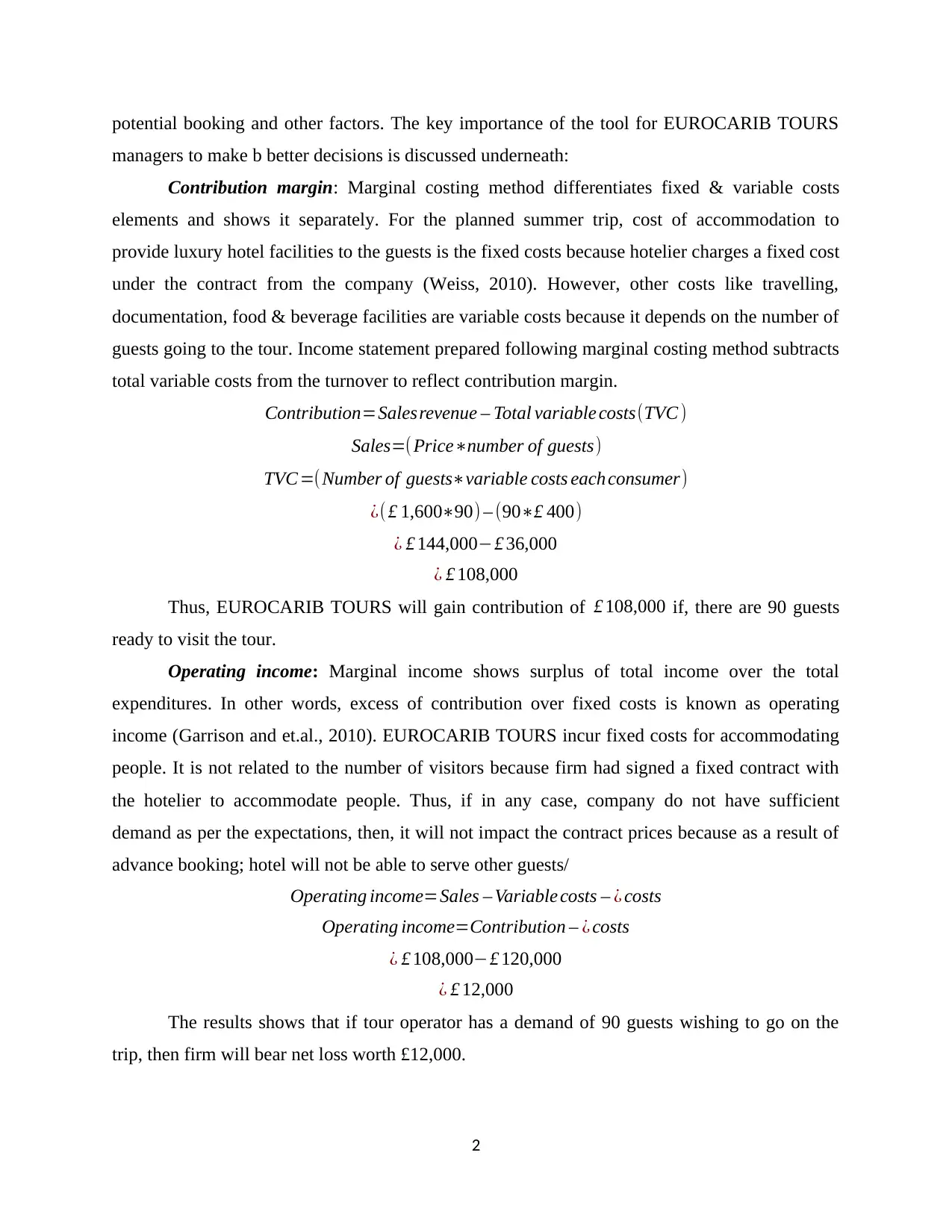

potential booking and other factors. The key importance of the tool for EUROCARIB TOURS

managers to make b better decisions is discussed underneath:

Contribution margin: Marginal costing method differentiates fixed & variable costs

elements and shows it separately. For the planned summer trip, cost of accommodation to

provide luxury hotel facilities to the guests is the fixed costs because hotelier charges a fixed cost

under the contract from the company (Weiss, 2010). However, other costs like travelling,

documentation, food & beverage facilities are variable costs because it depends on the number of

guests going to the tour. Income statement prepared following marginal costing method subtracts

total variable costs from the turnover to reflect contribution margin.

Contribution=Salesrevenue – Total variable costs(TVC )

Sales=(Price∗number of guests)

TVC =(Number of guests∗variable costs each consumer)

¿( £ 1,600∗90) – (90∗£ 400)

¿ £ 144,000−£ 36,000

¿ £ 108,000

Thus, EUROCARIB TOURS will gain contribution of £ 108,000 if, there are 90 guests

ready to visit the tour.

Operating income: Marginal income shows surplus of total income over the total

expenditures. In other words, excess of contribution over fixed costs is known as operating

income (Garrison and et.al., 2010). EUROCARIB TOURS incur fixed costs for accommodating

people. It is not related to the number of visitors because firm had signed a fixed contract with

the hotelier to accommodate people. Thus, if in any case, company do not have sufficient

demand as per the expectations, then, it will not impact the contract prices because as a result of

advance booking; hotel will not be able to serve other guests/

Operating income=Sales – Variable costs – ¿ costs

Operating income=Contribution – ¿ costs

¿ £ 108,000−£ 120,000

¿ £ 12,000

The results shows that if tour operator has a demand of 90 guests wishing to go on the

trip, then firm will bear net loss worth £12,000.

2

managers to make b better decisions is discussed underneath:

Contribution margin: Marginal costing method differentiates fixed & variable costs

elements and shows it separately. For the planned summer trip, cost of accommodation to

provide luxury hotel facilities to the guests is the fixed costs because hotelier charges a fixed cost

under the contract from the company (Weiss, 2010). However, other costs like travelling,

documentation, food & beverage facilities are variable costs because it depends on the number of

guests going to the tour. Income statement prepared following marginal costing method subtracts

total variable costs from the turnover to reflect contribution margin.

Contribution=Salesrevenue – Total variable costs(TVC )

Sales=(Price∗number of guests)

TVC =(Number of guests∗variable costs each consumer)

¿( £ 1,600∗90) – (90∗£ 400)

¿ £ 144,000−£ 36,000

¿ £ 108,000

Thus, EUROCARIB TOURS will gain contribution of £ 108,000 if, there are 90 guests

ready to visit the tour.

Operating income: Marginal income shows surplus of total income over the total

expenditures. In other words, excess of contribution over fixed costs is known as operating

income (Garrison and et.al., 2010). EUROCARIB TOURS incur fixed costs for accommodating

people. It is not related to the number of visitors because firm had signed a fixed contract with

the hotelier to accommodate people. Thus, if in any case, company do not have sufficient

demand as per the expectations, then, it will not impact the contract prices because as a result of

advance booking; hotel will not be able to serve other guests/

Operating income=Sales – Variable costs – ¿ costs

Operating income=Contribution – ¿ costs

¿ £ 108,000−£ 120,000

¿ £ 12,000

The results shows that if tour operator has a demand of 90 guests wishing to go on the

trip, then firm will bear net loss worth £12,000.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Desired sales volume: One of the another key benefit associated with the CVP analysis is

that it enable formulators to clearly set the target sales volume which generates expected return

(Pavlatos and Paggios, 2009).

Desired sales volume : ¿ costs+ Desired return /Contribution per unit

Contribution per unit : Selling price – total variable costs

¿( £ 120,000+ £ 30,000)/(£ 1600−£ 400)

¿ 125

EUROCARIB TOURS must attract 125 visitors on the tour so that its target profitability

of £30,000 can be achieved. At this level, contribution will be (£ 1200∗125)=£ 150,000.

Break-even point: The point which shows the best and most effective utilization of

resources is known as break-even point (Bebbington and Thomson, 2013).

Break−even point=Total ¿ cost /CPU

¿ £ 120,000/ £ 1200

¿ 100 visitors

BEP( £ )=100 visitors∗£ 1600

¿ £ 160,000

As per the results, it is clear that if there are only 90 tourists, EUROCARIB TOURS

should not plan the trip and put effort to maximize sales volume to 100 visitors to reach the

maximum point. If actual demand goes beyond that level, then it would be profitable for the

firm.

1.2 Pricing methods

Pricing is an important decision for tour operator which is a process of setting charges

that company will charge for the services provided. There are multitude of method which might

be used by the firm to set a right price as per the consumer need, enumerated underneath:

Cost-centered decision: As name itself, initially, the method determine total costs of the

planned tour including both the fixed and variable costs elements i.e. accommodation, air fare,

transportation and others. Total costs are allocated to the potential number of visitors to assess

unit costs. In this, expected margin is added together to fix selling price (Weiss, 2010. The

strength of the method is that it applying the method, EUROCARIB TOURS can easily recover

all the costs incurred. Moreover, company is sure that it will generate return by charging selling

prices with some margin above costs.

3

that it enable formulators to clearly set the target sales volume which generates expected return

(Pavlatos and Paggios, 2009).

Desired sales volume : ¿ costs+ Desired return /Contribution per unit

Contribution per unit : Selling price – total variable costs

¿( £ 120,000+ £ 30,000)/(£ 1600−£ 400)

¿ 125

EUROCARIB TOURS must attract 125 visitors on the tour so that its target profitability

of £30,000 can be achieved. At this level, contribution will be (£ 1200∗125)=£ 150,000.

Break-even point: The point which shows the best and most effective utilization of

resources is known as break-even point (Bebbington and Thomson, 2013).

Break−even point=Total ¿ cost /CPU

¿ £ 120,000/ £ 1200

¿ 100 visitors

BEP( £ )=100 visitors∗£ 1600

¿ £ 160,000

As per the results, it is clear that if there are only 90 tourists, EUROCARIB TOURS

should not plan the trip and put effort to maximize sales volume to 100 visitors to reach the

maximum point. If actual demand goes beyond that level, then it would be profitable for the

firm.

1.2 Pricing methods

Pricing is an important decision for tour operator which is a process of setting charges

that company will charge for the services provided. There are multitude of method which might

be used by the firm to set a right price as per the consumer need, enumerated underneath:

Cost-centered decision: As name itself, initially, the method determine total costs of the

planned tour including both the fixed and variable costs elements i.e. accommodation, air fare,

transportation and others. Total costs are allocated to the potential number of visitors to assess

unit costs. In this, expected margin is added together to fix selling price (Weiss, 2010. The

strength of the method is that it applying the method, EUROCARIB TOURS can easily recover

all the costs incurred. Moreover, company is sure that it will generate return by charging selling

prices with some margin above costs.

3

Competitive selling pricing: This method set prices of every tour operator after scanning

the external market. In this, key competitors are taken into account and their prices are examine

which enable EUROCARIB TOURS to set highly competitive charges. It enable firm in

successfully attracting more audience base as competitive or highly-concentrated prices gives

tough competition to the rival organizations. However, based on product differentiation, firm can

charge a bit higher prices by providing unique services to the end-users.

Demand based pricing: Under this method, prices are set by the organization after

analyzing potential market demand. It means, if there is larger number of guests expected to visit

on the tour, than it means, EUROCARIB TOURS will be able set higher charges for the planned

tour. In contrast to this, in case of lower demand, firm must charge cheaper prices so that more

prospective buyers can be attracted on the tour and thereby sales volume can be raised. Thus,

such pricing tactic helps firm in setting an appropriate price that helps business to succeed.

Target return: According to the name itself, prices are fixed after incorporating a target

return on the costs. The best part of the method is that it helps companies in generating some

return by charging greater prices above costs (Pavlatos and Paggios, 2009).

Seasonable pricing: Travel industry grows at rapid rate during vacations and holidays

when more number of buyers wish to go attractive tourist destinations all over the world. Thus,

in these pricing mechanism, period when market demand is very high, prices is charge high.

Unlike this, during period when there is very low market demand, EUROCARIB TOURS can

charge less and attract more audience base to drive larger sales volume and gain maximum

profitability.

Going rate: This method pays special attention to the prices of industry leaders and key

players. Besides this, external market environment such as demand fluctuation, political and

regulatory uncertainty, social preferences and others are considered to adjust charged prices

(Baumol and et.al., 2012).

1.3 Analysis of factors affecting travel and tourism business

There are number of factors that have due impact on travel and tourism business. It is very

important to take in to account these factors so that prudent decisions can be taken in the travel and

tourism business. Some of the relevant factors are as follows. Seasonal variation: It is the one of important factor that has due importance for the firms.

Seasonal variation refers to the situation where in few months sudden peak is observed in sales of

4

the external market. In this, key competitors are taken into account and their prices are examine

which enable EUROCARIB TOURS to set highly competitive charges. It enable firm in

successfully attracting more audience base as competitive or highly-concentrated prices gives

tough competition to the rival organizations. However, based on product differentiation, firm can

charge a bit higher prices by providing unique services to the end-users.

Demand based pricing: Under this method, prices are set by the organization after

analyzing potential market demand. It means, if there is larger number of guests expected to visit

on the tour, than it means, EUROCARIB TOURS will be able set higher charges for the planned

tour. In contrast to this, in case of lower demand, firm must charge cheaper prices so that more

prospective buyers can be attracted on the tour and thereby sales volume can be raised. Thus,

such pricing tactic helps firm in setting an appropriate price that helps business to succeed.

Target return: According to the name itself, prices are fixed after incorporating a target

return on the costs. The best part of the method is that it helps companies in generating some

return by charging greater prices above costs (Pavlatos and Paggios, 2009).

Seasonable pricing: Travel industry grows at rapid rate during vacations and holidays

when more number of buyers wish to go attractive tourist destinations all over the world. Thus,

in these pricing mechanism, period when market demand is very high, prices is charge high.

Unlike this, during period when there is very low market demand, EUROCARIB TOURS can

charge less and attract more audience base to drive larger sales volume and gain maximum

profitability.

Going rate: This method pays special attention to the prices of industry leaders and key

players. Besides this, external market environment such as demand fluctuation, political and

regulatory uncertainty, social preferences and others are considered to adjust charged prices

(Baumol and et.al., 2012).

1.3 Analysis of factors affecting travel and tourism business

There are number of factors that have due impact on travel and tourism business. It is very

important to take in to account these factors so that prudent decisions can be taken in the travel and

tourism business. Some of the relevant factors are as follows. Seasonal variation: It is the one of important factor that has due importance for the firms.

Seasonal variation refers to the situation where in few months sudden peak is observed in sales of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the products and services in the business. On other hand, in case of seasonal variation sometimes

sales declined consistently during off season. Hence, firm operating in travel and tourism sector

needs to consider seasonal factor while making any business decisions (Costa, Panyik and

Buhalis, 2014). During season firm can charge high product for its price and can earn maximum

profit but during off season in order to ensure survival of business it become important to reduce

product price. Thus, it can be said that seasonal variations have impact on tourism business. Economic environment: Economic environment is another factor that have due impact on the

business firm. Government of the nation frequently makes changes in its monetary and fiscal

policy and all these things positively and negatively affect business firms. Change in monetary

policy make availability of loan cheaper and costlier. Similarly, fiscal policy has impact on

taxation rate. Alteration in these policies has impact on profitability of the business firm. Thus, it

is very important to take in to consideration economic factors while making investment decisions. Political environment: Political environment also affect travel and tourism business. This is

because ideology and steps taken by the firm determined way in which nation economy will go.

In every nation government prepare plans and policies for its benefit and all these things in some

way affect firms operating in the nation. Hence, it can be said that political environment have due

impact on these firms and it is the one of factor that have due impact to travel and tourism

business. Social environment: Social environment have due impact on the business firms as it can be

observed that it contain ideologies and beliefs that people have towards firm and its product. All

these things have impact on sale of the firm products and number of factors in the business. It can

be said that social environment must be considered and according to it product must be designed

so that it can be acceptable to all sort of people. Staff: It is another factor that has very huge impact on the business firm (Pfueller, Lee and

Laing, 2011). It is very important to ensure that there is abundant amount of staff at the

workplace. In case there is lack of staff members it is very difficult task to manage business

operations in proper manner. It can be said that staff is also one of factor that have impact on the

business firm.

TASK 2

2.1 Different type of management accounting information that can be used in the business

Management accounting is widely used to make decisions in the business. There are number of

techniques in management accounting that can be used to measure firm performance. On basis of

5

sales declined consistently during off season. Hence, firm operating in travel and tourism sector

needs to consider seasonal factor while making any business decisions (Costa, Panyik and

Buhalis, 2014). During season firm can charge high product for its price and can earn maximum

profit but during off season in order to ensure survival of business it become important to reduce

product price. Thus, it can be said that seasonal variations have impact on tourism business. Economic environment: Economic environment is another factor that have due impact on the

business firm. Government of the nation frequently makes changes in its monetary and fiscal

policy and all these things positively and negatively affect business firms. Change in monetary

policy make availability of loan cheaper and costlier. Similarly, fiscal policy has impact on

taxation rate. Alteration in these policies has impact on profitability of the business firm. Thus, it

is very important to take in to consideration economic factors while making investment decisions. Political environment: Political environment also affect travel and tourism business. This is

because ideology and steps taken by the firm determined way in which nation economy will go.

In every nation government prepare plans and policies for its benefit and all these things in some

way affect firms operating in the nation. Hence, it can be said that political environment have due

impact on these firms and it is the one of factor that have due impact to travel and tourism

business. Social environment: Social environment have due impact on the business firms as it can be

observed that it contain ideologies and beliefs that people have towards firm and its product. All

these things have impact on sale of the firm products and number of factors in the business. It can

be said that social environment must be considered and according to it product must be designed

so that it can be acceptable to all sort of people. Staff: It is another factor that has very huge impact on the business firm (Pfueller, Lee and

Laing, 2011). It is very important to ensure that there is abundant amount of staff at the

workplace. In case there is lack of staff members it is very difficult task to manage business

operations in proper manner. It can be said that staff is also one of factor that have impact on the

business firm.

TASK 2

2.1 Different type of management accounting information that can be used in the business

Management accounting is widely used to make decisions in the business. There are number of

techniques in management accounting that can be used to measure firm performance. On basis of

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management accounting information weak spots are identified and corrective steps are taken to improve

performance. Different types of management accounting information that can be used in the business are

given below.

Budget: It is the statement that is prepared by the business firm and under this cash inflows and

outflows are projected. In this tool planning is prepared about way in which expenditures will be

made in the business. By considering values that are given in the budget expenses are made in the

business and in this way expenses are controlled in the business. There are number of advantage

and disadvantage of using budget for the business firms (Demirović, Simat and Radović,

2014). One of major advantage of using budget is that it help firm in cost control but negative

side is that one need to make estimation of cash flows which may be wrong. This is because one

needs to take percentage to make projection of cash flows. It can be said that budget is the one of

the important tool of making business decision.

Variance analysis: Variance analysis is another management accounting information that can be

used in the business. Under this method positive or negative performance of the firm is identified

by comparing actual values with budgeted value. If performance is good then in that case then it

is counted as strong point and is considered in strategy formulation. Variance analysis is used to

make decisions in respect to domain which need serious attention from side of management.

Break even analysis: Break even analysis is the one of the important tool that is used to make

decisions. By using this tool firms determine sales target for their employees and determine that

profit up to specific level will be achieved in the business. In this method it is identified that if all

variable expenses are paid from sales revenue amount then what amount of sales needs to be

made to cover entire cost in the business (Richards, 2017). By using this tool it is determined by

the managers that after paying all expense from sales units to earn determined net profit how

much units extra need to be sold in the market. It can be said that break even analysis is the one

of management accounting information that can be used to make business decisions.

These were the management accounting information that can be used by the firms in their

business because these tools help manager in looking at different directions to improve business

performance. However, they need to ensure that these management accounting tools are used in right way

so that reliable results can be obtained in proper manner. Managers of travel and tourism firm must

cautiously take business decisions in order to solve their problem.

2.2 Assessing the use of investment appraisal techniques as a decision making tool

Investment appraisal techniques include payback period, net present value, average and

internal rate of return. By using techniques of investment appraisal firm can assess the viability

6

performance. Different types of management accounting information that can be used in the business are

given below.

Budget: It is the statement that is prepared by the business firm and under this cash inflows and

outflows are projected. In this tool planning is prepared about way in which expenditures will be

made in the business. By considering values that are given in the budget expenses are made in the

business and in this way expenses are controlled in the business. There are number of advantage

and disadvantage of using budget for the business firms (Demirović, Simat and Radović,

2014). One of major advantage of using budget is that it help firm in cost control but negative

side is that one need to make estimation of cash flows which may be wrong. This is because one

needs to take percentage to make projection of cash flows. It can be said that budget is the one of

the important tool of making business decision.

Variance analysis: Variance analysis is another management accounting information that can be

used in the business. Under this method positive or negative performance of the firm is identified

by comparing actual values with budgeted value. If performance is good then in that case then it

is counted as strong point and is considered in strategy formulation. Variance analysis is used to

make decisions in respect to domain which need serious attention from side of management.

Break even analysis: Break even analysis is the one of the important tool that is used to make

decisions. By using this tool firms determine sales target for their employees and determine that

profit up to specific level will be achieved in the business. In this method it is identified that if all

variable expenses are paid from sales revenue amount then what amount of sales needs to be

made to cover entire cost in the business (Richards, 2017). By using this tool it is determined by

the managers that after paying all expense from sales units to earn determined net profit how

much units extra need to be sold in the market. It can be said that break even analysis is the one

of management accounting information that can be used to make business decisions.

These were the management accounting information that can be used by the firms in their

business because these tools help manager in looking at different directions to improve business

performance. However, they need to ensure that these management accounting tools are used in right way

so that reliable results can be obtained in proper manner. Managers of travel and tourism firm must

cautiously take business decisions in order to solve their problem.

2.2 Assessing the use of investment appraisal techniques as a decision making tool

Investment appraisal techniques include payback period, net present value, average and

internal rate of return. By using techniques of investment appraisal firm can assess the viability

6

of proposal and thereby would become able to take suitable decision. Payback period helps

EUROCARIB in identifying the time period within which initial investment will be covered. In

accordance with such technique firm should select project that has less payback period. Net

present value (NPV) is considered as discounted model which in turn helps company in assessing

the return that will be generated after the specific time frame (Moreno-Izquierdo, Ramón-

Rodríguez and Ribes, 2015). Such method offers solution by taking into account the time value

of money concept. Referring the method of NPV, it can be stated that EUROCARIB should

select the proposal that have higher NPV.

Along with this, average rate of return (ARR) method helps in assessing mean return

which will be offered by the concerned proposal. On the basis of such method, project that offers

high average return is highly beneficial over others. In contrast to this, IRR method helps in

assessing return in the form of percentage which is associated with the proposal. In this way,

such discounted method helps EUROCARIB in selecting suitable proposal that aid in the growth

and success. On the basis of cited case situation, firm has different proposal with the same initial

investment and different cash flows. In this regard, by using different techniques business entity

can assess whether proposal is financially viable or not. Options that are available for the

investment purpose are enumerated below:

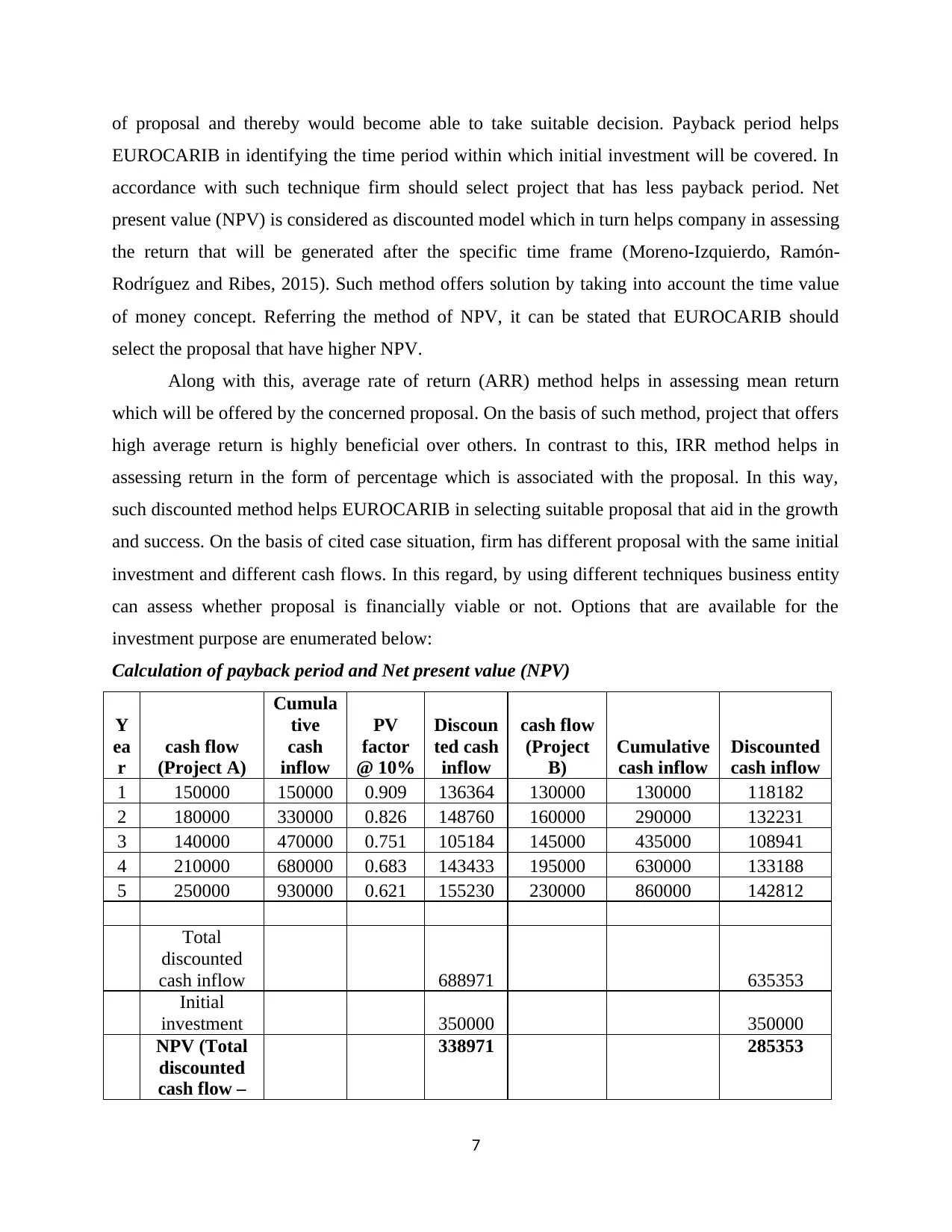

Calculation of payback period and Net present value (NPV)

Y

ea

r

cash flow

(Project A)

Cumula

tive

cash

inflow

PV

factor

@ 10%

Discoun

ted cash

inflow

cash flow

(Project

B)

Cumulative

cash inflow

Discounted

cash inflow

1 150000 150000 0.909 136364 130000 130000 118182

2 180000 330000 0.826 148760 160000 290000 132231

3 140000 470000 0.751 105184 145000 435000 108941

4 210000 680000 0.683 143433 195000 630000 133188

5 250000 930000 0.621 155230 230000 860000 142812

Total

discounted

cash inflow 688971 635353

Initial

investment 350000 350000

NPV (Total

discounted

cash flow –

338971 285353

7

EUROCARIB in identifying the time period within which initial investment will be covered. In

accordance with such technique firm should select project that has less payback period. Net

present value (NPV) is considered as discounted model which in turn helps company in assessing

the return that will be generated after the specific time frame (Moreno-Izquierdo, Ramón-

Rodríguez and Ribes, 2015). Such method offers solution by taking into account the time value

of money concept. Referring the method of NPV, it can be stated that EUROCARIB should

select the proposal that have higher NPV.

Along with this, average rate of return (ARR) method helps in assessing mean return

which will be offered by the concerned proposal. On the basis of such method, project that offers

high average return is highly beneficial over others. In contrast to this, IRR method helps in

assessing return in the form of percentage which is associated with the proposal. In this way,

such discounted method helps EUROCARIB in selecting suitable proposal that aid in the growth

and success. On the basis of cited case situation, firm has different proposal with the same initial

investment and different cash flows. In this regard, by using different techniques business entity

can assess whether proposal is financially viable or not. Options that are available for the

investment purpose are enumerated below:

Calculation of payback period and Net present value (NPV)

Y

ea

r

cash flow

(Project A)

Cumula

tive

cash

inflow

PV

factor

@ 10%

Discoun

ted cash

inflow

cash flow

(Project

B)

Cumulative

cash inflow

Discounted

cash inflow

1 150000 150000 0.909 136364 130000 130000 118182

2 180000 330000 0.826 148760 160000 290000 132231

3 140000 470000 0.751 105184 145000 435000 108941

4 210000 680000 0.683 143433 195000 630000 133188

5 250000 930000 0.621 155230 230000 860000 142812

Total

discounted

cash inflow 688971 635353

Initial

investment 350000 350000

NPV (Total

discounted

cash flow –

338971 285353

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

initial

investment)

Payback period

Project A: 2 + (350000 – 330000) / 140000

= 2.1 years

Project B: 2 + (350000 – 290000) / 145000

= 2.4 years

Computation of IRR

Year -350000 -350000

1 150000 130000

2 180000 160000

3 140000 145000

4 210000 195000

5 250000 230000

IRR 40% 35%

Interpretation: The above depicted table shows that payback period of project A and B

accounts are 2.1 & 2.4 years. This aspect shows that project A will offer opportunity to

EUROCARIB to recover initial investment within the suitable time frame. Along with this,

tabular presentation shows that NPV of project A & B accounts for £338971 & £285353

respectively. Further, outcome of investment appraisal shows that IRR of project A & B implies

for 40% and 35% significantly. Thus considering all such aspects and selection criteria it is

advised to EUROCARIB to employ money in option 1 which will prove to be beneficial for it.

TASK 3

3.1 Analysing financial statements of Thomas Cook

Ratio analysis tool is highly prominent that provides assistance in summarizing and

evaluating financial statements of firm. By undertaking such tool business entity or analyst can

measure performance of the firm from various aspects such as profitability, liquidity, solvency,

efficiency and investment. Hence, ratio analysis tool helps in assessing whether performance of

the firm is improved over the time frame or not. In this way, by determining ratios management

8

investment)

Payback period

Project A: 2 + (350000 – 330000) / 140000

= 2.1 years

Project B: 2 + (350000 – 290000) / 145000

= 2.4 years

Computation of IRR

Year -350000 -350000

1 150000 130000

2 180000 160000

3 140000 145000

4 210000 195000

5 250000 230000

IRR 40% 35%

Interpretation: The above depicted table shows that payback period of project A and B

accounts are 2.1 & 2.4 years. This aspect shows that project A will offer opportunity to

EUROCARIB to recover initial investment within the suitable time frame. Along with this,

tabular presentation shows that NPV of project A & B accounts for £338971 & £285353

respectively. Further, outcome of investment appraisal shows that IRR of project A & B implies

for 40% and 35% significantly. Thus considering all such aspects and selection criteria it is

advised to EUROCARIB to employ money in option 1 which will prove to be beneficial for it.

TASK 3

3.1 Analysing financial statements of Thomas Cook

Ratio analysis tool is highly prominent that provides assistance in summarizing and

evaluating financial statements of firm. By undertaking such tool business entity or analyst can

measure performance of the firm from various aspects such as profitability, liquidity, solvency,

efficiency and investment. Hence, ratio analysis tool helps in assessing whether performance of

the firm is improved over the time frame or not. In this way, by determining ratios management

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

team can take suitable action for improvements (Navickas and Malakauskaite, 2015). Along with

this, it also helps investors in deciding whether they need to invest money in firm’s operations or

not. On the basis of cited case situation, EUROCARIB wants to get information about the

financial aspects of Thomas Cook. In this regard, ratio analysis for the year of 2016 and 2017 is

as follows:

Profitability ratio analysis: It helps in ascertaining the return that is generated by the

firm over expenses including both direct and indirect. Hence, by evaluating profitability aspect

firm can take suitable decision for improvement and enhance its financial position.

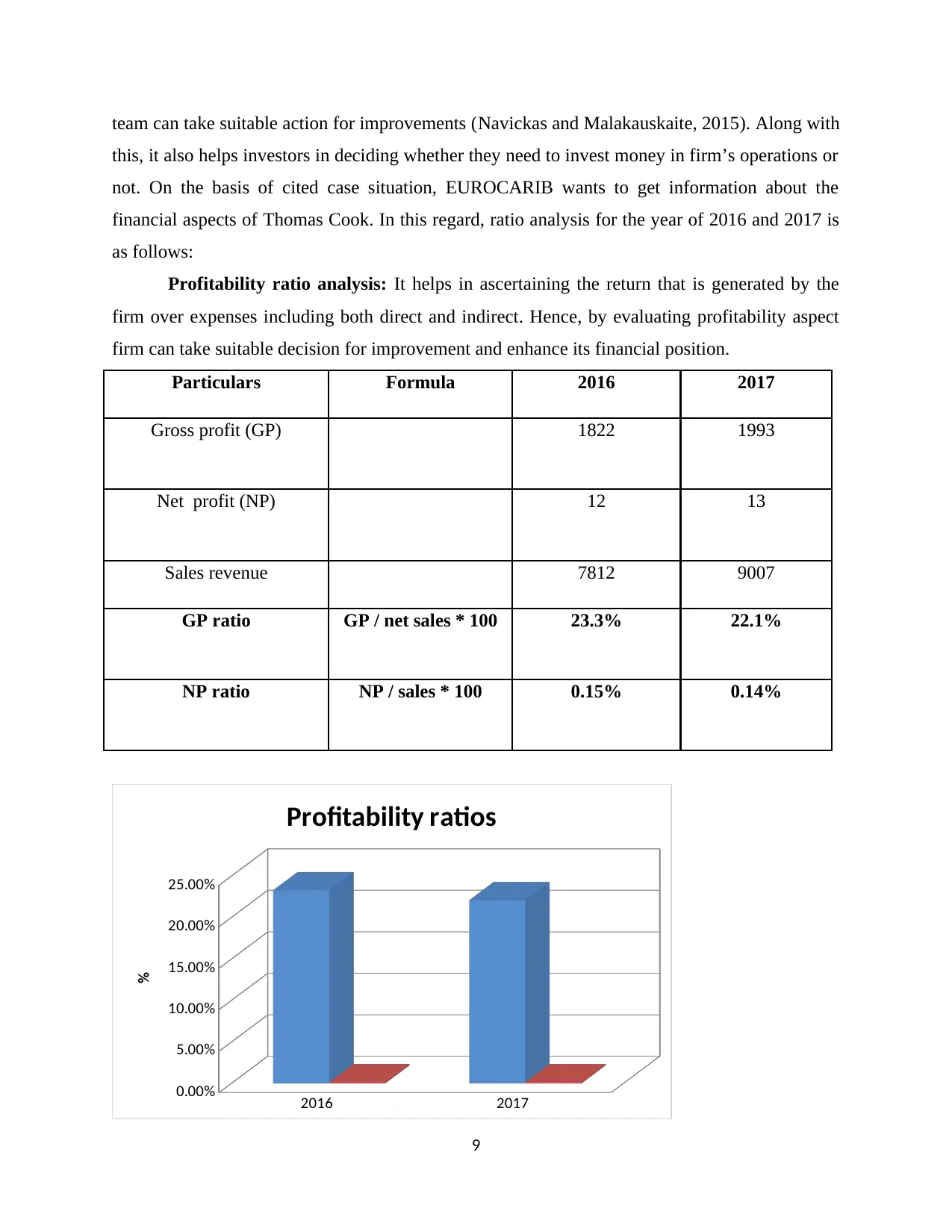

Particulars Formula 2016 2017

Gross profit (GP) 1822 1993

Net profit (NP) 12 13

Sales revenue 7812 9007

GP ratio GP / net sales * 100 23.3% 22.1%

NP ratio NP / sales * 100 0.15% 0.14%

2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Profitability ratios

%

9

this, it also helps investors in deciding whether they need to invest money in firm’s operations or

not. On the basis of cited case situation, EUROCARIB wants to get information about the

financial aspects of Thomas Cook. In this regard, ratio analysis for the year of 2016 and 2017 is

as follows:

Profitability ratio analysis: It helps in ascertaining the return that is generated by the

firm over expenses including both direct and indirect. Hence, by evaluating profitability aspect

firm can take suitable decision for improvement and enhance its financial position.

Particulars Formula 2016 2017

Gross profit (GP) 1822 1993

Net profit (NP) 12 13

Sales revenue 7812 9007

GP ratio GP / net sales * 100 23.3% 22.1%

NP ratio NP / sales * 100 0.15% 0.14%

2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Profitability ratios

%

9

Interpretation: Outcome of profitability ratio analysis clearly shows that GP margin of

Thomas Cook Plc declined from 23.30% to 22.10% in the year of 2017. However, on the other

side, increasing trend is identified in the sales revenue of Thomas Cook Plc from 1822 to 1993

GBP million. Referring such aspect, it can be said that firm’s control on direct expenses is not

good. Due to higher COGS (material, labour), such travel firm fails to attain high margin.

Further, percentage of NP margin shows that profitability margin or position of Thomas Cook

Group Plc is worst. The rationale behind such lower margin is higher operating or indirect and

interest expenses. Thus, for improving such worst position firm is required to undertake the

system of budgetary control which in turn helps in exerting control on both direct as well as

indirect expenses.

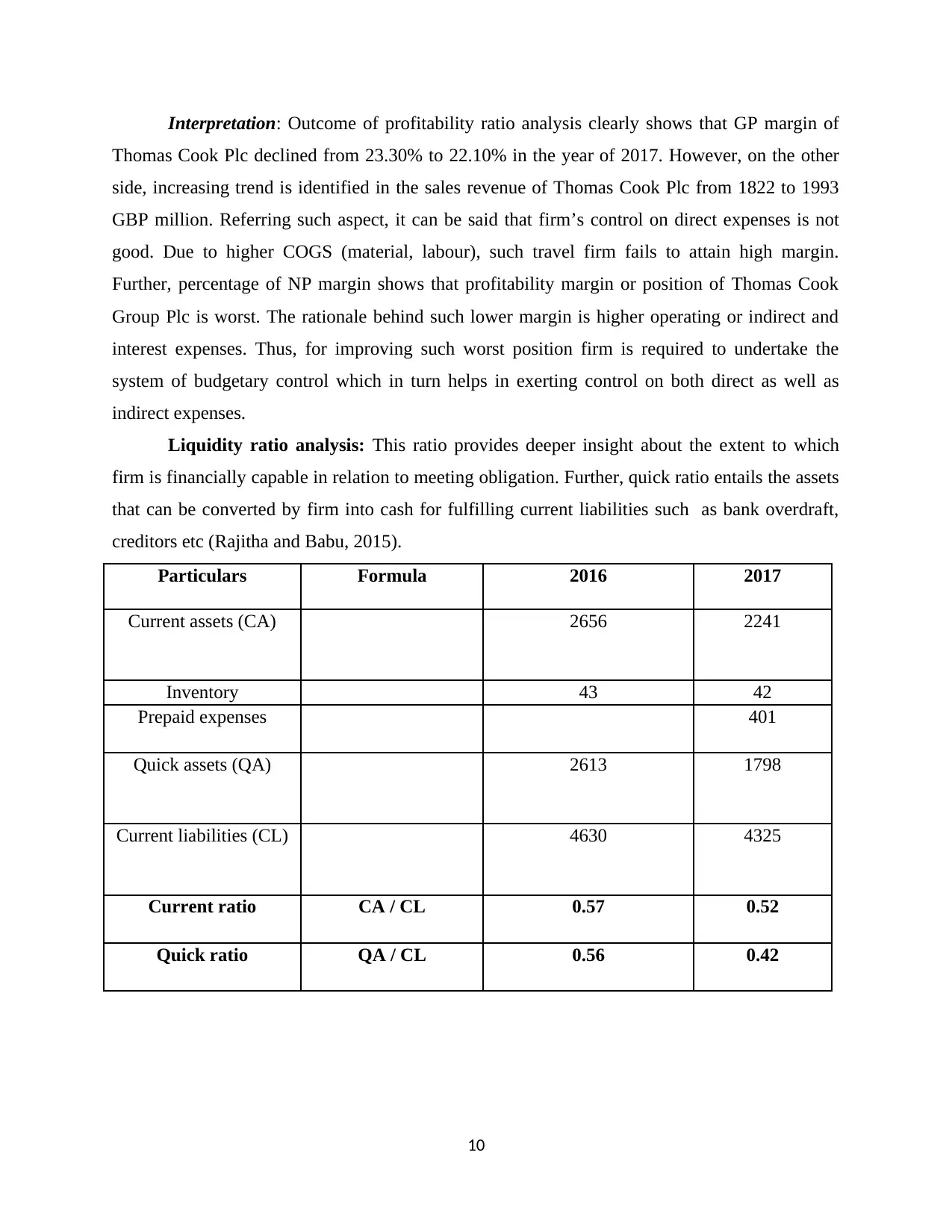

Liquidity ratio analysis: This ratio provides deeper insight about the extent to which

firm is financially capable in relation to meeting obligation. Further, quick ratio entails the assets

that can be converted by firm into cash for fulfilling current liabilities such as bank overdraft,

creditors etc (Rajitha and Babu, 2015).

Particulars Formula 2016 2017

Current assets (CA) 2656 2241

Inventory 43 42

Prepaid expenses 401

Quick assets (QA) 2613 1798

Current liabilities (CL) 4630 4325

Current ratio CA / CL 0.57 0.52

Quick ratio QA / CL 0.56 0.42

10

Thomas Cook Plc declined from 23.30% to 22.10% in the year of 2017. However, on the other

side, increasing trend is identified in the sales revenue of Thomas Cook Plc from 1822 to 1993

GBP million. Referring such aspect, it can be said that firm’s control on direct expenses is not

good. Due to higher COGS (material, labour), such travel firm fails to attain high margin.

Further, percentage of NP margin shows that profitability margin or position of Thomas Cook

Group Plc is worst. The rationale behind such lower margin is higher operating or indirect and

interest expenses. Thus, for improving such worst position firm is required to undertake the

system of budgetary control which in turn helps in exerting control on both direct as well as

indirect expenses.

Liquidity ratio analysis: This ratio provides deeper insight about the extent to which

firm is financially capable in relation to meeting obligation. Further, quick ratio entails the assets

that can be converted by firm into cash for fulfilling current liabilities such as bank overdraft,

creditors etc (Rajitha and Babu, 2015).

Particulars Formula 2016 2017

Current assets (CA) 2656 2241

Inventory 43 42

Prepaid expenses 401

Quick assets (QA) 2613 1798

Current liabilities (CL) 4630 4325

Current ratio CA / CL 0.57 0.52

Quick ratio QA / CL 0.56 0.42

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.