Comprehensive Treasury Risk Analysis Assignment - Finance

VerifiedAdded on 2022/08/21

|10

|2003

|12

Homework Assignment

AI Summary

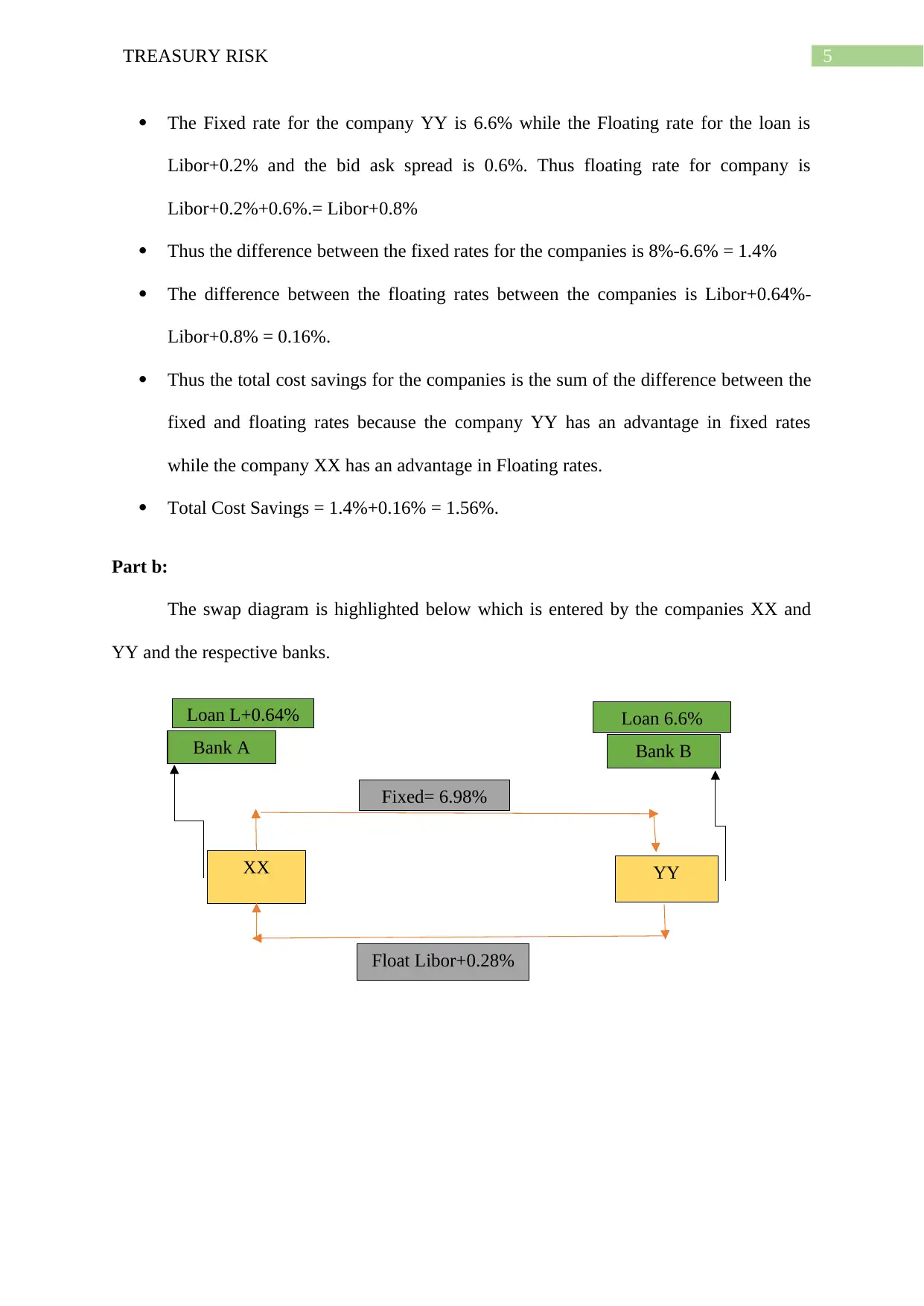

This finance assignment delves into treasury risk management, focusing on interest rate parity, arbitrage opportunities, and currency swaps. Question 1 examines interest rate parity between the US and Britain, calculating forward rates and exploring covered interest arbitrage. It investigates the presence of arbitrage profits and explains the differences in parity forward rates derived through different methods. Question 2 analyzes a currency swap scenario, outlining cost savings for companies, constructing a swap diagram, calculating effective fixed rates, and assessing the impact of interest rate fluctuations. It also discusses the risks associated with swap agreements, including swap price risk and credit default risk, particularly in the context of the 2008 financial crisis. The assignment provides a comprehensive overview of treasury risk concepts and their practical implications in financial decision-making.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.