Finance Assignment: Valuation of Shares, Capital Budgeting, and Loans

VerifiedAdded on 2020/05/28

|55

|9152

|106

Homework Assignment

AI Summary

This finance assignment solution addresses several key concepts in financial analysis. The first question involves a two-period certainty model, calculating consumption and income based on dividend payouts and equity holdings. The second question focuses on share valuation, determining the current selling price of a share given dividend growth expectations. The third question covers time value of money, deferred annuities, and loan repayments, including calculations for retirement funds, monthly pensions, effective interest rates, and loan amortization. The final question delves into capital budgeting, evaluating two mutually exclusive projects using payback period, NPV, IRR, and crossover point analysis, along with a capital budgeting problem for a new technology purchase, considering costs, savings, depreciation, and tax implications to determine the net present value of the investment.

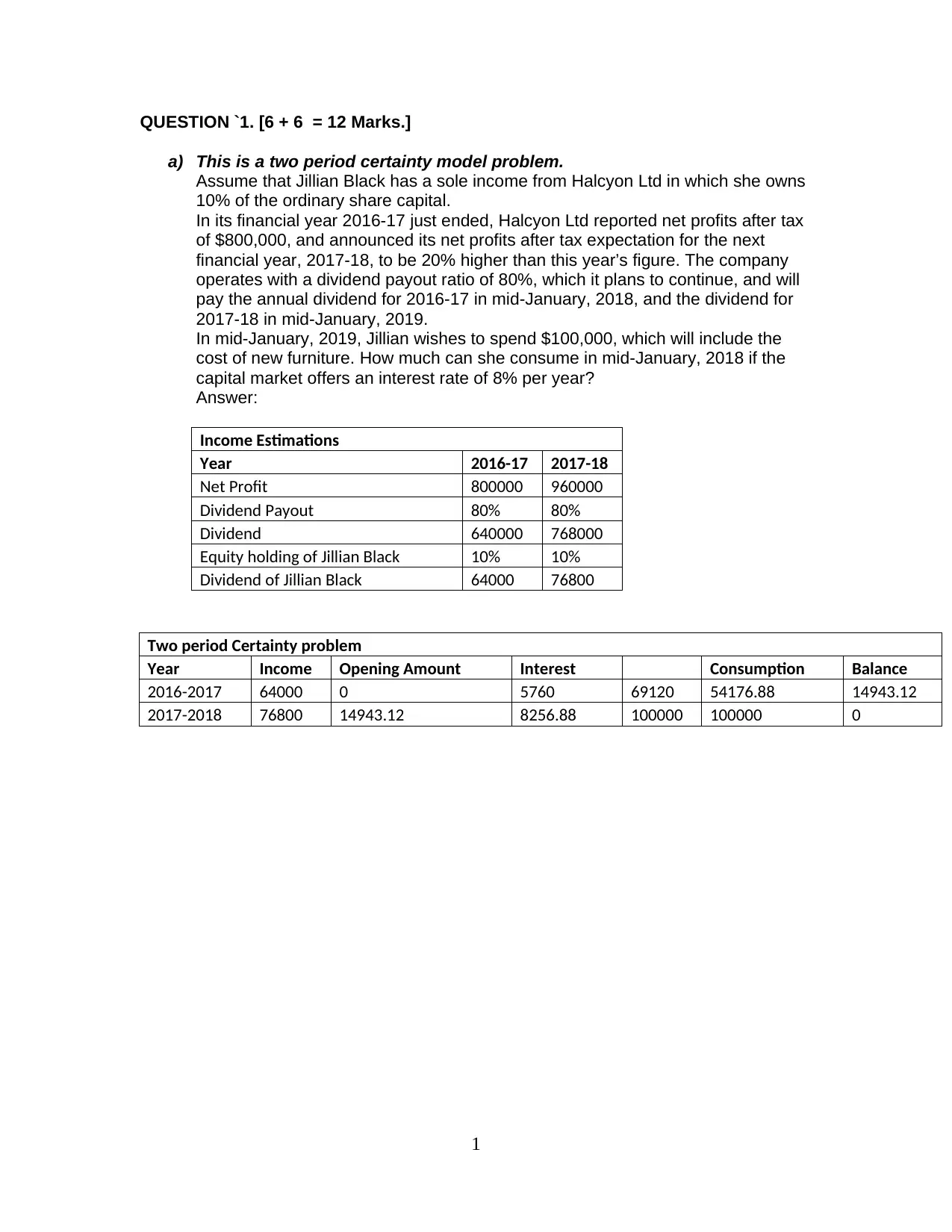

QUESTION `1. [6 + 6 = 12 Marks.]

a) This is a two period certainty model problem.

Assume that Jillian Black has a sole income from Halcyon Ltd in which she owns

10% of the ordinary share capital.

In its financial year 2016-17 just ended, Halcyon Ltd reported net profits after tax

of $800,000, and announced its net profits after tax expectation for the next

financial year, 2017-18, to be 20% higher than this year’s figure. The company

operates with a dividend payout ratio of 80%, which it plans to continue, and will

pay the annual dividend for 2016-17 in mid-January, 2018, and the dividend for

2017-18 in mid-January, 2019.

In mid-January, 2019, Jillian wishes to spend $100,000, which will include the

cost of new furniture. How much can she consume in mid-January, 2018 if the

capital market offers an interest rate of 8% per year?

Answer:

Income Estimations

Year 2016-17 2017-18

Net Profit 800000 960000

Dividend Payout 80% 80%

Dividend 640000 768000

Equity holding of Jillian Black 10% 10%

Dividend of Jillian Black 64000 76800

Two period Certainty problem

Year Income Opening Amount Interest Consumption Balance

2016-2017 64000 0 5760 69120 54176.88 14943.12

2017-2018 76800 14943.12 8256.88 100000 100000 0

1

a) This is a two period certainty model problem.

Assume that Jillian Black has a sole income from Halcyon Ltd in which she owns

10% of the ordinary share capital.

In its financial year 2016-17 just ended, Halcyon Ltd reported net profits after tax

of $800,000, and announced its net profits after tax expectation for the next

financial year, 2017-18, to be 20% higher than this year’s figure. The company

operates with a dividend payout ratio of 80%, which it plans to continue, and will

pay the annual dividend for 2016-17 in mid-January, 2018, and the dividend for

2017-18 in mid-January, 2019.

In mid-January, 2019, Jillian wishes to spend $100,000, which will include the

cost of new furniture. How much can she consume in mid-January, 2018 if the

capital market offers an interest rate of 8% per year?

Answer:

Income Estimations

Year 2016-17 2017-18

Net Profit 800000 960000

Dividend Payout 80% 80%

Dividend 640000 768000

Equity holding of Jillian Black 10% 10%

Dividend of Jillian Black 64000 76800

Two period Certainty problem

Year Income Opening Amount Interest Consumption Balance

2016-2017 64000 0 5760 69120 54176.88 14943.12

2017-2018 76800 14943.12 8256.88 100000 100000 0

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) This question relates to the valuation of shares.

Ram Shack Ltd has just paid a dividend of $3.00 a share. Investors require a

13% per annum return on investments such as Ram Shack. What would a share

in Ram Shack Ltd be expected to sell for today (January, 2018) if the dividend is

expected to increase by 20% in January, 2019, 16% in January, 2020, 12% in

January, 2021 and thereafter by 5 per cent a year forever, from January, 2022

onwards?

Answer:

Year Dividend PVF @ 13%

PV of

Dividend

2018 3.00 0.885 2.655

2019 3.60 0.783 2.819

2020 4.18 0.693 2.894

2021 4.68 0.613 2.869

2022 61.39* 0.543 33.319

Price of Share 44.555

* 4.68 x (1+0.05)/(0.13-0.05)= 61.39

2

Ram Shack Ltd has just paid a dividend of $3.00 a share. Investors require a

13% per annum return on investments such as Ram Shack. What would a share

in Ram Shack Ltd be expected to sell for today (January, 2018) if the dividend is

expected to increase by 20% in January, 2019, 16% in January, 2020, 12% in

January, 2021 and thereafter by 5 per cent a year forever, from January, 2022

onwards?

Answer:

Year Dividend PVF @ 13%

PV of

Dividend

2018 3.00 0.885 2.655

2019 3.60 0.783 2.819

2020 4.18 0.693 2.894

2021 4.68 0.613 2.869

2022 61.39* 0.543 33.319

Price of Share 44.555

* 4.68 x (1+0.05)/(0.13-0.05)= 61.39

2

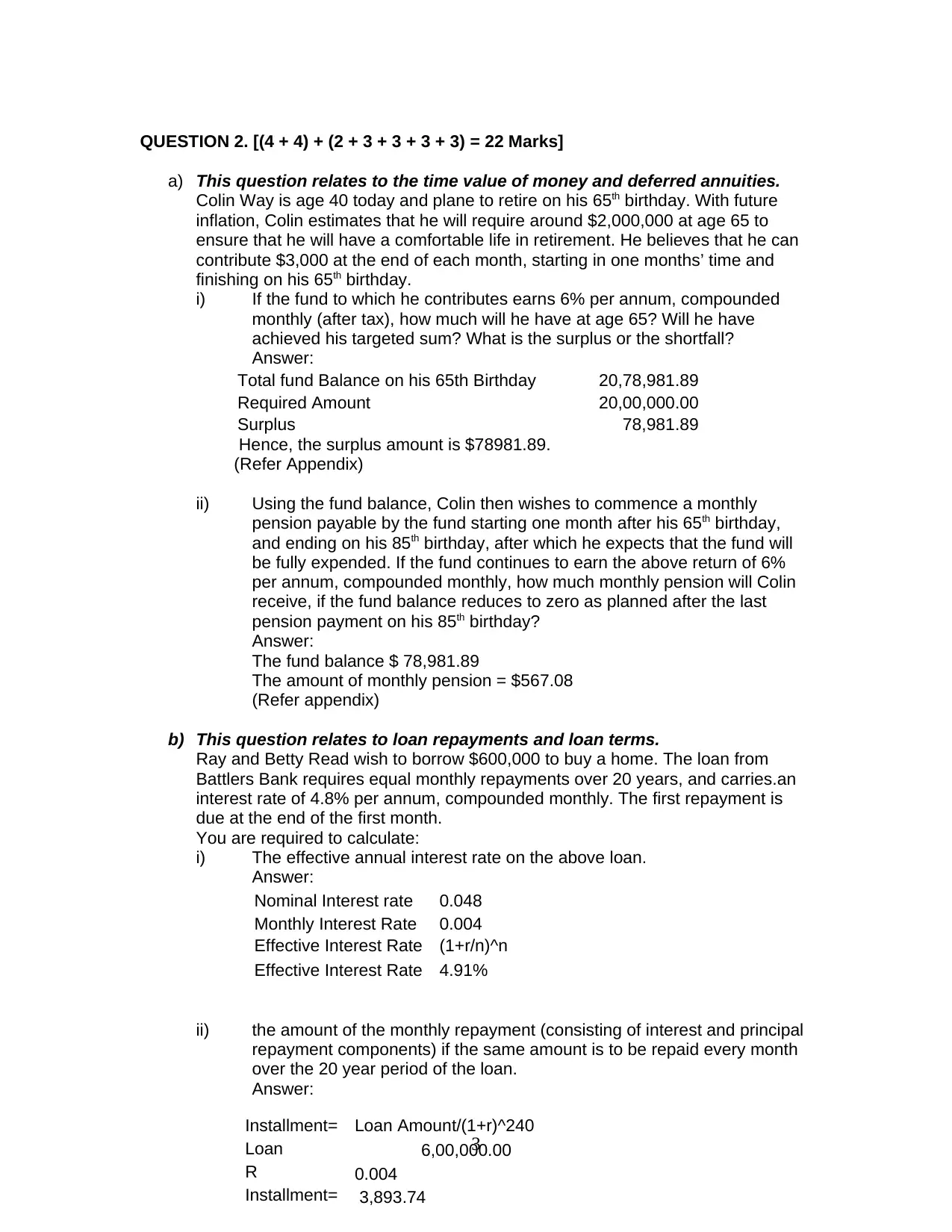

QUESTION 2. [(4 + 4) + (2 + 3 + 3 + 3 + 3) = 22 Marks]

a) This question relates to the time value of money and deferred annuities.

Colin Way is age 40 today and plane to retire on his 65th birthday. With future

inflation, Colin estimates that he will require around $2,000,000 at age 65 to

ensure that he will have a comfortable life in retirement. He believes that he can

contribute $3,000 at the end of each month, starting in one months’ time and

finishing on his 65th birthday.

i) If the fund to which he contributes earns 6% per annum, compounded

monthly (after tax), how much will he have at age 65? Will he have

achieved his targeted sum? What is the surplus or the shortfall?

Answer:

Total fund Balance on his 65th Birthday 20,78,981.89

Required Amount 20,00,000.00

Surplus 78,981.89

Hence, the surplus amount is $78981.89.

(Refer Appendix)

ii) Using the fund balance, Colin then wishes to commence a monthly

pension payable by the fund starting one month after his 65th birthday,

and ending on his 85th birthday, after which he expects that the fund will

be fully expended. If the fund continues to earn the above return of 6%

per annum, compounded monthly, how much monthly pension will Colin

receive, if the fund balance reduces to zero as planned after the last

pension payment on his 85th birthday?

Answer:

The fund balance $ 78,981.89

The amount of monthly pension = $567.08

(Refer appendix)

b) This question relates to loan repayments and loan terms.

Ray and Betty Read wish to borrow $600,000 to buy a home. The loan from

Battlers Bank requires equal monthly repayments over 20 years, and carries.an

interest rate of 4.8% per annum, compounded monthly. The first repayment is

due at the end of the first month.

You are required to calculate:

i) The effective annual interest rate on the above loan.

Answer:

Nominal Interest rate 0.048

Monthly Interest Rate 0.004

Effective Interest Rate (1+r/n)^n

Effective Interest Rate 4.91%

ii) the amount of the monthly repayment (consisting of interest and principal

repayment components) if the same amount is to be repaid every month

over the 20 year period of the loan.

Answer:

3

Installment= Loan Amount/(1+r)^240

Loan 6,00,000.00

R 0.004

Installment= 3,893.74

a) This question relates to the time value of money and deferred annuities.

Colin Way is age 40 today and plane to retire on his 65th birthday. With future

inflation, Colin estimates that he will require around $2,000,000 at age 65 to

ensure that he will have a comfortable life in retirement. He believes that he can

contribute $3,000 at the end of each month, starting in one months’ time and

finishing on his 65th birthday.

i) If the fund to which he contributes earns 6% per annum, compounded

monthly (after tax), how much will he have at age 65? Will he have

achieved his targeted sum? What is the surplus or the shortfall?

Answer:

Total fund Balance on his 65th Birthday 20,78,981.89

Required Amount 20,00,000.00

Surplus 78,981.89

Hence, the surplus amount is $78981.89.

(Refer Appendix)

ii) Using the fund balance, Colin then wishes to commence a monthly

pension payable by the fund starting one month after his 65th birthday,

and ending on his 85th birthday, after which he expects that the fund will

be fully expended. If the fund continues to earn the above return of 6%

per annum, compounded monthly, how much monthly pension will Colin

receive, if the fund balance reduces to zero as planned after the last

pension payment on his 85th birthday?

Answer:

The fund balance $ 78,981.89

The amount of monthly pension = $567.08

(Refer appendix)

b) This question relates to loan repayments and loan terms.

Ray and Betty Read wish to borrow $600,000 to buy a home. The loan from

Battlers Bank requires equal monthly repayments over 20 years, and carries.an

interest rate of 4.8% per annum, compounded monthly. The first repayment is

due at the end of the first month.

You are required to calculate:

i) The effective annual interest rate on the above loan.

Answer:

Nominal Interest rate 0.048

Monthly Interest Rate 0.004

Effective Interest Rate (1+r/n)^n

Effective Interest Rate 4.91%

ii) the amount of the monthly repayment (consisting of interest and principal

repayment components) if the same amount is to be repaid every month

over the 20 year period of the loan.

Answer:

3

Installment= Loan Amount/(1+r)^240

Loan 6,00,000.00

R 0.004

Installment= 3,893.74

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Refer appendix)

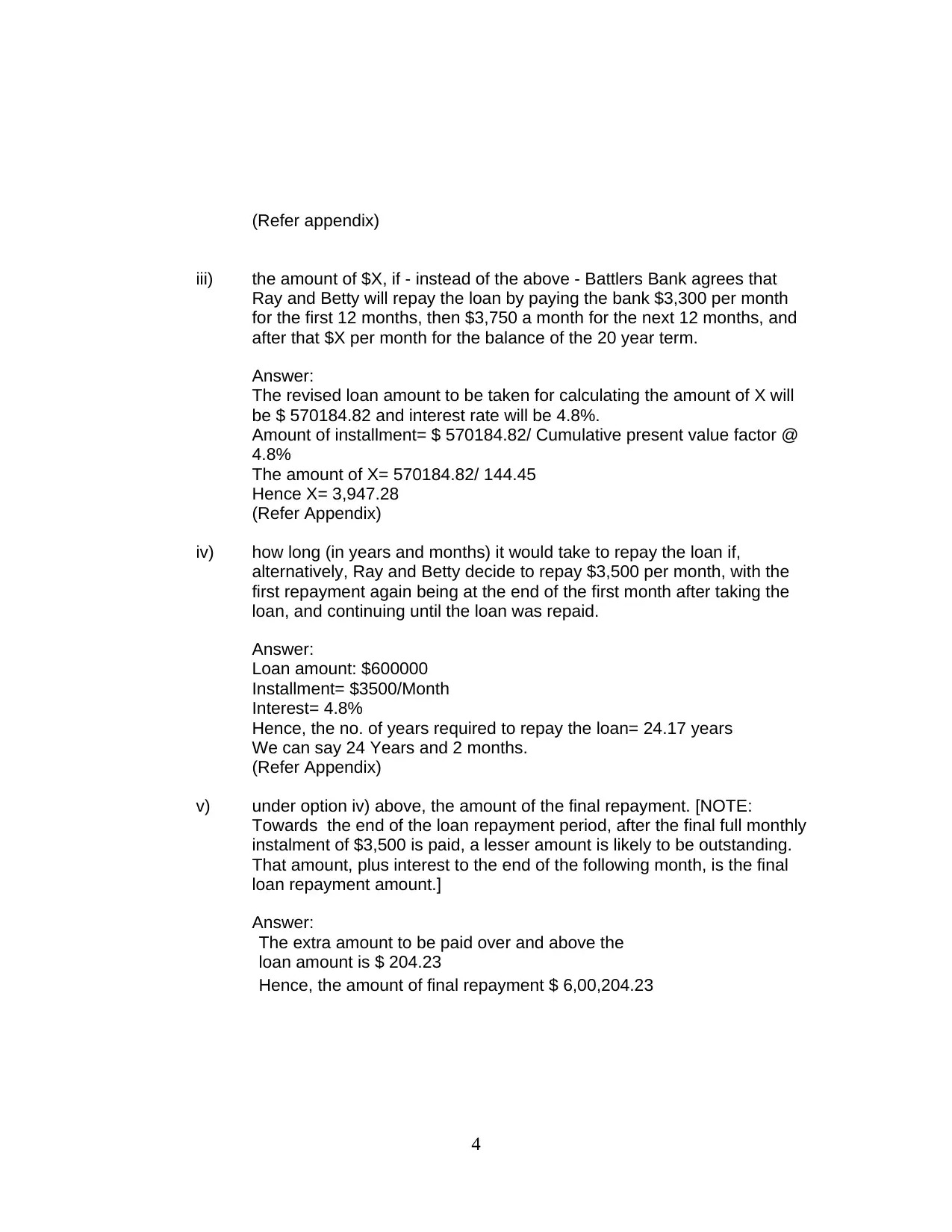

iii) the amount of $X, if - instead of the above - Battlers Bank agrees that

Ray and Betty will repay the loan by paying the bank $3,300 per month

for the first 12 months, then $3,750 a month for the next 12 months, and

after that $X per month for the balance of the 20 year term.

Answer:

The revised loan amount to be taken for calculating the amount of X will

be $ 570184.82 and interest rate will be 4.8%.

Amount of installment= $ 570184.82/ Cumulative present value factor @

4.8%

The amount of X= 570184.82/ 144.45

Hence X= 3,947.28

(Refer Appendix)

iv) how long (in years and months) it would take to repay the loan if,

alternatively, Ray and Betty decide to repay $3,500 per month, with the

first repayment again being at the end of the first month after taking the

loan, and continuing until the loan was repaid.

Answer:

Loan amount: $600000

Installment= $3500/Month

Interest= 4.8%

Hence, the no. of years required to repay the loan= 24.17 years

We can say 24 Years and 2 months.

(Refer Appendix)

v) under option iv) above, the amount of the final repayment. [NOTE:

Towards the end of the loan repayment period, after the final full monthly

instalment of $3,500 is paid, a lesser amount is likely to be outstanding.

That amount, plus interest to the end of the following month, is the final

loan repayment amount.]

Answer:

The extra amount to be paid over and above the

loan amount is $ 204.23

Hence, the amount of final repayment $ 6,00,204.23

4

iii) the amount of $X, if - instead of the above - Battlers Bank agrees that

Ray and Betty will repay the loan by paying the bank $3,300 per month

for the first 12 months, then $3,750 a month for the next 12 months, and

after that $X per month for the balance of the 20 year term.

Answer:

The revised loan amount to be taken for calculating the amount of X will

be $ 570184.82 and interest rate will be 4.8%.

Amount of installment= $ 570184.82/ Cumulative present value factor @

4.8%

The amount of X= 570184.82/ 144.45

Hence X= 3,947.28

(Refer Appendix)

iv) how long (in years and months) it would take to repay the loan if,

alternatively, Ray and Betty decide to repay $3,500 per month, with the

first repayment again being at the end of the first month after taking the

loan, and continuing until the loan was repaid.

Answer:

Loan amount: $600000

Installment= $3500/Month

Interest= 4.8%

Hence, the no. of years required to repay the loan= 24.17 years

We can say 24 Years and 2 months.

(Refer Appendix)

v) under option iv) above, the amount of the final repayment. [NOTE:

Towards the end of the loan repayment period, after the final full monthly

instalment of $3,500 is paid, a lesser amount is likely to be outstanding.

That amount, plus interest to the end of the following month, is the final

loan repayment amount.]

Answer:

The extra amount to be paid over and above the

loan amount is $ 204.23

Hence, the amount of final repayment $ 6,00,204.23

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

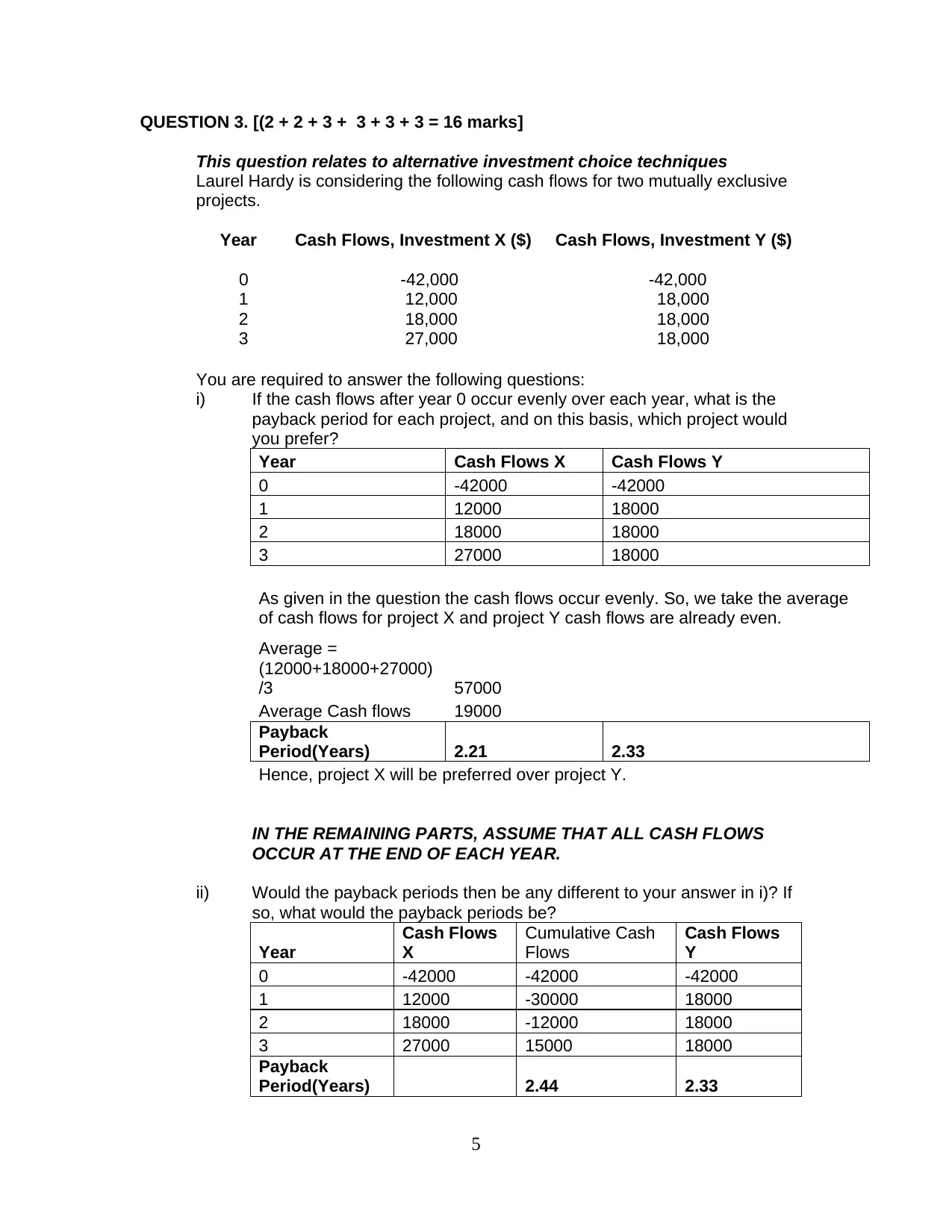

QUESTION 3. [(2 + 2 + 3 + 3 + 3 + 3 = 16 marks]

This question relates to alternative investment choice techniques

Laurel Hardy is considering the following cash flows for two mutually exclusive

projects.

Year Cash Flows, Investment X ($) Cash Flows, Investment Y ($)

0 -42,000 -42,000

1 12,000 18,000

2 18,000 18,000

3 27,000 18,000

You are required to answer the following questions:

i) If the cash flows after year 0 occur evenly over each year, what is the

payback period for each project, and on this basis, which project would

you prefer?

Year Cash Flows X Cash Flows Y

0 -42000 -42000

1 12000 18000

2 18000 18000

3 27000 18000

As given in the question the cash flows occur evenly. So, we take the average

of cash flows for project X and project Y cash flows are already even.

Average =

(12000+18000+27000)

/3 57000

Average Cash flows 19000

Payback

Period(Years) 2.21 2.33

Hence, project X will be preferred over project Y.

IN THE REMAINING PARTS, ASSUME THAT ALL CASH FLOWS

OCCUR AT THE END OF EACH YEAR.

ii) Would the payback periods then be any different to your answer in i)? If

so, what would the payback periods be?

Year

Cash Flows

X

Cumulative Cash

Flows

Cash Flows

Y

0 -42000 -42000 -42000

1 12000 -30000 18000

2 18000 -12000 18000

3 27000 15000 18000

Payback

Period(Years) 2.44 2.33

5

This question relates to alternative investment choice techniques

Laurel Hardy is considering the following cash flows for two mutually exclusive

projects.

Year Cash Flows, Investment X ($) Cash Flows, Investment Y ($)

0 -42,000 -42,000

1 12,000 18,000

2 18,000 18,000

3 27,000 18,000

You are required to answer the following questions:

i) If the cash flows after year 0 occur evenly over each year, what is the

payback period for each project, and on this basis, which project would

you prefer?

Year Cash Flows X Cash Flows Y

0 -42000 -42000

1 12000 18000

2 18000 18000

3 27000 18000

As given in the question the cash flows occur evenly. So, we take the average

of cash flows for project X and project Y cash flows are already even.

Average =

(12000+18000+27000)

/3 57000

Average Cash flows 19000

Payback

Period(Years) 2.21 2.33

Hence, project X will be preferred over project Y.

IN THE REMAINING PARTS, ASSUME THAT ALL CASH FLOWS

OCCUR AT THE END OF EACH YEAR.

ii) Would the payback periods then be any different to your answer in i)? If

so, what would the payback periods be?

Year

Cash Flows

X

Cumulative Cash

Flows

Cash Flows

Y

0 -42000 -42000 -42000

1 12000 -30000 18000

2 18000 -12000 18000

3 27000 15000 18000

Payback

Period(Years) 2.44 2.33

5

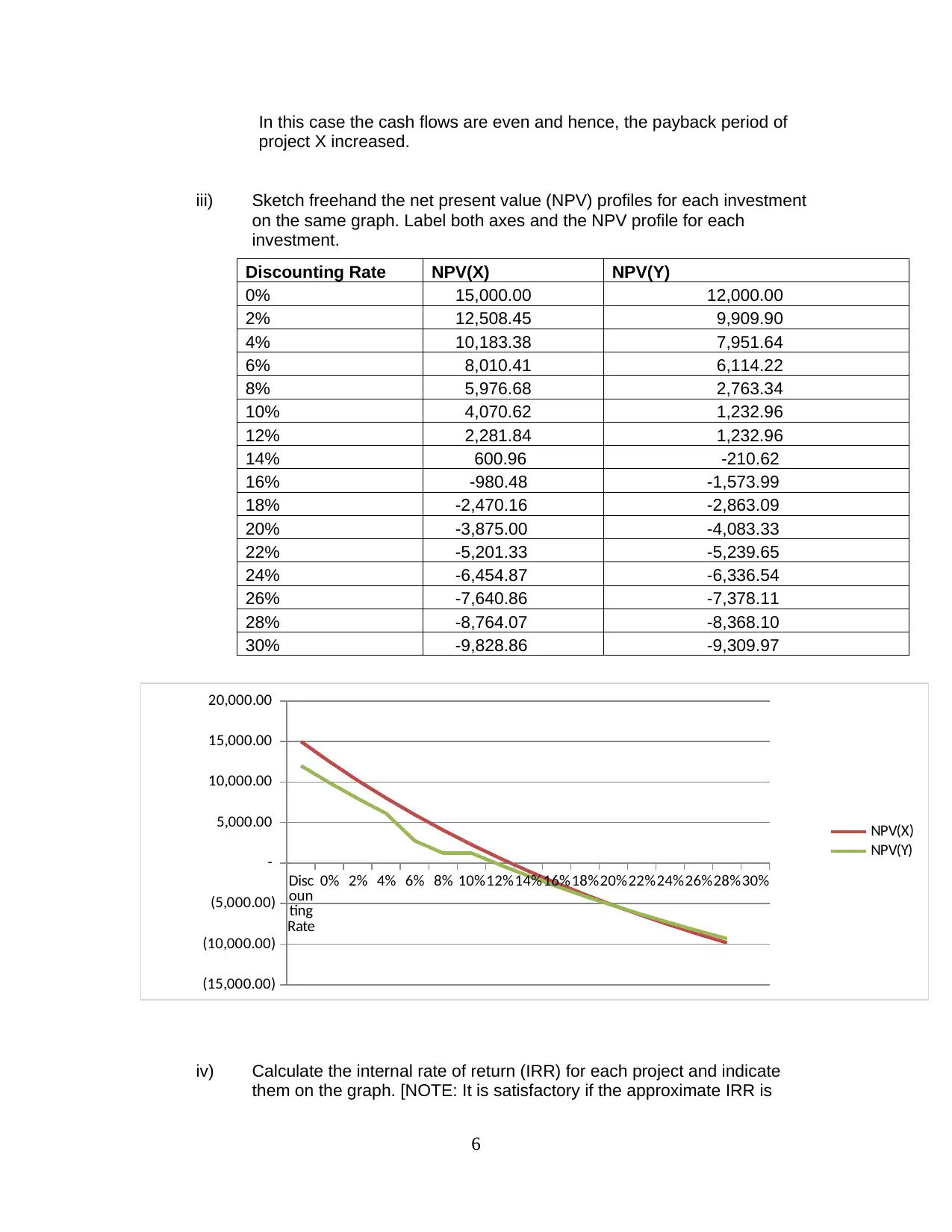

In this case the cash flows are even and hence, the payback period of

project X increased.

iii) Sketch freehand the net present value (NPV) profiles for each investment

on the same graph. Label both axes and the NPV profile for each

investment.

Disc

oun

ting

Rate

0% 2% 4% 6% 8% 10%12%14%16%18%20%22%24%26%28%30%

(15,000.00)

(10,000.00)

(5,000.00)

-

5,000.00

10,000.00

15,000.00

20,000.00

NPV(X)

NPV(Y)

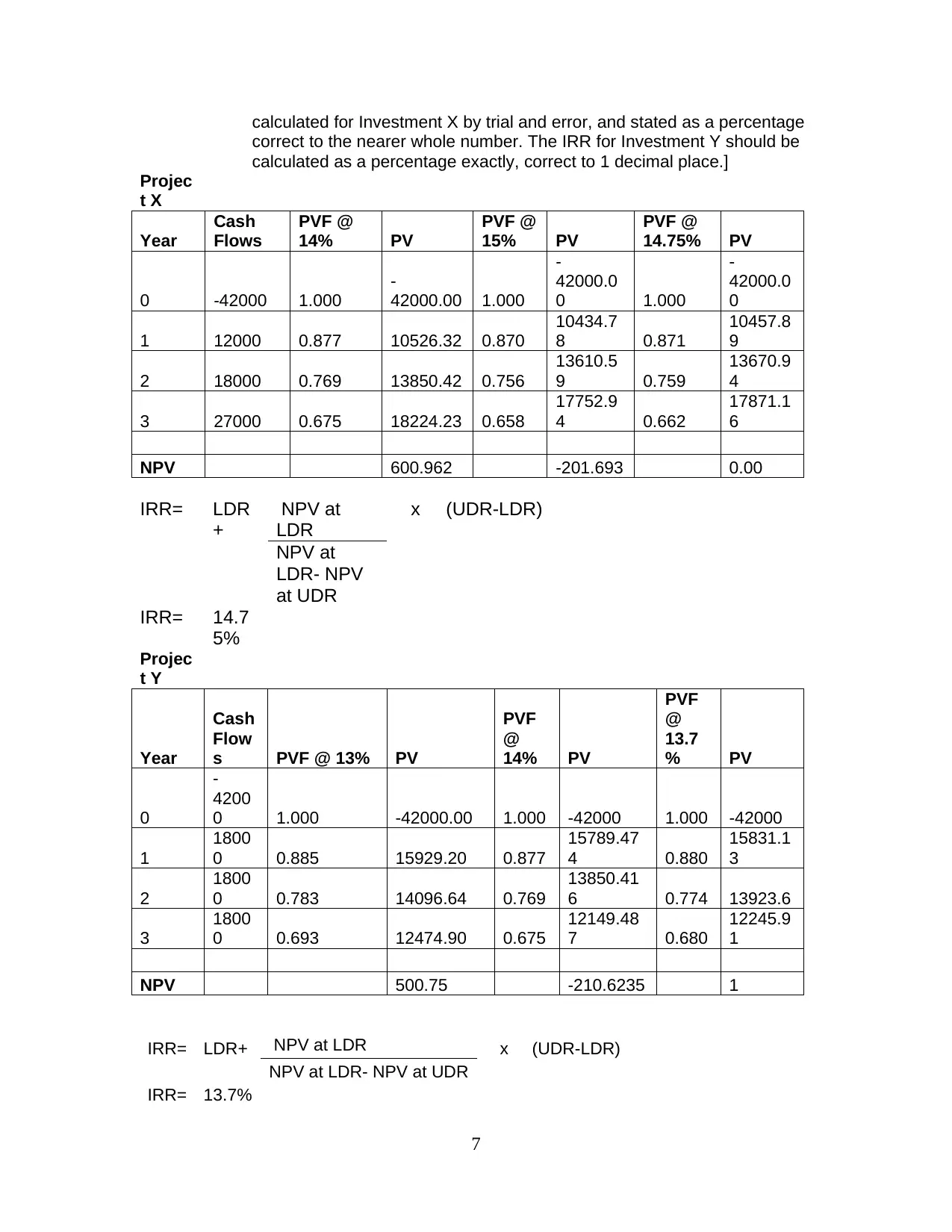

iv) Calculate the internal rate of return (IRR) for each project and indicate

them on the graph. [NOTE: It is satisfactory if the approximate IRR is

6

Discounting Rate NPV(X) NPV(Y)

0% 15,000.00 12,000.00

2% 12,508.45 9,909.90

4% 10,183.38 7,951.64

6% 8,010.41 6,114.22

8% 5,976.68 2,763.34

10% 4,070.62 1,232.96

12% 2,281.84 1,232.96

14% 600.96 -210.62

16% -980.48 -1,573.99

18% -2,470.16 -2,863.09

20% -3,875.00 -4,083.33

22% -5,201.33 -5,239.65

24% -6,454.87 -6,336.54

26% -7,640.86 -7,378.11

28% -8,764.07 -8,368.10

30% -9,828.86 -9,309.97

project X increased.

iii) Sketch freehand the net present value (NPV) profiles for each investment

on the same graph. Label both axes and the NPV profile for each

investment.

Disc

oun

ting

Rate

0% 2% 4% 6% 8% 10%12%14%16%18%20%22%24%26%28%30%

(15,000.00)

(10,000.00)

(5,000.00)

-

5,000.00

10,000.00

15,000.00

20,000.00

NPV(X)

NPV(Y)

iv) Calculate the internal rate of return (IRR) for each project and indicate

them on the graph. [NOTE: It is satisfactory if the approximate IRR is

6

Discounting Rate NPV(X) NPV(Y)

0% 15,000.00 12,000.00

2% 12,508.45 9,909.90

4% 10,183.38 7,951.64

6% 8,010.41 6,114.22

8% 5,976.68 2,763.34

10% 4,070.62 1,232.96

12% 2,281.84 1,232.96

14% 600.96 -210.62

16% -980.48 -1,573.99

18% -2,470.16 -2,863.09

20% -3,875.00 -4,083.33

22% -5,201.33 -5,239.65

24% -6,454.87 -6,336.54

26% -7,640.86 -7,378.11

28% -8,764.07 -8,368.10

30% -9,828.86 -9,309.97

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

calculated for Investment X by trial and error, and stated as a percentage

correct to the nearer whole number. The IRR for Investment Y should be

calculated as a percentage exactly, correct to 1 decimal place.]

Projec

t X

Year

Cash

Flows

PVF @

14% PV

PVF @

15% PV

PVF @

14.75% PV

0 -42000 1.000

-

42000.00 1.000

-

42000.0

0 1.000

-

42000.0

0

1 12000 0.877 10526.32 0.870

10434.7

8 0.871

10457.8

9

2 18000 0.769 13850.42 0.756

13610.5

9 0.759

13670.9

4

3 27000 0.675 18224.23 0.658

17752.9

4 0.662

17871.1

6

NPV 600.962 -201.693 0.00

IRR= LDR

+

NPV at

LDR

x (UDR-LDR)

NPV at

LDR- NPV

at UDR

IRR= 14.7

5%

Projec

t Y

Year

Cash

Flow

s PVF @ 13% PV

PVF

@

14% PV

PVF

@

13.7

% PV

0

-

4200

0 1.000 -42000.00 1.000 -42000 1.000 -42000

1

1800

0 0.885 15929.20 0.877

15789.47

4 0.880

15831.1

3

2

1800

0 0.783 14096.64 0.769

13850.41

6 0.774 13923.6

3

1800

0 0.693 12474.90 0.675

12149.48

7 0.680

12245.9

1

NPV 500.75 -210.6235 1

IRR= LDR+ NPV at LDR x (UDR-LDR)

NPV at LDR- NPV at UDR

IRR= 13.7%

7

correct to the nearer whole number. The IRR for Investment Y should be

calculated as a percentage exactly, correct to 1 decimal place.]

Projec

t X

Year

Cash

Flows

PVF @

14% PV

PVF @

15% PV

PVF @

14.75% PV

0 -42000 1.000

-

42000.00 1.000

-

42000.0

0 1.000

-

42000.0

0

1 12000 0.877 10526.32 0.870

10434.7

8 0.871

10457.8

9

2 18000 0.769 13850.42 0.756

13610.5

9 0.759

13670.9

4

3 27000 0.675 18224.23 0.658

17752.9

4 0.662

17871.1

6

NPV 600.962 -201.693 0.00

IRR= LDR

+

NPV at

LDR

x (UDR-LDR)

NPV at

LDR- NPV

at UDR

IRR= 14.7

5%

Projec

t Y

Year

Cash

Flow

s PVF @ 13% PV

PVF

@

14% PV

PVF

@

13.7

% PV

0

-

4200

0 1.000 -42000.00 1.000 -42000 1.000 -42000

1

1800

0 0.885 15929.20 0.877

15789.47

4 0.880

15831.1

3

2

1800

0 0.783 14096.64 0.769

13850.41

6 0.774 13923.6

3

1800

0 0.693 12474.90 0.675

12149.48

7 0.680

12245.9

1

NPV 500.75 -210.6235 1

IRR= LDR+ NPV at LDR x (UDR-LDR)

NPV at LDR- NPV at UDR

IRR= 13.7%

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

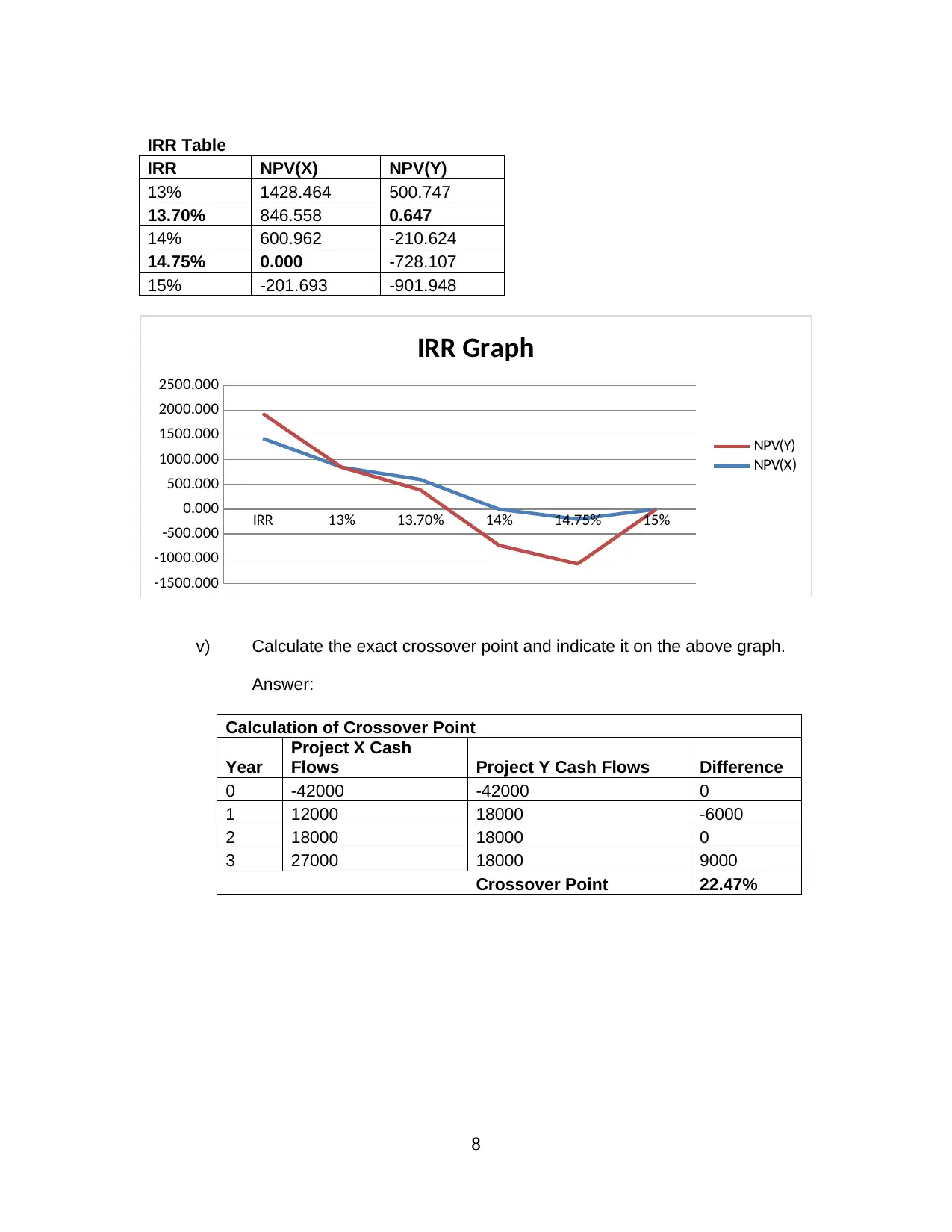

IRR Table

IRR NPV(X) NPV(Y)

13% 1428.464 500.747

13.70% 846.558 0.647

14% 600.962 -210.624

14.75% 0.000 -728.107

15% -201.693 -901.948

IRR 13% 13.70% 14% 14.75% 15%

-1500.000

-1000.000

-500.000

0.000

500.000

1000.000

1500.000

2000.000

2500.000

IRR Graph

NPV(Y)

NPV(X)

v) Calculate the exact crossover point and indicate it on the above graph.

Answer:

Calculation of Crossover Point

Year

Project X Cash

Flows Project Y Cash Flows Difference

0 -42000 -42000 0

1 12000 18000 -6000

2 18000 18000 0

3 27000 18000 9000

Crossover Point 22.47%

8

IRR NPV(X) NPV(Y)

13% 1428.464 500.747

13.70% 846.558 0.647

14% 600.962 -210.624

14.75% 0.000 -728.107

15% -201.693 -901.948

IRR 13% 13.70% 14% 14.75% 15%

-1500.000

-1000.000

-500.000

0.000

500.000

1000.000

1500.000

2000.000

2500.000

IRR Graph

NPV(Y)

NPV(X)

v) Calculate the exact crossover point and indicate it on the above graph.

Answer:

Calculation of Crossover Point

Year

Project X Cash

Flows Project Y Cash Flows Difference

0 -42000 -42000 0

1 12000 18000 -6000

2 18000 18000 0

3 27000 18000 9000

Crossover Point 22.47%

8

Dis

cou

nti

ng

Rat

e

0% 2% 4% 6% 8% 10

% 12

% 14

% 16

% 18

% 20

% 22

% 24

% 26

% 28

% 30

%

(15,000.00)

(10,000.00)

(5,000.00)

-

5,000.00

10,000.00

15,000.00

20,000.00

NPV(X)

NPV(Y)

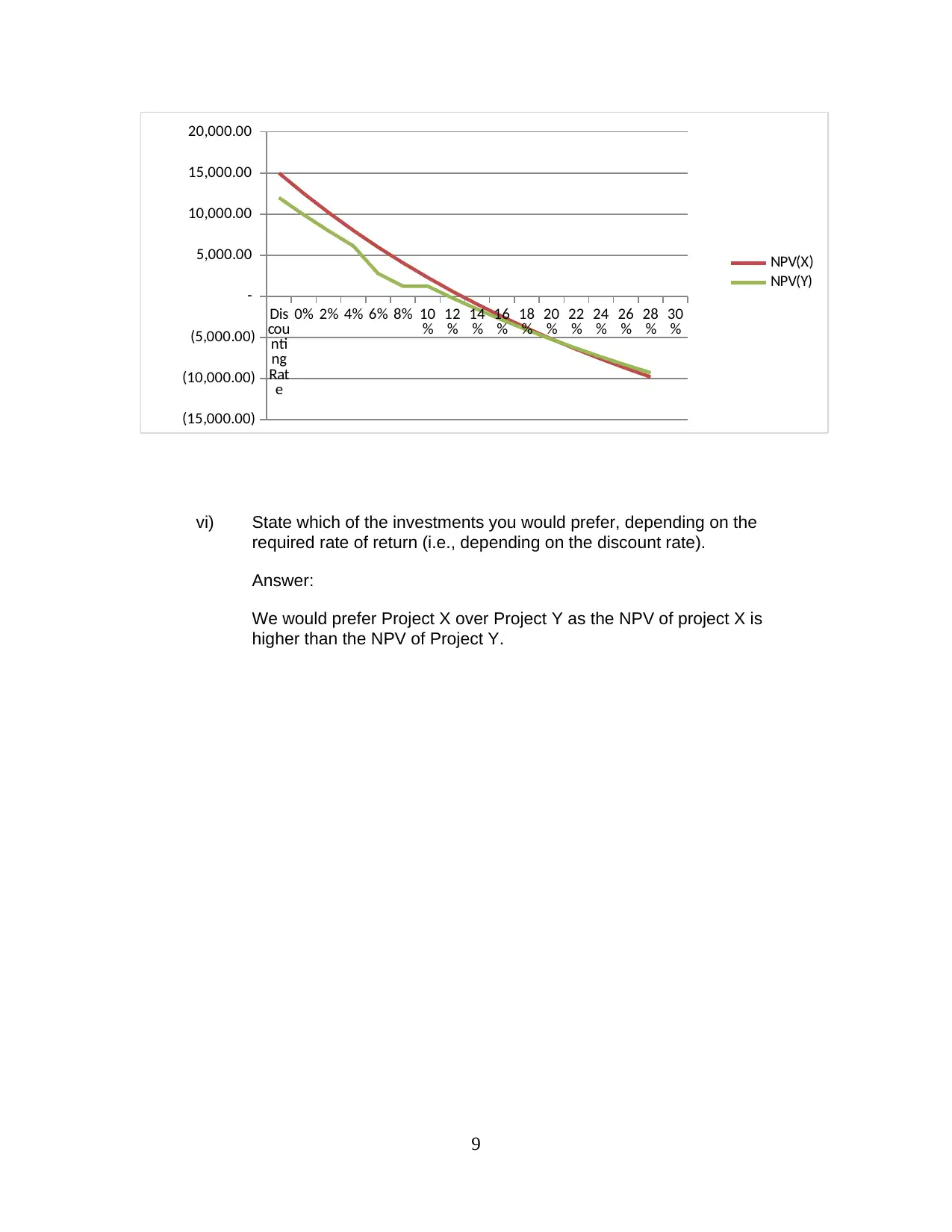

vi) State which of the investments you would prefer, depending on the

required rate of return (i.e., depending on the discount rate).

Answer:

We would prefer Project X over Project Y as the NPV of project X is

higher than the NPV of Project Y.

9

cou

nti

ng

Rat

e

0% 2% 4% 6% 8% 10

% 12

% 14

% 16

% 18

% 20

% 22

% 24

% 26

% 28

% 30

%

(15,000.00)

(10,000.00)

(5,000.00)

-

5,000.00

10,000.00

15,000.00

20,000.00

NPV(X)

NPV(Y)

vi) State which of the investments you would prefer, depending on the

required rate of return (i.e., depending on the discount rate).

Answer:

We would prefer Project X over Project Y as the NPV of project X is

higher than the NPV of Project Y.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

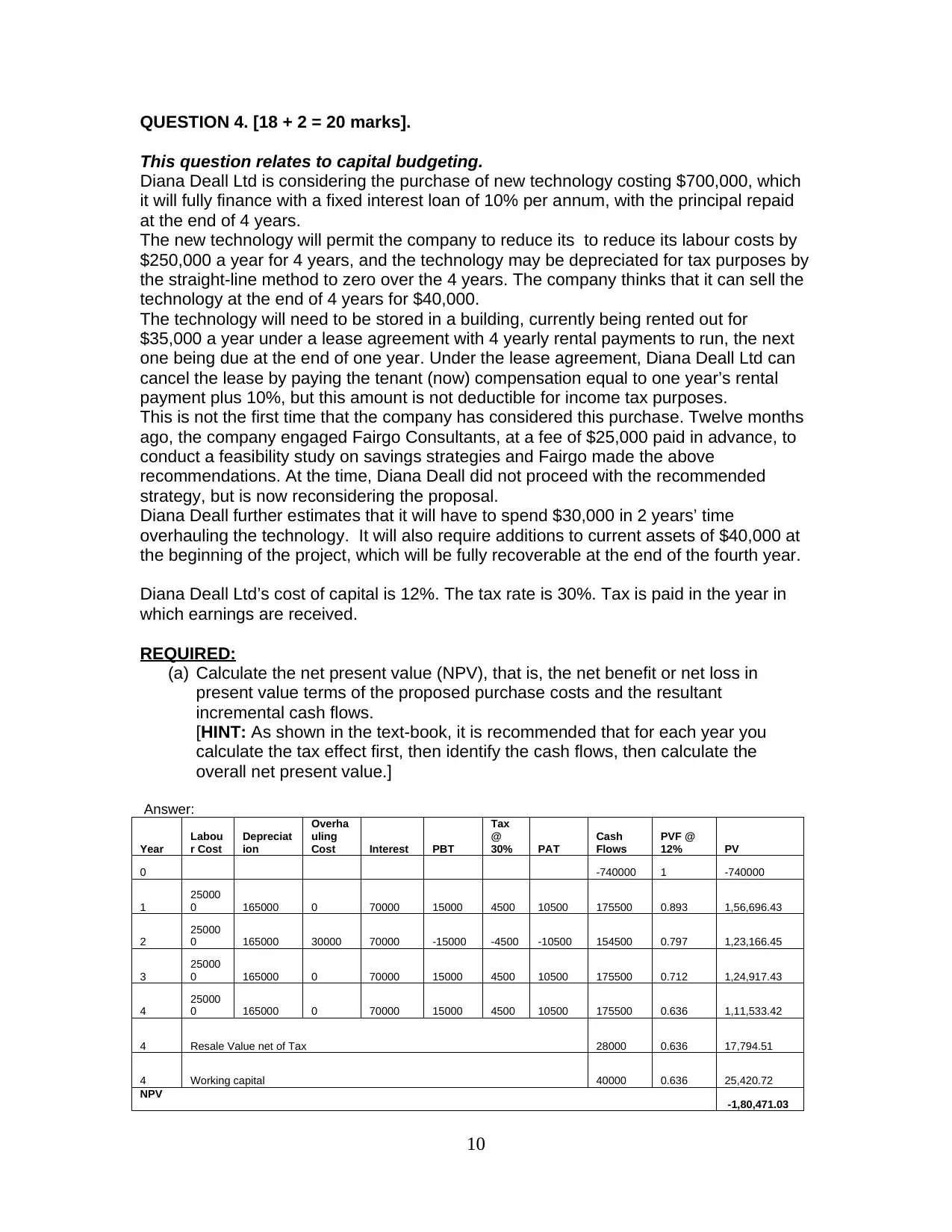

QUESTION 4. [18 + 2 = 20 marks].

This question relates to capital budgeting.

Diana Deall Ltd is considering the purchase of new technology costing $700,000, which

it will fully finance with a fixed interest loan of 10% per annum, with the principal repaid

at the end of 4 years.

The new technology will permit the company to reduce its to reduce its labour costs by

$250,000 a year for 4 years, and the technology may be depreciated for tax purposes by

the straight-line method to zero over the 4 years. The company thinks that it can sell the

technology at the end of 4 years for $40,000.

The technology will need to be stored in a building, currently being rented out for

$35,000 a year under a lease agreement with 4 yearly rental payments to run, the next

one being due at the end of one year. Under the lease agreement, Diana Deall Ltd can

cancel the lease by paying the tenant (now) compensation equal to one year’s rental

payment plus 10%, but this amount is not deductible for income tax purposes.

This is not the first time that the company has considered this purchase. Twelve months

ago, the company engaged Fairgo Consultants, at a fee of $25,000 paid in advance, to

conduct a feasibility study on savings strategies and Fairgo made the above

recommendations. At the time, Diana Deall did not proceed with the recommended

strategy, but is now reconsidering the proposal.

Diana Deall further estimates that it will have to spend $30,000 in 2 years’ time

overhauling the technology. It will also require additions to current assets of $40,000 at

the beginning of the project, which will be fully recoverable at the end of the fourth year.

Diana Deall Ltd’s cost of capital is 12%. The tax rate is 30%. Tax is paid in the year in

which earnings are received.

REQUIRED:

(a) Calculate the net present value (NPV), that is, the net benefit or net loss in

present value terms of the proposed purchase costs and the resultant

incremental cash flows.

[HINT: As shown in the text-book, it is recommended that for each year you

calculate the tax effect first, then identify the cash flows, then calculate the

overall net present value.]

Answer:

Year

Labou

r Cost

Depreciat

ion

Overha

uling

Cost Interest PBT

Tax

@

30% PAT

Cash

Flows

PVF @

12% PV

0 -740000 1 -740000

1

25000

0 165000 0 70000 15000 4500 10500 175500 0.893 1,56,696.43

2

25000

0 165000 30000 70000 -15000 -4500 -10500 154500 0.797 1,23,166.45

3

25000

0 165000 0 70000 15000 4500 10500 175500 0.712 1,24,917.43

4

25000

0 165000 0 70000 15000 4500 10500 175500 0.636 1,11,533.42

4 Resale Value net of Tax 28000 0.636 17,794.51

4 Working capital 40000 0.636 25,420.72

NPV -1,80,471.03

10

This question relates to capital budgeting.

Diana Deall Ltd is considering the purchase of new technology costing $700,000, which

it will fully finance with a fixed interest loan of 10% per annum, with the principal repaid

at the end of 4 years.

The new technology will permit the company to reduce its to reduce its labour costs by

$250,000 a year for 4 years, and the technology may be depreciated for tax purposes by

the straight-line method to zero over the 4 years. The company thinks that it can sell the

technology at the end of 4 years for $40,000.

The technology will need to be stored in a building, currently being rented out for

$35,000 a year under a lease agreement with 4 yearly rental payments to run, the next

one being due at the end of one year. Under the lease agreement, Diana Deall Ltd can

cancel the lease by paying the tenant (now) compensation equal to one year’s rental

payment plus 10%, but this amount is not deductible for income tax purposes.

This is not the first time that the company has considered this purchase. Twelve months

ago, the company engaged Fairgo Consultants, at a fee of $25,000 paid in advance, to

conduct a feasibility study on savings strategies and Fairgo made the above

recommendations. At the time, Diana Deall did not proceed with the recommended

strategy, but is now reconsidering the proposal.

Diana Deall further estimates that it will have to spend $30,000 in 2 years’ time

overhauling the technology. It will also require additions to current assets of $40,000 at

the beginning of the project, which will be fully recoverable at the end of the fourth year.

Diana Deall Ltd’s cost of capital is 12%. The tax rate is 30%. Tax is paid in the year in

which earnings are received.

REQUIRED:

(a) Calculate the net present value (NPV), that is, the net benefit or net loss in

present value terms of the proposed purchase costs and the resultant

incremental cash flows.

[HINT: As shown in the text-book, it is recommended that for each year you

calculate the tax effect first, then identify the cash flows, then calculate the

overall net present value.]

Answer:

Year

Labou

r Cost

Depreciat

ion

Overha

uling

Cost Interest PBT

Tax

@

30% PAT

Cash

Flows

PVF @

12% PV

0 -740000 1 -740000

1

25000

0 165000 0 70000 15000 4500 10500 175500 0.893 1,56,696.43

2

25000

0 165000 30000 70000 -15000 -4500 -10500 154500 0.797 1,23,166.45

3

25000

0 165000 0 70000 15000 4500 10500 175500 0.712 1,24,917.43

4

25000

0 165000 0 70000 15000 4500 10500 175500 0.636 1,11,533.42

4 Resale Value net of Tax 28000 0.636 17,794.51

4 Working capital 40000 0.636 25,420.72

NPV -1,80,471.03

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

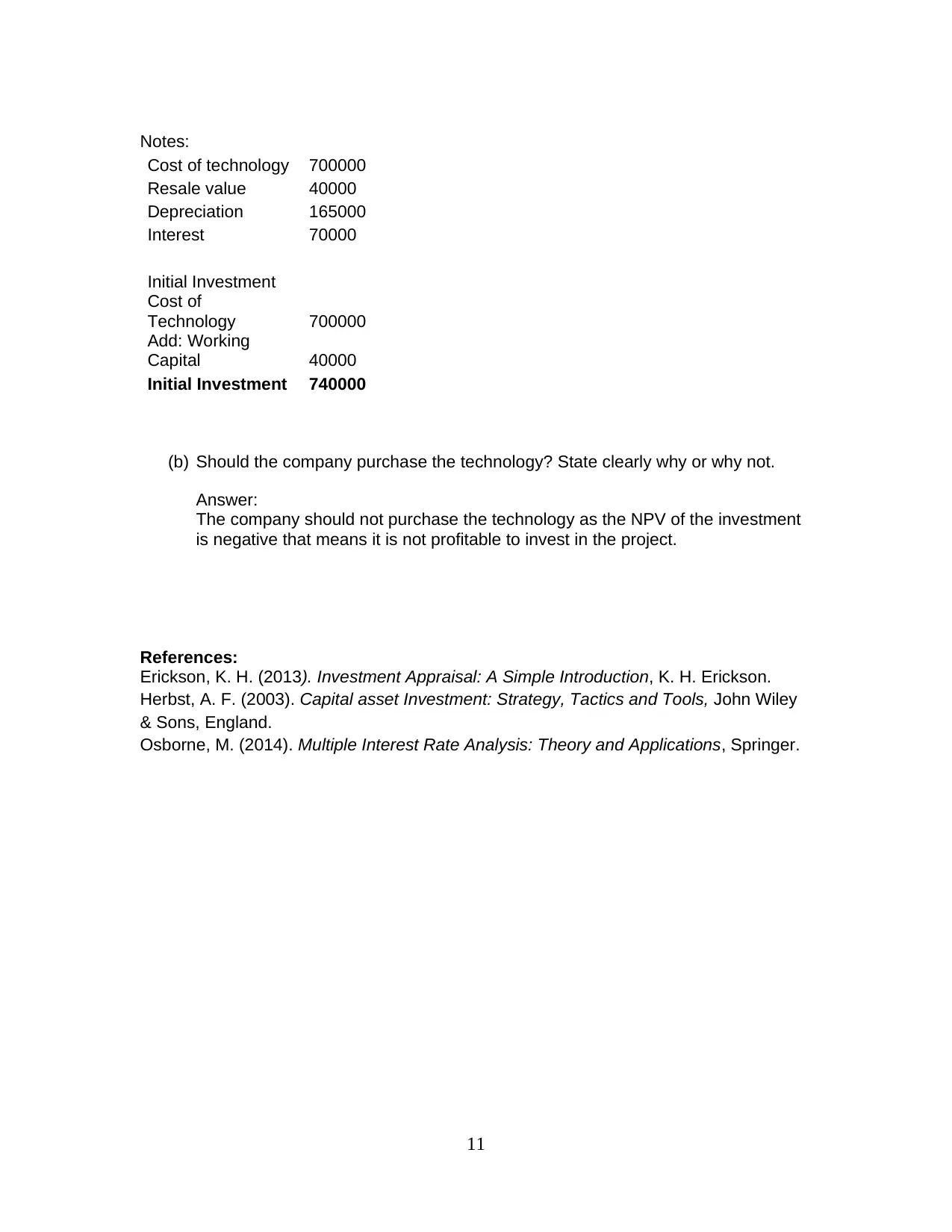

Notes:

Cost of technology 700000

Resale value 40000

Depreciation 165000

Interest 70000

Initial Investment

Cost of

Technology 700000

Add: Working

Capital 40000

Initial Investment 740000

(b) Should the company purchase the technology? State clearly why or why not.

Answer:

The company should not purchase the technology as the NPV of the investment

is negative that means it is not profitable to invest in the project.

References:

Erickson, K. H. (2013). Investment Appraisal: A Simple Introduction, K. H. Erickson.

Herbst, A. F. (2003). Capital asset Investment: Strategy, Tactics and Tools, John Wiley

& Sons, England.

Osborne, M. (2014). Multiple Interest Rate Analysis: Theory and Applications, Springer.

11

Cost of technology 700000

Resale value 40000

Depreciation 165000

Interest 70000

Initial Investment

Cost of

Technology 700000

Add: Working

Capital 40000

Initial Investment 740000

(b) Should the company purchase the technology? State clearly why or why not.

Answer:

The company should not purchase the technology as the NPV of the investment

is negative that means it is not profitable to invest in the project.

References:

Erickson, K. H. (2013). Investment Appraisal: A Simple Introduction, K. H. Erickson.

Herbst, A. F. (2003). Capital asset Investment: Strategy, Tactics and Tools, John Wiley

& Sons, England.

Osborne, M. (2014). Multiple Interest Rate Analysis: Theory and Applications, Springer.

11

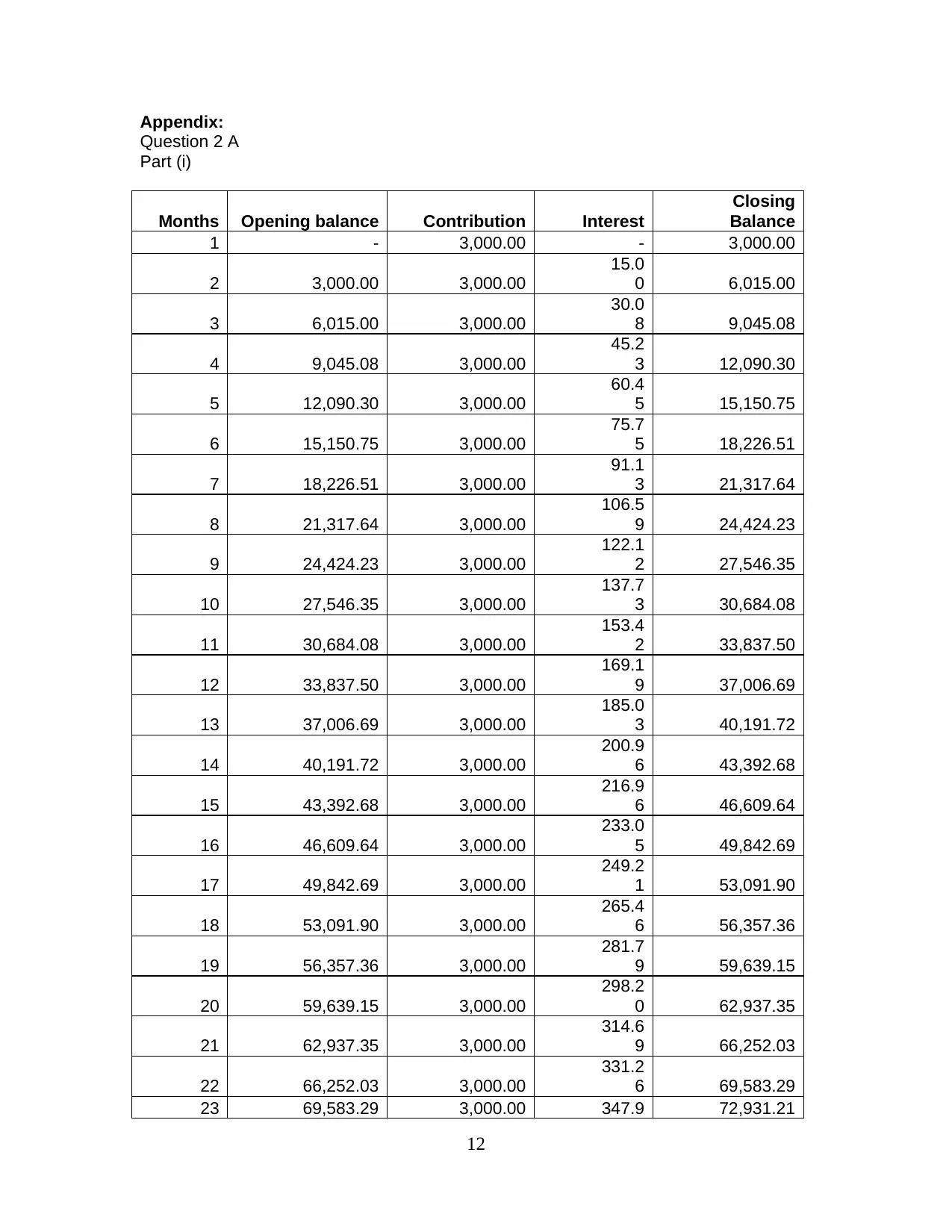

Appendix:

Question 2 A

Part (i)

Months Opening balance Contribution Interest

Closing

Balance

1 - 3,000.00 - 3,000.00

2 3,000.00 3,000.00

15.0

0 6,015.00

3 6,015.00 3,000.00

30.0

8 9,045.08

4 9,045.08 3,000.00

45.2

3 12,090.30

5 12,090.30 3,000.00

60.4

5 15,150.75

6 15,150.75 3,000.00

75.7

5 18,226.51

7 18,226.51 3,000.00

91.1

3 21,317.64

8 21,317.64 3,000.00

106.5

9 24,424.23

9 24,424.23 3,000.00

122.1

2 27,546.35

10 27,546.35 3,000.00

137.7

3 30,684.08

11 30,684.08 3,000.00

153.4

2 33,837.50

12 33,837.50 3,000.00

169.1

9 37,006.69

13 37,006.69 3,000.00

185.0

3 40,191.72

14 40,191.72 3,000.00

200.9

6 43,392.68

15 43,392.68 3,000.00

216.9

6 46,609.64

16 46,609.64 3,000.00

233.0

5 49,842.69

17 49,842.69 3,000.00

249.2

1 53,091.90

18 53,091.90 3,000.00

265.4

6 56,357.36

19 56,357.36 3,000.00

281.7

9 59,639.15

20 59,639.15 3,000.00

298.2

0 62,937.35

21 62,937.35 3,000.00

314.6

9 66,252.03

22 66,252.03 3,000.00

331.2

6 69,583.29

23 69,583.29 3,000.00 347.9 72,931.21

12

Question 2 A

Part (i)

Months Opening balance Contribution Interest

Closing

Balance

1 - 3,000.00 - 3,000.00

2 3,000.00 3,000.00

15.0

0 6,015.00

3 6,015.00 3,000.00

30.0

8 9,045.08

4 9,045.08 3,000.00

45.2

3 12,090.30

5 12,090.30 3,000.00

60.4

5 15,150.75

6 15,150.75 3,000.00

75.7

5 18,226.51

7 18,226.51 3,000.00

91.1

3 21,317.64

8 21,317.64 3,000.00

106.5

9 24,424.23

9 24,424.23 3,000.00

122.1

2 27,546.35

10 27,546.35 3,000.00

137.7

3 30,684.08

11 30,684.08 3,000.00

153.4

2 33,837.50

12 33,837.50 3,000.00

169.1

9 37,006.69

13 37,006.69 3,000.00

185.0

3 40,191.72

14 40,191.72 3,000.00

200.9

6 43,392.68

15 43,392.68 3,000.00

216.9

6 46,609.64

16 46,609.64 3,000.00

233.0

5 49,842.69

17 49,842.69 3,000.00

249.2

1 53,091.90

18 53,091.90 3,000.00

265.4

6 56,357.36

19 56,357.36 3,000.00

281.7

9 59,639.15

20 59,639.15 3,000.00

298.2

0 62,937.35

21 62,937.35 3,000.00

314.6

9 66,252.03

22 66,252.03 3,000.00

331.2

6 69,583.29

23 69,583.29 3,000.00 347.9 72,931.21

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 55

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.