Finance Report: Budget Analysis and Variance for Jackson Hotel

VerifiedAdded on 2023/01/12

|18

|4324

|69

Report

AI Summary

This report provides a comprehensive analysis of the Jackson Hotel's financial performance, focusing on budget management and variance analysis across multiple case studies. It examines variable and fixed costs, revenue streams, and expense categories. The report includes detailed calculations of variances between budgeted and actual figures for revenue, cost of sales, and expenses, highlighting areas of favorable and unfavorable performance. It also delves into strategies for cost control, inventory management, and supplier relationships, offering insights into operational improvements. The report presents findings on sales targets, cost deviations, and the overall financial health of the hotel, offering recommendations for future budgeting and financial planning.

Manage finance within a budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Case study A...............................................................................................................................1

Task 1 Monitor Budget...............................................................................................................1

Task 2 Calculation of variance....................................................................................................4

Task 3 .........................................................................................................................................5

Case study B....................................................................................................................................6

Task 1..........................................................................................................................................6

Task 2..........................................................................................................................................7

Task 3..........................................................................................................................................8

Case study C..................................................................................................................................10

Task 1........................................................................................................................................10

Task 2........................................................................................................................................10

Task 3........................................................................................................................................12

Task 4........................................................................................................................................12

Case study A...............................................................................................................................1

Task 1 Monitor Budget...............................................................................................................1

Task 2 Calculation of variance....................................................................................................4

Task 3 .........................................................................................................................................5

Case study B....................................................................................................................................6

Task 1..........................................................................................................................................6

Task 2..........................................................................................................................................7

Task 3..........................................................................................................................................8

Case study C..................................................................................................................................10

Task 1........................................................................................................................................10

Task 2........................................................................................................................................10

Task 3........................................................................................................................................12

Task 4........................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Case study A

Task 1 Monitor Budget

Question 1.

Variable direct cost

Some of the common variable direct cost for the Jackson hotel are as follows:

Laundry Maintenance.

Variable indirect cost

The major variable indirect cost to the hotel during the specific period are:

Wages Utilities

Fixed indirect cost

These are cost which are fixed for the period but do not have the impact over business

operation in direct way. Some the common fixed indirect cost are:

Rents

Salaries

Question 2

The main four categories which have been listed by the Jackson as per the allocation of

higher fund in the respective budgeted period these are named underneath:

Wages and on cost

Beverages purchase

Food purchase

Utilities

Question 3

It is very clear that company must have a proper plan to allocate the fund in significant

manner as without allocation limits overall expenditure can be greater than actual revenue which

further can result into financial problems like shortage of funds. Thus, Jackson hotel manager

prepare monthly budget in order to reduce the chances of financial pitfalls and as a results other

operation of hotel can also get impacted.

Question 4

1

Task 1 Monitor Budget

Question 1.

Variable direct cost

Some of the common variable direct cost for the Jackson hotel are as follows:

Laundry Maintenance.

Variable indirect cost

The major variable indirect cost to the hotel during the specific period are:

Wages Utilities

Fixed indirect cost

These are cost which are fixed for the period but do not have the impact over business

operation in direct way. Some the common fixed indirect cost are:

Rents

Salaries

Question 2

The main four categories which have been listed by the Jackson as per the allocation of

higher fund in the respective budgeted period these are named underneath:

Wages and on cost

Beverages purchase

Food purchase

Utilities

Question 3

It is very clear that company must have a proper plan to allocate the fund in significant

manner as without allocation limits overall expenditure can be greater than actual revenue which

further can result into financial problems like shortage of funds. Thus, Jackson hotel manager

prepare monthly budget in order to reduce the chances of financial pitfalls and as a results other

operation of hotel can also get impacted.

Question 4

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In hospitality industry, there is a specific need of communication of all plans and policies

made by the higher management which enables all worker in different department to understand

the need of company and perform work in most professional manner. This all help in reaching

the desired goals and maintain a good image of respective hotel in the competitive market. In the

context of Bistro department of Jackson Hotel the most important information which is needed to

be delivered to the entire team which make sure that they recognise the main target and objective

to be attained in respective period are as follows:

State of purpose:

Costing trends:

Market trends:

Outcome and results:

Question 5

There are number of common techniques which are used to promote awareness in

regards to methods of controlling cost or even increasing sales for the respective company to

reach the desired outcome. Some are elaborated underneath:

Conduct Inventory Consistently: Inventory of food, beverages and serving supplies

should be conducted at least once per week.

Pros:

It will show how food being used, lost or stolen.

Usage rate will help in deciding menu item costs. Helps in controlling and maintaining costs.

Cons: Staff might think that they are not trusted by management.

Impact on customer service: Customer will be happy to receive food at convenient price as compare to market.

Changing supplier: It always cheaper when orders in bulk but as of food industry,

purchase in huge quantity may not be possible. Hence join a purchase group can help Jackson to

enjoy lower food prices.

Pros:

Purchasing in huge quantity provides price advantage to respective hotel. Customer will enjoy cheap product nourishing with good quality products.

2

made by the higher management which enables all worker in different department to understand

the need of company and perform work in most professional manner. This all help in reaching

the desired goals and maintain a good image of respective hotel in the competitive market. In the

context of Bistro department of Jackson Hotel the most important information which is needed to

be delivered to the entire team which make sure that they recognise the main target and objective

to be attained in respective period are as follows:

State of purpose:

Costing trends:

Market trends:

Outcome and results:

Question 5

There are number of common techniques which are used to promote awareness in

regards to methods of controlling cost or even increasing sales for the respective company to

reach the desired outcome. Some are elaborated underneath:

Conduct Inventory Consistently: Inventory of food, beverages and serving supplies

should be conducted at least once per week.

Pros:

It will show how food being used, lost or stolen.

Usage rate will help in deciding menu item costs. Helps in controlling and maintaining costs.

Cons: Staff might think that they are not trusted by management.

Impact on customer service: Customer will be happy to receive food at convenient price as compare to market.

Changing supplier: It always cheaper when orders in bulk but as of food industry,

purchase in huge quantity may not be possible. Hence join a purchase group can help Jackson to

enjoy lower food prices.

Pros:

Purchasing in huge quantity provides price advantage to respective hotel. Customer will enjoy cheap product nourishing with good quality products.

2

Cons: It is not possible that all purchase group chain orders particular item at single point.

Do more prep work: Prepared food is more expensive than raw ingredients. For instance;

instead of purchasing chopped lettuce, kitchen department can buy heads of lettuce and cut by

chef itself.

Pros:

Buying raw food will help in maintaining overall cost of item. It will have both negative as well as positive impact on customer service.

Cons:

Preparing food at own place will increase the time of processing and requires more staff.

For instance; if Jackson manager assist with extra staff for processing semi finished

product than it will give reach taste to customer and thus having positive impact.

Review produce specifications: Jackson manager must know what it want to serve to its

customers and what quality it requires sometimes providing high quality ingredients and lesser

quality product creates less difference in taste but affect cost by much impact.

Pros:

It will help in reducing cost and maintenance of food price. It can impact negatively to company’s image if difference is much in taste of food.

Cons: Less quality ingredients can be tracked from regular customers using particular dish for

long time and it might be possible that he no longer use this service.

Manage taste: Keep record of all the waste your restaurant generates.

Use a waste chart and write down any of the following:

Food returned because it was made incorrectly.

Food that was spilled in the kitchen or on the floor.

Food that was burned in the kitchen.

Extra portion sizes that get thrown away.

By keeping track of this, you can keep better track of your inventory and manage your

food cost percentage. Additionally, then you can do what you can to reduce the instances of

waste.

3

Do more prep work: Prepared food is more expensive than raw ingredients. For instance;

instead of purchasing chopped lettuce, kitchen department can buy heads of lettuce and cut by

chef itself.

Pros:

Buying raw food will help in maintaining overall cost of item. It will have both negative as well as positive impact on customer service.

Cons:

Preparing food at own place will increase the time of processing and requires more staff.

For instance; if Jackson manager assist with extra staff for processing semi finished

product than it will give reach taste to customer and thus having positive impact.

Review produce specifications: Jackson manager must know what it want to serve to its

customers and what quality it requires sometimes providing high quality ingredients and lesser

quality product creates less difference in taste but affect cost by much impact.

Pros:

It will help in reducing cost and maintenance of food price. It can impact negatively to company’s image if difference is much in taste of food.

Cons: Less quality ingredients can be tracked from regular customers using particular dish for

long time and it might be possible that he no longer use this service.

Manage taste: Keep record of all the waste your restaurant generates.

Use a waste chart and write down any of the following:

Food returned because it was made incorrectly.

Food that was spilled in the kitchen or on the floor.

Food that was burned in the kitchen.

Extra portion sizes that get thrown away.

By keeping track of this, you can keep better track of your inventory and manage your

food cost percentage. Additionally, then you can do what you can to reduce the instances of

waste.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

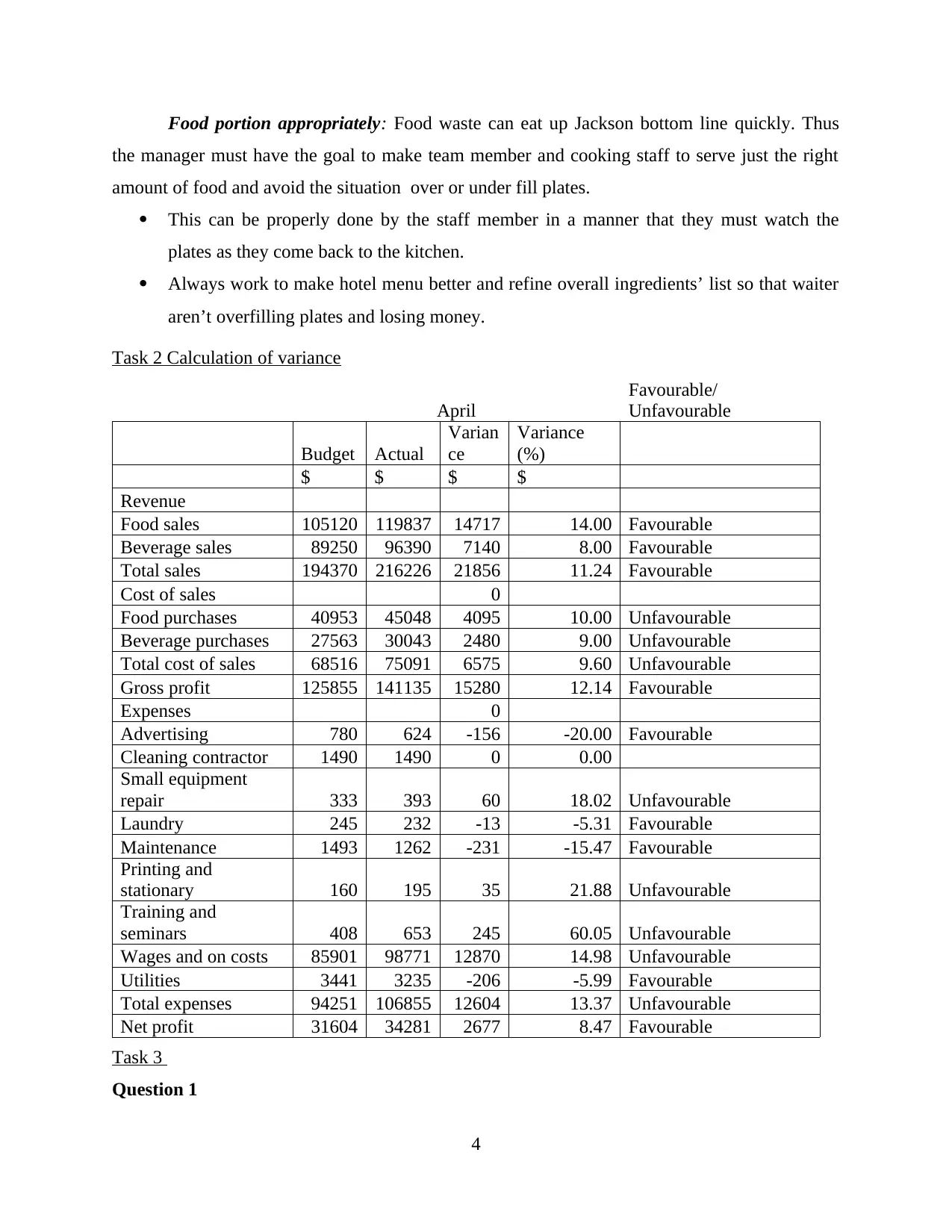

Food portion appropriately: Food waste can eat up Jackson bottom line quickly. Thus

the manager must have the goal to make team member and cooking staff to serve just the right

amount of food and avoid the situation over or under fill plates.

This can be properly done by the staff member in a manner that they must watch the

plates as they come back to the kitchen.

Always work to make hotel menu better and refine overall ingredients’ list so that waiter

aren’t overfilling plates and losing money.

Task 2 Calculation of variance

April

Favourable/

Unfavourable

Budget Actual

Varian

ce

Variance

(%)

$ $ $ $

Revenue

Food sales 105120 119837 14717 14.00 Favourable

Beverage sales 89250 96390 7140 8.00 Favourable

Total sales 194370 216226 21856 11.24 Favourable

Cost of sales 0

Food purchases 40953 45048 4095 10.00 Unfavourable

Beverage purchases 27563 30043 2480 9.00 Unfavourable

Total cost of sales 68516 75091 6575 9.60 Unfavourable

Gross profit 125855 141135 15280 12.14 Favourable

Expenses 0

Advertising 780 624 -156 -20.00 Favourable

Cleaning contractor 1490 1490 0 0.00

Small equipment

repair 333 393 60 18.02 Unfavourable

Laundry 245 232 -13 -5.31 Favourable

Maintenance 1493 1262 -231 -15.47 Favourable

Printing and

stationary 160 195 35 21.88 Unfavourable

Training and

seminars 408 653 245 60.05 Unfavourable

Wages and on costs 85901 98771 12870 14.98 Unfavourable

Utilities 3441 3235 -206 -5.99 Favourable

Total expenses 94251 106855 12604 13.37 Unfavourable

Net profit 31604 34281 2677 8.47 Favourable

Task 3

Question 1

4

the manager must have the goal to make team member and cooking staff to serve just the right

amount of food and avoid the situation over or under fill plates.

This can be properly done by the staff member in a manner that they must watch the

plates as they come back to the kitchen.

Always work to make hotel menu better and refine overall ingredients’ list so that waiter

aren’t overfilling plates and losing money.

Task 2 Calculation of variance

April

Favourable/

Unfavourable

Budget Actual

Varian

ce

Variance

(%)

$ $ $ $

Revenue

Food sales 105120 119837 14717 14.00 Favourable

Beverage sales 89250 96390 7140 8.00 Favourable

Total sales 194370 216226 21856 11.24 Favourable

Cost of sales 0

Food purchases 40953 45048 4095 10.00 Unfavourable

Beverage purchases 27563 30043 2480 9.00 Unfavourable

Total cost of sales 68516 75091 6575 9.60 Unfavourable

Gross profit 125855 141135 15280 12.14 Favourable

Expenses 0

Advertising 780 624 -156 -20.00 Favourable

Cleaning contractor 1490 1490 0 0.00

Small equipment

repair 333 393 60 18.02 Unfavourable

Laundry 245 232 -13 -5.31 Favourable

Maintenance 1493 1262 -231 -15.47 Favourable

Printing and

stationary 160 195 35 21.88 Unfavourable

Training and

seminars 408 653 245 60.05 Unfavourable

Wages and on costs 85901 98771 12870 14.98 Unfavourable

Utilities 3441 3235 -206 -5.99 Favourable

Total expenses 94251 106855 12604 13.37 Unfavourable

Net profit 31604 34281 2677 8.47 Favourable

Task 3

Question 1

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above calculation of variance it has been determined that the total sales for the

period of April is favourable because the budgeted sales was $ 194370 and actual sale was $

216226. As Food sales budgeted amount was $ 105120 and actual food sales was $ 119837, thus

variance was $ 14717 for the month April that define the difference was favourable by 14%. On

the other side, sales from beverages budgeted to amount $ 89250 and actual figures from selling

beverages in month April was $ 96390 thus the variance was favourable by 11.24 %.

Question 2

From the above table, it has been determined that there have been various variance in the

expenses category which are unfavourable for the company during the month of April such as

Wages and on costs, Training and seminars, Printing and stationary, Small equipment repair etc.

As a results there is no need of any furthermore investigate about these unfavourable variations

in figures because at the end company is earning a decent net profit which help in recovering all

extra funds.

Question 3

The above calculated variance table is helpful in determining that Yes Bistro is very well

operating throughout the April to meet its budgets targets. As a result there is a net income of $

34281.

Question 4

From the table above, it is identified that Wages and on cost have the highest budgeted

funds allocated because these expenses are related with cost paid by company to their labour.

These cost are strictly related to the operation of Bistro thus can not be reduce or cut down

because any cutting of cost related with wages can reduce the productivity of Bistro.

Question 5

Yes the overall Budget of April is beneficial in defining the status that budget of month

June will be attained by Bistro as results are favourable in the current period.

The table of variance shows that Printing and stationary, Wages and on costs and Small

equipment repair were the areas of under performing. Similarly, Utilities, Maintenance

and Laundry are the areas of over performing.

Outline of budget for May month:

5

period of April is favourable because the budgeted sales was $ 194370 and actual sale was $

216226. As Food sales budgeted amount was $ 105120 and actual food sales was $ 119837, thus

variance was $ 14717 for the month April that define the difference was favourable by 14%. On

the other side, sales from beverages budgeted to amount $ 89250 and actual figures from selling

beverages in month April was $ 96390 thus the variance was favourable by 11.24 %.

Question 2

From the above table, it has been determined that there have been various variance in the

expenses category which are unfavourable for the company during the month of April such as

Wages and on costs, Training and seminars, Printing and stationary, Small equipment repair etc.

As a results there is no need of any furthermore investigate about these unfavourable variations

in figures because at the end company is earning a decent net profit which help in recovering all

extra funds.

Question 3

The above calculated variance table is helpful in determining that Yes Bistro is very well

operating throughout the April to meet its budgets targets. As a result there is a net income of $

34281.

Question 4

From the table above, it is identified that Wages and on cost have the highest budgeted

funds allocated because these expenses are related with cost paid by company to their labour.

These cost are strictly related to the operation of Bistro thus can not be reduce or cut down

because any cutting of cost related with wages can reduce the productivity of Bistro.

Question 5

Yes the overall Budget of April is beneficial in defining the status that budget of month

June will be attained by Bistro as results are favourable in the current period.

The table of variance shows that Printing and stationary, Wages and on costs and Small

equipment repair were the areas of under performing. Similarly, Utilities, Maintenance

and Laundry are the areas of over performing.

Outline of budget for May month:

5

Some main organization factors have contributed in setting the budgeted target for the

next month is to increase the net profit, reduce the operating cost and most important is

to attain the superior position in competitive market.

Case study B

Task 1

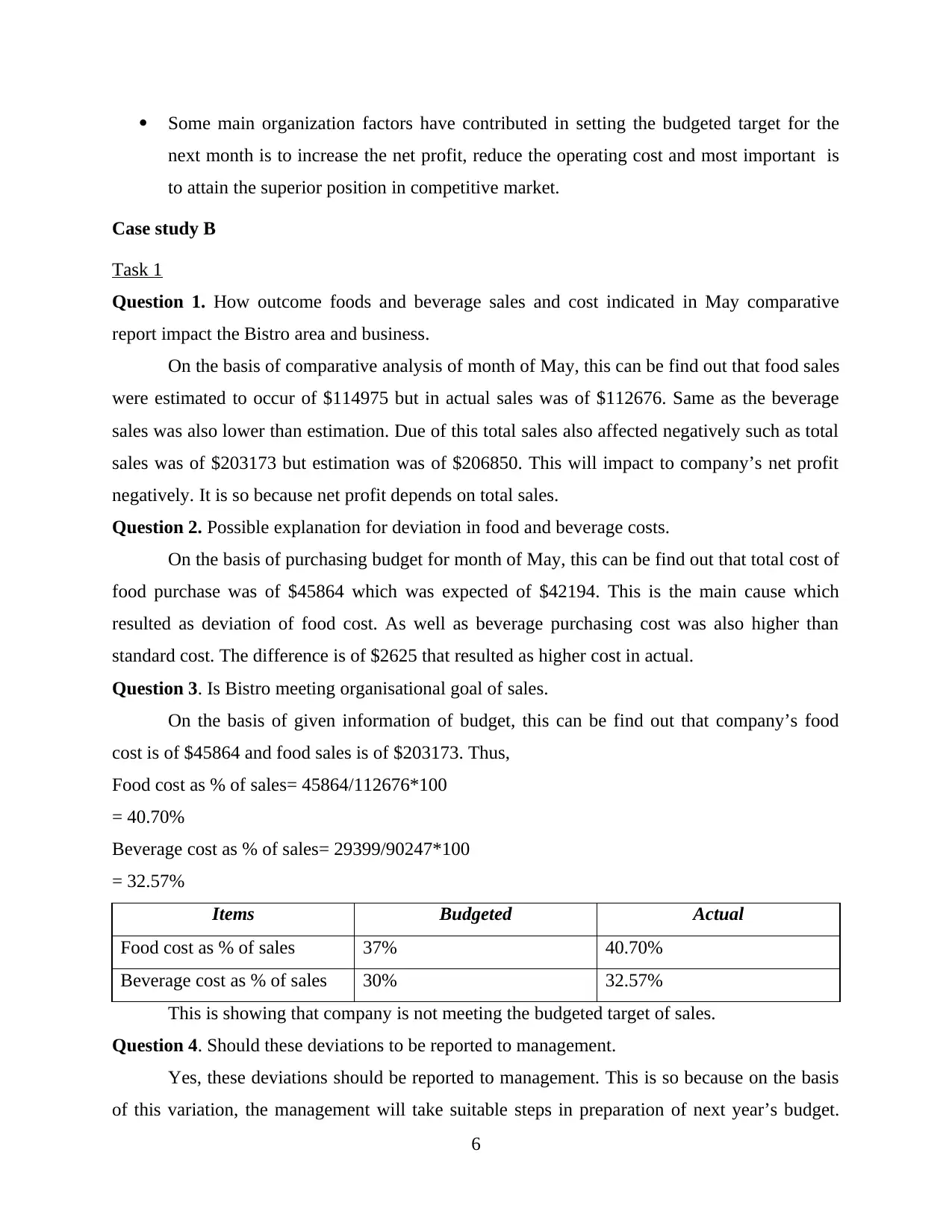

Question 1. How outcome foods and beverage sales and cost indicated in May comparative

report impact the Bistro area and business.

On the basis of comparative analysis of month of May, this can be find out that food sales

were estimated to occur of $114975 but in actual sales was of $112676. Same as the beverage

sales was also lower than estimation. Due of this total sales also affected negatively such as total

sales was of $203173 but estimation was of $206850. This will impact to company’s net profit

negatively. It is so because net profit depends on total sales.

Question 2. Possible explanation for deviation in food and beverage costs.

On the basis of purchasing budget for month of May, this can be find out that total cost of

food purchase was of $45864 which was expected of $42194. This is the main cause which

resulted as deviation of food cost. As well as beverage purchasing cost was also higher than

standard cost. The difference is of $2625 that resulted as higher cost in actual.

Question 3. Is Bistro meeting organisational goal of sales.

On the basis of given information of budget, this can be find out that company’s food

cost is of $45864 and food sales is of $203173. Thus,

Food cost as % of sales= 45864/112676*100

= 40.70%

Beverage cost as % of sales= 29399/90247*100

= 32.57%

Items Budgeted Actual

Food cost as % of sales 37% 40.70%

Beverage cost as % of sales 30% 32.57%

This is showing that company is not meeting the budgeted target of sales.

Question 4. Should these deviations to be reported to management.

Yes, these deviations should be reported to management. This is so because on the basis

of this variation, the management will take suitable steps in preparation of next year’s budget.

6

next month is to increase the net profit, reduce the operating cost and most important is

to attain the superior position in competitive market.

Case study B

Task 1

Question 1. How outcome foods and beverage sales and cost indicated in May comparative

report impact the Bistro area and business.

On the basis of comparative analysis of month of May, this can be find out that food sales

were estimated to occur of $114975 but in actual sales was of $112676. Same as the beverage

sales was also lower than estimation. Due of this total sales also affected negatively such as total

sales was of $203173 but estimation was of $206850. This will impact to company’s net profit

negatively. It is so because net profit depends on total sales.

Question 2. Possible explanation for deviation in food and beverage costs.

On the basis of purchasing budget for month of May, this can be find out that total cost of

food purchase was of $45864 which was expected of $42194. This is the main cause which

resulted as deviation of food cost. As well as beverage purchasing cost was also higher than

standard cost. The difference is of $2625 that resulted as higher cost in actual.

Question 3. Is Bistro meeting organisational goal of sales.

On the basis of given information of budget, this can be find out that company’s food

cost is of $45864 and food sales is of $203173. Thus,

Food cost as % of sales= 45864/112676*100

= 40.70%

Beverage cost as % of sales= 29399/90247*100

= 32.57%

Items Budgeted Actual

Food cost as % of sales 37% 40.70%

Beverage cost as % of sales 30% 32.57%

This is showing that company is not meeting the budgeted target of sales.

Question 4. Should these deviations to be reported to management.

Yes, these deviations should be reported to management. This is so because on the basis

of this variation, the management will take suitable steps in preparation of next year’s budget.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

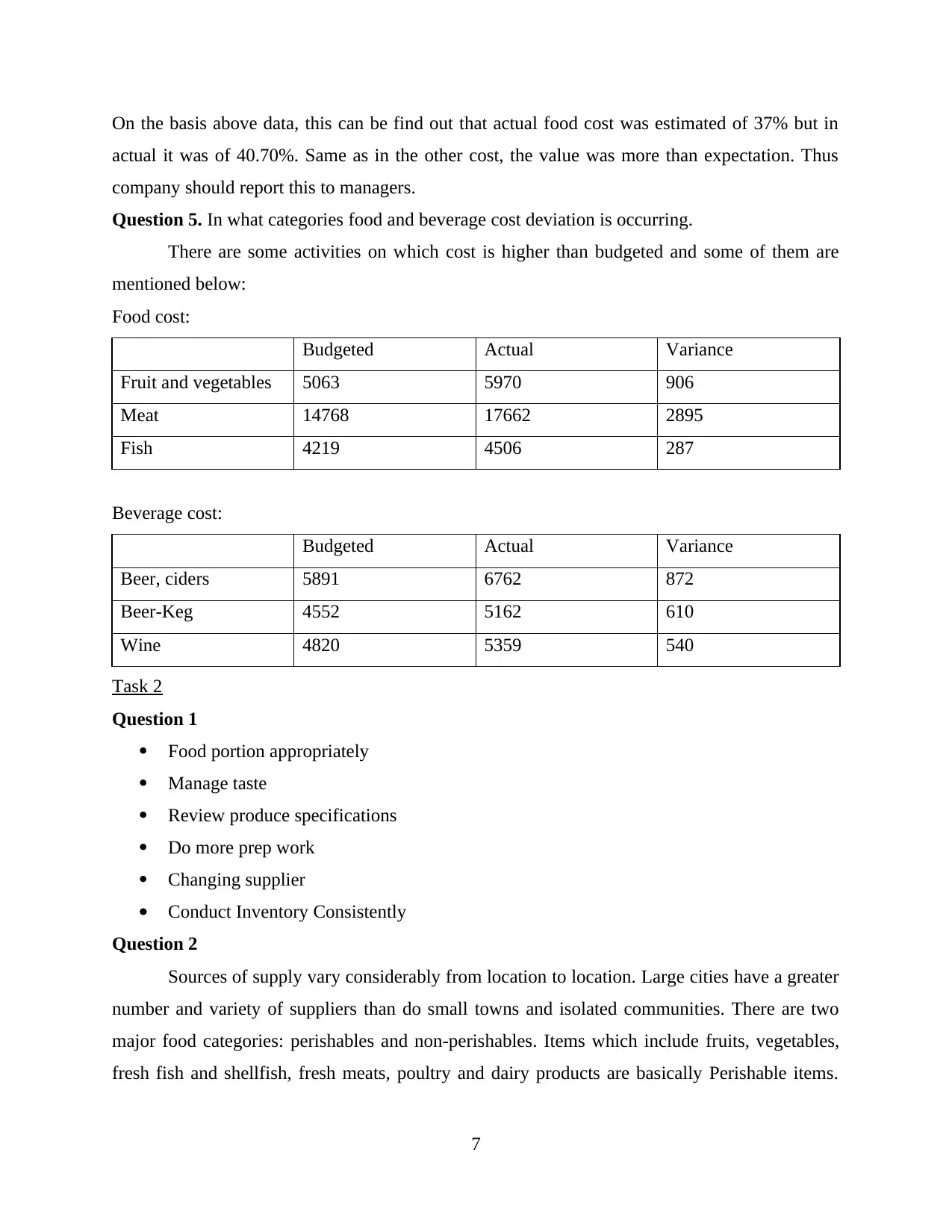

On the basis above data, this can be find out that actual food cost was estimated of 37% but in

actual it was of 40.70%. Same as in the other cost, the value was more than expectation. Thus

company should report this to managers.

Question 5. In what categories food and beverage cost deviation is occurring.

There are some activities on which cost is higher than budgeted and some of them are

mentioned below:

Food cost:

Budgeted Actual Variance

Fruit and vegetables 5063 5970 906

Meat 14768 17662 2895

Fish 4219 4506 287

Beverage cost:

Budgeted Actual Variance

Beer, ciders 5891 6762 872

Beer-Keg 4552 5162 610

Wine 4820 5359 540

Task 2

Question 1

Food portion appropriately

Manage taste

Review produce specifications

Do more prep work

Changing supplier

Conduct Inventory Consistently

Question 2

Sources of supply vary considerably from location to location. Large cities have a greater

number and variety of suppliers than do small towns and isolated communities. There are two

major food categories: perishables and non-perishables. Items which include fruits, vegetables,

fresh fish and shellfish, fresh meats, poultry and dairy products are basically Perishable items.

7

actual it was of 40.70%. Same as in the other cost, the value was more than expectation. Thus

company should report this to managers.

Question 5. In what categories food and beverage cost deviation is occurring.

There are some activities on which cost is higher than budgeted and some of them are

mentioned below:

Food cost:

Budgeted Actual Variance

Fruit and vegetables 5063 5970 906

Meat 14768 17662 2895

Fish 4219 4506 287

Beverage cost:

Budgeted Actual Variance

Beer, ciders 5891 6762 872

Beer-Keg 4552 5162 610

Wine 4820 5359 540

Task 2

Question 1

Food portion appropriately

Manage taste

Review produce specifications

Do more prep work

Changing supplier

Conduct Inventory Consistently

Question 2

Sources of supply vary considerably from location to location. Large cities have a greater

number and variety of suppliers than do small towns and isolated communities. There are two

major food categories: perishables and non-perishables. Items which include fruits, vegetables,

fresh fish and shellfish, fresh meats, poultry and dairy products are basically Perishable items.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Dry goods, flour, cereals, and miscellaneous items such as olives, pickles and other condiments

are basically Non-perishable items.

Question 3

The financial document which give the brief idea about the increase prices of supplier can

be:

Bistro Purchasing budget for particular month.

Invoice copy

Income statement for the specific month.

Question 4

As current supplier are selling food at higher cost and in case if manager determine other

reasonable supplier of same product in market then they make suitable decision for the

betterment of Bistro. Such as they should clearly pitch their old supplier to reduce the price,

supply regularly whenever there is a need of specific item otherwise they will move to new

supplier.

Question 5

In context of making any changes to the hotel supplier of fruit, vegetables and other

seafood, manager must concern the entire scenario with the Board of director of Hotel as well as

specific manager of supply chain manager in order to make profitable decision.

Task 3

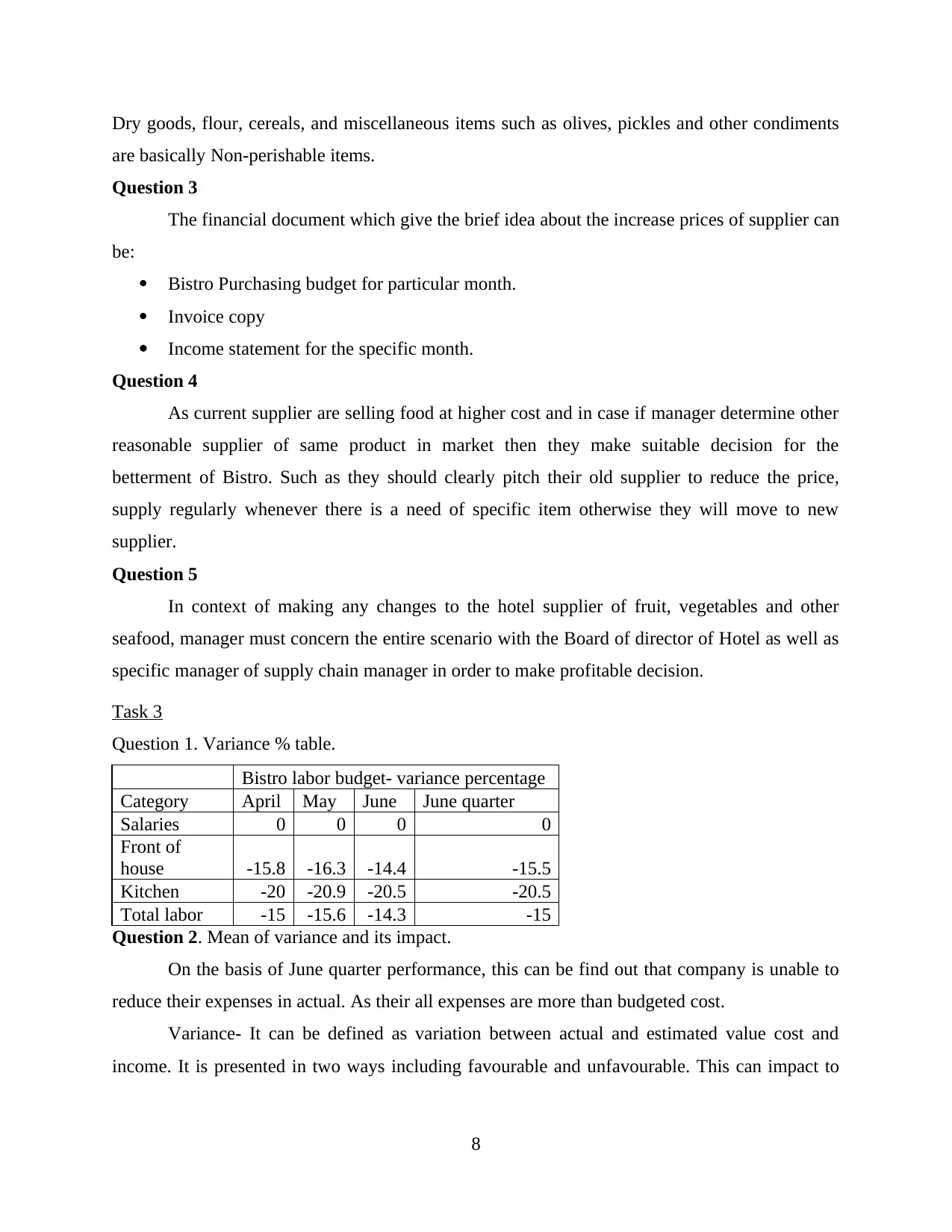

Question 1. Variance % table.

Bistro labor budget- variance percentage

Category April May June June quarter

Salaries 0 0 0 0

Front of

house -15.8 -16.3 -14.4 -15.5

Kitchen -20 -20.9 -20.5 -20.5

Total labor -15 -15.6 -14.3 -15

Question 2. Mean of variance and its impact.

On the basis of June quarter performance, this can be find out that company is unable to

reduce their expenses in actual. As their all expenses are more than budgeted cost.

Variance- It can be defined as variation between actual and estimated value cost and

income. It is presented in two ways including favourable and unfavourable. This can impact to

8

are basically Non-perishable items.

Question 3

The financial document which give the brief idea about the increase prices of supplier can

be:

Bistro Purchasing budget for particular month.

Invoice copy

Income statement for the specific month.

Question 4

As current supplier are selling food at higher cost and in case if manager determine other

reasonable supplier of same product in market then they make suitable decision for the

betterment of Bistro. Such as they should clearly pitch their old supplier to reduce the price,

supply regularly whenever there is a need of specific item otherwise they will move to new

supplier.

Question 5

In context of making any changes to the hotel supplier of fruit, vegetables and other

seafood, manager must concern the entire scenario with the Board of director of Hotel as well as

specific manager of supply chain manager in order to make profitable decision.

Task 3

Question 1. Variance % table.

Bistro labor budget- variance percentage

Category April May June June quarter

Salaries 0 0 0 0

Front of

house -15.8 -16.3 -14.4 -15.5

Kitchen -20 -20.9 -20.5 -20.5

Total labor -15 -15.6 -14.3 -15

Question 2. Mean of variance and its impact.

On the basis of June quarter performance, this can be find out that company is unable to

reduce their expenses in actual. As their all expenses are more than budgeted cost.

Variance- It can be defined as variation between actual and estimated value cost and

income. It is presented in two ways including favourable and unfavourable. This can impact to

8

companies’ goals. It is so because if expenses are in unfavourable condition than company will

not be able to generate higher profits.

Question 3. Impact of over staff on customer service level.

Due to more number of staff members, the level of customer service will surely increase

because there will be enough range of employees to serve customers in an effective manner.

Impact on team- There will be a positive impact on team members because if there will be more

staff than team will be able to manage more number of customers. But there will be a negative

impact also which is labour inefficiency.

Impact on budgeted target- Due to this budgeted target will also affected negatively because cost

will be higher.

Question 4

The main payroll documentation that can be used to maintain detail record as well as

manage funds related with labour cost during the budget period is:

Salary slips

Staffing level card

Question 5

At the time of making changes in the labour roster as well as modification in the desired

outcome there must be proper discussion with team leader managing staff, upper level manager

who actually delegate work and more importantly with cost accountant of hotel in order to revise

the entire payment structure for labour.

Question 6

This have been recommended that there must be not much changes to staffing levels

because changes will have a negative impact on customer service standards and food quality,

which will leading to an increase in customer complaints and as a result could lead to lower

customer numbers and sales revenue over the next year. Hence, it is strongly recommended only

smaller cuts to front of house team during busiest periods. It is also suggested to transfer more

work on casual staff during pick hours and customer feedback should be given more priority for

streamline work practices.

Case study C

Task 1.

Monthly actual June quarter actual results

9

not be able to generate higher profits.

Question 3. Impact of over staff on customer service level.

Due to more number of staff members, the level of customer service will surely increase

because there will be enough range of employees to serve customers in an effective manner.

Impact on team- There will be a positive impact on team members because if there will be more

staff than team will be able to manage more number of customers. But there will be a negative

impact also which is labour inefficiency.

Impact on budgeted target- Due to this budgeted target will also affected negatively because cost

will be higher.

Question 4

The main payroll documentation that can be used to maintain detail record as well as

manage funds related with labour cost during the budget period is:

Salary slips

Staffing level card

Question 5

At the time of making changes in the labour roster as well as modification in the desired

outcome there must be proper discussion with team leader managing staff, upper level manager

who actually delegate work and more importantly with cost accountant of hotel in order to revise

the entire payment structure for labour.

Question 6

This have been recommended that there must be not much changes to staffing levels

because changes will have a negative impact on customer service standards and food quality,

which will leading to an increase in customer complaints and as a result could lead to lower

customer numbers and sales revenue over the next year. Hence, it is strongly recommended only

smaller cuts to front of house team during busiest periods. It is also suggested to transfer more

work on casual staff during pick hours and customer feedback should be given more priority for

streamline work practices.

Case study C

Task 1.

Monthly actual June quarter actual results

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.