Macquarie University Finance Report: Watpac Acquisition Analysis

VerifiedAdded on 2022/08/18

|10

|2077

|12

Report

AI Summary

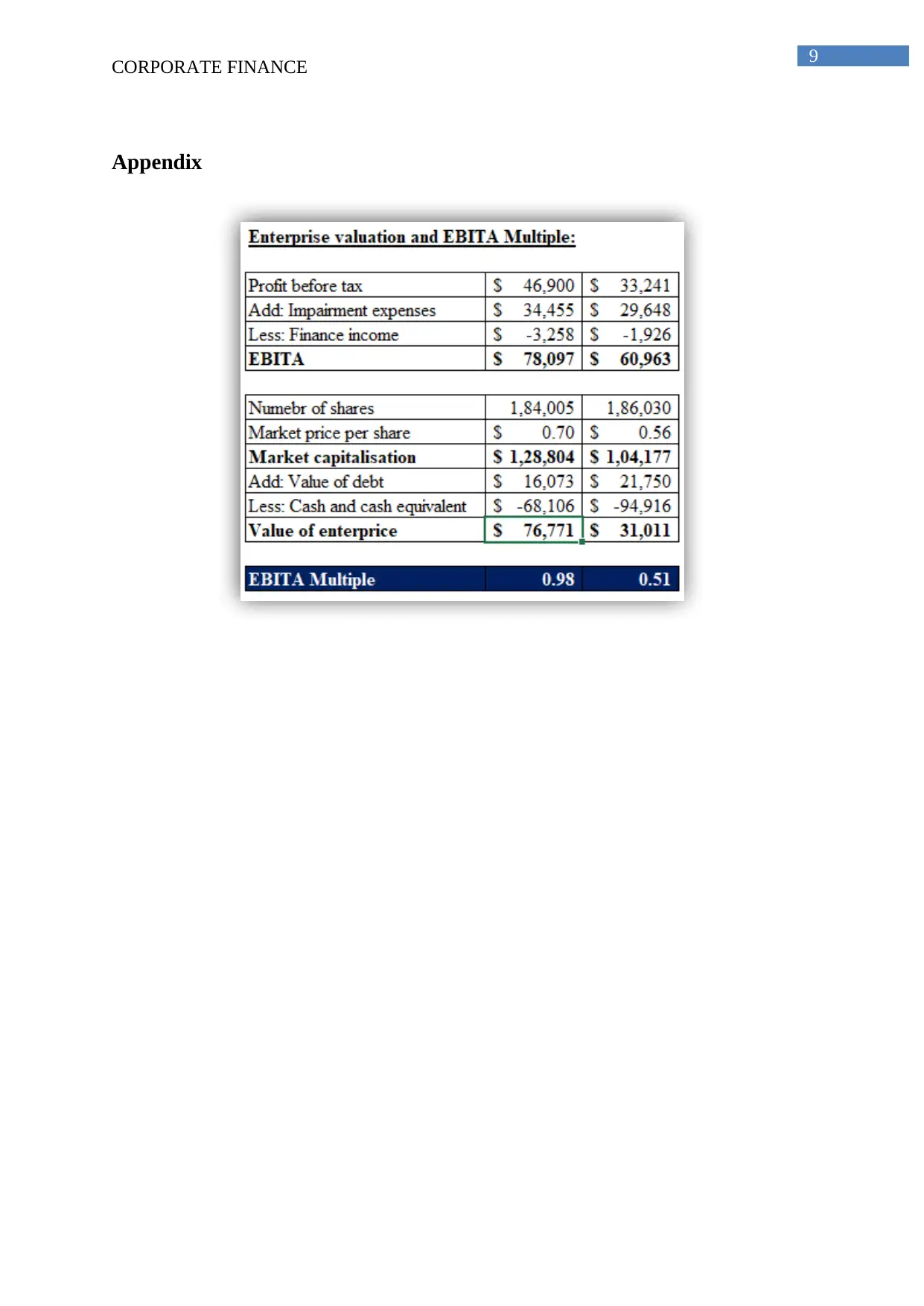

This report provides a comprehensive analysis of the Watpac acquisition by BESIX, focusing on financial valuation and appraisal. It begins with an executive summary that outlines the analysis and findings, including a recommendation regarding the acquisition and concerns arising from the appraisal. The report then delves into the valuation appraisal, discussing the methodologies used, such as the perpetuity model and EBITA multiplier, and the application of these methods to the case. It also assesses the offer made by BESIX, considering the ASX Settlement Operating Rules and the implications of the takeover bid. The report examines market capitalization, EBITA multiples, and the potential benefits of the acquisition, such as increased market share and access to resources. The analysis highlights the importance of considering the tax positions of shareholders and the limitations of valuation techniques, particularly the availability of detailed segment-specific data. Overall, the report offers a detailed financial perspective on the Watpac acquisition, providing valuable insights into the valuation process and the potential outcomes for stakeholders.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.