Business Finance Report: Fitt Ltd Working Capital and Budgeting

VerifiedAdded on 2023/01/10

|14

|3181

|57

Report

AI Summary

This report provides a comprehensive analysis of business finance, focusing on working capital management, cash flow analysis, and budgeting methods within the context of Fitt Ltd. The report begins by defining key financial terms such as profits, cash flow, working capital, receivables, inventory, and payables, and then explores the impact of changes in working capital on cash flow. It then analyzes the financial management of Fitt Ltd, evaluating its performance and identifying areas for improvement, particularly in relation to debt, inventory, and customer credit. Furthermore, the report proposes specific steps to improve the company's cash flow through effective working capital management, including incentives for timely payments, vendor negotiations, and debt restructuring. The second part of the report examines different budgeting methods, including traditional, rolling, and zero-based budgeting, evaluating their strengths and weaknesses. The report concludes with a recommendation for the most appropriate budgeting method for Fitt Ltd, considering its business expansion plans.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................3

Part 1................................................................................................................................................4

(i)............................................................................................................................................4

a. Meaning of profits and cash flow.......................................................................................4

b. Understanding working capital, receivables, inventory and payables...............................4

c. Impact of changes in working capital affect cash flow......................................................5

(ii) Analysing how company managed will affect its financial results..................................5

(iii) Steps for improving the cash flow of company through working capital management..6

EXECUTIVE SUMMARY.............................................................................................................8

Part 2................................................................................................................................................9

(i) Purpose of preparing budget with their strength and weaknesses.....................................9

(ii) Application of different budgeting methods for meeting the future cost management..11

(iii) Analysing the appropriate method of budgeting...........................................................12

REFERENCES..............................................................................................................................13

EXECUTIVE SUMMARY.............................................................................................................3

Part 1................................................................................................................................................4

(i)............................................................................................................................................4

a. Meaning of profits and cash flow.......................................................................................4

b. Understanding working capital, receivables, inventory and payables...............................4

c. Impact of changes in working capital affect cash flow......................................................5

(ii) Analysing how company managed will affect its financial results..................................5

(iii) Steps for improving the cash flow of company through working capital management..6

EXECUTIVE SUMMARY.............................................................................................................8

Part 2................................................................................................................................................9

(i) Purpose of preparing budget with their strength and weaknesses.....................................9

(ii) Application of different budgeting methods for meeting the future cost management..11

(iii) Analysing the appropriate method of budgeting...........................................................12

REFERENCES..............................................................................................................................13

EXECUTIVE SUMMARY

The part 1 of the report is about the understanding the basic financial terms and the

application of it in the organization name Fitt Ltd. It explains about the impact of working capital

over the cash flow of the business and steps that can be taken to manage the working capital and

cash flow of the business.

The part 1 of the report is about the understanding the basic financial terms and the

application of it in the organization name Fitt Ltd. It explains about the impact of working capital

over the cash flow of the business and steps that can be taken to manage the working capital and

cash flow of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 1

(i)

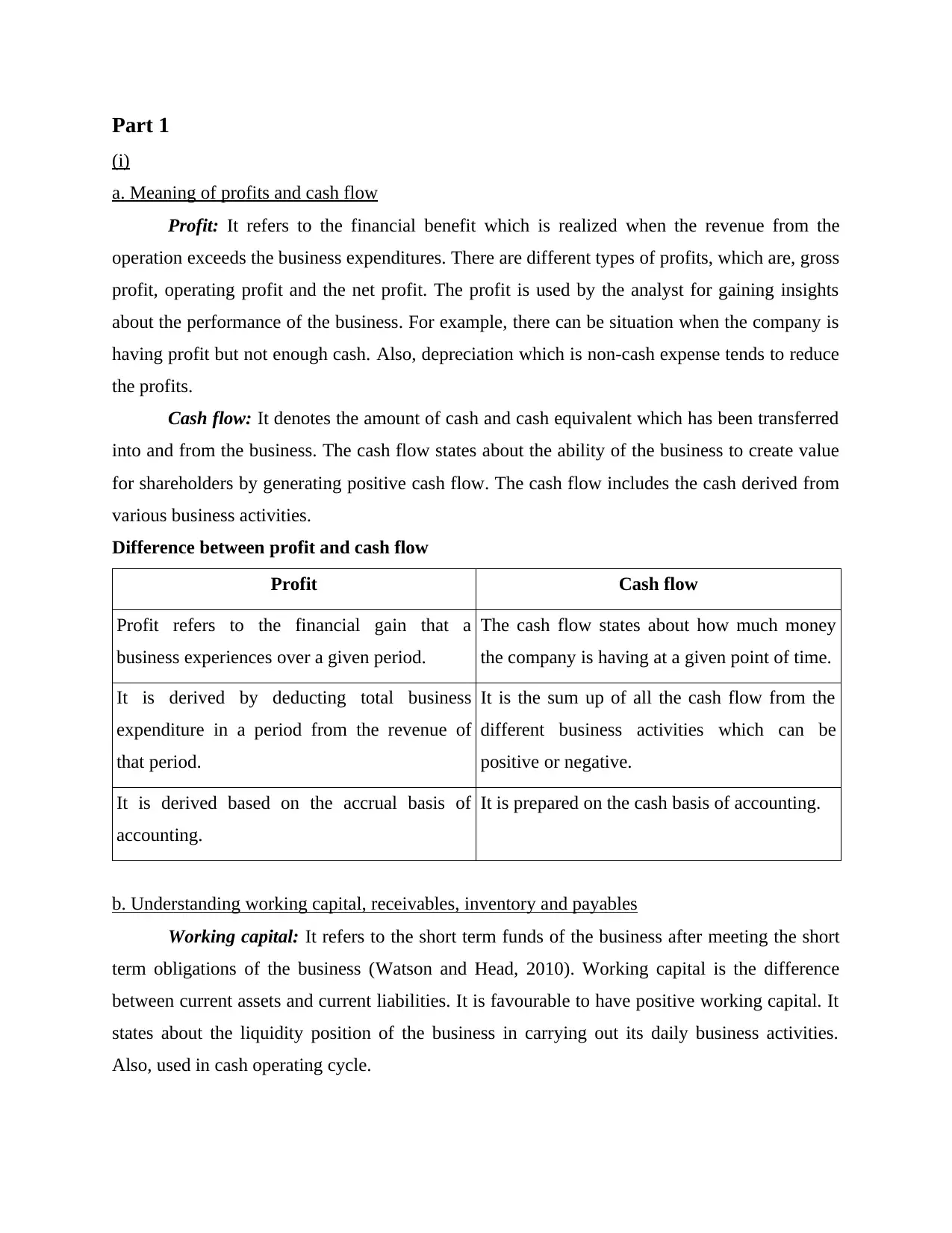

a. Meaning of profits and cash flow

Profit: It refers to the financial benefit which is realized when the revenue from the

operation exceeds the business expenditures. There are different types of profits, which are, gross

profit, operating profit and the net profit. The profit is used by the analyst for gaining insights

about the performance of the business. For example, there can be situation when the company is

having profit but not enough cash. Also, depreciation which is non-cash expense tends to reduce

the profits.

Cash flow: It denotes the amount of cash and cash equivalent which has been transferred

into and from the business. The cash flow states about the ability of the business to create value

for shareholders by generating positive cash flow. The cash flow includes the cash derived from

various business activities.

Difference between profit and cash flow

Profit Cash flow

Profit refers to the financial gain that a

business experiences over a given period.

The cash flow states about how much money

the company is having at a given point of time.

It is derived by deducting total business

expenditure in a period from the revenue of

that period.

It is the sum up of all the cash flow from the

different business activities which can be

positive or negative.

It is derived based on the accrual basis of

accounting.

It is prepared on the cash basis of accounting.

b. Understanding working capital, receivables, inventory and payables

Working capital: It refers to the short term funds of the business after meeting the short

term obligations of the business (Watson and Head, 2010). Working capital is the difference

between current assets and current liabilities. It is favourable to have positive working capital. It

states about the liquidity position of the business in carrying out its daily business activities.

Also, used in cash operating cycle.

(i)

a. Meaning of profits and cash flow

Profit: It refers to the financial benefit which is realized when the revenue from the

operation exceeds the business expenditures. There are different types of profits, which are, gross

profit, operating profit and the net profit. The profit is used by the analyst for gaining insights

about the performance of the business. For example, there can be situation when the company is

having profit but not enough cash. Also, depreciation which is non-cash expense tends to reduce

the profits.

Cash flow: It denotes the amount of cash and cash equivalent which has been transferred

into and from the business. The cash flow states about the ability of the business to create value

for shareholders by generating positive cash flow. The cash flow includes the cash derived from

various business activities.

Difference between profit and cash flow

Profit Cash flow

Profit refers to the financial gain that a

business experiences over a given period.

The cash flow states about how much money

the company is having at a given point of time.

It is derived by deducting total business

expenditure in a period from the revenue of

that period.

It is the sum up of all the cash flow from the

different business activities which can be

positive or negative.

It is derived based on the accrual basis of

accounting.

It is prepared on the cash basis of accounting.

b. Understanding working capital, receivables, inventory and payables

Working capital: It refers to the short term funds of the business after meeting the short

term obligations of the business (Watson and Head, 2010). Working capital is the difference

between current assets and current liabilities. It is favourable to have positive working capital. It

states about the liquidity position of the business in carrying out its daily business activities.

Also, used in cash operating cycle.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

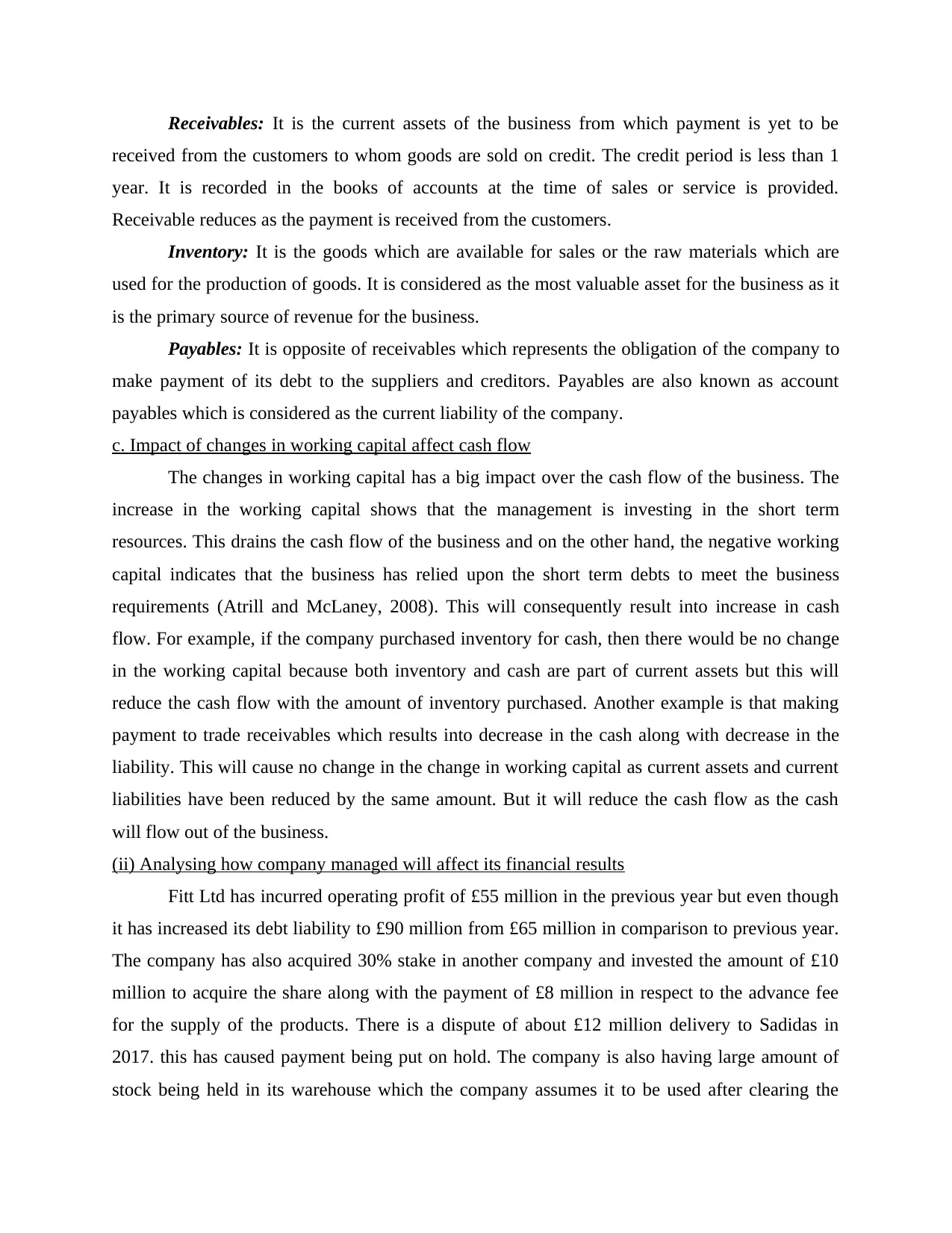

Receivables: It is the current assets of the business from which payment is yet to be

received from the customers to whom goods are sold on credit. The credit period is less than 1

year. It is recorded in the books of accounts at the time of sales or service is provided.

Receivable reduces as the payment is received from the customers.

Inventory: It is the goods which are available for sales or the raw materials which are

used for the production of goods. It is considered as the most valuable asset for the business as it

is the primary source of revenue for the business.

Payables: It is opposite of receivables which represents the obligation of the company to

make payment of its debt to the suppliers and creditors. Payables are also known as account

payables which is considered as the current liability of the company.

c. Impact of changes in working capital affect cash flow

The changes in working capital has a big impact over the cash flow of the business. The

increase in the working capital shows that the management is investing in the short term

resources. This drains the cash flow of the business and on the other hand, the negative working

capital indicates that the business has relied upon the short term debts to meet the business

requirements (Atrill and McLaney, 2008). This will consequently result into increase in cash

flow. For example, if the company purchased inventory for cash, then there would be no change

in the working capital because both inventory and cash are part of current assets but this will

reduce the cash flow with the amount of inventory purchased. Another example is that making

payment to trade receivables which results into decrease in the cash along with decrease in the

liability. This will cause no change in the change in working capital as current assets and current

liabilities have been reduced by the same amount. But it will reduce the cash flow as the cash

will flow out of the business.

(ii) Analysing how company managed will affect its financial results

Fitt Ltd has incurred operating profit of £55 million in the previous year but even though

it has increased its debt liability to £90 million from £65 million in comparison to previous year.

The company has also acquired 30% stake in another company and invested the amount of £10

million to acquire the share along with the payment of £8 million in respect to the advance fee

for the supply of the products. There is a dispute of about £12 million delivery to Sadidas in

2017. this has caused payment being put on hold. The company is also having large amount of

stock being held in its warehouse which the company assumes it to be used after clearing the

received from the customers to whom goods are sold on credit. The credit period is less than 1

year. It is recorded in the books of accounts at the time of sales or service is provided.

Receivable reduces as the payment is received from the customers.

Inventory: It is the goods which are available for sales or the raw materials which are

used for the production of goods. It is considered as the most valuable asset for the business as it

is the primary source of revenue for the business.

Payables: It is opposite of receivables which represents the obligation of the company to

make payment of its debt to the suppliers and creditors. Payables are also known as account

payables which is considered as the current liability of the company.

c. Impact of changes in working capital affect cash flow

The changes in working capital has a big impact over the cash flow of the business. The

increase in the working capital shows that the management is investing in the short term

resources. This drains the cash flow of the business and on the other hand, the negative working

capital indicates that the business has relied upon the short term debts to meet the business

requirements (Atrill and McLaney, 2008). This will consequently result into increase in cash

flow. For example, if the company purchased inventory for cash, then there would be no change

in the working capital because both inventory and cash are part of current assets but this will

reduce the cash flow with the amount of inventory purchased. Another example is that making

payment to trade receivables which results into decrease in the cash along with decrease in the

liability. This will cause no change in the change in working capital as current assets and current

liabilities have been reduced by the same amount. But it will reduce the cash flow as the cash

will flow out of the business.

(ii) Analysing how company managed will affect its financial results

Fitt Ltd has incurred operating profit of £55 million in the previous year but even though

it has increased its debt liability to £90 million from £65 million in comparison to previous year.

The company has also acquired 30% stake in another company and invested the amount of £10

million to acquire the share along with the payment of £8 million in respect to the advance fee

for the supply of the products. There is a dispute of about £12 million delivery to Sadidas in

2017. this has caused payment being put on hold. The company is also having large amount of

stock being held in its warehouse which the company assumes it to be used after clearing the

disputes. One of its key customer of Fitt Ltd is owned £12.5 million for the order which is being

placed last year. Based on the current management of Fitt Ltd, it can be said that the company is

not managed effectively. Fitt Ltd has invested a huge amount in capital investment which is

having a huge impact over its cash. The company is also holding excess amount of inventory

which is leading to increasing the unwanted inventory handling cost. Also, the management is

not effective in managing the credit provided to the customers and the collection team is not

trying hard to recover the due amount from the customers. Fitt Ltd has not taken advantage of

trade payables and has also used it limited.

(iii) Steps for improving the cash flow of company through working capital management

There are few steps that can be considered for improving the cash flow position of the

business by effectively managing its working capital requirements.

Providing attractive incentives to the customers if they make payment on time. Also,

identifying delinquency at the initial stage will help in taking proper actions at the right

time will helps in preventing the accounts from ageing. Fitt Ltd should avoid entering

into transactions with the customers having the record of defaulting.

Fitt Ltd the company make sure that all the debt payment is being made on time. The

electronic payment system will help in ensuring that the payment has been made on time

which will help in avoiding the situation of delayed payments and unwanted penalties.

The company should negotiate with the vendors and suppliers for better terms and

discounts. This can be possible only if the company establishes a good relation with the

suppliers (Aktas, Croci and Petmezas, 2015). The company should go for other vendors

as well for better deals. Building a cordial relationship will help Fitt Ltd in the times of

cash crunch and other uncertain events.

It should carefully examine the terms of debt and interest payment in order to know

whether it is eligible for any modification in the interest rate and lowering the amount of

instalment payment. Early paying off the debt will help the company in reducing the cost

of paying the future instalment. This will result into cost saving.

Fitt Ltd should try to resolve its ongoing issues and try to improve relationship with them

which will result into reducing the legal expenditure and managing the cash effectively.

Also, the company should sell off its unwanted assets which will help in gaining cash.

placed last year. Based on the current management of Fitt Ltd, it can be said that the company is

not managed effectively. Fitt Ltd has invested a huge amount in capital investment which is

having a huge impact over its cash. The company is also holding excess amount of inventory

which is leading to increasing the unwanted inventory handling cost. Also, the management is

not effective in managing the credit provided to the customers and the collection team is not

trying hard to recover the due amount from the customers. Fitt Ltd has not taken advantage of

trade payables and has also used it limited.

(iii) Steps for improving the cash flow of company through working capital management

There are few steps that can be considered for improving the cash flow position of the

business by effectively managing its working capital requirements.

Providing attractive incentives to the customers if they make payment on time. Also,

identifying delinquency at the initial stage will help in taking proper actions at the right

time will helps in preventing the accounts from ageing. Fitt Ltd should avoid entering

into transactions with the customers having the record of defaulting.

Fitt Ltd the company make sure that all the debt payment is being made on time. The

electronic payment system will help in ensuring that the payment has been made on time

which will help in avoiding the situation of delayed payments and unwanted penalties.

The company should negotiate with the vendors and suppliers for better terms and

discounts. This can be possible only if the company establishes a good relation with the

suppliers (Aktas, Croci and Petmezas, 2015). The company should go for other vendors

as well for better deals. Building a cordial relationship will help Fitt Ltd in the times of

cash crunch and other uncertain events.

It should carefully examine the terms of debt and interest payment in order to know

whether it is eligible for any modification in the interest rate and lowering the amount of

instalment payment. Early paying off the debt will help the company in reducing the cost

of paying the future instalment. This will result into cost saving.

Fitt Ltd should try to resolve its ongoing issues and try to improve relationship with them

which will result into reducing the legal expenditure and managing the cash effectively.

Also, the company should sell off its unwanted assets which will help in gaining cash.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The company should avoid the situation of overstocking and should make sure that the

goods are being sold as soon as possible and are not put idly in the warehouse. It should

cut out the products which are not gaining any profits.

Automated receivables and payable system should be introduced and make sure that the

collection team is strong enough to recover dues from the customers through attractive

rewards.

goods are being sold as soon as possible and are not put idly in the warehouse. It should

cut out the products which are not gaining any profits.

Automated receivables and payable system should be introduced and make sure that the

collection team is strong enough to recover dues from the customers through attractive

rewards.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The part B of the report states about the different types of budgets that can be used by

Phonus Plc. A detailed analysis of budgeting methods is carried out along with their strength and

weaknesses. Based on the findings, it is concluded that the Phonus Plc should go for activity

based budgeting method in respect to its business expansion plan.

The part B of the report states about the different types of budgets that can be used by

Phonus Plc. A detailed analysis of budgeting methods is carried out along with their strength and

weaknesses. Based on the findings, it is concluded that the Phonus Plc should go for activity

based budgeting method in respect to its business expansion plan.

Part 2

(i) Purpose of preparing budget with their strength and weaknesses

The Budgeting is used by the business organization for the purpose of business planning,

implementation and controlling. It is mainly prepared using the previous year budget or

performance as the basis for incremental amount to be added. It is also known as incremental

budget.

Traditional budgeting approaches

It is the process of preparing budget by looking at the past year's budget. This budget

exactly depends upon the previous year budget for developing the present year budget

(Weetman, 2010). It takes into consideration the changes in respect to inflation or any other

factors impacting the business. This approach is not useful for the newly established business

organization as it requires past years record.

Strengths:

This method is very simple and easy to use.

This helps in bringing stability in the organization as the staff of the organization are used

to it. It helps in taking quick decision as the problems can be easily identified

Weaknesses:

It is mainly relied upon the previous year's budget which may prove to be inaccurate or

wrong causing error in the budget.

There are chances of budget slack as the management can deliberately underestimate or

overestimate the budget as per the requirement.

It is rigid in nature and therefore changes cannot be made once it is prepared.

Other alternative budgets

Rolling budget

This budget is considered as the continuous budget as it is kept on revising after specific

time frame as the previous budget expires. It is also known as budget rollover. The rolling budget

is the extension of the present budget. It requires complete focus from the management for

implementing the changes. Such budget can be exceeded for 1 year.

Strengths:

After the budget is prepared, then it requires less time in extending it further.

(i) Purpose of preparing budget with their strength and weaknesses

The Budgeting is used by the business organization for the purpose of business planning,

implementation and controlling. It is mainly prepared using the previous year budget or

performance as the basis for incremental amount to be added. It is also known as incremental

budget.

Traditional budgeting approaches

It is the process of preparing budget by looking at the past year's budget. This budget

exactly depends upon the previous year budget for developing the present year budget

(Weetman, 2010). It takes into consideration the changes in respect to inflation or any other

factors impacting the business. This approach is not useful for the newly established business

organization as it requires past years record.

Strengths:

This method is very simple and easy to use.

This helps in bringing stability in the organization as the staff of the organization are used

to it. It helps in taking quick decision as the problems can be easily identified

Weaknesses:

It is mainly relied upon the previous year's budget which may prove to be inaccurate or

wrong causing error in the budget.

There are chances of budget slack as the management can deliberately underestimate or

overestimate the budget as per the requirement.

It is rigid in nature and therefore changes cannot be made once it is prepared.

Other alternative budgets

Rolling budget

This budget is considered as the continuous budget as it is kept on revising after specific

time frame as the previous budget expires. It is also known as budget rollover. The rolling budget

is the extension of the present budget. It requires complete focus from the management for

implementing the changes. Such budget can be exceeded for 1 year.

Strengths:

After the budget is prepared, then it requires less time in extending it further.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Rolling budget is very flexible as changes can be made in between. This budget is very useful in determining the areas of improvement.

Weaknesses:

Preparing this budget requires highly professional and skilled staff.

It is not suitable for the business organization where the working conditions are

fluctuating.

Initially preparing the budget is a very time-consuming process and incurs huge cost.

Zero based budgets

This method of budgeting is mostly preferred by the businesses. Under this approach, the

budget is initiated from the zero level (Drury, 2005). It involves complete analysis and

evaluation of each and every needs of the departments along with proper justification. After

analysis, the final budget si prepared. It more time consuming process as it undertakes analysis.

It follows certain criteria like identifying the business objectives, developing ways for achieving

goals, sources of financial resources etc.

Strengths:

This form of budgeting is useful for service based and non-profit organizations.

It is very flexible so relevant changes can be made even after it is prepared. This method provides complete information about the resources available with the

organization.

Weaknesses:

Preparing this budget requires a lot of time and efforts.

There are chances of personal bias being involved in decision-making.

It is based on cost and benefit analysis and the benefits of it can be seen in long run.

Activity-based budgets

Under this method, the budget is prepared taking into consideration the overhead

expenses of the business. This method does not use past historical data for preparing the budget.

It helps the company in analysing the cost drivers. Each activity that incur cost to the business is

analysed and researched and based on which the resources are being allocated. This budgeting

approach is used for bringing efficiency in the business activities and is considered as the activity

oriented approach.

Strengths:

Weaknesses:

Preparing this budget requires highly professional and skilled staff.

It is not suitable for the business organization where the working conditions are

fluctuating.

Initially preparing the budget is a very time-consuming process and incurs huge cost.

Zero based budgets

This method of budgeting is mostly preferred by the businesses. Under this approach, the

budget is initiated from the zero level (Drury, 2005). It involves complete analysis and

evaluation of each and every needs of the departments along with proper justification. After

analysis, the final budget si prepared. It more time consuming process as it undertakes analysis.

It follows certain criteria like identifying the business objectives, developing ways for achieving

goals, sources of financial resources etc.

Strengths:

This form of budgeting is useful for service based and non-profit organizations.

It is very flexible so relevant changes can be made even after it is prepared. This method provides complete information about the resources available with the

organization.

Weaknesses:

Preparing this budget requires a lot of time and efforts.

There are chances of personal bias being involved in decision-making.

It is based on cost and benefit analysis and the benefits of it can be seen in long run.

Activity-based budgets

Under this method, the budget is prepared taking into consideration the overhead

expenses of the business. This method does not use past historical data for preparing the budget.

It helps the company in analysing the cost drivers. Each activity that incur cost to the business is

analysed and researched and based on which the resources are being allocated. This budgeting

approach is used for bringing efficiency in the business activities and is considered as the activity

oriented approach.

Strengths:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It takes into account each activity which results into eliminating the unnecessary and non-

value added activities.

It helps in improving the relation between the company and its customers as by

eliminating unwanted activities will result into high quality product. This method helps in cost saving which consequently leads to competitive advantage.

Weaknesses:

It requires complete understanding about the various functional units of the organization,

otherwise it would lead to wrong budget.

This method is very complex and requires research and analysis of various factors.

It requires highly trained and skilled employees.

(ii) Application of different budgeting methods for meeting the future cost management

Following are the detailed analysis of the budgeting methods which are useful for Phonus

Plc.

Traditional budgeting approach

The organization Phonus Plc presently uses traditional method of budgeting. This has

been used by the organization for many years. This method helps the organization in exercising

coordination among other departments and functional units. Since, it is very easy to use which

makes it easy for the management to handle the activities (Atrill and McLaney, 2009). It can be

used where business conditions remains stable. For instance, the previous year budget amounted

to £2 million and therefore, the same budget will be used in the current year as well with little

changes in respect to inflation and other market conditions.

Rolling budget

This approach of budgeting takes into account the changes that are taking place. The

Phonus Plc can effectively use it in estimating the business plan and also relevant changes can be

made to the budget when required with respect to the goals. For example, the organization has

introduced a 12 month plan which starts from January to December. After completion of one

month, it adds another month to the budget so that it still be 12 months. From February of the

current year to the January of the following year.

Zero based budget

This form of budgeting can be used by Phonus Plc while carrying out the planning and

budgeting process. This budget is prepared from the zero level. For example, the organization

value added activities.

It helps in improving the relation between the company and its customers as by

eliminating unwanted activities will result into high quality product. This method helps in cost saving which consequently leads to competitive advantage.

Weaknesses:

It requires complete understanding about the various functional units of the organization,

otherwise it would lead to wrong budget.

This method is very complex and requires research and analysis of various factors.

It requires highly trained and skilled employees.

(ii) Application of different budgeting methods for meeting the future cost management

Following are the detailed analysis of the budgeting methods which are useful for Phonus

Plc.

Traditional budgeting approach

The organization Phonus Plc presently uses traditional method of budgeting. This has

been used by the organization for many years. This method helps the organization in exercising

coordination among other departments and functional units. Since, it is very easy to use which

makes it easy for the management to handle the activities (Atrill and McLaney, 2009). It can be

used where business conditions remains stable. For instance, the previous year budget amounted

to £2 million and therefore, the same budget will be used in the current year as well with little

changes in respect to inflation and other market conditions.

Rolling budget

This approach of budgeting takes into account the changes that are taking place. The

Phonus Plc can effectively use it in estimating the business plan and also relevant changes can be

made to the budget when required with respect to the goals. For example, the organization has

introduced a 12 month plan which starts from January to December. After completion of one

month, it adds another month to the budget so that it still be 12 months. From February of the

current year to the January of the following year.

Zero based budget

This form of budgeting can be used by Phonus Plc while carrying out the planning and

budgeting process. This budget is prepared from the zero level. For example, the organization

Phonus Plc hires additional staff which will result into increase in the budget of the company as

additional wages are required to be paid which will be added to the payroll expenses. This

approach requires application of lot of time and efforts in comparison to traditional method.

Thus, this method can be beneficial for the business.

Activity based budget

This budget is prepared considering various cost like direct material, labour and overhead

expenses. For instance, Phonus Plc has expects to sell 1000 units of goods in the coming month

which cost £5. Thus, the estimated COGS will be £5000. Thus, this budget can be used by the

organization as budget is being prepared based on activity and not on expected rate.

(iii) Analysing the appropriate method of budgeting

The traditional method of budgeting which was being used by the Phonus Plc for many

years. But this is not appropriate for the organization as it is mainly an adjustment which is being

made to the previous year budget on account of inflation or change in the level of sales. In place

of traditional method, the company can use activity based budgeting. It will help the organization

in meeting with the changing needs of the business and also helps in identifying unwanted and

unnecessary activities which can be removed resulting into cost saving. It will assist the

organization in knowing the profitability associated with the different activities being carried out.

Also, relevant changes can be made in the system resulting into accurate forecasting. Phonus Plc

is looking to expand it business so this approach can be appropriate for getting better results.

Since, it will take into consideration all the relevant factors which are required for preparing the

budget. It will help in cost saving, improving the quality of the product along with the right price

for gaining the customer base and taking competitive advantage.

additional wages are required to be paid which will be added to the payroll expenses. This

approach requires application of lot of time and efforts in comparison to traditional method.

Thus, this method can be beneficial for the business.

Activity based budget

This budget is prepared considering various cost like direct material, labour and overhead

expenses. For instance, Phonus Plc has expects to sell 1000 units of goods in the coming month

which cost £5. Thus, the estimated COGS will be £5000. Thus, this budget can be used by the

organization as budget is being prepared based on activity and not on expected rate.

(iii) Analysing the appropriate method of budgeting

The traditional method of budgeting which was being used by the Phonus Plc for many

years. But this is not appropriate for the organization as it is mainly an adjustment which is being

made to the previous year budget on account of inflation or change in the level of sales. In place

of traditional method, the company can use activity based budgeting. It will help the organization

in meeting with the changing needs of the business and also helps in identifying unwanted and

unnecessary activities which can be removed resulting into cost saving. It will assist the

organization in knowing the profitability associated with the different activities being carried out.

Also, relevant changes can be made in the system resulting into accurate forecasting. Phonus Plc

is looking to expand it business so this approach can be appropriate for getting better results.

Since, it will take into consideration all the relevant factors which are required for preparing the

budget. It will help in cost saving, improving the quality of the product along with the right price

for gaining the customer base and taking competitive advantage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.