HI5002 Finance: A2 Milk Company Performance Analysis Report

VerifiedAdded on 2022/11/16

|14

|4271

|219

Report

AI Summary

This report provides a comprehensive financial analysis of the A2 Milk Company Limited, an ASX-listed company. The analysis includes an overview of the company's operations, followed by a detailed examination of its financial performance using profitability and operating efficiency ratios from 2016 to 2018. The report evaluates gross margin, net margin, and return on capital employed (ROCE) to assess profitability. It also assesses operating efficiency through inventory turnover, receivables turnover, payables turnover, and cash conversion cycle. Furthermore, the report analyzes cash management, examining marketable securities, and conducts a sensitivity analysis to assess the impact of potential changes on project viability. The systemic and un-systemic risks are discussed, along with the company's dividend policy. Finally, the report provides recommendations to investors regarding investment in the A2 Milk Company Limited.

Running head: COMPANY PERFORMANCE ANALYSIS

Company Performance Analysis

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Company Performance Analysis

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COMPANY PERFORMANCE ANALYSIS

Abstract:

The evaluation of the financial performance of the organisations is deemed to be a vital

tool for gauging the existing financial performance along with gaining an overview about

their future performance. It has been evaluated that the A2 Milk Company Limited is

operating in the Australian milk and dairy industry. It has been found that the

organisation has maintained both stable profitability and operating efficiency positions.

Moreover, the proposed project is observed to provide significant benefits to the

organisation in future. However, it has been analysed that the organisation follows zero

dividend policy and hence, it does not provide any return to its shareholders over the

year. Since majority of the financial aspects are found to be positive, it is recommended

to the investor to invest in the shares of the A2 Milk Company Limited for earning better

returns in future.

Abstract:

The evaluation of the financial performance of the organisations is deemed to be a vital

tool for gauging the existing financial performance along with gaining an overview about

their future performance. It has been evaluated that the A2 Milk Company Limited is

operating in the Australian milk and dairy industry. It has been found that the

organisation has maintained both stable profitability and operating efficiency positions.

Moreover, the proposed project is observed to provide significant benefits to the

organisation in future. However, it has been analysed that the organisation follows zero

dividend policy and hence, it does not provide any return to its shareholders over the

year. Since majority of the financial aspects are found to be positive, it is recommended

to the investor to invest in the shares of the A2 Milk Company Limited for earning better

returns in future.

2COMPANY PERFORMANCE ANALYSIS

Table of Contents

I. Introduction:................................................................................................................3

II. Financial analysis of the A2 Milk Company Limited:.................................................3

2.1 Company description:..............................................................................................3

2.2 Computation and evaluation of performance ratios:................................................3

2.3 Cash management analysis:....................................................................................6

2.4 Sensitivity analysis:..................................................................................................7

2.5 Systemic and un-systemic risks:............................................................................10

2.6 Dividend payout ratio and dividend policy:............................................................10

III. Recommendation letter:.............................................................................................11

IV. Conclusion:.................................................................................................................11

References:......................................................................................................................12

Table of Contents

I. Introduction:................................................................................................................3

II. Financial analysis of the A2 Milk Company Limited:.................................................3

2.1 Company description:..............................................................................................3

2.2 Computation and evaluation of performance ratios:................................................3

2.3 Cash management analysis:....................................................................................6

2.4 Sensitivity analysis:..................................................................................................7

2.5 Systemic and un-systemic risks:............................................................................10

2.6 Dividend payout ratio and dividend policy:............................................................10

III. Recommendation letter:.............................................................................................11

IV. Conclusion:.................................................................................................................11

References:......................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COMPANY PERFORMANCE ANALYSIS

I. Introduction:

The evaluation of the financial performance of the organisations is deemed to be

a vital tool for gauging the existing financial performance along with gaining an overview

about their future performance (Alhabeeb 2014). Due to the same reason, the

investment professionals take into account the analysis of the financial performance of

the organisations as a vital part of the decision-making process related to investment.

There are various tools and methods used for meeting this purpose that include ratio

analysis of the chosen organisation, analysis of its risks, marketable securities and

others. The report intends to provide an in-depth overview of the financial performance

of an organisation listed in ASX in order to undertake investment decision. The

organisation chosen for this purpose is the A2 Milk Company Limited, which is a New

Zealand-based organisation dealing with milk-related products in the global market (The

a2 Milk Company 2019).

The entire report is segregated into different sections. The initial section would

provide a brief overview of the chosen organisation. The second section would focus on

the computation and analysis of various efficiency and profitability ratios of the A2 Milk

Company Limited. The next section would emphasise on the cash management

analysis of the firm by detecting its marketable securities. After this, sensitivity analysis

would be performed in order to ascertain the viability of the project. The next objective is

to determine the systemic and un-systemic risks of the A2 Milk Company. In addition,

the dividend payout ratio as well as the dividend policy of the firm would be identified.

Finally, the report would shed light on providing recommendation to the investors

regarding whether to invest in the organisation or not.

II. Financial analysis of the A2 Milk Company Limited:

2.1 Company description:

The A2 Milk Company Limited is an ASX 200 listed organisation engaging in the

commercialisation of intellectual property associated with A1 protein-free milk, which it

sells under the A2 milk brands as well as other milk-related products. Currently, the

head office of the organisation is in Sydney, Australia and it has been established in

2000. It operates in the dairy sector of Australia and it is one of the pioneers in the

entire sector (The a2 Milk Company 2019). The A2 Milk Company Limited has a

predecessor, which was A2 Corporation Limited. This is because A2 Corporation

Limited has sold its interest to A2 Australia, which is deemed to be the commencement

of operations of the A2 Milk Company Limited. However, since the organisation is a part

of the dairy and milk sector in Australia, it has to encounter significant competition and

some of its main rivals include Bega Cheese, Freedom Foods Group, Bellamy’s

Australia, Inghams Group and Freedom Foods Group.

2.2 Computation and evaluation of performance ratios:

The evaluation of operating efficiency and profitability is adjudged as the crucial

aspects in order to determine the existing financial health of the A2 Milk Company

Limited. The below discussion would represent the evaluation of various ratios under

operating efficiency and profitability of the concerned organisation:

Profitability evaluation:

The evaluation of the profitability ratios is made with the intent of determining the

capability of the organisation for income generation compared to all expenses needed

to be incurred for carrying out business activities (Atanasov and Black 2016). There are

I. Introduction:

The evaluation of the financial performance of the organisations is deemed to be

a vital tool for gauging the existing financial performance along with gaining an overview

about their future performance (Alhabeeb 2014). Due to the same reason, the

investment professionals take into account the analysis of the financial performance of

the organisations as a vital part of the decision-making process related to investment.

There are various tools and methods used for meeting this purpose that include ratio

analysis of the chosen organisation, analysis of its risks, marketable securities and

others. The report intends to provide an in-depth overview of the financial performance

of an organisation listed in ASX in order to undertake investment decision. The

organisation chosen for this purpose is the A2 Milk Company Limited, which is a New

Zealand-based organisation dealing with milk-related products in the global market (The

a2 Milk Company 2019).

The entire report is segregated into different sections. The initial section would

provide a brief overview of the chosen organisation. The second section would focus on

the computation and analysis of various efficiency and profitability ratios of the A2 Milk

Company Limited. The next section would emphasise on the cash management

analysis of the firm by detecting its marketable securities. After this, sensitivity analysis

would be performed in order to ascertain the viability of the project. The next objective is

to determine the systemic and un-systemic risks of the A2 Milk Company. In addition,

the dividend payout ratio as well as the dividend policy of the firm would be identified.

Finally, the report would shed light on providing recommendation to the investors

regarding whether to invest in the organisation or not.

II. Financial analysis of the A2 Milk Company Limited:

2.1 Company description:

The A2 Milk Company Limited is an ASX 200 listed organisation engaging in the

commercialisation of intellectual property associated with A1 protein-free milk, which it

sells under the A2 milk brands as well as other milk-related products. Currently, the

head office of the organisation is in Sydney, Australia and it has been established in

2000. It operates in the dairy sector of Australia and it is one of the pioneers in the

entire sector (The a2 Milk Company 2019). The A2 Milk Company Limited has a

predecessor, which was A2 Corporation Limited. This is because A2 Corporation

Limited has sold its interest to A2 Australia, which is deemed to be the commencement

of operations of the A2 Milk Company Limited. However, since the organisation is a part

of the dairy and milk sector in Australia, it has to encounter significant competition and

some of its main rivals include Bega Cheese, Freedom Foods Group, Bellamy’s

Australia, Inghams Group and Freedom Foods Group.

2.2 Computation and evaluation of performance ratios:

The evaluation of operating efficiency and profitability is adjudged as the crucial

aspects in order to determine the existing financial health of the A2 Milk Company

Limited. The below discussion would represent the evaluation of various ratios under

operating efficiency and profitability of the concerned organisation:

Profitability evaluation:

The evaluation of the profitability ratios is made with the intent of determining the

capability of the organisation for income generation compared to all expenses needed

to be incurred for carrying out business activities (Atanasov and Black 2016). There are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COMPANY PERFORMANCE ANALYSIS

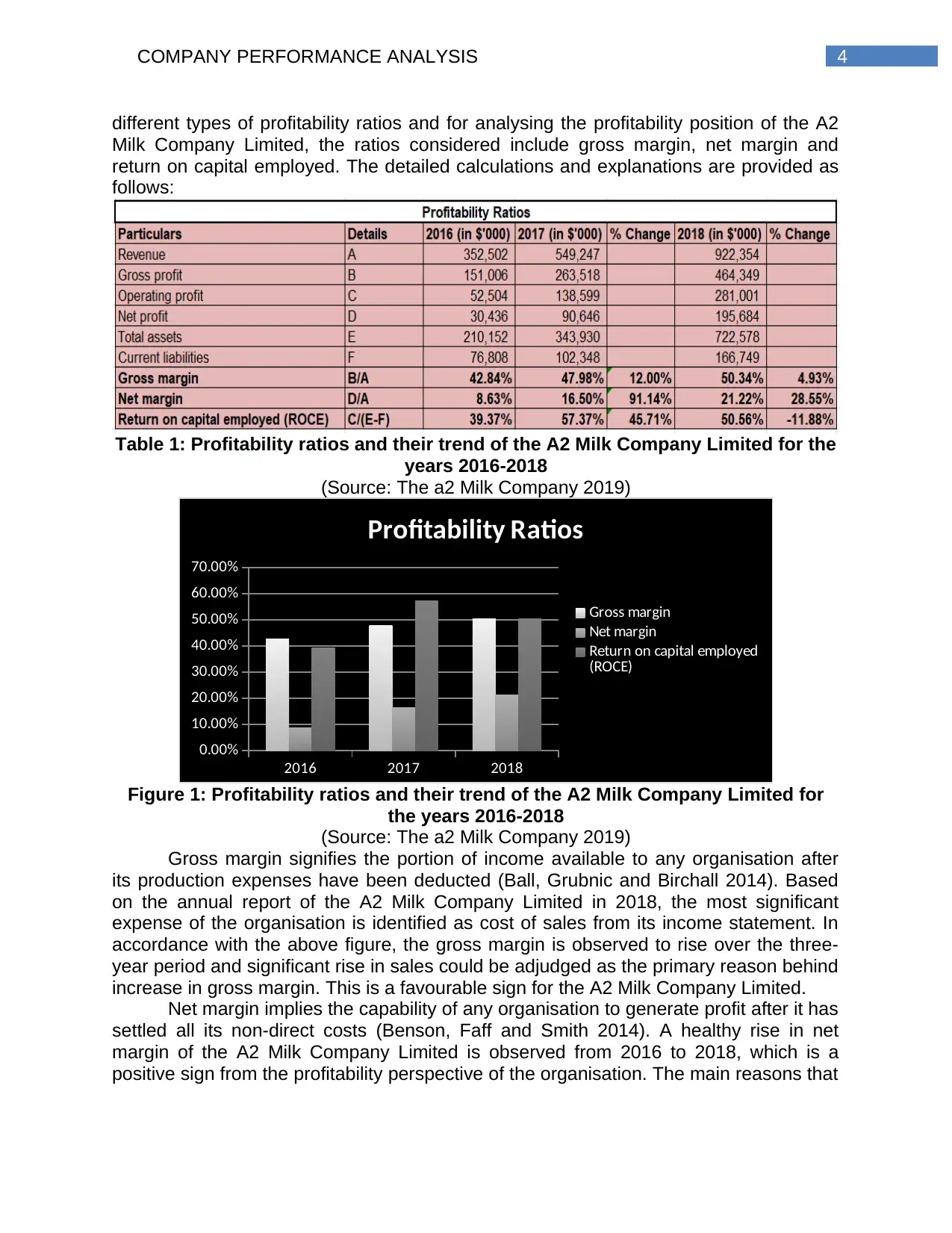

different types of profitability ratios and for analysing the profitability position of the A2

Milk Company Limited, the ratios considered include gross margin, net margin and

return on capital employed. The detailed calculations and explanations are provided as

follows:

Table 1: Profitability ratios and their trend of the A2 Milk Company Limited for the

years 2016-2018

(Source: The a2 Milk Company 2019)

2016 2017 2018

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Profitability Ratios

Gross margin

Net margin

Return on capital employed

(ROCE)

Figure 1: Profitability ratios and their trend of the A2 Milk Company Limited for

the years 2016-2018

(Source: The a2 Milk Company 2019)

Gross margin signifies the portion of income available to any organisation after

its production expenses have been deducted (Ball, Grubnic and Birchall 2014). Based

on the annual report of the A2 Milk Company Limited in 2018, the most significant

expense of the organisation is identified as cost of sales from its income statement. In

accordance with the above figure, the gross margin is observed to rise over the three-

year period and significant rise in sales could be adjudged as the primary reason behind

increase in gross margin. This is a favourable sign for the A2 Milk Company Limited.

Net margin implies the capability of any organisation to generate profit after it has

settled all its non-direct costs (Benson, Faff and Smith 2014). A healthy rise in net

margin of the A2 Milk Company Limited is observed from 2016 to 2018, which is a

positive sign from the profitability perspective of the organisation. The main reasons that

different types of profitability ratios and for analysing the profitability position of the A2

Milk Company Limited, the ratios considered include gross margin, net margin and

return on capital employed. The detailed calculations and explanations are provided as

follows:

Table 1: Profitability ratios and their trend of the A2 Milk Company Limited for the

years 2016-2018

(Source: The a2 Milk Company 2019)

2016 2017 2018

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Profitability Ratios

Gross margin

Net margin

Return on capital employed

(ROCE)

Figure 1: Profitability ratios and their trend of the A2 Milk Company Limited for

the years 2016-2018

(Source: The a2 Milk Company 2019)

Gross margin signifies the portion of income available to any organisation after

its production expenses have been deducted (Ball, Grubnic and Birchall 2014). Based

on the annual report of the A2 Milk Company Limited in 2018, the most significant

expense of the organisation is identified as cost of sales from its income statement. In

accordance with the above figure, the gross margin is observed to rise over the three-

year period and significant rise in sales could be adjudged as the primary reason behind

increase in gross margin. This is a favourable sign for the A2 Milk Company Limited.

Net margin implies the capability of any organisation to generate profit after it has

settled all its non-direct costs (Benson, Faff and Smith 2014). A healthy rise in net

margin of the A2 Milk Company Limited is observed from 2016 to 2018, which is a

positive sign from the profitability perspective of the organisation. The main reasons that

5COMPANY PERFORMANCE ANALYSIS

attributed to rise in net margin include decline in marketing costs and rise in interest

income.

ROCE gauges the capability of a firm to earn profit from the deployed capital by

comparing operating income to the employed capital (Brewer and Stout 2014).

According to the above figure, there is healthy rise in ROCE from 2016 to 2017 due to

considerable rise in operating income. However, this ratio has decreased in 2018 owing

to considerable rise in the amount of current liabilities.

By considering the above analysis, it is necessary to mention that the profitability

position of the A2 Milk Company Limited is stable because it has witnessed

considerable increase in gross profit as well as net profit. However, emphasis needs to

be provided in order to improve ROCE in future, as it is one of the vital indicators of

business profitability.

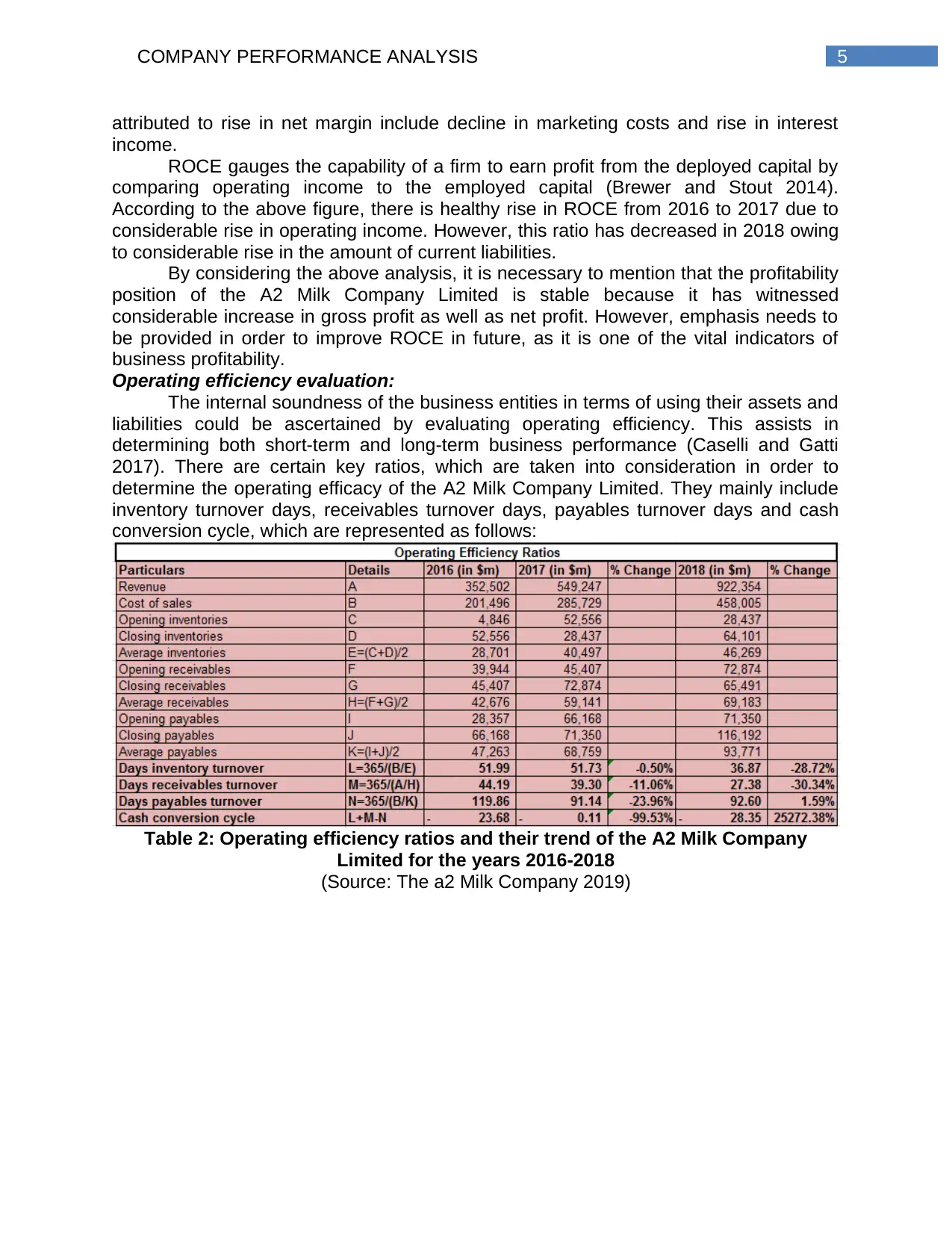

Operating efficiency evaluation:

The internal soundness of the business entities in terms of using their assets and

liabilities could be ascertained by evaluating operating efficiency. This assists in

determining both short-term and long-term business performance (Caselli and Gatti

2017). There are certain key ratios, which are taken into consideration in order to

determine the operating efficacy of the A2 Milk Company Limited. They mainly include

inventory turnover days, receivables turnover days, payables turnover days and cash

conversion cycle, which are represented as follows:

Table 2: Operating efficiency ratios and their trend of the A2 Milk Company

Limited for the years 2016-2018

(Source: The a2 Milk Company 2019)

attributed to rise in net margin include decline in marketing costs and rise in interest

income.

ROCE gauges the capability of a firm to earn profit from the deployed capital by

comparing operating income to the employed capital (Brewer and Stout 2014).

According to the above figure, there is healthy rise in ROCE from 2016 to 2017 due to

considerable rise in operating income. However, this ratio has decreased in 2018 owing

to considerable rise in the amount of current liabilities.

By considering the above analysis, it is necessary to mention that the profitability

position of the A2 Milk Company Limited is stable because it has witnessed

considerable increase in gross profit as well as net profit. However, emphasis needs to

be provided in order to improve ROCE in future, as it is one of the vital indicators of

business profitability.

Operating efficiency evaluation:

The internal soundness of the business entities in terms of using their assets and

liabilities could be ascertained by evaluating operating efficiency. This assists in

determining both short-term and long-term business performance (Caselli and Gatti

2017). There are certain key ratios, which are taken into consideration in order to

determine the operating efficacy of the A2 Milk Company Limited. They mainly include

inventory turnover days, receivables turnover days, payables turnover days and cash

conversion cycle, which are represented as follows:

Table 2: Operating efficiency ratios and their trend of the A2 Milk Company

Limited for the years 2016-2018

(Source: The a2 Milk Company 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

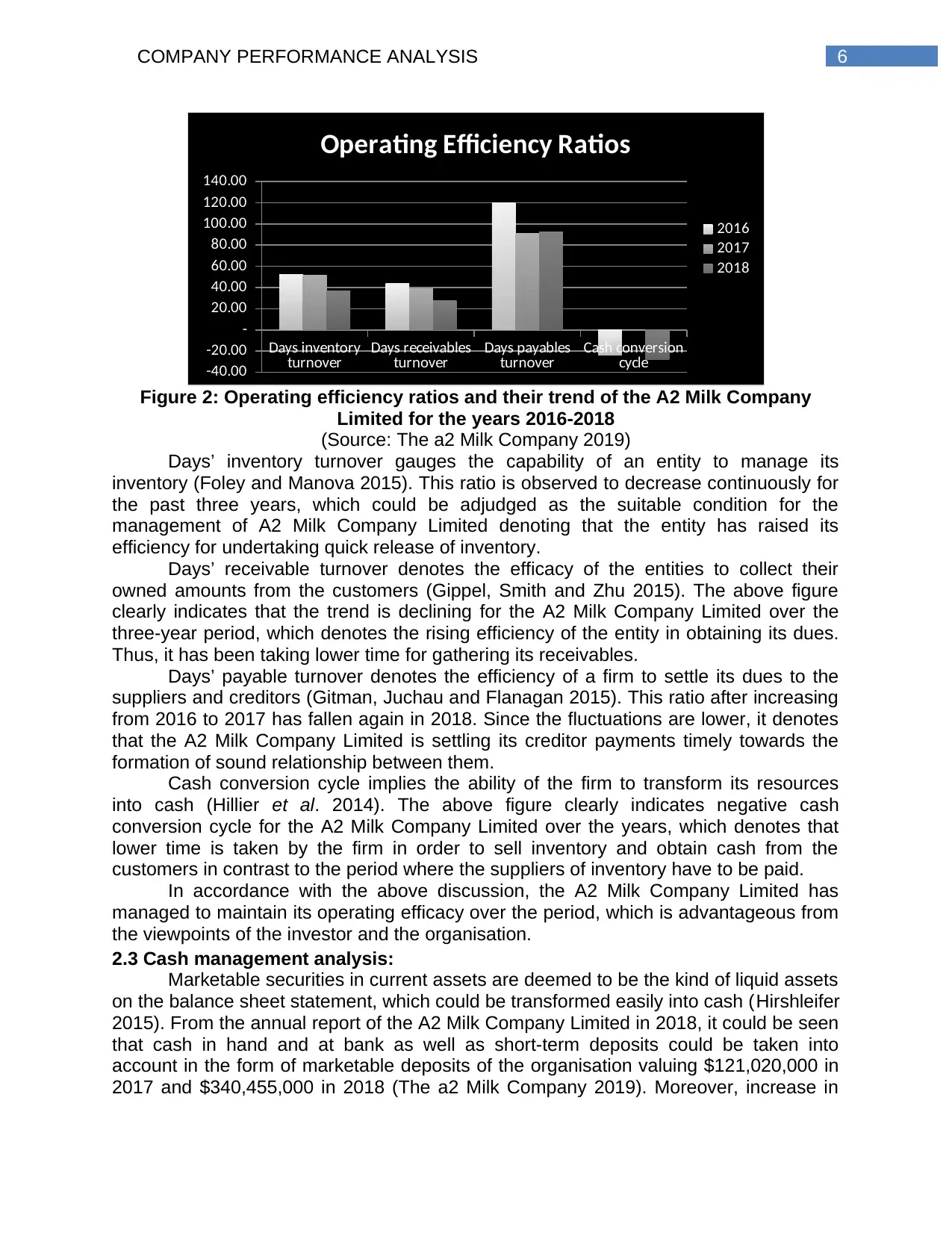

6COMPANY PERFORMANCE ANALYSIS

Days inventory

turnover Days receivables

turnover Days payables

turnover Cash conversion

cycle

-40.00

-20.00

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Operating Efficiency Ratios

2016

2017

2018

Figure 2: Operating efficiency ratios and their trend of the A2 Milk Company

Limited for the years 2016-2018

(Source: The a2 Milk Company 2019)

Days’ inventory turnover gauges the capability of an entity to manage its

inventory (Foley and Manova 2015). This ratio is observed to decrease continuously for

the past three years, which could be adjudged as the suitable condition for the

management of A2 Milk Company Limited denoting that the entity has raised its

efficiency for undertaking quick release of inventory.

Days’ receivable turnover denotes the efficacy of the entities to collect their

owned amounts from the customers (Gippel, Smith and Zhu 2015). The above figure

clearly indicates that the trend is declining for the A2 Milk Company Limited over the

three-year period, which denotes the rising efficiency of the entity in obtaining its dues.

Thus, it has been taking lower time for gathering its receivables.

Days’ payable turnover denotes the efficiency of a firm to settle its dues to the

suppliers and creditors (Gitman, Juchau and Flanagan 2015). This ratio after increasing

from 2016 to 2017 has fallen again in 2018. Since the fluctuations are lower, it denotes

that the A2 Milk Company Limited is settling its creditor payments timely towards the

formation of sound relationship between them.

Cash conversion cycle implies the ability of the firm to transform its resources

into cash (Hillier et al. 2014). The above figure clearly indicates negative cash

conversion cycle for the A2 Milk Company Limited over the years, which denotes that

lower time is taken by the firm in order to sell inventory and obtain cash from the

customers in contrast to the period where the suppliers of inventory have to be paid.

In accordance with the above discussion, the A2 Milk Company Limited has

managed to maintain its operating efficacy over the period, which is advantageous from

the viewpoints of the investor and the organisation.

2.3 Cash management analysis:

Marketable securities in current assets are deemed to be the kind of liquid assets

on the balance sheet statement, which could be transformed easily into cash (Hirshleifer

2015). From the annual report of the A2 Milk Company Limited in 2018, it could be seen

that cash in hand and at bank as well as short-term deposits could be taken into

account in the form of marketable deposits of the organisation valuing $121,020,000 in

2017 and $340,455,000 in 2018 (The a2 Milk Company 2019). Moreover, increase in

Days inventory

turnover Days receivables

turnover Days payables

turnover Cash conversion

cycle

-40.00

-20.00

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Operating Efficiency Ratios

2016

2017

2018

Figure 2: Operating efficiency ratios and their trend of the A2 Milk Company

Limited for the years 2016-2018

(Source: The a2 Milk Company 2019)

Days’ inventory turnover gauges the capability of an entity to manage its

inventory (Foley and Manova 2015). This ratio is observed to decrease continuously for

the past three years, which could be adjudged as the suitable condition for the

management of A2 Milk Company Limited denoting that the entity has raised its

efficiency for undertaking quick release of inventory.

Days’ receivable turnover denotes the efficacy of the entities to collect their

owned amounts from the customers (Gippel, Smith and Zhu 2015). The above figure

clearly indicates that the trend is declining for the A2 Milk Company Limited over the

three-year period, which denotes the rising efficiency of the entity in obtaining its dues.

Thus, it has been taking lower time for gathering its receivables.

Days’ payable turnover denotes the efficiency of a firm to settle its dues to the

suppliers and creditors (Gitman, Juchau and Flanagan 2015). This ratio after increasing

from 2016 to 2017 has fallen again in 2018. Since the fluctuations are lower, it denotes

that the A2 Milk Company Limited is settling its creditor payments timely towards the

formation of sound relationship between them.

Cash conversion cycle implies the ability of the firm to transform its resources

into cash (Hillier et al. 2014). The above figure clearly indicates negative cash

conversion cycle for the A2 Milk Company Limited over the years, which denotes that

lower time is taken by the firm in order to sell inventory and obtain cash from the

customers in contrast to the period where the suppliers of inventory have to be paid.

In accordance with the above discussion, the A2 Milk Company Limited has

managed to maintain its operating efficacy over the period, which is advantageous from

the viewpoints of the investor and the organisation.

2.3 Cash management analysis:

Marketable securities in current assets are deemed to be the kind of liquid assets

on the balance sheet statement, which could be transformed easily into cash (Hirshleifer

2015). From the annual report of the A2 Milk Company Limited in 2018, it could be seen

that cash in hand and at bank as well as short-term deposits could be taken into

account in the form of marketable deposits of the organisation valuing $121,020,000 in

2017 and $340,455,000 in 2018 (The a2 Milk Company 2019). Moreover, increase in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COMPANY PERFORMANCE ANALYSIS

cash as well as other short-term deposits of the A2 Milk Company Limited could be

witnessed in 2018 compared to the previous year.

In this case, it is necessary to mention that these instruments are used by the

organisations for generating return on cash and the similar aspect could be witnessed in

case of the A2 Milk Company Limited as well. In accordance with “Note D3 of the

Annual Report”, the organisation earns floating rate interest based on the daily rates of

bank deposits. This denotes that such securities function as source of cash for the

organisation, which is required for effective cash management (Kim and Zhang 2016).

The organisations could not ignore the significance of sound mechanisms of cash

management. The rise in these marketable securities in the balance sheet statement

represents the strategy of the A2 Milk Company Limited for improving cash collection,

as it would boost the liquidity position, which is a critical cash management aspect.

Moreover, by maintaining adequate cash balance, the A2 Milk Company Limited has the

opportunity of combating with the economic fluctuations as well as financial stability for

undertaking investments, when there is effective price. The big corporate investors

could consider the A2 Milk Company Limited as a target when there is adequate cash

balance that could be utilised productively (Lee, Sameen and Cowling 2015).

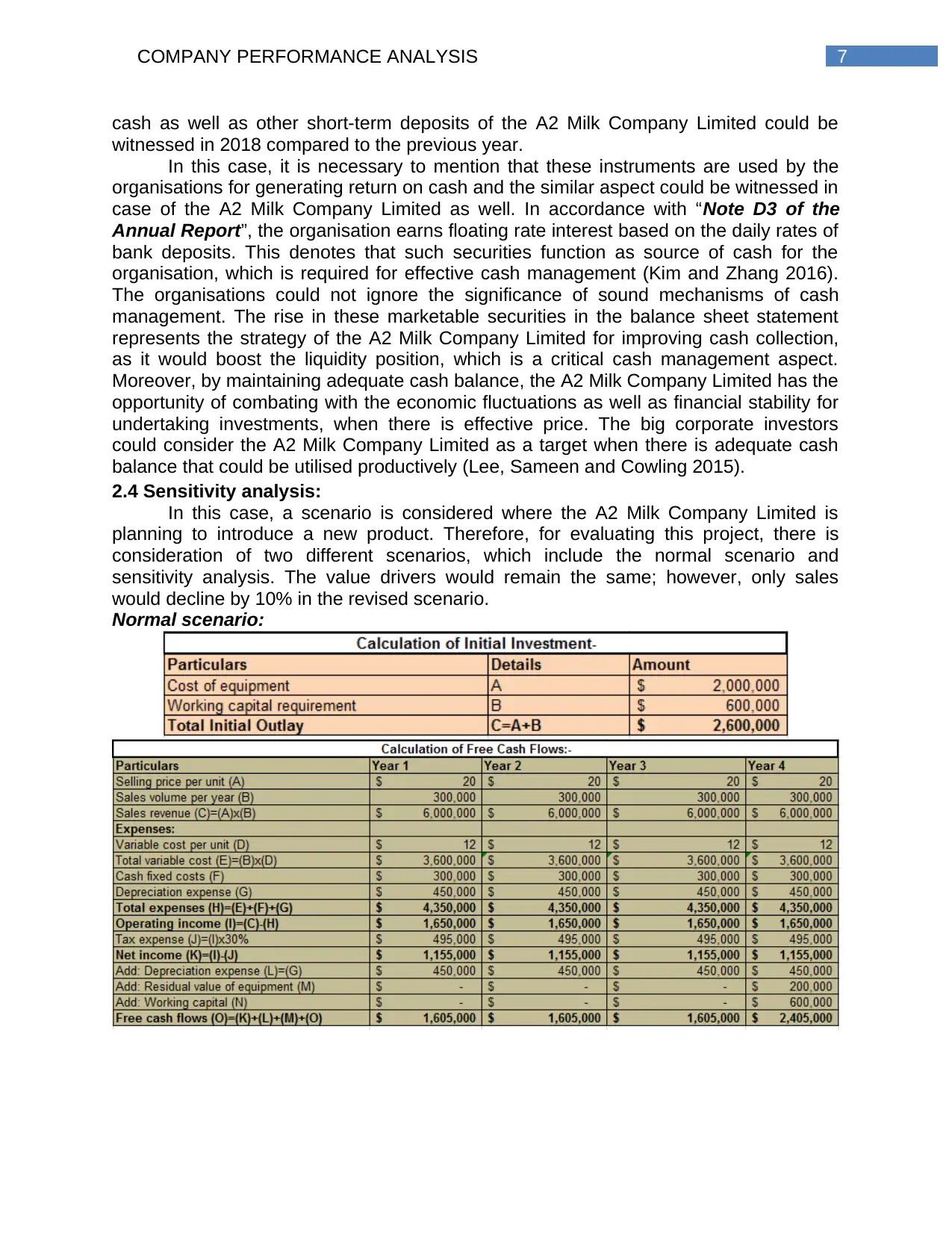

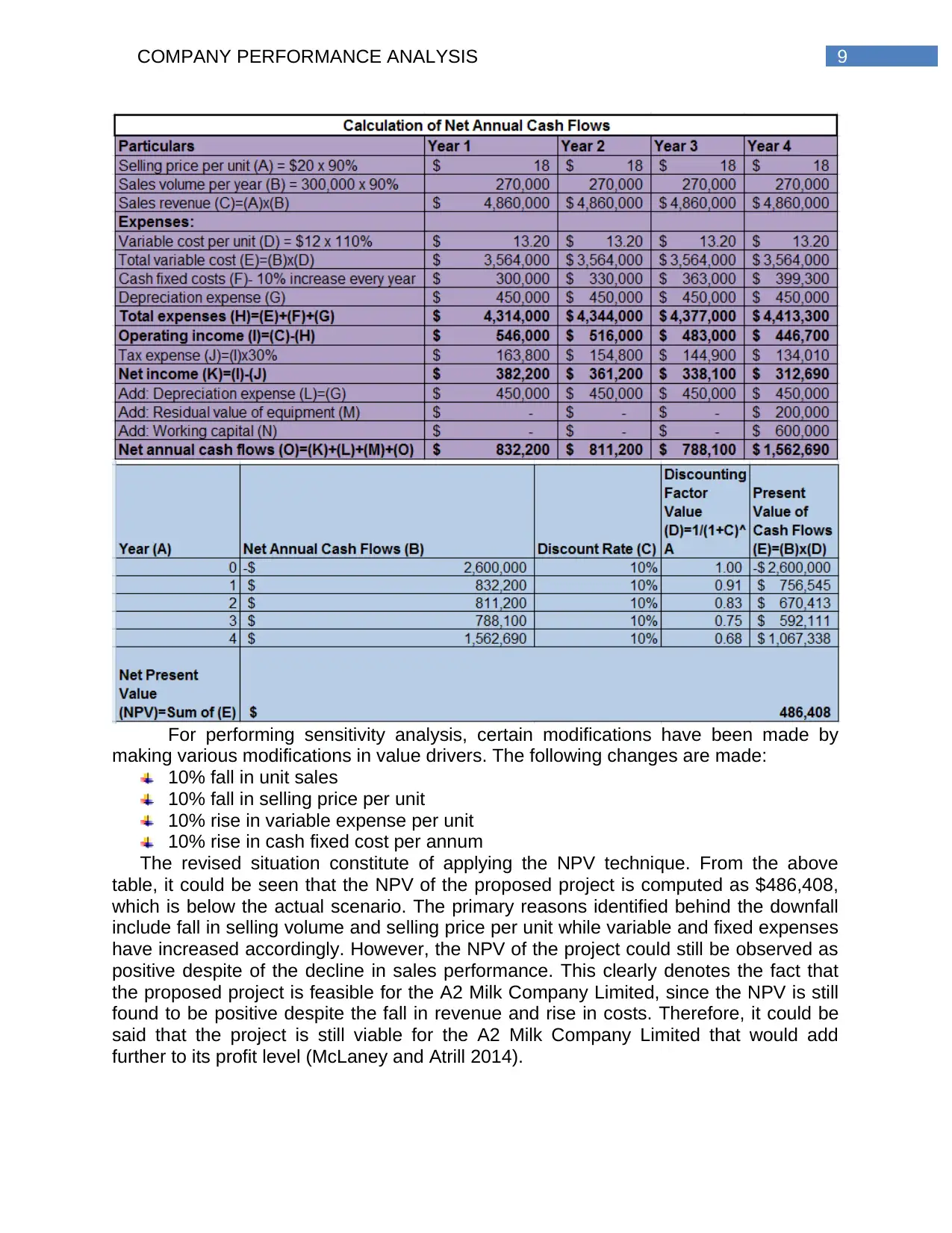

2.4 Sensitivity analysis:

In this case, a scenario is considered where the A2 Milk Company Limited is

planning to introduce a new product. Therefore, for evaluating this project, there is

consideration of two different scenarios, which include the normal scenario and

sensitivity analysis. The value drivers would remain the same; however, only sales

would decline by 10% in the revised scenario.

Normal scenario:

cash as well as other short-term deposits of the A2 Milk Company Limited could be

witnessed in 2018 compared to the previous year.

In this case, it is necessary to mention that these instruments are used by the

organisations for generating return on cash and the similar aspect could be witnessed in

case of the A2 Milk Company Limited as well. In accordance with “Note D3 of the

Annual Report”, the organisation earns floating rate interest based on the daily rates of

bank deposits. This denotes that such securities function as source of cash for the

organisation, which is required for effective cash management (Kim and Zhang 2016).

The organisations could not ignore the significance of sound mechanisms of cash

management. The rise in these marketable securities in the balance sheet statement

represents the strategy of the A2 Milk Company Limited for improving cash collection,

as it would boost the liquidity position, which is a critical cash management aspect.

Moreover, by maintaining adequate cash balance, the A2 Milk Company Limited has the

opportunity of combating with the economic fluctuations as well as financial stability for

undertaking investments, when there is effective price. The big corporate investors

could consider the A2 Milk Company Limited as a target when there is adequate cash

balance that could be utilised productively (Lee, Sameen and Cowling 2015).

2.4 Sensitivity analysis:

In this case, a scenario is considered where the A2 Milk Company Limited is

planning to introduce a new product. Therefore, for evaluating this project, there is

consideration of two different scenarios, which include the normal scenario and

sensitivity analysis. The value drivers would remain the same; however, only sales

would decline by 10% in the revised scenario.

Normal scenario:

8COMPANY PERFORMANCE ANALYSIS

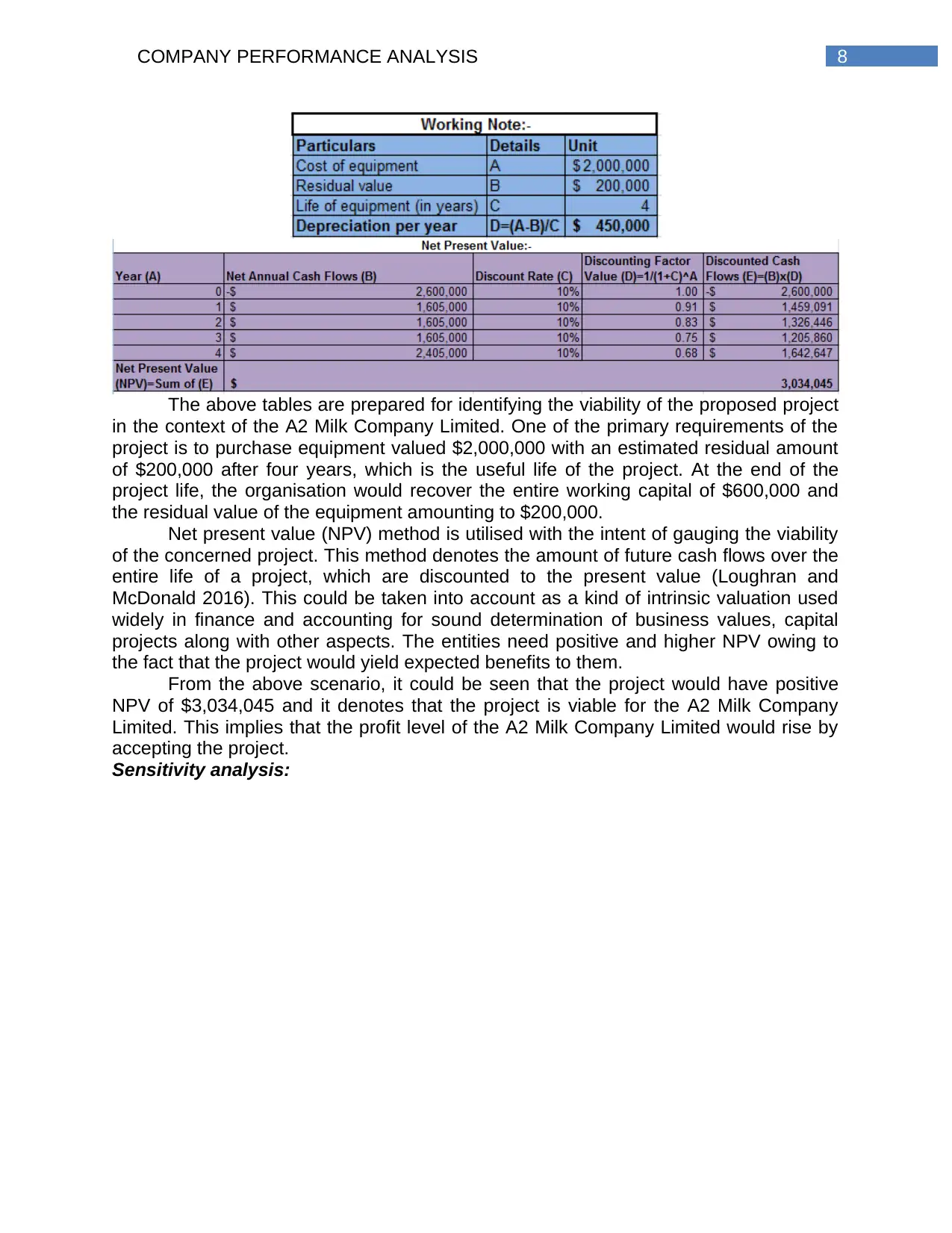

The above tables are prepared for identifying the viability of the proposed project

in the context of the A2 Milk Company Limited. One of the primary requirements of the

project is to purchase equipment valued $2,000,000 with an estimated residual amount

of $200,000 after four years, which is the useful life of the project. At the end of the

project life, the organisation would recover the entire working capital of $600,000 and

the residual value of the equipment amounting to $200,000.

Net present value (NPV) method is utilised with the intent of gauging the viability

of the concerned project. This method denotes the amount of future cash flows over the

entire life of a project, which are discounted to the present value (Loughran and

McDonald 2016). This could be taken into account as a kind of intrinsic valuation used

widely in finance and accounting for sound determination of business values, capital

projects along with other aspects. The entities need positive and higher NPV owing to

the fact that the project would yield expected benefits to them.

From the above scenario, it could be seen that the project would have positive

NPV of $3,034,045 and it denotes that the project is viable for the A2 Milk Company

Limited. This implies that the profit level of the A2 Milk Company Limited would rise by

accepting the project.

Sensitivity analysis:

The above tables are prepared for identifying the viability of the proposed project

in the context of the A2 Milk Company Limited. One of the primary requirements of the

project is to purchase equipment valued $2,000,000 with an estimated residual amount

of $200,000 after four years, which is the useful life of the project. At the end of the

project life, the organisation would recover the entire working capital of $600,000 and

the residual value of the equipment amounting to $200,000.

Net present value (NPV) method is utilised with the intent of gauging the viability

of the concerned project. This method denotes the amount of future cash flows over the

entire life of a project, which are discounted to the present value (Loughran and

McDonald 2016). This could be taken into account as a kind of intrinsic valuation used

widely in finance and accounting for sound determination of business values, capital

projects along with other aspects. The entities need positive and higher NPV owing to

the fact that the project would yield expected benefits to them.

From the above scenario, it could be seen that the project would have positive

NPV of $3,034,045 and it denotes that the project is viable for the A2 Milk Company

Limited. This implies that the profit level of the A2 Milk Company Limited would rise by

accepting the project.

Sensitivity analysis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9COMPANY PERFORMANCE ANALYSIS

For performing sensitivity analysis, certain modifications have been made by

making various modifications in value drivers. The following changes are made:

10% fall in unit sales

10% fall in selling price per unit

10% rise in variable expense per unit

10% rise in cash fixed cost per annum

The revised situation constitute of applying the NPV technique. From the above

table, it could be seen that the NPV of the proposed project is computed as $486,408,

which is below the actual scenario. The primary reasons identified behind the downfall

include fall in selling volume and selling price per unit while variable and fixed expenses

have increased accordingly. However, the NPV of the project could still be observed as

positive despite of the decline in sales performance. This clearly denotes the fact that

the proposed project is feasible for the A2 Milk Company Limited, since the NPV is still

found to be positive despite the fall in revenue and rise in costs. Therefore, it could be

said that the project is still viable for the A2 Milk Company Limited that would add

further to its profit level (McLaney and Atrill 2014).

For performing sensitivity analysis, certain modifications have been made by

making various modifications in value drivers. The following changes are made:

10% fall in unit sales

10% fall in selling price per unit

10% rise in variable expense per unit

10% rise in cash fixed cost per annum

The revised situation constitute of applying the NPV technique. From the above

table, it could be seen that the NPV of the proposed project is computed as $486,408,

which is below the actual scenario. The primary reasons identified behind the downfall

include fall in selling volume and selling price per unit while variable and fixed expenses

have increased accordingly. However, the NPV of the project could still be observed as

positive despite of the decline in sales performance. This clearly denotes the fact that

the proposed project is feasible for the A2 Milk Company Limited, since the NPV is still

found to be positive despite the fall in revenue and rise in costs. Therefore, it could be

said that the project is still viable for the A2 Milk Company Limited that would add

further to its profit level (McLaney and Atrill 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COMPANY PERFORMANCE ANALYSIS

2.5 Systemic and un-systemic risks:

The systemic risk occurs owing to the alterations in macroeconomic factors such

as interest rate changes, inflation and others (Quattrone 2016). The A2 Milk Company

Limited is exposed to the following types of systemic risks:

Equity price risk:

The organisation is exposed to this specific risk on listed investments, which are

categorised as well as gauged at fair value via other comprehensive income. However,

this risk is not hedged by the management of the organisation. However, it monitors this

specific risk exposure by comparing the quoted share price movement of long-term

investments (Rogers and Makonnen 2014).

Foreign currency risk:

The business operations of the entity are prone towards foreign currency risk

arising out of the fluctuations in the currencies of the nations such as UK, China and US

compared to the AUD and NZD currencies. There is no hedging strategy adopted by the

organisation; however, it might shift its cash balances within time between currencies

for exposure minimisation.

Un-systemic risk could be observed only with the particular sector and these

risks of the A2 Milk Company Limited are represented as follows:

Supply chain:

The organisation might lose its ability of maintaining its product supply, if there is

any adverse or material modification in the operations of suppliers or fall in support from

its suppliers.

Product quality:

The organisation is prone to this risk, since its products might be polluted or they

might be tampered or adulterated or it might face unsafe competition. These aspects

could result in injury or harm to the rivals.

Rise in competition:

Since the industry where the A2 Milk Company Limited operates is highly

competitive, rise in competition could tamper the business operations, particularly in

sales as well as revenue bases. These are identified as significant un-systemic risk

associated with the operations of the A2 Milk Company Limited (Xiang and Worthington

2015).

2.6 Dividend payout ratio and dividend policy:

Table 3: Dividend payout ratio of the A2 Milk Company Limited for the years 2016-

2018

(Source: The A2 Milk Company 2019)

This ratio is a crucial tool for the organisations as well as the investors for

gauging the proportion of net profit, which is distributed to the shareholders by the

organisation as dividend payments over the period. More precisely, this ratio assists in

reporting the proportion of profit that an organisation decides to keep in order to finance

its operations and the proportion of profit distributed to the shareholders (Scholes 2015).

2.5 Systemic and un-systemic risks:

The systemic risk occurs owing to the alterations in macroeconomic factors such

as interest rate changes, inflation and others (Quattrone 2016). The A2 Milk Company

Limited is exposed to the following types of systemic risks:

Equity price risk:

The organisation is exposed to this specific risk on listed investments, which are

categorised as well as gauged at fair value via other comprehensive income. However,

this risk is not hedged by the management of the organisation. However, it monitors this

specific risk exposure by comparing the quoted share price movement of long-term

investments (Rogers and Makonnen 2014).

Foreign currency risk:

The business operations of the entity are prone towards foreign currency risk

arising out of the fluctuations in the currencies of the nations such as UK, China and US

compared to the AUD and NZD currencies. There is no hedging strategy adopted by the

organisation; however, it might shift its cash balances within time between currencies

for exposure minimisation.

Un-systemic risk could be observed only with the particular sector and these

risks of the A2 Milk Company Limited are represented as follows:

Supply chain:

The organisation might lose its ability of maintaining its product supply, if there is

any adverse or material modification in the operations of suppliers or fall in support from

its suppliers.

Product quality:

The organisation is prone to this risk, since its products might be polluted or they

might be tampered or adulterated or it might face unsafe competition. These aspects

could result in injury or harm to the rivals.

Rise in competition:

Since the industry where the A2 Milk Company Limited operates is highly

competitive, rise in competition could tamper the business operations, particularly in

sales as well as revenue bases. These are identified as significant un-systemic risk

associated with the operations of the A2 Milk Company Limited (Xiang and Worthington

2015).

2.6 Dividend payout ratio and dividend policy:

Table 3: Dividend payout ratio of the A2 Milk Company Limited for the years 2016-

2018

(Source: The A2 Milk Company 2019)

This ratio is a crucial tool for the organisations as well as the investors for

gauging the proportion of net profit, which is distributed to the shareholders by the

organisation as dividend payments over the period. More precisely, this ratio assists in

reporting the proportion of profit that an organisation decides to keep in order to finance

its operations and the proportion of profit distributed to the shareholders (Scholes 2015).

11COMPANY PERFORMANCE ANALYSIS

It is necessary to be stated that the investors have significant interest in the ratio, since

they intend to have an idea of whether the organisations are distributing adequate

proportion of net income to the investors (Swift and Piff 2014).

The situation is not the same for the A2 Milk Company Limited. From the above

table, it is evident that the dividend payout ratio of the organisation is zero over all the

three-year period. The dividend per share of the firm has been nil over the three-year

period. All these aspects signify that no dividend has been paid by the A2 Milk

Company Limited over the years. This clearly denotes that the organisation follows zero

dividend policy, as it has focused on increasing its retained earnings. As a result, there

might be decline in the confidence of the investors and shareholders associated with the

organisation (Vernimmen et al. 2014).

III. Recommendation letter:

To,

The Investor,

Date: 22nd May 2019

Subject: Letter of Recommendation

There are various critical aspects that have to be taken into account while

undertaking investment decision on the A2 Milk Company Limited. By ensuring that the

aim of this recommendation is to ensure maximum return on investment, it has been

identified that the A2 Milk Company Limited has shown effective movements in terms of

profitability as well as operating efficiency. The organisation has both systemic and un-

systemic risks like other organisations; however, it is possible for the firm to control

these risks. Moreover, owing to the presence of marketable securities, it is deemed to

be a suitable option for investment. However, it has been analysed that the organisation

follows zero dividend policy and hence, it does not provide any return to its

shareholders over the year. Since majority of the financial aspects are found to be

positive, it is recommended to the investor to invest in the shares of the A2 Milk

Company Limited for earning better returns in future.

IV. Conclusion:

Based on the above discussion, it has been evaluated that the A2 Milk Company

Limited is operating in the Australian milk and dairy industry. It has been found that the

organisation has maintained both stable profitability and operating efficiency positions.

Moreover, the proposed project is observed to provide significant benefits to the

organisation in future. However, it has been analysed that the organisation follows zero

dividend policy and hence, it does not provide any return to its shareholders over the

year. Since majority of the financial aspects are found to be positive, it is recommended

to the investor to invest in the shares of the A2 Milk Company Limited for earning better

returns in future.

It is necessary to be stated that the investors have significant interest in the ratio, since

they intend to have an idea of whether the organisations are distributing adequate

proportion of net income to the investors (Swift and Piff 2014).

The situation is not the same for the A2 Milk Company Limited. From the above

table, it is evident that the dividend payout ratio of the organisation is zero over all the

three-year period. The dividend per share of the firm has been nil over the three-year

period. All these aspects signify that no dividend has been paid by the A2 Milk

Company Limited over the years. This clearly denotes that the organisation follows zero

dividend policy, as it has focused on increasing its retained earnings. As a result, there

might be decline in the confidence of the investors and shareholders associated with the

organisation (Vernimmen et al. 2014).

III. Recommendation letter:

To,

The Investor,

Date: 22nd May 2019

Subject: Letter of Recommendation

There are various critical aspects that have to be taken into account while

undertaking investment decision on the A2 Milk Company Limited. By ensuring that the

aim of this recommendation is to ensure maximum return on investment, it has been

identified that the A2 Milk Company Limited has shown effective movements in terms of

profitability as well as operating efficiency. The organisation has both systemic and un-

systemic risks like other organisations; however, it is possible for the firm to control

these risks. Moreover, owing to the presence of marketable securities, it is deemed to

be a suitable option for investment. However, it has been analysed that the organisation

follows zero dividend policy and hence, it does not provide any return to its

shareholders over the year. Since majority of the financial aspects are found to be

positive, it is recommended to the investor to invest in the shares of the A2 Milk

Company Limited for earning better returns in future.

IV. Conclusion:

Based on the above discussion, it has been evaluated that the A2 Milk Company

Limited is operating in the Australian milk and dairy industry. It has been found that the

organisation has maintained both stable profitability and operating efficiency positions.

Moreover, the proposed project is observed to provide significant benefits to the

organisation in future. However, it has been analysed that the organisation follows zero

dividend policy and hence, it does not provide any return to its shareholders over the

year. Since majority of the financial aspects are found to be positive, it is recommended

to the investor to invest in the shares of the A2 Milk Company Limited for earning better

returns in future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.