Comprehensive Report on Financial Accounting Principles and Practices

VerifiedAdded on 2020/10/22

|34

|4624

|336

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles, regulations, and practical applications. It begins with an introduction to financial accounting, its importance, and the relevant regulations, including IFRS, IASB, FRC, and GAAP. The report then details key accounting principles such as accrual, matching, cost, economic entity, going concern, full disclosure, and monetary unit principles. The report includes case studies of six clients, detailing journal entries, ledger accounts, trial balances, profit and loss statements, and balance sheets. It explores control accounts, suspense accounts, and the importance of depreciation. The report also includes financial statements for clients like Peter Piper and Raintree Limited. Overall, the report provides a thorough analysis of financial accounting practices and their application in various business scenarios, including the preparation of financial statements, and the importance of the discussed accounting principles.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A. Report of accounting regulations to line manager of organisation........................................1

1. Describing financial accounting..............................................................................................1

2. Financial accounting regulations.............................................................................................2

3. Principles of accounting with its rules....................................................................................3

4. Concepts related to material disclosure and consistency........................................................3

CLIENT 1........................................................................................................................................4

1. Journal entry of client 1 as per date 1st may 2017...................................................................4

2. Drafting ledger account of above journal entries....................................................................7

3. Client 1's trial balance...........................................................................................................15

CLIENT 2......................................................................................................................................16

A. Profit and loss statement of Peter Piper for year ended 31st December 2017......................16

B. Balance sheet of Peter Piper for the year ended 31st December 2017..................................17

CLIENT 3......................................................................................................................................18

A. Income statement of Raintree limited for the year ended 30th Septmeber, 2017.................18

B. Financial position of client 3 (Raintree limited)...................................................................19

C. Justifying various principles and concepts of accounting principles...................................24

C. Importance of deprecation by both methods with context of organization..........................25

CLIENT 4......................................................................................................................................25

A. Objective of preparing bank statement.................................................................................25

B. Justification related to recording of bank statements...........................................................26

C. Cash book of client...............................................................................................................26

CLIENT 5......................................................................................................................................27

Drafting purchase ledger control account and sales ledger control account of Henderson for

May 2017..................................................................................................................................27

A. Describing control account...................................................................................................28

CLIENT 6......................................................................................................................................28

A. Define suspense account with features.................................................................................28

B. Drafting trial balance............................................................................................................28

C. Journal entries.......................................................................................................................29

D. Clearing account vs Suspense account.................................................................................29

CONCLUSION..............................................................................................................................29

REFERENCES..............................................................................................................................31

INTRODUCTION...........................................................................................................................1

A. Report of accounting regulations to line manager of organisation........................................1

1. Describing financial accounting..............................................................................................1

2. Financial accounting regulations.............................................................................................2

3. Principles of accounting with its rules....................................................................................3

4. Concepts related to material disclosure and consistency........................................................3

CLIENT 1........................................................................................................................................4

1. Journal entry of client 1 as per date 1st may 2017...................................................................4

2. Drafting ledger account of above journal entries....................................................................7

3. Client 1's trial balance...........................................................................................................15

CLIENT 2......................................................................................................................................16

A. Profit and loss statement of Peter Piper for year ended 31st December 2017......................16

B. Balance sheet of Peter Piper for the year ended 31st December 2017..................................17

CLIENT 3......................................................................................................................................18

A. Income statement of Raintree limited for the year ended 30th Septmeber, 2017.................18

B. Financial position of client 3 (Raintree limited)...................................................................19

C. Justifying various principles and concepts of accounting principles...................................24

C. Importance of deprecation by both methods with context of organization..........................25

CLIENT 4......................................................................................................................................25

A. Objective of preparing bank statement.................................................................................25

B. Justification related to recording of bank statements...........................................................26

C. Cash book of client...............................................................................................................26

CLIENT 5......................................................................................................................................27

Drafting purchase ledger control account and sales ledger control account of Henderson for

May 2017..................................................................................................................................27

A. Describing control account...................................................................................................28

CLIENT 6......................................................................................................................................28

A. Define suspense account with features.................................................................................28

B. Drafting trial balance............................................................................................................28

C. Journal entries.......................................................................................................................29

D. Clearing account vs Suspense account.................................................................................29

CONCLUSION..............................................................................................................................29

REFERENCES..............................................................................................................................31

INTRODUCTION

In present era, financial accounting is determined as the most important element of

organization. The present report is giving brief discussion on various principles of accounting,

rules and regulations which are followed by all the industries. While following these concepts

along with regulation are giving great advantage for drafting financial performance of their own.

These concepts, rules and regulation will lead to achieve great success of the organization in

terms on monetary aspect and even brand image. The report is discussing about six clients in

which all the financial statements such as trial balance, balance sheet, profit and loss statement

are covered with proper journal entry and ledger account. This report has also highlighted on

control account that is sales ledger control account and purchase ledger control account.

A. Report of accounting regulations to line manager of organisation

To : Line Manager

From : Junior accountant

Subject: Expressing the term accounting and its awareness with respect to accounting

regulations

Respected Sir,

There is essential need of analysing all the rules and regulations as well as different

methods for applying various principles of accounting for improving the transactions which are

based on activities which are directly linked to business. Different accounting techniques help

in improving different business operations and all transactional activities. The outcomes of such

techniques will be beneficial for allocating cost, predicting and budgeting with different

operational tasks in context of business and organisation.

1. Describing financial accounting

Financial accounting refers to the area whose special emphasis is on giving useful

information to all external users. It is replicated as a way for reporting each and every business

activity and all important information related to finance has been provided to creditors,

investors and various people who are considered as outsiders but are relevant for organization.

Outsiders include creditors and investors as they use financial information of organization for

making appropriate decisions (Shroff, 2017). The set of financial statements which are been

issued to external users by organisation. Financial statements are of different types and which

1

In present era, financial accounting is determined as the most important element of

organization. The present report is giving brief discussion on various principles of accounting,

rules and regulations which are followed by all the industries. While following these concepts

along with regulation are giving great advantage for drafting financial performance of their own.

These concepts, rules and regulation will lead to achieve great success of the organization in

terms on monetary aspect and even brand image. The report is discussing about six clients in

which all the financial statements such as trial balance, balance sheet, profit and loss statement

are covered with proper journal entry and ledger account. This report has also highlighted on

control account that is sales ledger control account and purchase ledger control account.

A. Report of accounting regulations to line manager of organisation

To : Line Manager

From : Junior accountant

Subject: Expressing the term accounting and its awareness with respect to accounting

regulations

Respected Sir,

There is essential need of analysing all the rules and regulations as well as different

methods for applying various principles of accounting for improving the transactions which are

based on activities which are directly linked to business. Different accounting techniques help

in improving different business operations and all transactional activities. The outcomes of such

techniques will be beneficial for allocating cost, predicting and budgeting with different

operational tasks in context of business and organisation.

1. Describing financial accounting

Financial accounting refers to the area whose special emphasis is on giving useful

information to all external users. It is replicated as a way for reporting each and every business

activity and all important information related to finance has been provided to creditors,

investors and various people who are considered as outsiders but are relevant for organization.

Outsiders include creditors and investors as they use financial information of organization for

making appropriate decisions (Shroff, 2017). The set of financial statements which are been

issued to external users by organisation. Financial statements are of different types and which

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

provided very general objectives such as Profit and loss statement, Balance sheet, statement of

cash flow and statement of stockholder's equity. All the financial transactions are tracked with

the help of financial accounting. It can be summarized, recorded and presented in the financial

statements which are stated above. The financial statements are issued on daily schedule which

have been set by organization. As all these are used by outsiders, stock holders and even

lenders.

2. Financial accounting regulations

There are various rules and regulations in financial accounting which will be giving

great advantage for providing legal framework for accounting. In UK, there is presence of its

own government regulator which is named as Financial Reporting Council. There are various

disclosure about all units, corporates and different departments of government (Basic

accounting principles. 2018). In the series of regulations, there is the presence of different legal

frameworks which are accepted universally:

IFRS: International Financial reporting standards can be defined as standards which are

issued for giving a specific global language for the affairs of different business and so, in this

context, organizations will be able to understand the accounts and even it will be giving good

contribution towards comparison. IFRS standards provides a basic framework which will

include complete information in the perspective of financial statement and it will lead to attract

a high number of investors.

IASB: International Accounting Standards Board leads to private sector body and it also

has its significance in IFRS Foundation. It performs its various operations in technical matters

in the context of IFRS Foundation. The technical agenda has been pursued for developing full

liberty and even requirements of consultation with different trustees and public. In other words,

its main aim of IASB is to give information to accounting professionals and for framing

database of each financial with disclosure (International Accounting Standards Boards. 2017).

FRC: As discussed above, it is the regulator of UK for the purpose of audit, accounting

and actuarial professions and even for UK's corporate governance. It considers accounting

standards which are framed on the basis of executing all financial disclosure who are closely

related to accounting (Financial Reporting Council. 2017).

GAAP: Generally accepted accounting principles are the rules and procedures which

2

cash flow and statement of stockholder's equity. All the financial transactions are tracked with

the help of financial accounting. It can be summarized, recorded and presented in the financial

statements which are stated above. The financial statements are issued on daily schedule which

have been set by organization. As all these are used by outsiders, stock holders and even

lenders.

2. Financial accounting regulations

There are various rules and regulations in financial accounting which will be giving

great advantage for providing legal framework for accounting. In UK, there is presence of its

own government regulator which is named as Financial Reporting Council. There are various

disclosure about all units, corporates and different departments of government (Basic

accounting principles. 2018). In the series of regulations, there is the presence of different legal

frameworks which are accepted universally:

IFRS: International Financial reporting standards can be defined as standards which are

issued for giving a specific global language for the affairs of different business and so, in this

context, organizations will be able to understand the accounts and even it will be giving good

contribution towards comparison. IFRS standards provides a basic framework which will

include complete information in the perspective of financial statement and it will lead to attract

a high number of investors.

IASB: International Accounting Standards Board leads to private sector body and it also

has its significance in IFRS Foundation. It performs its various operations in technical matters

in the context of IFRS Foundation. The technical agenda has been pursued for developing full

liberty and even requirements of consultation with different trustees and public. In other words,

its main aim of IASB is to give information to accounting professionals and for framing

database of each financial with disclosure (International Accounting Standards Boards. 2017).

FRC: As discussed above, it is the regulator of UK for the purpose of audit, accounting

and actuarial professions and even for UK's corporate governance. It considers accounting

standards which are framed on the basis of executing all financial disclosure who are closely

related to accounting (Financial Reporting Council. 2017).

GAAP: Generally accepted accounting principles are the rules and procedures which

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are defined by industry of professional accounting and they are mostly adopted by all US

companies who are traded publicly (GAAP generally accepted accounting principles. 2018).

3. Principles of accounting with its rules

There is presence of various accounting principles which are developed for basic usage

and on the basis of modern accounting. Some basic principles are as follows :

Accrual principle: All the accounting transactions should be recorded in that specific

accounting period when it has been actually occurred instead of period cash flow which is

associated with it.

Matching principle: While recording revenue, all the expenses related to same time

must be recorded. This refers as a cornerstone of principle of accrual basis of accounting.

Cost principle: In this concept, all assets, liabilities and equity investment should be

recorded at their original purchase price.

Economic entity principle: The transactions should be recorded separately of both

business and its owners. It will be preventing the mix match of assets and liabilities of various

identities.

Going concern principle: Business should stay in operation for future which can be

easily predictable as there is requirement of proper justification of deferring some expenses for

recognition.

Full disclosure principle: On the basis of this principle, all the financial statements

related to business must be included and it should be understandable for each reader. Various

disclosures of financial information should be implied by accounting standards (Financial

Accounting. 2018).

Monetary unit principle: Business should always record those transactions which can

be elaborated with respect to currency.

4. Concepts related to material disclosure and consistency

In the present era, there are different concepts and conventions related to financial

accounting such as materiality, full disclosure, conservatism convention and consistency. For

highlighting these principles, there is need to draft appropriate disclosure on the basis of various

accounts such as :

Materiality principle: The specific transactions must be traced in accounting records

3

companies who are traded publicly (GAAP generally accepted accounting principles. 2018).

3. Principles of accounting with its rules

There is presence of various accounting principles which are developed for basic usage

and on the basis of modern accounting. Some basic principles are as follows :

Accrual principle: All the accounting transactions should be recorded in that specific

accounting period when it has been actually occurred instead of period cash flow which is

associated with it.

Matching principle: While recording revenue, all the expenses related to same time

must be recorded. This refers as a cornerstone of principle of accrual basis of accounting.

Cost principle: In this concept, all assets, liabilities and equity investment should be

recorded at their original purchase price.

Economic entity principle: The transactions should be recorded separately of both

business and its owners. It will be preventing the mix match of assets and liabilities of various

identities.

Going concern principle: Business should stay in operation for future which can be

easily predictable as there is requirement of proper justification of deferring some expenses for

recognition.

Full disclosure principle: On the basis of this principle, all the financial statements

related to business must be included and it should be understandable for each reader. Various

disclosures of financial information should be implied by accounting standards (Financial

Accounting. 2018).

Monetary unit principle: Business should always record those transactions which can

be elaborated with respect to currency.

4. Concepts related to material disclosure and consistency

In the present era, there are different concepts and conventions related to financial

accounting such as materiality, full disclosure, conservatism convention and consistency. For

highlighting these principles, there is need to draft appropriate disclosure on the basis of various

accounts such as :

Materiality principle: The specific transactions must be traced in accounting records

3

which include various material required for accounting record and if there is absence of doing

this activity, then it has been altered in process of decision making for reading the financial

statement of company. This concept is usually known as very vague because it is tough to

quantify (Materiality Principle. 2018).

Consistency: This principle leads to be consistent. In other words, accounting principle

which has been adopted once should remain consistent until better principle or method has not

been generated. If there is mismatch in accounting principle from year to year then it will be

giving long term financial results very difficult for recognize.

CLIENT 1

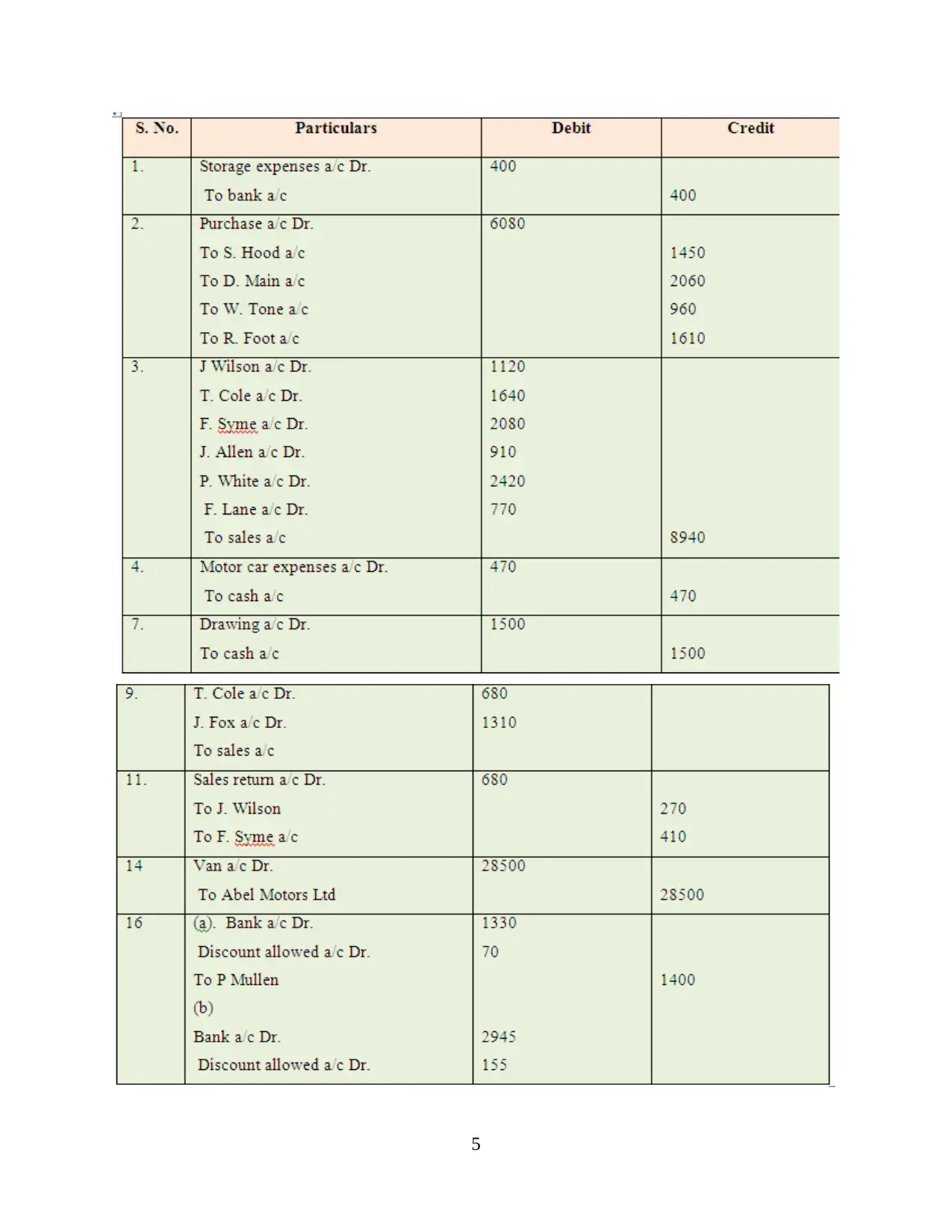

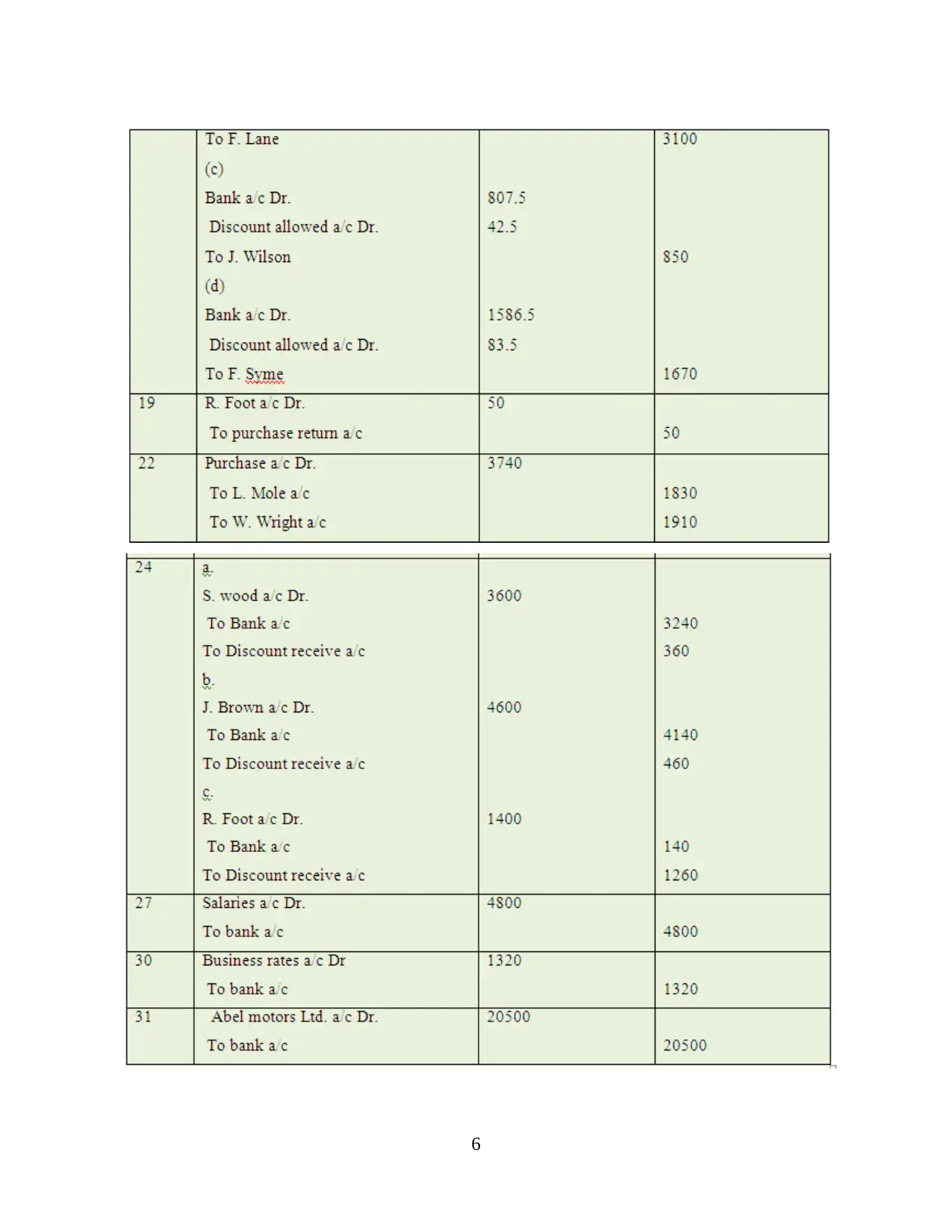

1. Journal entry of client 1 as per date 1st may 2017

The journal entries are disclosed below as they are also required for analysing balance

sheet and profit and loss statement of May 2017 with context of Alexander. The transactions can

be recorded and traced with various techniques of accounting who are framed in specific

duration and transactions which are summarized in the given data set are:

4

this activity, then it has been altered in process of decision making for reading the financial

statement of company. This concept is usually known as very vague because it is tough to

quantify (Materiality Principle. 2018).

Consistency: This principle leads to be consistent. In other words, accounting principle

which has been adopted once should remain consistent until better principle or method has not

been generated. If there is mismatch in accounting principle from year to year then it will be

giving long term financial results very difficult for recognize.

CLIENT 1

1. Journal entry of client 1 as per date 1st may 2017

The journal entries are disclosed below as they are also required for analysing balance

sheet and profit and loss statement of May 2017 with context of Alexander. The transactions can

be recorded and traced with various techniques of accounting who are framed in specific

duration and transactions which are summarized in the given data set are:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

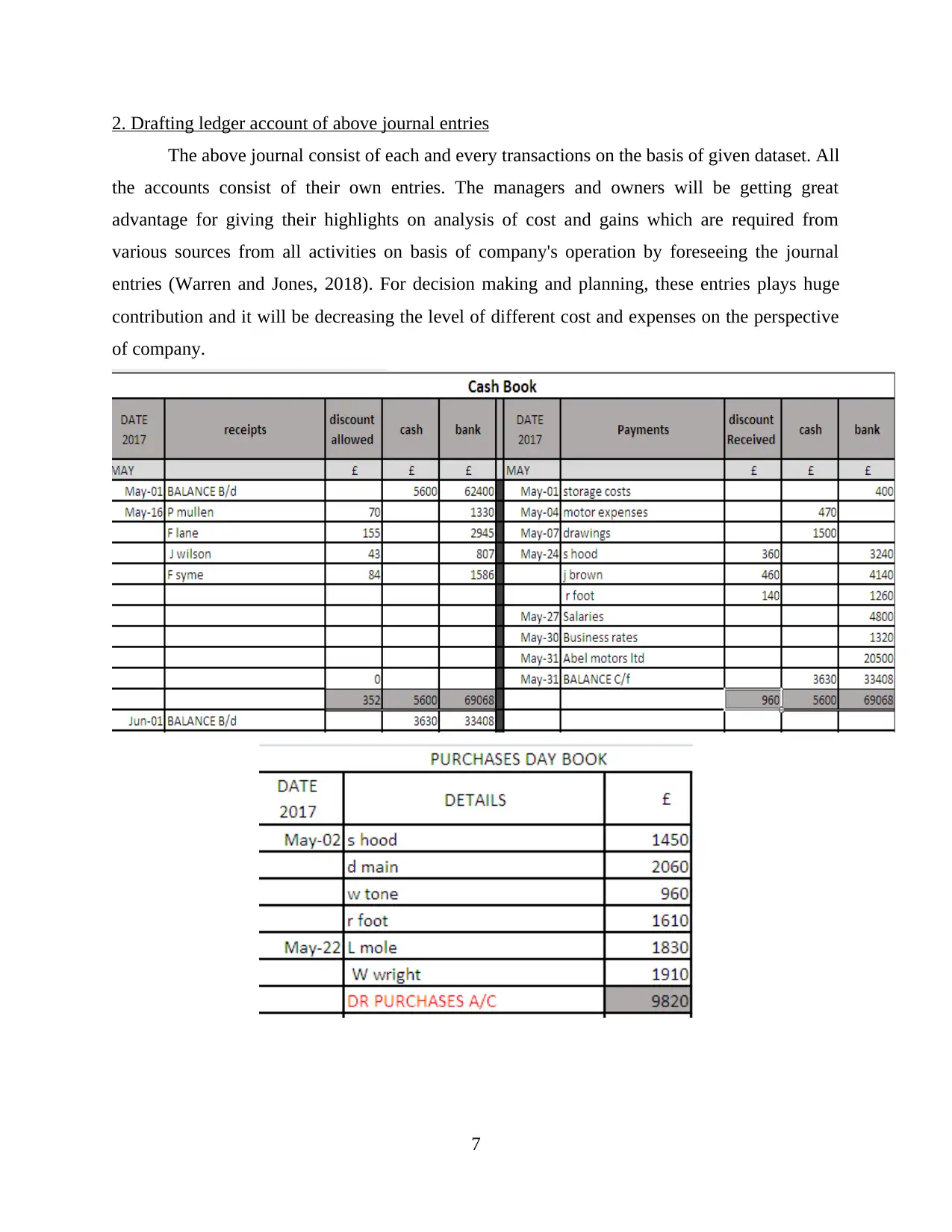

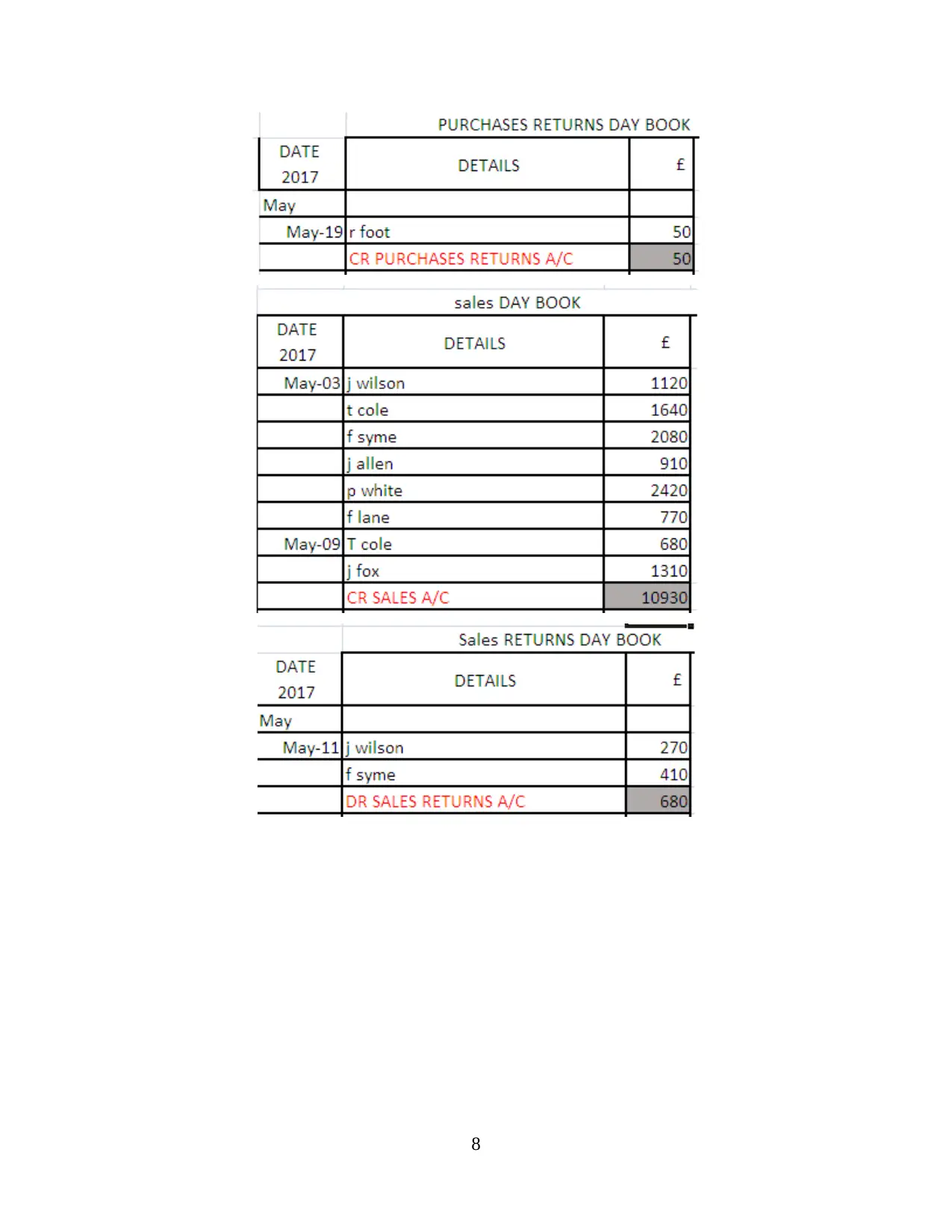

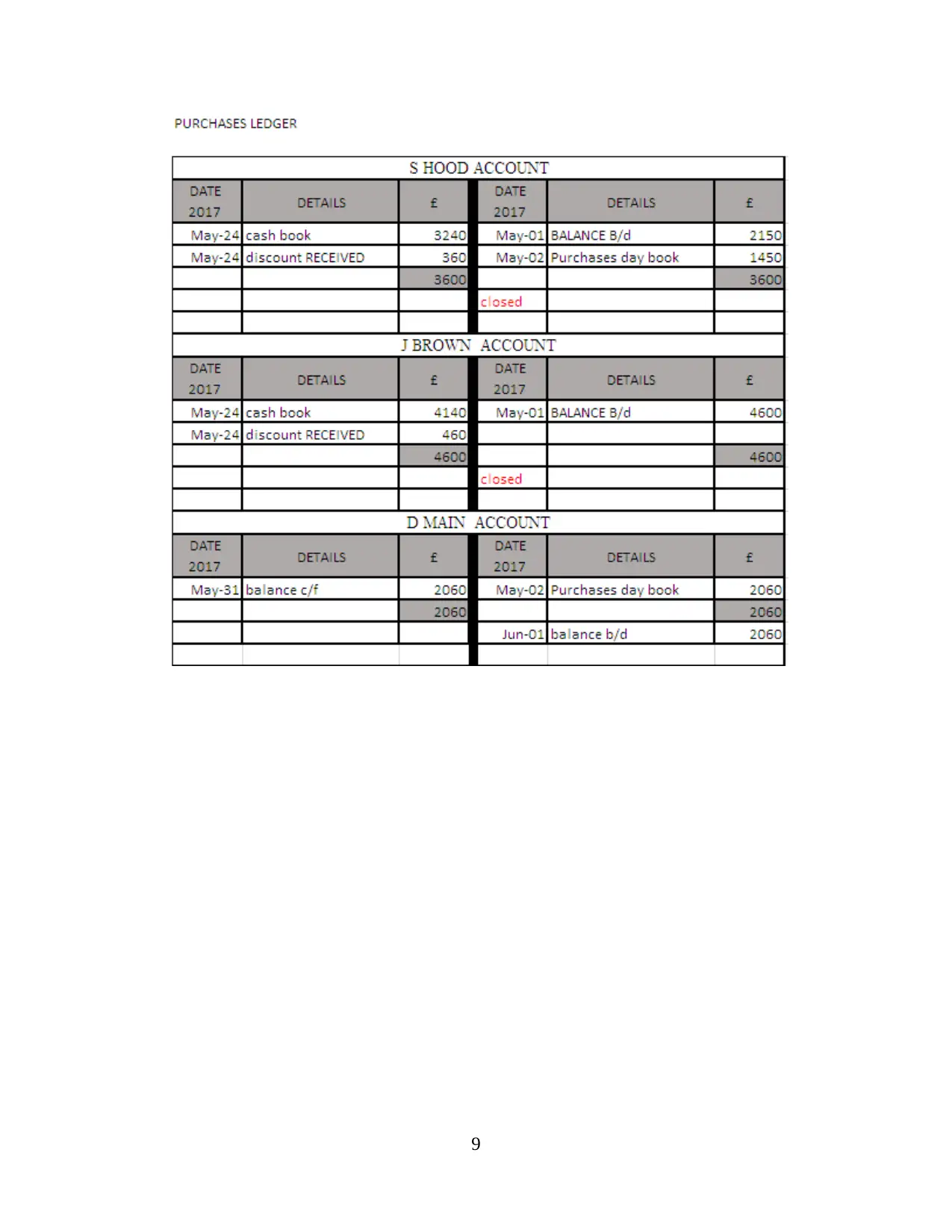

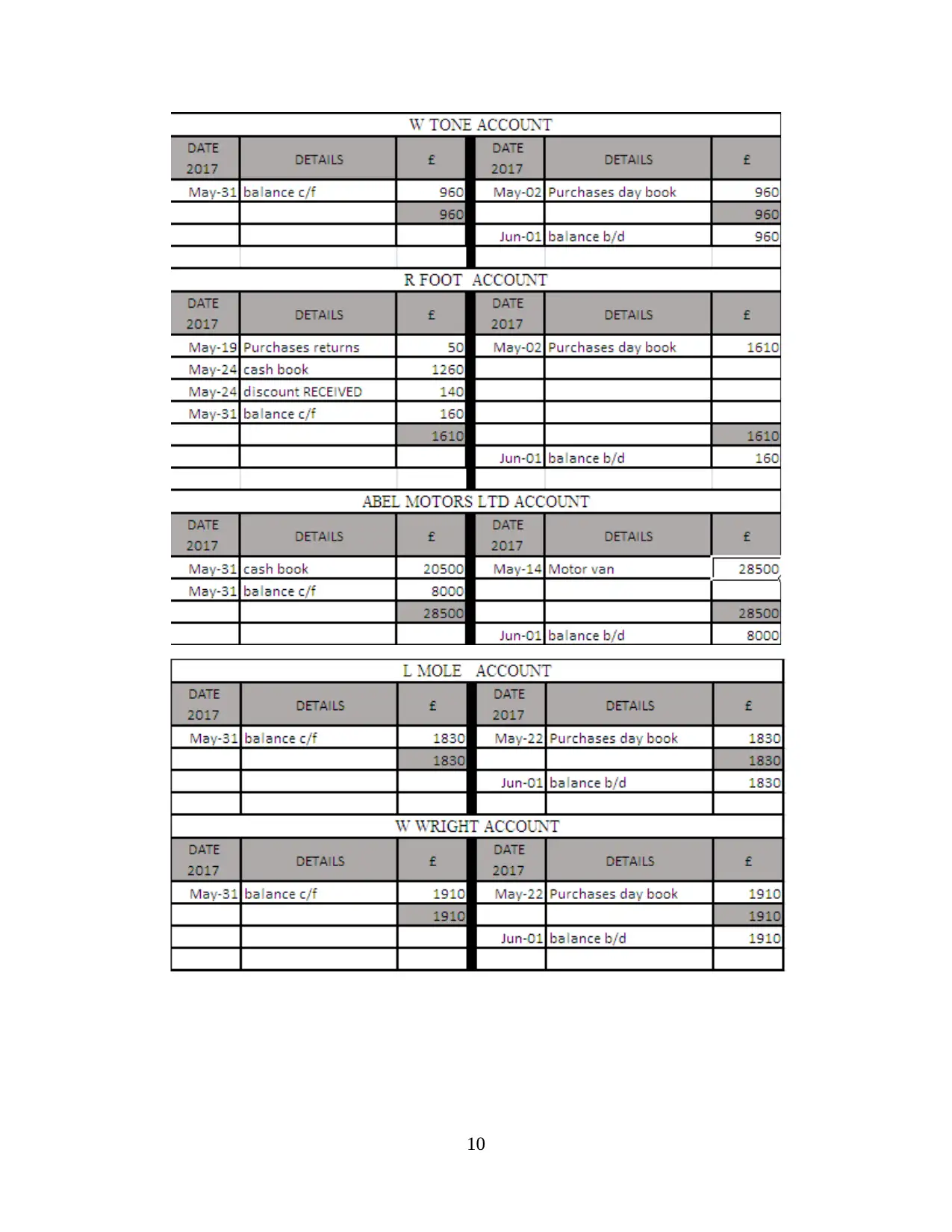

2. Drafting ledger account of above journal entries

The above journal consist of each and every transactions on the basis of given dataset. All

the accounts consist of their own entries. The managers and owners will be getting great

advantage for giving their highlights on analysis of cost and gains which are required from

various sources from all activities on basis of company's operation by foreseeing the journal

entries (Warren and Jones, 2018). For decision making and planning, these entries plays huge

contribution and it will be decreasing the level of different cost and expenses on the perspective

of company.

7

The above journal consist of each and every transactions on the basis of given dataset. All

the accounts consist of their own entries. The managers and owners will be getting great

advantage for giving their highlights on analysis of cost and gains which are required from

various sources from all activities on basis of company's operation by foreseeing the journal

entries (Warren and Jones, 2018). For decision making and planning, these entries plays huge

contribution and it will be decreasing the level of different cost and expenses on the perspective

of company.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.