Financial Accounting 2 Report

VerifiedAdded on 2020/03/16

|10

|1911

|357

Report

AI Summary

This report covers various aspects of financial accounting, including the treatment of contingent liabilities, lease obligations, and long-term service leave provisions. It includes detailed calculations, journal entries, and a cash flow statement for T Pty Limited, along with references to relevant literature. The report aims to provide a comprehensive understanding of financial accounting practices and their implications for financial reporting.

Financial Accounting 1

FINANCIAL ACCOUNTING

By Name

Course Title

Instructor’s name

Name of Institution

Name of Department

FINANCIAL ACCOUNTING

By Name

Course Title

Instructor’s name

Name of Institution

Name of Department

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

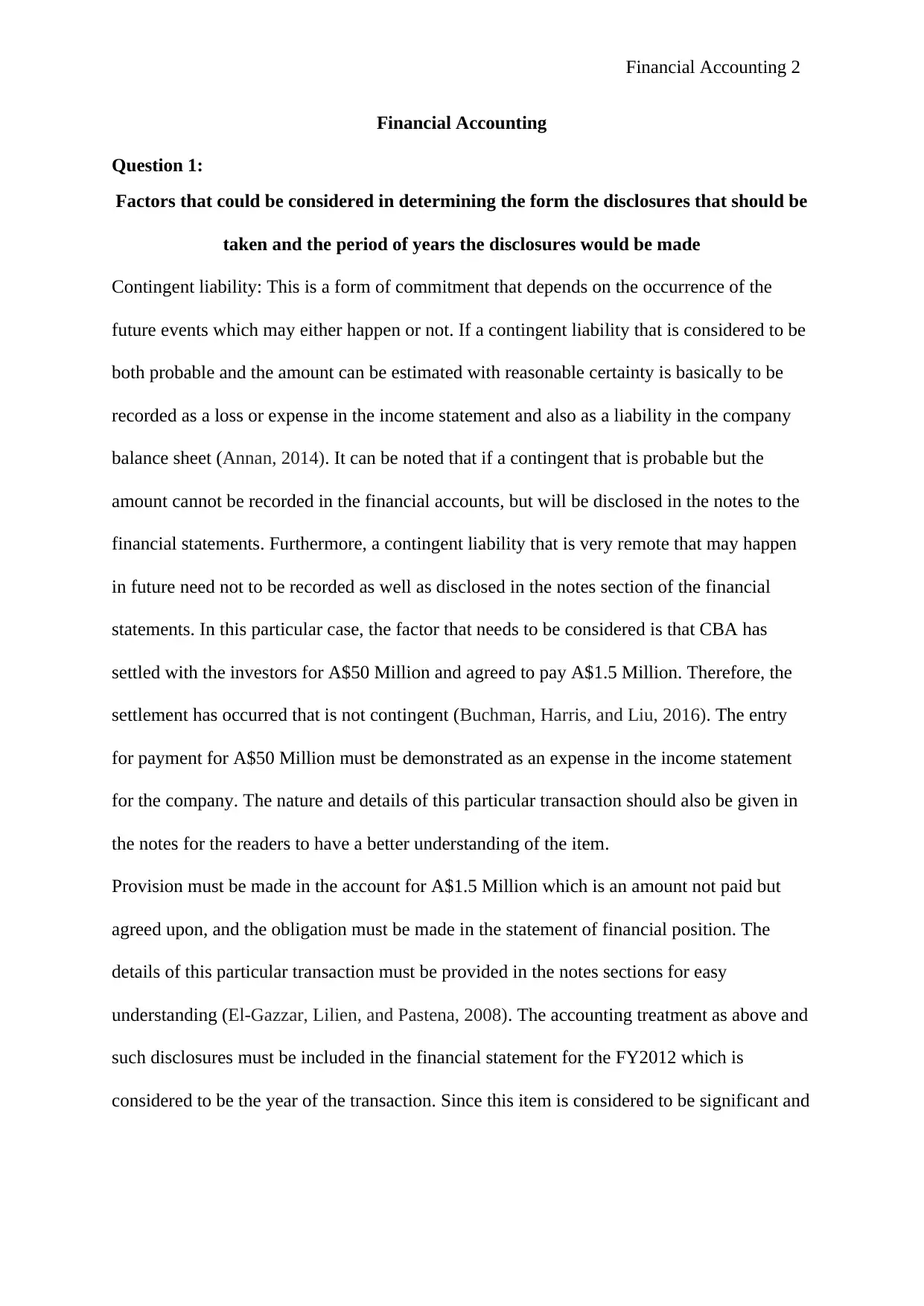

Financial Accounting 2

Financial Accounting

Question 1:

Factors that could be considered in determining the form the disclosures that should be

taken and the period of years the disclosures would be made

Contingent liability: This is a form of commitment that depends on the occurrence of the

future events which may either happen or not. If a contingent liability that is considered to be

both probable and the amount can be estimated with reasonable certainty is basically to be

recorded as a loss or expense in the income statement and also as a liability in the company

balance sheet (Annan, 2014). It can be noted that if a contingent that is probable but the

amount cannot be recorded in the financial accounts, but will be disclosed in the notes to the

financial statements. Furthermore, a contingent liability that is very remote that may happen

in future need not to be recorded as well as disclosed in the notes section of the financial

statements. In this particular case, the factor that needs to be considered is that CBA has

settled with the investors for A$50 Million and agreed to pay A$1.5 Million. Therefore, the

settlement has occurred that is not contingent (Buchman, Harris, and Liu, 2016). The entry

for payment for A$50 Million must be demonstrated as an expense in the income statement

for the company. The nature and details of this particular transaction should also be given in

the notes for the readers to have a better understanding of the item.

Provision must be made in the account for A$1.5 Million which is an amount not paid but

agreed upon, and the obligation must be made in the statement of financial position. The

details of this particular transaction must be provided in the notes sections for easy

understanding (El-Gazzar, Lilien, and Pastena, 2008). The accounting treatment as above and

such disclosures must be included in the financial statement for the FY2012 which is

considered to be the year of the transaction. Since this item is considered to be significant and

Financial Accounting

Question 1:

Factors that could be considered in determining the form the disclosures that should be

taken and the period of years the disclosures would be made

Contingent liability: This is a form of commitment that depends on the occurrence of the

future events which may either happen or not. If a contingent liability that is considered to be

both probable and the amount can be estimated with reasonable certainty is basically to be

recorded as a loss or expense in the income statement and also as a liability in the company

balance sheet (Annan, 2014). It can be noted that if a contingent that is probable but the

amount cannot be recorded in the financial accounts, but will be disclosed in the notes to the

financial statements. Furthermore, a contingent liability that is very remote that may happen

in future need not to be recorded as well as disclosed in the notes section of the financial

statements. In this particular case, the factor that needs to be considered is that CBA has

settled with the investors for A$50 Million and agreed to pay A$1.5 Million. Therefore, the

settlement has occurred that is not contingent (Buchman, Harris, and Liu, 2016). The entry

for payment for A$50 Million must be demonstrated as an expense in the income statement

for the company. The nature and details of this particular transaction should also be given in

the notes for the readers to have a better understanding of the item.

Provision must be made in the account for A$1.5 Million which is an amount not paid but

agreed upon, and the obligation must be made in the statement of financial position. The

details of this particular transaction must be provided in the notes sections for easy

understanding (El-Gazzar, Lilien, and Pastena, 2008). The accounting treatment as above and

such disclosures must be included in the financial statement for the FY2012 which is

considered to be the year of the transaction. Since this item is considered to be significant and

Financial Accounting 3

repetitive, complete disclosures must be made in the director's report and the action plan that

would be implemented in future so as to ensure that such incidents do not repeat itself.

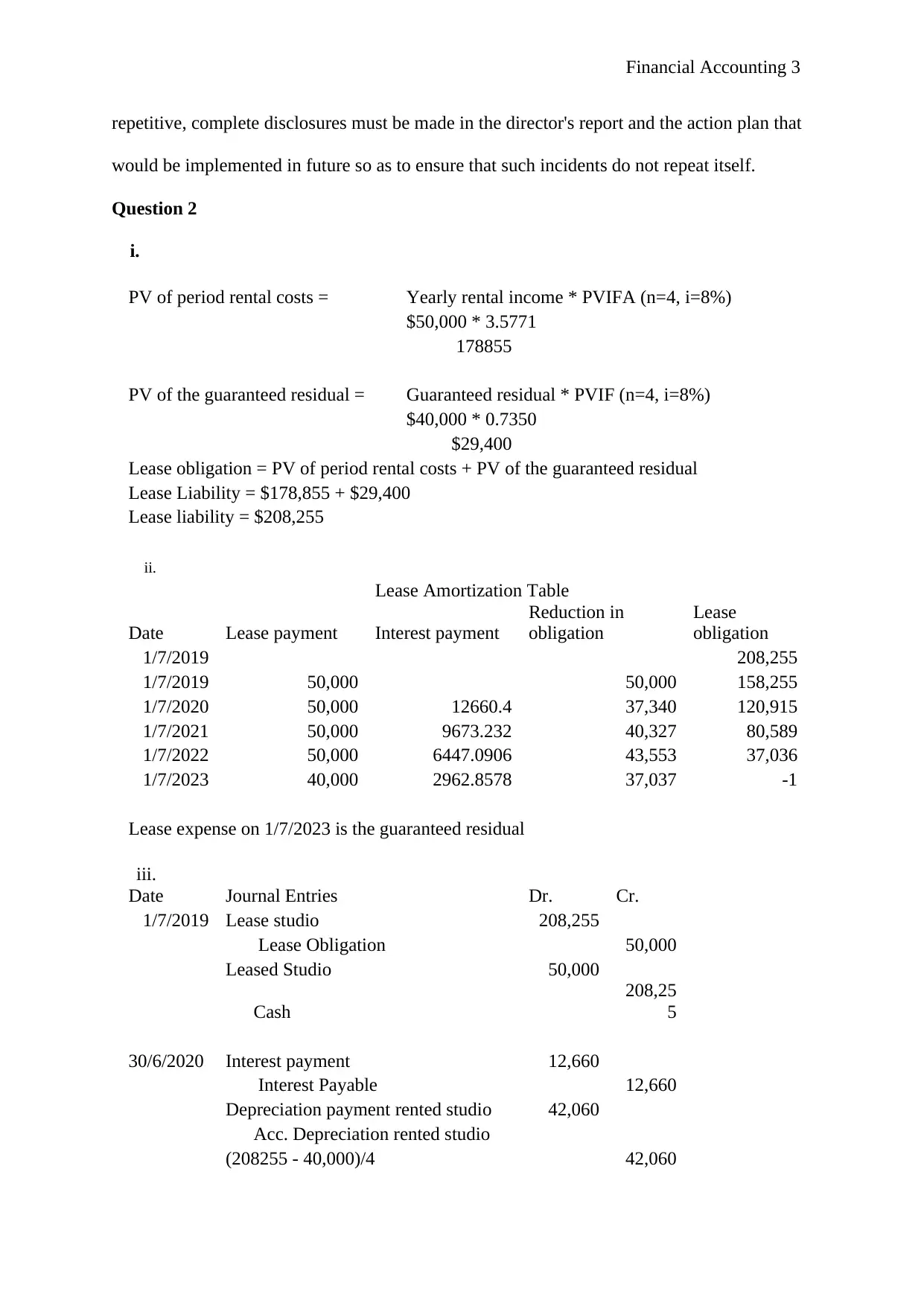

Question 2

i.

PV of period rental costs = Yearly rental income * PVIFA (n=4, i=8%)

$50,000 * 3.5771

178855

PV of the guaranteed residual = Guaranteed residual * PVIF (n=4, i=8%)

$40,000 * 0.7350

$29,400

Lease obligation = PV of period rental costs + PV of the guaranteed residual

Lease Liability = $178,855 + $29,400

Lease liability = $208,255

ii.

Lease Amortization Table

Date Lease payment Interest payment

Reduction in

obligation

Lease

obligation

1/7/2019 208,255

1/7/2019 50,000 50,000 158,255

1/7/2020 50,000 12660.4 37,340 120,915

1/7/2021 50,000 9673.232 40,327 80,589

1/7/2022 50,000 6447.0906 43,553 37,036

1/7/2023 40,000 2962.8578 37,037 -1

Lease expense on 1/7/2023 is the guaranteed residual

iii.

Date Journal Entries Dr. Cr.

1/7/2019 Lease studio 208,255

Lease Obligation 50,000

Leased Studio 50,000

Cash

208,25

5

30/6/2020 Interest payment 12,660

Interest Payable 12,660

Depreciation payment rented studio 42,060

Acc. Depreciation rented studio

(208255 - 40,000)/4 42,060

repetitive, complete disclosures must be made in the director's report and the action plan that

would be implemented in future so as to ensure that such incidents do not repeat itself.

Question 2

i.

PV of period rental costs = Yearly rental income * PVIFA (n=4, i=8%)

$50,000 * 3.5771

178855

PV of the guaranteed residual = Guaranteed residual * PVIF (n=4, i=8%)

$40,000 * 0.7350

$29,400

Lease obligation = PV of period rental costs + PV of the guaranteed residual

Lease Liability = $178,855 + $29,400

Lease liability = $208,255

ii.

Lease Amortization Table

Date Lease payment Interest payment

Reduction in

obligation

Lease

obligation

1/7/2019 208,255

1/7/2019 50,000 50,000 158,255

1/7/2020 50,000 12660.4 37,340 120,915

1/7/2021 50,000 9673.232 40,327 80,589

1/7/2022 50,000 6447.0906 43,553 37,036

1/7/2023 40,000 2962.8578 37,037 -1

Lease expense on 1/7/2023 is the guaranteed residual

iii.

Date Journal Entries Dr. Cr.

1/7/2019 Lease studio 208,255

Lease Obligation 50,000

Leased Studio 50,000

Cash

208,25

5

30/6/2020 Interest payment 12,660

Interest Payable 12,660

Depreciation payment rented studio 42,060

Acc. Depreciation rented studio

(208255 - 40,000)/4 42,060

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

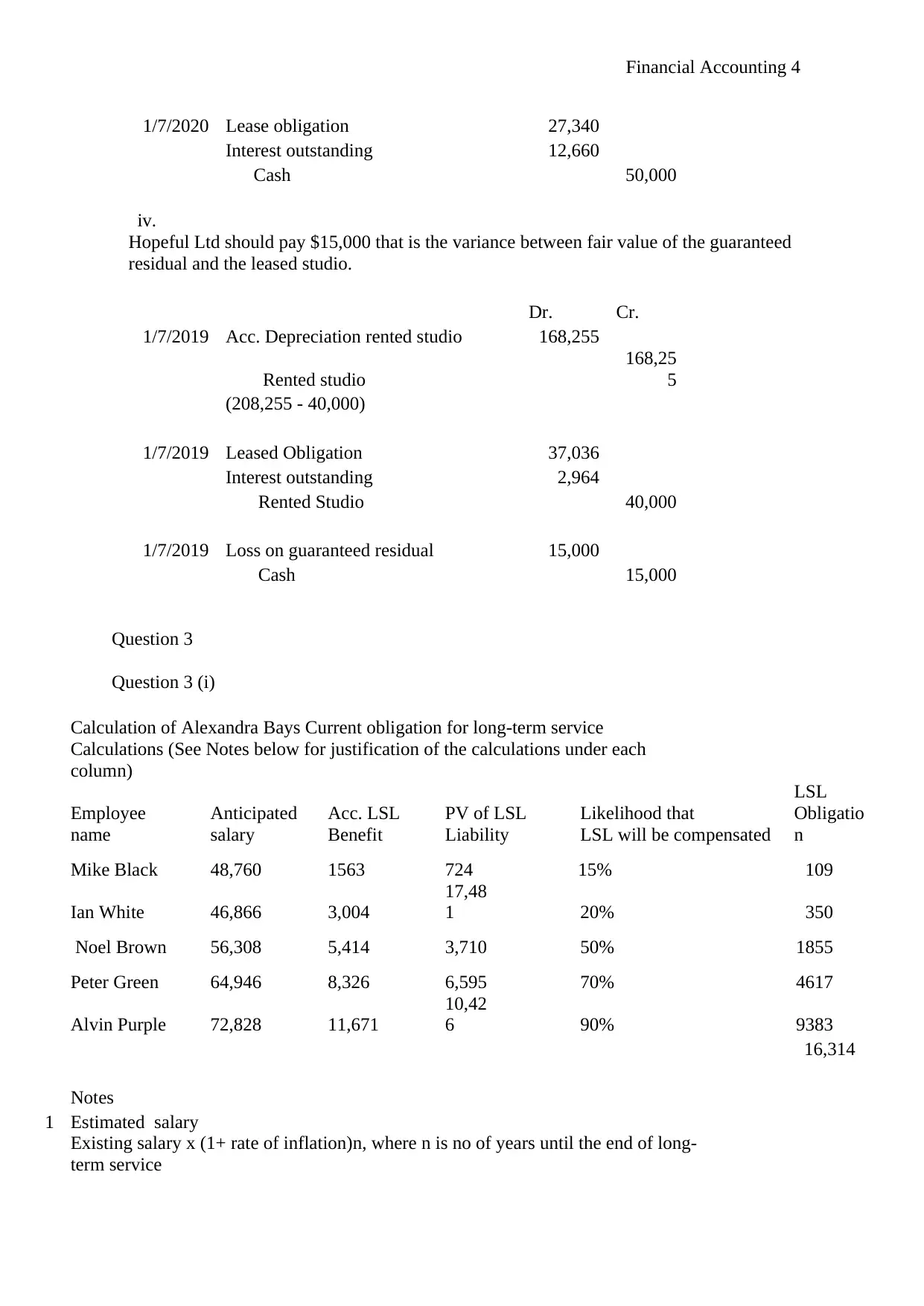

Financial Accounting 4

1/7/2020 Lease obligation 27,340

Interest outstanding 12,660

Cash 50,000

iv.

Hopeful Ltd should pay $15,000 that is the variance between fair value of the guaranteed

residual and the leased studio.

Dr. Cr.

1/7/2019 Acc. Depreciation rented studio 168,255

Rented studio

168,25

5

(208,255 - 40,000)

1/7/2019 Leased Obligation 37,036

Interest outstanding 2,964

Rented Studio 40,000

1/7/2019 Loss on guaranteed residual 15,000

Cash 15,000

Question 3

Question 3 (i)

Calculation of Alexandra Bays Current obligation for long-term service

Calculations (See Notes below for justification of the calculations under each

column)

Employee

name

Anticipated

salary

Acc. LSL

Benefit

PV of LSL

Liability

Likelihood that

LSL will be compensated

LSL

Obligatio

n

Mike Black 48,760 1563 724 15% 109

Ian White 46,866 3,004

17,48

1 20% 350

Noel Brown 56,308 5,414 3,710 50% 1855

Peter Green 64,946 8,326 6,595 70% 4617

Alvin Purple 72,828 11,671

10,42

6 90% 9383

16,314

Notes

1 Estimated salary

Existing salary x (1+ rate of inflation)n, where n is no of years until the end of long-

term service

1/7/2020 Lease obligation 27,340

Interest outstanding 12,660

Cash 50,000

iv.

Hopeful Ltd should pay $15,000 that is the variance between fair value of the guaranteed

residual and the leased studio.

Dr. Cr.

1/7/2019 Acc. Depreciation rented studio 168,255

Rented studio

168,25

5

(208,255 - 40,000)

1/7/2019 Leased Obligation 37,036

Interest outstanding 2,964

Rented Studio 40,000

1/7/2019 Loss on guaranteed residual 15,000

Cash 15,000

Question 3

Question 3 (i)

Calculation of Alexandra Bays Current obligation for long-term service

Calculations (See Notes below for justification of the calculations under each

column)

Employee

name

Anticipated

salary

Acc. LSL

Benefit

PV of LSL

Liability

Likelihood that

LSL will be compensated

LSL

Obligatio

n

Mike Black 48,760 1563 724 15% 109

Ian White 46,866 3,004

17,48

1 20% 350

Noel Brown 56,308 5,414 3,710 50% 1855

Peter Green 64,946 8,326 6,595 70% 4617

Alvin Purple 72,828 11,671

10,42

6 90% 9383

16,314

Notes

1 Estimated salary

Existing salary x (1+ rate of inflation)n, where n is no of years until the end of long-

term service

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

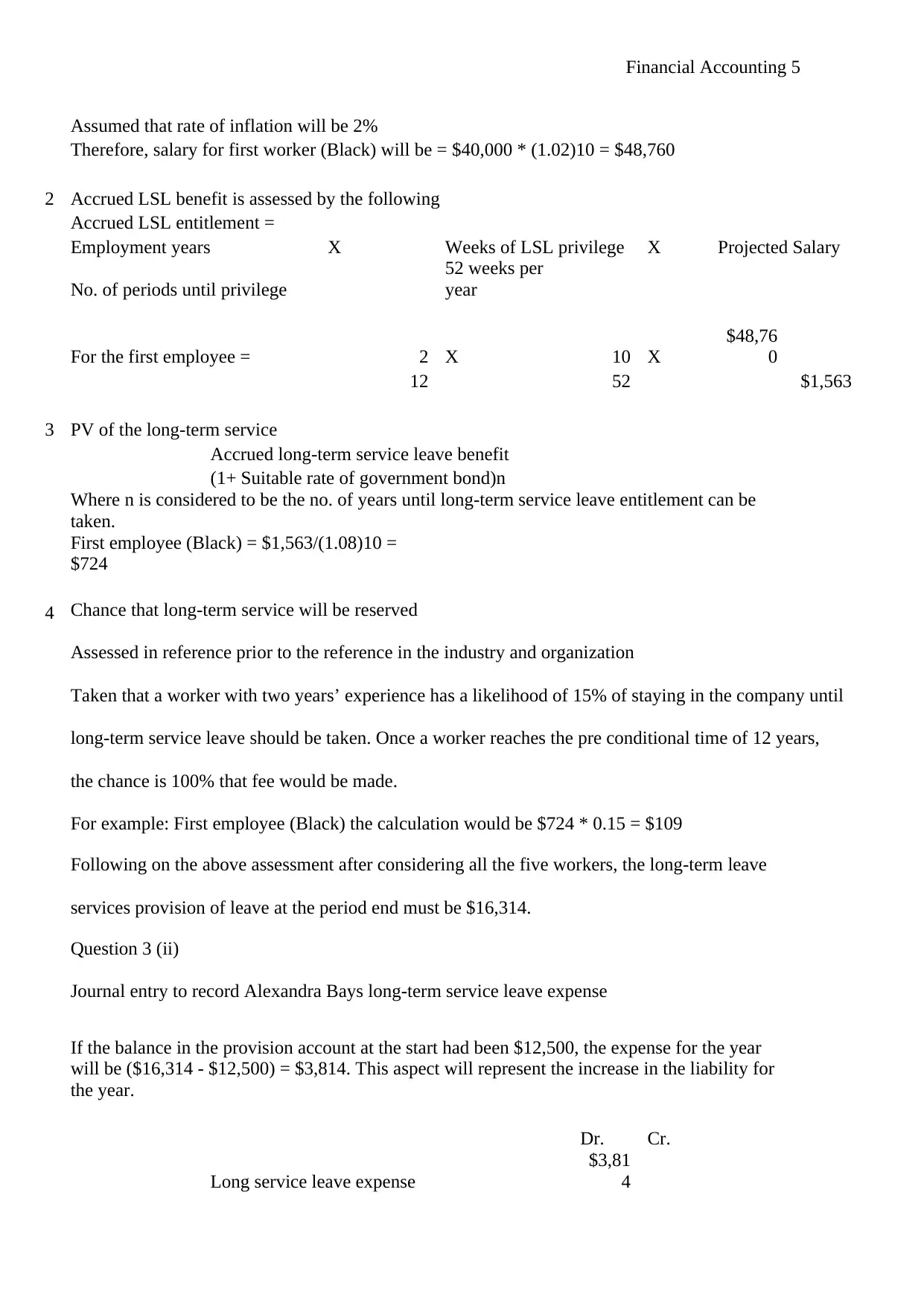

Financial Accounting 5

Assumed that rate of inflation will be 2%

Therefore, salary for first worker (Black) will be = $40,000 * (1.02)10 = $48,760

2 Accrued LSL benefit is assessed by the following

Accrued LSL entitlement =

Employment years X Weeks of LSL privilege X Projected Salary

No. of periods until privilege

52 weeks per

year

For the first employee = 2 X 10 X

$48,76

0

12 52 $1,563

3 PV of the long-term service

Accrued long-term service leave benefit

(1+ Suitable rate of government bond)n

Where n is considered to be the no. of years until long-term service leave entitlement can be

taken.

First employee (Black) = $1,563/(1.08)10 =

$724

4 Chance that long-term service will be reserved

Assessed in reference prior to the reference in the industry and organization

Taken that a worker with two years’ experience has a likelihood of 15% of staying in the company until

long-term service leave should be taken. Once a worker reaches the pre conditional time of 12 years,

the chance is 100% that fee would be made.

For example: First employee (Black) the calculation would be $724 * 0.15 = $109

Following on the above assessment after considering all the five workers, the long-term leave

services provision of leave at the period end must be $16,314.

Question 3 (ii)

Journal entry to record Alexandra Bays long-term service leave expense

If the balance in the provision account at the start had been $12,500, the expense for the year

will be ($16,314 - $12,500) = $3,814. This aspect will represent the increase in the liability for

the year.

Dr. Cr.

Long service leave expense

$3,81

4

Assumed that rate of inflation will be 2%

Therefore, salary for first worker (Black) will be = $40,000 * (1.02)10 = $48,760

2 Accrued LSL benefit is assessed by the following

Accrued LSL entitlement =

Employment years X Weeks of LSL privilege X Projected Salary

No. of periods until privilege

52 weeks per

year

For the first employee = 2 X 10 X

$48,76

0

12 52 $1,563

3 PV of the long-term service

Accrued long-term service leave benefit

(1+ Suitable rate of government bond)n

Where n is considered to be the no. of years until long-term service leave entitlement can be

taken.

First employee (Black) = $1,563/(1.08)10 =

$724

4 Chance that long-term service will be reserved

Assessed in reference prior to the reference in the industry and organization

Taken that a worker with two years’ experience has a likelihood of 15% of staying in the company until

long-term service leave should be taken. Once a worker reaches the pre conditional time of 12 years,

the chance is 100% that fee would be made.

For example: First employee (Black) the calculation would be $724 * 0.15 = $109

Following on the above assessment after considering all the five workers, the long-term leave

services provision of leave at the period end must be $16,314.

Question 3 (ii)

Journal entry to record Alexandra Bays long-term service leave expense

If the balance in the provision account at the start had been $12,500, the expense for the year

will be ($16,314 - $12,500) = $3,814. This aspect will represent the increase in the liability for

the year.

Dr. Cr.

Long service leave expense

$3,81

4

Financial Accounting 6

Long service leave provision $3,814

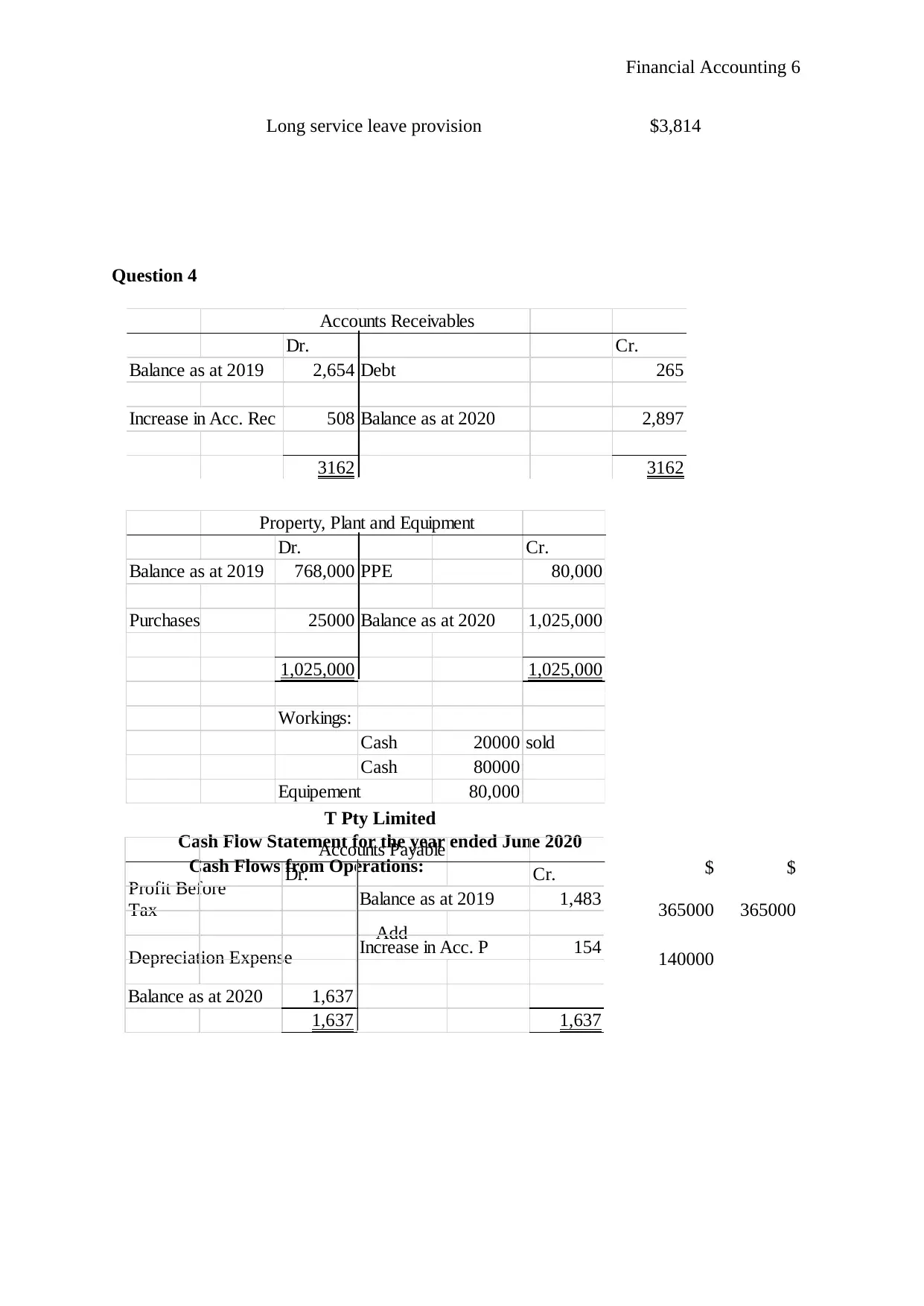

Question 4

T Pty Limited

Cash Flow Statement for the year ended June 2020

Cash Flows from Operations: $ $

Profit Before

Tax 365000 365000

Add

Depreciation Expense 140000

Accounts Receivables

Dr. Cr.

Balance as at 2019 2,654 Debt 265

Increase in Acc. Rec 508 Balance as at 2020 2,897

3162 3162

Property, Plant and Equipment

Dr. Cr.

Balance as at 2019 768,000 PPE 80,000

Purchases 25000 Balance as at 2020 1,025,000

1,025,000 1,025,000

Workings:

Cash 20000 sold

Cash 80000

Equipement 80,000

Accounts Payable

Dr. Cr.

Balance as at 2019 1,483

Increase in Acc. P 154

Balance as at 2020 1,637

1,637 1,637

Long service leave provision $3,814

Question 4

T Pty Limited

Cash Flow Statement for the year ended June 2020

Cash Flows from Operations: $ $

Profit Before

Tax 365000 365000

Add

Depreciation Expense 140000

Accounts Receivables

Dr. Cr.

Balance as at 2019 2,654 Debt 265

Increase in Acc. Rec 508 Balance as at 2020 2,897

3162 3162

Property, Plant and Equipment

Dr. Cr.

Balance as at 2019 768,000 PPE 80,000

Purchases 25000 Balance as at 2020 1,025,000

1,025,000 1,025,000

Workings:

Cash 20000 sold

Cash 80000

Equipement 80,000

Accounts Payable

Dr. Cr.

Balance as at 2019 1,483

Increase in Acc. P 154

Balance as at 2020 1,637

1,637 1,637

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

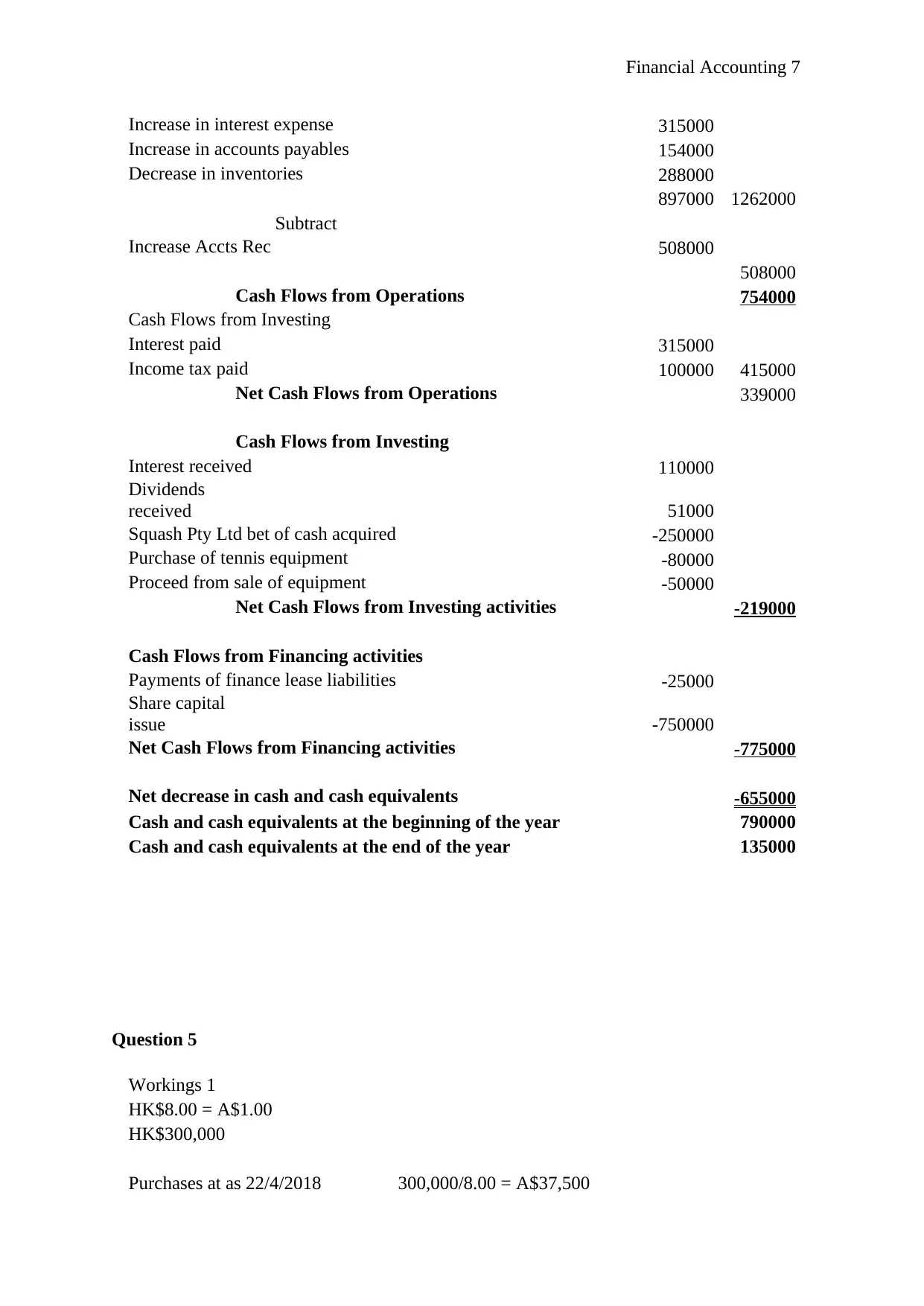

Financial Accounting 7

Increase in interest expense 315000

Increase in accounts payables 154000

Decrease in inventories 288000

897000 1262000

Subtract

Increase Accts Rec 508000

508000

Cash Flows from Operations 754000

Cash Flows from Investing

Interest paid 315000

Income tax paid 100000 415000

Net Cash Flows from Operations 339000

Cash Flows from Investing

Interest received 110000

Dividends

received 51000

Squash Pty Ltd bet of cash acquired -250000

Purchase of tennis equipment -80000

Proceed from sale of equipment -50000

Net Cash Flows from Investing activities -219000

Cash Flows from Financing activities

Payments of finance lease liabilities -25000

Share capital

issue -750000

Net Cash Flows from Financing activities -775000

Net decrease in cash and cash equivalents -655000

Cash and cash equivalents at the beginning of the year 790000

Cash and cash equivalents at the end of the year 135000

Question 5

Workings 1

HK$8.00 = A$1.00

HK$300,000

Purchases at as 22/4/2018 300,000/8.00 = A$37,500

Increase in interest expense 315000

Increase in accounts payables 154000

Decrease in inventories 288000

897000 1262000

Subtract

Increase Accts Rec 508000

508000

Cash Flows from Operations 754000

Cash Flows from Investing

Interest paid 315000

Income tax paid 100000 415000

Net Cash Flows from Operations 339000

Cash Flows from Investing

Interest received 110000

Dividends

received 51000

Squash Pty Ltd bet of cash acquired -250000

Purchase of tennis equipment -80000

Proceed from sale of equipment -50000

Net Cash Flows from Investing activities -219000

Cash Flows from Financing activities

Payments of finance lease liabilities -25000

Share capital

issue -750000

Net Cash Flows from Financing activities -775000

Net decrease in cash and cash equivalents -655000

Cash and cash equivalents at the beginning of the year 790000

Cash and cash equivalents at the end of the year 135000

Question 5

Workings 1

HK$8.00 = A$1.00

HK$300,000

Purchases at as 22/4/2018 300,000/8.00 = A$37,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Accounting 8

(HF$300,000/

3) HK$100,000

HK$8.56 = A$1.00

HK$100,000

Purchases at as 30/5/2018 100,000/8.56 = A$11682

Foreign exchange gain

(12500-11682) =

818

HK$8.56 = A$1.00

HK$100,000

Purchases at as 30/6/2018 100,000/8.59 = A$11641

Foreign exchange gain

(12500-11641) =

859

HK$8.56 = A$1.00

HK$100,000

Purchases at as 31/7/2018 100,000/8.94 = A$11186

Foreign exchange gain

(12500-11186) =

1314

Workings 1

Yen160 = A$1.00

Yen 5,000,000

Purchases at as 30/5/2018 5,000,000/160 = A$31,250

Purchases at as 31/7/2018 5,000,000/260 = A$19,230

Foreign exchange

gain (31250-19231) = 12019

20, 000,000 * 11.5 *

10

23,000,00

0

Loan = 3,000,000

Date Dr. Cr.

30/4 Purchases A$37500

Accounts Payables A$37500

To record Purchases at as 22/4/2018

(HF$300,000/

3) HK$100,000

HK$8.56 = A$1.00

HK$100,000

Purchases at as 30/5/2018 100,000/8.56 = A$11682

Foreign exchange gain

(12500-11682) =

818

HK$8.56 = A$1.00

HK$100,000

Purchases at as 30/6/2018 100,000/8.59 = A$11641

Foreign exchange gain

(12500-11641) =

859

HK$8.56 = A$1.00

HK$100,000

Purchases at as 31/7/2018 100,000/8.94 = A$11186

Foreign exchange gain

(12500-11186) =

1314

Workings 1

Yen160 = A$1.00

Yen 5,000,000

Purchases at as 30/5/2018 5,000,000/160 = A$31,250

Purchases at as 31/7/2018 5,000,000/260 = A$19,230

Foreign exchange

gain (31250-19231) = 12019

20, 000,000 * 11.5 *

10

23,000,00

0

Loan = 3,000,000

Date Dr. Cr.

30/4 Purchases A$37500

Accounts Payables A$37500

To record Purchases at as 22/4/2018

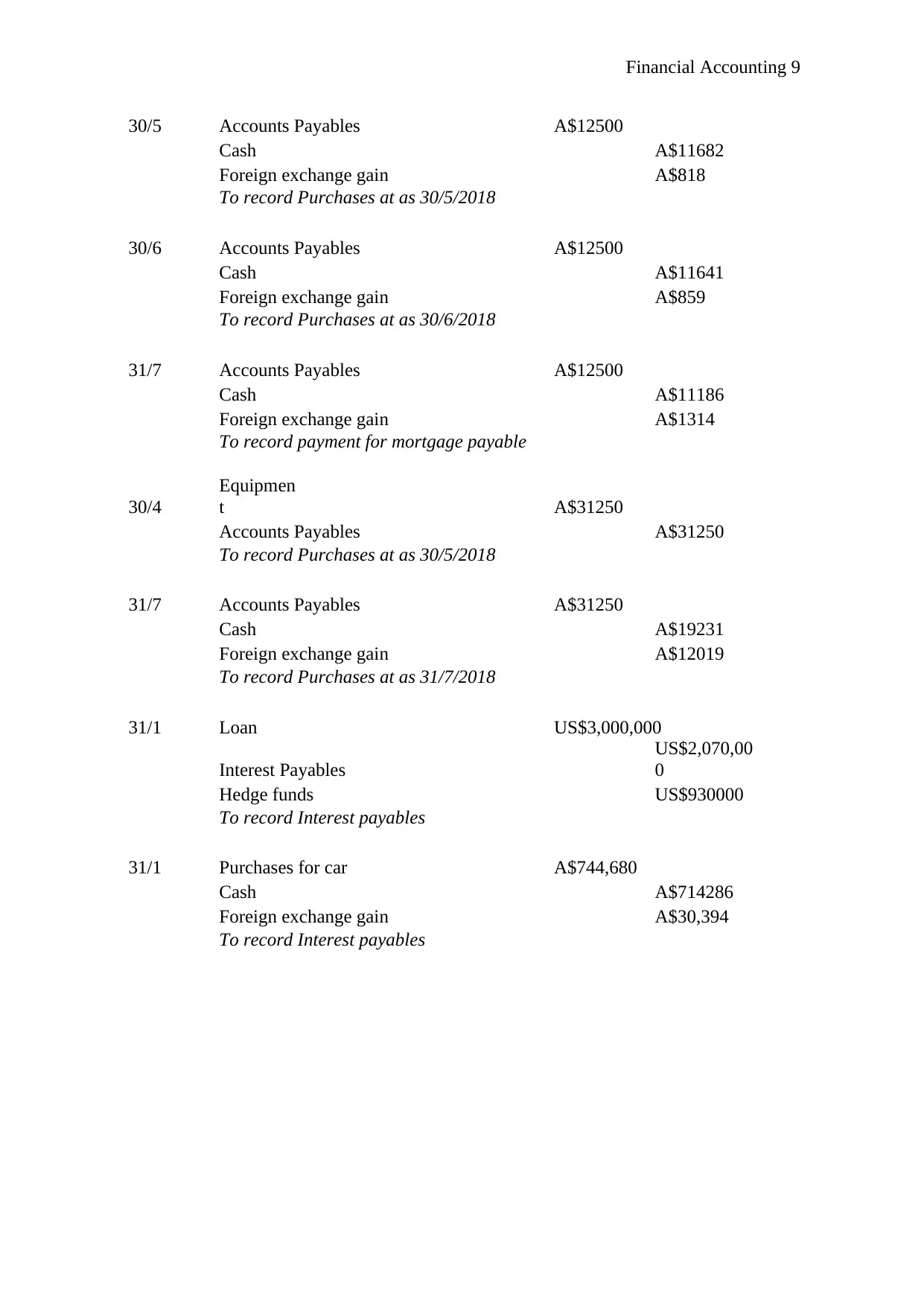

Financial Accounting 9

30/5 Accounts Payables A$12500

Cash A$11682

Foreign exchange gain A$818

To record Purchases at as 30/5/2018

30/6 Accounts Payables A$12500

Cash A$11641

Foreign exchange gain A$859

To record Purchases at as 30/6/2018

31/7 Accounts Payables A$12500

Cash A$11186

Foreign exchange gain A$1314

To record payment for mortgage payable

30/4

Equipmen

t A$31250

Accounts Payables A$31250

To record Purchases at as 30/5/2018

31/7 Accounts Payables A$31250

Cash A$19231

Foreign exchange gain A$12019

To record Purchases at as 31/7/2018

31/1 Loan US$3,000,000

Interest Payables

US$2,070,00

0

Hedge funds US$930000

To record Interest payables

31/1 Purchases for car A$744,680

Cash A$714286

Foreign exchange gain A$30,394

To record Interest payables

30/5 Accounts Payables A$12500

Cash A$11682

Foreign exchange gain A$818

To record Purchases at as 30/5/2018

30/6 Accounts Payables A$12500

Cash A$11641

Foreign exchange gain A$859

To record Purchases at as 30/6/2018

31/7 Accounts Payables A$12500

Cash A$11186

Foreign exchange gain A$1314

To record payment for mortgage payable

30/4

Equipmen

t A$31250

Accounts Payables A$31250

To record Purchases at as 30/5/2018

31/7 Accounts Payables A$31250

Cash A$19231

Foreign exchange gain A$12019

To record Purchases at as 31/7/2018

31/1 Loan US$3,000,000

Interest Payables

US$2,070,00

0

Hedge funds US$930000

To record Interest payables

31/1 Purchases for car A$744,680

Cash A$714286

Foreign exchange gain A$30,394

To record Interest payables

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Accounting 10

Bibliography

Annan, M., 2014. The Case of Lease Accounting (Doctoral dissertation, University of

Amsterdam).

Biondi, Y., Bloomfield, R. J., Glover, J. C., Jamal, K., Ohlson, J. A., Penman, S. H., ... &

Wilks, T. J. 2011. A Perspective on the Joint IASB/FASB Exposure Draft on Accounting for

Leases: American Accounting Association's Financial Accounting Standards Committee

(AAA FASC). Accounting Horizons, 25(4), 861-871.

Buchman, T. A., Harris, P., & Liu, M. 2016. GAAP vs. IFRS Treatment of Leases and the

Impact on Financial Ratios.

Deegan, C. (2012). Australian financial accounting. McGraw-Hill Education Australia.

El-Gazzar, S., Lilien, S., & Pastena, V. 2008. Accounting for leases by lessees. Journal of

Accounting and Economics, 8(3), 217-237.

Ji, S. and Deegan, C., 2011. Accounting for contaminated sites: how transparent are

Australian companies?. Australian Accounting Review, 21(2), pp.131-153.

Grenier, J. H., Pomeroy, B., & Stern, M. T. 2015. The effects of accounting standard

precision, auditor task expertise, and judgment frameworks on audit firm litigation

exposure. Contemporary Accounting Research, 32(1), 336-357.

Riccardi, L., 2016. Accounting Standards for Business Enterprises No. 3—Investment Real

Estates. In China Accounting Standards (pp. 25-29). Springer Singapore.

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and

key ratios: Evidence from Australia. Australasian Accounting Business & Finance

Journal, 9(3), p.27.

Bibliography

Annan, M., 2014. The Case of Lease Accounting (Doctoral dissertation, University of

Amsterdam).

Biondi, Y., Bloomfield, R. J., Glover, J. C., Jamal, K., Ohlson, J. A., Penman, S. H., ... &

Wilks, T. J. 2011. A Perspective on the Joint IASB/FASB Exposure Draft on Accounting for

Leases: American Accounting Association's Financial Accounting Standards Committee

(AAA FASC). Accounting Horizons, 25(4), 861-871.

Buchman, T. A., Harris, P., & Liu, M. 2016. GAAP vs. IFRS Treatment of Leases and the

Impact on Financial Ratios.

Deegan, C. (2012). Australian financial accounting. McGraw-Hill Education Australia.

El-Gazzar, S., Lilien, S., & Pastena, V. 2008. Accounting for leases by lessees. Journal of

Accounting and Economics, 8(3), 217-237.

Ji, S. and Deegan, C., 2011. Accounting for contaminated sites: how transparent are

Australian companies?. Australian Accounting Review, 21(2), pp.131-153.

Grenier, J. H., Pomeroy, B., & Stern, M. T. 2015. The effects of accounting standard

precision, auditor task expertise, and judgment frameworks on audit firm litigation

exposure. Contemporary Accounting Research, 32(1), 336-357.

Riccardi, L., 2016. Accounting Standards for Business Enterprises No. 3—Investment Real

Estates. In China Accounting Standards (pp. 25-29). Springer Singapore.

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and

key ratios: Evidence from Australia. Australasian Accounting Business & Finance

Journal, 9(3), p.27.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.