Technology Enterprise Ltd: Intangible Assets & AASB 138/IAS 38 Review

VerifiedAdded on 2022/12/26

|8

|3062

|29

Report

AI Summary

This report provides a comprehensive analysis of Technology Enterprise Ltd's accounting practices concerning an R&D project, focusing on compliance with AASB 138/IAS 38. It examines the accounting treatment of the project's costs, including research and development expenses, and the recognition and measurement of the resulting intangible asset. The report details the application of present value techniques to estimate the asset's value and addresses the potential reduction in comparability of financial statements due to varying interpretations and applications of accounting standards. Furthermore, it offers insights into the specific requirements of AASB 138/IAS 38, emphasizing the distinction between research and development costs and the importance of proper asset valuation and impairment reviews. The report concludes with recommendations for Technology Enterprise Ltd to ensure accurate and transparent financial reporting in accordance with accounting standards.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student

Name of the University

Author’s Note

Financial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING

Executive Summary

The first part of the report sheds light on the accounting treatments that Technology

Enterprise Ltd needs to follow for the accounting of the project through the consideration of

AASB 138/IAS 38. The second part discusses about the limitation of the comparability

characteristic of the financial statements. The last part provides discussion on AASB 138/IAS

38 while recommending certain action for the company to address the concerns.

Executive Summary

The first part of the report sheds light on the accounting treatments that Technology

Enterprise Ltd needs to follow for the accounting of the project through the consideration of

AASB 138/IAS 38. The second part discusses about the limitation of the comparability

characteristic of the financial statements. The last part provides discussion on AASB 138/IAS

38 while recommending certain action for the company to address the concerns.

2FINANCIAL ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

1. Accounting of the Project in the Financial Statements..........................................................3

2. Reduction of Comparability of Financial Statements............................................................5

3. Understanding of AASB 138/IAS 38.....................................................................................5

Conclusion and Recommendation..............................................................................................6

References..................................................................................................................................7

Table of Contents

Introduction................................................................................................................................3

1. Accounting of the Project in the Financial Statements..........................................................3

2. Reduction of Comparability of Financial Statements............................................................5

3. Understanding of AASB 138/IAS 38.....................................................................................5

Conclusion and Recommendation..............................................................................................6

References..................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING

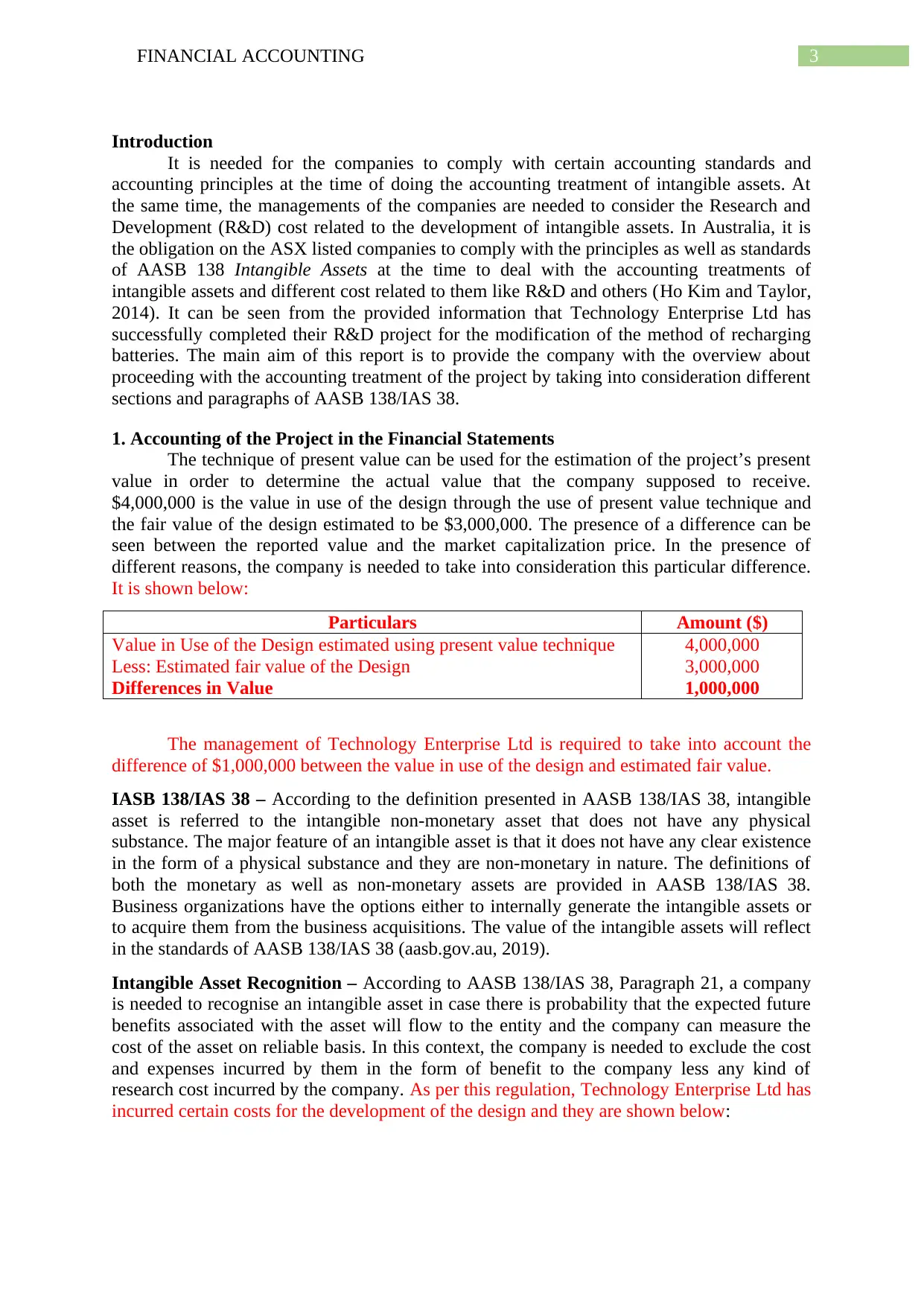

Introduction

It is needed for the companies to comply with certain accounting standards and

accounting principles at the time of doing the accounting treatment of intangible assets. At

the same time, the managements of the companies are needed to consider the Research and

Development (R&D) cost related to the development of intangible assets. In Australia, it is

the obligation on the ASX listed companies to comply with the principles as well as standards

of AASB 138 Intangible Assets at the time to deal with the accounting treatments of

intangible assets and different cost related to them like R&D and others (Ho Kim and Taylor,

2014). It can be seen from the provided information that Technology Enterprise Ltd has

successfully completed their R&D project for the modification of the method of recharging

batteries. The main aim of this report is to provide the company with the overview about

proceeding with the accounting treatment of the project by taking into consideration different

sections and paragraphs of AASB 138/IAS 38.

1. Accounting of the Project in the Financial Statements

The technique of present value can be used for the estimation of the project’s present

value in order to determine the actual value that the company supposed to receive.

$4,000,000 is the value in use of the design through the use of present value technique and

the fair value of the design estimated to be $3,000,000. The presence of a difference can be

seen between the reported value and the market capitalization price. In the presence of

different reasons, the company is needed to take into consideration this particular difference.

It is shown below:

Particulars Amount ($)

Value in Use of the Design estimated using present value technique

Less: Estimated fair value of the Design

Differences in Value

4,000,000

3,000,000

1,000,000

The management of Technology Enterprise Ltd is required to take into account the

difference of $1,000,000 between the value in use of the design and estimated fair value.

IASB 138/IAS 38 – According to the definition presented in AASB 138/IAS 38, intangible

asset is referred to the intangible non-monetary asset that does not have any physical

substance. The major feature of an intangible asset is that it does not have any clear existence

in the form of a physical substance and they are non-monetary in nature. The definitions of

both the monetary as well as non-monetary assets are provided in AASB 138/IAS 38.

Business organizations have the options either to internally generate the intangible assets or

to acquire them from the business acquisitions. The value of the intangible assets will reflect

in the standards of AASB 138/IAS 38 (aasb.gov.au, 2019).

Intangible Asset Recognition – According to AASB 138/IAS 38, Paragraph 21, a company

is needed to recognise an intangible asset in case there is probability that the expected future

benefits associated with the asset will flow to the entity and the company can measure the

cost of the asset on reliable basis. In this context, the company is needed to exclude the cost

and expenses incurred by them in the form of benefit to the company less any kind of

research cost incurred by the company. As per this regulation, Technology Enterprise Ltd has

incurred certain costs for the development of the design and they are shown below:

Introduction

It is needed for the companies to comply with certain accounting standards and

accounting principles at the time of doing the accounting treatment of intangible assets. At

the same time, the managements of the companies are needed to consider the Research and

Development (R&D) cost related to the development of intangible assets. In Australia, it is

the obligation on the ASX listed companies to comply with the principles as well as standards

of AASB 138 Intangible Assets at the time to deal with the accounting treatments of

intangible assets and different cost related to them like R&D and others (Ho Kim and Taylor,

2014). It can be seen from the provided information that Technology Enterprise Ltd has

successfully completed their R&D project for the modification of the method of recharging

batteries. The main aim of this report is to provide the company with the overview about

proceeding with the accounting treatment of the project by taking into consideration different

sections and paragraphs of AASB 138/IAS 38.

1. Accounting of the Project in the Financial Statements

The technique of present value can be used for the estimation of the project’s present

value in order to determine the actual value that the company supposed to receive.

$4,000,000 is the value in use of the design through the use of present value technique and

the fair value of the design estimated to be $3,000,000. The presence of a difference can be

seen between the reported value and the market capitalization price. In the presence of

different reasons, the company is needed to take into consideration this particular difference.

It is shown below:

Particulars Amount ($)

Value in Use of the Design estimated using present value technique

Less: Estimated fair value of the Design

Differences in Value

4,000,000

3,000,000

1,000,000

The management of Technology Enterprise Ltd is required to take into account the

difference of $1,000,000 between the value in use of the design and estimated fair value.

IASB 138/IAS 38 – According to the definition presented in AASB 138/IAS 38, intangible

asset is referred to the intangible non-monetary asset that does not have any physical

substance. The major feature of an intangible asset is that it does not have any clear existence

in the form of a physical substance and they are non-monetary in nature. The definitions of

both the monetary as well as non-monetary assets are provided in AASB 138/IAS 38.

Business organizations have the options either to internally generate the intangible assets or

to acquire them from the business acquisitions. The value of the intangible assets will reflect

in the standards of AASB 138/IAS 38 (aasb.gov.au, 2019).

Intangible Asset Recognition – According to AASB 138/IAS 38, Paragraph 21, a company

is needed to recognise an intangible asset in case there is probability that the expected future

benefits associated with the asset will flow to the entity and the company can measure the

cost of the asset on reliable basis. In this context, the company is needed to exclude the cost

and expenses incurred by them in the form of benefit to the company less any kind of

research cost incurred by the company. As per this regulation, Technology Enterprise Ltd has

incurred certain costs for the development of the design and they are shown below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING

Particulars Amount ($)

Cost to search and evaluate alternative materials

Cost to design models, construct and test protocols

Cost to train maintenance workers for the new design

Total Incurred Cost

100,000

700,000

200,000

1,000,000

The above table shows that the company has incurred a total cost of $1,000,000 which

is related to the design and the obligation on the company is to ensure recognizing this cost as

expenses.

Measurement of Intangible Assets – According to AASB 138/IAS 38, Paragraph 24, a

company is needed to initially measure an intangible asset at cost. For this reason, the

company is needed to ensure reporting the internally generated asset at the value of

$4,000,000 due to the presence of the fact that the internally generated asset of the firm

complies with the accounting standards of AASB 138/IAS 38. The expenses incurred by

Technology Enterprise Ltd in the form of cost or the amount of time spend by the firm in the

form of R&D; and in the presence of these aspects, it is needed to take into account the

possible alternative techniques for the analysis purpose. According to the norm of AASB

138/IAS 38, the R&D cost of the firms needs to be recognized in the firm’s income statement

as a portion of sank cost (Ji and Lu, 2014).

The company may create their internally generated intangible asset over a certain

period. In opposite to the process of acquisition or in the form of business combination, in

case a business acquire the same asset due to the result of business consolidation, it is needed

to shows the excess of the purchase consideration in the form of goodwill in the appropriate

accounting books. As per the norms of AASB 138/IAS 38, the value of acquisition is that

value that the company needs to consider and the company is needed to review the same on

periodical basis in order to get the indication of impairment (Hu, Percy and Yao, 2015).

Research Cost – According to AASB 138/IAS 38, Paragraph 8, the companies are needed to

undertake the planned and original investigation with the aim to gain effective scientific as

well as technical knowledge for the purpose of better research. In case of Technology

Enterprise Ltd, the cost that the company has incurred is in line with the standards of AASB

138/IAS 38 whereby the cost incurred for the purpose to increase the batteries’ economic life

since it is beneficial for the firm to generate cash flows for the period of ten years. The firm

considered research for the best as well as alternative model in the beginning of the years and

the same was in line with the proper accounting standards (Yao, Percy and Hu, 2015). The

company should consider $1,000,000 as the expenses since this amount is associated with the

development of the design.

Asset Development – According to AASB 138/IAS 38, an asset is developed at the

completion of the research phase of the project and the project outlay is in the form of the

developed asset. In this process, the firm can recognize the asset after proving the technical

feasibility of the asset and the company gain the ability to use as well as sale the same asset

in most significant manner (Bugeja and Loyeung, 2015). Another crucial aspect is the

identification of correct accounting standards in order to identify the value of assets in the

balance sheet when the technical feasibility of the same asset is also proved. As per the

provided information, Technology Enterprise Ltd has incurred significant research cost for

the development of the asset. After conducting the feasibility analysis, the firm has made the

estimation that the project will create a value of $4,000,000 for them (Yao, Percy and Hu,

2013).

Particulars Amount ($)

Cost to search and evaluate alternative materials

Cost to design models, construct and test protocols

Cost to train maintenance workers for the new design

Total Incurred Cost

100,000

700,000

200,000

1,000,000

The above table shows that the company has incurred a total cost of $1,000,000 which

is related to the design and the obligation on the company is to ensure recognizing this cost as

expenses.

Measurement of Intangible Assets – According to AASB 138/IAS 38, Paragraph 24, a

company is needed to initially measure an intangible asset at cost. For this reason, the

company is needed to ensure reporting the internally generated asset at the value of

$4,000,000 due to the presence of the fact that the internally generated asset of the firm

complies with the accounting standards of AASB 138/IAS 38. The expenses incurred by

Technology Enterprise Ltd in the form of cost or the amount of time spend by the firm in the

form of R&D; and in the presence of these aspects, it is needed to take into account the

possible alternative techniques for the analysis purpose. According to the norm of AASB

138/IAS 38, the R&D cost of the firms needs to be recognized in the firm’s income statement

as a portion of sank cost (Ji and Lu, 2014).

The company may create their internally generated intangible asset over a certain

period. In opposite to the process of acquisition or in the form of business combination, in

case a business acquire the same asset due to the result of business consolidation, it is needed

to shows the excess of the purchase consideration in the form of goodwill in the appropriate

accounting books. As per the norms of AASB 138/IAS 38, the value of acquisition is that

value that the company needs to consider and the company is needed to review the same on

periodical basis in order to get the indication of impairment (Hu, Percy and Yao, 2015).

Research Cost – According to AASB 138/IAS 38, Paragraph 8, the companies are needed to

undertake the planned and original investigation with the aim to gain effective scientific as

well as technical knowledge for the purpose of better research. In case of Technology

Enterprise Ltd, the cost that the company has incurred is in line with the standards of AASB

138/IAS 38 whereby the cost incurred for the purpose to increase the batteries’ economic life

since it is beneficial for the firm to generate cash flows for the period of ten years. The firm

considered research for the best as well as alternative model in the beginning of the years and

the same was in line with the proper accounting standards (Yao, Percy and Hu, 2015). The

company should consider $1,000,000 as the expenses since this amount is associated with the

development of the design.

Asset Development – According to AASB 138/IAS 38, an asset is developed at the

completion of the research phase of the project and the project outlay is in the form of the

developed asset. In this process, the firm can recognize the asset after proving the technical

feasibility of the asset and the company gain the ability to use as well as sale the same asset

in most significant manner (Bugeja and Loyeung, 2015). Another crucial aspect is the

identification of correct accounting standards in order to identify the value of assets in the

balance sheet when the technical feasibility of the same asset is also proved. As per the

provided information, Technology Enterprise Ltd has incurred significant research cost for

the development of the asset. After conducting the feasibility analysis, the firm has made the

estimation that the project will create a value of $4,000,000 for them (Yao, Percy and Hu,

2013).

5FINANCIAL ACCOUNTING

2. Reduction of Comparability of Financial Statements

Comparability is considered as a crucial characteristic of financial statements. The

accounting standards and policies adopted by the company reflect the comparability feature

of financial statements. Under the Australian Accounting Standards Board (AASB), the

applicability of both the processes can be seen which are the acquisition of intangible assets

through business combination and measurement of goodwill at cost value (Francis, Pinnuck

and Watanabe, 2013). Earlier discussion states that the intangible assets can be identified and

non-monetary in existence nature that lacks physical incidence. Thus, the recognition of these

kinds of assets varies company to company based on the benefits that these companies expect

to receive from these assets and these companies are needed to recognize these benefits in the

form of assets. In addition, the company needs to classify the relevant expenses incurred

related to these assets as expenses (Wang, 2014).

According to AASB 138/IAS 38, the profit of the asset needs to be recognized on

similar basis in case the company acquires the intangible asset as a portion of a different

asset. For this reason, the company is needed to follow the accounting policies of AASB

138/IAS 38 for recognizing these assets and the company is needed to capitalize the costs

incurred for the research and development of the assets (Kim et al. 2016). One essential

aspect is that that there is the presence of comparability feature in the company’s financial

statements in case of the intangible assets. This particular feature of the financial statements

needs to be such that it provides the users with the scope to compare the financial information

of this company with other company or the different timeline of the same company. In this

aspect, it needs to be mentioned that in case valuation, recognition and measurement of

intangible assets of the company majorly differs with the same aspects of other companies,

there can be material impact on the financial statements of the company. This can create

major impact on the financial decision-making process of the users of the financial statements

(Kim, Kraft and Ryan, 2013).

According to the regulation of AASB 138/IAS 38 related to intangible assets, the

companies are needed to comply with different kinds of rules and regulations for the correct

accounting treatment of different expenses and developments (Chen et al. 2018). It is needed

for the company to consider the cost incurred for the research of any product or the

development of the same as sunk cost. Further, the company is needed to consider this as an

expense in the income statement of the company instead of capitalizing the same. According

to the rules of classification, recognition and measurement, the companies are needed to

consider these expenses and to record them in the correct accounting book (Chen et al. 2018).

3. Understanding of AASB 138/IAS 38

AASB 138/IAS 38 is considered as a crucial document published by the AASB for

the ASX listed companies that provides these companies with the required standards as well

as accounting policies for the correct accounting treatment of intangible assets and other

aspects related to these assets (aasb.gov.au, 2019). The accounting policy of AASB 138/IAS

38 indicates towards the crucial fact that intangible assets are identifiable as well as non-

monetary assets which do not have any physical existence (Cheung and Lau, 2016).

According to the same accounting standard, the asset identified as the intangible asset must

be divisible from the firm in such a manner that they can be sold or exchanged in the market.

The definition of monetary and non-monetary assets of the companies can be obtained from

AASB 138/IAS 38. As per AASB 138/IAS 38, business organizations can acquire the

intangible assets from the result of business combination and they can also internally generate

these intangible assets that is called goodwill (Jin, Shan and Taylor, 2015). The value of these

kinds of assets on the basis of the assets created reflects from the regulations of AASB

2. Reduction of Comparability of Financial Statements

Comparability is considered as a crucial characteristic of financial statements. The

accounting standards and policies adopted by the company reflect the comparability feature

of financial statements. Under the Australian Accounting Standards Board (AASB), the

applicability of both the processes can be seen which are the acquisition of intangible assets

through business combination and measurement of goodwill at cost value (Francis, Pinnuck

and Watanabe, 2013). Earlier discussion states that the intangible assets can be identified and

non-monetary in existence nature that lacks physical incidence. Thus, the recognition of these

kinds of assets varies company to company based on the benefits that these companies expect

to receive from these assets and these companies are needed to recognize these benefits in the

form of assets. In addition, the company needs to classify the relevant expenses incurred

related to these assets as expenses (Wang, 2014).

According to AASB 138/IAS 38, the profit of the asset needs to be recognized on

similar basis in case the company acquires the intangible asset as a portion of a different

asset. For this reason, the company is needed to follow the accounting policies of AASB

138/IAS 38 for recognizing these assets and the company is needed to capitalize the costs

incurred for the research and development of the assets (Kim et al. 2016). One essential

aspect is that that there is the presence of comparability feature in the company’s financial

statements in case of the intangible assets. This particular feature of the financial statements

needs to be such that it provides the users with the scope to compare the financial information

of this company with other company or the different timeline of the same company. In this

aspect, it needs to be mentioned that in case valuation, recognition and measurement of

intangible assets of the company majorly differs with the same aspects of other companies,

there can be material impact on the financial statements of the company. This can create

major impact on the financial decision-making process of the users of the financial statements

(Kim, Kraft and Ryan, 2013).

According to the regulation of AASB 138/IAS 38 related to intangible assets, the

companies are needed to comply with different kinds of rules and regulations for the correct

accounting treatment of different expenses and developments (Chen et al. 2018). It is needed

for the company to consider the cost incurred for the research of any product or the

development of the same as sunk cost. Further, the company is needed to consider this as an

expense in the income statement of the company instead of capitalizing the same. According

to the rules of classification, recognition and measurement, the companies are needed to

consider these expenses and to record them in the correct accounting book (Chen et al. 2018).

3. Understanding of AASB 138/IAS 38

AASB 138/IAS 38 is considered as a crucial document published by the AASB for

the ASX listed companies that provides these companies with the required standards as well

as accounting policies for the correct accounting treatment of intangible assets and other

aspects related to these assets (aasb.gov.au, 2019). The accounting policy of AASB 138/IAS

38 indicates towards the crucial fact that intangible assets are identifiable as well as non-

monetary assets which do not have any physical existence (Cheung and Lau, 2016).

According to the same accounting standard, the asset identified as the intangible asset must

be divisible from the firm in such a manner that they can be sold or exchanged in the market.

The definition of monetary and non-monetary assets of the companies can be obtained from

AASB 138/IAS 38. As per AASB 138/IAS 38, business organizations can acquire the

intangible assets from the result of business combination and they can also internally generate

these intangible assets that is called goodwill (Jin, Shan and Taylor, 2015). The value of these

kinds of assets on the basis of the assets created reflects from the regulations of AASB

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING

138/IAS 38. The regulations of AASB 138/IAS 38 states that the companies are needed to

measure the intangible assets at cost initially whereby the company is needed to report the

internally generated intangible assets at the cost value. The companies can recognize the

value of these assets at the time of the presence of the probability that the future economic

benefit associated with these assets will flow to the company and it is possible to measure the

cost value of these assets reliably. AASB 138/IAS 38 also indicates towards the aspects that it

is needed for the business organizations to prove the technical feasibility of these assets

before the identification of the value of these assets in the balance sheet of the company

(Hodgson and Russell, 2014).

Conclusion and Recommendation

As per the standards of financial reporting, accounting policies and financial reporting

regulations, it is utmost important for the companies to report the values of the assets and

liabilities in accordance with the proper accounting standards. Technology Enterprise Ltd has

the option to reduce the concerns of the investors by ensuring certain disclosures related to

certain financial aspects where the company will be responsible for disclosing the valuation

of the assets on a regular interval. The company is needed to make the valuation and

estimation of the financial assets through the estimation of the financial viability of the assets

as done by Technology Enterprise Ltd since they have determined the value of the assets

through the assessment of the financial viability of the same assets. For this, it is needed for

the company to mandate certain rules and regulations in the form of disclosure and

compliance regarding the financial assets. These financial disclosures about the financial

assets play crucial role in the interpretation of the financial information regarding the assets

and liabilities. The same aspect needs to be followed in case of the flow of the economic

benefits since the company needs to ensure that there the flow of economic benefit comes

towards them.

138/IAS 38. The regulations of AASB 138/IAS 38 states that the companies are needed to

measure the intangible assets at cost initially whereby the company is needed to report the

internally generated intangible assets at the cost value. The companies can recognize the

value of these assets at the time of the presence of the probability that the future economic

benefit associated with these assets will flow to the company and it is possible to measure the

cost value of these assets reliably. AASB 138/IAS 38 also indicates towards the aspects that it

is needed for the business organizations to prove the technical feasibility of these assets

before the identification of the value of these assets in the balance sheet of the company

(Hodgson and Russell, 2014).

Conclusion and Recommendation

As per the standards of financial reporting, accounting policies and financial reporting

regulations, it is utmost important for the companies to report the values of the assets and

liabilities in accordance with the proper accounting standards. Technology Enterprise Ltd has

the option to reduce the concerns of the investors by ensuring certain disclosures related to

certain financial aspects where the company will be responsible for disclosing the valuation

of the assets on a regular interval. The company is needed to make the valuation and

estimation of the financial assets through the estimation of the financial viability of the assets

as done by Technology Enterprise Ltd since they have determined the value of the assets

through the assessment of the financial viability of the same assets. For this, it is needed for

the company to mandate certain rules and regulations in the form of disclosure and

compliance regarding the financial assets. These financial disclosures about the financial

assets play crucial role in the interpretation of the financial information regarding the assets

and liabilities. The same aspect needs to be followed in case of the flow of the economic

benefits since the company needs to ensure that there the flow of economic benefit comes

towards them.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

References

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf

[Accessed 7 May 2019].

Bugeja, M. and Loyeung, A., 2015. What drives the allocation of the purchase price to

goodwill?. Journal of Contemporary Accounting & Economics, 11(3), pp.245-261.

Chen, C.W., Collins, D.W., Kravet, T.D. and Mergenthaler, R.D., 2018. Financial statement

comparability and the efficiency of acquisition decisions. Contemporary Accounting

Research, 35(1), pp.164-202.

Cheung, E. and Lau, J., 2016. Readability of Notes to the Financial Statements and the

Adoption of IFRS. Australian Accounting Review, 26(2), pp.162-176.

Francis, J.R., Pinnuck, M.L. and Watanabe, O., 2013. Auditor style and financial statement

comparability. The Accounting Review, 89(2), pp.605-633.

Ho Kim, S. and Taylor, D., 2014. Intellectual capital vs the book-value of assets: A value-

relevance comparison based on productivity measures. Journal of Intellectual Capital, 15(1),

pp.65-82.

Hodgson, A. and Russell, M., 2014. Comprehending comprehensive income. Australian

Accounting Review, 24(2), pp.100-110.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Iasplus.com. 2019. IAS 38 — Intangible Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias38 [Accessed 7 May 2019].

Ji, X.D. and Lu, W., 2014. The value relevance and reliability of intangible assets: Evidence

from Australia before and after adopting IFRS. Asian Review of Accounting, 22(3), pp.182-

216.

Jin, K., Shan, Y. and Taylor, S., 2015. Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

pp.90-107.

Kim, J.B., Li, L., Lu, L.Y. and Yu, Y., 2016. Financial statement comparability and expected

crash risk. Journal of Accounting and Economics, 61(2-3), pp.294-312.

Kim, S., Kraft, P. and Ryan, S.G., 2013. Financial statement comparability and credit

risk. Review of Accounting Studies, 18(3), pp.783-823.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Yao, D.F., Percy, M. and Hu, F., 2013. Fair values and audit fees: Evidence from asset

revaluations in Australia.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

References

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf

[Accessed 7 May 2019].

Bugeja, M. and Loyeung, A., 2015. What drives the allocation of the purchase price to

goodwill?. Journal of Contemporary Accounting & Economics, 11(3), pp.245-261.

Chen, C.W., Collins, D.W., Kravet, T.D. and Mergenthaler, R.D., 2018. Financial statement

comparability and the efficiency of acquisition decisions. Contemporary Accounting

Research, 35(1), pp.164-202.

Cheung, E. and Lau, J., 2016. Readability of Notes to the Financial Statements and the

Adoption of IFRS. Australian Accounting Review, 26(2), pp.162-176.

Francis, J.R., Pinnuck, M.L. and Watanabe, O., 2013. Auditor style and financial statement

comparability. The Accounting Review, 89(2), pp.605-633.

Ho Kim, S. and Taylor, D., 2014. Intellectual capital vs the book-value of assets: A value-

relevance comparison based on productivity measures. Journal of Intellectual Capital, 15(1),

pp.65-82.

Hodgson, A. and Russell, M., 2014. Comprehending comprehensive income. Australian

Accounting Review, 24(2), pp.100-110.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Iasplus.com. 2019. IAS 38 — Intangible Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias38 [Accessed 7 May 2019].

Ji, X.D. and Lu, W., 2014. The value relevance and reliability of intangible assets: Evidence

from Australia before and after adopting IFRS. Asian Review of Accounting, 22(3), pp.182-

216.

Jin, K., Shan, Y. and Taylor, S., 2015. Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

pp.90-107.

Kim, J.B., Li, L., Lu, L.Y. and Yu, Y., 2016. Financial statement comparability and expected

crash risk. Journal of Accounting and Economics, 61(2-3), pp.294-312.

Kim, S., Kraft, P. and Ryan, S.G., 2013. Financial statement comparability and credit

risk. Review of Accounting Studies, 18(3), pp.783-823.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Yao, D.F., Percy, M. and Hu, F., 2013. Fair values and audit fees: Evidence from asset

revaluations in Australia.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.