Financial Accounting Assignment 1: Revenue Recognition and Taxation

VerifiedAdded on 2023/06/08

|15

|3401

|173

Homework Assignment

AI Summary

This financial accounting assignment explores the impact of the new revenue recognition standard (AASB 15) replacing the old standards (AASB 8 and AASB 11) and its implications for financial reporting. It analyzes the shortcomings of the old standard and how the new standard addresses them, along with a five-step procedure for revenue recognition. The assignment includes case studies of two Australian companies, Telstra Limited and Wesfarmers Limited, examining how their accounting practices would be affected by the new standard. The solution further addresses the treatment of current and deferred taxation, with journal entries for provision for annual leave and accounts receivable. The assignment provides a detailed analysis of financial accounting principles and their practical applications.

FINANCIAL

ACCOUNTING

ASSIGNMENT

ACCOUNTING

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

A report has been prepared to discuss on the effect of the replacement of old revenue recognition

standard with the new revenue recognition standard. The new standard AASB 15 replaces the old

ones being AASB 8 and AASB 11 (that on the construction contract). The report highlights the

major shortcomings of the old standard, which is being replaced, by the new standard and two

listed Australian companies, which would be affected due to these changes. The changes in

reporting and accounting has also been captured in the report. The second question given in the

assignment has been solved to show the treatment of the current as well as deferred taxation.

Finally, requisite journal entry has been passed and discussion on accounting treatment of

provision for annual leave and accounts receivable has been made.

2 | P a g e

Executive Summary

A report has been prepared to discuss on the effect of the replacement of old revenue recognition

standard with the new revenue recognition standard. The new standard AASB 15 replaces the old

ones being AASB 8 and AASB 11 (that on the construction contract). The report highlights the

major shortcomings of the old standard, which is being replaced, by the new standard and two

listed Australian companies, which would be affected due to these changes. The changes in

reporting and accounting has also been captured in the report. The second question given in the

assignment has been solved to show the treatment of the current as well as deferred taxation.

Finally, requisite journal entry has been passed and discussion on accounting treatment of

provision for annual leave and accounts receivable has been made.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Question 1 (a)..............................................................................................................................................4

Question 1 (b)..............................................................................................................................................6

Question 2 (a)..............................................................................................................................................9

Question 2 (b)............................................................................................................................................11

Question 2 (c)............................................................................................................................................12

Question 2 (d)............................................................................................................................................12

References.................................................................................................................................................13

3 | P a g e

Contents

Question 1 (a)..............................................................................................................................................4

Question 1 (b)..............................................................................................................................................6

Question 2 (a)..............................................................................................................................................9

Question 2 (b)............................................................................................................................................11

Question 2 (c)............................................................................................................................................12

Question 2 (d)............................................................................................................................................12

References.................................................................................................................................................13

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Question 1 (a)

When the new revenue recognition standard is being implemented, the same be complex as well

as challenging to reciprocate in the existing affairs of the business. It can drastically change the

way in which the financial reporting is being done. This new standard would be effective from 1st

January 2018 for the profit making entities and from 01st January 2019 for the non-profit

organizations (Belton, 2017). The new standard is very integrated as well as very comprehensive

and sets up a five-step procedure in order to recognise revenue in the books of accounts. There

steps have been described below in brief:

1. Identification of the contract from the customer, which can be in written form, oral, or

verbal or even implied. All the terms and conditions would be clearly stated in the

contract.

2. The second step in the process is the identification of the performance to be done in

respect of the contract. The same can be in the form of the delivery of goods or the

provision of services or both of these. These may again be divided into a number of sub

parts or different components of goods delivery or services levels within a given period.

3. The 3rd step in the process is the determination of the transaction prices. For this, several

aspects are taken into consideration like the discount, refund, bonus, concession, etc.

Once the entire final contract price has been determined, it also needs to be seen that

what will be the scenario in case of escalation in prices (Alexander, 2016).

4. The fourth step in the process is the allocation of the transaction price to the different

components of the contract. This needs various estimates, assumptions and supporting in

terms of cost incurred on each component.

5. The fifth and the last step as per the new revenue standard is recognition of the revenue in

the books when the Performance is completed (Dichev, 2017).

Besides this, there are a number of shortcomings in the old standard, which the new standard

purports to resolve.

1. Uniformity and comparable status: Before the new standard, several guidance’s processes

and standards were being used for revenue recognition in different countries. This led

financial statements to be incomparable and thus missing one of the qualitative

4 | P a g e

Question 1 (a)

When the new revenue recognition standard is being implemented, the same be complex as well

as challenging to reciprocate in the existing affairs of the business. It can drastically change the

way in which the financial reporting is being done. This new standard would be effective from 1st

January 2018 for the profit making entities and from 01st January 2019 for the non-profit

organizations (Belton, 2017). The new standard is very integrated as well as very comprehensive

and sets up a five-step procedure in order to recognise revenue in the books of accounts. There

steps have been described below in brief:

1. Identification of the contract from the customer, which can be in written form, oral, or

verbal or even implied. All the terms and conditions would be clearly stated in the

contract.

2. The second step in the process is the identification of the performance to be done in

respect of the contract. The same can be in the form of the delivery of goods or the

provision of services or both of these. These may again be divided into a number of sub

parts or different components of goods delivery or services levels within a given period.

3. The 3rd step in the process is the determination of the transaction prices. For this, several

aspects are taken into consideration like the discount, refund, bonus, concession, etc.

Once the entire final contract price has been determined, it also needs to be seen that

what will be the scenario in case of escalation in prices (Alexander, 2016).

4. The fourth step in the process is the allocation of the transaction price to the different

components of the contract. This needs various estimates, assumptions and supporting in

terms of cost incurred on each component.

5. The fifth and the last step as per the new revenue standard is recognition of the revenue in

the books when the Performance is completed (Dichev, 2017).

Besides this, there are a number of shortcomings in the old standard, which the new standard

purports to resolve.

1. Uniformity and comparable status: Before the new standard, several guidance’s processes

and standards were being used for revenue recognition in different countries. This led

financial statements to be incomparable and thus missing one of the qualitative

4 | P a g e

5

characteristics of conceptual framework. However, AASB 15 proposes to remove all

these inconsistencies and giving flexibility in the hands of the auditors and accountants

while preparation and presentation of financial statements.

2. Disclosure requirements: The new revenue standard warrants for more detailed disclosure

in respect of revenue line item, which is shown just as a single line item in the profit and

loss account. This will help the user of the financial statement in understanding the

nature, extent and timing of the revenues recorded and if at all there is any uncertainty in

the collection of revenues. It will also help the user in understanding the estimates,

judgements of management and what are the terms of major contracts (Choy, 2018).

3. Focus shift from income statement to the balance sheet: The previous standard on

revenue used to focus only on the income statement aspect for recognizing revenue in

books, as if the same should have been realized, realizable as well as earned. The new

standard does away with this rule and focuses on whether the goods and services, which

were promised to the customer, have been delivered or rendered and whether the entity

expects to receive payment in respect of that. The new standard will require the

companies to move the asset out of the books and the pay off the liabilities in order to

recognize revenue.

In addition to the above-mentioned points, it can be said that the new standards are

fundamentally balanced and do away with the inherent deficiencies in the old standard. The old

standard measured the revenue at the fair value whereas the new standard recognizes the revenue

based on assets and liabilities approach. Even though the contractual; delivery of the goods has

happened or not, irrespective of the same, the revenue can be booked in the P&L under the new

standard if the net assets have increased. Few of the advantages with new standard are as

follows:

1. The old concept was based on the principle of prudence whereas the new concept is

based on neutrality concept and hence it will help the company to show the true and

fair view of the books of accounts (Das, 2017).

2. The new standard also does away with the concept of deferred revenue, which is

against the definition of liability.

5 | P a g e

characteristics of conceptual framework. However, AASB 15 proposes to remove all

these inconsistencies and giving flexibility in the hands of the auditors and accountants

while preparation and presentation of financial statements.

2. Disclosure requirements: The new revenue standard warrants for more detailed disclosure

in respect of revenue line item, which is shown just as a single line item in the profit and

loss account. This will help the user of the financial statement in understanding the

nature, extent and timing of the revenues recorded and if at all there is any uncertainty in

the collection of revenues. It will also help the user in understanding the estimates,

judgements of management and what are the terms of major contracts (Choy, 2018).

3. Focus shift from income statement to the balance sheet: The previous standard on

revenue used to focus only on the income statement aspect for recognizing revenue in

books, as if the same should have been realized, realizable as well as earned. The new

standard does away with this rule and focuses on whether the goods and services, which

were promised to the customer, have been delivered or rendered and whether the entity

expects to receive payment in respect of that. The new standard will require the

companies to move the asset out of the books and the pay off the liabilities in order to

recognize revenue.

In addition to the above-mentioned points, it can be said that the new standards are

fundamentally balanced and do away with the inherent deficiencies in the old standard. The old

standard measured the revenue at the fair value whereas the new standard recognizes the revenue

based on assets and liabilities approach. Even though the contractual; delivery of the goods has

happened or not, irrespective of the same, the revenue can be booked in the P&L under the new

standard if the net assets have increased. Few of the advantages with new standard are as

follows:

1. The old concept was based on the principle of prudence whereas the new concept is

based on neutrality concept and hence it will help the company to show the true and

fair view of the books of accounts (Das, 2017).

2. The new standard also does away with the concept of deferred revenue, which is

against the definition of liability.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

3. This development will also eliminate the different approaches being used by the

accountants in revenue accounting based on industry. This will ensure uniformity and

comparability of financials throughout the world (Trieu, 2017).

Thus, the new standard overcomes all the inefficiencies being posed by the old standard.

Question 1 (b)

For analysing the impact of new revenue accounting standard on the Australian companies, two

companies have been chosen, both listed on the Australian Stock Exchange. The companies are

namely Telstra Limited and Wesfarmers Limited. Telstra is the largest telecommunication

company in Australia serving millions of customers and engaged in construction, operation and

maintenance of the telecommunication networks including broadband services, mobile, internet,

voice media and several other services. Out of the many impacts due to the introduction of the

new revenue recognition standard, some of the major impacts are listed below:

1. The long term contracts which were usually bundled under the old standard can no more

be bundled and have to be separated between the hardware and services component

upfront while entering into the contract and the revenue on account of each component

would also be divided and fixed upfront so that there is no ambiguity later on (Saeidi,

2012).

2. In the earlier standard, discount was given to the customers in case of the bundled

contracts but now the same will be required to be allocated or apportioned in between the

services and goods going forward.

3. Earlier revenue standard allowed for deferred payment terms in the contract but as per the

new standard, the finance portion in the contract will be required to be separated using an

appropriate discounting factor and the basis of the calculation would need to be disclosed.

4. Furthermore, in case of telecommunication industry like Telstra, the treatment of few

types of costs like the activation costs, customer acquisition cost and the contract

fulfilment cost may change in greater proportion (Raiborn, et al., 2016).

5. At present, in the telecommunication industries, concept of residual method is being

followed but with the elimination of concept of “contingent revenue cap” under the new

6 | P a g e

3. This development will also eliminate the different approaches being used by the

accountants in revenue accounting based on industry. This will ensure uniformity and

comparability of financials throughout the world (Trieu, 2017).

Thus, the new standard overcomes all the inefficiencies being posed by the old standard.

Question 1 (b)

For analysing the impact of new revenue accounting standard on the Australian companies, two

companies have been chosen, both listed on the Australian Stock Exchange. The companies are

namely Telstra Limited and Wesfarmers Limited. Telstra is the largest telecommunication

company in Australia serving millions of customers and engaged in construction, operation and

maintenance of the telecommunication networks including broadband services, mobile, internet,

voice media and several other services. Out of the many impacts due to the introduction of the

new revenue recognition standard, some of the major impacts are listed below:

1. The long term contracts which were usually bundled under the old standard can no more

be bundled and have to be separated between the hardware and services component

upfront while entering into the contract and the revenue on account of each component

would also be divided and fixed upfront so that there is no ambiguity later on (Saeidi,

2012).

2. In the earlier standard, discount was given to the customers in case of the bundled

contracts but now the same will be required to be allocated or apportioned in between the

services and goods going forward.

3. Earlier revenue standard allowed for deferred payment terms in the contract but as per the

new standard, the finance portion in the contract will be required to be separated using an

appropriate discounting factor and the basis of the calculation would need to be disclosed.

4. Furthermore, in case of telecommunication industry like Telstra, the treatment of few

types of costs like the activation costs, customer acquisition cost and the contract

fulfilment cost may change in greater proportion (Raiborn, et al., 2016).

5. At present, in the telecommunication industries, concept of residual method is being

followed but with the elimination of concept of “contingent revenue cap” under the new

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

standard, additional revenue will be required to be allocated to products which are being

sold at discounted prices or free of cost.

6. The new set of standards are not only applicable on the new contracts but also on the

existing contracts and portfolio of performance obligations, thus this is bound to increase

the complexities in accounting and reporting for a while. In addition, since the restated

number s would also be required to be reported, it will increase the workload as else the

data would be incomparable with the last year.

7. The goods and services, which were earlier being offered as free samples, gifts etc. will

now be required to be reported as distinct goods and services.

8. It can be seen that the telecommunication companies offer a number of services through a

single contract like usage of, access to, data and other network facilities like data, media,

internet, etc. Under the new rules, the classification would be required to be made under

the different heads and it can be complex task (Kuhn & Morris, 2016).

The second company, which has been selected, is Wesfarmers Limited, which is the largest

conglomerate in Australia. It is the largest Australian company in terms of revenue as well as

employability and deals in products like chemicals, fertilizers, and mining business. It majorly

operates in New Zealand and Australia and has presence in several other countries. As per the

past annual report of the company, it has been disclosing the revenue recognition process and the

assumptions with regard to the same but with the introduction of new revenue recognition

standard, there will be several changes mentioned below:

1. There will be separate disclosures in few aspects in the annual report like the estimates,

judgements and assumptions with respect to unbilled revenue, customer acquisition cost

like the upfront fees and sales commission now need to be separately disclosed.

2. Since in the mining industry, there can be different stages of development of mine and

the production stage, this might have an impact in the form of different performance

obligations and therefore the revenue may be recognised at different times, which can be

either deferred or even accelerated.

3. Reversals and claims have an impact of reducing the revenue; therefore, going forward,

the revenue will be recognised in the books only when it is certain that the reversal will

not happen (Werner, 2017).

7 | P a g e

standard, additional revenue will be required to be allocated to products which are being

sold at discounted prices or free of cost.

6. The new set of standards are not only applicable on the new contracts but also on the

existing contracts and portfolio of performance obligations, thus this is bound to increase

the complexities in accounting and reporting for a while. In addition, since the restated

number s would also be required to be reported, it will increase the workload as else the

data would be incomparable with the last year.

7. The goods and services, which were earlier being offered as free samples, gifts etc. will

now be required to be reported as distinct goods and services.

8. It can be seen that the telecommunication companies offer a number of services through a

single contract like usage of, access to, data and other network facilities like data, media,

internet, etc. Under the new rules, the classification would be required to be made under

the different heads and it can be complex task (Kuhn & Morris, 2016).

The second company, which has been selected, is Wesfarmers Limited, which is the largest

conglomerate in Australia. It is the largest Australian company in terms of revenue as well as

employability and deals in products like chemicals, fertilizers, and mining business. It majorly

operates in New Zealand and Australia and has presence in several other countries. As per the

past annual report of the company, it has been disclosing the revenue recognition process and the

assumptions with regard to the same but with the introduction of new revenue recognition

standard, there will be several changes mentioned below:

1. There will be separate disclosures in few aspects in the annual report like the estimates,

judgements and assumptions with respect to unbilled revenue, customer acquisition cost

like the upfront fees and sales commission now need to be separately disclosed.

2. Since in the mining industry, there can be different stages of development of mine and

the production stage, this might have an impact in the form of different performance

obligations and therefore the revenue may be recognised at different times, which can be

either deferred or even accelerated.

3. Reversals and claims have an impact of reducing the revenue; therefore, going forward,

the revenue will be recognised in the books only when it is certain that the reversal will

not happen (Werner, 2017).

7 | P a g e

8

4. Due to the underlining shipping term, the freight revenue may have to be deferred.

5. Due to the implementation of the new leasing standards, it is expected that the liabilities

of Wesfarmers to be doubled as now the operating leases will also be reported as

liabilities.

6. Furthermore, there are a number of costs, which are required for acquiring a contract or

fulfilling a given contract. Going forward, the same needs to be established by the

company that these costs belong to a given contract before reporting the same in financial

statements. These costs should be reported in the books if at all it is increasing the overall

resources of the company and is expected to be recovered back (Vieira, et al., 2017).

8 | P a g e

4. Due to the underlining shipping term, the freight revenue may have to be deferred.

5. Due to the implementation of the new leasing standards, it is expected that the liabilities

of Wesfarmers to be doubled as now the operating leases will also be reported as

liabilities.

6. Furthermore, there are a number of costs, which are required for acquiring a contract or

fulfilling a given contract. Going forward, the same needs to be established by the

company that these costs belong to a given contract before reporting the same in financial

statements. These costs should be reported in the books if at all it is increasing the overall

resources of the company and is expected to be recovered back (Vieira, et al., 2017).

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

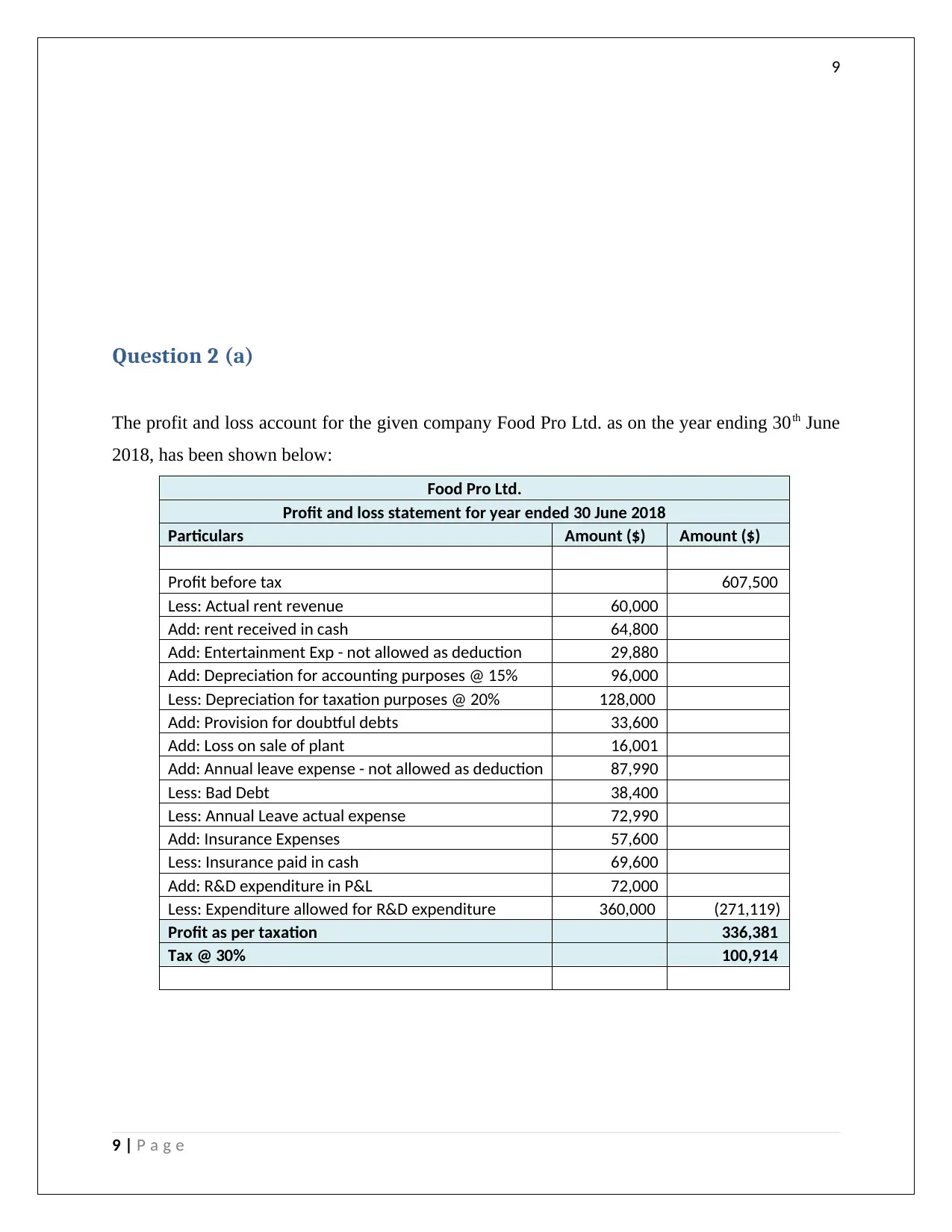

Question 2 (a)

The profit and loss account for the given company Food Pro Ltd. as on the year ending 30th June

2018, has been shown below:

Food Pro Ltd.

Profit and loss statement for year ended 30 June 2018

Particulars Amount ($) Amount ($)

Profit before tax 607,500

Less: Actual rent revenue 60,000

Add: rent received in cash 64,800

Add: Entertainment Exp - not allowed as deduction 29,880

Add: Depreciation for accounting purposes @ 15% 96,000

Less: Depreciation for taxation purposes @ 20% 128,000

Add: Provision for doubtful debts 33,600

Add: Loss on sale of plant 16,001

Add: Annual leave expense - not allowed as deduction 87,990

Less: Bad Debt 38,400

Less: Annual Leave actual expense 72,990

Add: Insurance Expenses 57,600

Less: Insurance paid in cash 69,600

Add: R&D expenditure in P&L 72,000

Less: Expenditure allowed for R&D expenditure 360,000 (271,119)

Profit as per taxation 336,381

Tax @ 30% 100,914

9 | P a g e

Question 2 (a)

The profit and loss account for the given company Food Pro Ltd. as on the year ending 30th June

2018, has been shown below:

Food Pro Ltd.

Profit and loss statement for year ended 30 June 2018

Particulars Amount ($) Amount ($)

Profit before tax 607,500

Less: Actual rent revenue 60,000

Add: rent received in cash 64,800

Add: Entertainment Exp - not allowed as deduction 29,880

Add: Depreciation for accounting purposes @ 15% 96,000

Less: Depreciation for taxation purposes @ 20% 128,000

Add: Provision for doubtful debts 33,600

Add: Loss on sale of plant 16,001

Add: Annual leave expense - not allowed as deduction 87,990

Less: Bad Debt 38,400

Less: Annual Leave actual expense 72,990

Add: Insurance Expenses 57,600

Less: Insurance paid in cash 69,600

Add: R&D expenditure in P&L 72,000

Less: Expenditure allowed for R&D expenditure 360,000 (271,119)

Profit as per taxation 336,381

Tax @ 30% 100,914

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

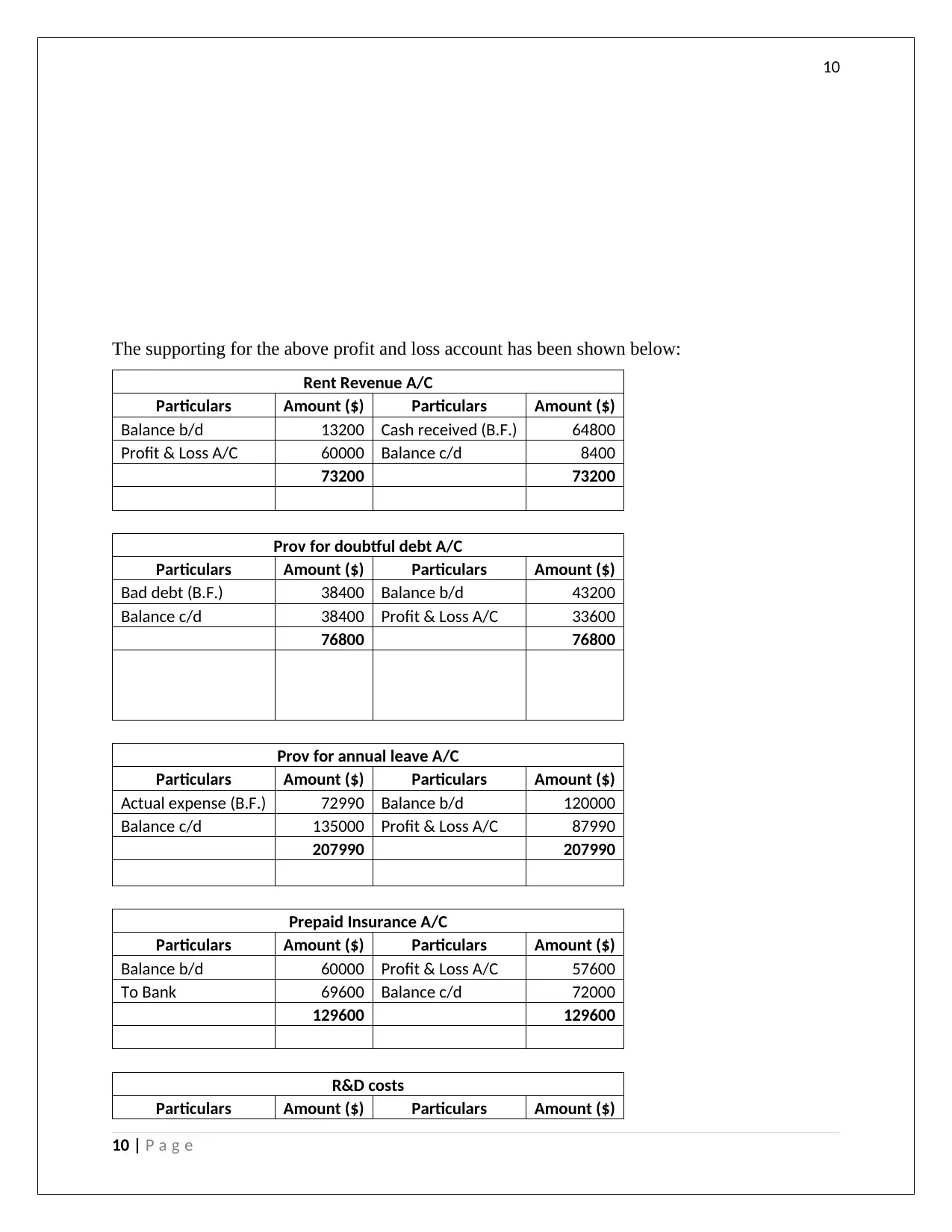

The supporting for the above profit and loss account has been shown below:

Rent Revenue A/C

Particulars Amount ($) Particulars Amount ($)

Balance b/d 13200 Cash received (B.F.) 64800

Profit & Loss A/C 60000 Balance c/d 8400

73200 73200

Prov for doubtful debt A/C

Particulars Amount ($) Particulars Amount ($)

Bad debt (B.F.) 38400 Balance b/d 43200

Balance c/d 38400 Profit & Loss A/C 33600

76800 76800

Prov for annual leave A/C

Particulars Amount ($) Particulars Amount ($)

Actual expense (B.F.) 72990 Balance b/d 120000

Balance c/d 135000 Profit & Loss A/C 87990

207990 207990

Prepaid Insurance A/C

Particulars Amount ($) Particulars Amount ($)

Balance b/d 60000 Profit & Loss A/C 57600

To Bank 69600 Balance c/d 72000

129600 129600

R&D costs

Particulars Amount ($) Particulars Amount ($)

10 | P a g e

The supporting for the above profit and loss account has been shown below:

Rent Revenue A/C

Particulars Amount ($) Particulars Amount ($)

Balance b/d 13200 Cash received (B.F.) 64800

Profit & Loss A/C 60000 Balance c/d 8400

73200 73200

Prov for doubtful debt A/C

Particulars Amount ($) Particulars Amount ($)

Bad debt (B.F.) 38400 Balance b/d 43200

Balance c/d 38400 Profit & Loss A/C 33600

76800 76800

Prov for annual leave A/C

Particulars Amount ($) Particulars Amount ($)

Actual expense (B.F.) 72990 Balance b/d 120000

Balance c/d 135000 Profit & Loss A/C 87990

207990 207990

Prepaid Insurance A/C

Particulars Amount ($) Particulars Amount ($)

Balance b/d 60000 Profit & Loss A/C 57600

To Bank 69600 Balance c/d 72000

129600 129600

R&D costs

Particulars Amount ($) Particulars Amount ($)

10 | P a g e

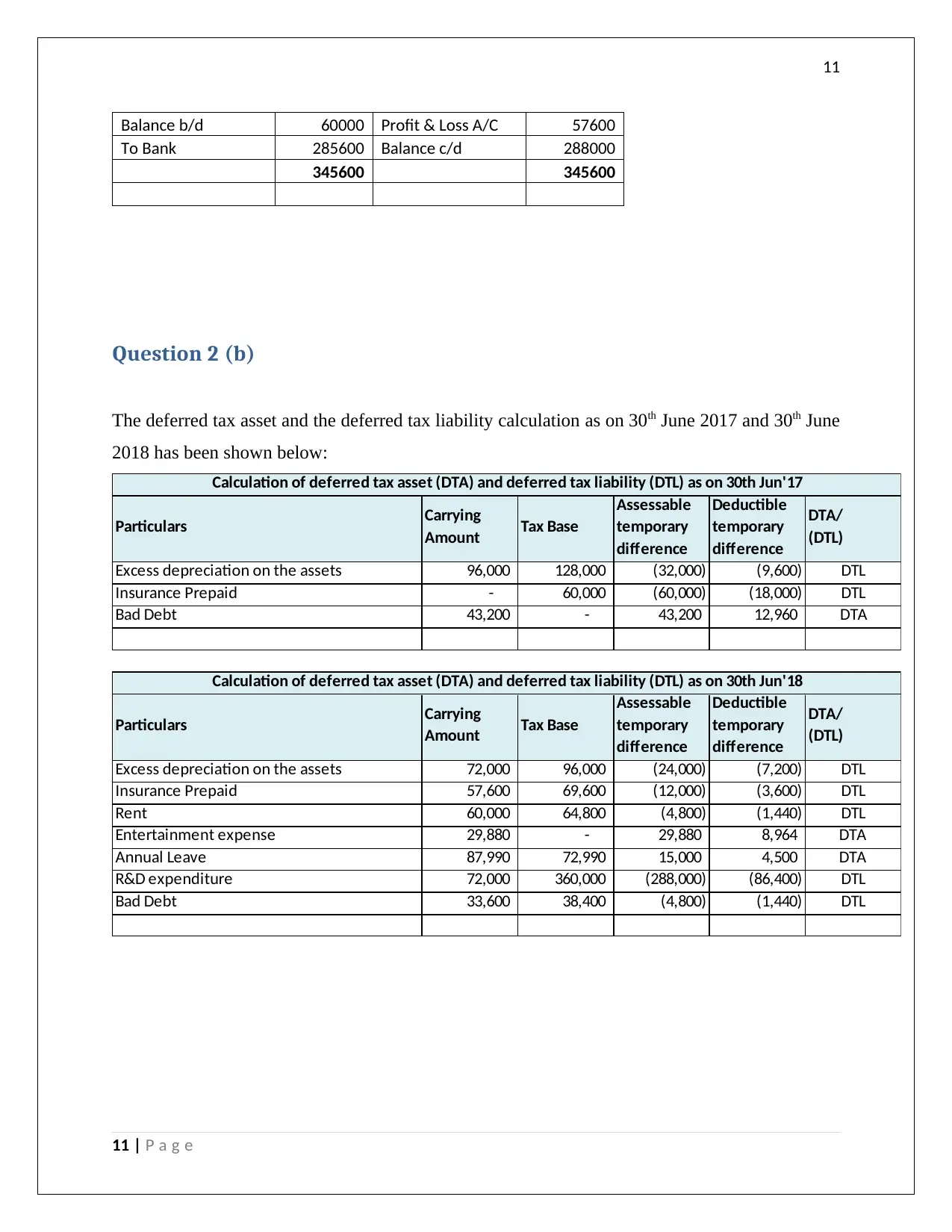

11

Balance b/d 60000 Profit & Loss A/C 57600

To Bank 285600 Balance c/d 288000

345600 345600

Question 2 (b)

The deferred tax asset and the deferred tax liability calculation as on 30th June 2017 and 30th June

2018 has been shown below:

Particulars Carrying

Amount Tax Base

Assessable

temporary

difference

Deductible

temporary

difference

DTA/

(DTL)

Excess depreciation on the assets 96,000 128,000 (32,000) (9,600) DTL

Insurance Prepaid - 60,000 (60,000) (18,000) DTL

Bad Debt 43,200 - 43,200 12,960 DTA

Particulars Carrying

Amount Tax Base

Assessable

temporary

difference

Deductible

temporary

difference

DTA/

(DTL)

Excess depreciation on the assets 72,000 96,000 (24,000) (7,200) DTL

Insurance Prepaid 57,600 69,600 (12,000) (3,600) DTL

Rent 60,000 64,800 (4,800) (1,440) DTL

Entertainment expense 29,880 - 29,880 8,964 DTA

Annual Leave 87,990 72,990 15,000 4,500 DTA

R&D expenditure 72,000 360,000 (288,000) (86,400) DTL

Bad Debt 33,600 38,400 (4,800) (1,440) DTL

Calculation of deferred tax asset (DTA) and deferred tax liability (DTL) as on 30th Jun'17

Calculation of deferred tax asset (DTA) and deferred tax liability (DTL) as on 30th Jun'18

11 | P a g e

Balance b/d 60000 Profit & Loss A/C 57600

To Bank 285600 Balance c/d 288000

345600 345600

Question 2 (b)

The deferred tax asset and the deferred tax liability calculation as on 30th June 2017 and 30th June

2018 has been shown below:

Particulars Carrying

Amount Tax Base

Assessable

temporary

difference

Deductible

temporary

difference

DTA/

(DTL)

Excess depreciation on the assets 96,000 128,000 (32,000) (9,600) DTL

Insurance Prepaid - 60,000 (60,000) (18,000) DTL

Bad Debt 43,200 - 43,200 12,960 DTA

Particulars Carrying

Amount Tax Base

Assessable

temporary

difference

Deductible

temporary

difference

DTA/

(DTL)

Excess depreciation on the assets 72,000 96,000 (24,000) (7,200) DTL

Insurance Prepaid 57,600 69,600 (12,000) (3,600) DTL

Rent 60,000 64,800 (4,800) (1,440) DTL

Entertainment expense 29,880 - 29,880 8,964 DTA

Annual Leave 87,990 72,990 15,000 4,500 DTA

R&D expenditure 72,000 360,000 (288,000) (86,400) DTL

Bad Debt 33,600 38,400 (4,800) (1,440) DTL

Calculation of deferred tax asset (DTA) and deferred tax liability (DTL) as on 30th Jun'17

Calculation of deferred tax asset (DTA) and deferred tax liability (DTL) as on 30th Jun'18

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.