University Assignment: Financial Accounting Processes, ACCT6003

VerifiedAdded on 2022/09/14

|11

|1243

|11

Homework Assignment

AI Summary

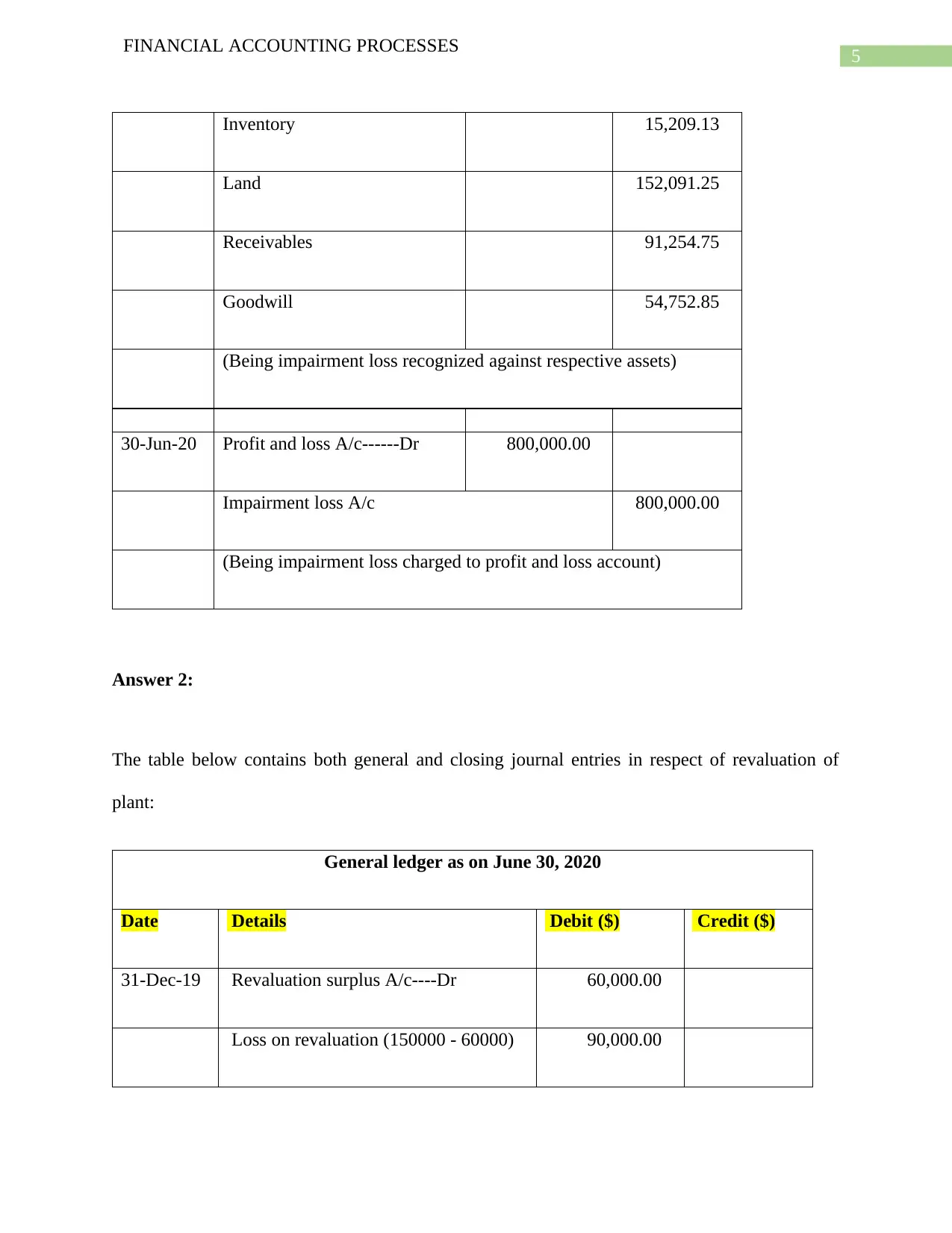

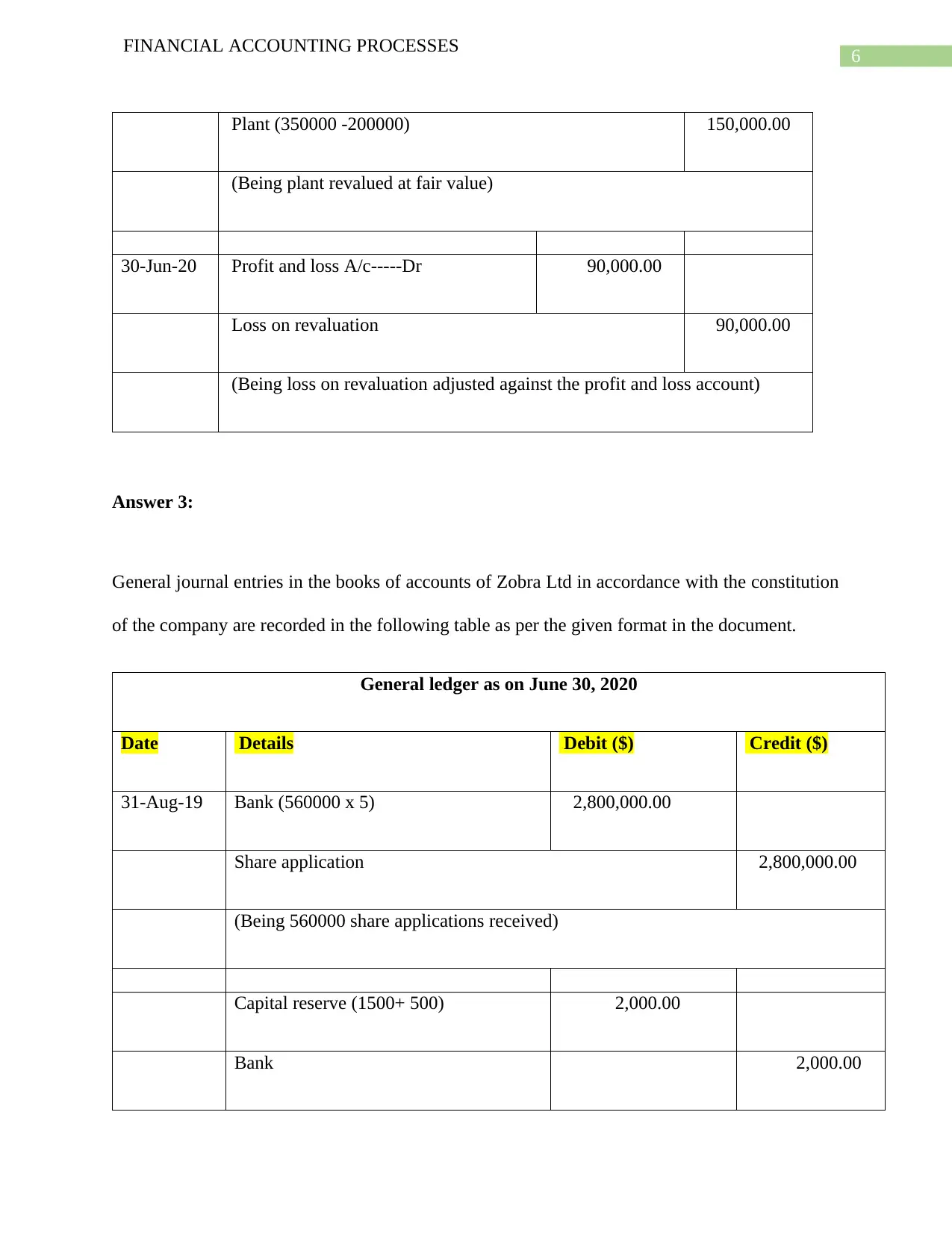

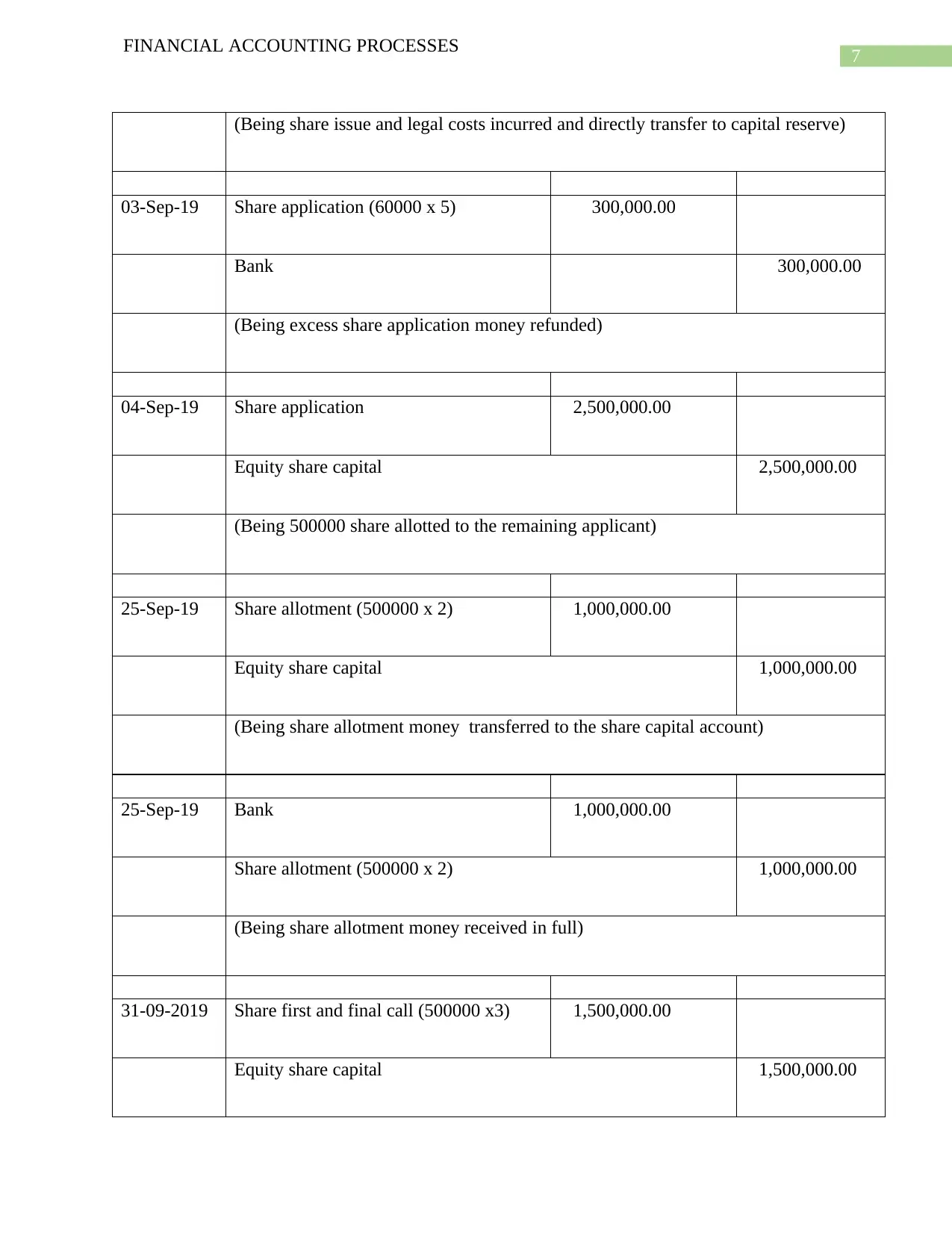

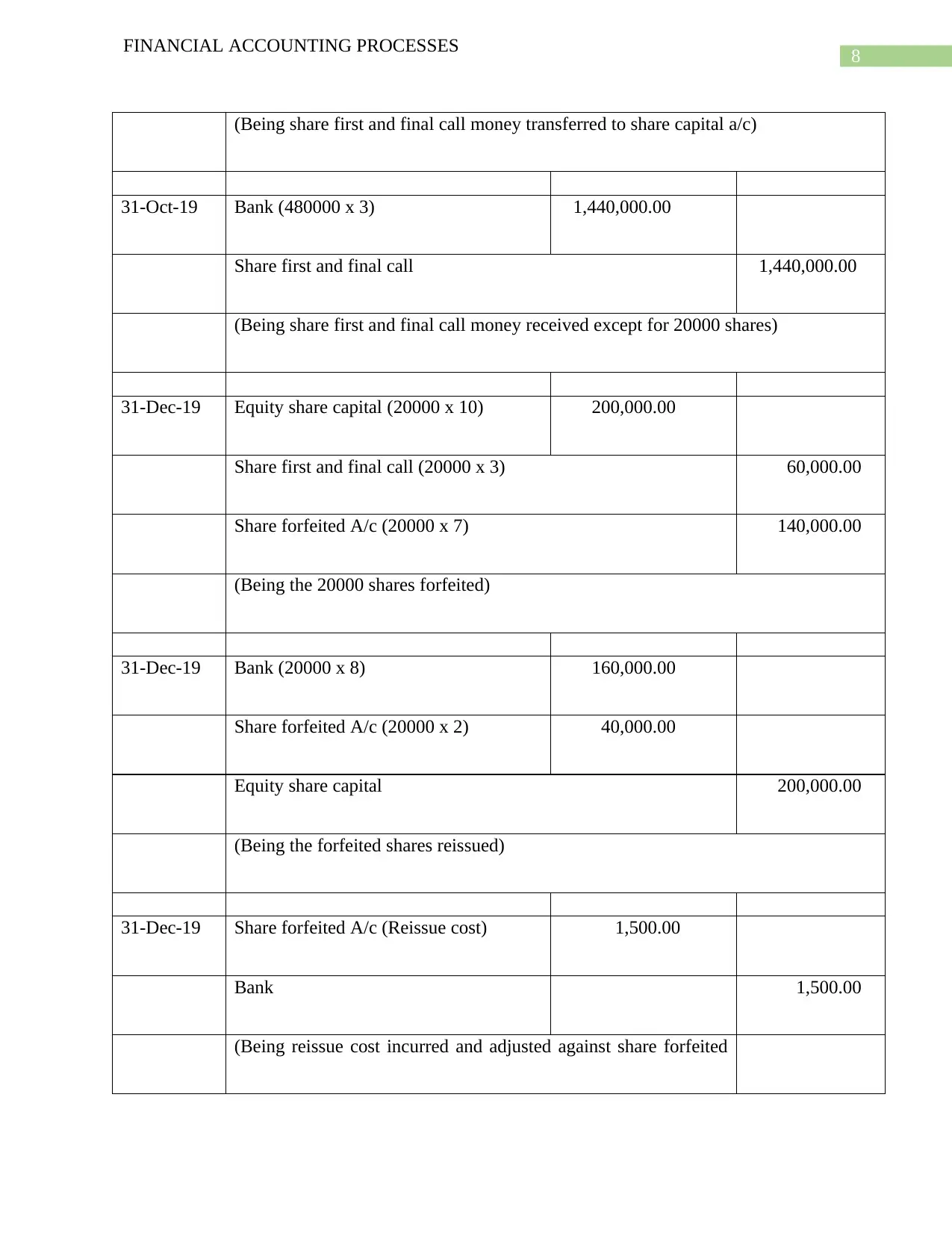

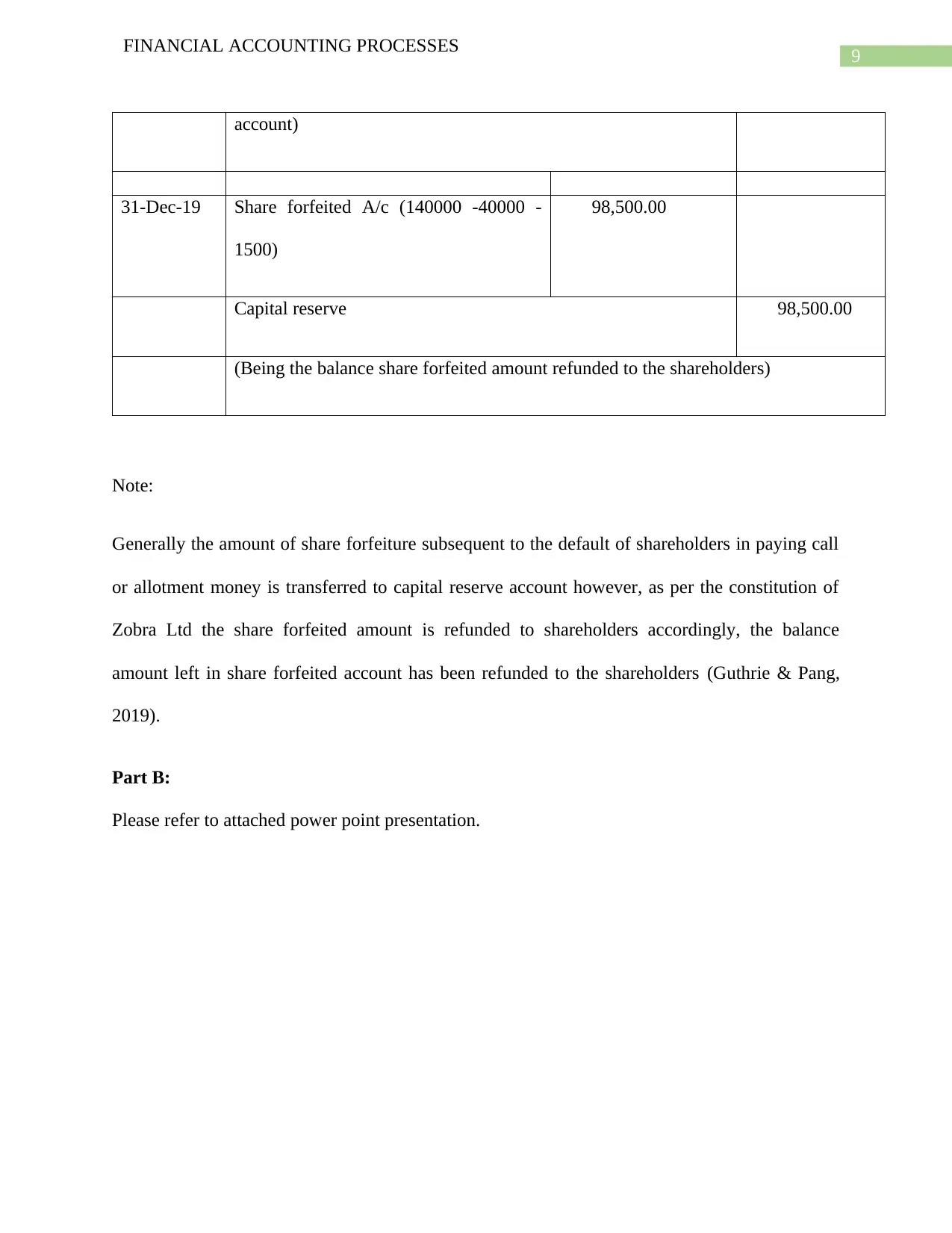

This assignment addresses key financial accounting processes, focusing on non-current assets, share transactions, and impairment. Part A provides detailed calculations and general journal entries for asset impairment, revaluation of plant, and share issuance, allotment, and forfeiture. The calculations include determining impairment loss, allocating the loss to individual assets, and preparing corresponding journal entries. The revaluation section includes general and closing journal entries for plant revaluation. The share transaction section covers journal entries for share applications, allotments, and calls, including the handling of forfeited shares and their subsequent reissue. Part B is a PowerPoint presentation which covers the topics in detail. The assignment demonstrates the application of accounting principles and standards, specifically AASB 136 for impairment and the accounting for equity transactions.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.