Financial Accounting Principles Report - Comprehensive Overview

VerifiedAdded on 2020/12/26

|26

|4145

|222

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles. It begins with an introduction to financial accounting and its purpose, followed by an exploration of accounting regulations, including those from IASB, FRC, and IFRS. The report then details the accounting rules and principles that govern financial statement preparation, such as the single entity concept, money measurement concept, and dual aspect concept. It also explains the concepts of consistency and material disclosure. Several client examples are analyzed to illustrate the application of these principles, covering topics like depreciation, bank reconciliation, control accounts, and suspense accounts. The report concludes by differentiating between suspense and clearing accounts and provides examples of depreciation methods. The report's aim is to provide a clear understanding of accounting principles, their application, and the importance of financial statements.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION..........................................................................................................................4

MAIN BODY.................................................................................................................................4

1.Financial accounting and its purpose..................................................................................4

2.The regulations of the Financial accounting.......................................................................5

3. The Accounting rules and principles that governs the presentation and preparation of the

financial statements................................................................................................................6

4. Explain the convention and concepts relating to consistency and material disclosure......7

CLIENT 1.......................................................................................................................................8

a..............................................................................................................................................8

b..............................................................................................................................................9

c............................................................................................................................................10

CLIENT 2.....................................................................................................................................11

a............................................................................................................................................11

b............................................................................................................................................11

CLIENT 3.....................................................................................................................................13

a............................................................................................................................................13

b............................................................................................................................................14

C. Explain the following concept, consistency and prudency..............................................14

CLIENT 4.....................................................................................................................................16

a. Explain the purpose of bank-reconciliation-statement and its importance.......................16

c............................................................................................................................................18

CLIENT 5.....................................................................................................................................20

a............................................................................................................................................20

B. Explain the term Control account and the need to prepare the account..........................21

CLIENT 6.....................................................................................................................................22

a. Explain the purpose of the suspense accounts..................................................................22

b............................................................................................................................................23

D. Differentiating between suspense account and clearing account....................................23

INTRODUCTION..........................................................................................................................4

MAIN BODY.................................................................................................................................4

1.Financial accounting and its purpose..................................................................................4

2.The regulations of the Financial accounting.......................................................................5

3. The Accounting rules and principles that governs the presentation and preparation of the

financial statements................................................................................................................6

4. Explain the convention and concepts relating to consistency and material disclosure......7

CLIENT 1.......................................................................................................................................8

a..............................................................................................................................................8

b..............................................................................................................................................9

c............................................................................................................................................10

CLIENT 2.....................................................................................................................................11

a............................................................................................................................................11

b............................................................................................................................................11

CLIENT 3.....................................................................................................................................13

a............................................................................................................................................13

b............................................................................................................................................14

C. Explain the following concept, consistency and prudency..............................................14

CLIENT 4.....................................................................................................................................16

a. Explain the purpose of bank-reconciliation-statement and its importance.......................16

c............................................................................................................................................18

CLIENT 5.....................................................................................................................................20

a............................................................................................................................................20

B. Explain the term Control account and the need to prepare the account..........................21

CLIENT 6.....................................................................................................................................22

a. Explain the purpose of the suspense accounts..................................................................22

b............................................................................................................................................23

D. Differentiating between suspense account and clearing account....................................23

CONCLUSION............................................................................................................................24

REFERENCES.............................................................................................................................25

REFERENCES.............................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting principle are general guidelines and rules on the basis of which the

company prepares its financial statements. If company distributes its financial statements to the

public, it is required to follow generally accepted accounting principles in the preparation of

those statements. This report aims at giving an overview of accounting principles and concepts

and recording transactions using double entry book keeping. Along with this there will be

presentation and illustration of recording various financial statements. The report presents

depict the depreciation accounting and its methods with examples. The report mentioned the

importance of making control account. The report extract the trail balance and helps in

understanding the purpose of making suspense account and clearing account with the

differentiation of both.

MAIN BODY

1.Financial accounting and its purpose.

It is the specialized branch of accounting that keeps track of all the financial

transactions of the company. Using the financial standards the financial transactions are

recorded and summarized in the financial statements such as balance sheet. Financial

accounting measures the economy performance of a company with the means of money. The

main objective of financial accounting is to show an accurate and fair picture of financial

affairs of the company for external users with useful information to investors, creditors and

other people outside the organization.

The following are some important financial statements which are made with the financial

accounting: Income Statements: in a specific period of time, the company's profitability is measures

through the income statements. Revenue, expenses, gains and losses are the main

components of the income statements (Basu and Waymire, 2017). It provides

information to the outsiders not only about the company's financial affairs but it also

provides an overview of company sales and net income. Balance Sheet : It is the financial statements of the company which includes the assets,

liability,equity capital, total debt etc, at a point in time. Balance sheet is more like a

picture of the financial position of the company is specific period of time like six

months, or one year.

Financial accounting principle are general guidelines and rules on the basis of which the

company prepares its financial statements. If company distributes its financial statements to the

public, it is required to follow generally accepted accounting principles in the preparation of

those statements. This report aims at giving an overview of accounting principles and concepts

and recording transactions using double entry book keeping. Along with this there will be

presentation and illustration of recording various financial statements. The report presents

depict the depreciation accounting and its methods with examples. The report mentioned the

importance of making control account. The report extract the trail balance and helps in

understanding the purpose of making suspense account and clearing account with the

differentiation of both.

MAIN BODY

1.Financial accounting and its purpose.

It is the specialized branch of accounting that keeps track of all the financial

transactions of the company. Using the financial standards the financial transactions are

recorded and summarized in the financial statements such as balance sheet. Financial

accounting measures the economy performance of a company with the means of money. The

main objective of financial accounting is to show an accurate and fair picture of financial

affairs of the company for external users with useful information to investors, creditors and

other people outside the organization.

The following are some important financial statements which are made with the financial

accounting: Income Statements: in a specific period of time, the company's profitability is measures

through the income statements. Revenue, expenses, gains and losses are the main

components of the income statements (Basu and Waymire, 2017). It provides

information to the outsiders not only about the company's financial affairs but it also

provides an overview of company sales and net income. Balance Sheet : It is the financial statements of the company which includes the assets,

liability,equity capital, total debt etc, at a point in time. Balance sheet is more like a

picture of the financial position of the company is specific period of time like six

months, or one year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash Flow Statements: this statements shows the cash inflow and outflow in the

business. Cash flow statements reports the operating cash flow, investing cash flow and

financial cash flow, it is important for assessing the company's liability, flexibility and

overall financial performance.

The purpose of the financial accounting are as follows:

The main purpose of financial accounting is to provide information to the investors and

creditors about financial position of the company in a specific time periods.

Financial accounting helps in the systematic recording of the financial transactions of

the company (Ijiri, 2014).

Financial accounting helps in the ascertaining the net profit earned or loss in the

business with he help of financial statements.

The accounting gives the amount of profit and loss occurred in a specific period of time.

2.The regulations of the Financial accounting.

Regulation defined as the set of rules that is designed to control and conduct by

authority. The rules that are developed by independent authoritative body to govern the

preparation of financial statements which are accounting standards. The user of financial

information are broad and diverse group. Every user of accounting has a common requirement

that the information in the financial statement should be relevant, fairly presented,

understandable and comparable. In UK, the major authorities involves in formatting the

regulation of accounting are as follows: IASB: The international Accounting Standards Board in the conceptual framework for

financial reporting and the general purpose of financial reporting is to provide financial

information about the reporting entity that is useful foe external users for decisions

regarding providing resources to the entity.. It is also used for revealing the financial

statements to the public. FRC: Financial regulation council is the regulation for the accounting formulated by

different authorities and corporation of UK to make some standards for accounting in

UK (Jayaram and et.al., 2018). It is the domestic regulation board which frame worked

the guidelines after monitoring and execution of different financial disclosure associated

with financial accounting.

business. Cash flow statements reports the operating cash flow, investing cash flow and

financial cash flow, it is important for assessing the company's liability, flexibility and

overall financial performance.

The purpose of the financial accounting are as follows:

The main purpose of financial accounting is to provide information to the investors and

creditors about financial position of the company in a specific time periods.

Financial accounting helps in the systematic recording of the financial transactions of

the company (Ijiri, 2014).

Financial accounting helps in the ascertaining the net profit earned or loss in the

business with he help of financial statements.

The accounting gives the amount of profit and loss occurred in a specific period of time.

2.The regulations of the Financial accounting.

Regulation defined as the set of rules that is designed to control and conduct by

authority. The rules that are developed by independent authoritative body to govern the

preparation of financial statements which are accounting standards. The user of financial

information are broad and diverse group. Every user of accounting has a common requirement

that the information in the financial statement should be relevant, fairly presented,

understandable and comparable. In UK, the major authorities involves in formatting the

regulation of accounting are as follows: IASB: The international Accounting Standards Board in the conceptual framework for

financial reporting and the general purpose of financial reporting is to provide financial

information about the reporting entity that is useful foe external users for decisions

regarding providing resources to the entity.. It is also used for revealing the financial

statements to the public. FRC: Financial regulation council is the regulation for the accounting formulated by

different authorities and corporation of UK to make some standards for accounting in

UK (Jayaram and et.al., 2018). It is the domestic regulation board which frame worked

the guidelines after monitoring and execution of different financial disclosure associated

with financial accounting.

IFRS: international financial regulation system in the internationally accepted

accounting standard, which stated to the full disclosure of the organization's key

financial statements.

3. The Accounting rules and principles that governs the presentation and preparation of the

financial statements.

Generally accepted accounting principles are the set of ten accounting standard and

guidelines created and maintained by FASB. GAAP guidelines ensures that the financial

statements are both informative and reliable. The ten basic accounting rules are as follows: Single entity concept: the business should be considered as separate entity from its

owner in the eye of the law. In legal term a business can exist longer even after the

existence of its owner or promoters. Money Measurement Concept: This concept stated that a particular measure of

currency is specified for recording financial statements (Jerry, J. and et.al., 2018). If

other type of transaction are made they should keep aside of the financial statements. Dual aspect concept: This concept stated that there will be dual system for every

transaction. For example, for every debit there should be a credit and vice versa. Going concern concept: In this concept it is expected that the business will work for

the infinite time period. Cost Concept: this concept only apply to the fixed assets, it stated that the assets will be

recorded on their original price and in the first year. Than this assets will be recorded in

next year with the subtraction of depreciation. Accounting year concept: Financial statements are always prepared in a specific time

period to complete a cycle of the accounting process. For example, monthly , quarterly,

annually. Matching concept: this principles stated that for every entry of revenue recorded in a

accounting period, an equal expense entry has to be recorded for correctly calculating

profit or loss (Khan, 2015). Realization concept: According is said to made only when it is earned. An advance or

fee paid is not considered a profit until the good is being transferred to the buyer.

accounting standard, which stated to the full disclosure of the organization's key

financial statements.

3. The Accounting rules and principles that governs the presentation and preparation of the

financial statements.

Generally accepted accounting principles are the set of ten accounting standard and

guidelines created and maintained by FASB. GAAP guidelines ensures that the financial

statements are both informative and reliable. The ten basic accounting rules are as follows: Single entity concept: the business should be considered as separate entity from its

owner in the eye of the law. In legal term a business can exist longer even after the

existence of its owner or promoters. Money Measurement Concept: This concept stated that a particular measure of

currency is specified for recording financial statements (Jerry, J. and et.al., 2018). If

other type of transaction are made they should keep aside of the financial statements. Dual aspect concept: This concept stated that there will be dual system for every

transaction. For example, for every debit there should be a credit and vice versa. Going concern concept: In this concept it is expected that the business will work for

the infinite time period. Cost Concept: this concept only apply to the fixed assets, it stated that the assets will be

recorded on their original price and in the first year. Than this assets will be recorded in

next year with the subtraction of depreciation. Accounting year concept: Financial statements are always prepared in a specific time

period to complete a cycle of the accounting process. For example, monthly , quarterly,

annually. Matching concept: this principles stated that for every entry of revenue recorded in a

accounting period, an equal expense entry has to be recorded for correctly calculating

profit or loss (Khan, 2015). Realization concept: According is said to made only when it is earned. An advance or

fee paid is not considered a profit until the good is being transferred to the buyer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Full-Disclosure concept: it id the important concept which requires the full disclosure

of the financial statements to the outsider for the decision making (Financial Accounting

Concepts, 2018).

4. Explain the convention and concepts relating to consistency and material disclosure. Consistency concepts: this convention stated that once an entity has decided to adopt

one method of accounting, it should use the same method for over and over the

accounting year. The business can never ever use a different method of accounting

unless there are more than a sound reason for the change in method. And if a company is

changing a accounting method the new method should show the better financial position

than the previous accounting method (Lessambo, 2018). Id there occurs any change it

should be disclosed, as it would be difficult for the outsiders to compares the financial

statement with previous year's financial statements.

Materialist Concept: It refers to the importance of an item or an event. It is important to

report every material item in the financial statements as the knowledge of the item might

influence the decisions of users of financial statements. The financial reporting process

should be cost effective, that is the value of information should exceed the cost of its

preparation (Mellemvik and Badshah, 2017). Convention of materiality allows

accountants to ignore other principles with respect to item that are not principle. It helps

in overburden of minute detail in the statements.

of the financial statements to the outsider for the decision making (Financial Accounting

Concepts, 2018).

4. Explain the convention and concepts relating to consistency and material disclosure. Consistency concepts: this convention stated that once an entity has decided to adopt

one method of accounting, it should use the same method for over and over the

accounting year. The business can never ever use a different method of accounting

unless there are more than a sound reason for the change in method. And if a company is

changing a accounting method the new method should show the better financial position

than the previous accounting method (Lessambo, 2018). Id there occurs any change it

should be disclosed, as it would be difficult for the outsiders to compares the financial

statement with previous year's financial statements.

Materialist Concept: It refers to the importance of an item or an event. It is important to

report every material item in the financial statements as the knowledge of the item might

influence the decisions of users of financial statements. The financial reporting process

should be cost effective, that is the value of information should exceed the cost of its

preparation (Mellemvik and Badshah, 2017). Convention of materiality allows

accountants to ignore other principles with respect to item that are not principle. It helps

in overburden of minute detail in the statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

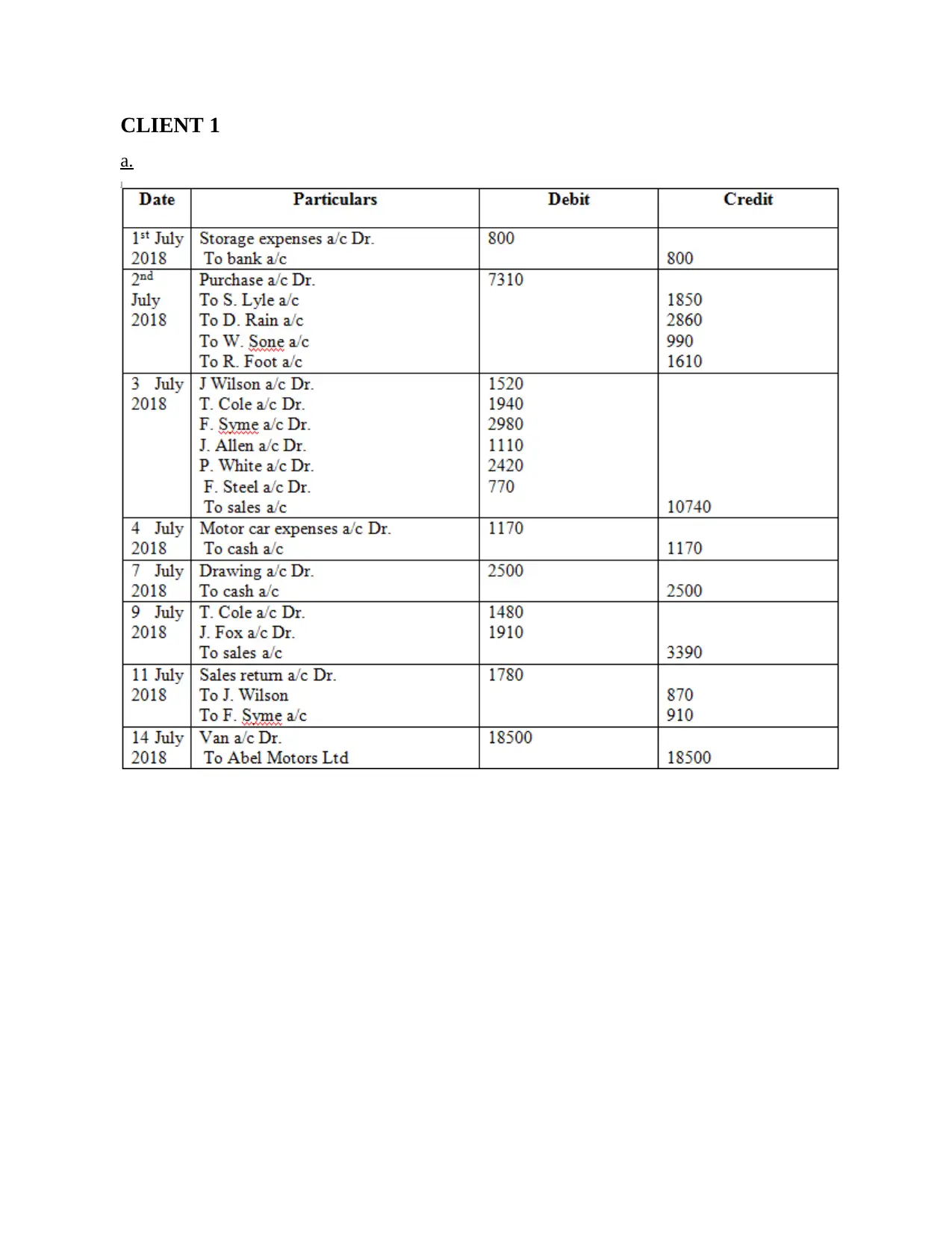

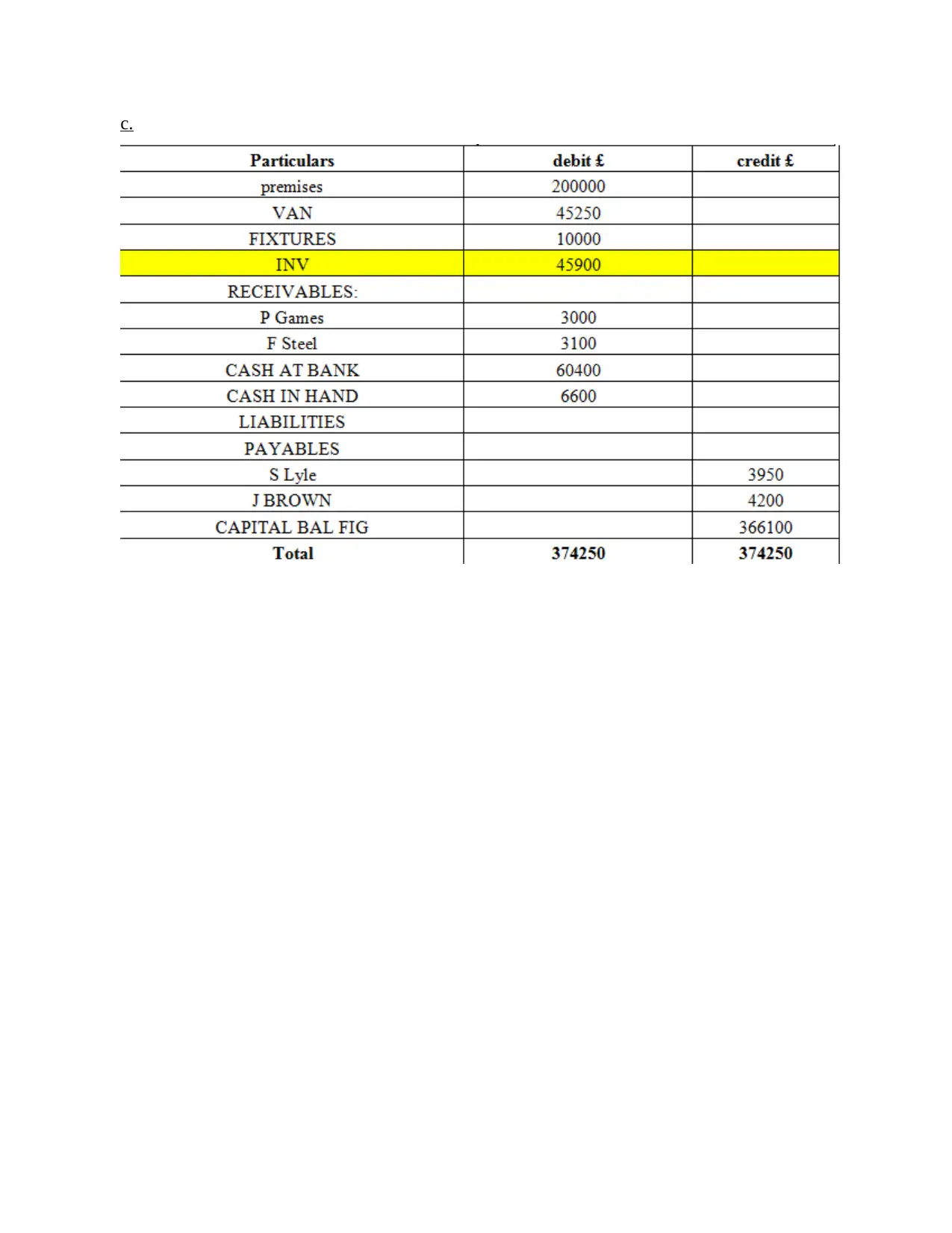

CLIENT 1

a.

a.

b.

Mentioned in appendix.

Mentioned in appendix.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

c.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

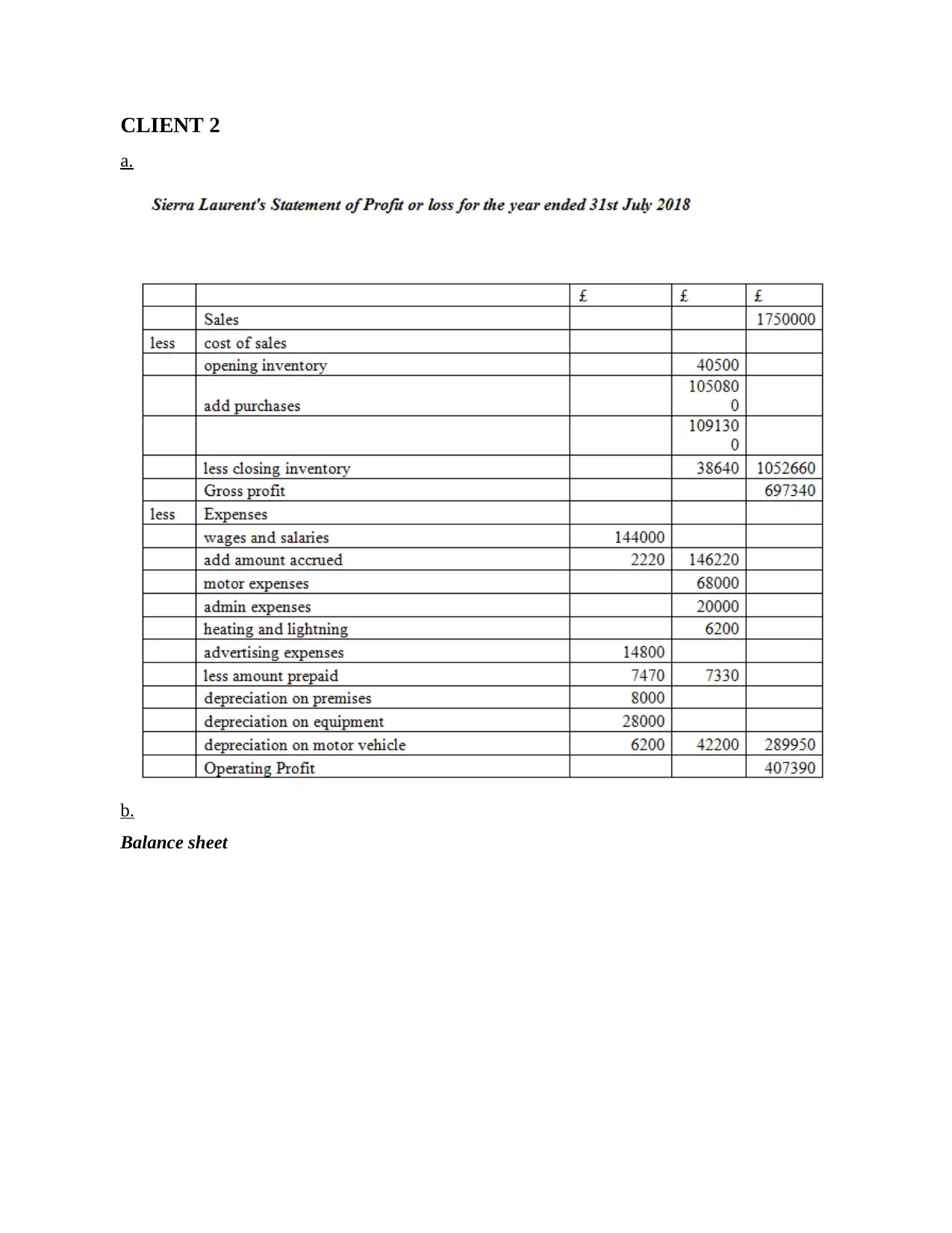

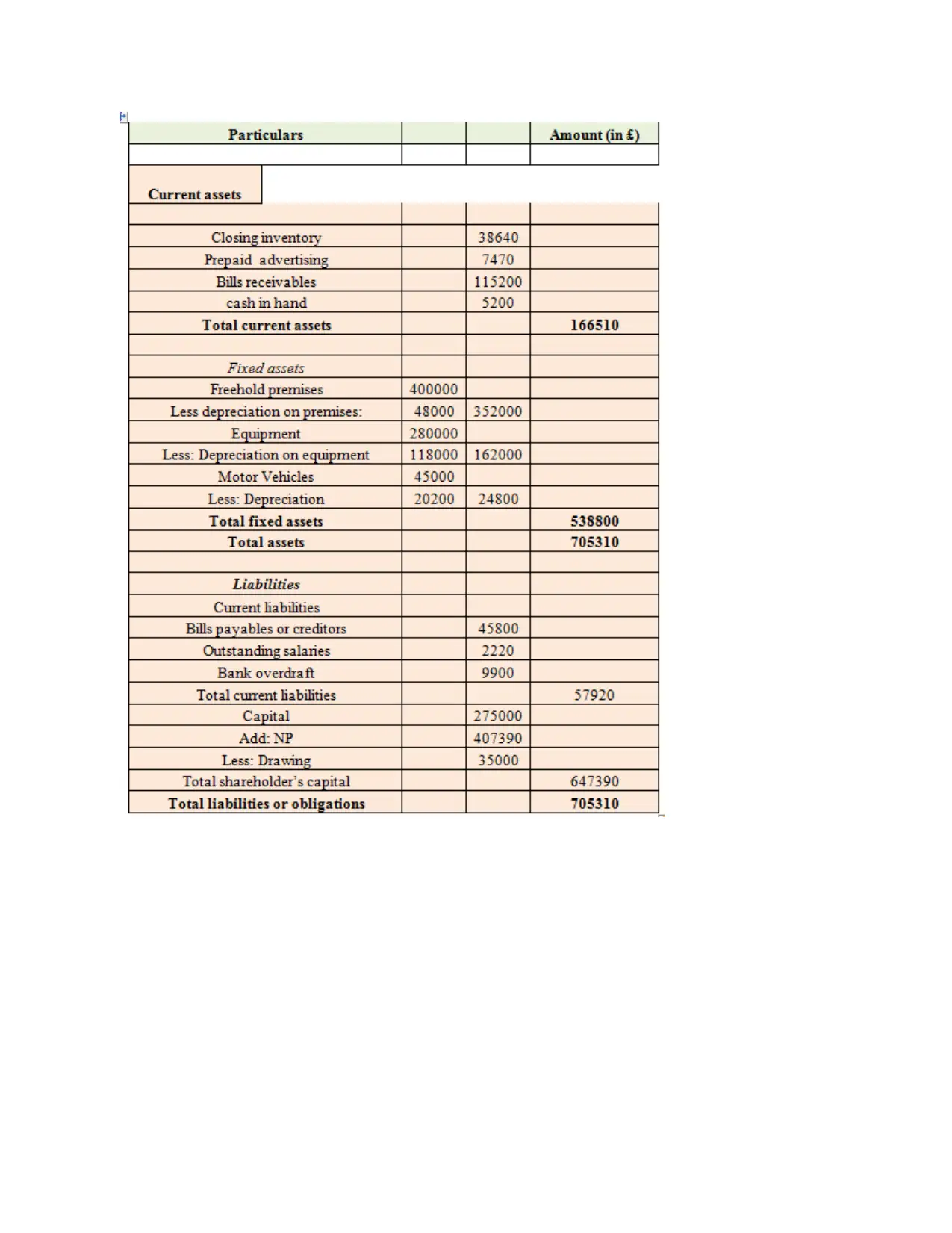

CLIENT 2

a.

b.

Balance sheet

a.

b.

Balance sheet

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.