Financial Accounting Report for Junior Accountant at PH Accountancy

VerifiedAdded on 2020/12/09

|27

|4352

|449

Report

AI Summary

This report, prepared by a junior accountant for PH Accountancy, provides a comprehensive overview of financial accounting principles and practices. It begins with an introduction to financial accounting, its purpose, and the preparation of financial statements. The report details the roles of internal and external stakeholders, including owners, management, customers, suppliers, creditors, and the government. It then moves on to practical applications, including recording transactions, preparing profit and loss statements, and creating statements of financial position for various clients like Munteanu Ltd. The report further explains key accounting concepts such as consistency, along with the purpose and methods of depreciation. It also covers bank reconciliation statements, sales and purchase ledger control accounts, suspense accounts, and the preparation of trial balances. The report concludes by emphasizing the importance of accurate financial reporting for decision-making and compliance.

Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

REPORT TO LINE MANAGERS..................................................................................................1

1. Financial accounting and its purpose......................................................................................1

2. Internal and external stockholders of the company.................................................................3

CLIENT 1........................................................................................................................................6

Recording transactions in the books of Alexender.....................................................................6

CLIENT 2........................................................................................................................................6

A) preparation of profit and loss statement of Munteanu Ltd.....................................................6

B) statement of financial position of the Manuteanu Ltd...........................................................8

C) Explanation of the accounting concepts ................................................................................8

D) Purpose of depreciation and its methods in formulation of accounting statements...............9

E) Difference between financial statements prepared by Sole trader and a limited company..11

CLIENT 3......................................................................................................................................11

A) Purpose of bank reconciliation statements...........................................................................11

B) Areas that may cause he variation in bank records and company's records.........................12

C) Imprest system.....................................................................................................................12

D) Preparation of Bank reconciliation statement of Burcu Ltd................................................12

CLIENT 4.....................................................................................................................................13

A) Preparation of Sales and purchase ledger control account of Hilly.....................................13

B) Control account....................................................................................................................14

CLIENT 5......................................................................................................................................14

A) Suspense accounts and its main features.............................................................................14

B) preparation of Trail balance.................................................................................................15

C) Preparation of trial balance from suspense account.............................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

REPORT TO LINE MANAGERS..................................................................................................1

1. Financial accounting and its purpose......................................................................................1

2. Internal and external stockholders of the company.................................................................3

CLIENT 1........................................................................................................................................6

Recording transactions in the books of Alexender.....................................................................6

CLIENT 2........................................................................................................................................6

A) preparation of profit and loss statement of Munteanu Ltd.....................................................6

B) statement of financial position of the Manuteanu Ltd...........................................................8

C) Explanation of the accounting concepts ................................................................................8

D) Purpose of depreciation and its methods in formulation of accounting statements...............9

E) Difference between financial statements prepared by Sole trader and a limited company..11

CLIENT 3......................................................................................................................................11

A) Purpose of bank reconciliation statements...........................................................................11

B) Areas that may cause he variation in bank records and company's records.........................12

C) Imprest system.....................................................................................................................12

D) Preparation of Bank reconciliation statement of Burcu Ltd................................................12

CLIENT 4.....................................................................................................................................13

A) Preparation of Sales and purchase ledger control account of Hilly.....................................13

B) Control account....................................................................................................................14

CLIENT 5......................................................................................................................................14

A) Suspense accounts and its main features.............................................................................14

B) preparation of Trail balance.................................................................................................15

C) Preparation of trial balance from suspense account.............................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Financial accounting is a system of accounting that includes all the financial informations

of the a company. It a process of recording all the financial transactions and preparing financial

reports by summarizing all the financial details for the purpose of showing financial condition of

the company during a specific time period. PH Accountancy company is professional service

provider company that was establisheds in the year 1987. Ttoday the company is ranked as the

big four service provider company in the world. The present study shows a report of junior

accountant of the PH Accountancy company to be submitted to its line manager. The report

includes a brief introduction about the meaning and purpose of the financial accounting. It also

shows a detailed discussion about internal and external stakeholder of the company that have

interest in the financial informations of the company. The assignment shows preparation of

financial statements of the sole trader, partnership and limited companies. Further, the present

report also shows preparation of bank reconciliation statement for the purpose of ensuring both

bank and company's records are providing same and accurate results.

REPORT TO LINE MANAGERS

PH Accountancy LTD.

To,

The Line manager,

From, Junior accountant

Subject: for showing principles, roles and conventions of accountnacyaccountancy

1. Financial accounting and its purpose

“Financial accounting system is a branch of accounting system which concerns with

recording and summarizing each financial transaction made by a company during the financial

period or during a specific time.”

Financial accounting includes preparation of income statement, balance sheet and bank

reconciliation statements, etc. that helps the business in showing its actual financial position

(Henderson, 2015). While preparing these statements, the accountant uses specific guidelines,

methods and process of the financial accounting system.

PH Accountancy needs to prepare the financial statements of the company so that it can

provide all the relevant informations to the interested parties of the company. Further,

preparation of financial reports can also help its managers and board members in determining

1

Financial accounting is a system of accounting that includes all the financial informations

of the a company. It a process of recording all the financial transactions and preparing financial

reports by summarizing all the financial details for the purpose of showing financial condition of

the company during a specific time period. PH Accountancy company is professional service

provider company that was establisheds in the year 1987. Ttoday the company is ranked as the

big four service provider company in the world. The present study shows a report of junior

accountant of the PH Accountancy company to be submitted to its line manager. The report

includes a brief introduction about the meaning and purpose of the financial accounting. It also

shows a detailed discussion about internal and external stakeholder of the company that have

interest in the financial informations of the company. The assignment shows preparation of

financial statements of the sole trader, partnership and limited companies. Further, the present

report also shows preparation of bank reconciliation statement for the purpose of ensuring both

bank and company's records are providing same and accurate results.

REPORT TO LINE MANAGERS

PH Accountancy LTD.

To,

The Line manager,

From, Junior accountant

Subject: for showing principles, roles and conventions of accountnacyaccountancy

1. Financial accounting and its purpose

“Financial accounting system is a branch of accounting system which concerns with

recording and summarizing each financial transaction made by a company during the financial

period or during a specific time.”

Financial accounting includes preparation of income statement, balance sheet and bank

reconciliation statements, etc. that helps the business in showing its actual financial position

(Henderson, 2015). While preparing these statements, the accountant uses specific guidelines,

methods and process of the financial accounting system.

PH Accountancy needs to prepare the financial statements of the company so that it can

provide all the relevant informations to the interested parties of the company. Further,

preparation of financial reports can also help its managers and board members in determining

1

the actual position and performance of the company so that they can easily make the appropriate

policies and strategies for its betterment.

Purpose of financial accounting

The main purpose of the whole financial accounting system in PH Accountancy is to

show the actual financial position of it. Further, other objectives of the financial accounting

systems are as follows:

Summarize the financial informations: It is also one of the major objective of the

financial accounting system. In financial accounting system, all the transactions made

by the company during specific time are summarized so that they could be available in a

single set of reports (Macve, 2015). It helps the managers, board of directors and other

interested parties in collecting all the relevant informations of the business that can

affect their interest.

Investment decisions: Shareholders and other investors of the company wants to know

the actual position of the company for the sake of estimating their returns from the

investment made in the company and risk involved with the investment. Financial

accounting reports provides all the relevant informations to the investors to help them in

their decision making.

Existing shareholders: As, the existing shareholders are the real owners of the

company, they need to know each information about the company (Narayanaswamy,

2017). Therefore, providing relevant information to the existing shareholders of the

company is also a main purpose of preparation of financial statements of the company.

Taxation decisions: Financial accounting reports also provides all information to the

Government agencies for the purpose of calculating the amount of taxation tpto be

imposed of the company. They can determine the income earned by the company, assets

and liabilities held by the company, all the investments made by it, etc.

Keeping records: The financial accounting reports are also prepared for the purpose of

recording all the incomes and expenditure of the business. It helps the organisation in

tracking each area where the company is spending its funds. It also provides help to the

managers in observing the financial behaviour of the company.

Ensuring earning: Further, financial reports of the company also helps in determining

the actual income earned by the firm. It shows each income and expenditure made by

2

policies and strategies for its betterment.

Purpose of financial accounting

The main purpose of the whole financial accounting system in PH Accountancy is to

show the actual financial position of it. Further, other objectives of the financial accounting

systems are as follows:

Summarize the financial informations: It is also one of the major objective of the

financial accounting system. In financial accounting system, all the transactions made

by the company during specific time are summarized so that they could be available in a

single set of reports (Macve, 2015). It helps the managers, board of directors and other

interested parties in collecting all the relevant informations of the business that can

affect their interest.

Investment decisions: Shareholders and other investors of the company wants to know

the actual position of the company for the sake of estimating their returns from the

investment made in the company and risk involved with the investment. Financial

accounting reports provides all the relevant informations to the investors to help them in

their decision making.

Existing shareholders: As, the existing shareholders are the real owners of the

company, they need to know each information about the company (Narayanaswamy,

2017). Therefore, providing relevant information to the existing shareholders of the

company is also a main purpose of preparation of financial statements of the company.

Taxation decisions: Financial accounting reports also provides all information to the

Government agencies for the purpose of calculating the amount of taxation tpto be

imposed of the company. They can determine the income earned by the company, assets

and liabilities held by the company, all the investments made by it, etc.

Keeping records: The financial accounting reports are also prepared for the purpose of

recording all the incomes and expenditure of the business. It helps the organisation in

tracking each area where the company is spending its funds. It also provides help to the

managers in observing the financial behaviour of the company.

Ensuring earning: Further, financial reports of the company also helps in determining

the actual income earned by the firm. It shows each income and expenditure made by

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the firm. With the help of these informations, managers and directors can ensure the

actual earning of the firm. In this regard, the financial reports of the firm are also

prepared for the purpose of ensuring the earnings of the business organisation.

Credit decisions: Preparation of financial statements also have a purpose of taking

decision regarding providing credit to the company (Nudurupati, 2015). It helps in

determining the condition of the company for repaying the debts of the company by

observing its balance sheet.

Determination of actual debts and assets: PH accountancy also should prepare each

statements of the financial accounting system as it can help the company in determining

the actual amount of assets and debts held by the company as to determine the actual

position of the business organisation.

Determination of liquidity: It is also a major purpose of the preparation of financial

statements as to determine the liquidity of the firm. It shows the amount of assets held

by the company over the debts.

In this regard, there are several purposes and objectives of preparing financial

accounting reports by a business organisation.

2. Internal and external stockholders of the company

Stakeholders can be defined as the individuals or group of individuals that have interest

in the company. Each action of the company may affect the interest of the stakeholders. From

the above analysis it can be evaluated that there are many individuals and firms that have

interest in the business of PH accountancywhich can be termed as the stakeholders of company

(Kieso, Weygandt and Warfield, 2016). The stakeholders can be divided into two parts i.e.

internal stakeholders and external stakeholders. List of internal and external stakeholders is as

under:

Internal stakeholders:

Internal stakeholders can be defined as the group of individuals that serves the company.

They performs several activities for the company as board members. For example: Owner: Owners are those individuals that have invested the capital amount in the

business. They are the internal stakeholders of the company. In terms of a limited

company, the shareholders can be defined as the true owners of it. They have interest in

the financial informations of the company as they have invested a sum of amount in the

3

actual earning of the firm. In this regard, the financial reports of the firm are also

prepared for the purpose of ensuring the earnings of the business organisation.

Credit decisions: Preparation of financial statements also have a purpose of taking

decision regarding providing credit to the company (Nudurupati, 2015). It helps in

determining the condition of the company for repaying the debts of the company by

observing its balance sheet.

Determination of actual debts and assets: PH accountancy also should prepare each

statements of the financial accounting system as it can help the company in determining

the actual amount of assets and debts held by the company as to determine the actual

position of the business organisation.

Determination of liquidity: It is also a major purpose of the preparation of financial

statements as to determine the liquidity of the firm. It shows the amount of assets held

by the company over the debts.

In this regard, there are several purposes and objectives of preparing financial

accounting reports by a business organisation.

2. Internal and external stockholders of the company

Stakeholders can be defined as the individuals or group of individuals that have interest

in the company. Each action of the company may affect the interest of the stakeholders. From

the above analysis it can be evaluated that there are many individuals and firms that have

interest in the business of PH accountancywhich can be termed as the stakeholders of company

(Kieso, Weygandt and Warfield, 2016). The stakeholders can be divided into two parts i.e.

internal stakeholders and external stakeholders. List of internal and external stakeholders is as

under:

Internal stakeholders:

Internal stakeholders can be defined as the group of individuals that serves the company.

They performs several activities for the company as board members. For example: Owner: Owners are those individuals that have invested the capital amount in the

business. They are the internal stakeholders of the company. In terms of a limited

company, the shareholders can be defined as the true owners of it. They have interest in

the financial informations of the company as they have invested a sum of amount in the

3

company (Barker, 2015). They can also take decision regarding making the further

investment in the : PH accountancy. They takes the decision about investing their fund

in the company by analysing its financial position and evaluating the chances of growth

in the future. Further, the profitability of the company affects their return on the

investment and risk of investment as well.

Management: Management can be defined as a group of professionals appointed by the

PH Accountancy in the firm for making strategies and plans and help the company in

attaining rapid growth in the near future. Managers perform their task in the business to

enhance the efficiency of its operations. The performance of the business shows the

efficiency of overall business in performing the business operations. There fore,

management also have interest in the financial statements of the company as with the

help of it managers can determine the efficiency and effectiveness of working of the

business organisation.

External shareholders:

External stakeholders are those individuals that have not invested their money in

the company, but they have some sort of interest in the business. For example: Customers: Customers do not invest their money into the business. But, their interest in

the product of a specific brand get affected by the financial performance of the

company (Oulasvirta, 2016). if a company is suffering loss frequently, it may loose its

customers due it. Suppliers: Suppliers are those individuals or organisations who supplies raw material to

the company. A business organisation purchases a large amount of raw materials or

goods for the purpose of further sale. Suppliers needs financial records of the company

as to determine the risk involved in providing further credits to the company. Creditors: Creditors can be bank, individuals, financial institutions which have provided

credit to the firm. Creditors needs to determine the actual financial position of the

company for the purpose of taking decisions regarding providing credit to the company

by evaluating the risk involved in the decision and condition of the company for the

repayment.

Government: Government agencies are also interested in the financial informations of

the company for many reasons. For example, for the purpose of determining the amount

4

investment in the : PH accountancy. They takes the decision about investing their fund

in the company by analysing its financial position and evaluating the chances of growth

in the future. Further, the profitability of the company affects their return on the

investment and risk of investment as well.

Management: Management can be defined as a group of professionals appointed by the

PH Accountancy in the firm for making strategies and plans and help the company in

attaining rapid growth in the near future. Managers perform their task in the business to

enhance the efficiency of its operations. The performance of the business shows the

efficiency of overall business in performing the business operations. There fore,

management also have interest in the financial statements of the company as with the

help of it managers can determine the efficiency and effectiveness of working of the

business organisation.

External shareholders:

External stakeholders are those individuals that have not invested their money in

the company, but they have some sort of interest in the business. For example: Customers: Customers do not invest their money into the business. But, their interest in

the product of a specific brand get affected by the financial performance of the

company (Oulasvirta, 2016). if a company is suffering loss frequently, it may loose its

customers due it. Suppliers: Suppliers are those individuals or organisations who supplies raw material to

the company. A business organisation purchases a large amount of raw materials or

goods for the purpose of further sale. Suppliers needs financial records of the company

as to determine the risk involved in providing further credits to the company. Creditors: Creditors can be bank, individuals, financial institutions which have provided

credit to the firm. Creditors needs to determine the actual financial position of the

company for the purpose of taking decisions regarding providing credit to the company

by evaluating the risk involved in the decision and condition of the company for the

repayment.

Government: Government agencies are also interested in the financial informations of

the company for many reasons. For example, for the purpose of determining the amount

4

to be collected from company as corporate tax, for taking decisions regarding providing

grants to the company, for determining compliance of regulations while preparing

financial position of the company, etc.

In this order, it can be analysed that, both internal and external stakeholders of a large

business have interest in the financial informations of the company.

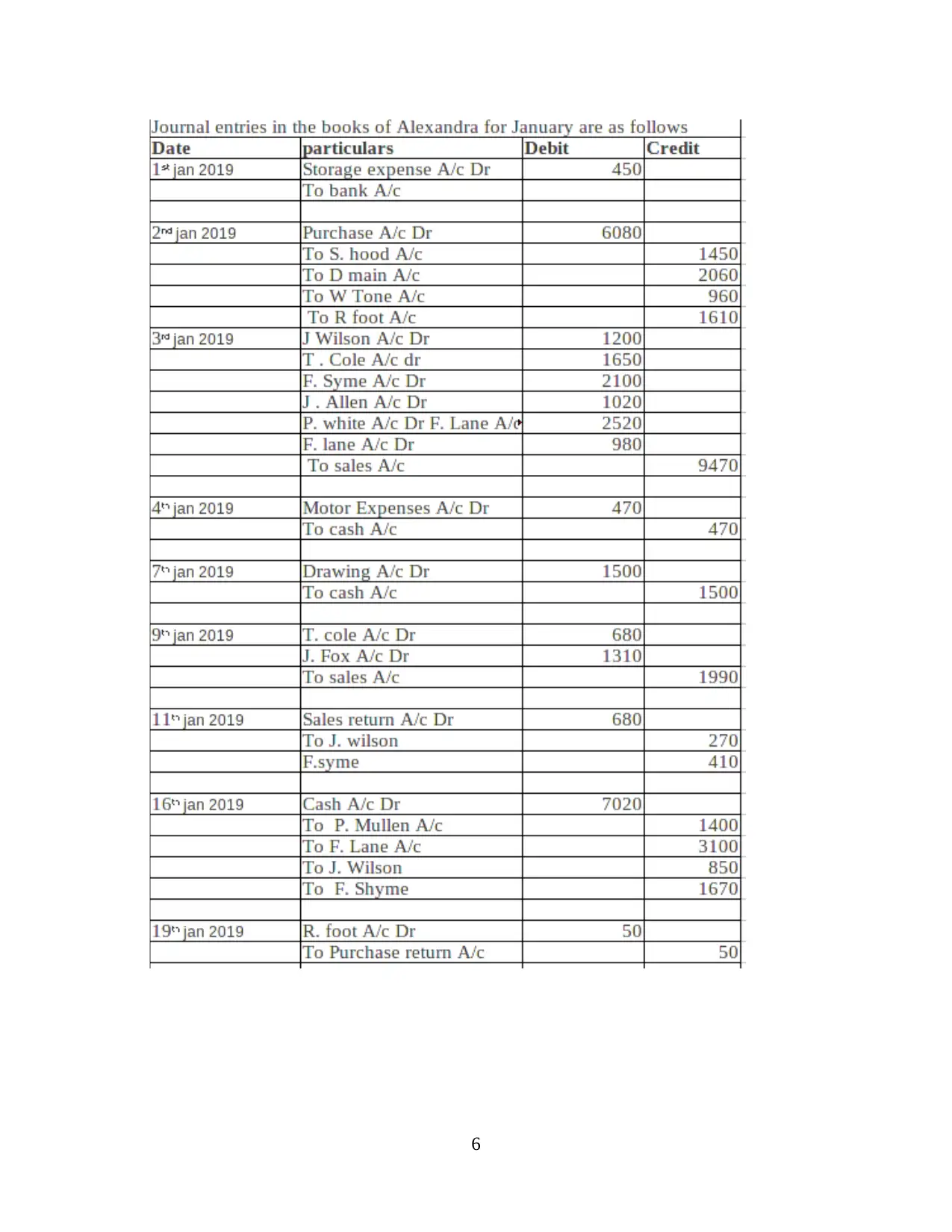

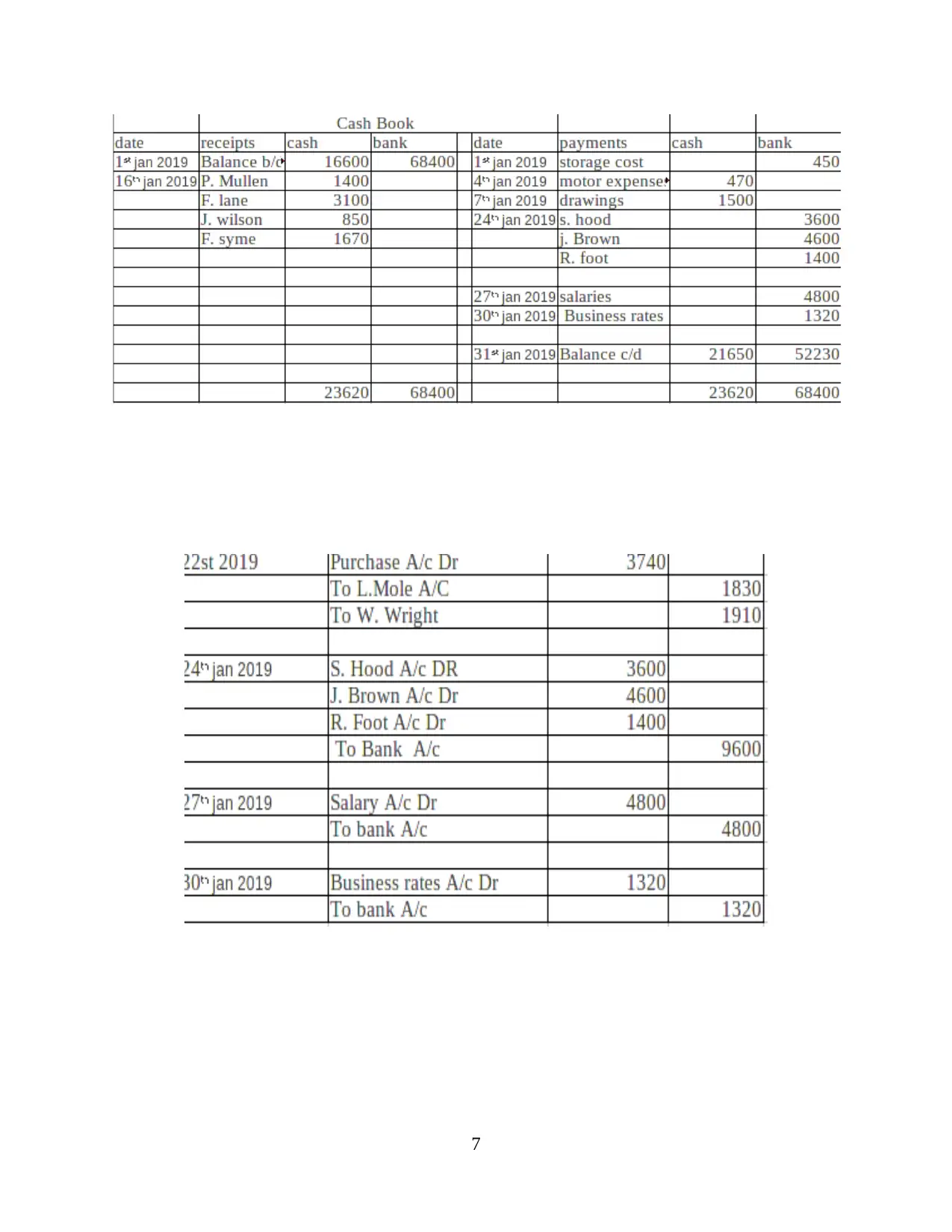

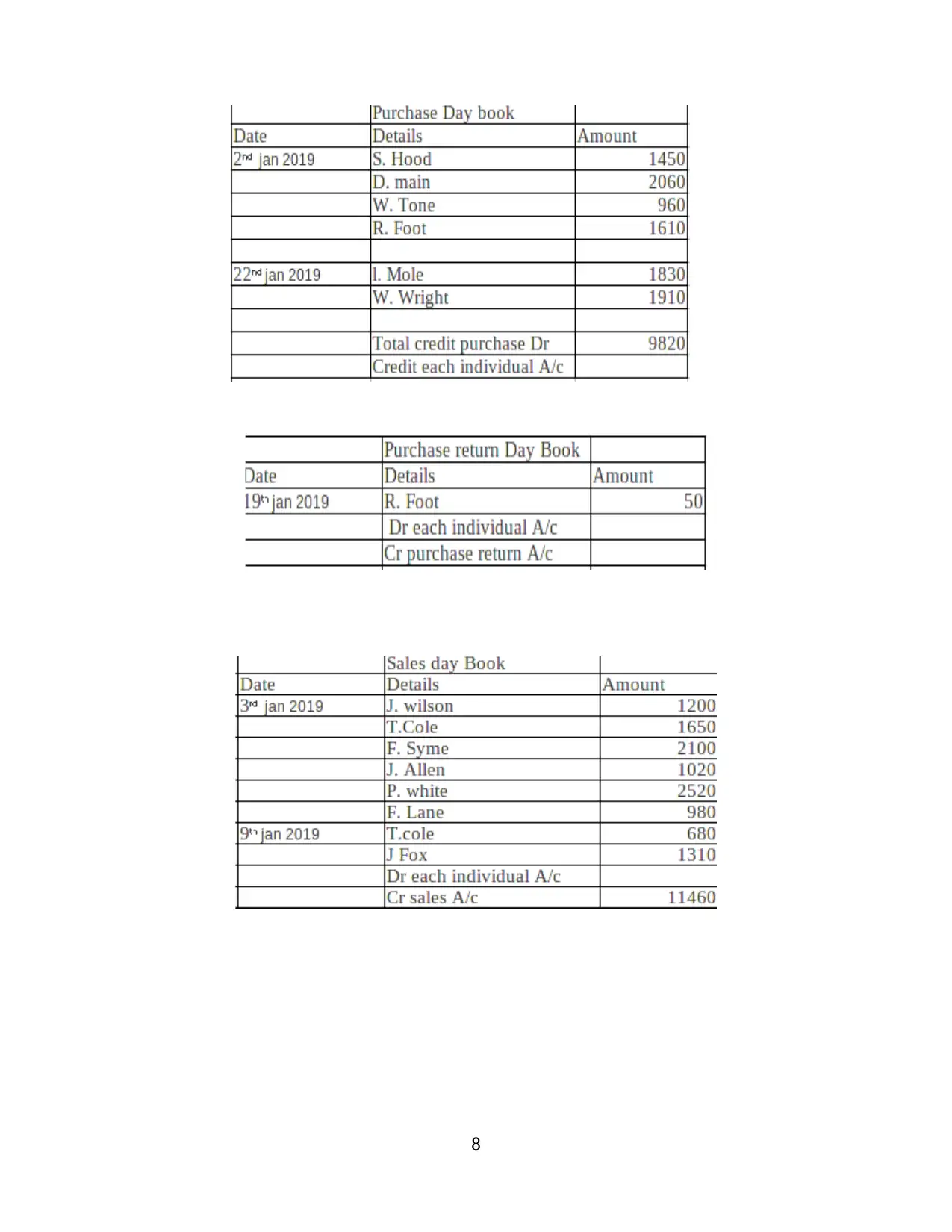

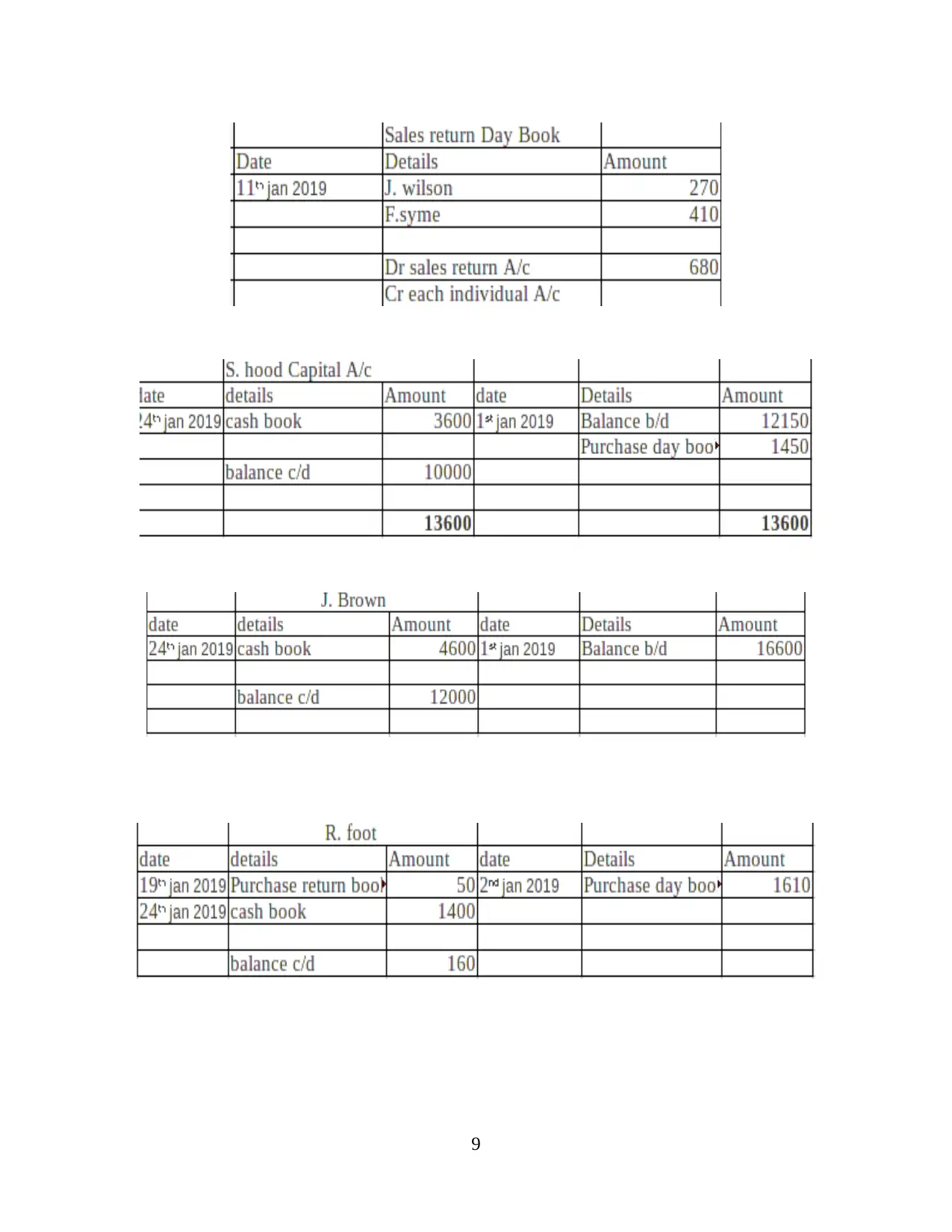

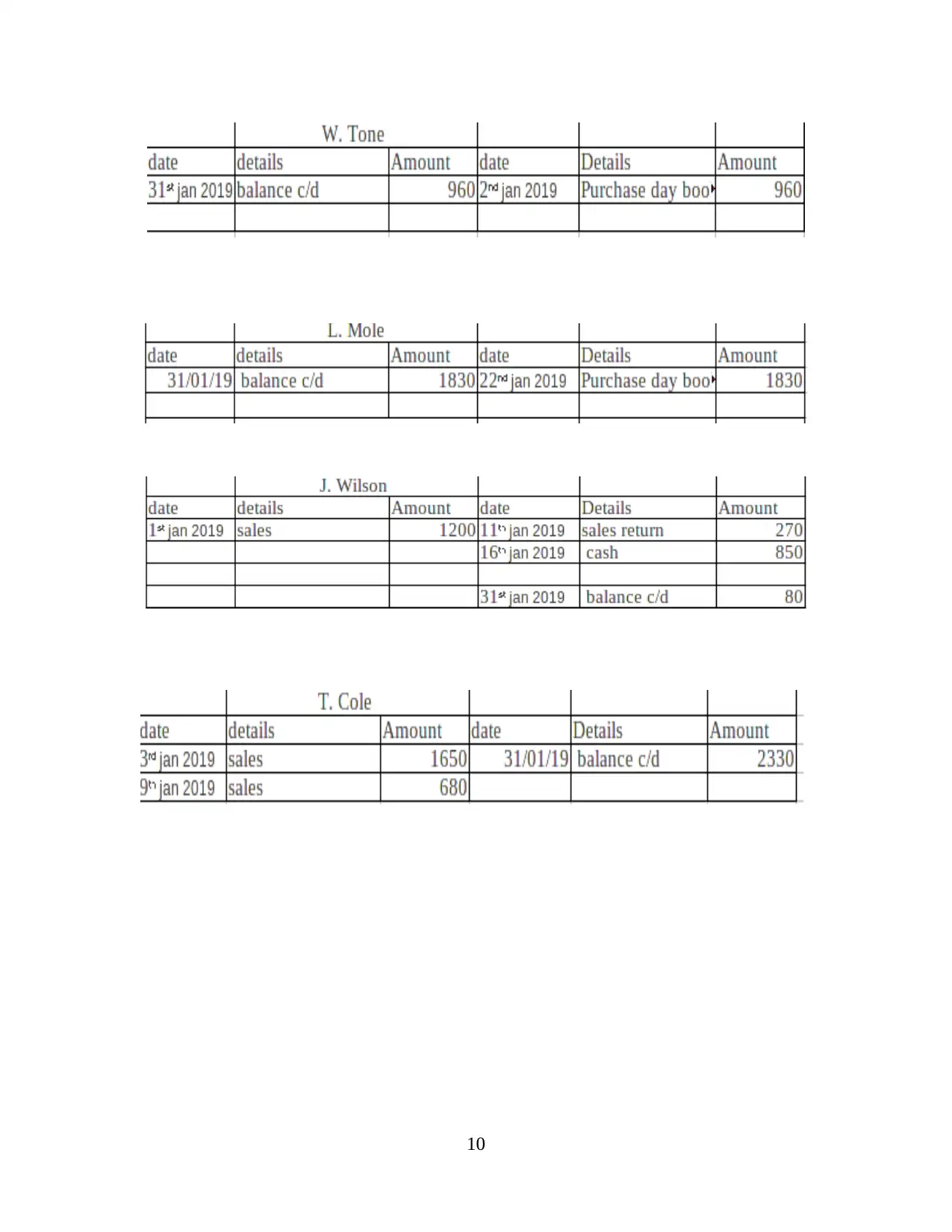

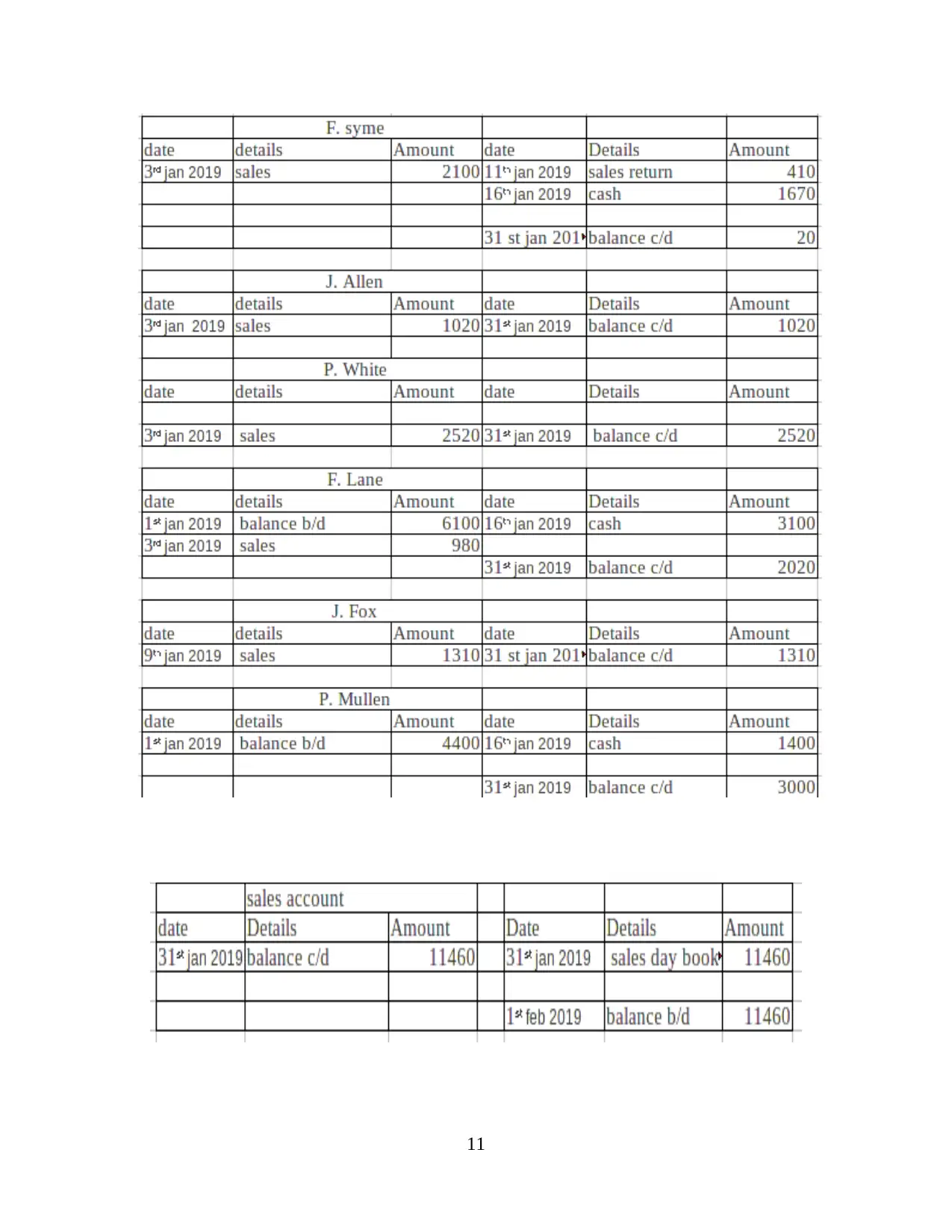

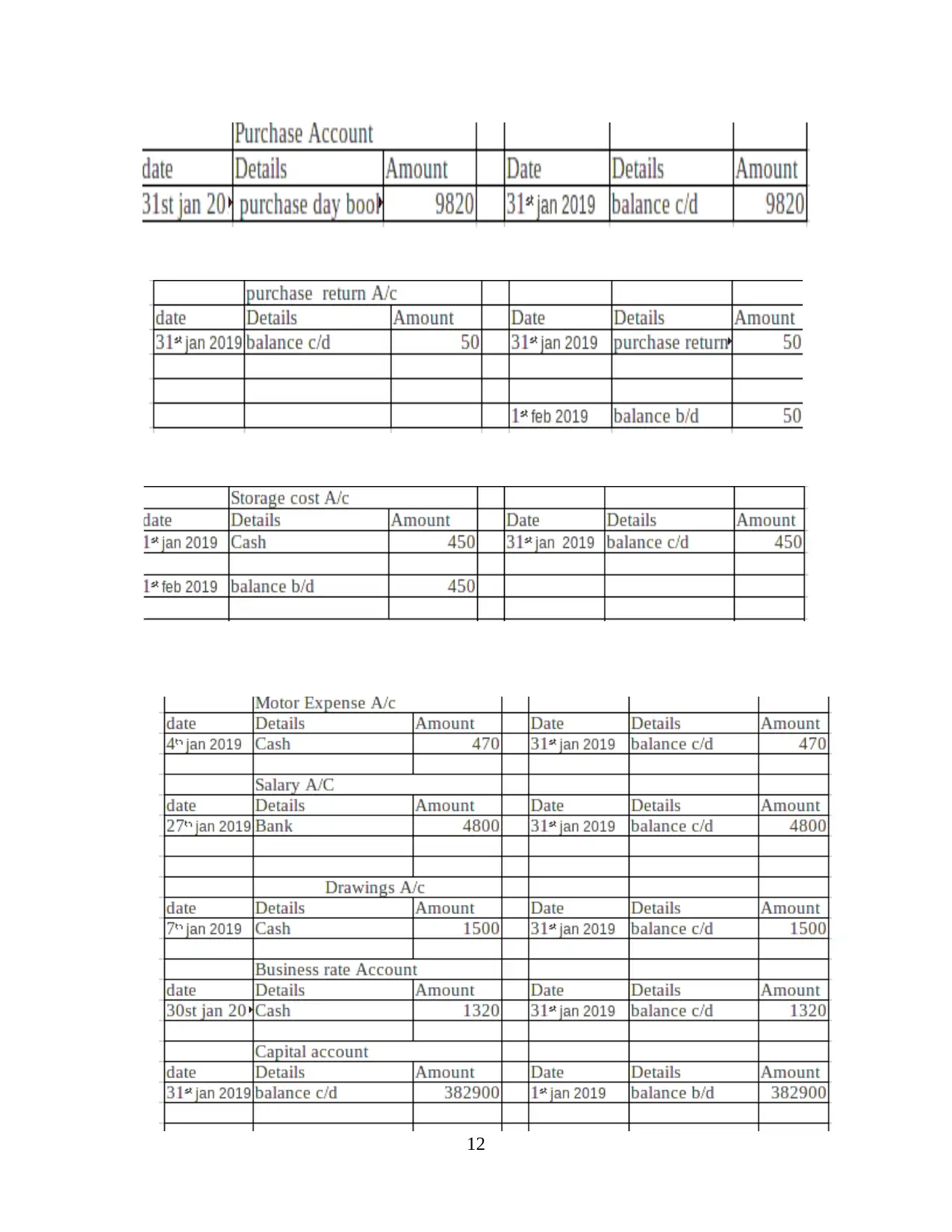

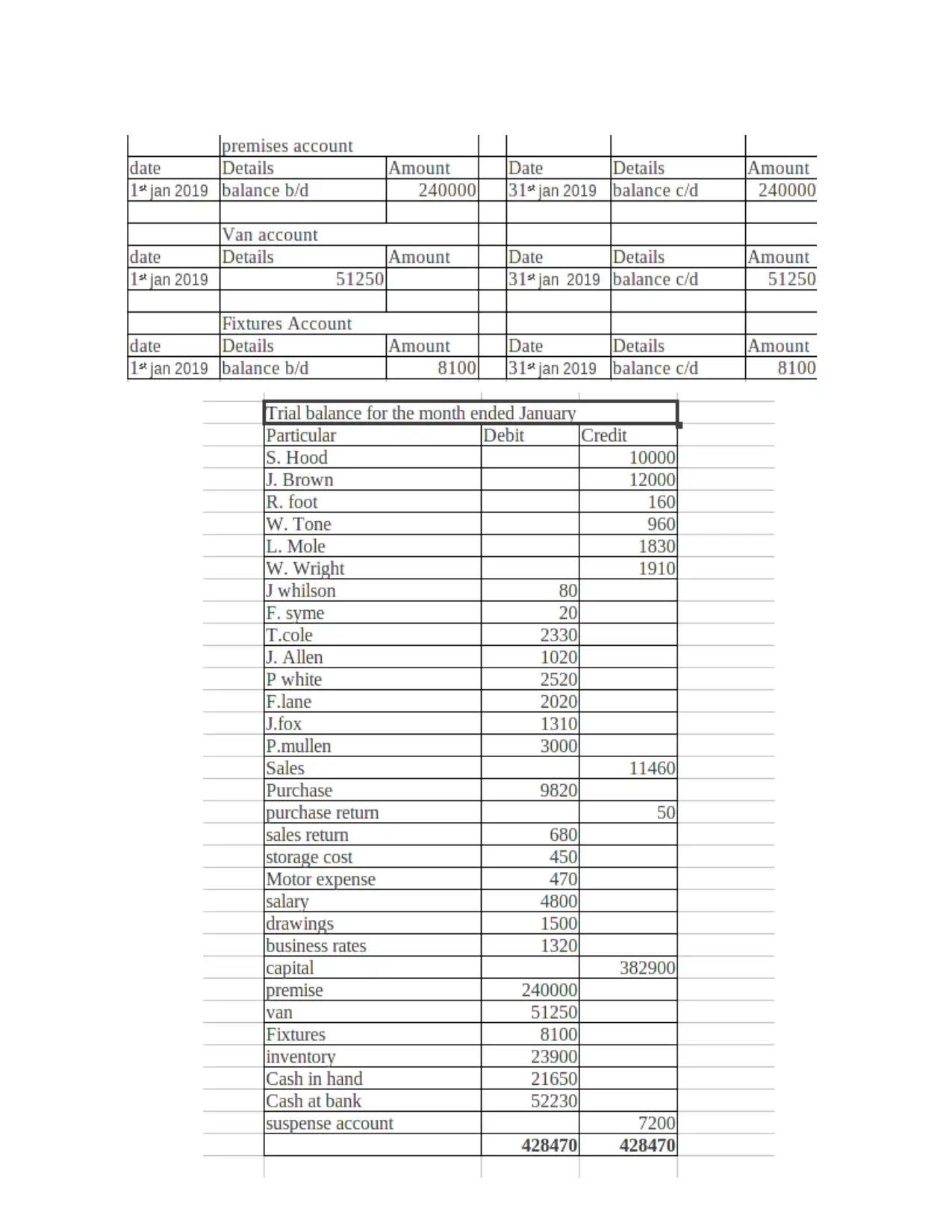

CLIENT 1

Recording transactions in the books of Alexender

5

grants to the company, for determining compliance of regulations while preparing

financial position of the company, etc.

In this order, it can be analysed that, both internal and external stakeholders of a large

business have interest in the financial informations of the company.

CLIENT 1

Recording transactions in the books of Alexender

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

7

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

9

10

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

12

13

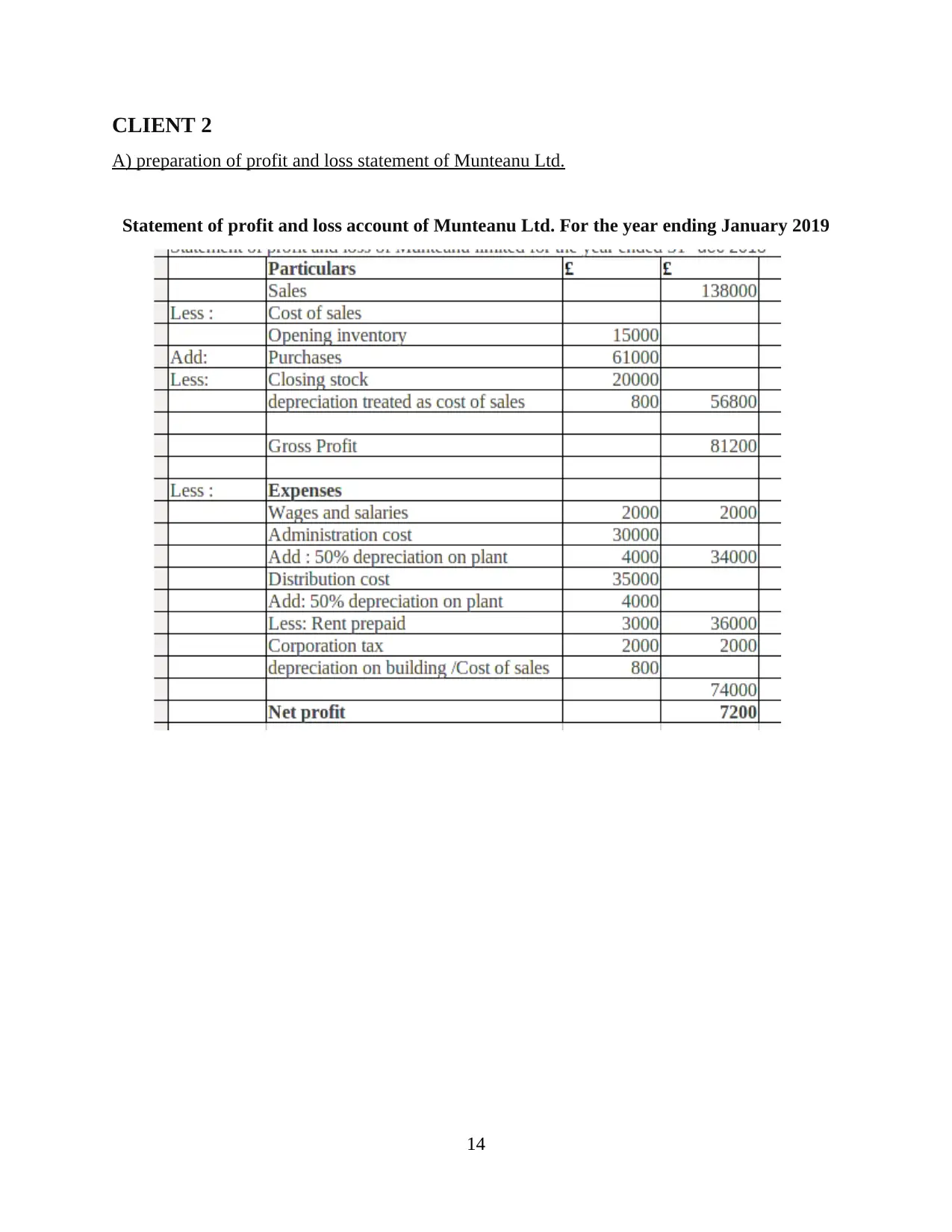

CLIENT 2

A) preparation of profit and loss statement of Munteanu Ltd.

Statement of profit and loss account of Munteanu Ltd. For the year ending January 2019

14

A) preparation of profit and loss statement of Munteanu Ltd.

Statement of profit and loss account of Munteanu Ltd. For the year ending January 2019

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

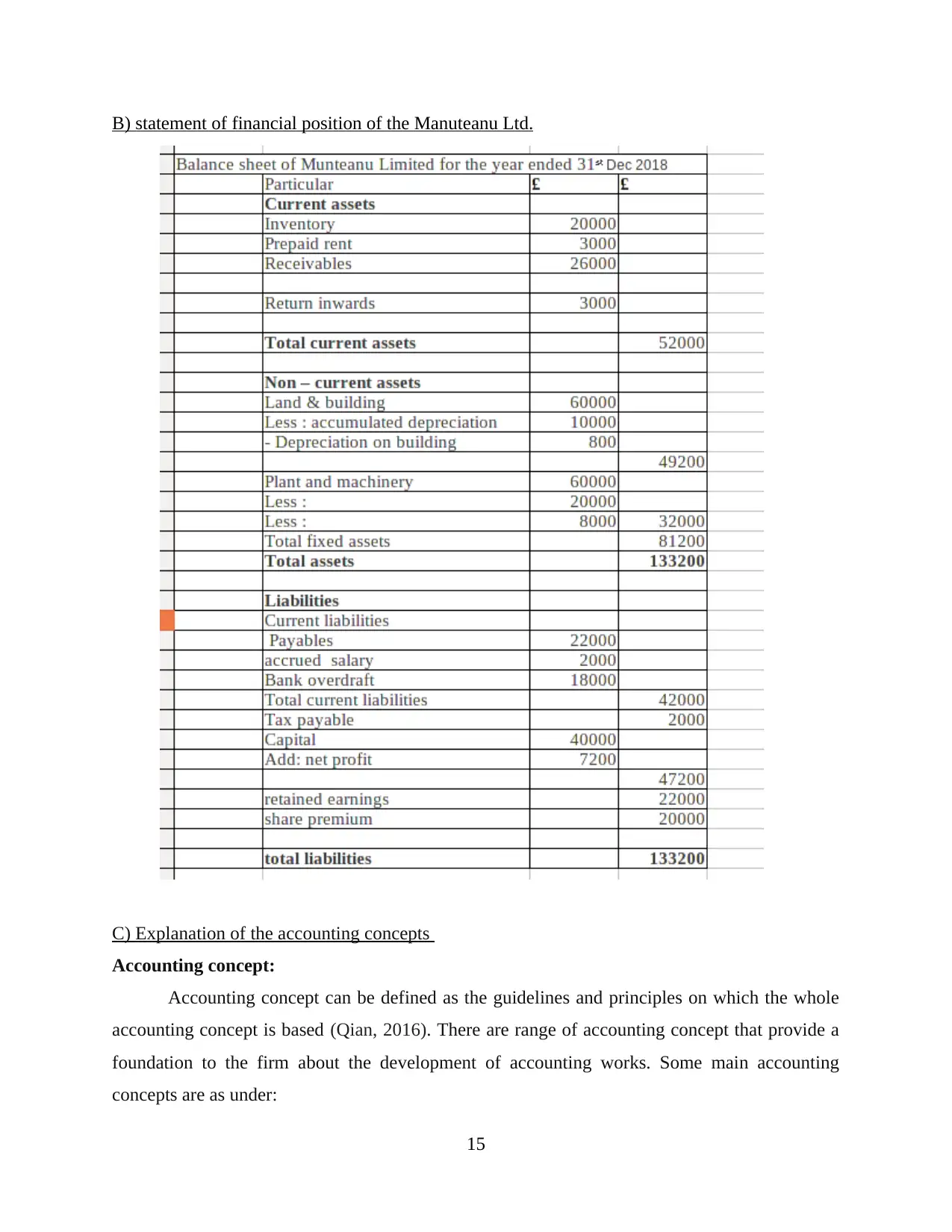

B) statement of financial position of the Manuteanu Ltd.

C) Explanation of the accounting concepts

Accounting concept:

Accounting concept can be defined as the guidelines and principles on which the whole

accounting concept is based (Qian, 2016). There are range of accounting concept that provide a

foundation to the firm about the development of accounting works. Some main accounting

concepts are as under:

15

C) Explanation of the accounting concepts

Accounting concept:

Accounting concept can be defined as the guidelines and principles on which the whole

accounting concept is based (Qian, 2016). There are range of accounting concept that provide a

foundation to the firm about the development of accounting works. Some main accounting

concepts are as under:

15

Consistency:

There are several methods and principles on the basis of which a business can prepare its

financial statements. Preparation of financial statements by different methods ay provide

different results to the company. Therefore, as per this concept, a firm needsneed to prepare the

financial statements using single method only. The company should not change the adoption of

methods frequently. Frequent change in the adoption of methods of the accounting system will

result in providing inappropriate result to the company.

Further, statements prepared through different methods, can not be used for the

comparison as to determine the enhancement of efficiency of the firm (Del Giudice, Manganelli

and De Paola, 2016). In this regard, a company need to comply with this concept for the purpose

of determining actual results from the financial statements of the it.

Prudence:

Prudence concept can also be termed as the conservatism concept of the company. As per

this concept, the company should record the liabilities and expenses should be recorded by the

business organisation as soon as they occur. On the other hand, revenues of the firm should be

recorded in the books of accounts after getting the certainty of the revenues and incomes to be

realized in future.

As per prudence concept, recording of revenues and income like sales, profits, discount

received, etc. should be done after getting a level of probability of earning the incomes. This

concept helps the company in determining actual position of the company.

Prudence concept ensures that the company shall not undervalue any liability or

overalueovervalue any income of the business. In this regard, adoption of this concept can help

the company in determination of actual profit.

D) Purpose of depreciation and its methods in formulation of accounting statements

Depreciation

Depreciation is a decline in the value of assets on the basis of its usage and passing of

time. It is a method of accounting in which a firm allocates the overall cost of the assets in the

useful life of the assets (Liapis and Kantianis, 2015)). In this method, tThe value of the assets are

declined by the firm so that it could become zero at the time of converting the assets into a scrap.

In other words, it can be stated that the depreciation is a decline in the value of assets due

to its wear and tear use and passage

16

There are several methods and principles on the basis of which a business can prepare its

financial statements. Preparation of financial statements by different methods ay provide

different results to the company. Therefore, as per this concept, a firm needsneed to prepare the

financial statements using single method only. The company should not change the adoption of

methods frequently. Frequent change in the adoption of methods of the accounting system will

result in providing inappropriate result to the company.

Further, statements prepared through different methods, can not be used for the

comparison as to determine the enhancement of efficiency of the firm (Del Giudice, Manganelli

and De Paola, 2016). In this regard, a company need to comply with this concept for the purpose

of determining actual results from the financial statements of the it.

Prudence:

Prudence concept can also be termed as the conservatism concept of the company. As per

this concept, the company should record the liabilities and expenses should be recorded by the

business organisation as soon as they occur. On the other hand, revenues of the firm should be

recorded in the books of accounts after getting the certainty of the revenues and incomes to be

realized in future.

As per prudence concept, recording of revenues and income like sales, profits, discount

received, etc. should be done after getting a level of probability of earning the incomes. This

concept helps the company in determining actual position of the company.

Prudence concept ensures that the company shall not undervalue any liability or

overalueovervalue any income of the business. In this regard, adoption of this concept can help

the company in determination of actual profit.

D) Purpose of depreciation and its methods in formulation of accounting statements

Depreciation

Depreciation is a decline in the value of assets on the basis of its usage and passing of

time. It is a method of accounting in which a firm allocates the overall cost of the assets in the

useful life of the assets (Liapis and Kantianis, 2015)). In this method, tThe value of the assets are

declined by the firm so that it could become zero at the time of converting the assets into a scrap.

In other words, it can be stated that the depreciation is a decline in the value of assets due

to its wear and tear use and passage

16

Purpose of depreciation

The main purposes of charging the depreciation over the assets are:

To match the actual cost of the productive assets of the company with the revenues

generated by it.

To estimate the scrap value of the assets (The purpose of financial statement, 2018).

To make the value of assets zero or equivalent to the scrap value of it at the time of its

sale.

To determine the true results of the business operations in terms of profit or loss.

To determine the actual value of the assets in the market.

In this order, the company charges the depreciation on its fixed assets over the time.

Methods of depreciation

There are numerous methods by which a business can calculate the amount of

depreciation to be charged over its fixed assets (Elliott, Lee and Hussainy, 2016). The company

needs to select the most appropriate method that suits with the business conditions and the nature

of assets held by it.

Some main methods of the depreciation are as under:

Straight line method: It is the simplest method of determining the amount of

depreciation. In this method, the depreciation is allocated over the assets on the basis of

life of the assets. The amount of depreciation is charges at same level in all years. The

amount of depreciation is calculated by subtracting the scrap value of assets and dividing

it with useful life of the assets.

The straight line method is useful for those fixed assets that are being used by the organisation

same manner. There is no particular manner or pattern for using the assets. This method is also

appropriate for those assets that provides same revenues to the company over the year.

Units of production method: In this method of depreciation, the depreciation is charged

over the assets on the basis of unit produced through the assets during the year (Agyei-

Mensah, 2016). Unit of production method of depreciation is used by those organisations

that manufactures the goods for the purpose of further sales.

This method is useful for the manufacturing businesses. They apply this method of depreciation

over the assets like plans, machinery, etc. that are used by the business for the purpose of

producing the goods.

17

The main purposes of charging the depreciation over the assets are:

To match the actual cost of the productive assets of the company with the revenues

generated by it.

To estimate the scrap value of the assets (The purpose of financial statement, 2018).

To make the value of assets zero or equivalent to the scrap value of it at the time of its

sale.

To determine the true results of the business operations in terms of profit or loss.

To determine the actual value of the assets in the market.

In this order, the company charges the depreciation on its fixed assets over the time.

Methods of depreciation

There are numerous methods by which a business can calculate the amount of

depreciation to be charged over its fixed assets (Elliott, Lee and Hussainy, 2016). The company

needs to select the most appropriate method that suits with the business conditions and the nature

of assets held by it.

Some main methods of the depreciation are as under:

Straight line method: It is the simplest method of determining the amount of

depreciation. In this method, the depreciation is allocated over the assets on the basis of

life of the assets. The amount of depreciation is charges at same level in all years. The

amount of depreciation is calculated by subtracting the scrap value of assets and dividing

it with useful life of the assets.

The straight line method is useful for those fixed assets that are being used by the organisation

same manner. There is no particular manner or pattern for using the assets. This method is also

appropriate for those assets that provides same revenues to the company over the year.

Units of production method: In this method of depreciation, the depreciation is charged

over the assets on the basis of unit produced through the assets during the year (Agyei-

Mensah, 2016). Unit of production method of depreciation is used by those organisations

that manufactures the goods for the purpose of further sales.

This method is useful for the manufacturing businesses. They apply this method of depreciation

over the assets like plans, machinery, etc. that are used by the business for the purpose of

producing the goods.

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In this regard, it can be evaluated that there are some methods of depreciation that can be

used by a business organisation for the purpose of charging depreciation over its fixed assets.

Each method is useful for different purposes. Therefore, a company should choose the method of

depreciation on the basis of the nature and use of the assets.

E) Difference between financial statements prepared by Sole trader and a limited company

Basis Sole trader Limited company

Capital account Capital account of the sole trader

includes only owner's equity.

Capital account of a limited

company is inclusion of share

capital, retained earningearnings

and capital reserve.

Tax The tax is calculated on the income

of the sole trader.

Tax of limited company is

calculated on the income of the

company due to the principle of

separate legal entity.

Auditing These financial statements are not

required to be audited.

Financial statements of the limited

company needs to be audited after

a certain time (Miller and Hadley,

2016).

Application of

principles

Sole trader does not required to

prepare their financial statements

on the basis of any principle, rule

or accounting standards.

Limited company need to comply

with the accounting standards,

principles and rules applicable on

it.

CLIENT 3

A) Purpose of bank reconciliation statements

Bank reconciliation statements are prepared for matching the records of bank and

company's records of bank transactions. While preparing the financial statements, in case the

bank statement of Burcu does not comply with the transactions recorded in its books, it would

need to prepare this statement as to determine the area that are causing the difference to eliminate

it as well.

18

used by a business organisation for the purpose of charging depreciation over its fixed assets.

Each method is useful for different purposes. Therefore, a company should choose the method of

depreciation on the basis of the nature and use of the assets.

E) Difference between financial statements prepared by Sole trader and a limited company

Basis Sole trader Limited company

Capital account Capital account of the sole trader

includes only owner's equity.

Capital account of a limited

company is inclusion of share

capital, retained earningearnings

and capital reserve.

Tax The tax is calculated on the income

of the sole trader.

Tax of limited company is

calculated on the income of the

company due to the principle of

separate legal entity.

Auditing These financial statements are not

required to be audited.

Financial statements of the limited

company needs to be audited after

a certain time (Miller and Hadley,

2016).

Application of

principles

Sole trader does not required to

prepare their financial statements

on the basis of any principle, rule

or accounting standards.

Limited company need to comply

with the accounting standards,

principles and rules applicable on

it.

CLIENT 3

A) Purpose of bank reconciliation statements

Bank reconciliation statements are prepared for matching the records of bank and

company's records of bank transactions. While preparing the financial statements, in case the

bank statement of Burcu does not comply with the transactions recorded in its books, it would

need to prepare this statement as to determine the area that are causing the difference to eliminate

it as well.

18

B) Areas that may cause he variation in bank records and company's records

There are many areas due to which the bank statement may vary from the company's

records. The main reasons behind it are:

Any cheque given by the company but not presented in the bank (Reasons for Preparing

Bank Reconciliation Statement, 2019).

Any cheque dishonoured but not known to company.

Any fee charged by bank but not recorded by business, etc.

C) Imprest system

It is the system in which a fixed amount is reserved by company which is remain inactive

at a fixed amount (Lehne and Koelsch, 2015). When the amount of petty cash is spent, the same

amount is again added to the petty cash in this system.

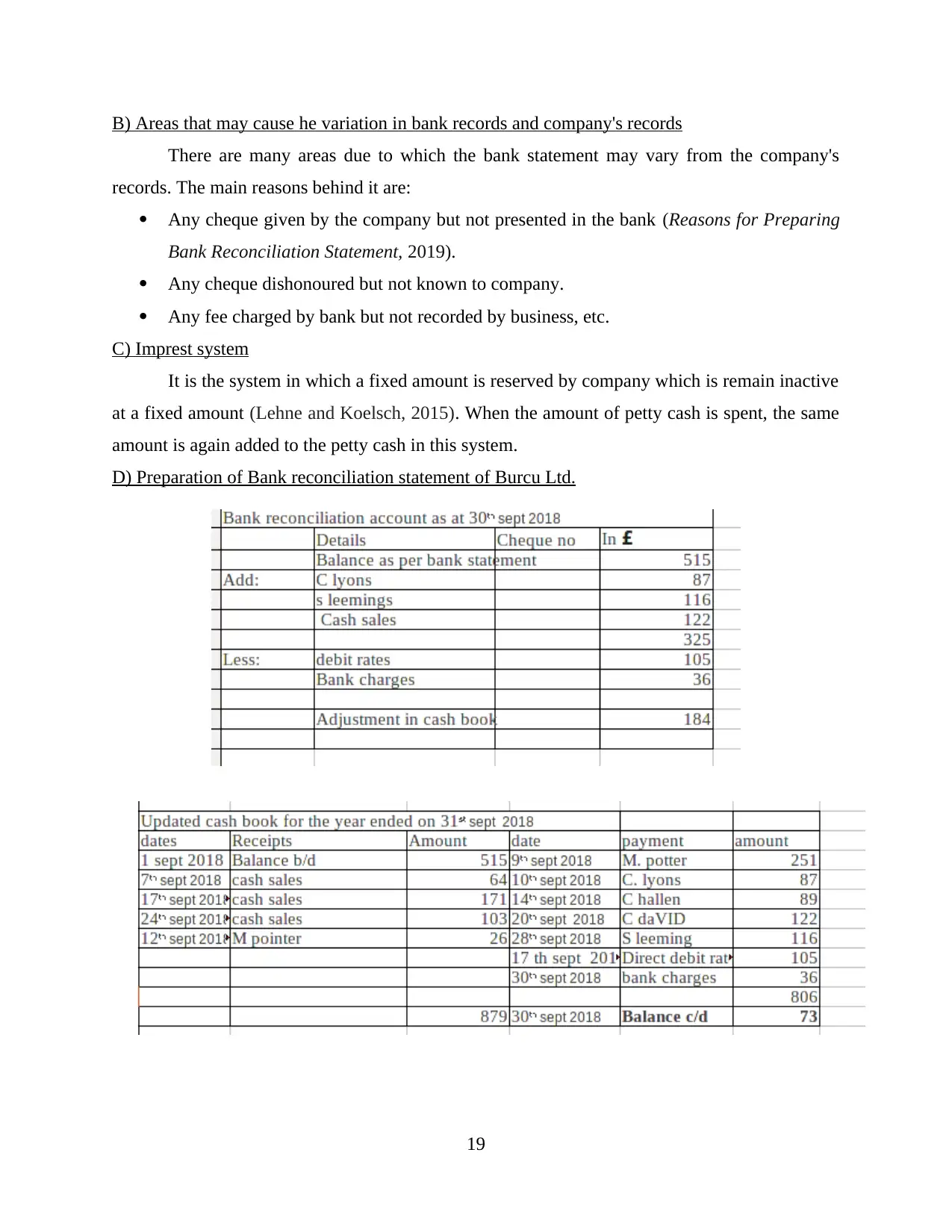

D) Preparation of Bank reconciliation statement of Burcu Ltd.

19

There are many areas due to which the bank statement may vary from the company's

records. The main reasons behind it are:

Any cheque given by the company but not presented in the bank (Reasons for Preparing

Bank Reconciliation Statement, 2019).

Any cheque dishonoured but not known to company.

Any fee charged by bank but not recorded by business, etc.

C) Imprest system

It is the system in which a fixed amount is reserved by company which is remain inactive

at a fixed amount (Lehne and Koelsch, 2015). When the amount of petty cash is spent, the same

amount is again added to the petty cash in this system.

D) Preparation of Bank reconciliation statement of Burcu Ltd.

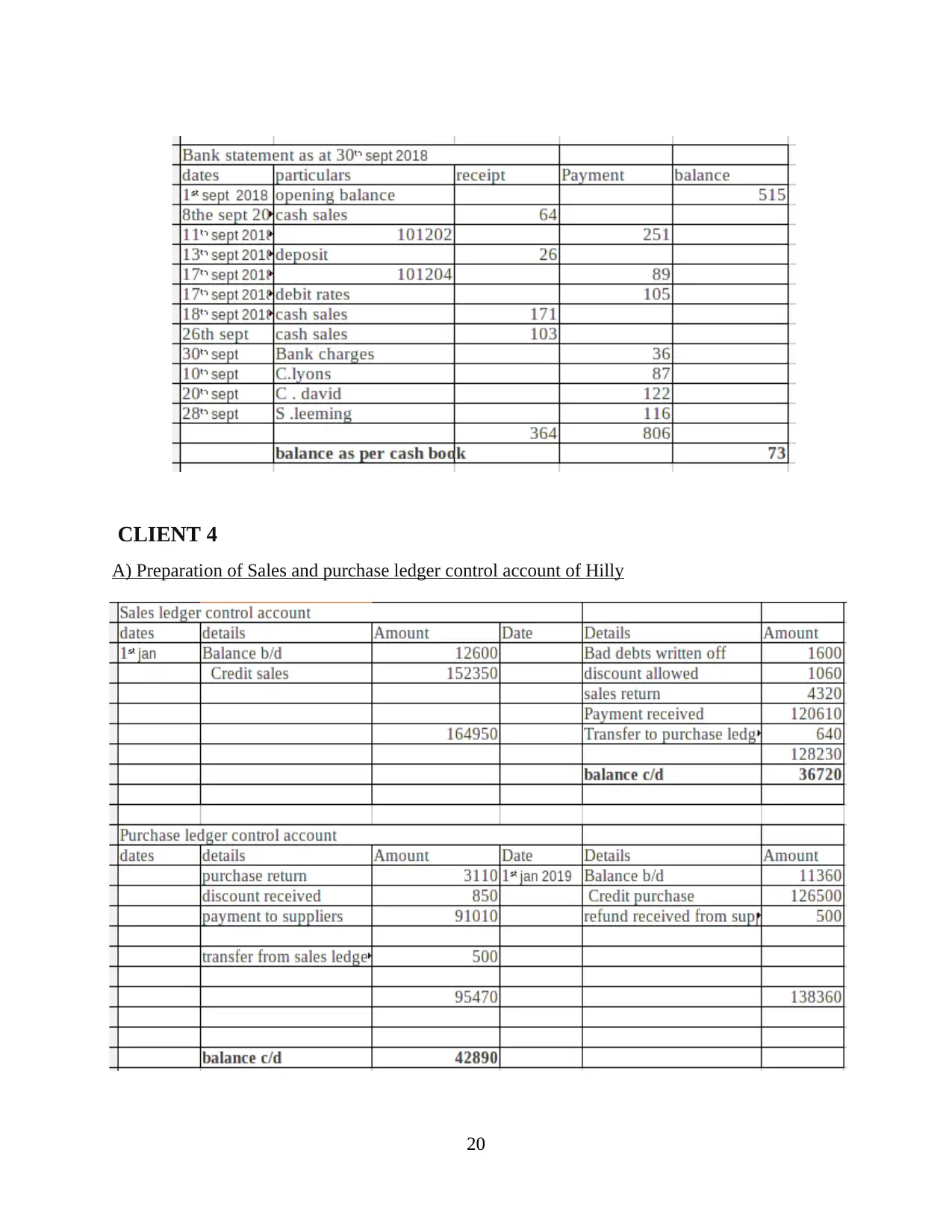

19

CLIENT 4

A) Preparation of Sales and purchase ledger control account of Hilly

20

A) Preparation of Sales and purchase ledger control account of Hilly

20

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

B) Control account

Control account is a general ledger account that contains the summary details of all the

transactions. It helps the business in preparing financial accounts free from any summarized

details. These are prepared by large level of businesses that make large amount of transactions in

a specific period.

CLIENT 5

A) Suspense accounts and its main features

Suspense account is that account which is prepared by a business organisation on a

temporary basis. Organisation records those transactions that are not identifieds by the company

and are also affecting the preparation of financial statements of the company. For example, if

the business has purchased any assets and failed to record in anywhere in the books, the

transaction is quite difficult to be identified (Jayaram, Abidi and Mandell, 2018). In this case, the

business can prepare the suspense account to match the difference in the financial statements

arisen due to this failure.

Features:

Suspense account is a general ledger account and kept by the company on a temporary

basis.

It is recorded in the books under the head current assets.

Commonly the suspense account is prepared for the account receivables and payables.

21

Control account is a general ledger account that contains the summary details of all the

transactions. It helps the business in preparing financial accounts free from any summarized

details. These are prepared by large level of businesses that make large amount of transactions in

a specific period.

CLIENT 5

A) Suspense accounts and its main features

Suspense account is that account which is prepared by a business organisation on a

temporary basis. Organisation records those transactions that are not identifieds by the company

and are also affecting the preparation of financial statements of the company. For example, if

the business has purchased any assets and failed to record in anywhere in the books, the

transaction is quite difficult to be identified (Jayaram, Abidi and Mandell, 2018). In this case, the

business can prepare the suspense account to match the difference in the financial statements

arisen due to this failure.

Features:

Suspense account is a general ledger account and kept by the company on a temporary

basis.

It is recorded in the books under the head current assets.

Commonly the suspense account is prepared for the account receivables and payables.

21

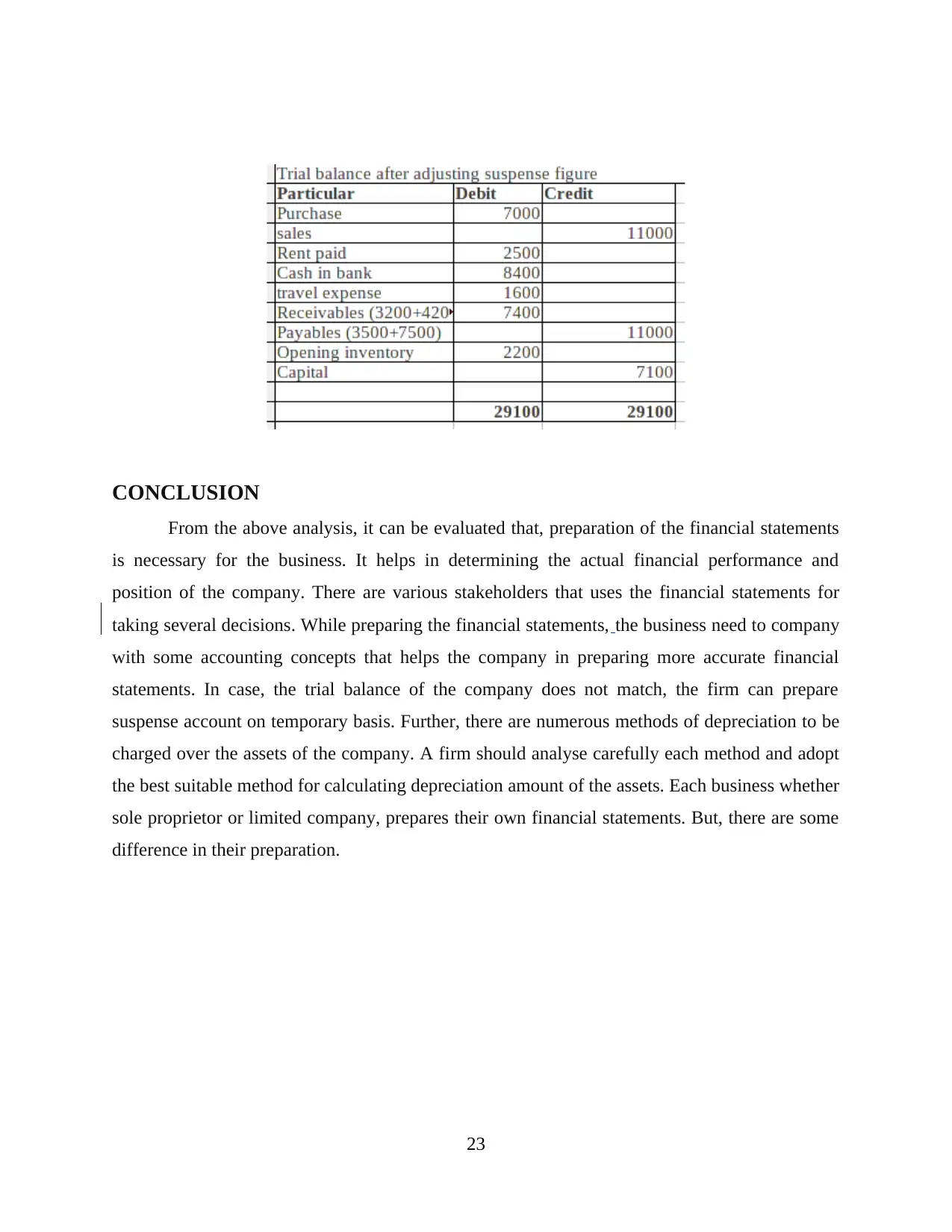

It helps in eliminating the variation in the trial balance of the company.

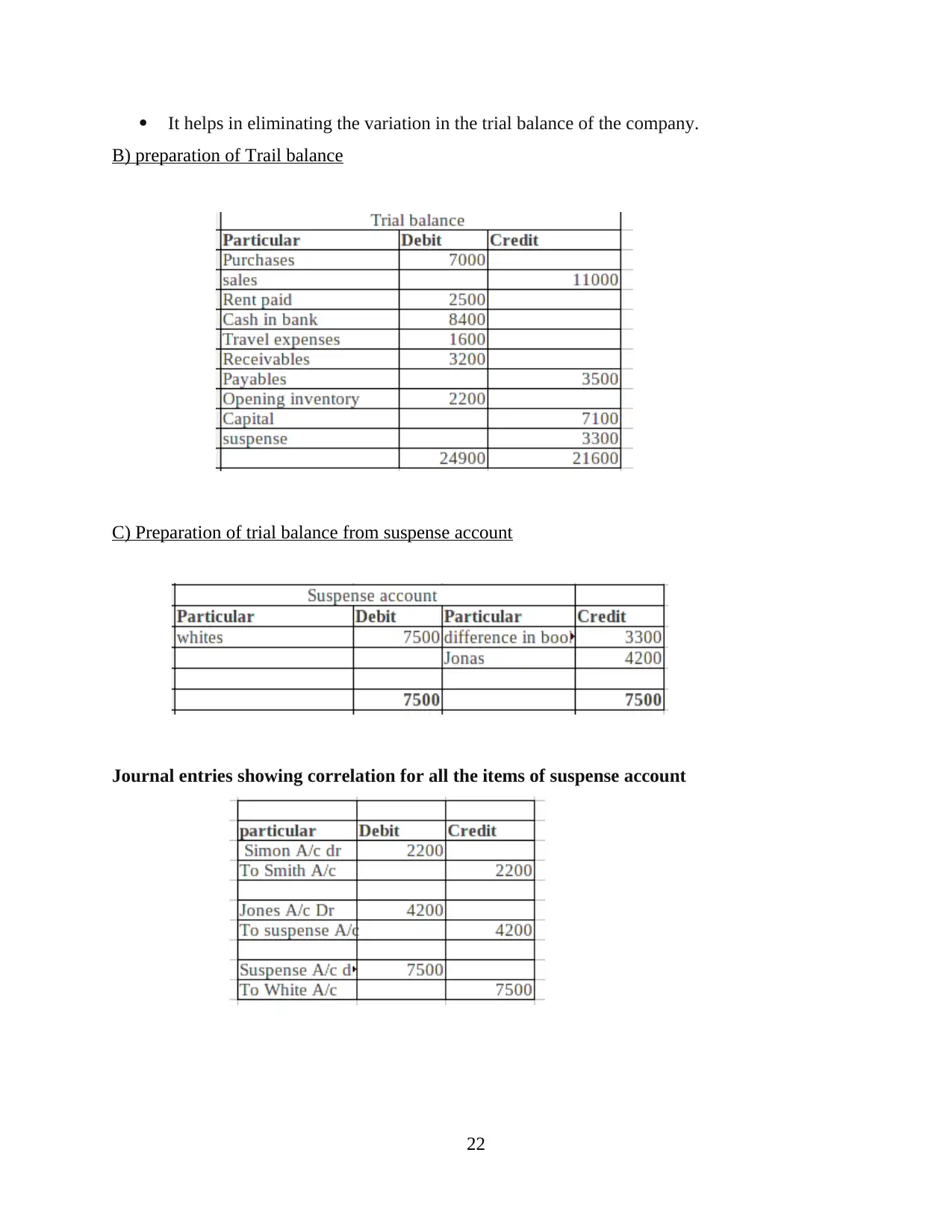

B) preparation of Trail balance

C) Preparation of trial balance from suspense account

Journal entries showing correlation for all the items of suspense account

22

B) preparation of Trail balance

C) Preparation of trial balance from suspense account

Journal entries showing correlation for all the items of suspense account

22

CONCLUSION

From the above analysis, it can be evaluated that, preparation of the financial statements

is necessary for the business. It helps in determining the actual financial performance and

position of the company. There are various stakeholders that uses the financial statements for

taking several decisions. While preparing the financial statements, the business need to company

with some accounting concepts that helps the company in preparing more accurate financial

statements. In case, the trial balance of the company does not match, the firm can prepare

suspense account on temporary basis. Further, there are numerous methods of depreciation to be

charged over the assets of the company. A firm should analyse carefully each method and adopt

the best suitable method for calculating depreciation amount of the assets. Each business whether

sole proprietor or limited company, prepares their own financial statements. But, there are some

difference in their preparation.

23

From the above analysis, it can be evaluated that, preparation of the financial statements

is necessary for the business. It helps in determining the actual financial performance and

position of the company. There are various stakeholders that uses the financial statements for

taking several decisions. While preparing the financial statements, the business need to company

with some accounting concepts that helps the company in preparing more accurate financial

statements. In case, the trial balance of the company does not match, the firm can prepare

suspense account on temporary basis. Further, there are numerous methods of depreciation to be

charged over the assets of the company. A firm should analyse carefully each method and adopt

the best suitable method for calculating depreciation amount of the assets. Each business whether

sole proprietor or limited company, prepares their own financial statements. But, there are some

difference in their preparation.

23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Agyei-Mensah, B. K., 2016. Accountability and internal control in religious organisations: a

study of Methodist church Ghana. African Journal of Accounting, Auditing and

Finance. 5(2). pp.95-112.

Barker, R., 2015. Conservatism, prudence and the IASB's conceptual framework. Accounting

and Business Research, 45(4), pp.514-538.

Del Giudice, V., Manganelli, B. and De Paola, P., 2016, July. Depreciation methods for firm’s

assets. In International Conference on Computational Science and Its Applications(pp.

214-227). Springer, Cham.

Elliott, R. A., Lee, C. Y. and Hussainy, S. Y., 2016. Evaluation of a hybrid paper–electronic

medication management system at a residential aged care facility. Australian Health

Review. 40(3). pp.244-250.

Henderson, S. and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Jayaram, A., Abidi, M. T. and Mandell, D. C., Baton Systems Inc, 2018. Time stamping systems

and methods. U.S. Patent Application 15/957,871.

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2016. Intermediate Accounting, Binder Ready

Version. John Wiley & Sons.

Lehne, M. and Koelsch, S., 2015. Toward a general psychological model of tension and

suspense. Frontiers in Psychology. 6. p.79.

Liapis, K. J. and Kantianis, D. D., 2015. Depreciation methods and life-cycle costing (LCC)

methodology. Procedia Economics and Finance. 19. pp.314-324.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Miller, M. and Hadley, S., 2016. Cash management in cash-constrained environments.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Nudurupati, S.S. and et.al., 2015. Strategic sourcing with multi-stakeholders through value co-

creation: An evidence from global health care company. International Journal of

Production Economics. 166. pp.248-257.

Oulasvirta, L., 2016. Accounting Principles. Global Encyclopedia of Public Administration,

Public Policy, and Governance, pp.1-9.

Qian, C. and et.al., 2016. An accelerated test method of luminous flux depreciation for LED

luminaires and lamps. Reliability Engineering & System Safety. 147. pp.84-92.

Online

The purpose of financial statements. 2018. [Online] Available Through:

<https://www.accountingtools.com/articles/what-is-the-purpose-of-financial-

statements.html>

24

Books and Journals

Agyei-Mensah, B. K., 2016. Accountability and internal control in religious organisations: a

study of Methodist church Ghana. African Journal of Accounting, Auditing and

Finance. 5(2). pp.95-112.

Barker, R., 2015. Conservatism, prudence and the IASB's conceptual framework. Accounting

and Business Research, 45(4), pp.514-538.

Del Giudice, V., Manganelli, B. and De Paola, P., 2016, July. Depreciation methods for firm’s

assets. In International Conference on Computational Science and Its Applications(pp.

214-227). Springer, Cham.

Elliott, R. A., Lee, C. Y. and Hussainy, S. Y., 2016. Evaluation of a hybrid paper–electronic

medication management system at a residential aged care facility. Australian Health

Review. 40(3). pp.244-250.

Henderson, S. and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Jayaram, A., Abidi, M. T. and Mandell, D. C., Baton Systems Inc, 2018. Time stamping systems

and methods. U.S. Patent Application 15/957,871.

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2016. Intermediate Accounting, Binder Ready

Version. John Wiley & Sons.

Lehne, M. and Koelsch, S., 2015. Toward a general psychological model of tension and

suspense. Frontiers in Psychology. 6. p.79.

Liapis, K. J. and Kantianis, D. D., 2015. Depreciation methods and life-cycle costing (LCC)

methodology. Procedia Economics and Finance. 19. pp.314-324.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Miller, M. and Hadley, S., 2016. Cash management in cash-constrained environments.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Nudurupati, S.S. and et.al., 2015. Strategic sourcing with multi-stakeholders through value co-

creation: An evidence from global health care company. International Journal of

Production Economics. 166. pp.248-257.

Oulasvirta, L., 2016. Accounting Principles. Global Encyclopedia of Public Administration,

Public Policy, and Governance, pp.1-9.

Qian, C. and et.al., 2016. An accelerated test method of luminous flux depreciation for LED

luminaires and lamps. Reliability Engineering & System Safety. 147. pp.84-92.

Online

The purpose of financial statements. 2018. [Online] Available Through:

<https://www.accountingtools.com/articles/what-is-the-purpose-of-financial-

statements.html>

24

Reasons for Preparing Bank Reconciliation Statement. 2019. [Online] Available Through:

<http://aristotleconsultancy.com/blog/reasons-preparing-bank-reconciliation-statement/>

25

<http://aristotleconsultancy.com/blog/reasons-preparing-bank-reconciliation-statement/>

25

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.