Financial Accounting Report for Junior Accountant at PH Accountancy

VerifiedAdded on 2020/12/09

|27

|4352

|449

Report

AI Summary

This report, prepared by a junior accountant for PH Accountancy, provides a comprehensive overview of financial accounting principles and practices. It begins with an introduction to financial accounting, its purpose, and the preparation of financial statements. The report details the roles of internal and external stakeholders, including owners, management, customers, suppliers, creditors, and the government. It then moves on to practical applications, including recording transactions, preparing profit and loss statements, and creating statements of financial position for various clients like Munteanu Ltd. The report further explains key accounting concepts such as consistency, along with the purpose and methods of depreciation. It also covers bank reconciliation statements, sales and purchase ledger control accounts, suspense accounts, and the preparation of trial balances. The report concludes by emphasizing the importance of accurate financial reporting for decision-making and compliance.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

REPORT TO LINE MANAGERS..................................................................................................1

1. Financial accounting and its purpose......................................................................................1

2. Internal and external stockholders of the company.................................................................3

CLIENT 1........................................................................................................................................6

Recording transactions in the books of Alexender.....................................................................6

CLIENT 2........................................................................................................................................6

A) preparation of profit and loss statement of Munteanu Ltd.....................................................6

B) statement of financial position of the Manuteanu Ltd...........................................................8

C) Explanation of the accounting concepts ................................................................................8

D) Purpose of depreciation and its methods in formulation of accounting statements...............9

E) Difference between financial statements prepared by Sole trader and a limited company..11

CLIENT 3......................................................................................................................................11

A) Purpose of bank reconciliation statements...........................................................................11

B) Areas that may cause he variation in bank records and company's records.........................12

C) Imprest system.....................................................................................................................12

D) Preparation of Bank reconciliation statement of Burcu Ltd................................................12

CLIENT 4.....................................................................................................................................13

A) Preparation of Sales and purchase ledger control account of Hilly.....................................13

B) Control account....................................................................................................................14

CLIENT 5......................................................................................................................................14

A) Suspense accounts and its main features.............................................................................14

B) preparation of Trail balance.................................................................................................15

C) Preparation of trial balance from suspense account.............................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

REPORT TO LINE MANAGERS..................................................................................................1

1. Financial accounting and its purpose......................................................................................1

2. Internal and external stockholders of the company.................................................................3

CLIENT 1........................................................................................................................................6

Recording transactions in the books of Alexender.....................................................................6

CLIENT 2........................................................................................................................................6

A) preparation of profit and loss statement of Munteanu Ltd.....................................................6

B) statement of financial position of the Manuteanu Ltd...........................................................8

C) Explanation of the accounting concepts ................................................................................8

D) Purpose of depreciation and its methods in formulation of accounting statements...............9

E) Difference between financial statements prepared by Sole trader and a limited company..11

CLIENT 3......................................................................................................................................11

A) Purpose of bank reconciliation statements...........................................................................11

B) Areas that may cause he variation in bank records and company's records.........................12

C) Imprest system.....................................................................................................................12

D) Preparation of Bank reconciliation statement of Burcu Ltd................................................12

CLIENT 4.....................................................................................................................................13

A) Preparation of Sales and purchase ledger control account of Hilly.....................................13

B) Control account....................................................................................................................14

CLIENT 5......................................................................................................................................14

A) Suspense accounts and its main features.............................................................................14

B) preparation of Trail balance.................................................................................................15

C) Preparation of trial balance from suspense account.............................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Financial accounting is a system of accounting that includes all the financial informations

of the a company. It a process of recording all the financial transactions and preparing financial

reports by summarizing all the financial details for the purpose of showing financial condition of

the company during a specific time period. PH Accountancy company is professional service

provider company that was establisheds in the year 1987. Ttoday the company is ranked as the

big four service provider company in the world. The present study shows a report of junior

accountant of the PH Accountancy company to be submitted to its line manager. The report

includes a brief introduction about the meaning and purpose of the financial accounting. It also

shows a detailed discussion about internal and external stakeholder of the company that have

interest in the financial informations of the company. The assignment shows preparation of

financial statements of the sole trader, partnership and limited companies. Further, the present

report also shows preparation of bank reconciliation statement for the purpose of ensuring both

bank and company's records are providing same and accurate results.

REPORT TO LINE MANAGERS

PH Accountancy LTD.

To,

The Line manager,

From, Junior accountant

Subject: for showing principles, roles and conventions of accountnacyaccountancy

1. Financial accounting and its purpose

“Financial accounting system is a branch of accounting system which concerns with

recording and summarizing each financial transaction made by a company during the financial

period or during a specific time.”

Financial accounting includes preparation of income statement, balance sheet and bank

reconciliation statements, etc. that helps the business in showing its actual financial position

(Henderson, 2015). While preparing these statements, the accountant uses specific guidelines,

methods and process of the financial accounting system.

PH Accountancy needs to prepare the financial statements of the company so that it can

provide all the relevant informations to the interested parties of the company. Further,

preparation of financial reports can also help its managers and board members in determining

1

Financial accounting is a system of accounting that includes all the financial informations

of the a company. It a process of recording all the financial transactions and preparing financial

reports by summarizing all the financial details for the purpose of showing financial condition of

the company during a specific time period. PH Accountancy company is professional service

provider company that was establisheds in the year 1987. Ttoday the company is ranked as the

big four service provider company in the world. The present study shows a report of junior

accountant of the PH Accountancy company to be submitted to its line manager. The report

includes a brief introduction about the meaning and purpose of the financial accounting. It also

shows a detailed discussion about internal and external stakeholder of the company that have

interest in the financial informations of the company. The assignment shows preparation of

financial statements of the sole trader, partnership and limited companies. Further, the present

report also shows preparation of bank reconciliation statement for the purpose of ensuring both

bank and company's records are providing same and accurate results.

REPORT TO LINE MANAGERS

PH Accountancy LTD.

To,

The Line manager,

From, Junior accountant

Subject: for showing principles, roles and conventions of accountnacyaccountancy

1. Financial accounting and its purpose

“Financial accounting system is a branch of accounting system which concerns with

recording and summarizing each financial transaction made by a company during the financial

period or during a specific time.”

Financial accounting includes preparation of income statement, balance sheet and bank

reconciliation statements, etc. that helps the business in showing its actual financial position

(Henderson, 2015). While preparing these statements, the accountant uses specific guidelines,

methods and process of the financial accounting system.

PH Accountancy needs to prepare the financial statements of the company so that it can

provide all the relevant informations to the interested parties of the company. Further,

preparation of financial reports can also help its managers and board members in determining

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the actual position and performance of the company so that they can easily make the appropriate

policies and strategies for its betterment.

Purpose of financial accounting

The main purpose of the whole financial accounting system in PH Accountancy is to

show the actual financial position of it. Further, other objectives of the financial accounting

systems are as follows:

Summarize the financial informations: It is also one of the major objective of the

financial accounting system. In financial accounting system, all the transactions made

by the company during specific time are summarized so that they could be available in a

single set of reports (Macve, 2015). It helps the managers, board of directors and other

interested parties in collecting all the relevant informations of the business that can

affect their interest.

Investment decisions: Shareholders and other investors of the company wants to know

the actual position of the company for the sake of estimating their returns from the

investment made in the company and risk involved with the investment. Financial

accounting reports provides all the relevant informations to the investors to help them in

their decision making.

Existing shareholders: As, the existing shareholders are the real owners of the

company, they need to know each information about the company (Narayanaswamy,

2017). Therefore, providing relevant information to the existing shareholders of the

company is also a main purpose of preparation of financial statements of the company.

Taxation decisions: Financial accounting reports also provides all information to the

Government agencies for the purpose of calculating the amount of taxation tpto be

imposed of the company. They can determine the income earned by the company, assets

and liabilities held by the company, all the investments made by it, etc.

Keeping records: The financial accounting reports are also prepared for the purpose of

recording all the incomes and expenditure of the business. It helps the organisation in

tracking each area where the company is spending its funds. It also provides help to the

managers in observing the financial behaviour of the company.

Ensuring earning: Further, financial reports of the company also helps in determining

the actual income earned by the firm. It shows each income and expenditure made by

2

policies and strategies for its betterment.

Purpose of financial accounting

The main purpose of the whole financial accounting system in PH Accountancy is to

show the actual financial position of it. Further, other objectives of the financial accounting

systems are as follows:

Summarize the financial informations: It is also one of the major objective of the

financial accounting system. In financial accounting system, all the transactions made

by the company during specific time are summarized so that they could be available in a

single set of reports (Macve, 2015). It helps the managers, board of directors and other

interested parties in collecting all the relevant informations of the business that can

affect their interest.

Investment decisions: Shareholders and other investors of the company wants to know

the actual position of the company for the sake of estimating their returns from the

investment made in the company and risk involved with the investment. Financial

accounting reports provides all the relevant informations to the investors to help them in

their decision making.

Existing shareholders: As, the existing shareholders are the real owners of the

company, they need to know each information about the company (Narayanaswamy,

2017). Therefore, providing relevant information to the existing shareholders of the

company is also a main purpose of preparation of financial statements of the company.

Taxation decisions: Financial accounting reports also provides all information to the

Government agencies for the purpose of calculating the amount of taxation tpto be

imposed of the company. They can determine the income earned by the company, assets

and liabilities held by the company, all the investments made by it, etc.

Keeping records: The financial accounting reports are also prepared for the purpose of

recording all the incomes and expenditure of the business. It helps the organisation in

tracking each area where the company is spending its funds. It also provides help to the

managers in observing the financial behaviour of the company.

Ensuring earning: Further, financial reports of the company also helps in determining

the actual income earned by the firm. It shows each income and expenditure made by

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the firm. With the help of these informations, managers and directors can ensure the

actual earning of the firm. In this regard, the financial reports of the firm are also

prepared for the purpose of ensuring the earnings of the business organisation.

Credit decisions: Preparation of financial statements also have a purpose of taking

decision regarding providing credit to the company (Nudurupati, 2015). It helps in

determining the condition of the company for repaying the debts of the company by

observing its balance sheet.

Determination of actual debts and assets: PH accountancy also should prepare each

statements of the financial accounting system as it can help the company in determining

the actual amount of assets and debts held by the company as to determine the actual

position of the business organisation.

Determination of liquidity: It is also a major purpose of the preparation of financial

statements as to determine the liquidity of the firm. It shows the amount of assets held

by the company over the debts.

In this regard, there are several purposes and objectives of preparing financial

accounting reports by a business organisation.

2. Internal and external stockholders of the company

Stakeholders can be defined as the individuals or group of individuals that have interest

in the company. Each action of the company may affect the interest of the stakeholders. From

the above analysis it can be evaluated that there are many individuals and firms that have

interest in the business of PH accountancywhich can be termed as the stakeholders of company

(Kieso, Weygandt and Warfield, 2016). The stakeholders can be divided into two parts i.e.

internal stakeholders and external stakeholders. List of internal and external stakeholders is as

under:

Internal stakeholders:

Internal stakeholders can be defined as the group of individuals that serves the company.

They performs several activities for the company as board members. For example: Owner: Owners are those individuals that have invested the capital amount in the

business. They are the internal stakeholders of the company. In terms of a limited

company, the shareholders can be defined as the true owners of it. They have interest in

the financial informations of the company as they have invested a sum of amount in the

3

actual earning of the firm. In this regard, the financial reports of the firm are also

prepared for the purpose of ensuring the earnings of the business organisation.

Credit decisions: Preparation of financial statements also have a purpose of taking

decision regarding providing credit to the company (Nudurupati, 2015). It helps in

determining the condition of the company for repaying the debts of the company by

observing its balance sheet.

Determination of actual debts and assets: PH accountancy also should prepare each

statements of the financial accounting system as it can help the company in determining

the actual amount of assets and debts held by the company as to determine the actual

position of the business organisation.

Determination of liquidity: It is also a major purpose of the preparation of financial

statements as to determine the liquidity of the firm. It shows the amount of assets held

by the company over the debts.

In this regard, there are several purposes and objectives of preparing financial

accounting reports by a business organisation.

2. Internal and external stockholders of the company

Stakeholders can be defined as the individuals or group of individuals that have interest

in the company. Each action of the company may affect the interest of the stakeholders. From

the above analysis it can be evaluated that there are many individuals and firms that have

interest in the business of PH accountancywhich can be termed as the stakeholders of company

(Kieso, Weygandt and Warfield, 2016). The stakeholders can be divided into two parts i.e.

internal stakeholders and external stakeholders. List of internal and external stakeholders is as

under:

Internal stakeholders:

Internal stakeholders can be defined as the group of individuals that serves the company.

They performs several activities for the company as board members. For example: Owner: Owners are those individuals that have invested the capital amount in the

business. They are the internal stakeholders of the company. In terms of a limited

company, the shareholders can be defined as the true owners of it. They have interest in

the financial informations of the company as they have invested a sum of amount in the

3

company (Barker, 2015). They can also take decision regarding making the further

investment in the : PH accountancy. They takes the decision about investing their fund

in the company by analysing its financial position and evaluating the chances of growth

in the future. Further, the profitability of the company affects their return on the

investment and risk of investment as well.

Management: Management can be defined as a group of professionals appointed by the

PH Accountancy in the firm for making strategies and plans and help the company in

attaining rapid growth in the near future. Managers perform their task in the business to

enhance the efficiency of its operations. The performance of the business shows the

efficiency of overall business in performing the business operations. There fore,

management also have interest in the financial statements of the company as with the

help of it managers can determine the efficiency and effectiveness of working of the

business organisation.

External shareholders:

External stakeholders are those individuals that have not invested their money in

the company, but they have some sort of interest in the business. For example: Customers: Customers do not invest their money into the business. But, their interest in

the product of a specific brand get affected by the financial performance of the

company (Oulasvirta, 2016). if a company is suffering loss frequently, it may loose its

customers due it. Suppliers: Suppliers are those individuals or organisations who supplies raw material to

the company. A business organisation purchases a large amount of raw materials or

goods for the purpose of further sale. Suppliers needs financial records of the company

as to determine the risk involved in providing further credits to the company. Creditors: Creditors can be bank, individuals, financial institutions which have provided

credit to the firm. Creditors needs to determine the actual financial position of the

company for the purpose of taking decisions regarding providing credit to the company

by evaluating the risk involved in the decision and condition of the company for the

repayment.

Government: Government agencies are also interested in the financial informations of

the company for many reasons. For example, for the purpose of determining the amount

4

investment in the : PH accountancy. They takes the decision about investing their fund

in the company by analysing its financial position and evaluating the chances of growth

in the future. Further, the profitability of the company affects their return on the

investment and risk of investment as well.

Management: Management can be defined as a group of professionals appointed by the

PH Accountancy in the firm for making strategies and plans and help the company in

attaining rapid growth in the near future. Managers perform their task in the business to

enhance the efficiency of its operations. The performance of the business shows the

efficiency of overall business in performing the business operations. There fore,

management also have interest in the financial statements of the company as with the

help of it managers can determine the efficiency and effectiveness of working of the

business organisation.

External shareholders:

External stakeholders are those individuals that have not invested their money in

the company, but they have some sort of interest in the business. For example: Customers: Customers do not invest their money into the business. But, their interest in

the product of a specific brand get affected by the financial performance of the

company (Oulasvirta, 2016). if a company is suffering loss frequently, it may loose its

customers due it. Suppliers: Suppliers are those individuals or organisations who supplies raw material to

the company. A business organisation purchases a large amount of raw materials or

goods for the purpose of further sale. Suppliers needs financial records of the company

as to determine the risk involved in providing further credits to the company. Creditors: Creditors can be bank, individuals, financial institutions which have provided

credit to the firm. Creditors needs to determine the actual financial position of the

company for the purpose of taking decisions regarding providing credit to the company

by evaluating the risk involved in the decision and condition of the company for the

repayment.

Government: Government agencies are also interested in the financial informations of

the company for many reasons. For example, for the purpose of determining the amount

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to be collected from company as corporate tax, for taking decisions regarding providing

grants to the company, for determining compliance of regulations while preparing

financial position of the company, etc.

In this order, it can be analysed that, both internal and external stakeholders of a large

business have interest in the financial informations of the company.

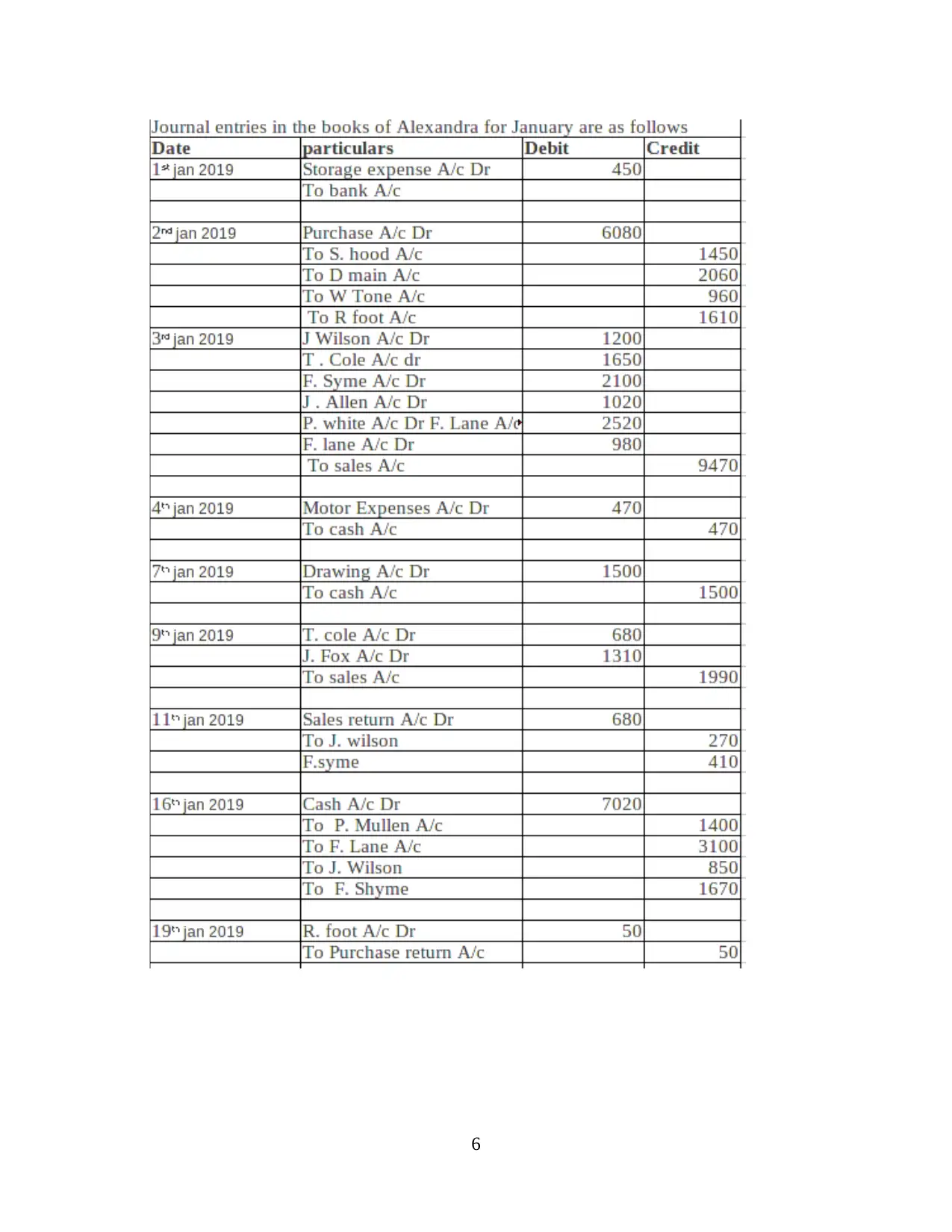

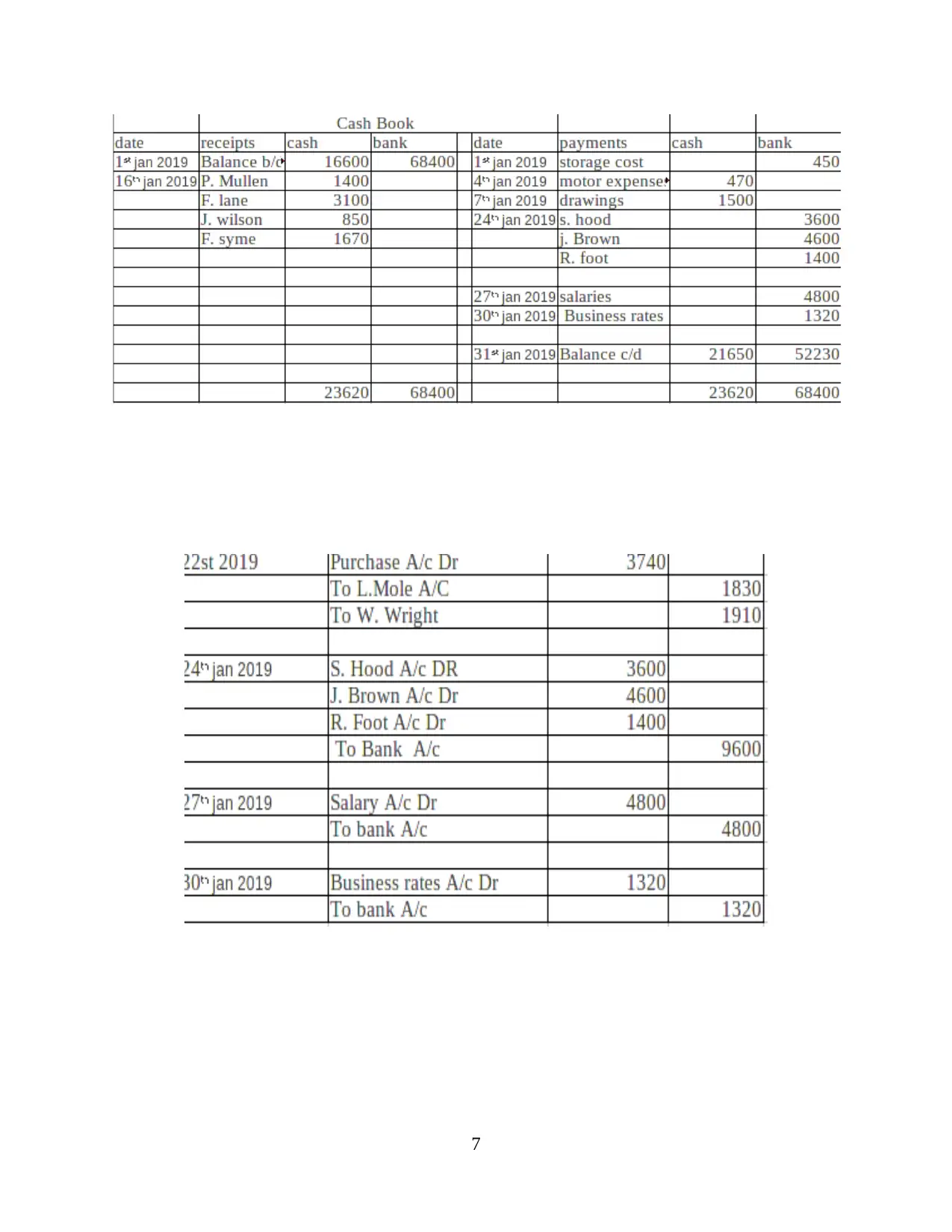

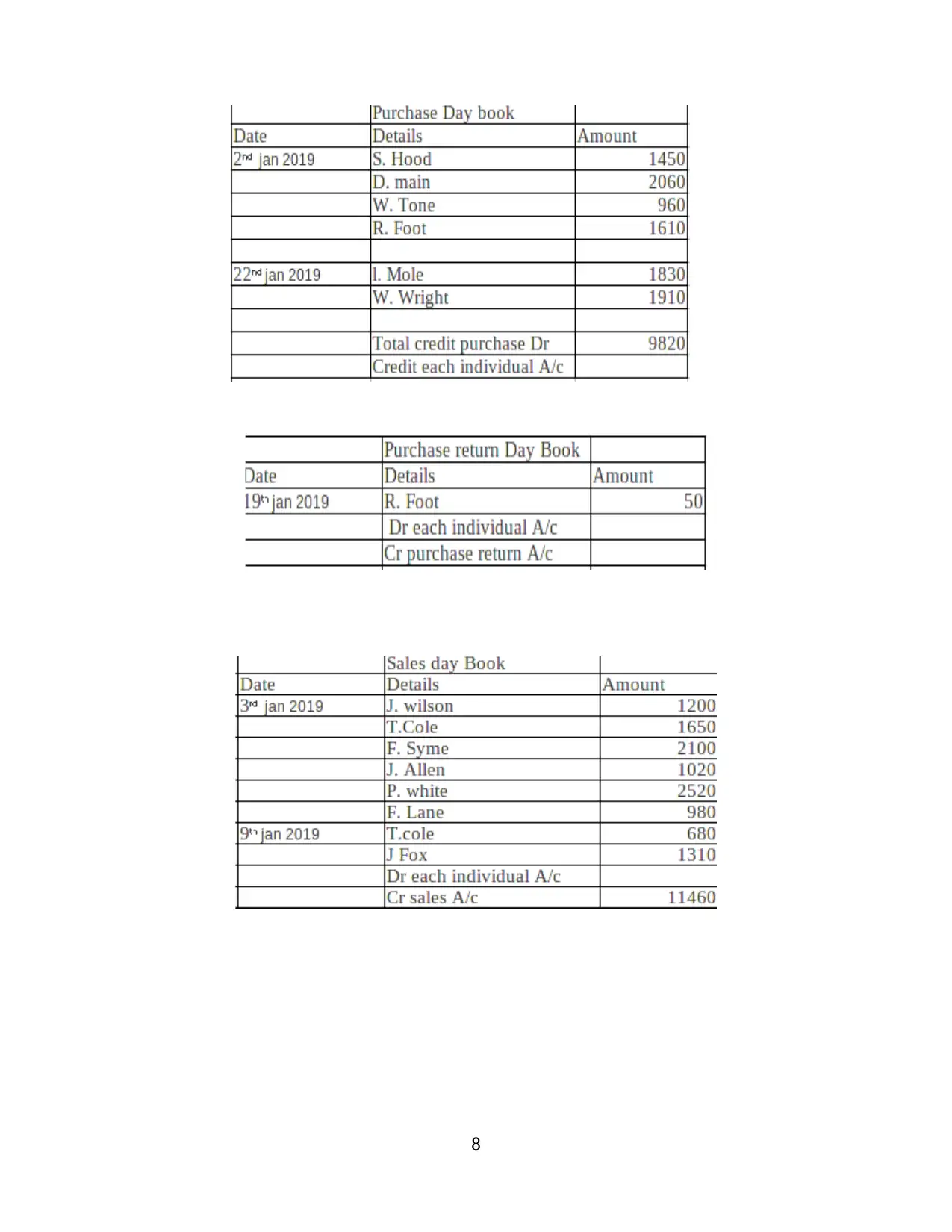

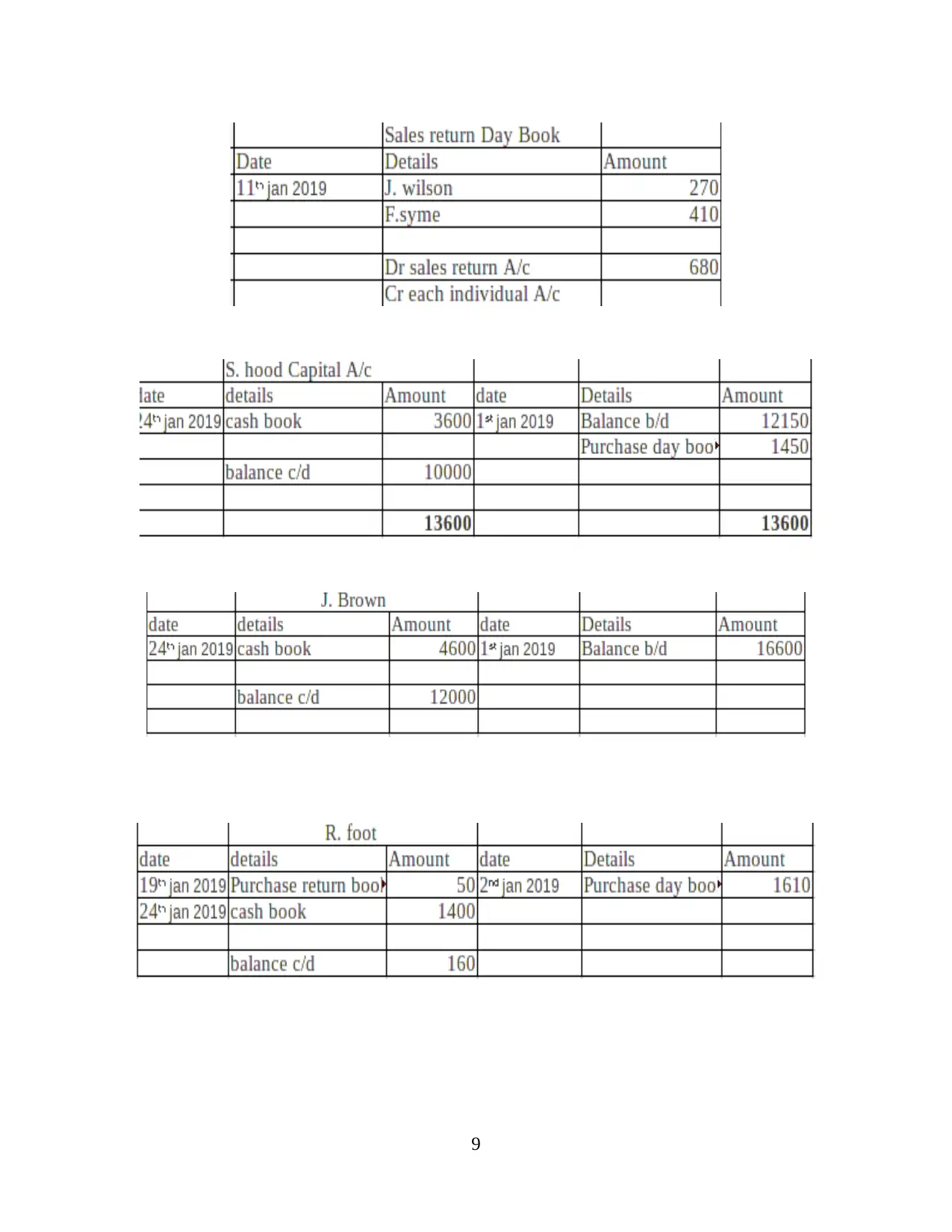

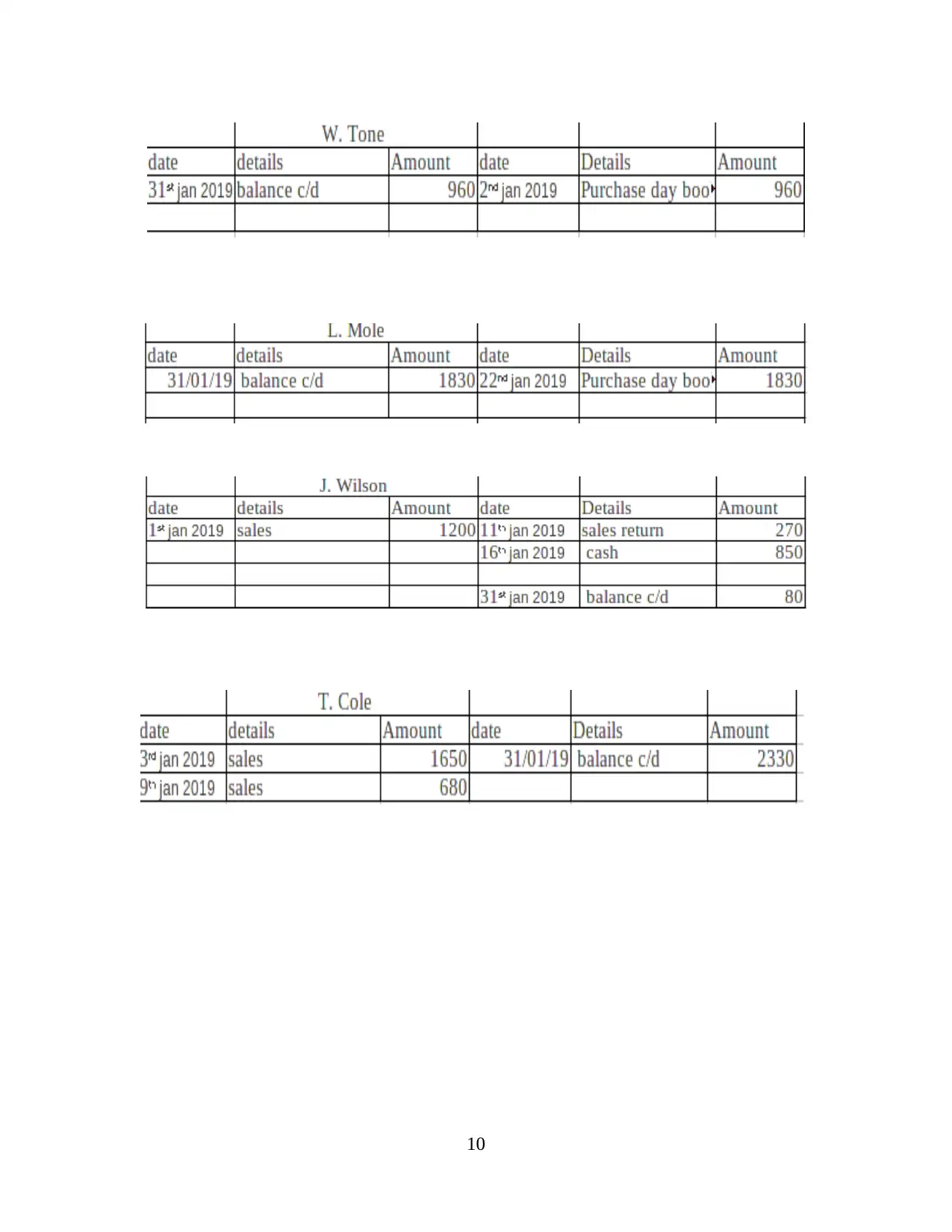

CLIENT 1

Recording transactions in the books of Alexender

5

grants to the company, for determining compliance of regulations while preparing

financial position of the company, etc.

In this order, it can be analysed that, both internal and external stakeholders of a large

business have interest in the financial informations of the company.

CLIENT 1

Recording transactions in the books of Alexender

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.