Financial Accounting Principles: Stakeholders and Reporting Analysis

VerifiedAdded on 2021/02/19

|26

|4897

|64

Report

AI Summary

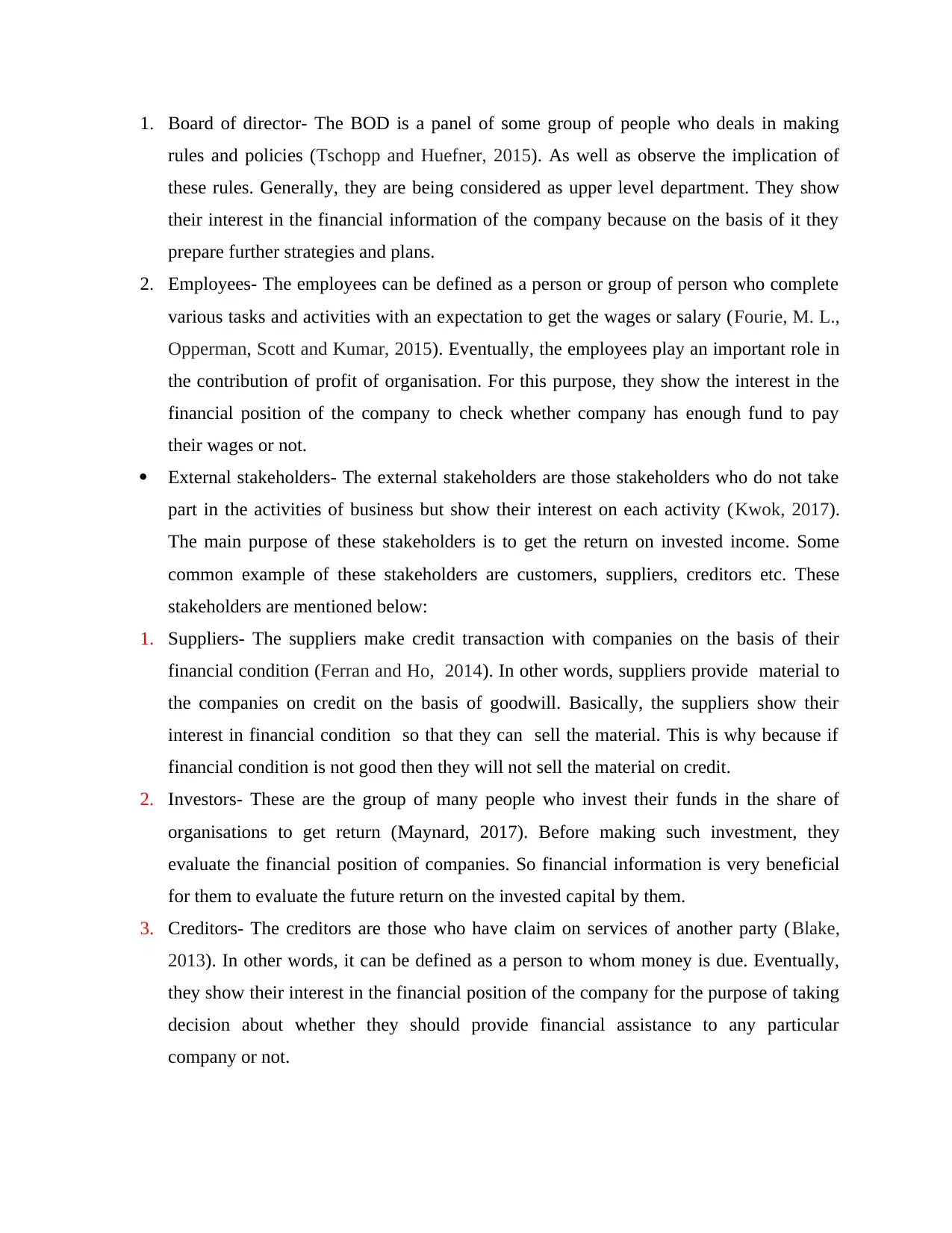

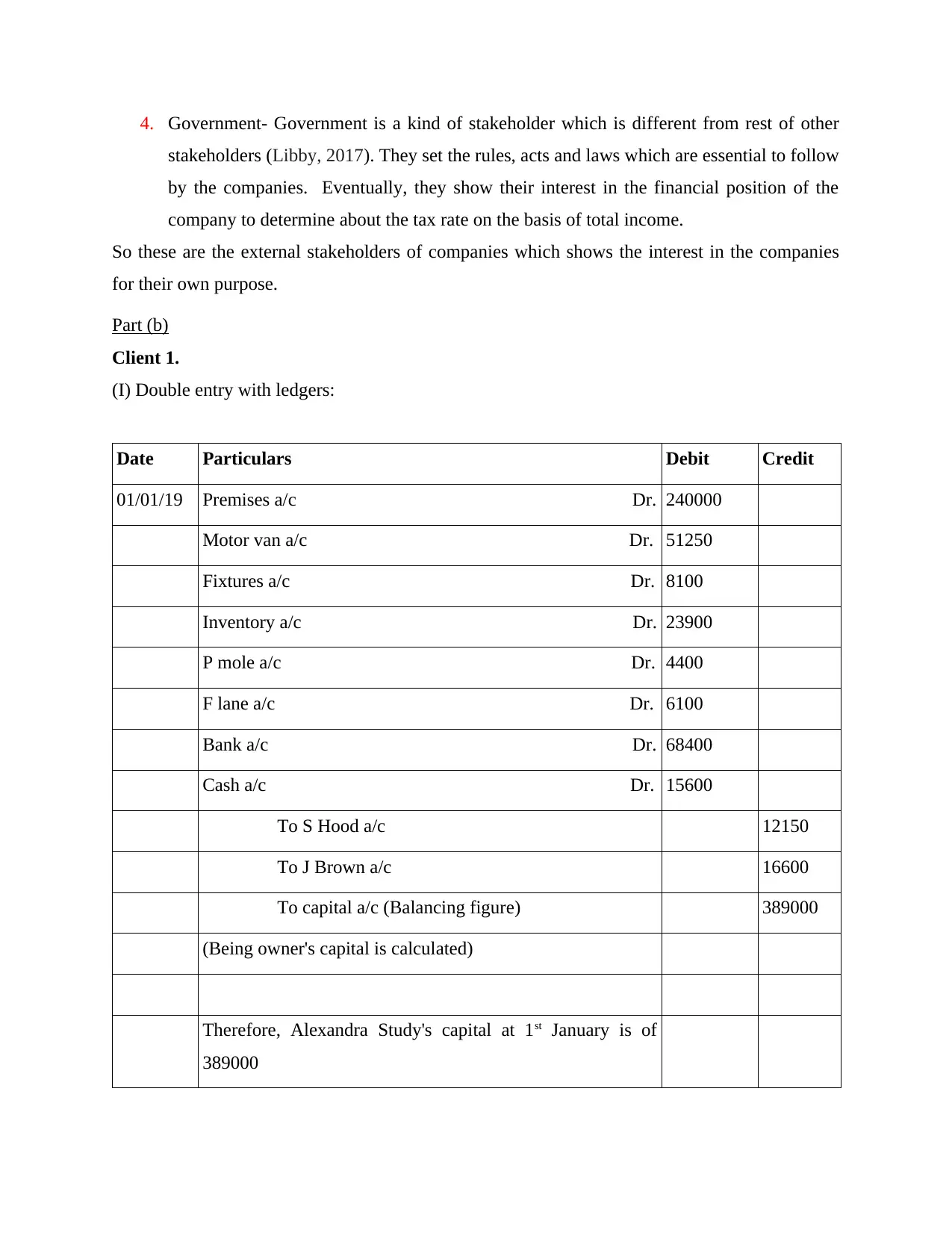

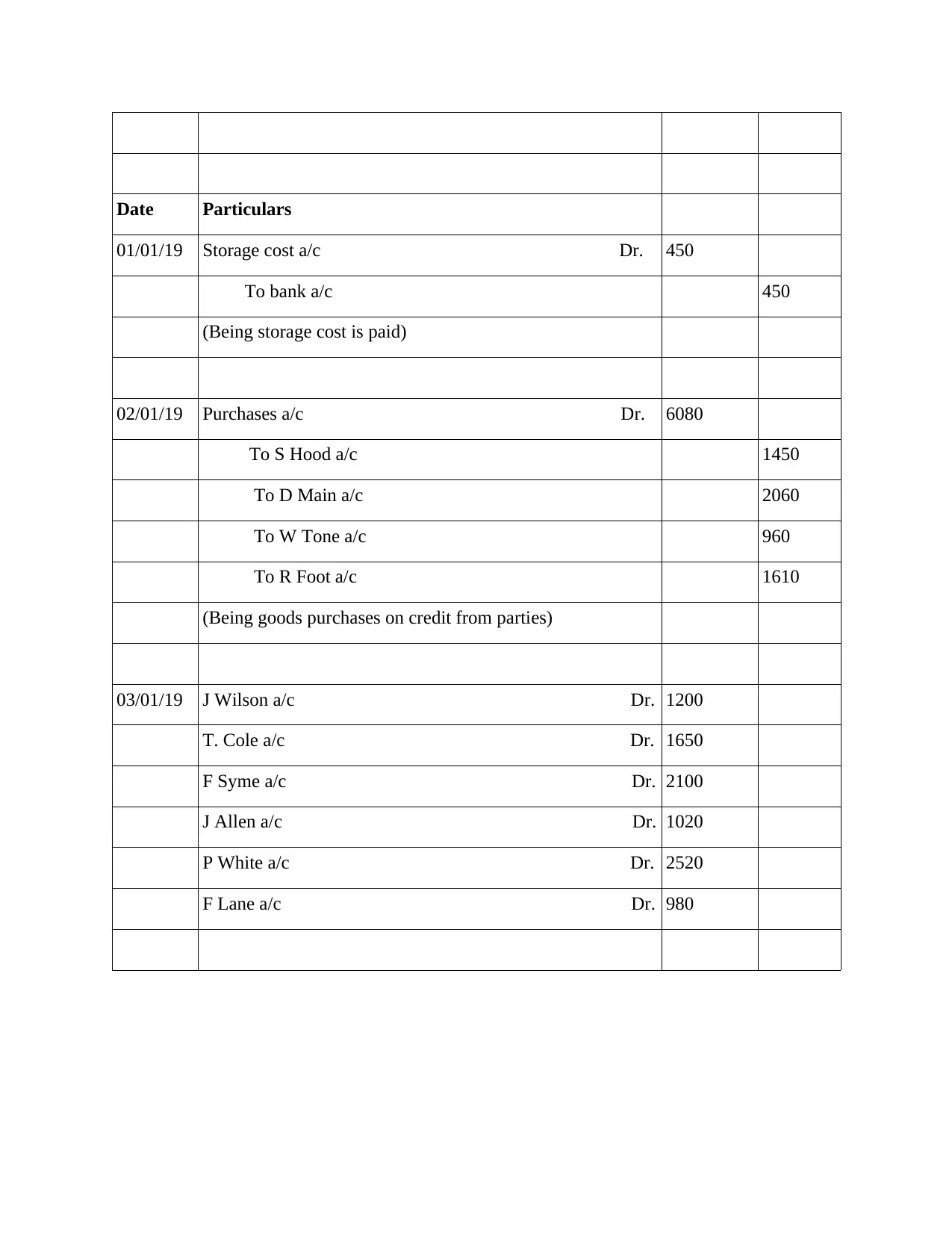

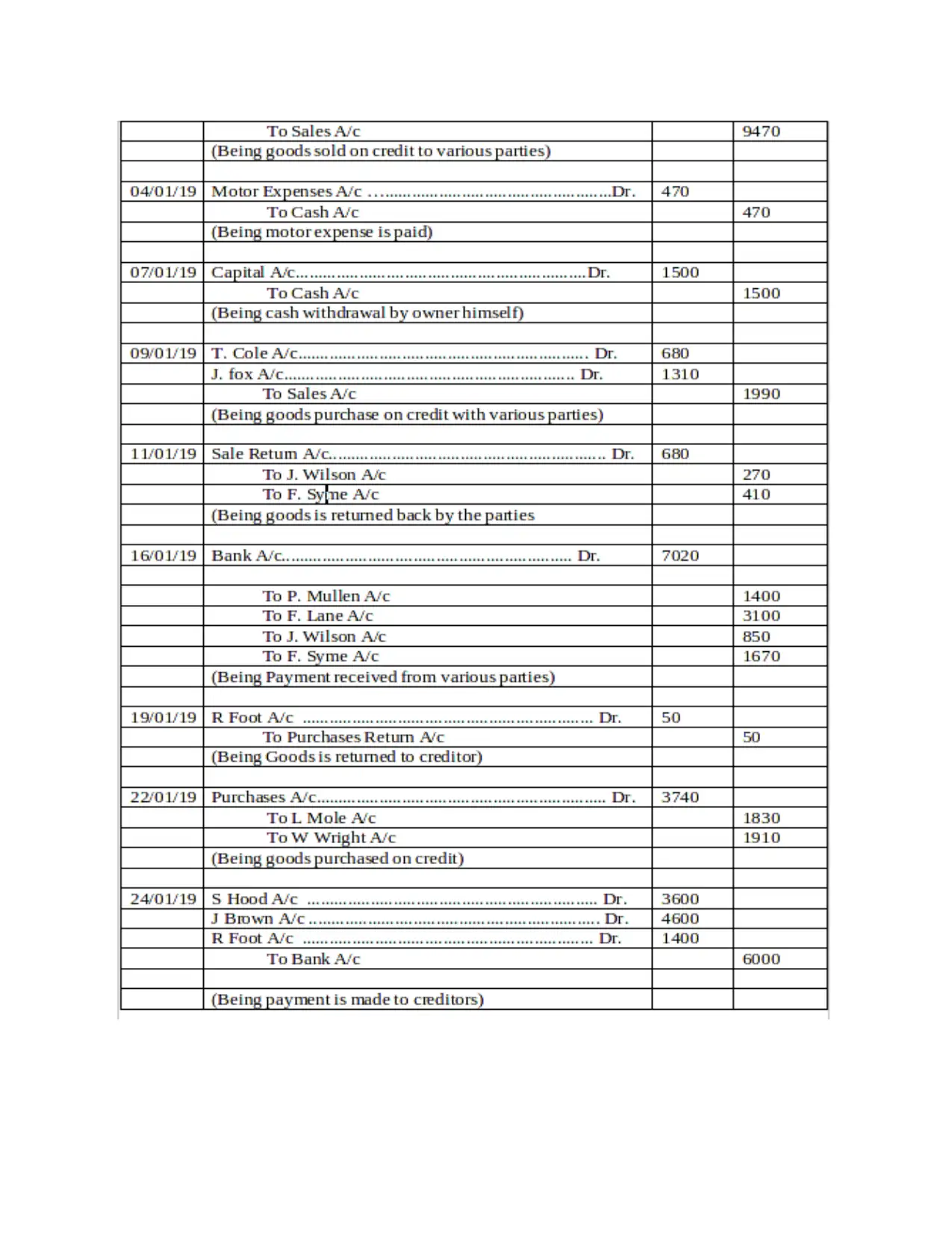

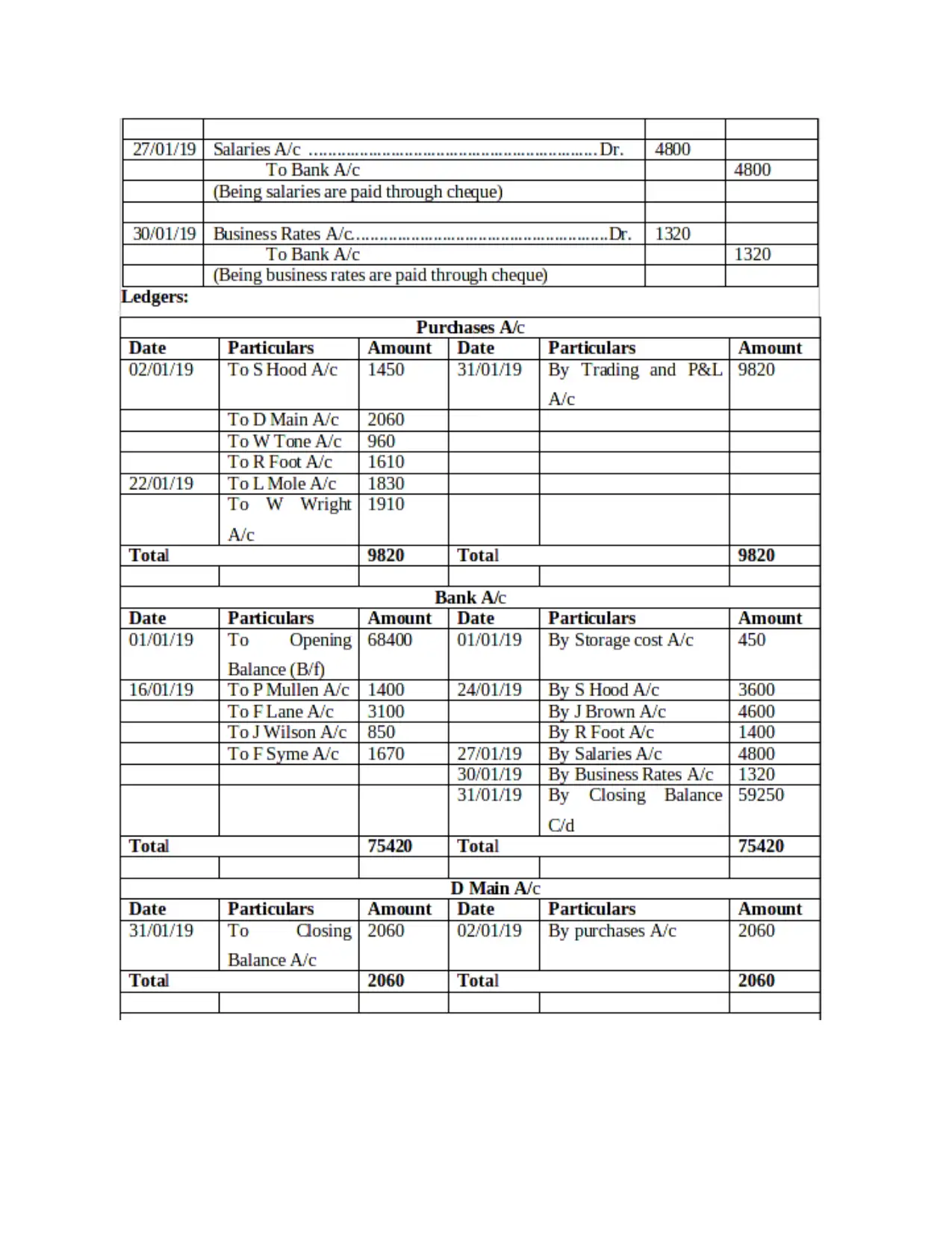

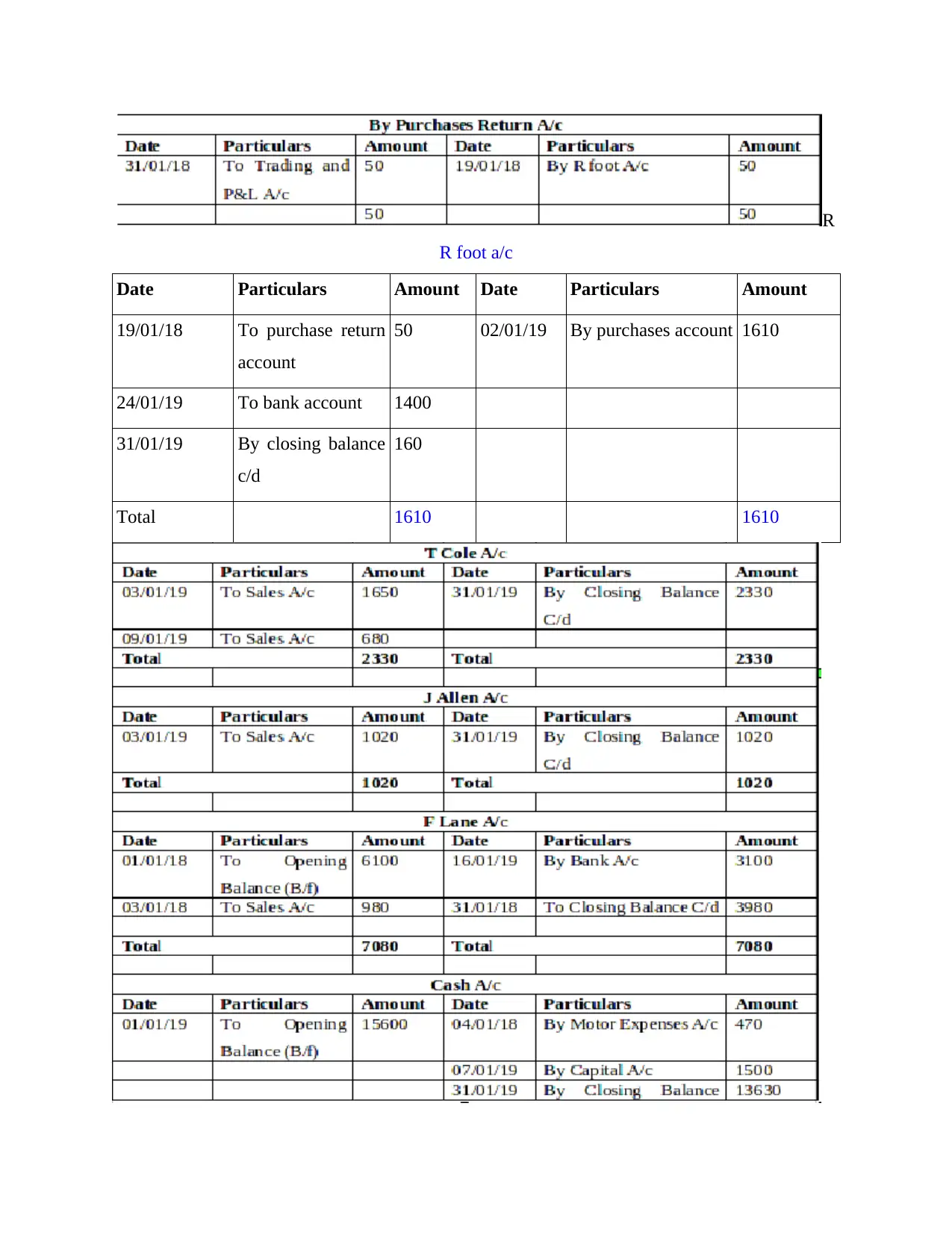

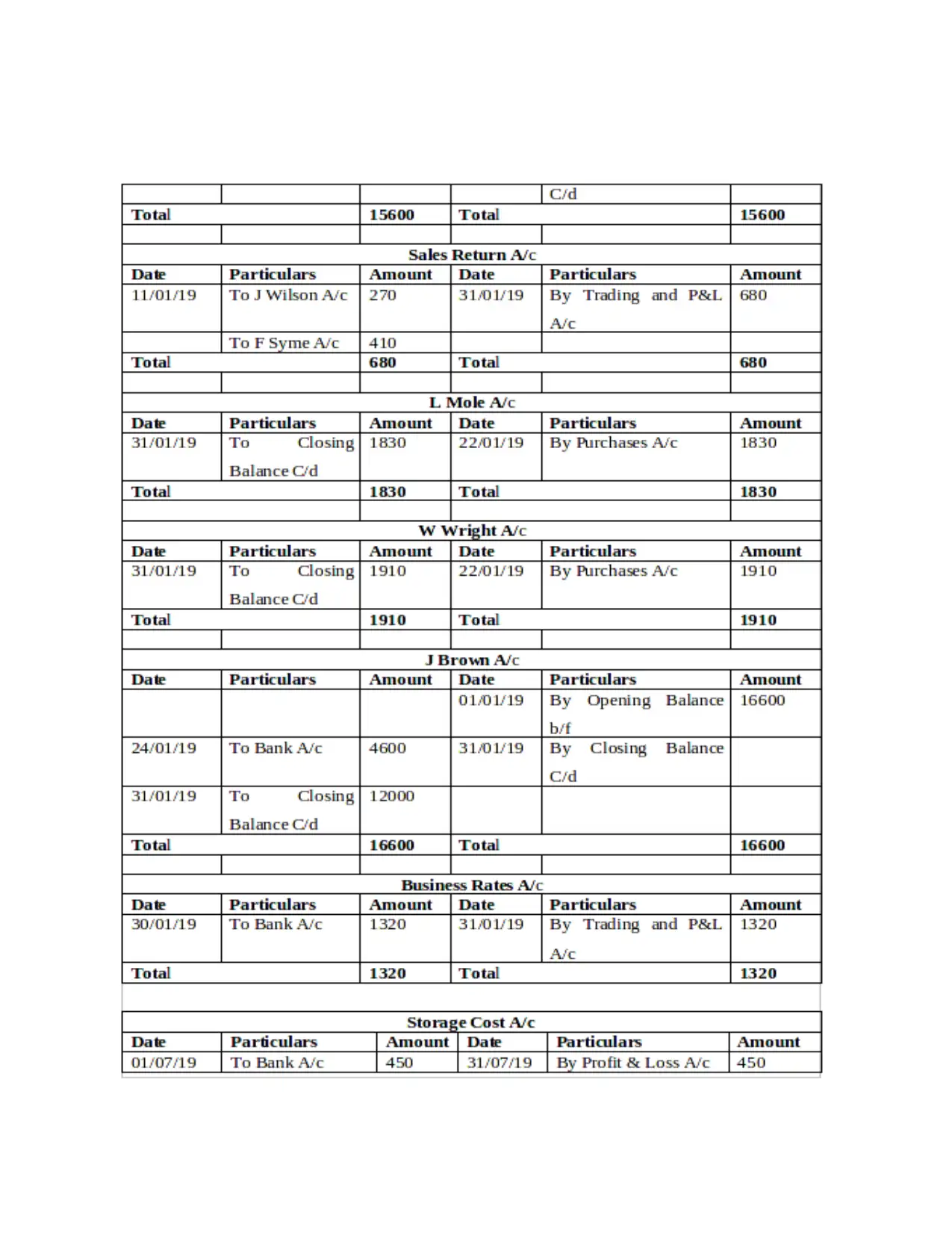

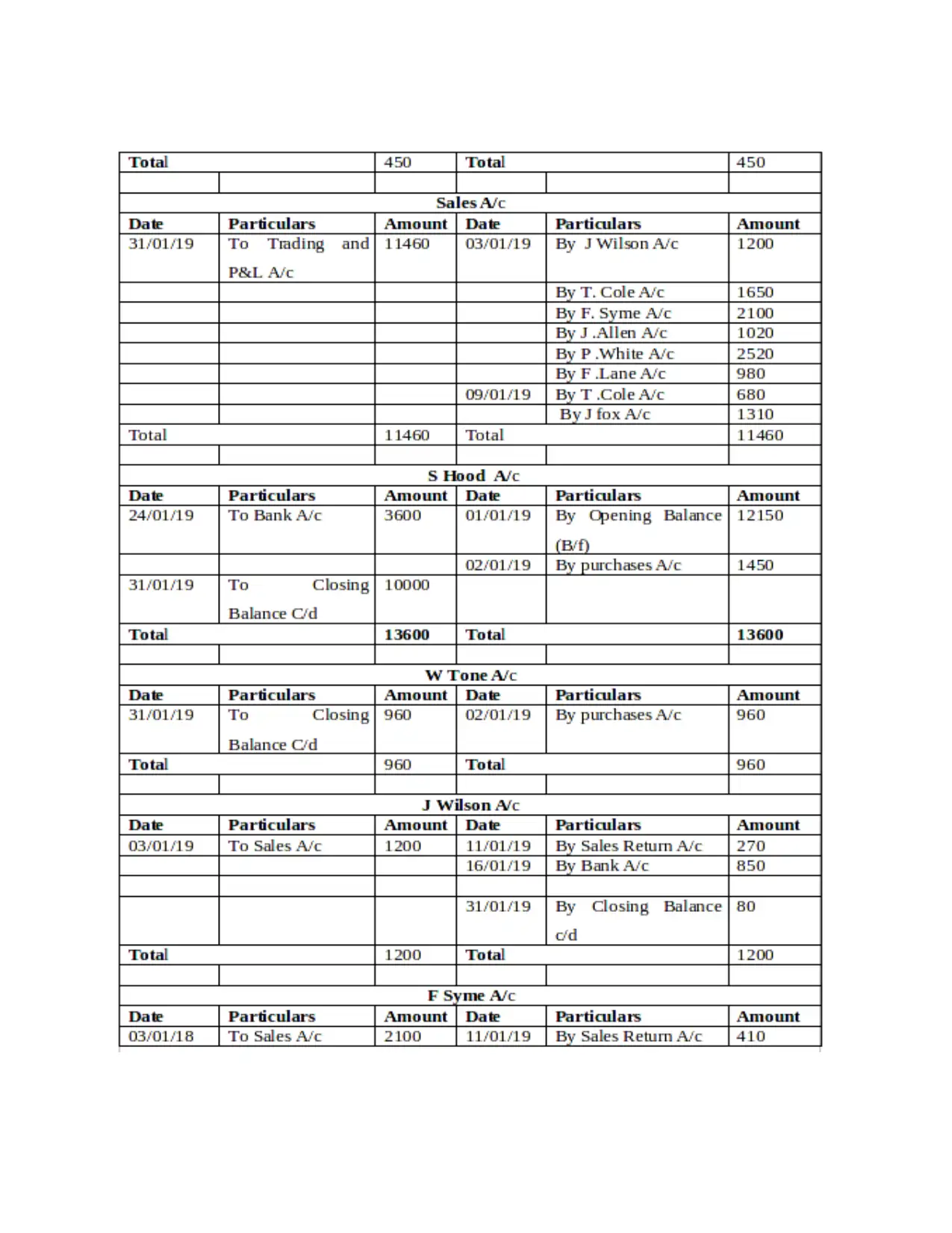

This report delves into the core principles of financial accounting, examining its role in collecting, analyzing, and presenting financial information through statements like the P&L account and balance sheet. The report focuses on a small accountancy firm, Brooks City Consultancy, and defines financial accounting's significance for internal and external stakeholders. It explores double-entry bookkeeping with ledgers, including a trial balance, and analyzes financial statements like a P&L account for Munteanu Limited. The report also covers key accounting concepts such as consistency and prudence, emphasizing their importance in ensuring the reliability and accuracy of financial reporting. The report then details various types of stakeholders and their specific interests in the financial information provided. The report concludes by outlining the purpose of depreciation in formulating financial statements.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.