Financial Accounting Report: Principles, Rules, and Client Analysis

VerifiedAdded on 2020/10/22

|24

|4953

|335

Report

AI Summary

This comprehensive financial accounting report provides a detailed overview of essential concepts, rules, and regulations. Part A of the report illustrates financial accounting, covering cash flow statements, financial position statements, changes in equity, and income statements. It also discusses rules and regulations, including GAAP, IFRS, and the role of regulatory bodies. Part B presents client case studies, analyzing financial transactions and accounting practices. The report covers accounting principles such as matching principle, income acknowledgment, going concern, full disclosure and cost, and conventions like consistency and materiality. The report also includes a discussion on the importance of financial statements and how they assist in effective decision-making and ethical financial practices.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTENTS

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A BUSINESS REPORT.......................................................................................................1

Illustrate the financial accounting................................................................................................1

Rules and regulations subject to financial accounting.................................................................2

Accounting principles and rules..................................................................................................4

Concepts and convention related to consistency and material disclosure...................................5

PART B...........................................................................................................................................6

CLIENT 1........................................................................................................................................6

CLIENT 2......................................................................................................................................15

CLIENT 3......................................................................................................................................16

CLIENT 4......................................................................................................................................17

CLIENT 5......................................................................................................................................18

CLIENT 6......................................................................................................................................20

Suspense account and reconcile.................................................................................................20

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A BUSINESS REPORT.......................................................................................................1

Illustrate the financial accounting................................................................................................1

Rules and regulations subject to financial accounting.................................................................2

Accounting principles and rules..................................................................................................4

Concepts and convention related to consistency and material disclosure...................................5

PART B...........................................................................................................................................6

CLIENT 1........................................................................................................................................6

CLIENT 2......................................................................................................................................15

CLIENT 3......................................................................................................................................16

CLIENT 4......................................................................................................................................17

CLIENT 5......................................................................................................................................18

CLIENT 6......................................................................................................................................20

Suspense account and reconcile.................................................................................................20

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

INTRODUCTION

Financial accounting is one of the essential aspect in terms of making the strategies and

plan to attain financial ethicalness and terminology. There are type of information and details

remain required for managing and operating the business in organisational context. Financial

statements analysis, formulation of finance plans are some essential elements which assist the

finance structure in effective manner. The different procedure of compromise is talked about in

this reports, for example, accounting framework, record posting framework, readiness of trial

adjusts and so on (Narayanaswamy, 2017). The standards of bookkeeping, significance of

budgetary records are likewise examined in this task report.

In the advanced world, data is the best. Monetary bookkeeping helps the organizations in

speaking with the intrigued partners through planning money related articulations. It is the

obligation of the money related directors to guarantee that the data displayed in the budgetary

proclamations of the organization speaks to genuine and reasonable perspective of the

organization and it is dependable for the speculators of the organization to take choices in

regards to whether to put resources into the organization or not. In this venture of money related

bookkeeping we will talk about the how budgetary exchanges are overseen and posted in the

announcements with the goal that they wind up powerful in taking choices.

PART A BUSINESS REPORT

Illustrate the financial accounting

Cash flow statement: this announcement gets data identified with benefit and

consumption for a year. Pay enunciation is moreover considered as a pay, costs, gets and loses of

affiliation. It contains the business, organizations, and interest wages. which is prepare by

relationship to choose advantage and misfortunes. With the help of compensation announcement

proprietors, primary gatherings and accomplices have the ability to choose the advantage of

affiliation. More finished salary explanation decides the general use brought about with a

specific end goal to get wanted pay. This is additionally called as productivity articulation or

benefit and misfortune account.

Financial position statement: this announcement covers all the data and points of

interest identified with resources and the liabilities. The whole of the risk and resources stay

approach. This is one of the prime articulation according to partner's point of view. Budgetary

position explanation additionally called as accounting report. This announcement is set up based

1

Financial accounting is one of the essential aspect in terms of making the strategies and

plan to attain financial ethicalness and terminology. There are type of information and details

remain required for managing and operating the business in organisational context. Financial

statements analysis, formulation of finance plans are some essential elements which assist the

finance structure in effective manner. The different procedure of compromise is talked about in

this reports, for example, accounting framework, record posting framework, readiness of trial

adjusts and so on (Narayanaswamy, 2017). The standards of bookkeeping, significance of

budgetary records are likewise examined in this task report.

In the advanced world, data is the best. Monetary bookkeeping helps the organizations in

speaking with the intrigued partners through planning money related articulations. It is the

obligation of the money related directors to guarantee that the data displayed in the budgetary

proclamations of the organization speaks to genuine and reasonable perspective of the

organization and it is dependable for the speculators of the organization to take choices in

regards to whether to put resources into the organization or not. In this venture of money related

bookkeeping we will talk about the how budgetary exchanges are overseen and posted in the

announcements with the goal that they wind up powerful in taking choices.

PART A BUSINESS REPORT

Illustrate the financial accounting

Cash flow statement: this announcement gets data identified with benefit and

consumption for a year. Pay enunciation is moreover considered as a pay, costs, gets and loses of

affiliation. It contains the business, organizations, and interest wages. which is prepare by

relationship to choose advantage and misfortunes. With the help of compensation announcement

proprietors, primary gatherings and accomplices have the ability to choose the advantage of

affiliation. More finished salary explanation decides the general use brought about with a

specific end goal to get wanted pay. This is additionally called as productivity articulation or

benefit and misfortune account.

Financial position statement: this announcement covers all the data and points of

interest identified with resources and the liabilities. The whole of the risk and resources stay

approach. This is one of the prime articulation according to partner's point of view. Budgetary

position explanation additionally called as accounting report. This announcement is set up based

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on significant bookkeeping condition which is (resources = capital + liabilities). With the help of

money related position articulation speculators and partners have the capacity to outline the

budgetary position of association (Cernusca and Balaciu, 2015). This likewise unites the benefits

and the obligation. Settled resources, liabilities are characterized in this specific situation. There

are kind of data, for example, unforeseen obligation and dealing with the budgetary execution of

association.

Change in equity: this announcement introduce the data and points of interest identified

with value share capital, securities premium, stores and excess, recovery saves and so on with the

help of progress in value articulations partners and administrators have the capacity to

comprehend the adjustment in value position of organisation in different terms. The real angle

which remain related with investigating the value position and holds. Solid value and save

structure pulls in light of a legitimate concern for financial specialists and partners.

Income statement: it is one of the basic necessity of business to oversee and control the

stream of trade without the association and investigate the monetary prerequisite for additionally

utilize. There are three noteworthy exercises are considered in this setting as far as dissecting the

budgetary stream of association. Income from working movement, income frame financing

action and income from contributing action.

Rules and regulations subject to financial accounting

There are a couple of standards and controls are made the extent that managing the cash

related exercises and organization for better execution of budgetary errands. Money related

Itemizing Chamber (FRC) are made in respect of indicating budgetary information specifically

association. Accounting benchmarks and checks which are given by Sound bookkeeping

measures (GAAP). This is on a very basic level stay related with incurred significant damage

norms, going concern, planning principle, financial component, relevance, protection and

steadfastness of cash related presentation. The principal arrangement of standards was computed

as Uniform Arrangement of Records (USOA) and Irish and UK GAAP issues tenets and

enactments as far as making principles and enactments for keeping up and plan budgetary

explanations. Huge proportion of bookkeeping direction frequently issued to develop and clarify

bookkeeping traditions by specific ventures (Romolini, Fissi and Gori, 2017). Specific ventures,

as philanthropies, annuity, keeping money and protection. Explanations which are set up

2

money related position articulation speculators and partners have the capacity to outline the

budgetary position of association (Cernusca and Balaciu, 2015). This likewise unites the benefits

and the obligation. Settled resources, liabilities are characterized in this specific situation. There

are kind of data, for example, unforeseen obligation and dealing with the budgetary execution of

association.

Change in equity: this announcement introduce the data and points of interest identified

with value share capital, securities premium, stores and excess, recovery saves and so on with the

help of progress in value articulations partners and administrators have the capacity to

comprehend the adjustment in value position of organisation in different terms. The real angle

which remain related with investigating the value position and holds. Solid value and save

structure pulls in light of a legitimate concern for financial specialists and partners.

Income statement: it is one of the basic necessity of business to oversee and control the

stream of trade without the association and investigate the monetary prerequisite for additionally

utilize. There are three noteworthy exercises are considered in this setting as far as dissecting the

budgetary stream of association. Income from working movement, income frame financing

action and income from contributing action.

Rules and regulations subject to financial accounting

There are a couple of standards and controls are made the extent that managing the cash

related exercises and organization for better execution of budgetary errands. Money related

Itemizing Chamber (FRC) are made in respect of indicating budgetary information specifically

association. Accounting benchmarks and checks which are given by Sound bookkeeping

measures (GAAP). This is on a very basic level stay related with incurred significant damage

norms, going concern, planning principle, financial component, relevance, protection and

steadfastness of cash related presentation. The principal arrangement of standards was computed

as Uniform Arrangement of Records (USOA) and Irish and UK GAAP issues tenets and

enactments as far as making principles and enactments for keeping up and plan budgetary

explanations. Huge proportion of bookkeeping direction frequently issued to develop and clarify

bookkeeping traditions by specific ventures (Romolini, Fissi and Gori, 2017). Specific ventures,

as philanthropies, annuity, keeping money and protection. Explanations which are set up

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

according to these controls and guidelines are called as proclamations of prescribed practice

(SORPs).

GAAP (Proper accounting standard) are taken after at comprehensive level. General

association which works business practices in different nations get a handle on the benchmarks

and measures of ISA and GAAP. IASB is of the administrative which issues tenets, techniques

and benchmarks subject to cash related bookkeeping and bookkeeping presentation. IFRS which

is known as General Budgetary Indicating Models are the measures issues by IASB. There are

techniques working gathering was shaped in 1997 and accused of auditing with terms of

structure and process. The structure of IASB of various components, for example, Checking

board (open capital market experts), IFRS establishment trustees, worldwide bookkeeping

guidelines sheets, IFRS warning chamber, IFRS understanding panel.

ASB (Bookkeeping Standard Board) in like manner gives establishments and standards

related to fiscal clarifications are moreover described in this special condition. It likewise issues

the team proclamations which gives fast direction on the prescribed treatment of a specific

exchange where unforeseen understanding of a suggested bookkeeping standard and treatment is

required. There is a particular board is made subject to screen the exercises and the undertaking

to create new principles and enactments. There is no any power of law made as far as following

the universal monetary and bookkeeping rules for associations working at local level. These

standards altogether urges chiefs and accountants to present the budgetary information and

accounting revelation of accounting systems. Standards which are outfitted under ASB stay

related with examining treatment of utilization and salary structure of affiliation (Sulimierska,

2013).

It is essential for associations as far as making the monetary structure in different

structures. Fundamental target of administrative experts and the administrative bodies is to

advance the purposeful straightforwardness and consistency with the money related

proclamations arranged by associations around the world. There are a few tenets and directions

additionally gave by the Global Bookkeeping Standard Advisory group (IASC) regarding

orchestrating in 1973. the IASC produces bookkeeping models which are called as universal

bookkeeping measures (IAS) (Sales Ledger Control Account. 2018).

3

(SORPs).

GAAP (Proper accounting standard) are taken after at comprehensive level. General

association which works business practices in different nations get a handle on the benchmarks

and measures of ISA and GAAP. IASB is of the administrative which issues tenets, techniques

and benchmarks subject to cash related bookkeeping and bookkeeping presentation. IFRS which

is known as General Budgetary Indicating Models are the measures issues by IASB. There are

techniques working gathering was shaped in 1997 and accused of auditing with terms of

structure and process. The structure of IASB of various components, for example, Checking

board (open capital market experts), IFRS establishment trustees, worldwide bookkeeping

guidelines sheets, IFRS warning chamber, IFRS understanding panel.

ASB (Bookkeeping Standard Board) in like manner gives establishments and standards

related to fiscal clarifications are moreover described in this special condition. It likewise issues

the team proclamations which gives fast direction on the prescribed treatment of a specific

exchange where unforeseen understanding of a suggested bookkeeping standard and treatment is

required. There is a particular board is made subject to screen the exercises and the undertaking

to create new principles and enactments. There is no any power of law made as far as following

the universal monetary and bookkeeping rules for associations working at local level. These

standards altogether urges chiefs and accountants to present the budgetary information and

accounting revelation of accounting systems. Standards which are outfitted under ASB stay

related with examining treatment of utilization and salary structure of affiliation (Sulimierska,

2013).

It is essential for associations as far as making the monetary structure in different

structures. Fundamental target of administrative experts and the administrative bodies is to

advance the purposeful straightforwardness and consistency with the money related

proclamations arranged by associations around the world. There are a few tenets and directions

additionally gave by the Global Bookkeeping Standard Advisory group (IASC) regarding

orchestrating in 1973. the IASC produces bookkeeping models which are called as universal

bookkeeping measures (IAS) (Sales Ledger Control Account. 2018).

3

Accounting principles and rules

Bookkeeping rules: These standards are charge the collector and credit the provider;

Charge what comes in and credit what goes out; Charge all costs and misfortunes and credit all

earnings and additions. There are three essential standards of bookkeeping that is critical ,

without which the bookkeeping is impossible. These guidelines are talked about as under in a

nutshell:

Charge what comes in and credit what goes out: This bookkeeping principle considers all the

genuine records of the organization. The genuine records are identified with the benefits of the

organization which can either come in or go out from the business. On the off chance that any of

the advantage, for example, apparatus and stock come into the organization then this record is

charged by the lead charge what comes in. What's more, if the organization disposes of or offers

any benefit then the record of that specific resource is attributed by the organization as indicated

by the bookkeeping preclude credit what goes. As illustrated that, let’s say an organization buys

a hardware of 25000 by paying money (Lundberg and Sundbaum, 2016). Around here exchanges

the hardware is coming in organization that implies it will be charged in the records of the

organization and money is going out as instalments source which implies it will be credited in

the organization's record.

Charge all costs, misfortunes and credit all salaries , picks up: This bookkeeping standard

thinks about all the ostensible records. The ostensible records are those which thinks about the

costs and livelihoods of the organization. The consumptions and misfortunes are charged

according to the govern and the wage and picks up are credited in the organization account (Zeff,

2016).

For example: Gives say a chance to organization pays the lease for the building where its

office is, at that point the organization will charge the lease account when the lease will be paid.

Accounting principles

Matching Principle - It is a fundamental hidden rule in a bookkeeping. It guides firm to

report use in its salary explanation in comparative era worried about incomes.

Income Acknowledgement: It is a compelling bookkeeping rule in which Sound

accounting standards (GAAP) distinguished specific circumstance in which benefit is

accounted or perceived.

4

Bookkeeping rules: These standards are charge the collector and credit the provider;

Charge what comes in and credit what goes out; Charge all costs and misfortunes and credit all

earnings and additions. There are three essential standards of bookkeeping that is critical ,

without which the bookkeeping is impossible. These guidelines are talked about as under in a

nutshell:

Charge what comes in and credit what goes out: This bookkeeping principle considers all the

genuine records of the organization. The genuine records are identified with the benefits of the

organization which can either come in or go out from the business. On the off chance that any of

the advantage, for example, apparatus and stock come into the organization then this record is

charged by the lead charge what comes in. What's more, if the organization disposes of or offers

any benefit then the record of that specific resource is attributed by the organization as indicated

by the bookkeeping preclude credit what goes. As illustrated that, let’s say an organization buys

a hardware of 25000 by paying money (Lundberg and Sundbaum, 2016). Around here exchanges

the hardware is coming in organization that implies it will be charged in the records of the

organization and money is going out as instalments source which implies it will be credited in

the organization's record.

Charge all costs, misfortunes and credit all salaries , picks up: This bookkeeping standard

thinks about all the ostensible records. The ostensible records are those which thinks about the

costs and livelihoods of the organization. The consumptions and misfortunes are charged

according to the govern and the wage and picks up are credited in the organization account (Zeff,

2016).

For example: Gives say a chance to organization pays the lease for the building where its

office is, at that point the organization will charge the lease account when the lease will be paid.

Accounting principles

Matching Principle - It is a fundamental hidden rule in a bookkeeping. It guides firm to

report use in its salary explanation in comparative era worried about incomes.

Income Acknowledgement: It is a compelling bookkeeping rule in which Sound

accounting standards (GAAP) distinguished specific circumstance in which benefit is

accounted or perceived.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Going concern -It expresses that firm is beginning to doing the business related undertakings or

activities toward the end. Every one of these models are remain to be shown subject to

practicality and additionally huge pull destinations (May, 2013).

Full disclosure: It is a compelling bookkeeping standards which offers rules to tell

seeing the spotless and in addition sensible depiction of approach identified with booking

and furthermore budgetary benchmarks through affiliation. Furthermore, it is basic for

organization to delineate all standards and furthermore game plan of firm through which

rules and furthermore accounting are trailered.

Cost - Under this, there are two unique techniques which are utilized to record a powerful

estimation of advantages in books like for an example net possible cost and

unquestionable cost. Certain cost gained in start of year. Under this, all assets are

recorded in the books with a specific end goal to deducting a weakening based on net

attainable regard.

Concepts and convention related to consistency and material disclosure

Consistency Convention

At the point when the steady bookkeeping strategies are utilized by the organizations in

its monetary proclamations then it ends up less demanding for the speculators and administrators

in contrasting it and another organizations and furthermore the organizations financials

explanations with the earlier years. This must be inspected that the whether the affiliation is

remaining unsurprising with the standards and standards later on. For instance, if the

organization is predictable with its standards, and it utilizes FIFO stock administration

framework then it will turn out to be simple for the organization in contrasting the inventories of

earlier years and the present year rather at that point if the organization was conflicting with its

standards. This bookkeeping tradition expresses that the standards and arrangements that are

received by the association ought to be steady for a more drawn out period and traverse

(McCarthy, Shelmon and Mattie, 2012).

Materiality Convention

Materiality is identified with the size and specific circumstances of the associations. As it

may, is the data expressed in those announcements are excluded or misquoted then it could

impact the choices of the clients. Along these lines it is essential that the data that is contained in

the financials of the organization ought to be finished in all the material angles with the goal that

5

activities toward the end. Every one of these models are remain to be shown subject to

practicality and additionally huge pull destinations (May, 2013).

Full disclosure: It is a compelling bookkeeping standards which offers rules to tell

seeing the spotless and in addition sensible depiction of approach identified with booking

and furthermore budgetary benchmarks through affiliation. Furthermore, it is basic for

organization to delineate all standards and furthermore game plan of firm through which

rules and furthermore accounting are trailered.

Cost - Under this, there are two unique techniques which are utilized to record a powerful

estimation of advantages in books like for an example net possible cost and

unquestionable cost. Certain cost gained in start of year. Under this, all assets are

recorded in the books with a specific end goal to deducting a weakening based on net

attainable regard.

Concepts and convention related to consistency and material disclosure

Consistency Convention

At the point when the steady bookkeeping strategies are utilized by the organizations in

its monetary proclamations then it ends up less demanding for the speculators and administrators

in contrasting it and another organizations and furthermore the organizations financials

explanations with the earlier years. This must be inspected that the whether the affiliation is

remaining unsurprising with the standards and standards later on. For instance, if the

organization is predictable with its standards, and it utilizes FIFO stock administration

framework then it will turn out to be simple for the organization in contrasting the inventories of

earlier years and the present year rather at that point if the organization was conflicting with its

standards. This bookkeeping tradition expresses that the standards and arrangements that are

received by the association ought to be steady for a more drawn out period and traverse

(McCarthy, Shelmon and Mattie, 2012).

Materiality Convention

Materiality is identified with the size and specific circumstances of the associations. As it

may, is the data expressed in those announcements are excluded or misquoted then it could

impact the choices of the clients. Along these lines it is essential that the data that is contained in

the financials of the organization ought to be finished in all the material angles with the goal that

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

they can speak to the genuine and reasonable perspective of the budgetary soundness of the

organization. This bookkeeping tradition expresses that the budgetary articulations of the

organization and the bookkeeping exchange and equalizations are having mistaken in them.

Money related explanations are arranged so the clients of them can settle on pertinent choices by

utilizing them (Mulford and Comiskey, 2011).

PART B

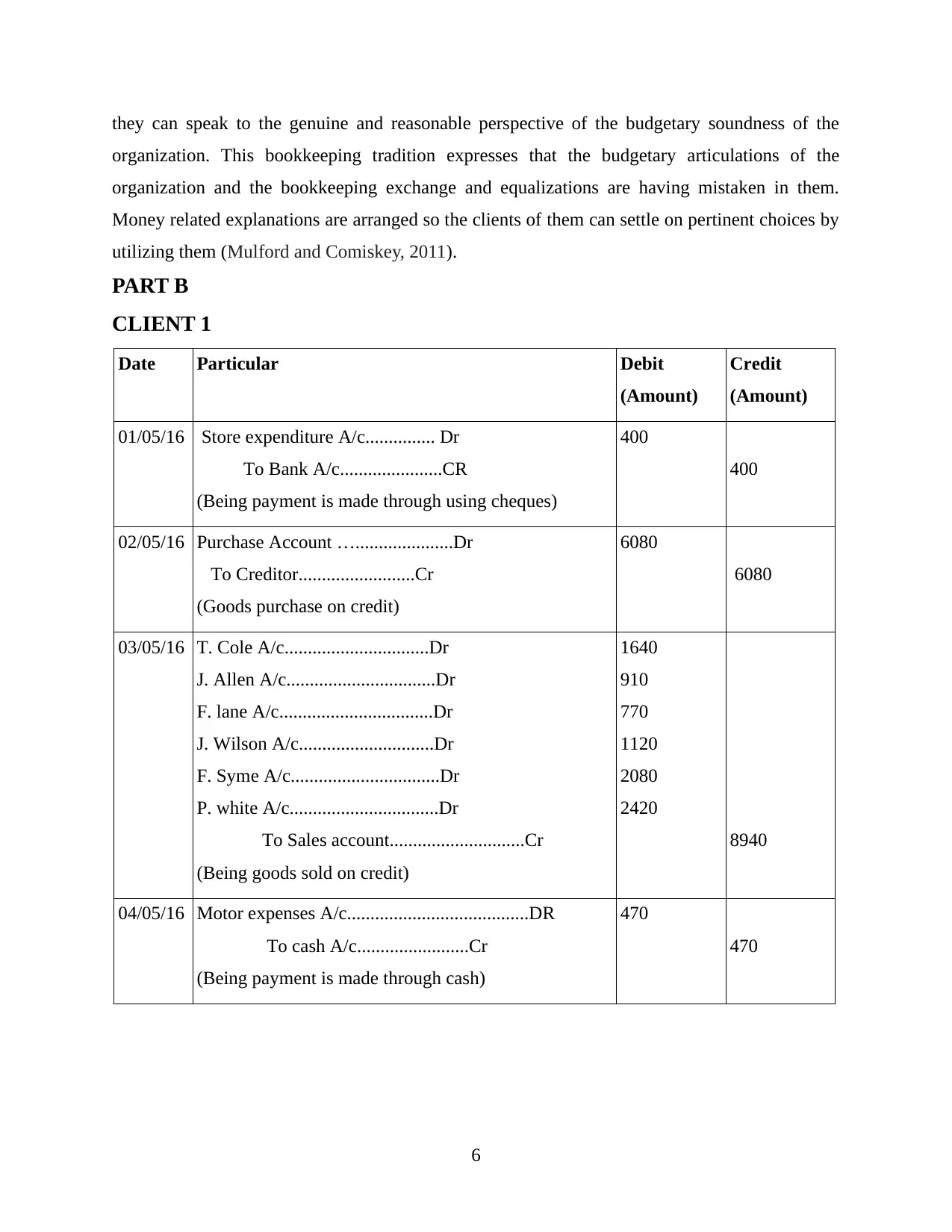

CLIENT 1

Date Particular Debit

(Amount)

Credit

(Amount)

01/05/16 Store expenditure A/c............... Dr

To Bank A/c......................CR

(Being payment is made through using cheques)

400

400

02/05/16 Purchase Account ….....................Dr

To Creditor.........................Cr

(Goods purchase on credit)

6080

6080

03/05/16 T. Cole A/c...............................Dr

J. Allen A/c................................Dr

F. lane A/c.................................Dr

J. Wilson A/c.............................Dr

F. Syme A/c................................Dr

P. white A/c................................Dr

To Sales account.............................Cr

(Being goods sold on credit)

1640

910

770

1120

2080

2420

8940

04/05/16 Motor expenses A/c.......................................DR

To cash A/c........................Cr

(Being payment is made through cash)

470

470

6

organization. This bookkeeping tradition expresses that the budgetary articulations of the

organization and the bookkeeping exchange and equalizations are having mistaken in them.

Money related explanations are arranged so the clients of them can settle on pertinent choices by

utilizing them (Mulford and Comiskey, 2011).

PART B

CLIENT 1

Date Particular Debit

(Amount)

Credit

(Amount)

01/05/16 Store expenditure A/c............... Dr

To Bank A/c......................CR

(Being payment is made through using cheques)

400

400

02/05/16 Purchase Account ….....................Dr

To Creditor.........................Cr

(Goods purchase on credit)

6080

6080

03/05/16 T. Cole A/c...............................Dr

J. Allen A/c................................Dr

F. lane A/c.................................Dr

J. Wilson A/c.............................Dr

F. Syme A/c................................Dr

P. white A/c................................Dr

To Sales account.............................Cr

(Being goods sold on credit)

1640

910

770

1120

2080

2420

8940

04/05/16 Motor expenses A/c.......................................DR

To cash A/c........................Cr

(Being payment is made through cash)

470

470

6

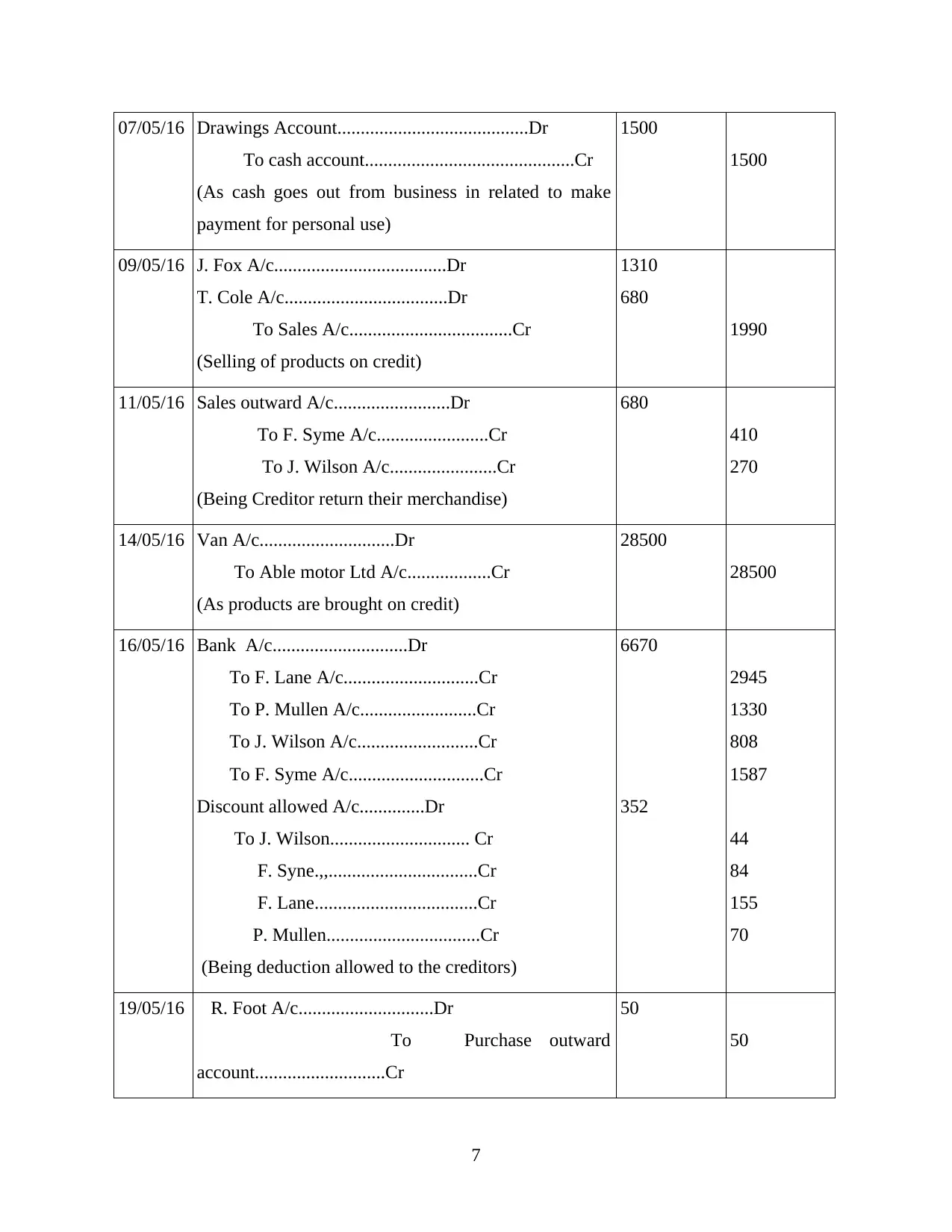

07/05/16 Drawings Account.........................................Dr

To cash account.............................................Cr

(As cash goes out from business in related to make

payment for personal use)

1500

1500

09/05/16 J. Fox A/c.....................................Dr

T. Cole A/c...................................Dr

To Sales A/c...................................Cr

(Selling of products on credit)

1310

680

1990

11/05/16 Sales outward A/c.........................Dr

To F. Syme A/c........................Cr

To J. Wilson A/c.......................Cr

(Being Creditor return their merchandise)

680

410

270

14/05/16 Van A/c.............................Dr

To Able motor Ltd A/c..................Cr

(As products are brought on credit)

28500

28500

16/05/16 Bank A/c.............................Dr

To F. Lane A/c.............................Cr

To P. Mullen A/c.........................Cr

To J. Wilson A/c..........................Cr

To F. Syme A/c.............................Cr

Discount allowed A/c..............Dr

To J. Wilson.............................. Cr

F. Syne.,,................................Cr

F. Lane...................................Cr

P. Mullen.................................Cr

(Being deduction allowed to the creditors)

6670

352

2945

1330

808

1587

44

84

155

70

19/05/16 R. Foot A/c.............................Dr

To Purchase outward

account............................Cr

50

50

7

To cash account.............................................Cr

(As cash goes out from business in related to make

payment for personal use)

1500

1500

09/05/16 J. Fox A/c.....................................Dr

T. Cole A/c...................................Dr

To Sales A/c...................................Cr

(Selling of products on credit)

1310

680

1990

11/05/16 Sales outward A/c.........................Dr

To F. Syme A/c........................Cr

To J. Wilson A/c.......................Cr

(Being Creditor return their merchandise)

680

410

270

14/05/16 Van A/c.............................Dr

To Able motor Ltd A/c..................Cr

(As products are brought on credit)

28500

28500

16/05/16 Bank A/c.............................Dr

To F. Lane A/c.............................Cr

To P. Mullen A/c.........................Cr

To J. Wilson A/c..........................Cr

To F. Syme A/c.............................Cr

Discount allowed A/c..............Dr

To J. Wilson.............................. Cr

F. Syne.,,................................Cr

F. Lane...................................Cr

P. Mullen.................................Cr

(Being deduction allowed to the creditors)

6670

352

2945

1330

808

1587

44

84

155

70

19/05/16 R. Foot A/c.............................Dr

To Purchase outward

account............................Cr

50

50

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

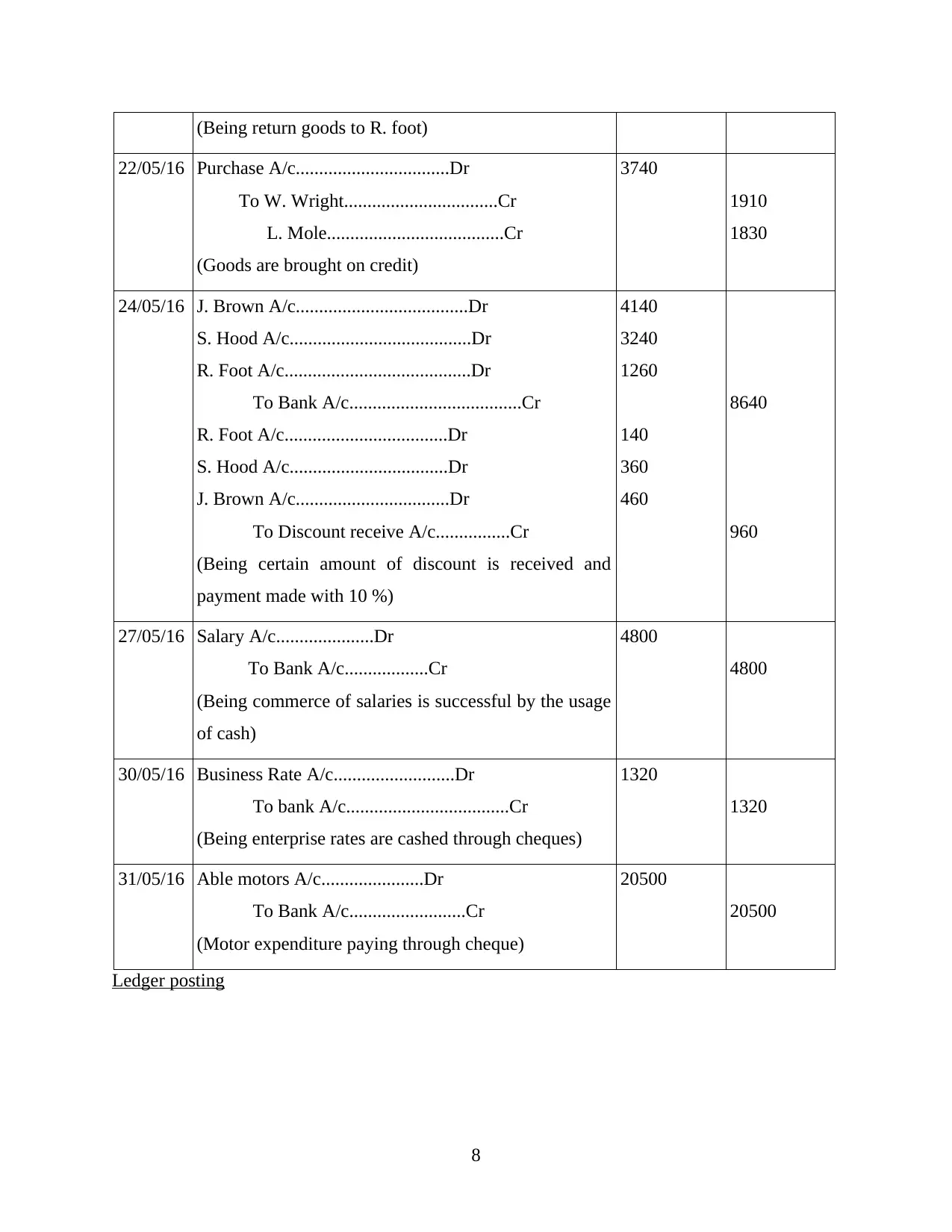

(Being return goods to R. foot)

22/05/16 Purchase A/c.................................Dr

To W. Wright.................................Cr

L. Mole......................................Cr

(Goods are brought on credit)

3740

1910

1830

24/05/16 J. Brown A/c.....................................Dr

S. Hood A/c.......................................Dr

R. Foot A/c........................................Dr

To Bank A/c.....................................Cr

R. Foot A/c...................................Dr

S. Hood A/c..................................Dr

J. Brown A/c.................................Dr

To Discount receive A/c................Cr

(Being certain amount of discount is received and

payment made with 10 %)

4140

3240

1260

140

360

460

8640

960

27/05/16 Salary A/c.....................Dr

To Bank A/c..................Cr

(Being commerce of salaries is successful by the usage

of cash)

4800

4800

30/05/16 Business Rate A/c..........................Dr

To bank A/c...................................Cr

(Being enterprise rates are cashed through cheques)

1320

1320

31/05/16 Able motors A/c......................Dr

To Bank A/c.........................Cr

(Motor expenditure paying through cheque)

20500

20500

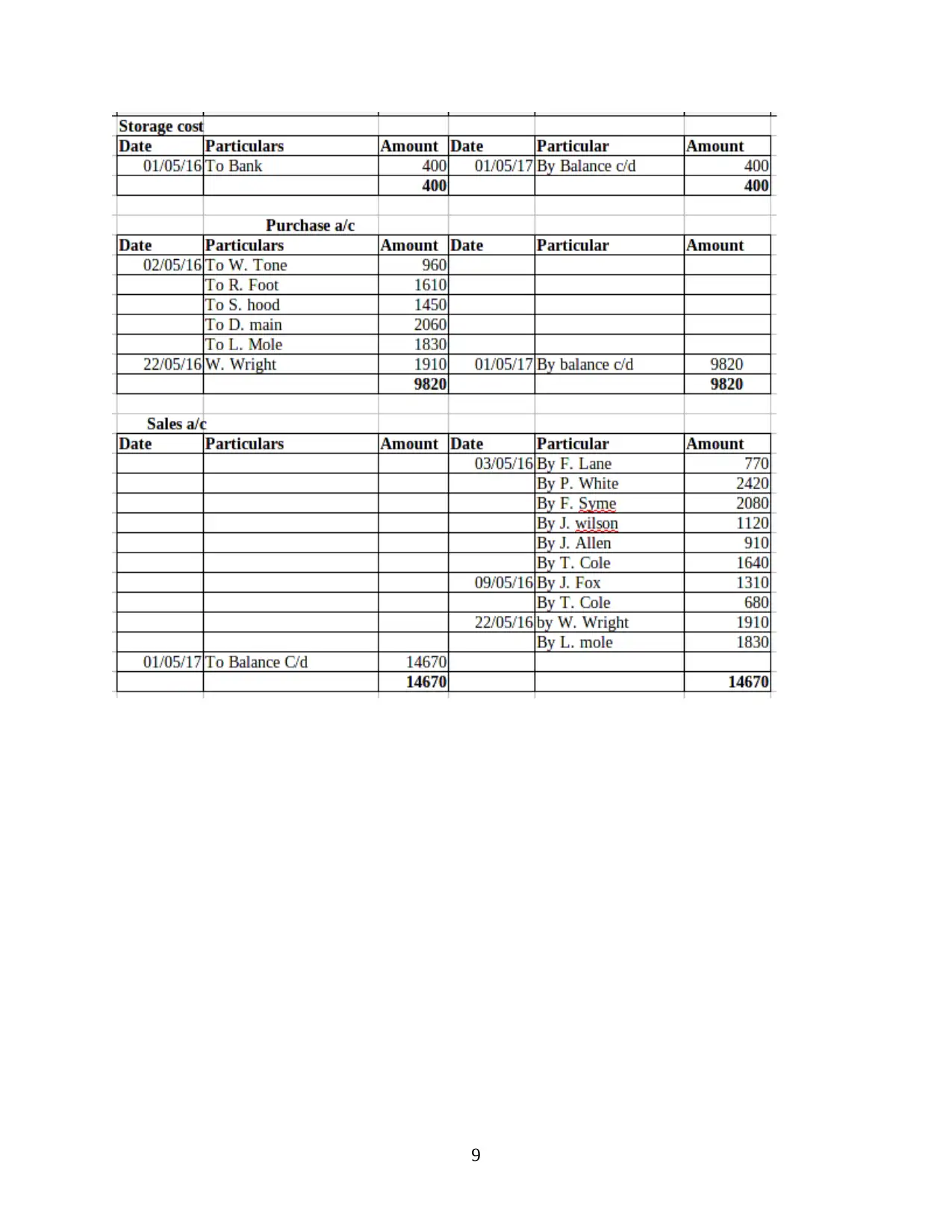

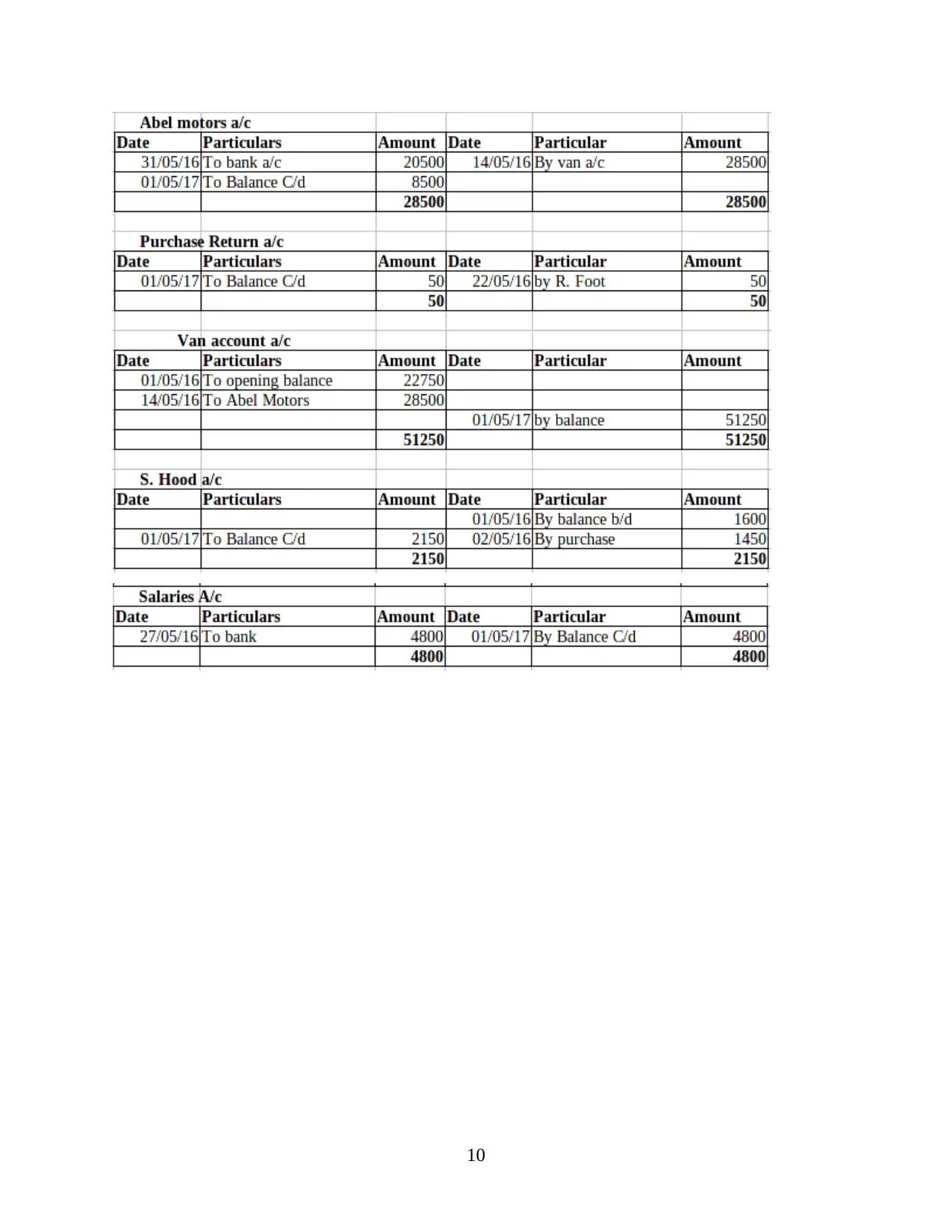

Ledger posting

8

22/05/16 Purchase A/c.................................Dr

To W. Wright.................................Cr

L. Mole......................................Cr

(Goods are brought on credit)

3740

1910

1830

24/05/16 J. Brown A/c.....................................Dr

S. Hood A/c.......................................Dr

R. Foot A/c........................................Dr

To Bank A/c.....................................Cr

R. Foot A/c...................................Dr

S. Hood A/c..................................Dr

J. Brown A/c.................................Dr

To Discount receive A/c................Cr

(Being certain amount of discount is received and

payment made with 10 %)

4140

3240

1260

140

360

460

8640

960

27/05/16 Salary A/c.....................Dr

To Bank A/c..................Cr

(Being commerce of salaries is successful by the usage

of cash)

4800

4800

30/05/16 Business Rate A/c..........................Dr

To bank A/c...................................Cr

(Being enterprise rates are cashed through cheques)

1320

1320

31/05/16 Able motors A/c......................Dr

To Bank A/c.........................Cr

(Motor expenditure paying through cheque)

20500

20500

Ledger posting

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.