Financial Accounting Report: Frankham Consultancy Group Analysis

VerifiedAdded on 2021/02/21

|25

|4847

|60

Report

AI Summary

This report provides a comprehensive overview of financial accounting, focusing on its definition, purpose, and the roles of internal and external stakeholders. It examines the preparation of financial statements, such as balance sheets and income statements, and their importance in decision-making for both internal management and external parties like investors and creditors. The report also delves into the application of Generally Accepted Accounting Principles (GAAP) and the importance of accurate financial reporting. Additionally, the report includes practical examples of journal entries and ledgers for a fictional company, Alexandra Study, demonstrating the recording of various financial transactions including purchases, sales, expenses, and payments. The analysis includes detailed examples of how to record transactions related to owner's capital, purchases, sales, returns, and payments, illustrating key accounting concepts.

FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part (a)..........................................................................................................................................3

Part (b).........................................................................................................................................6

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part (a)..........................................................................................................................................3

Part (b).........................................................................................................................................6

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION

Financial accounting can be defined as a type of accounting system which is related with

the collecting, analysing, presenting and interpreting the financial transactions of any company

(Christensen, Cottrell and Baker, 2013). This accounting system includes preparation of various

kind of financial statements such as income statement, balance sheet, profit & loss account etc.

These financial statements play an important role in the context of internal and external decision-

making. Herein, for this project report frankham consultancy group limited firm is selected

which is an accountancy firm and provides different kind of accounting services such as

auditing, tax consultant etc. In this report definition of financial accounting, its purpose and

internal, external stakeholders are mentioned. Apart from it, various tasks are completed as per

the given data about the clients.

MAIN BODY

Part (a)

1. Definition of financial accounting and its purpose.

Financial accounting- The financial accounting can be defined as a kind of accounting

system which is associated with the preparation of various financial statements that is useful in

providing information regarding to the financial performance of the organisations (Eng, Lea,

2014). Apart from it, this accounting system provide a kind of framework which can be

beneficial in making appropriate financial decisions. Additionally, these financial statements are

not only beneficial for the internal decision making but also useful for the external stakeholders.

It can be understand by an example like if a company prepares financial statements such as

balance sheet, profit & loss accounts etc. Due to this their external stakeholders like investors,

creditors can evaluate their actual financial conditions. It is helpful for the internal management

of that company. So overall due to these financial statements businesses can take many crucial

decisions whether they should invest more capital or not. In other words, it reflects the actual

position of the company in front of internal and external stakeholders.

Apart from it, this is necessary for the organisations to follow the Generally accepted

accounting principles (GAAP). Eventually, it is the responsibility of an accountant to follow all

the rules and regulations during preparation of financial statements so that information can be

reliable and accurate. In the absence of implementing proper accounting principles, it can be

Financial accounting can be defined as a type of accounting system which is related with

the collecting, analysing, presenting and interpreting the financial transactions of any company

(Christensen, Cottrell and Baker, 2013). This accounting system includes preparation of various

kind of financial statements such as income statement, balance sheet, profit & loss account etc.

These financial statements play an important role in the context of internal and external decision-

making. Herein, for this project report frankham consultancy group limited firm is selected

which is an accountancy firm and provides different kind of accounting services such as

auditing, tax consultant etc. In this report definition of financial accounting, its purpose and

internal, external stakeholders are mentioned. Apart from it, various tasks are completed as per

the given data about the clients.

MAIN BODY

Part (a)

1. Definition of financial accounting and its purpose.

Financial accounting- The financial accounting can be defined as a kind of accounting

system which is associated with the preparation of various financial statements that is useful in

providing information regarding to the financial performance of the organisations (Eng, Lea,

2014). Apart from it, this accounting system provide a kind of framework which can be

beneficial in making appropriate financial decisions. Additionally, these financial statements are

not only beneficial for the internal decision making but also useful for the external stakeholders.

It can be understand by an example like if a company prepares financial statements such as

balance sheet, profit & loss accounts etc. Due to this their external stakeholders like investors,

creditors can evaluate their actual financial conditions. It is helpful for the internal management

of that company. So overall due to these financial statements businesses can take many crucial

decisions whether they should invest more capital or not. In other words, it reflects the actual

position of the company in front of internal and external stakeholders.

Apart from it, this is necessary for the organisations to follow the Generally accepted

accounting principles (GAAP). Eventually, it is the responsibility of an accountant to follow all

the rules and regulations during preparation of financial statements so that information can be

reliable and accurate. In the absence of implementing proper accounting principles, it can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

difficult for the companies to take risky decisions. For this purpose, organisations conduct

auditing process so that accuracy of financial statements can be analysed. Herein, some purposes

of financial accounting are mentioned below: Provide financial information- The basic purpose of financial accounting is to provide

needed reliable financial information with the help of different kind of financial accounts

such as balance sheet, income statements etc. Provide framework for decision-making- The financial accounting is also helpful in

taking many crucial and important decisions on the basis of prepared financial statements

(Knežević, Stanković and Tepavac, 2012). Helpful in taking taxation decisions- Additionally, this accounting system is useful in

taking taxation decision. On the basis of income and expenditures companies can

calculate the actual taxation. Helps in comparison- Due to the financial accounting system, companies can compare

their current year's profits and expenditures from past year. It can be possible by

comparison of previous year's profit & loss account and balance sheets with current year.

With the help of it, organisation can analyse their actual condition.

Beneficial in making future plans and strategies- The another purpose of financial

accounting system is that on the basis of financial information, companies can make their

further plans and competitive strategies. It becomes possible because several financial

statements consist important which can be useful in making important strategies. Helpful in attracting investors- If company's financial statements are presenting better

financial condition then it can be profitable for them to attract more investors. This is

why because investors make invest on the basis of financial condition and it is provided

by financial accounting in the form of income statements, balance sheet etc.

2. Internal and external stakeholders.

Stakeholder- It can be defined as a person or group of person who are interested in the

activities of any business. The main purpose of them to show the interest is to evaluate financial

position so that they can make invest in companies. Eventually, there are two types of

stakeholders which are internal and external stakeholders. If companies change their plans,

policies and strategies then it impacts to the stakeholders. As well as for organisations it is

auditing process so that accuracy of financial statements can be analysed. Herein, some purposes

of financial accounting are mentioned below: Provide financial information- The basic purpose of financial accounting is to provide

needed reliable financial information with the help of different kind of financial accounts

such as balance sheet, income statements etc. Provide framework for decision-making- The financial accounting is also helpful in

taking many crucial and important decisions on the basis of prepared financial statements

(Knežević, Stanković and Tepavac, 2012). Helpful in taking taxation decisions- Additionally, this accounting system is useful in

taking taxation decision. On the basis of income and expenditures companies can

calculate the actual taxation. Helps in comparison- Due to the financial accounting system, companies can compare

their current year's profits and expenditures from past year. It can be possible by

comparison of previous year's profit & loss account and balance sheets with current year.

With the help of it, organisation can analyse their actual condition.

Beneficial in making future plans and strategies- The another purpose of financial

accounting system is that on the basis of financial information, companies can make their

further plans and competitive strategies. It becomes possible because several financial

statements consist important which can be useful in making important strategies. Helpful in attracting investors- If company's financial statements are presenting better

financial condition then it can be profitable for them to attract more investors. This is

why because investors make invest on the basis of financial condition and it is provided

by financial accounting in the form of income statements, balance sheet etc.

2. Internal and external stakeholders.

Stakeholder- It can be defined as a person or group of person who are interested in the

activities of any business. The main purpose of them to show the interest is to evaluate financial

position so that they can make invest in companies. Eventually, there are two types of

stakeholders which are internal and external stakeholders. If companies change their plans,

policies and strategies then it impacts to the stakeholders. As well as for organisations it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

beneficial if they have more stakeholders then there will be possibility of higher investment.

Herein, below internal and external stakeholders are mentioned:

Internal stakeholders- These stakeholders are the group of person who can be effected

by the company (Vogel, 2014). The internal stakeholders are employees, managers etc.

Basically, these stakeholders are the main part of the organisations because all necessary

decisions are taken by them. Herein, below some types of internal stakeholders are mentioned

below: Employees- These are the group of individuals who performs various kind of tasks and

activities as per their skills and capabilities to get wages, salary in return. Though the

employees are just hired to perform organisational task but they have the interest in the

financial position of the company. This why because if employees will aware about the

financial condition of the company then they will ensure about their growth. Board of director- The board of director is a panel or group of some people who make

rules and regulations for organisations and these rules must be followed by all the

members. The broad of directors are interested in the financial information of the

company because on the basis of it they can take important decision for the organisation.

As well as can make competitive strategies and plans.

External stakeholders- These stakeholders are those who are not the part of organisation and are

not involved in the day to day activities. Some example of these stakeholders are such as

customers, regulators, government, investors, suppliers etc. Herein, below these stakeholders are

mentioned below:

Suppliers- These are the group of person or individual who provides raw material, goods

and services to the organisations. The suppliers might be interested in the financial

information of the company because on the basis of financial situation of the company

they judge to provide credit facility. If financial situation of an organisation is weak then

suppliers will not provide raw material or other facility to them on credit. On the other

hand, if financial condition is weak then suppliers will not offer material on credit.

Investors- The investors are those who invest their fund in the companies with an

expectation to earn profit on the invested fund. These investors are interested in the

financial information of the company because on the basis of financial condition of the

company they take decision whether they should invest further in that company or not.

Herein, below internal and external stakeholders are mentioned:

Internal stakeholders- These stakeholders are the group of person who can be effected

by the company (Vogel, 2014). The internal stakeholders are employees, managers etc.

Basically, these stakeholders are the main part of the organisations because all necessary

decisions are taken by them. Herein, below some types of internal stakeholders are mentioned

below: Employees- These are the group of individuals who performs various kind of tasks and

activities as per their skills and capabilities to get wages, salary in return. Though the

employees are just hired to perform organisational task but they have the interest in the

financial position of the company. This why because if employees will aware about the

financial condition of the company then they will ensure about their growth. Board of director- The board of director is a panel or group of some people who make

rules and regulations for organisations and these rules must be followed by all the

members. The broad of directors are interested in the financial information of the

company because on the basis of it they can take important decision for the organisation.

As well as can make competitive strategies and plans.

External stakeholders- These stakeholders are those who are not the part of organisation and are

not involved in the day to day activities. Some example of these stakeholders are such as

customers, regulators, government, investors, suppliers etc. Herein, below these stakeholders are

mentioned below:

Suppliers- These are the group of person or individual who provides raw material, goods

and services to the organisations. The suppliers might be interested in the financial

information of the company because on the basis of financial situation of the company

they judge to provide credit facility. If financial situation of an organisation is weak then

suppliers will not provide raw material or other facility to them on credit. On the other

hand, if financial condition is weak then suppliers will not offer material on credit.

Investors- The investors are those who invest their fund in the companies with an

expectation to earn profit on the invested fund. These investors are interested in the

financial information of the company because on the basis of financial condition of the

company they take decision whether they should invest further in that company or not.

Creditors- The creditors are those who gives fund or goods on credit to the companies.

Eventually, they give the credit on the basis of financial condition of the organisation.

They show their interest in the financial information of the company to check their

profitability, borrowings etc. On the basis of their financial condition, creditors lend

money to the companies. Government- Eventually, the government is one of the important stakeholder for the

companies. They set the particular laws, rules and regulations which must be followed by

the organisations. They might be interested in the financial information of the companies

so that tax rate can be determined of the organisations.

Part (b)

Client 1.

Journals- In the context of accounting, journal entry means putting the financial

transactions in an accounting journal that defines debit and credit balance (Aiken, 2013). Herein,

it is important that addition of debit and credit side must be equal.

Owner's capital- The account of owner's capital defines about how much capital from the

total capital is invested by the owner of company.

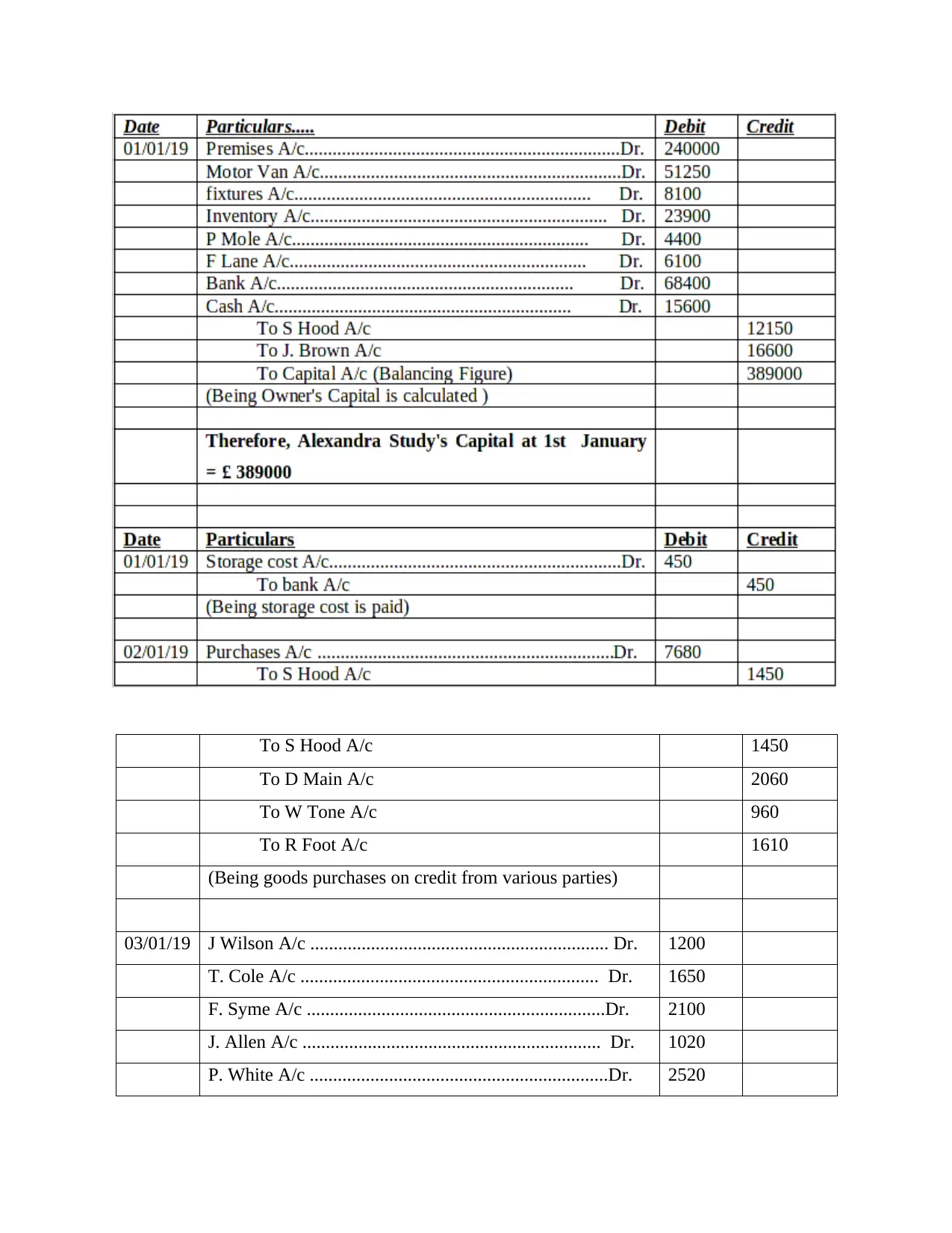

(a) Journal Entries and Ledgers in the book of Alexandra Study

Eventually, they give the credit on the basis of financial condition of the organisation.

They show their interest in the financial information of the company to check their

profitability, borrowings etc. On the basis of their financial condition, creditors lend

money to the companies. Government- Eventually, the government is one of the important stakeholder for the

companies. They set the particular laws, rules and regulations which must be followed by

the organisations. They might be interested in the financial information of the companies

so that tax rate can be determined of the organisations.

Part (b)

Client 1.

Journals- In the context of accounting, journal entry means putting the financial

transactions in an accounting journal that defines debit and credit balance (Aiken, 2013). Herein,

it is important that addition of debit and credit side must be equal.

Owner's capital- The account of owner's capital defines about how much capital from the

total capital is invested by the owner of company.

(a) Journal Entries and Ledgers in the book of Alexandra Study

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To S Hood A/c 1450

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

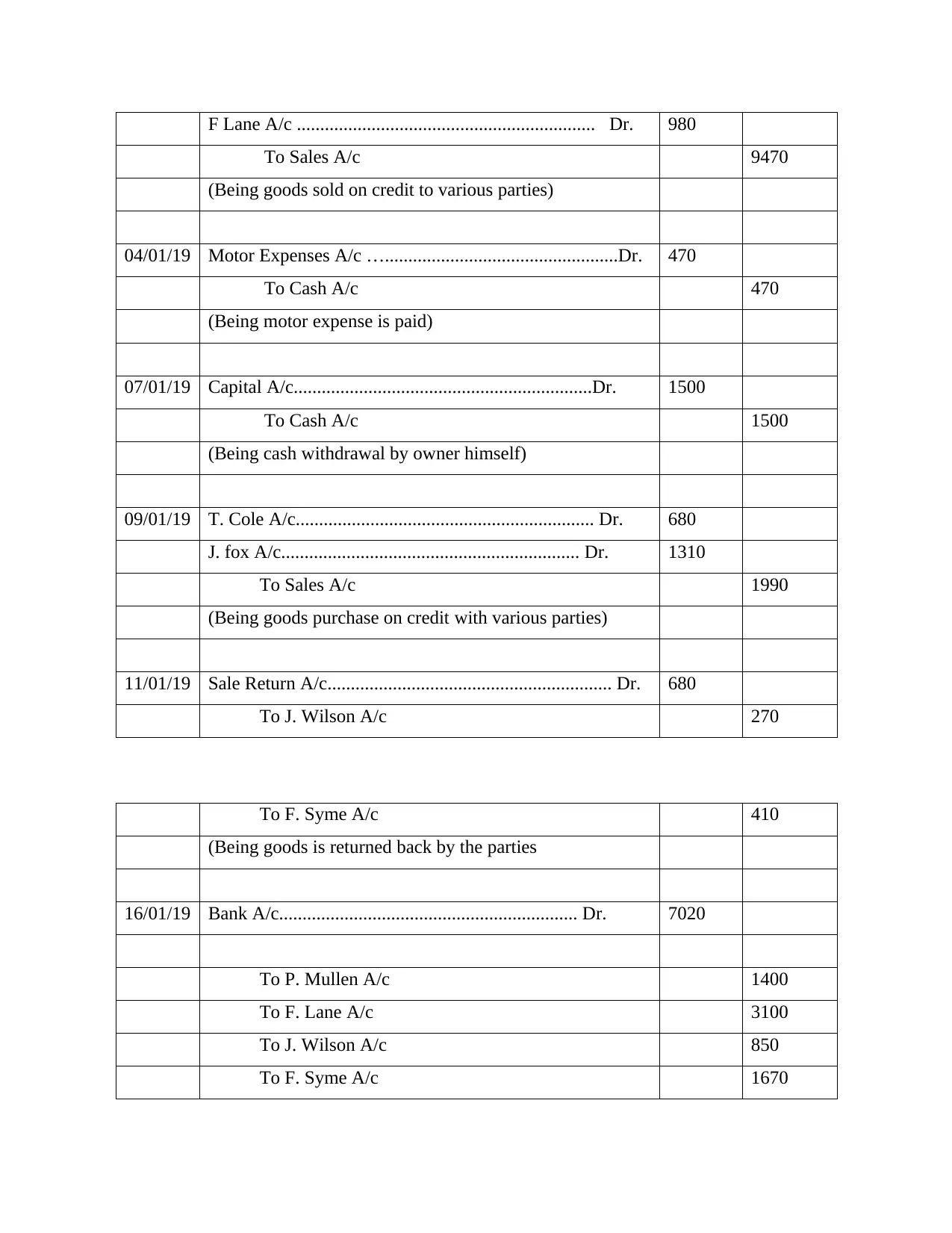

03/01/19 J Wilson A/c ................................................................ Dr. 1200

T. Cole A/c ................................................................ Dr. 1650

F. Syme A/c ................................................................Dr. 2100

J. Allen A/c ................................................................ Dr. 1020

P. White A/c ................................................................Dr. 2520

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/19 J Wilson A/c ................................................................ Dr. 1200

T. Cole A/c ................................................................ Dr. 1650

F. Syme A/c ................................................................Dr. 2100

J. Allen A/c ................................................................ Dr. 1020

P. White A/c ................................................................Dr. 2520

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

F Lane A/c ................................................................ Dr. 980

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/19 Motor Expenses A/c …..................................................Dr. 470

To Cash A/c 470

(Being motor expense is paid)

07/01/19 Capital A/c................................................................Dr. 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/19 T. Cole A/c................................................................ Dr. 680

J. fox A/c................................................................ Dr. 1310

To Sales A/c 1990

(Being goods purchase on credit with various parties)

11/01/19 Sale Return A/c............................................................. Dr. 680

To J. Wilson A/c 270

To F. Syme A/c 410

(Being goods is returned back by the parties

16/01/19 Bank A/c................................................................ Dr. 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/19 Motor Expenses A/c …..................................................Dr. 470

To Cash A/c 470

(Being motor expense is paid)

07/01/19 Capital A/c................................................................Dr. 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/19 T. Cole A/c................................................................ Dr. 680

J. fox A/c................................................................ Dr. 1310

To Sales A/c 1990

(Being goods purchase on credit with various parties)

11/01/19 Sale Return A/c............................................................. Dr. 680

To J. Wilson A/c 270

To F. Syme A/c 410

(Being goods is returned back by the parties

16/01/19 Bank A/c................................................................ Dr. 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

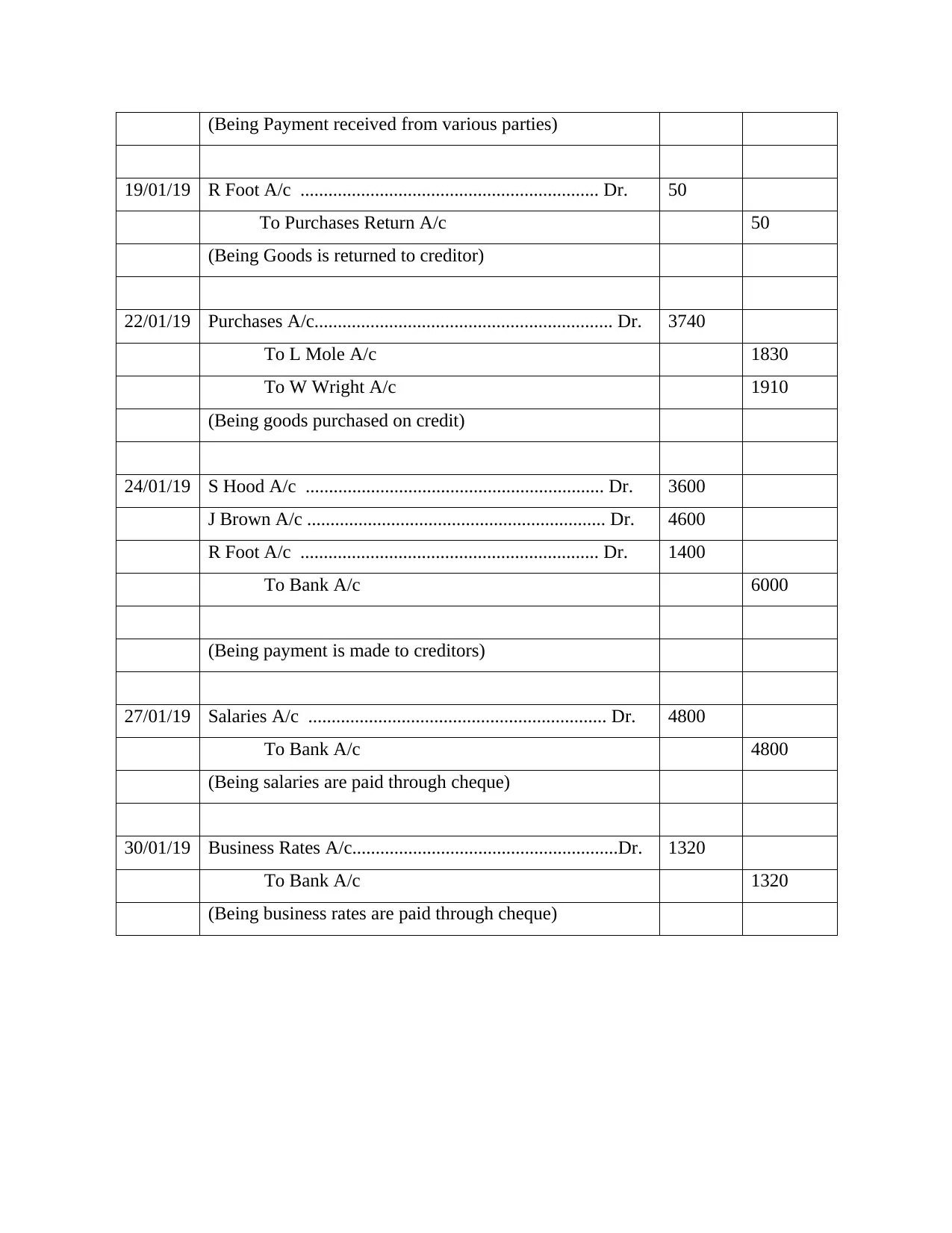

(Being Payment received from various parties)

19/01/19 R Foot A/c ................................................................ Dr. 50

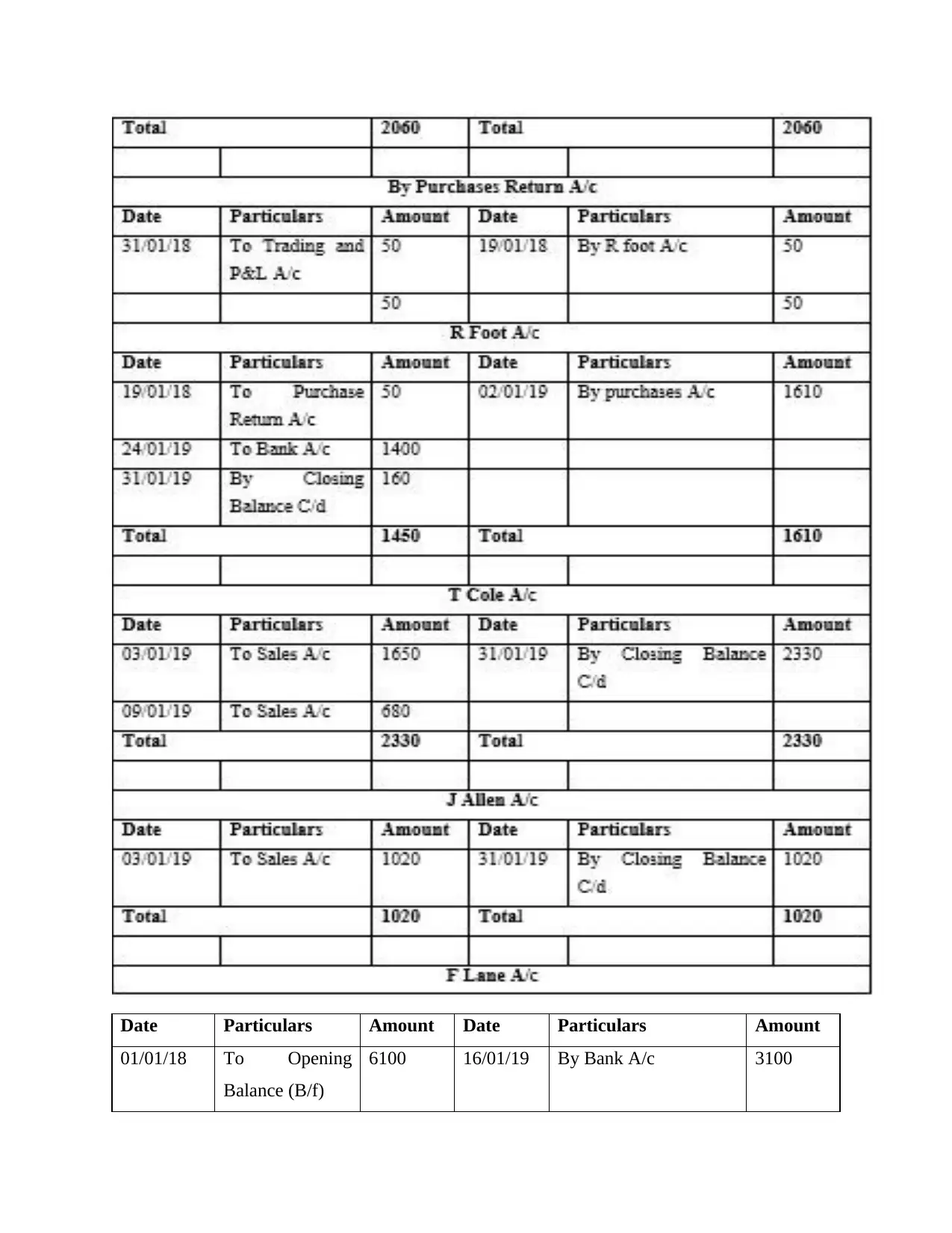

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/19 Purchases A/c................................................................ Dr. 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/19 S Hood A/c ................................................................ Dr. 3600

J Brown A/c ................................................................ Dr. 4600

R Foot A/c ................................................................ Dr. 1400

To Bank A/c 6000

(Being payment is made to creditors)

27/01/19 Salaries A/c ................................................................ Dr. 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

30/01/19 Business Rates A/c.........................................................Dr. 1320

To Bank A/c 1320

(Being business rates are paid through cheque)

19/01/19 R Foot A/c ................................................................ Dr. 50

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/19 Purchases A/c................................................................ Dr. 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/19 S Hood A/c ................................................................ Dr. 3600

J Brown A/c ................................................................ Dr. 4600

R Foot A/c ................................................................ Dr. 1400

To Bank A/c 6000

(Being payment is made to creditors)

27/01/19 Salaries A/c ................................................................ Dr. 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

30/01/19 Business Rates A/c.........................................................Dr. 1320

To Bank A/c 1320

(Being business rates are paid through cheque)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

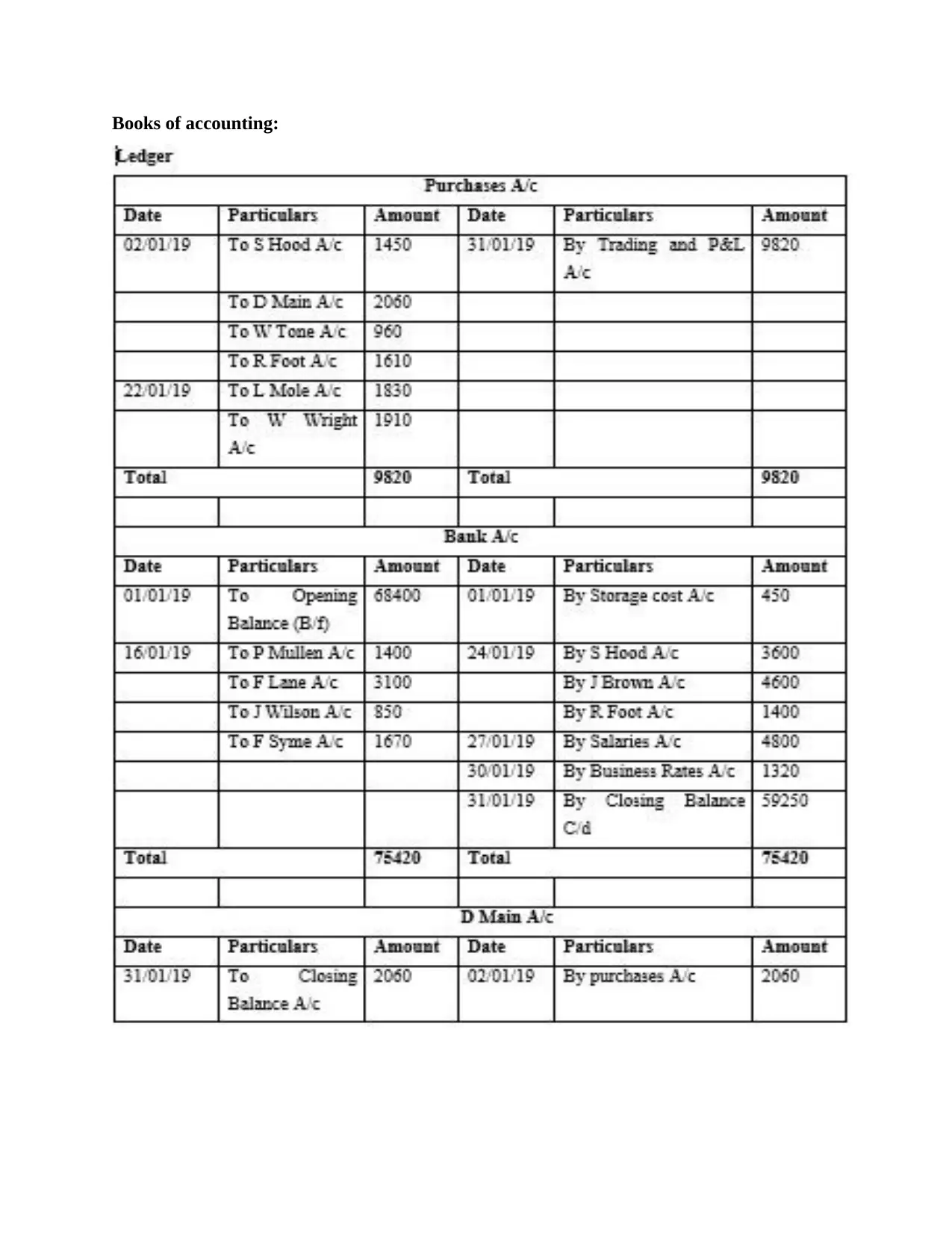

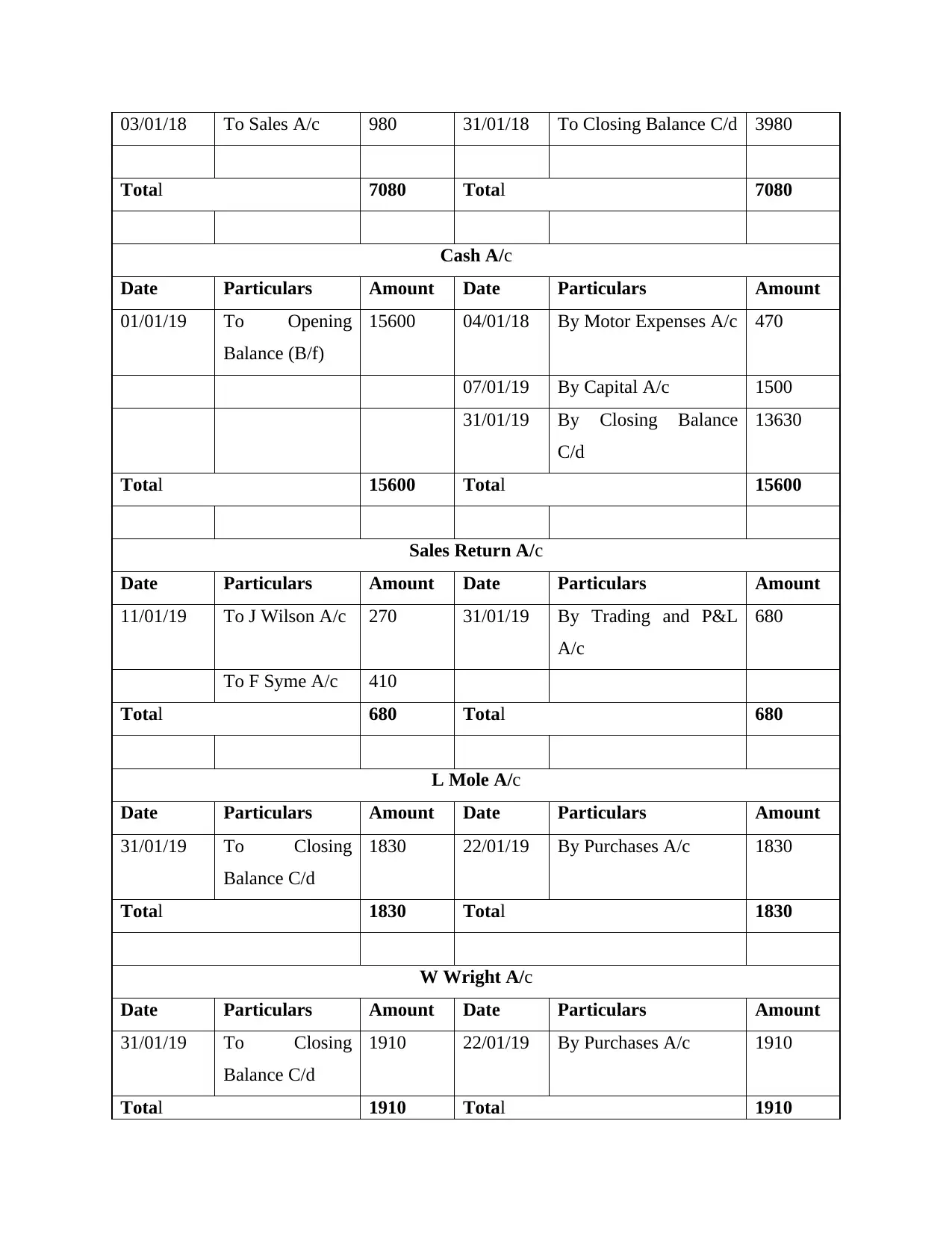

Books of accounting:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Particulars Amount Date Particulars Amount

01/01/18 To Opening

Balance (B/f)

6100 16/01/19 By Bank A/c 3100

01/01/18 To Opening

Balance (B/f)

6100 16/01/19 By Bank A/c 3100

03/01/18 To Sales A/c 980 31/01/18 To Closing Balance C/d 3980

Total 7080 Total 7080

Cash A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

15600 04/01/18 By Motor Expenses A/c 470

07/01/19 By Capital A/c 1500

31/01/19 By Closing Balance

C/d

13630

Total 15600 Total 15600

Sales Return A/c

Date Particulars Amount Date Particulars Amount

11/01/19 To J Wilson A/c 270 31/01/19 By Trading and P&L

A/c

680

To F Syme A/c 410

Total 680 Total 680

L Mole A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1830 22/01/19 By Purchases A/c 1830

Total 1830 Total 1830

W Wright A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1910 22/01/19 By Purchases A/c 1910

Total 1910 Total 1910

Total 7080 Total 7080

Cash A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

15600 04/01/18 By Motor Expenses A/c 470

07/01/19 By Capital A/c 1500

31/01/19 By Closing Balance

C/d

13630

Total 15600 Total 15600

Sales Return A/c

Date Particulars Amount Date Particulars Amount

11/01/19 To J Wilson A/c 270 31/01/19 By Trading and P&L

A/c

680

To F Syme A/c 410

Total 680 Total 680

L Mole A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1830 22/01/19 By Purchases A/c 1830

Total 1830 Total 1830

W Wright A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1910 22/01/19 By Purchases A/c 1910

Total 1910 Total 1910

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.