Financial Accounting Report: Stakeholders, Statements, and Analysis

VerifiedAdded on 2021/01/02

|25

|5660

|250

Report

AI Summary

This report provides a comprehensive overview of financial accounting, starting with definitions and purposes. It delves into accounting rules, principles, and the roles of internal and external stakeholders within a business. The report examines the qualitative characteristics of financial reporting and their impact on public limited companies. It includes detailed journal entries, ledger accounts, and a trial balance for a specific client (Alexandra Study), followed by an analysis of financial statements, including profit and loss accounts and balance sheets for another client (Munteanu Limited). The report further explores accounting concepts such as consistency and prudence, the meaning and methods of depreciation, and a comparison of financial statements prepared by sole traders and limited companies. It concludes with a discussion on the purpose of bank reconciliation statements and areas of variance between bank and personal records, and the importance of control accounts. The report offers a thorough understanding of financial accounting concepts and their practical application.

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1 Define financial accounting & purposes...................................................................................1

2. Accounting rules & principles.................................................................................................1

3. Internal & External stakeholders of business organisation......................................................2

4. Qualitative characteristic of financial reporting impact on the financial information

published by public limited companies.......................................................................................3

CLIENT 1........................................................................................................................................3

Journal Entry in the books of Alexandra Study...........................................................................4

(b) LEDGER ACCOUNTS.........................................................................................................7

c. Trial balance at 31st January 2019.........................................................................................15

CLIENT 2......................................................................................................................................16

(a) Profit and loss account of Munteanu Limited......................................................................16

(b) Balance Sheet of Munteanu Limited....................................................................................17

C. Accounts concepts such as consistency & prudency............................................................18

D. Meaning of depreciation & its methods................................................................................18

e. Evaluate the difference between financial statements prepared by the sole trader & the

limited companies......................................................................................................................19

CLIENT 3......................................................................................................................................19

1 . Purpose of BRS & why the business is facing difficulties...................................................19

2 . Areas where bank records vary from personal records........................................................20

Bank reconciliation statement....................................................................................................20

CLIENT 4......................................................................................................................................20

(a) Books of Hilly......................................................................................................................21

B .Control account.....................................................................................................................22

Client 5...........................................................................................................................................22

a. suspense account and its features...........................................................................................22

(b) Drafting of Trail Balance:....................................................................................................22

(c) Trial balance have credit balance of £ 3300 as suspense account........................................23

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1 Define financial accounting & purposes...................................................................................1

2. Accounting rules & principles.................................................................................................1

3. Internal & External stakeholders of business organisation......................................................2

4. Qualitative characteristic of financial reporting impact on the financial information

published by public limited companies.......................................................................................3

CLIENT 1........................................................................................................................................3

Journal Entry in the books of Alexandra Study...........................................................................4

(b) LEDGER ACCOUNTS.........................................................................................................7

c. Trial balance at 31st January 2019.........................................................................................15

CLIENT 2......................................................................................................................................16

(a) Profit and loss account of Munteanu Limited......................................................................16

(b) Balance Sheet of Munteanu Limited....................................................................................17

C. Accounts concepts such as consistency & prudency............................................................18

D. Meaning of depreciation & its methods................................................................................18

e. Evaluate the difference between financial statements prepared by the sole trader & the

limited companies......................................................................................................................19

CLIENT 3......................................................................................................................................19

1 . Purpose of BRS & why the business is facing difficulties...................................................19

2 . Areas where bank records vary from personal records........................................................20

Bank reconciliation statement....................................................................................................20

CLIENT 4......................................................................................................................................20

(a) Books of Hilly......................................................................................................................21

B .Control account.....................................................................................................................22

Client 5...........................................................................................................................................22

a. suspense account and its features...........................................................................................22

(b) Drafting of Trail Balance:....................................................................................................22

(c) Trial balance have credit balance of £ 3300 as suspense account........................................23

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................25

REFERENCES..............................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is a term describing the various elements of an business such as investments,

money and other financial instruments. It is the backbone of the corporation and without it

company can not start its business activities. To be successful it is necessary to manage financial

sources so that more profits can be generated (Hong and Kostovetsky, 2012). To better

understand this concept, Corporate financial solutions is selected, which is London based

company. In this report there are following topics are covered such as: financial accounting & its

purposes, internal and external stakeholders of a large organisation. Apart from this, report

discuss about journal, ledger, trial balance, sole trader and Bank reconciliation statement.

MAIN BODY

1 Define financial accounting & purposes

Financial accounting is the process of recording transaction, summarising and reporting

and analysing the information at every financial year. In Corporate financial solutions the

financial statements are prepared by the accountant (Huang and Kisgen, 2013). It involves

balance sheet, income statement etc. It help the organisation to prepare their financial statement

as per the accounting regulations. Importance of financial accounting is describe as below :

Financial accounting is important because it helpful to record the transactions.

Business organisation use financial accounting to communicate information & data to

external parties which is helpful to take important decisions (Jordà and Taylor, 2016).

Small business owners use financial accounting information to analyse competitors &

identify investment opportunities.

2. Accounting rules & principles

There are various accounting rules which are helpful to make financial statements which

are as:

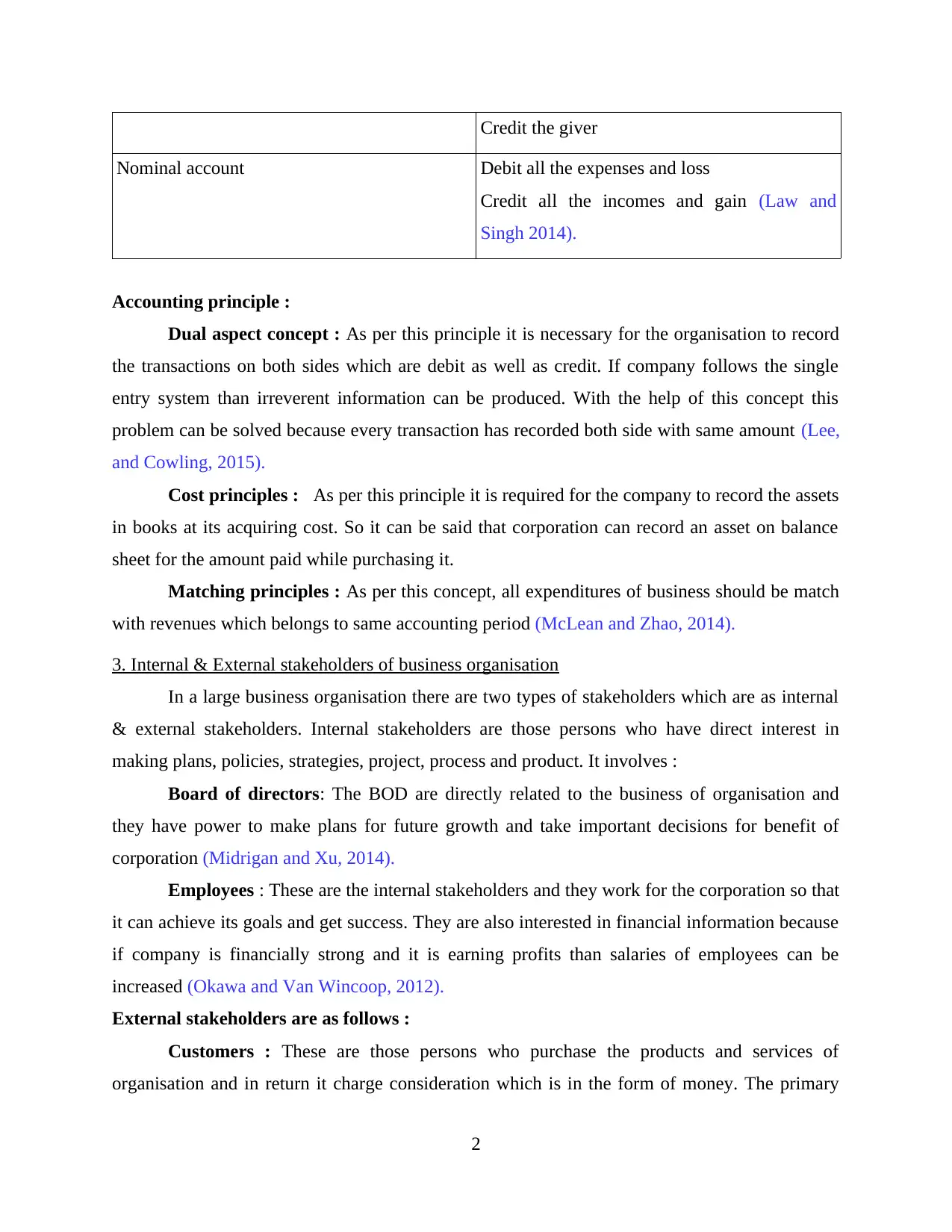

Type of account Golden rules

Real account Debit what comes into the business

Credit what goes out from the business

Personal account Debit the receiver (Kaczynski and Smith,

2014).

1

Finance is a term describing the various elements of an business such as investments,

money and other financial instruments. It is the backbone of the corporation and without it

company can not start its business activities. To be successful it is necessary to manage financial

sources so that more profits can be generated (Hong and Kostovetsky, 2012). To better

understand this concept, Corporate financial solutions is selected, which is London based

company. In this report there are following topics are covered such as: financial accounting & its

purposes, internal and external stakeholders of a large organisation. Apart from this, report

discuss about journal, ledger, trial balance, sole trader and Bank reconciliation statement.

MAIN BODY

1 Define financial accounting & purposes

Financial accounting is the process of recording transaction, summarising and reporting

and analysing the information at every financial year. In Corporate financial solutions the

financial statements are prepared by the accountant (Huang and Kisgen, 2013). It involves

balance sheet, income statement etc. It help the organisation to prepare their financial statement

as per the accounting regulations. Importance of financial accounting is describe as below :

Financial accounting is important because it helpful to record the transactions.

Business organisation use financial accounting to communicate information & data to

external parties which is helpful to take important decisions (Jordà and Taylor, 2016).

Small business owners use financial accounting information to analyse competitors &

identify investment opportunities.

2. Accounting rules & principles

There are various accounting rules which are helpful to make financial statements which

are as:

Type of account Golden rules

Real account Debit what comes into the business

Credit what goes out from the business

Personal account Debit the receiver (Kaczynski and Smith,

2014).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Credit the giver

Nominal account Debit all the expenses and loss

Credit all the incomes and gain (Law and

Singh 2014).

Accounting principle :

Dual aspect concept : As per this principle it is necessary for the organisation to record

the transactions on both sides which are debit as well as credit. If company follows the single

entry system than irreverent information can be produced. With the help of this concept this

problem can be solved because every transaction has recorded both side with same amount (Lee,

and Cowling, 2015).

Cost principles : As per this principle it is required for the company to record the assets

in books at its acquiring cost. So it can be said that corporation can record an asset on balance

sheet for the amount paid while purchasing it.

Matching principles : As per this concept, all expenditures of business should be match

with revenues which belongs to same accounting period (McLean and Zhao, 2014).

3. Internal & External stakeholders of business organisation

In a large business organisation there are two types of stakeholders which are as internal

& external stakeholders. Internal stakeholders are those persons who have direct interest in

making plans, policies, strategies, project, process and product. It involves :

Board of directors: The BOD are directly related to the business of organisation and

they have power to make plans for future growth and take important decisions for benefit of

corporation (Midrigan and Xu, 2014).

Employees : These are the internal stakeholders and they work for the corporation so that

it can achieve its goals and get success. They are also interested in financial information because

if company is financially strong and it is earning profits than salaries of employees can be

increased (Okawa and Van Wincoop, 2012).

External stakeholders are as follows :

Customers : These are those persons who purchase the products and services of

organisation and in return it charge consideration which is in the form of money. The primary

2

Nominal account Debit all the expenses and loss

Credit all the incomes and gain (Law and

Singh 2014).

Accounting principle :

Dual aspect concept : As per this principle it is necessary for the organisation to record

the transactions on both sides which are debit as well as credit. If company follows the single

entry system than irreverent information can be produced. With the help of this concept this

problem can be solved because every transaction has recorded both side with same amount (Lee,

and Cowling, 2015).

Cost principles : As per this principle it is required for the company to record the assets

in books at its acquiring cost. So it can be said that corporation can record an asset on balance

sheet for the amount paid while purchasing it.

Matching principles : As per this concept, all expenditures of business should be match

with revenues which belongs to same accounting period (McLean and Zhao, 2014).

3. Internal & External stakeholders of business organisation

In a large business organisation there are two types of stakeholders which are as internal

& external stakeholders. Internal stakeholders are those persons who have direct interest in

making plans, policies, strategies, project, process and product. It involves :

Board of directors: The BOD are directly related to the business of organisation and

they have power to make plans for future growth and take important decisions for benefit of

corporation (Midrigan and Xu, 2014).

Employees : These are the internal stakeholders and they work for the corporation so that

it can achieve its goals and get success. They are also interested in financial information because

if company is financially strong and it is earning profits than salaries of employees can be

increased (Okawa and Van Wincoop, 2012).

External stakeholders are as follows :

Customers : These are those persons who purchase the products and services of

organisation and in return it charge consideration which is in the form of money. The primary

2

focus of company is to satisfy the needs of consumers (Philippon and Reshef, 2012). They are

interested in financial information because if it financially strong than it can produce quality

products because it can use quality resources in manufacturing as a result persons get superior

products.

Suppliers : The person who provide raw material to the organisation is known as

supplier so that company can produce final products and sell it to the market. They are interested

in financial information because if corporation is financially strong than it can pay money on

time to the suppliers (Loughran and McDonald, 2016).

Government : It collect the tax form the profits which is earned by organisation and it

makes rules & regulations which are needed to be follow. They are interested in financial

information of the business as they can ascertain whether or not company is paying its all due

taxes (Guiso and Sodini, 2013).

Creditors : The person from which company can borrow money so that it can expand its

business and make future plans for expansion. In return it have to pay interest. On the basis of

financial information creditors can analyse the capability of organisation to pay the borrowed

money (Greenwood and Scharfstein, 2013).

4. Qualitative characteristic of financial reporting impact on the financial information published

by public limited companies

There are various qualitative characteristics of financial reporting which are beneficial for

the company to take important decisions. It involves: understandability, relevance, reliability and

comparability. It is necessary for the public limited companies to publish its financial statements

and it provide various information which useful in decision making process. Organisation is

impacted as they require to publish financial information in such a way that it can fulfil

relevancy & reliability feature. If these information will be reliable than important decision can

be taken for the benefit & growth of organisation (Gallagher and Koleski, 2012).

CLIENT 1

3

interested in financial information because if it financially strong than it can produce quality

products because it can use quality resources in manufacturing as a result persons get superior

products.

Suppliers : The person who provide raw material to the organisation is known as

supplier so that company can produce final products and sell it to the market. They are interested

in financial information because if corporation is financially strong than it can pay money on

time to the suppliers (Loughran and McDonald, 2016).

Government : It collect the tax form the profits which is earned by organisation and it

makes rules & regulations which are needed to be follow. They are interested in financial

information of the business as they can ascertain whether or not company is paying its all due

taxes (Guiso and Sodini, 2013).

Creditors : The person from which company can borrow money so that it can expand its

business and make future plans for expansion. In return it have to pay interest. On the basis of

financial information creditors can analyse the capability of organisation to pay the borrowed

money (Greenwood and Scharfstein, 2013).

4. Qualitative characteristic of financial reporting impact on the financial information published

by public limited companies

There are various qualitative characteristics of financial reporting which are beneficial for

the company to take important decisions. It involves: understandability, relevance, reliability and

comparability. It is necessary for the public limited companies to publish its financial statements

and it provide various information which useful in decision making process. Organisation is

impacted as they require to publish financial information in such a way that it can fulfil

relevancy & reliability feature. If these information will be reliable than important decision can

be taken for the benefit & growth of organisation (Gallagher and Koleski, 2012).

CLIENT 1

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

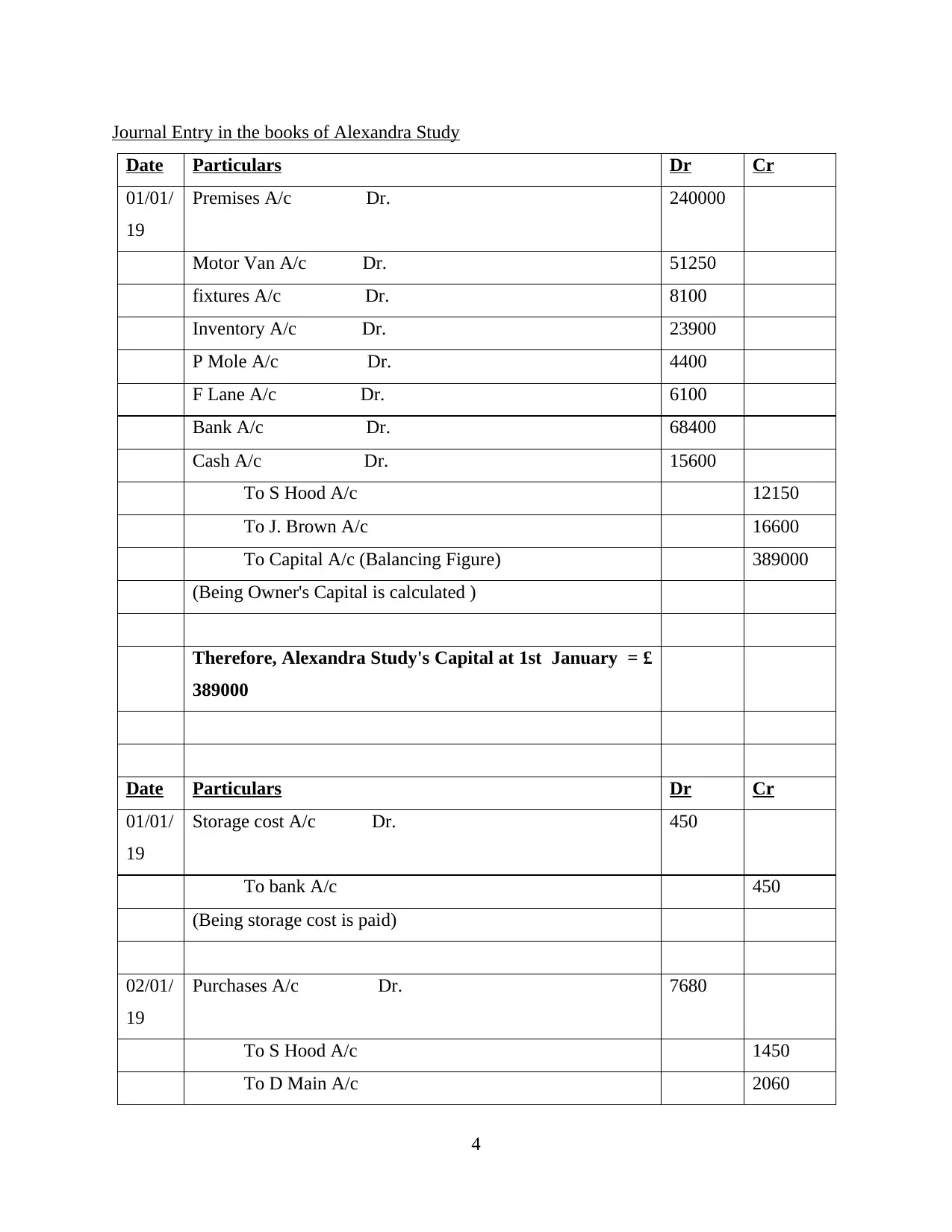

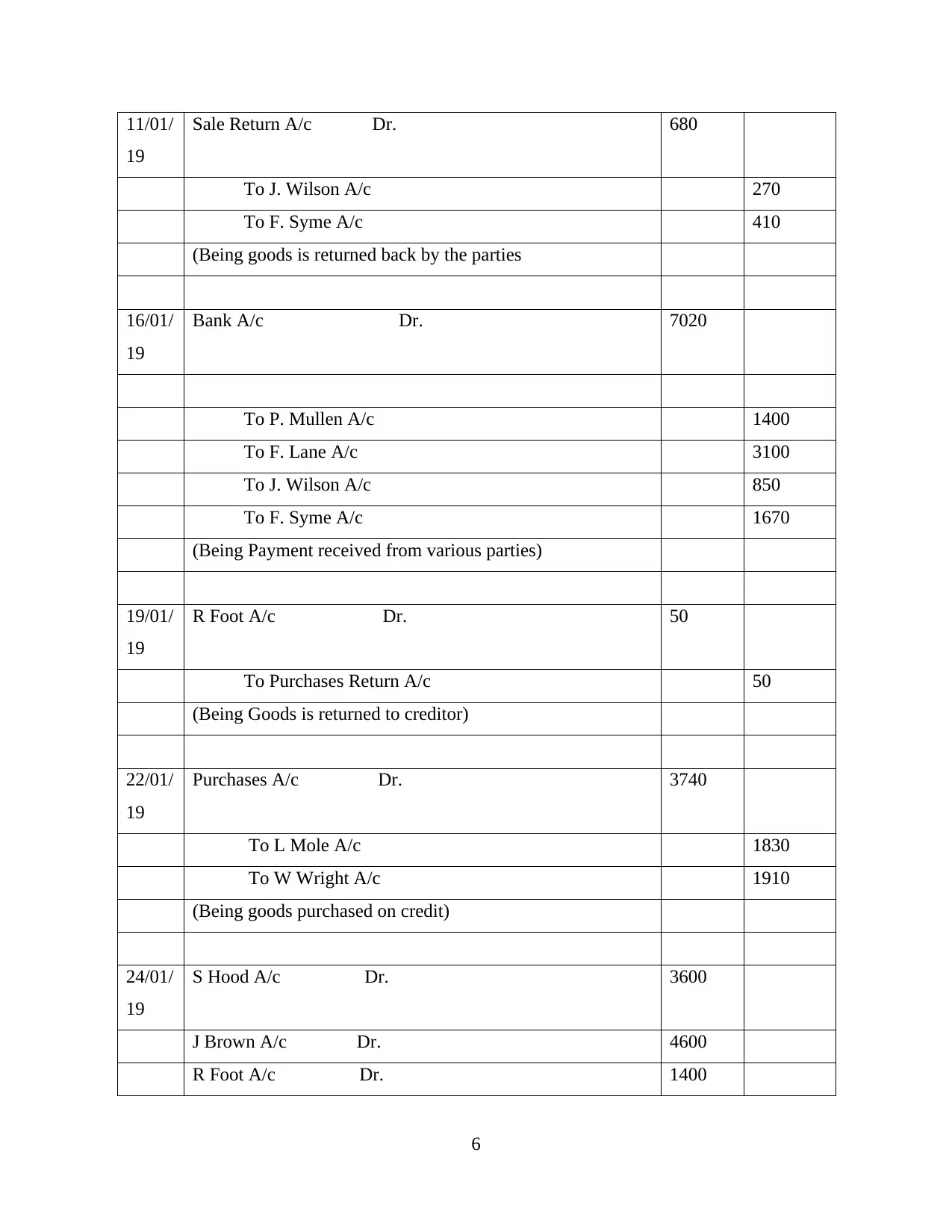

Journal Entry in the books of Alexandra Study

Date Particulars Dr Cr

01/01/

19

Premises A/c Dr. 240000

Motor Van A/c Dr. 51250

fixtures A/c Dr. 8100

Inventory A/c Dr. 23900

P Mole A/c Dr. 4400

F Lane A/c Dr. 6100

Bank A/c Dr. 68400

Cash A/c Dr. 15600

To S Hood A/c 12150

To J. Brown A/c 16600

To Capital A/c (Balancing Figure) 389000

(Being Owner's Capital is calculated )

Therefore, Alexandra Study's Capital at 1st January = £

389000

Date Particulars Dr Cr

01/01/

19

Storage cost A/c Dr. 450

To bank A/c 450

(Being storage cost is paid)

02/01/

19

Purchases A/c Dr. 7680

To S Hood A/c 1450

To D Main A/c 2060

4

Date Particulars Dr Cr

01/01/

19

Premises A/c Dr. 240000

Motor Van A/c Dr. 51250

fixtures A/c Dr. 8100

Inventory A/c Dr. 23900

P Mole A/c Dr. 4400

F Lane A/c Dr. 6100

Bank A/c Dr. 68400

Cash A/c Dr. 15600

To S Hood A/c 12150

To J. Brown A/c 16600

To Capital A/c (Balancing Figure) 389000

(Being Owner's Capital is calculated )

Therefore, Alexandra Study's Capital at 1st January = £

389000

Date Particulars Dr Cr

01/01/

19

Storage cost A/c Dr. 450

To bank A/c 450

(Being storage cost is paid)

02/01/

19

Purchases A/c Dr. 7680

To S Hood A/c 1450

To D Main A/c 2060

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

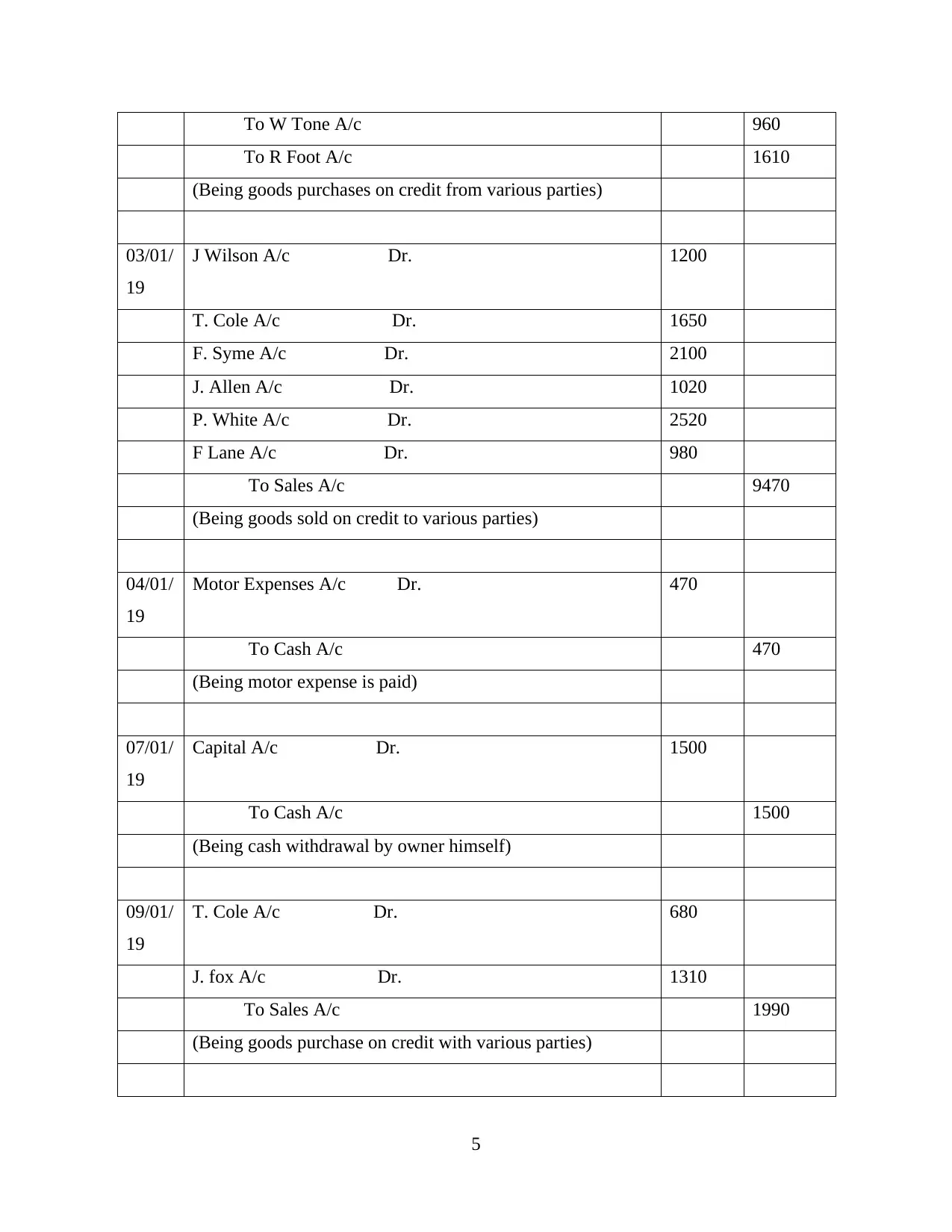

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/

19

J Wilson A/c Dr. 1200

T. Cole A/c Dr. 1650

F. Syme A/c Dr. 2100

J. Allen A/c Dr. 1020

P. White A/c Dr. 2520

F Lane A/c Dr. 980

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/

19

Motor Expenses A/c Dr. 470

To Cash A/c 470

(Being motor expense is paid)

07/01/

19

Capital A/c Dr. 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/

19

T. Cole A/c Dr. 680

J. fox A/c Dr. 1310

To Sales A/c 1990

(Being goods purchase on credit with various parties)

5

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/

19

J Wilson A/c Dr. 1200

T. Cole A/c Dr. 1650

F. Syme A/c Dr. 2100

J. Allen A/c Dr. 1020

P. White A/c Dr. 2520

F Lane A/c Dr. 980

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/

19

Motor Expenses A/c Dr. 470

To Cash A/c 470

(Being motor expense is paid)

07/01/

19

Capital A/c Dr. 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/

19

T. Cole A/c Dr. 680

J. fox A/c Dr. 1310

To Sales A/c 1990

(Being goods purchase on credit with various parties)

5

11/01/

19

Sale Return A/c Dr. 680

To J. Wilson A/c 270

To F. Syme A/c 410

(Being goods is returned back by the parties

16/01/

19

Bank A/c Dr. 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

(Being Payment received from various parties)

19/01/

19

R Foot A/c Dr. 50

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/

19

Purchases A/c Dr. 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/

19

S Hood A/c Dr. 3600

J Brown A/c Dr. 4600

R Foot A/c Dr. 1400

6

19

Sale Return A/c Dr. 680

To J. Wilson A/c 270

To F. Syme A/c 410

(Being goods is returned back by the parties

16/01/

19

Bank A/c Dr. 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

(Being Payment received from various parties)

19/01/

19

R Foot A/c Dr. 50

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/

19

Purchases A/c Dr. 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/

19

S Hood A/c Dr. 3600

J Brown A/c Dr. 4600

R Foot A/c Dr. 1400

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

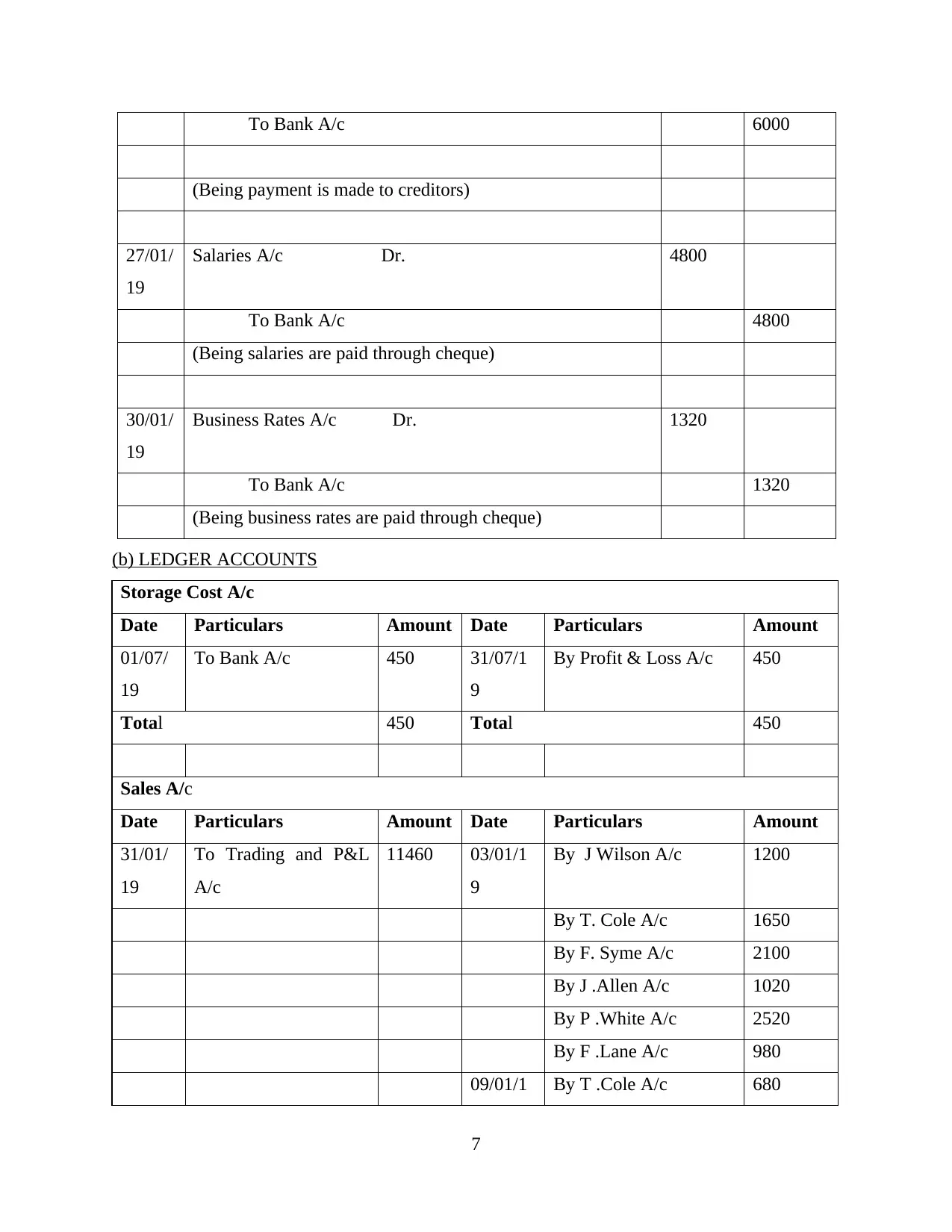

To Bank A/c 6000

(Being payment is made to creditors)

27/01/

19

Salaries A/c Dr. 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

30/01/

19

Business Rates A/c Dr. 1320

To Bank A/c 1320

(Being business rates are paid through cheque)

(b) LEDGER ACCOUNTS

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/

19

To Bank A/c 450 31/07/1

9

By Profit & Loss A/c 450

Total 450 Total 450

Sales A/c

Date Particulars Amount Date Particulars Amount

31/01/

19

To Trading and P&L

A/c

11460 03/01/1

9

By J Wilson A/c 1200

By T. Cole A/c 1650

By F. Syme A/c 2100

By J .Allen A/c 1020

By P .White A/c 2520

By F .Lane A/c 980

09/01/1 By T .Cole A/c 680

7

(Being payment is made to creditors)

27/01/

19

Salaries A/c Dr. 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

30/01/

19

Business Rates A/c Dr. 1320

To Bank A/c 1320

(Being business rates are paid through cheque)

(b) LEDGER ACCOUNTS

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/

19

To Bank A/c 450 31/07/1

9

By Profit & Loss A/c 450

Total 450 Total 450

Sales A/c

Date Particulars Amount Date Particulars Amount

31/01/

19

To Trading and P&L

A/c

11460 03/01/1

9

By J Wilson A/c 1200

By T. Cole A/c 1650

By F. Syme A/c 2100

By J .Allen A/c 1020

By P .White A/c 2520

By F .Lane A/c 980

09/01/1 By T .Cole A/c 680

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

By J fox A/c 1310

Total 11460 Total 11460

S Hood A/c

Date Particulars Amount Date Particulars Amount

24/01/

19

To Bank A/c 3600 01/01/1

9

By Opening Balance

(B/f)

12150

02/01/1

9

By purchases A/c 1450

31/01/

19

To Closing Balance

C/d

10000

Total 13600 Total 13600

W Tone A/c

Date Particulars Amount Date Particulars Amount

31/01/

19

To Closing Balance

C/d

960 02/01/1

9

By purchases A/c 960

Total 960 Total 960

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/

19

To Sales A/c 1200 11/01/1

9

By Sales Return A/c 270

16/01/1

9

By Bank A/c 850

31/01/1

9

By Closing Balance c/d 80

Total 1200 Total 1200

8

By J fox A/c 1310

Total 11460 Total 11460

S Hood A/c

Date Particulars Amount Date Particulars Amount

24/01/

19

To Bank A/c 3600 01/01/1

9

By Opening Balance

(B/f)

12150

02/01/1

9

By purchases A/c 1450

31/01/

19

To Closing Balance

C/d

10000

Total 13600 Total 13600

W Tone A/c

Date Particulars Amount Date Particulars Amount

31/01/

19

To Closing Balance

C/d

960 02/01/1

9

By purchases A/c 960

Total 960 Total 960

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/

19

To Sales A/c 1200 11/01/1

9

By Sales Return A/c 270

16/01/1

9

By Bank A/c 850

31/01/1

9

By Closing Balance c/d 80

Total 1200 Total 1200

8

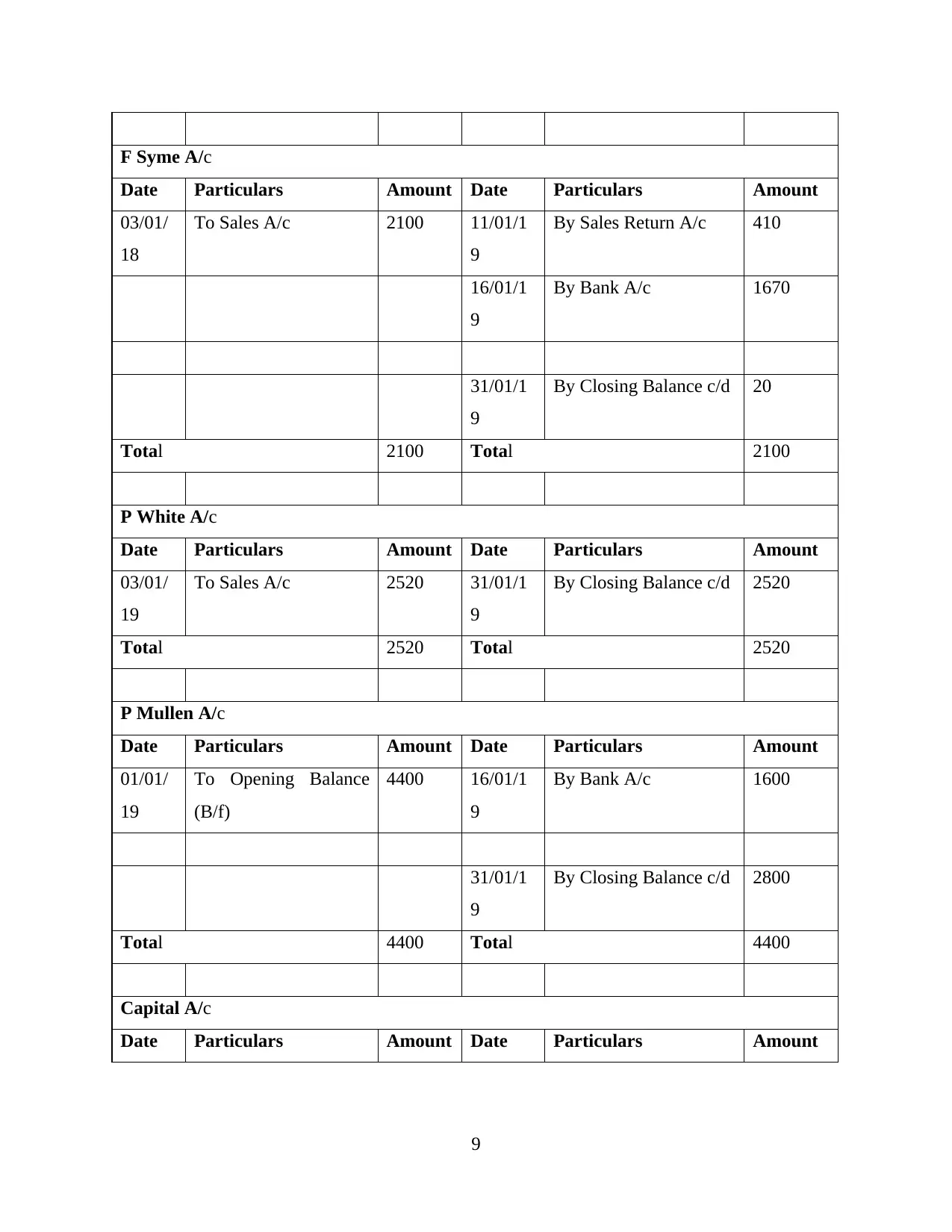

F Syme A/c

Date Particulars Amount Date Particulars Amount

03/01/

18

To Sales A/c 2100 11/01/1

9

By Sales Return A/c 410

16/01/1

9

By Bank A/c 1670

31/01/1

9

By Closing Balance c/d 20

Total 2100 Total 2100

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/

19

To Sales A/c 2520 31/01/1

9

By Closing Balance c/d 2520

Total 2520 Total 2520

P Mullen A/c

Date Particulars Amount Date Particulars Amount

01/01/

19

To Opening Balance

(B/f)

4400 16/01/1

9

By Bank A/c 1600

31/01/1

9

By Closing Balance c/d 2800

Total 4400 Total 4400

Capital A/c

Date Particulars Amount Date Particulars Amount

9

Date Particulars Amount Date Particulars Amount

03/01/

18

To Sales A/c 2100 11/01/1

9

By Sales Return A/c 410

16/01/1

9

By Bank A/c 1670

31/01/1

9

By Closing Balance c/d 20

Total 2100 Total 2100

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/

19

To Sales A/c 2520 31/01/1

9

By Closing Balance c/d 2520

Total 2520 Total 2520

P Mullen A/c

Date Particulars Amount Date Particulars Amount

01/01/

19

To Opening Balance

(B/f)

4400 16/01/1

9

By Bank A/c 1600

31/01/1

9

By Closing Balance c/d 2800

Total 4400 Total 4400

Capital A/c

Date Particulars Amount Date Particulars Amount

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.