Financial Accounting Report: Client Cases and Analysis

VerifiedAdded on 2023/02/07

|23

|3722

|28

Report

AI Summary

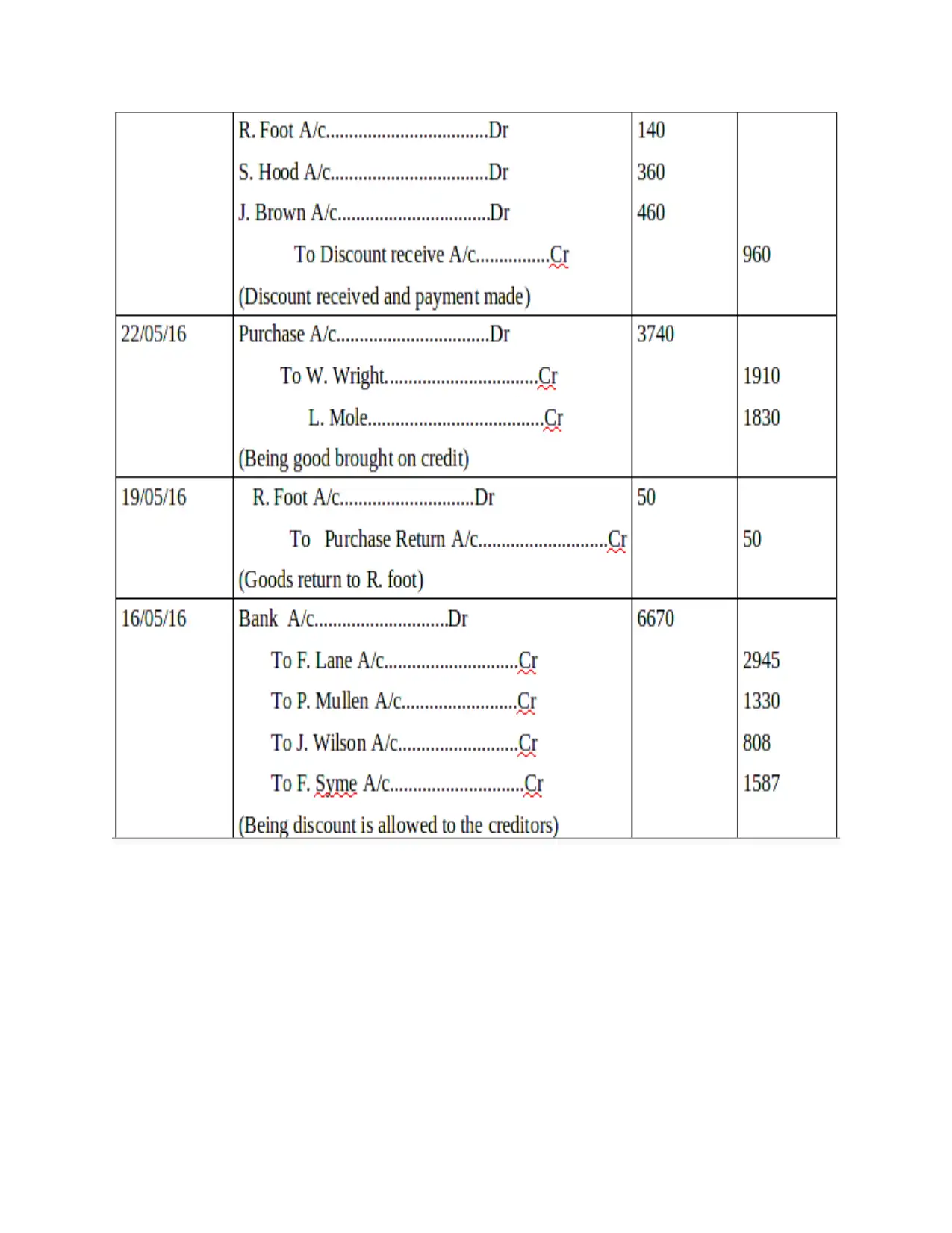

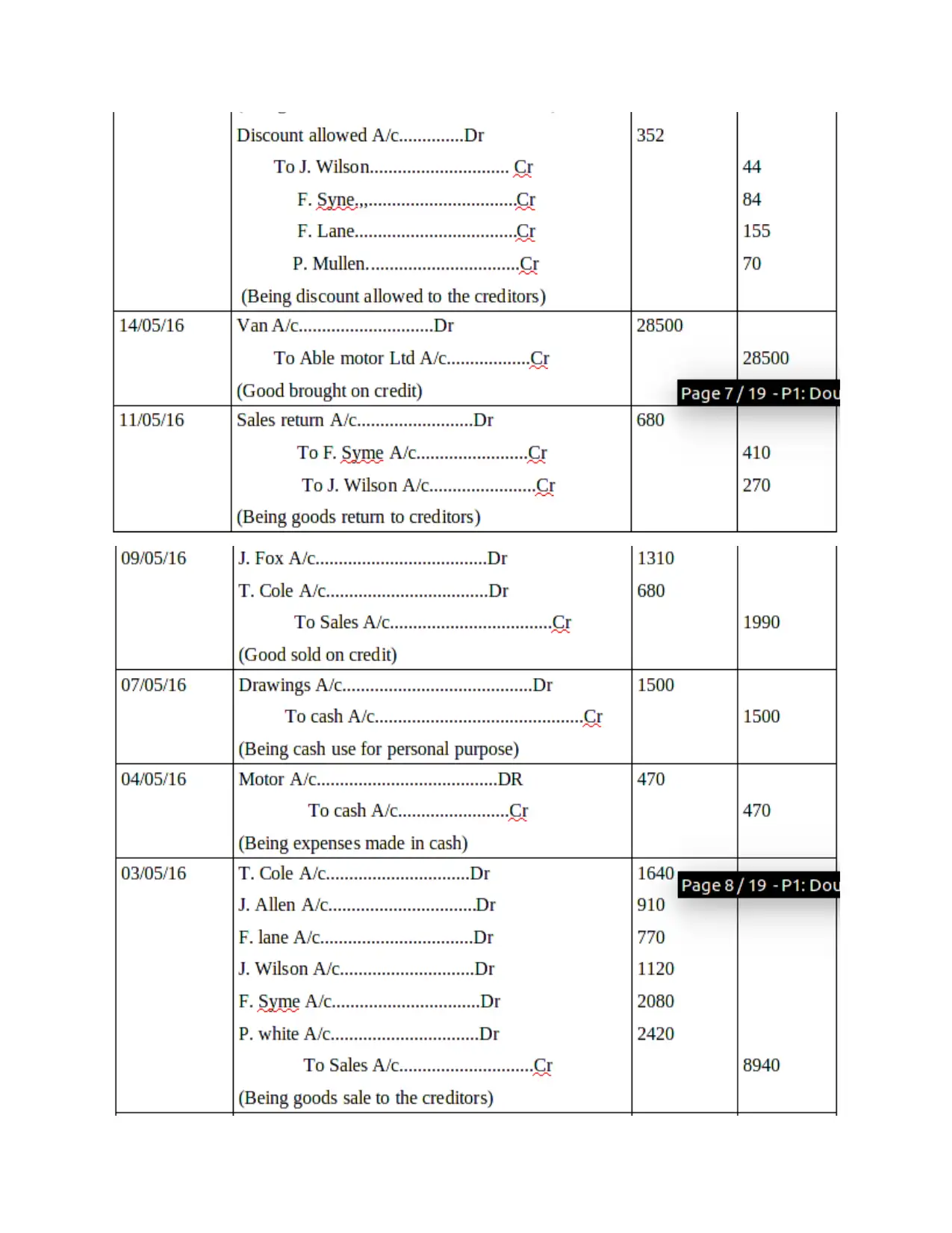

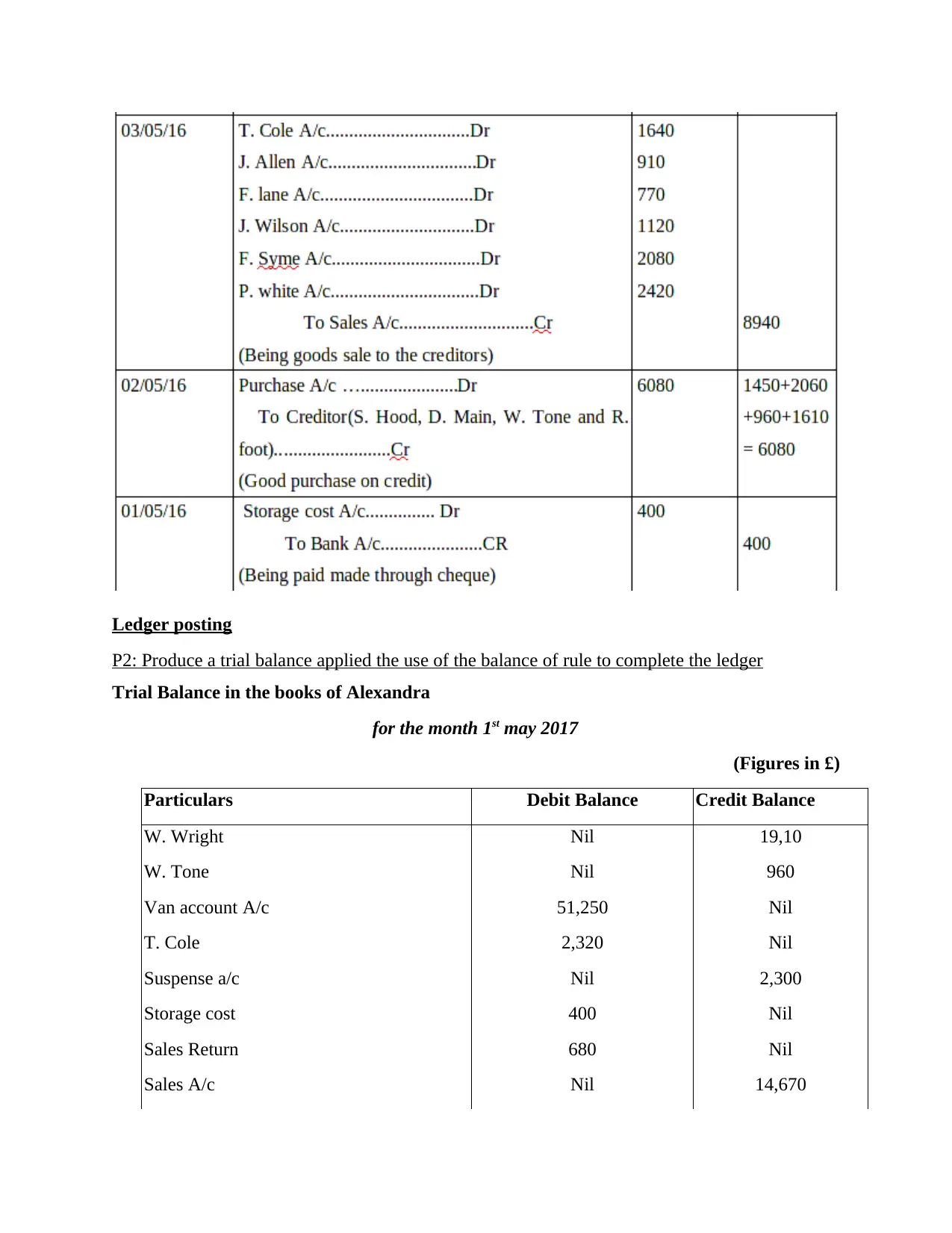

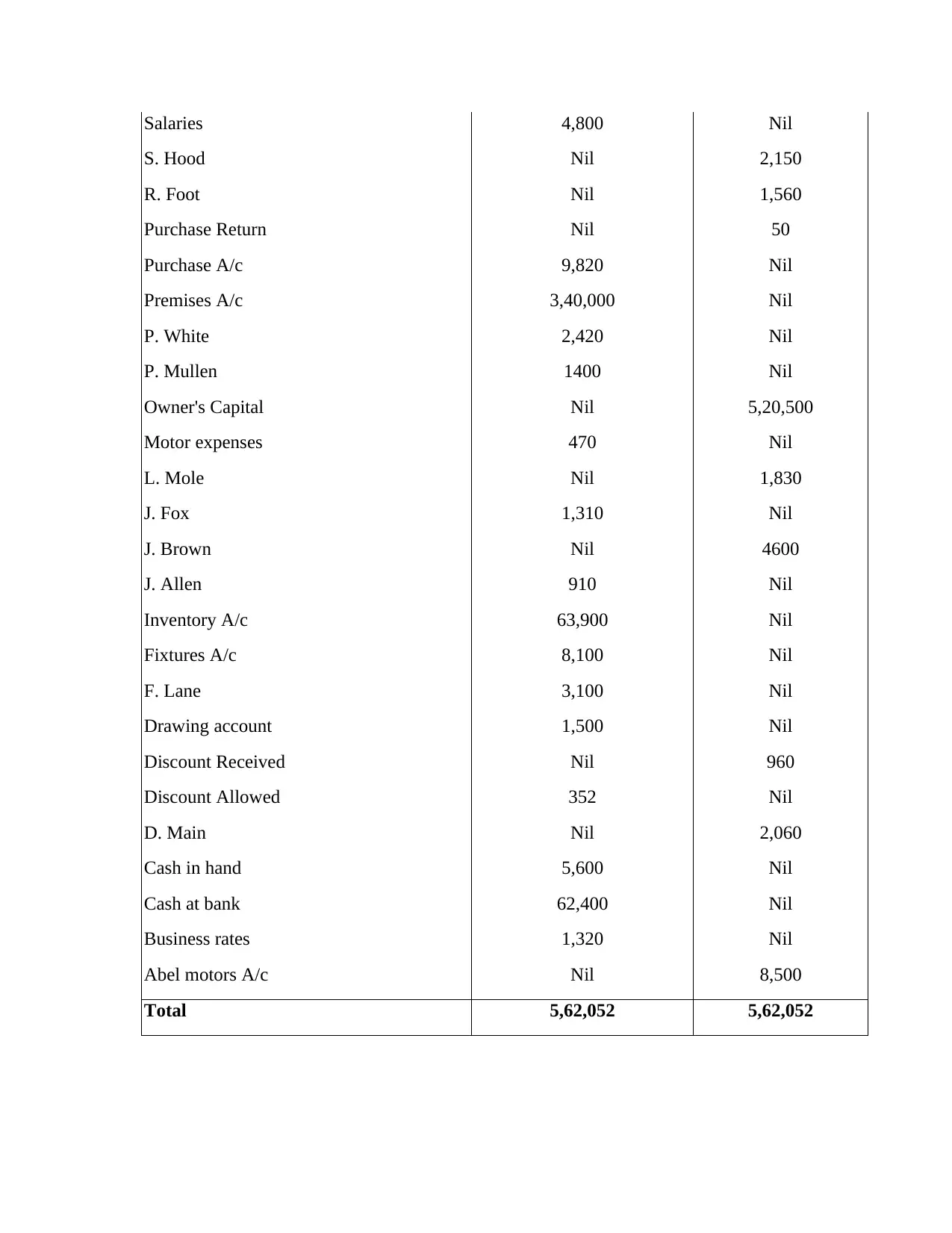

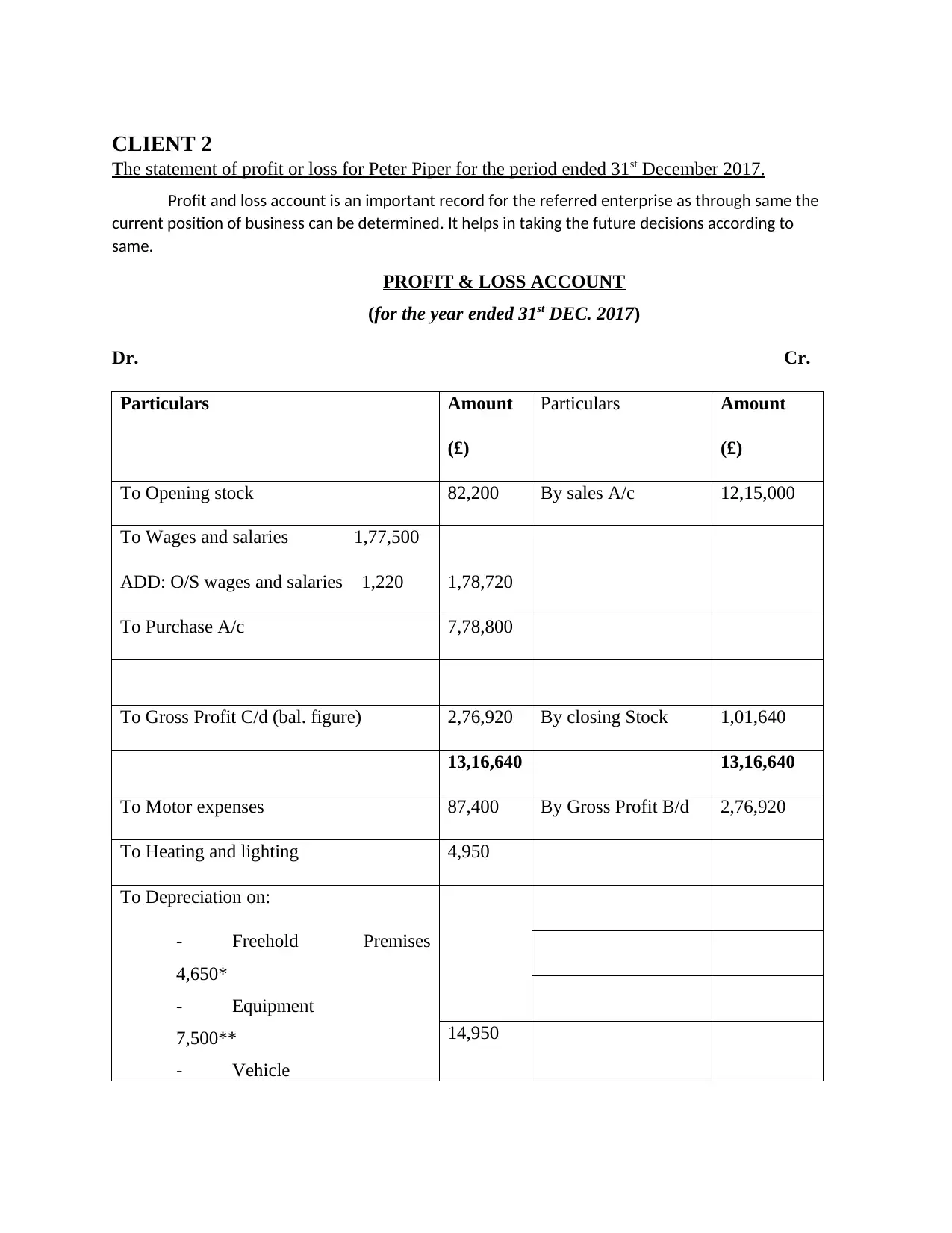

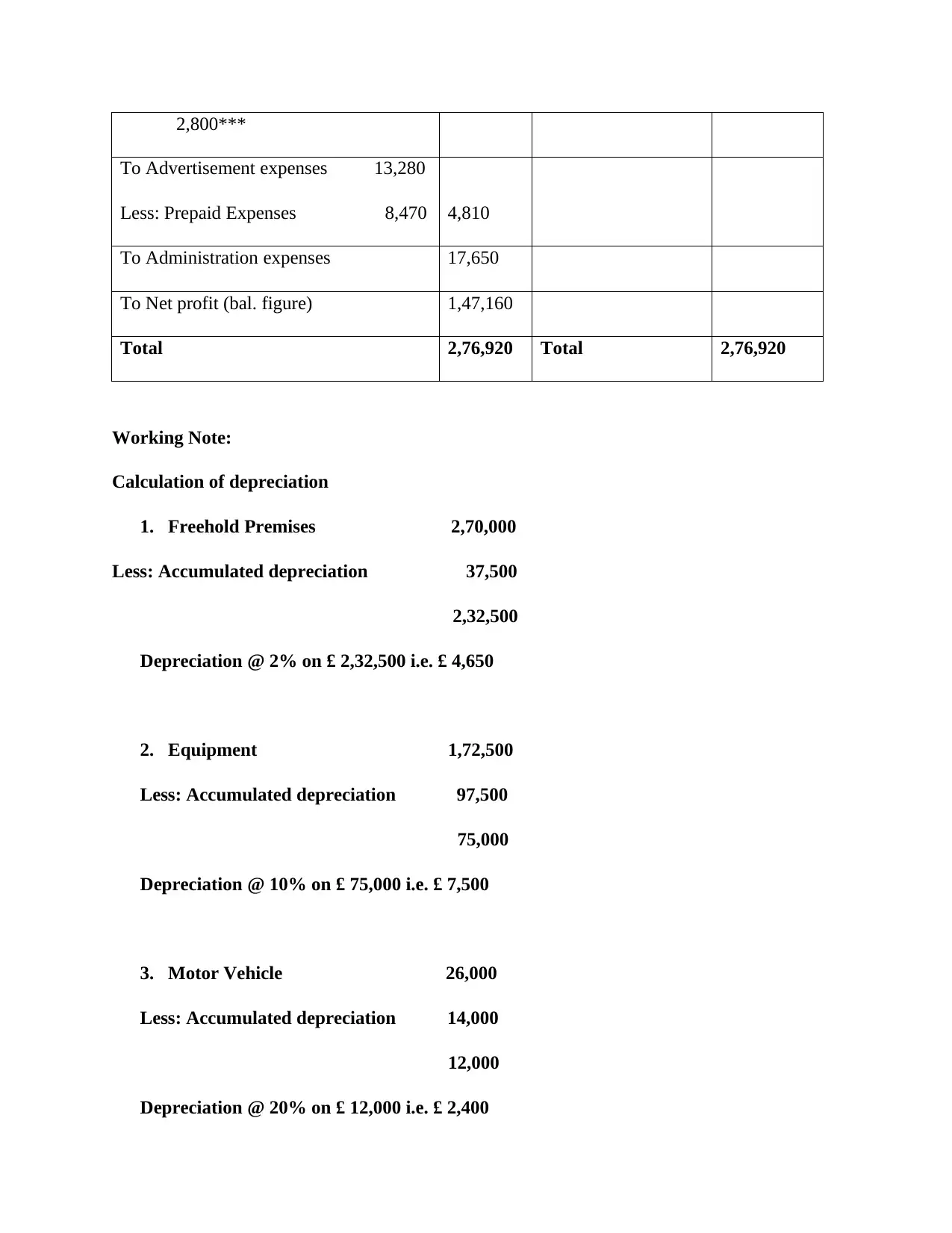

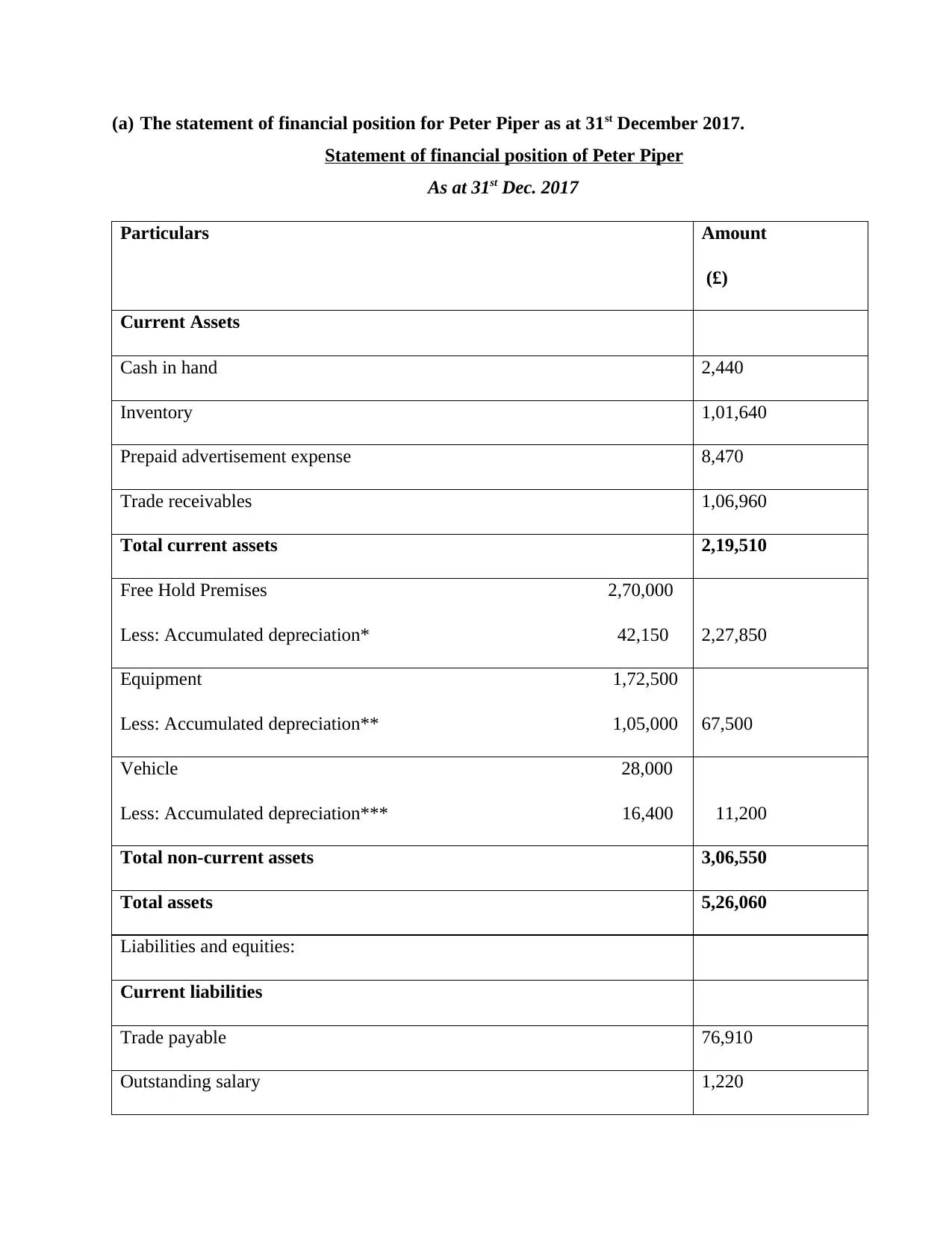

This report provides a comprehensive analysis of financial accounting principles and practices. It begins with an introduction to financial accounting, defining its role in business and outlining key financial statements such as the profit and loss account, balance sheet, and cash flow statement. The report then delves into the double-entry system, accrual basis of accounting, and accounting rules and regulations. It includes detailed case studies of various clients, demonstrating the application of accounting principles through double-entry recording, trial balances, and the preparation of financial statements like profit and loss accounts and statements of financial position. The report also covers ledger control accounts and the reconciliation process. Furthermore, it explores accounting concepts such as consistency and prudence, providing a well-rounded understanding of financial accounting for business operations. The report is a valuable resource for students seeking to understand and apply financial accounting principles.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.