Financial Accounting Report: In-depth Analysis of Financial Accounting

VerifiedAdded on 2020/10/05

|19

|4339

|392

Report

AI Summary

This report provides a comprehensive overview of financial accounting, covering fundamental concepts, and practical applications. It begins by defining financial accounting and its purposes, emphasizing its role in recording and summarizing financial transactions for both internal and external stakeholders. The report then delves into double-entry recording, journal entries, and the preparation of a trial balance for a specific client. Further, it includes detailed financial statements such as the statement of profit and loss and the statement of financial position for a company, along with explanations of key accounting concepts like consistency and prudence, as well as the role of depreciation. The report also explores the differences between financial statements prepared by sole traders and limited companies. Additional topics include the purpose of bank reconciliation statements, the implications of imprest systems, and the use of suspense accounts. The report concludes with a critical evaluation of these concepts, offering insights into the practical application of financial accounting principles.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

A.1). Defining Financial accounting and its purposes................................................................1

2. Identifying the use of the financial information of a company to the internal and stakeholder

of an organisation........................................................................................................................2

CLIENT 1........................................................................................................................................3

Double entry recording for the relevant journals and trail balance 31st January 2019...............3

CLIENT 2........................................................................................................................................6

A). Statement of profit and loss of Munteanu Ltd, for the year ended 31st Dec 2018...............6

B). Statement of financial position of Munteanu Ltd. As at 31st December 2018.....................7

C). Explaining the accounting concept of consistency and prudency.........................................7

d). Describing the purpose of depreciation in formulating accounting standards.......................8

e). Critically evaluating the difference between the financial statement prepared by the sole

trader and limited companies......................................................................................................9

CLIENT 3......................................................................................................................................10

A). Explaining the purpose of bank reconciliation statement and its requirement of preparing

every month...............................................................................................................................10

B). Explaining some areas which may cause varies in the bank statement.............................10

C). Explaining the term “Imprest” as used in a petty cash book...............................................11

D). Update the Burcu Ltd' s cash-book for September 2018 and bank reconciliation statement

as at 30 September 2018...........................................................................................................11

CLIENT 4......................................................................................................................................12

B). Explaining the control account...........................................................................................13

CLIENT 5......................................................................................................................................14

A). What is suspense account and what are the main features of suspense accounts...............14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

A.1). Defining Financial accounting and its purposes................................................................1

2. Identifying the use of the financial information of a company to the internal and stakeholder

of an organisation........................................................................................................................2

CLIENT 1........................................................................................................................................3

Double entry recording for the relevant journals and trail balance 31st January 2019...............3

CLIENT 2........................................................................................................................................6

A). Statement of profit and loss of Munteanu Ltd, for the year ended 31st Dec 2018...............6

B). Statement of financial position of Munteanu Ltd. As at 31st December 2018.....................7

C). Explaining the accounting concept of consistency and prudency.........................................7

d). Describing the purpose of depreciation in formulating accounting standards.......................8

e). Critically evaluating the difference between the financial statement prepared by the sole

trader and limited companies......................................................................................................9

CLIENT 3......................................................................................................................................10

A). Explaining the purpose of bank reconciliation statement and its requirement of preparing

every month...............................................................................................................................10

B). Explaining some areas which may cause varies in the bank statement.............................10

C). Explaining the term “Imprest” as used in a petty cash book...............................................11

D). Update the Burcu Ltd' s cash-book for September 2018 and bank reconciliation statement

as at 30 September 2018...........................................................................................................11

CLIENT 4......................................................................................................................................12

B). Explaining the control account...........................................................................................13

CLIENT 5......................................................................................................................................14

A). What is suspense account and what are the main features of suspense accounts...............14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Financial can be termed as an important field for any organisation. It assists in recording

and summarizing the financial transaction of the company which stimulate the process of

preparing the financial statements and financial reporting which are essential for the external

users. The preset report will assist in understanding the different concepts of financial accounting

and the purpose of preparing it. Further, the report will highlight the different accounting

statements for the different clients which assist in providing deep insight of the financial

accounting.

A.1). Defining Financial accounting and its purposes.

It can be termed as a specialised branch of accounting which will assist the company in

keeping track of all the financial transaction of a company. Financial accounting consist of some

guidelines which assist the company in recording and keeping the transaction in a particular

manner. Th financial accounting is very essential as it will assist in making the financial

statement or the final accounts of the company (What is Financial Accounting? , 2019).

Financial accounting users an established accounting principles that are framed by the

accounting board such as GAAP, IASB and IAS. In other words, it can be said that financial

accounting can be termed as the way of recording and reporting business activity and financial

information to investors, creditors and other people outside the business organisation which will

assist them in taking decisions regarding the financial performance of the business and stimulate

their decision making process.

Financial statement can be prepared in an accounting period which can be quarterly, half-

yearly or annually. It can be said this statement are prepared for the external users, thus financial

reporting is considered as very essential process of the growth and development of a company.

The purpose of the financial statements or the purpose of financial accounting are as follows:

One of the main purpose of the financial accounting is to provide information to the

company's management and the outside users regarding the financial performance of the

company (Edwards, 2013).

Financial accounting helps in preparing the final accounts of the company in the form of

financial statements.

1

Financial can be termed as an important field for any organisation. It assists in recording

and summarizing the financial transaction of the company which stimulate the process of

preparing the financial statements and financial reporting which are essential for the external

users. The preset report will assist in understanding the different concepts of financial accounting

and the purpose of preparing it. Further, the report will highlight the different accounting

statements for the different clients which assist in providing deep insight of the financial

accounting.

A.1). Defining Financial accounting and its purposes.

It can be termed as a specialised branch of accounting which will assist the company in

keeping track of all the financial transaction of a company. Financial accounting consist of some

guidelines which assist the company in recording and keeping the transaction in a particular

manner. Th financial accounting is very essential as it will assist in making the financial

statement or the final accounts of the company (What is Financial Accounting? , 2019).

Financial accounting users an established accounting principles that are framed by the

accounting board such as GAAP, IASB and IAS. In other words, it can be said that financial

accounting can be termed as the way of recording and reporting business activity and financial

information to investors, creditors and other people outside the business organisation which will

assist them in taking decisions regarding the financial performance of the business and stimulate

their decision making process.

Financial statement can be prepared in an accounting period which can be quarterly, half-

yearly or annually. It can be said this statement are prepared for the external users, thus financial

reporting is considered as very essential process of the growth and development of a company.

The purpose of the financial statements or the purpose of financial accounting are as follows:

One of the main purpose of the financial accounting is to provide information to the

company's management and the outside users regarding the financial performance of the

company (Edwards, 2013).

Financial accounting helps in preparing the final accounts of the company in the form of

financial statements.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting overall purpose is to create the information to the external users to

base their financial decisions on whether to invest money in the company or not.

2. Identifying the use of the financial information of a company to the internal and stakeholder of

an organisation.

The stakeholders of the company can be termed as the individuals, group or the

companies who are interested in organisation's affairs, its business activity and growth. They are

one who has some benefit or interest with the company (Weil, Schipper and Francis, 2013). This

stakeholder van be affected or can affect the business operations and development of an

organisation. In large organisations, there are two types of stakeholders internal and externals.

Both the internal and external stakeholders are very essential for an organisation, they are keen to

know the business performance and increasing in profitability (Beatty and Liao, 2014). Financial

accounting and its statements serves as an essential source of information which assist them in

order to know and make the essential decisions.

Internals Stakeholders:

Internal stakeholders are the individual or group who are directly or financially involves

in the organization. The two main internals' stakeholder in the business entity are their

employees and board members. They are directly concerns as they are directly connected to the

success of the firm

Employees: They are the one who perform and works for the business growth and

development. Financial information will assist them knowing their contribution in the financial

performance. Through this information, they can also get to know their future in the business and

will help in increasing the employee involvement in and understanding of the business.

Board members: They are the group of persons who are responsible in making policies

and goals of the company (Edmonds and et.al., 2013). They are the one who makes the strategies

for the enhancement of the business performance. It can be said that, financial information is

very essential for them in order to access the return off their earning from the firm. Financial

information will assist them in analysing the profitability, liquidity and cash flow of the

organisation which help in their decision and strategies related process.

Eternal Stakeholder:

2

base their financial decisions on whether to invest money in the company or not.

2. Identifying the use of the financial information of a company to the internal and stakeholder of

an organisation.

The stakeholders of the company can be termed as the individuals, group or the

companies who are interested in organisation's affairs, its business activity and growth. They are

one who has some benefit or interest with the company (Weil, Schipper and Francis, 2013). This

stakeholder van be affected or can affect the business operations and development of an

organisation. In large organisations, there are two types of stakeholders internal and externals.

Both the internal and external stakeholders are very essential for an organisation, they are keen to

know the business performance and increasing in profitability (Beatty and Liao, 2014). Financial

accounting and its statements serves as an essential source of information which assist them in

order to know and make the essential decisions.

Internals Stakeholders:

Internal stakeholders are the individual or group who are directly or financially involves

in the organization. The two main internals' stakeholder in the business entity are their

employees and board members. They are directly concerns as they are directly connected to the

success of the firm

Employees: They are the one who perform and works for the business growth and

development. Financial information will assist them knowing their contribution in the financial

performance. Through this information, they can also get to know their future in the business and

will help in increasing the employee involvement in and understanding of the business.

Board members: They are the group of persons who are responsible in making policies

and goals of the company (Edmonds and et.al., 2013). They are the one who makes the strategies

for the enhancement of the business performance. It can be said that, financial information is

very essential for them in order to access the return off their earning from the firm. Financial

information will assist them in analysing the profitability, liquidity and cash flow of the

organisation which help in their decision and strategies related process.

Eternal Stakeholder:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

They can be termed as the individuals, group or the company that are not the part of the

organisation but are indirectly connected to the organisation. They are the outside parties which

are form a part of the company and are affected by the work and the performance of the

company. The main external stakeholder of the company are as follows:

Customers: they are the one whop consumes goods and services of the organisation.

They are the most essential source which created revenue for the organisation. Customer can use

the financial information of the company in order to judge the stability and survival of the

company for the longer time.

Competitors: these are the rivals of the company in the industry which will make

strategies by identifying the financial statement of other company in order to gain the

competitive advantage in industry by evaluating their financial position (Marshall, McManus and

Viele, 2011).

Shareholders or investors: They are considered as the main source of earning for the

organisation which are invested their money in the company. They are the main person who are

considered with the financial performance of the company. They can use the financial

information in order to evaluate the ability if the company to return their money.

Government: They are the authority which are interested in knowing the financial

performance of the company in order to pay the right amount of taxes and relevant to laws that

are being adhered.

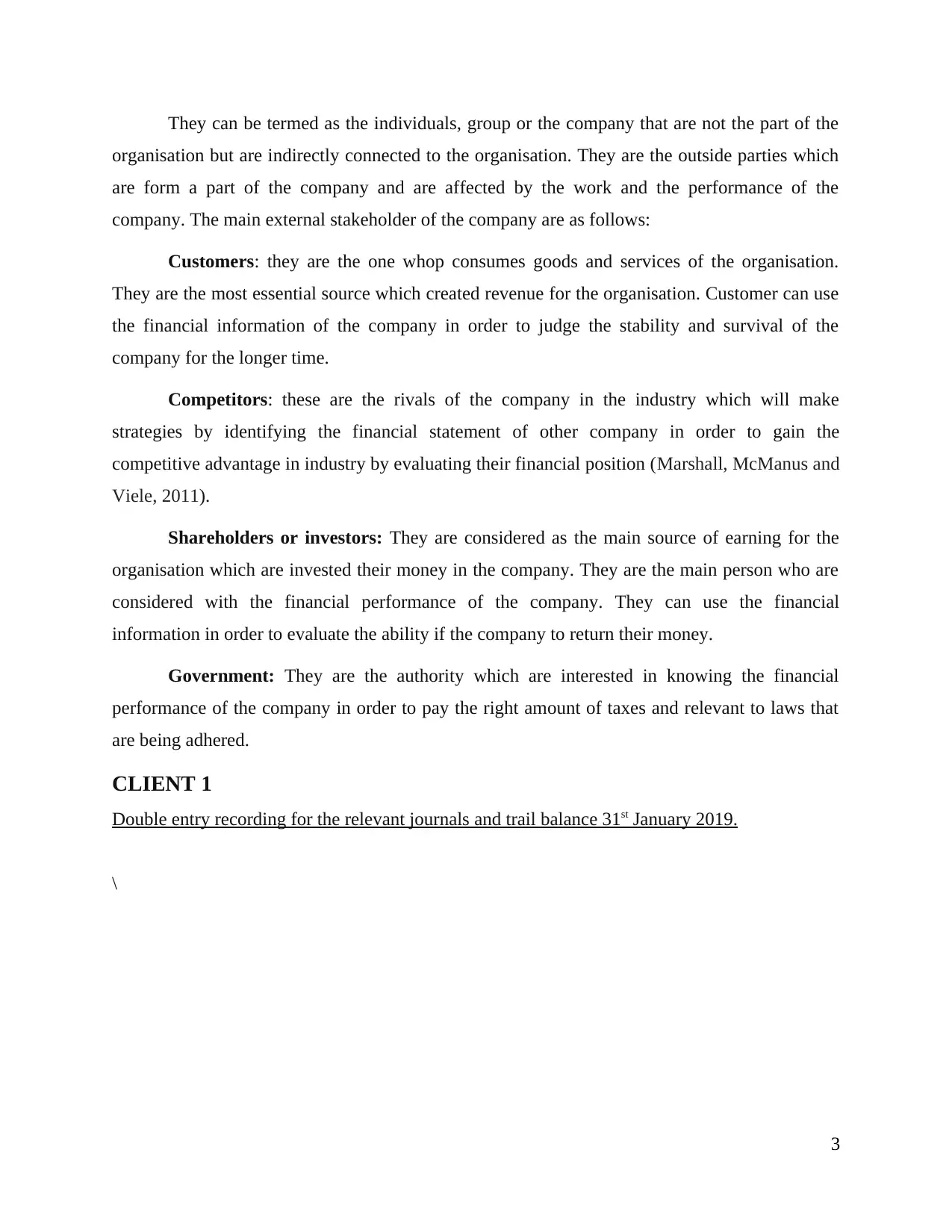

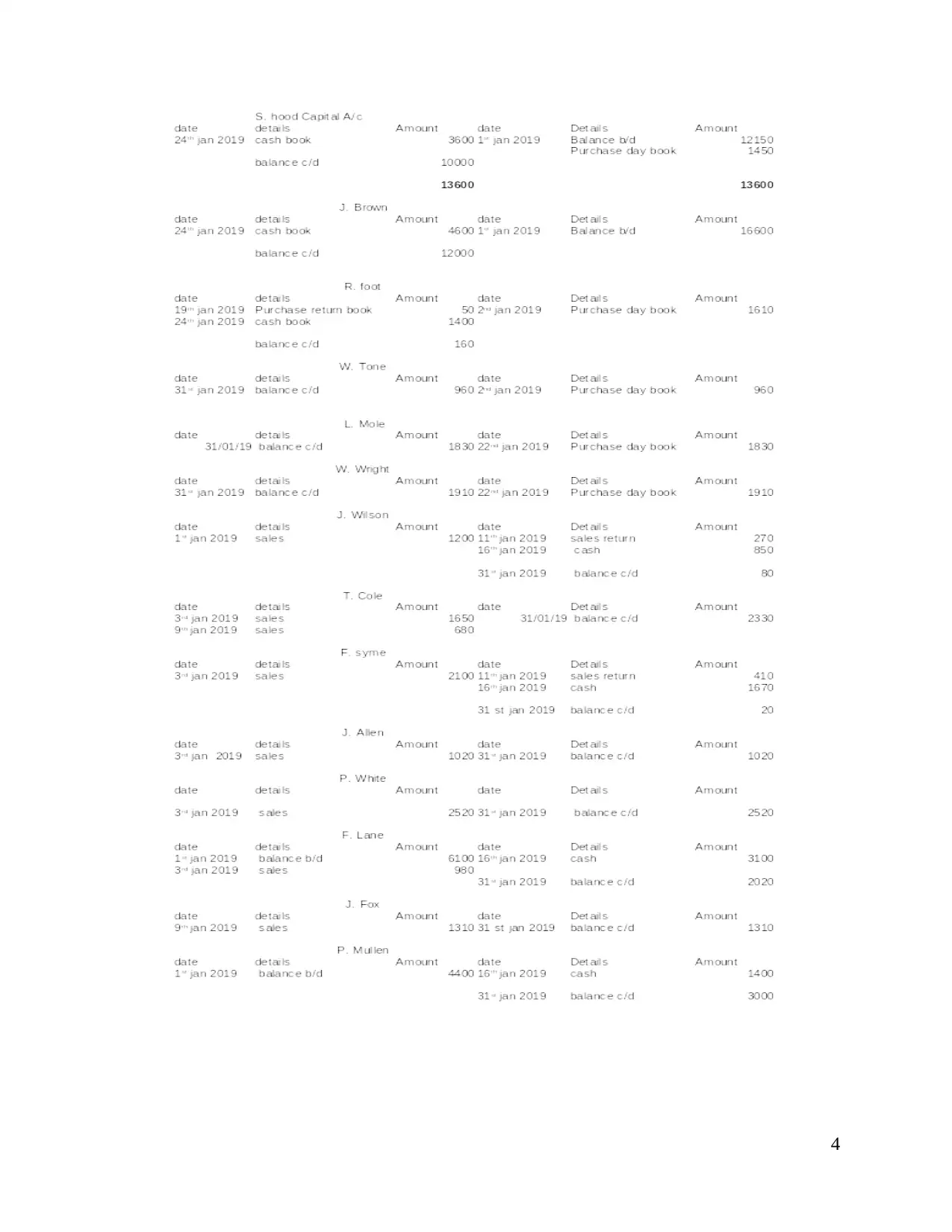

CLIENT 1

Double entry recording for the relevant journals and trail balance 31st January 2019.

\

3

organisation but are indirectly connected to the organisation. They are the outside parties which

are form a part of the company and are affected by the work and the performance of the

company. The main external stakeholder of the company are as follows:

Customers: they are the one whop consumes goods and services of the organisation.

They are the most essential source which created revenue for the organisation. Customer can use

the financial information of the company in order to judge the stability and survival of the

company for the longer time.

Competitors: these are the rivals of the company in the industry which will make

strategies by identifying the financial statement of other company in order to gain the

competitive advantage in industry by evaluating their financial position (Marshall, McManus and

Viele, 2011).

Shareholders or investors: They are considered as the main source of earning for the

organisation which are invested their money in the company. They are the main person who are

considered with the financial performance of the company. They can use the financial

information in order to evaluate the ability if the company to return their money.

Government: They are the authority which are interested in knowing the financial

performance of the company in order to pay the right amount of taxes and relevant to laws that

are being adhered.

CLIENT 1

Double entry recording for the relevant journals and trail balance 31st January 2019.

\

3

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

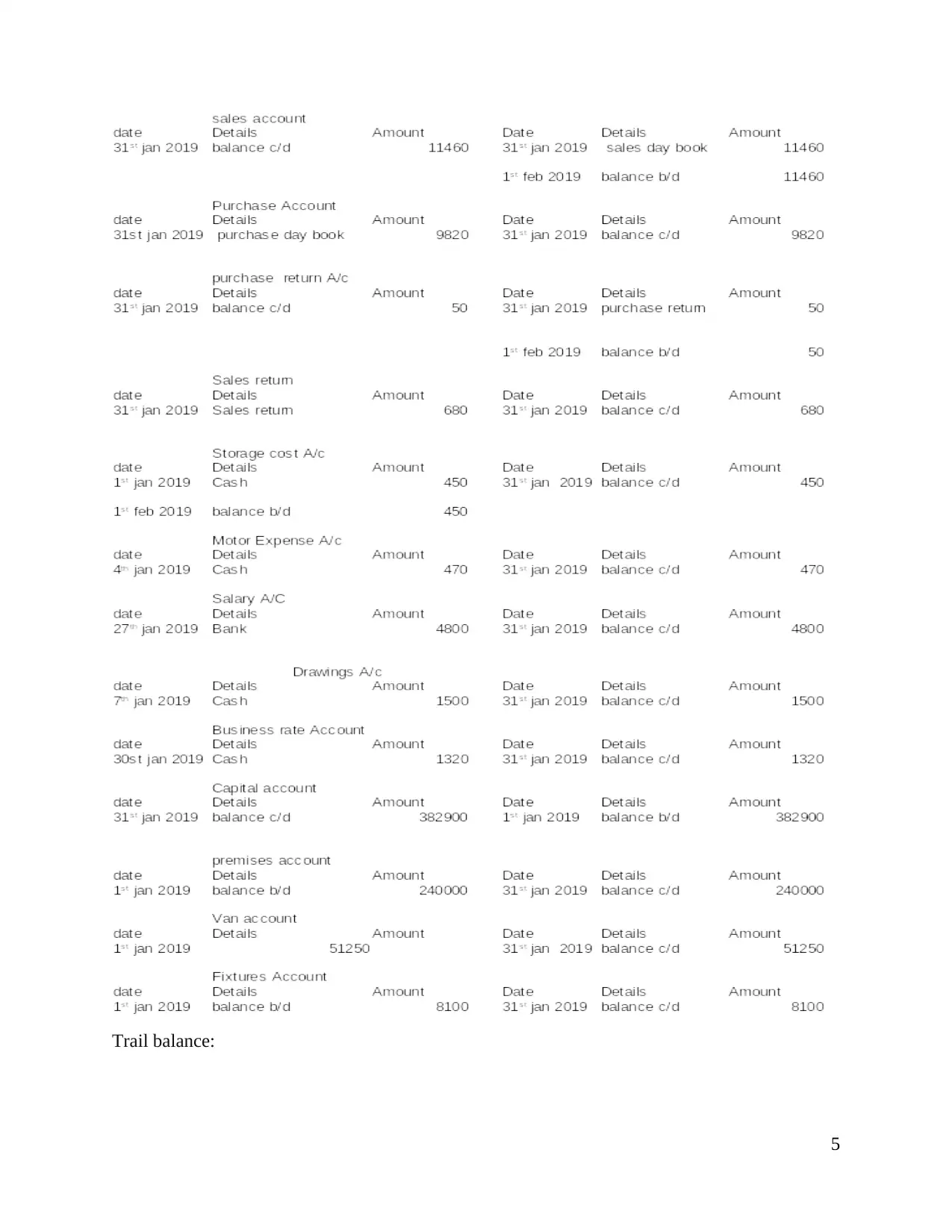

Trail balance:

5

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

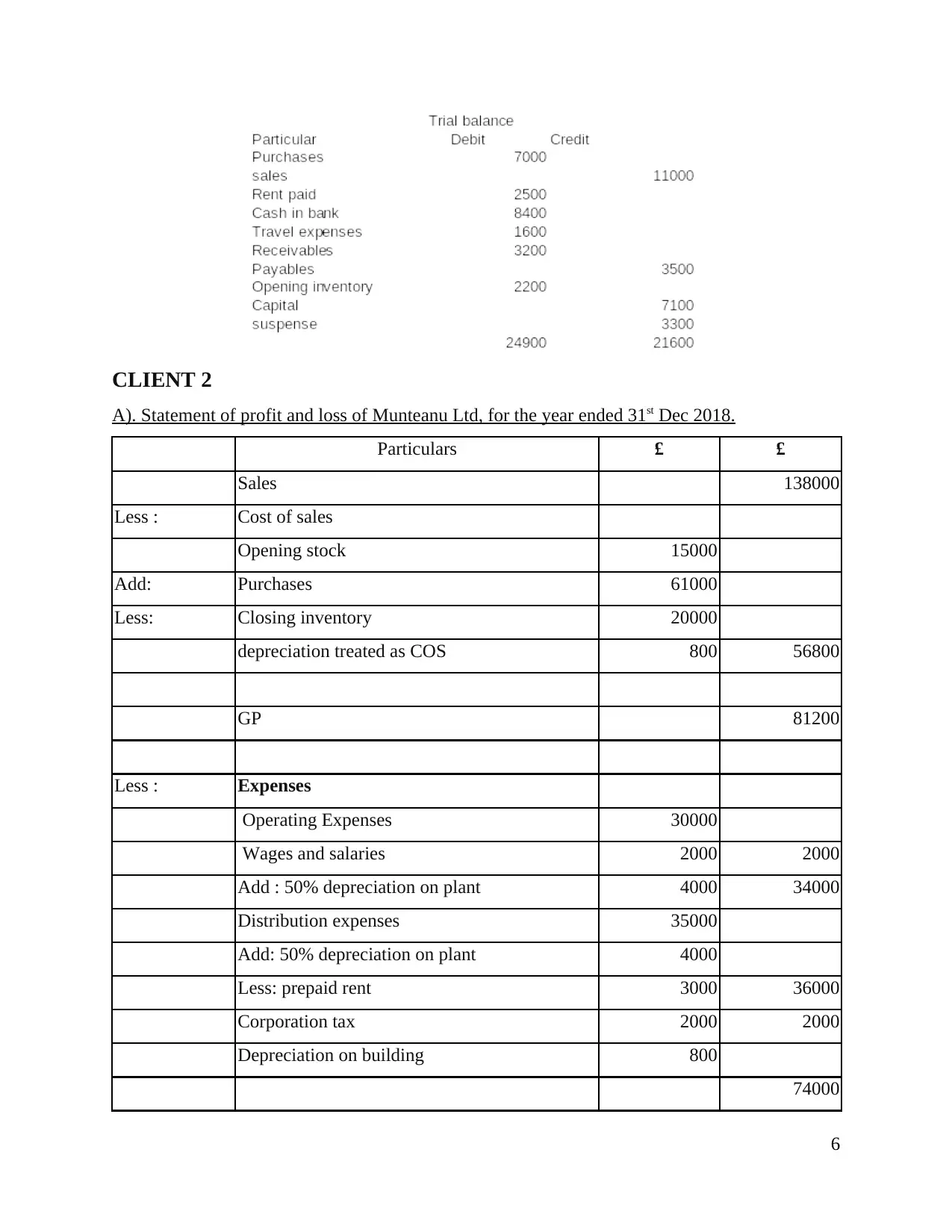

CLIENT 2

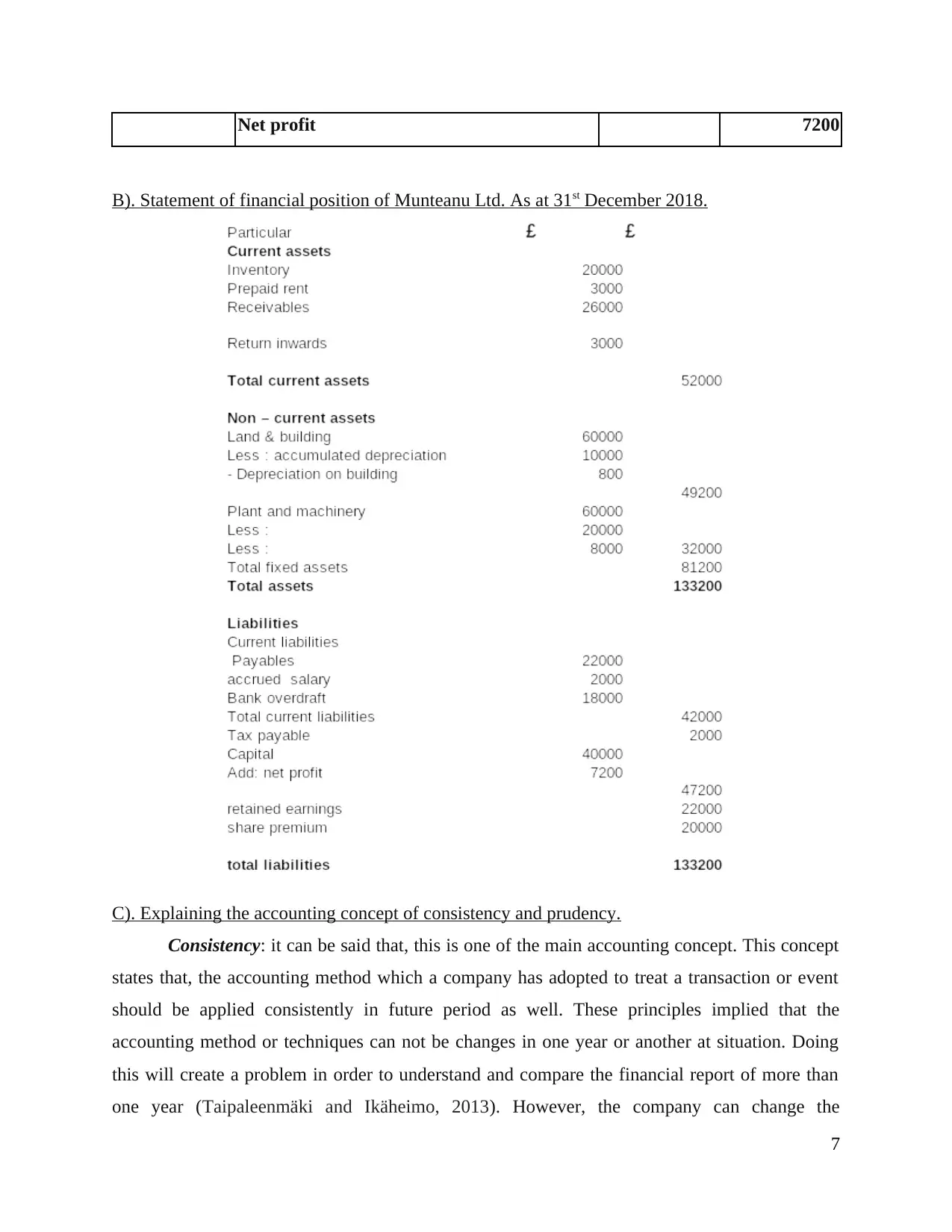

A). Statement of profit and loss of Munteanu Ltd, for the year ended 31st Dec 2018.

Particulars £ £

Sales 138000

Less : Cost of sales

Opening stock 15000

Add: Purchases 61000

Less: Closing inventory 20000

depreciation treated as COS 800 56800

GP 81200

Less : Expenses

Operating Expenses 30000

Wages and salaries 2000 2000

Add : 50% depreciation on plant 4000 34000

Distribution expenses 35000

Add: 50% depreciation on plant 4000

Less: prepaid rent 3000 36000

Corporation tax 2000 2000

Depreciation on building 800

74000

6

A). Statement of profit and loss of Munteanu Ltd, for the year ended 31st Dec 2018.

Particulars £ £

Sales 138000

Less : Cost of sales

Opening stock 15000

Add: Purchases 61000

Less: Closing inventory 20000

depreciation treated as COS 800 56800

GP 81200

Less : Expenses

Operating Expenses 30000

Wages and salaries 2000 2000

Add : 50% depreciation on plant 4000 34000

Distribution expenses 35000

Add: 50% depreciation on plant 4000

Less: prepaid rent 3000 36000

Corporation tax 2000 2000

Depreciation on building 800

74000

6

Net profit 7200

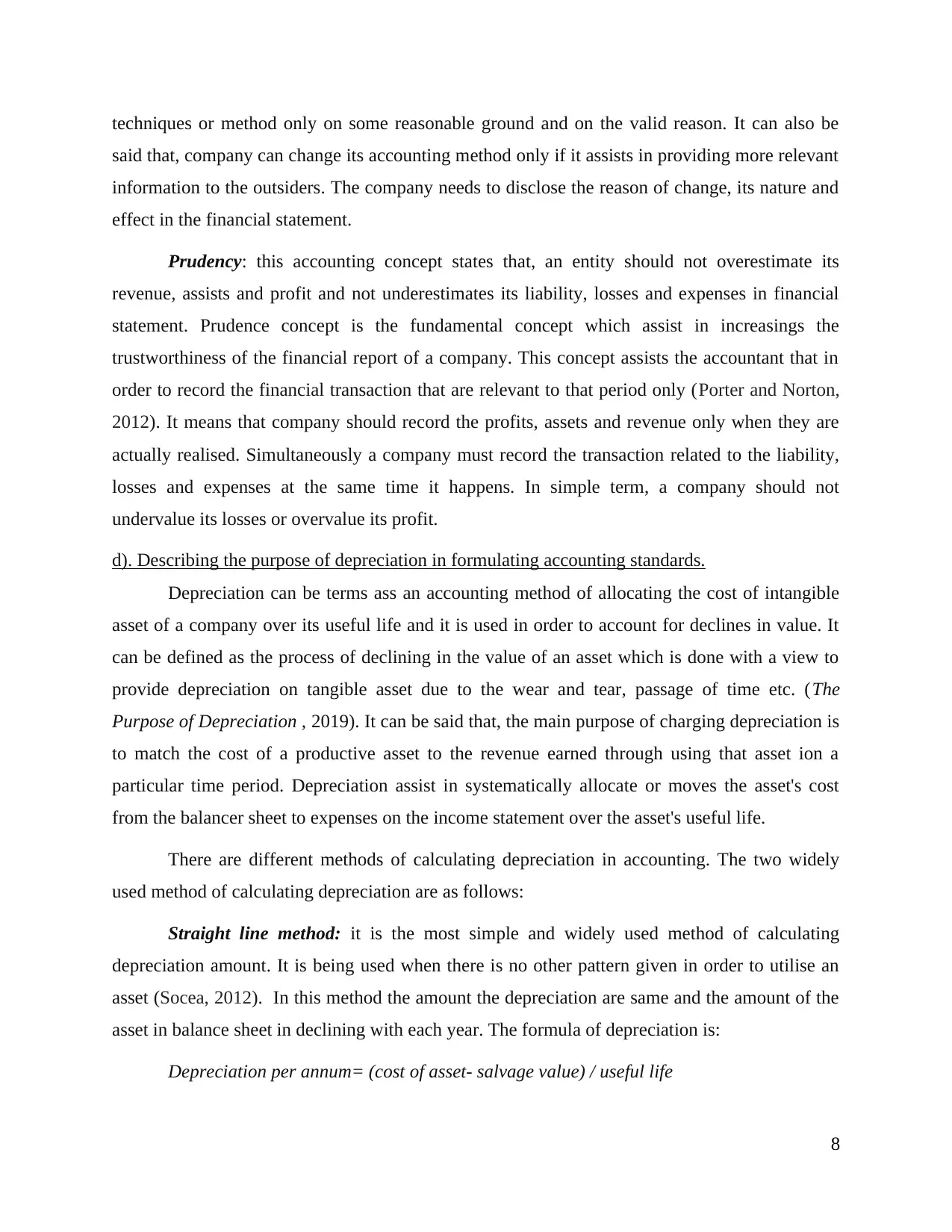

B). Statement of financial position of Munteanu Ltd. As at 31st December 2018.

C). Explaining the accounting concept of consistency and prudency.

Consistency: it can be said that, this is one of the main accounting concept. This concept

states that, the accounting method which a company has adopted to treat a transaction or event

should be applied consistently in future period as well. These principles implied that the

accounting method or techniques can not be changes in one year or another at situation. Doing

this will create a problem in order to understand and compare the financial report of more than

one year (Taipaleenmäki and Ikäheimo, 2013). However, the company can change the

7

B). Statement of financial position of Munteanu Ltd. As at 31st December 2018.

C). Explaining the accounting concept of consistency and prudency.

Consistency: it can be said that, this is one of the main accounting concept. This concept

states that, the accounting method which a company has adopted to treat a transaction or event

should be applied consistently in future period as well. These principles implied that the

accounting method or techniques can not be changes in one year or another at situation. Doing

this will create a problem in order to understand and compare the financial report of more than

one year (Taipaleenmäki and Ikäheimo, 2013). However, the company can change the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

techniques or method only on some reasonable ground and on the valid reason. It can also be

said that, company can change its accounting method only if it assists in providing more relevant

information to the outsiders. The company needs to disclose the reason of change, its nature and

effect in the financial statement.

Prudency: this accounting concept states that, an entity should not overestimate its

revenue, assists and profit and not underestimates its liability, losses and expenses in financial

statement. Prudence concept is the fundamental concept which assist in increasings the

trustworthiness of the financial report of a company. This concept assists the accountant that in

order to record the financial transaction that are relevant to that period only (Porter and Norton,

2012). It means that company should record the profits, assets and revenue only when they are

actually realised. Simultaneously a company must record the transaction related to the liability,

losses and expenses at the same time it happens. In simple term, a company should not

undervalue its losses or overvalue its profit.

d). Describing the purpose of depreciation in formulating accounting standards.

Depreciation can be terms ass an accounting method of allocating the cost of intangible

asset of a company over its useful life and it is used in order to account for declines in value. It

can be defined as the process of declining in the value of an asset which is done with a view to

provide depreciation on tangible asset due to the wear and tear, passage of time etc. (The

Purpose of Depreciation , 2019). It can be said that, the main purpose of charging depreciation is

to match the cost of a productive asset to the revenue earned through using that asset ion a

particular time period. Depreciation assist in systematically allocate or moves the asset's cost

from the balancer sheet to expenses on the income statement over the asset's useful life.

There are different methods of calculating depreciation in accounting. The two widely

used method of calculating depreciation are as follows:

Straight line method: it is the most simple and widely used method of calculating

depreciation amount. It is being used when there is no other pattern given in order to utilise an

asset (Socea, 2012). In this method the amount the depreciation are same and the amount of the

asset in balance sheet in declining with each year. The formula of depreciation is:

Depreciation per annum= (cost of asset- salvage value) / useful life

8

said that, company can change its accounting method only if it assists in providing more relevant

information to the outsiders. The company needs to disclose the reason of change, its nature and

effect in the financial statement.

Prudency: this accounting concept states that, an entity should not overestimate its

revenue, assists and profit and not underestimates its liability, losses and expenses in financial

statement. Prudence concept is the fundamental concept which assist in increasings the

trustworthiness of the financial report of a company. This concept assists the accountant that in

order to record the financial transaction that are relevant to that period only (Porter and Norton,

2012). It means that company should record the profits, assets and revenue only when they are

actually realised. Simultaneously a company must record the transaction related to the liability,

losses and expenses at the same time it happens. In simple term, a company should not

undervalue its losses or overvalue its profit.

d). Describing the purpose of depreciation in formulating accounting standards.

Depreciation can be terms ass an accounting method of allocating the cost of intangible

asset of a company over its useful life and it is used in order to account for declines in value. It

can be defined as the process of declining in the value of an asset which is done with a view to

provide depreciation on tangible asset due to the wear and tear, passage of time etc. (The

Purpose of Depreciation , 2019). It can be said that, the main purpose of charging depreciation is

to match the cost of a productive asset to the revenue earned through using that asset ion a

particular time period. Depreciation assist in systematically allocate or moves the asset's cost

from the balancer sheet to expenses on the income statement over the asset's useful life.

There are different methods of calculating depreciation in accounting. The two widely

used method of calculating depreciation are as follows:

Straight line method: it is the most simple and widely used method of calculating

depreciation amount. It is being used when there is no other pattern given in order to utilise an

asset (Socea, 2012). In this method the amount the depreciation are same and the amount of the

asset in balance sheet in declining with each year. The formula of depreciation is:

Depreciation per annum= (cost of asset- salvage value) / useful life

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reducing balance method: This method changes the amount of depreciation over time. It

is more appropriate method for an asset which typically loses the most value in the recent years,

but than slowing the depreciation in later years. It is the most useful method when as asset has

higher productivity at the start of its useful life. Formula of reducing balance method are as

follows:

Depreciation charge per year =(net book value – residual value) * depreciation factor

e). Critically evaluating the difference between the financial statement prepared by the sole

trader and limited companies.

It can be said that, the sole trader is the person who is singly handling the business. He is

responsible to all the losses and profit. The business activities and decision s are taken by the

owner itself. Whereas, the limited company is the private organisation that are owned by a single

person or by group of partners. In limited company, the business can get a different identity

through incorporate the company (Warren and Jones, 2018). All the finances and accounts of the

company will be separated than its owner. The financial statement of both the companies are

different. The most difference between the financial statement of sole trader and limited

companies are as follows:

Sole Trader Limited Company

It has only one capital account It has more than one capital account which are

depends on the number of partners.

All the net profit belongs to the single owner Profit and loss is distributed to the partner's

capital account as per the agreed ratio.

There is no income statement prepared in sole

trader-ship.

The income statement of the partnership shows

the schedule on how the newt profit/loss is

distributed to the partners (Cañibano, 2018).

Balance sheet shows only one capital account

which is belongs to the single owner of

company

The balance sheet sows the balance of the

capital amount of each partner which are

classified under owner's equity.

9

is more appropriate method for an asset which typically loses the most value in the recent years,

but than slowing the depreciation in later years. It is the most useful method when as asset has

higher productivity at the start of its useful life. Formula of reducing balance method are as

follows:

Depreciation charge per year =(net book value – residual value) * depreciation factor

e). Critically evaluating the difference between the financial statement prepared by the sole

trader and limited companies.

It can be said that, the sole trader is the person who is singly handling the business. He is

responsible to all the losses and profit. The business activities and decision s are taken by the

owner itself. Whereas, the limited company is the private organisation that are owned by a single

person or by group of partners. In limited company, the business can get a different identity

through incorporate the company (Warren and Jones, 2018). All the finances and accounts of the

company will be separated than its owner. The financial statement of both the companies are

different. The most difference between the financial statement of sole trader and limited

companies are as follows:

Sole Trader Limited Company

It has only one capital account It has more than one capital account which are

depends on the number of partners.

All the net profit belongs to the single owner Profit and loss is distributed to the partner's

capital account as per the agreed ratio.

There is no income statement prepared in sole

trader-ship.

The income statement of the partnership shows

the schedule on how the newt profit/loss is

distributed to the partners (Cañibano, 2018).

Balance sheet shows only one capital account

which is belongs to the single owner of

company

The balance sheet sows the balance of the

capital amount of each partner which are

classified under owner's equity.

9

CLIENT 3

A). Explaining the purpose of bank reconciliation statement and its requirement of preparing

every month.

In order to record the bank as well as cash transactions, every business maintain a book

which is known as cash-book. This book has both cash column and bank column which shows

their respective balances. Simultaneously, banks also keeps record of the every customer's

account in their passbooks (Tong and Saladrigues, 2018). Some times, due to various reasons,

cash book and bank statement does not match. It is very essential for the company as well as for

the bank to reconcile the differences. A statement has been prepared in order to reconcile the

balance shown in cash book and pass book, such statement is known as bank reconciliation

statement. It can be said that, BRS is the statement which assist in evaluating the reason for the

differences in the balance as per cash-book's bank column and passbook. The main purpose of

preparing BRS are as follows:

BRS assist in comparing the records of bank as well as of the company in order to find

any differences in the balance amount.

It confirms the accuracy ODF the balances that are shown in the company's cook and

bank records (Trotman and Carson, 2018).

It assists in checking any undue delaying in the collection and clearance of some cheque.

It can be said that, preparing BRS is not compulsory and there is no fixed date in order to

prepare BRS. It can be prepared as and when required. However, it can be said that, preparing

BRS on monthly basis will assist the company and the bank in order to check the accuracy in the

bank and cash records. Hence, it can be said that bank statement should be taken by company in

regular basis in order to check the accuracy. It will assist the company in making further

accounting statements.

B). Explaining some areas which may cause varies in the bank statement.

There are various reasons which causes difference in bank statement and bank column of

cash-book, some of them are as follows:

Unrepresented cheque: when companies issues the cheque for the payment, the

company makes the direct entry in the credit side in the bank column (Crowther, 2018).

10

A). Explaining the purpose of bank reconciliation statement and its requirement of preparing

every month.

In order to record the bank as well as cash transactions, every business maintain a book

which is known as cash-book. This book has both cash column and bank column which shows

their respective balances. Simultaneously, banks also keeps record of the every customer's

account in their passbooks (Tong and Saladrigues, 2018). Some times, due to various reasons,

cash book and bank statement does not match. It is very essential for the company as well as for

the bank to reconcile the differences. A statement has been prepared in order to reconcile the

balance shown in cash book and pass book, such statement is known as bank reconciliation

statement. It can be said that, BRS is the statement which assist in evaluating the reason for the

differences in the balance as per cash-book's bank column and passbook. The main purpose of

preparing BRS are as follows:

BRS assist in comparing the records of bank as well as of the company in order to find

any differences in the balance amount.

It confirms the accuracy ODF the balances that are shown in the company's cook and

bank records (Trotman and Carson, 2018).

It assists in checking any undue delaying in the collection and clearance of some cheque.

It can be said that, preparing BRS is not compulsory and there is no fixed date in order to

prepare BRS. It can be prepared as and when required. However, it can be said that, preparing

BRS on monthly basis will assist the company and the bank in order to check the accuracy in the

bank and cash records. Hence, it can be said that bank statement should be taken by company in

regular basis in order to check the accuracy. It will assist the company in making further

accounting statements.

B). Explaining some areas which may cause varies in the bank statement.

There are various reasons which causes difference in bank statement and bank column of

cash-book, some of them are as follows:

Unrepresented cheque: when companies issues the cheque for the payment, the

company makes the direct entry in the credit side in the bank column (Crowther, 2018).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.