HA 3011 Advanced Financial Accounting: Enron & Coca-Cola Report

VerifiedAdded on 2023/06/04

|12

|1100

|138

Report

AI Summary

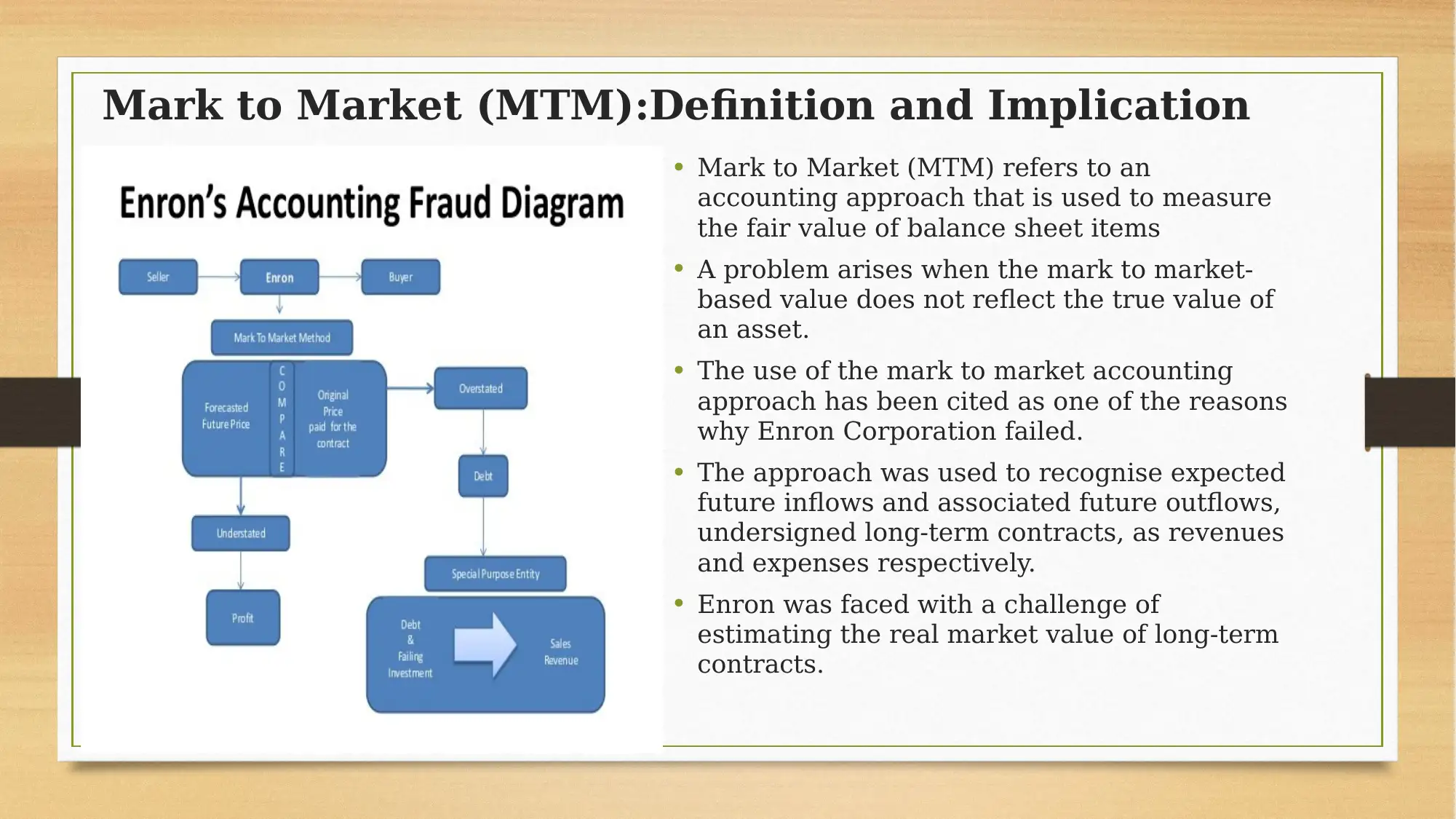

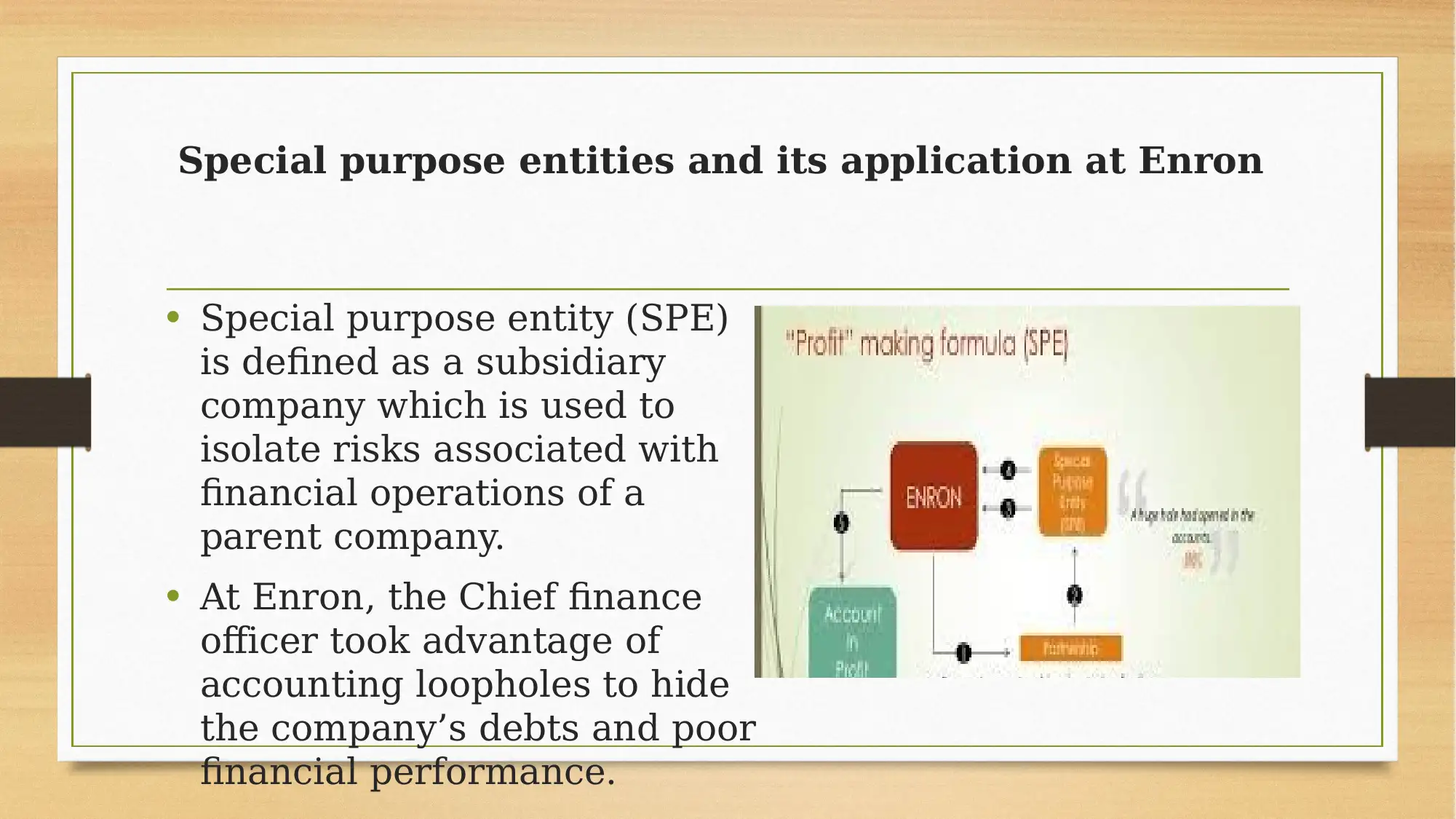

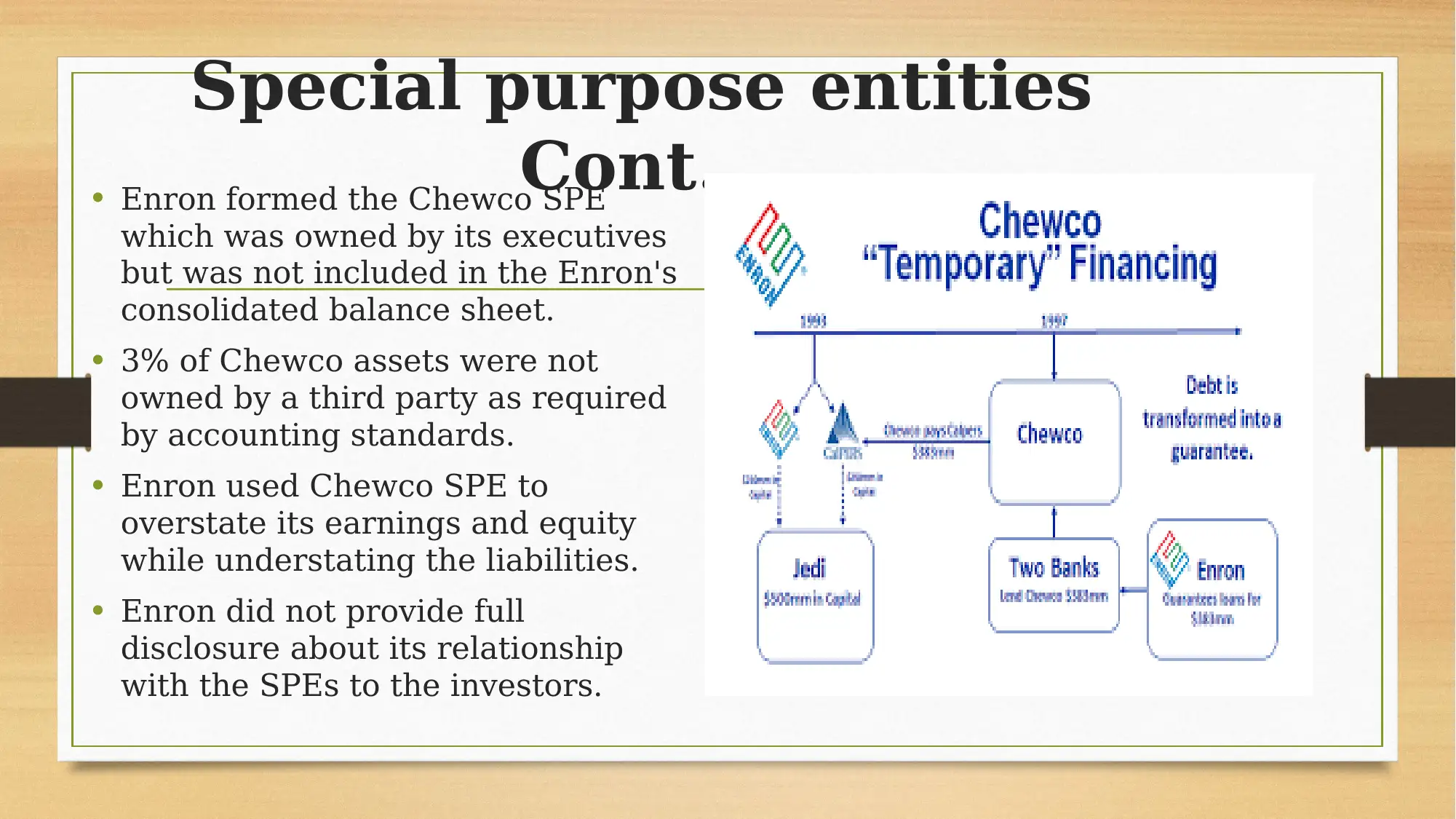

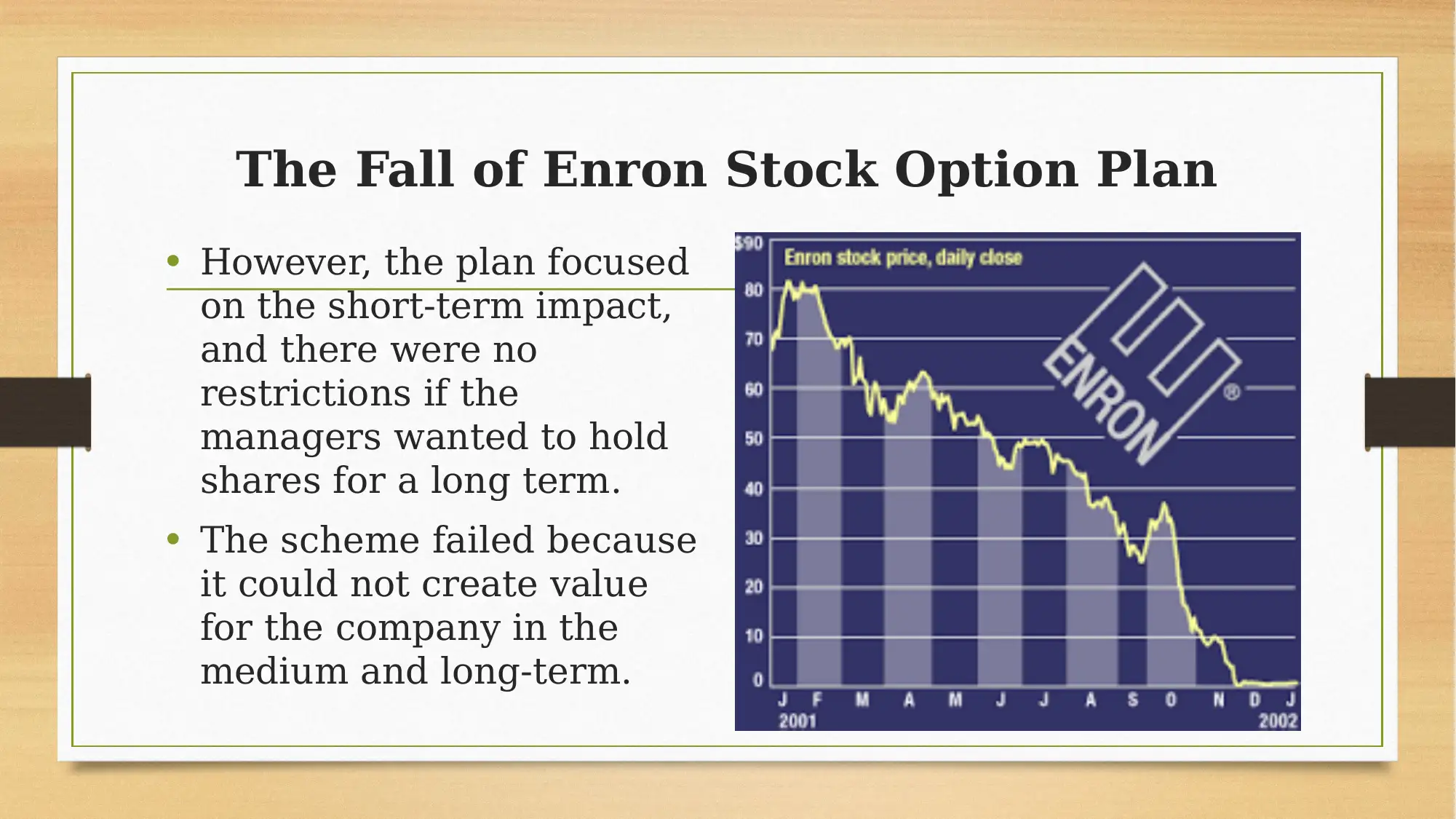

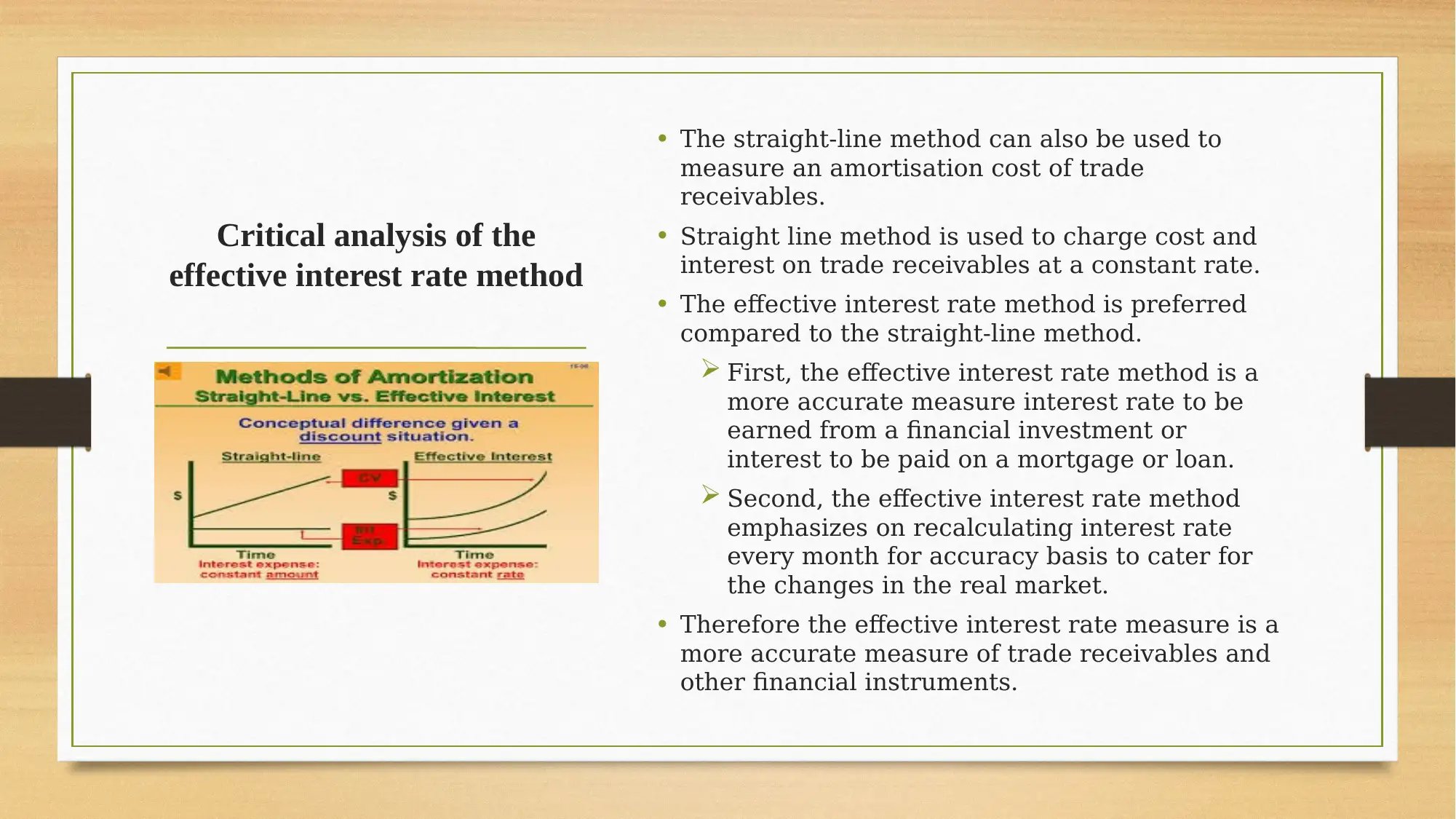

This report provides a detailed analysis of the financial practices of Enron and Coca-Cola. The first part of the report focuses on Enron, examining the use and misuse of mark-to-market accounting, special purpose entities (SPEs), and stock option plans. It explores how these accounting approaches and financial instruments were used, and the implications of each. The second part of the report analyzes the methodologies used by Coca-Cola to measure its financial elements, including sales, finance costs, taxation, intangible assets, property, plant, and equipment, associates and joint arrangements, inventories, trade receivables, trade payables, net debt, and equity. The report also compares the effective interest rate method with the straight-line method for measuring trade receivables, concluding that the effective interest rate method is more accurate. The study uses the IFRS conceptual framework, which prefers the use of fair value and amortisation cost to obtain the real value of a financial element.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.