HA2032 Corporate and Financial Accounting: Equity and Debt Analysis

VerifiedAdded on 2023/06/04

|14

|2781

|213

Report

AI Summary

This report provides a comprehensive analysis of corporate and financial accounting, addressing key aspects such as corporate regulation, accounting standard setting, and the analysis of owners' equity and debt components. The report begins by examining the importance of financial information disclosure, discussing the merits of both voluntary disclosure and regulated financial reporting, and highlighting the role of managers in providing relevant and reliable financial data to stakeholders. It then delves into accounting standard setting, specifically focusing on the role of the Australian Accounting Standards Board (AASB) in relation to international standards (IFRS) and the reasons some countries, like the United States, have not fully adopted IFRS. The analysis extends to examining the owners' equity of four Australian companies (A2 Milk Company, Bega Cheese Limited, Wesfarmers Limited, and Woolworths Group Limited) over a four-year period, detailing changes in share capital, retained earnings, and reserves. Finally, the report compares the debt and equity components of these firms, assessing their capital structures and financial risk profiles, and concludes by highlighting key financial metrics and the overall financial health of the selected companies. The report utilizes data from company annual reports and provides insights into the financial performance and position of each entity.

RUNNING HEAD: CORPORATE AND FINANCIAL ACCOUNTING

Corporate accounting

Corporate accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and financial accounting 2

Executive Summary

The report provides a brief summary about the corporate regulation and setting of accounting

standards. In the first section, it deals with the importance of disclosing the financial information

voluntarily and regulating the corporate financial reporting. The section provides insights about

the fact that it is very important for the manager to disclose the relevant and reliable financial

information that is important for the stakeholders. It also highlights the fact that the financial

reporting should be regulated properly so that no misstatement or error can be occurred. In

addition, it defines the role played by AASB in setting international standards and the reasons

why some members have not accepted IFRS yet. In the later part, the report discusses the items

of owners’ equity of the four Australian firms and identifies the changes in the equity.

Furthermore, it also compares the debt and equity components of the firm. In the last, a

conclusion is provided which states that Wesfarmers has low financial risk and the share capital

of Bega Cheese has been the highest among all.

Executive Summary

The report provides a brief summary about the corporate regulation and setting of accounting

standards. In the first section, it deals with the importance of disclosing the financial information

voluntarily and regulating the corporate financial reporting. The section provides insights about

the fact that it is very important for the manager to disclose the relevant and reliable financial

information that is important for the stakeholders. It also highlights the fact that the financial

reporting should be regulated properly so that no misstatement or error can be occurred. In

addition, it defines the role played by AASB in setting international standards and the reasons

why some members have not accepted IFRS yet. In the later part, the report discusses the items

of owners’ equity of the four Australian firms and identifies the changes in the equity.

Furthermore, it also compares the debt and equity components of the firm. In the last, a

conclusion is provided which states that Wesfarmers has low financial risk and the share capital

of Bega Cheese has been the highest among all.

Corporate and financial accounting 3

Contents

Contents.......................................................................................................................................................3

Corporate Regulation...................................................................................................................................4

Question 1...............................................................................................................................................4

Accounting standard setting........................................................................................................................5

Question 2...............................................................................................................................................5

Owners’ equity............................................................................................................................................7

Question 3...............................................................................................................................................7

Question 4.............................................................................................................................................10

Conclusion.................................................................................................................................................12

References.................................................................................................................................................13

Contents

Contents.......................................................................................................................................................3

Corporate Regulation...................................................................................................................................4

Question 1...............................................................................................................................................4

Accounting standard setting........................................................................................................................5

Question 2...............................................................................................................................................5

Owners’ equity............................................................................................................................................7

Question 3...............................................................................................................................................7

Question 4.............................................................................................................................................10

Conclusion.................................................................................................................................................12

References.................................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and financial accounting 4

Corporate Regulation

Question 1

Many researches conducting in field of accounting and reporting suggested that the disclosure of

financial information has become very much necessary for the businesses and the managers.

Reporting of financial data in respect of a company has become significant in the last few years

due to the complexity of the businesses and their operations. The management of the company

communicates all the relevant and reliable information to the stakeholders through the annual

reports which consists all the data in financial and non-financial aspect. The stakeholders are

those people who hold some percentage of interest in company’s profits and are authorized to

have all the information about the performance and position of the entity. Disclosure of financial

information helps the shareholders to determine that whether the company is financially sound or

not. Specifically, external stakeholders that include government, investors, creditors and other

individuals who are not involved in the day to day activities of the firm require more information

about the operations and activities of the business in order to assess its overall performance from

all the aspects. There are various aspects which are kept in mind while analysing the financial

performance of an organization. They are known as liquidity, solvency, efficiency and

profitability. As far as non-financial performance is considered, factors like corporate social

responsibility, sustainability reporting and compliance with standards like GRI are analysed

(Campbell, 2015)

As the above paragraph reflects the importance of financial information, the regulation and

management of reporting the same should be the essential function of the managers. They must

disclose the accounting information voluntarily to all the stakeholders so that they do not need to

Corporate Regulation

Question 1

Many researches conducting in field of accounting and reporting suggested that the disclosure of

financial information has become very much necessary for the businesses and the managers.

Reporting of financial data in respect of a company has become significant in the last few years

due to the complexity of the businesses and their operations. The management of the company

communicates all the relevant and reliable information to the stakeholders through the annual

reports which consists all the data in financial and non-financial aspect. The stakeholders are

those people who hold some percentage of interest in company’s profits and are authorized to

have all the information about the performance and position of the entity. Disclosure of financial

information helps the shareholders to determine that whether the company is financially sound or

not. Specifically, external stakeholders that include government, investors, creditors and other

individuals who are not involved in the day to day activities of the firm require more information

about the operations and activities of the business in order to assess its overall performance from

all the aspects. There are various aspects which are kept in mind while analysing the financial

performance of an organization. They are known as liquidity, solvency, efficiency and

profitability. As far as non-financial performance is considered, factors like corporate social

responsibility, sustainability reporting and compliance with standards like GRI are analysed

(Campbell, 2015)

As the above paragraph reflects the importance of financial information, the regulation and

management of reporting the same should be the essential function of the managers. They must

disclose the accounting information voluntarily to all the stakeholders so that they do not need to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and financial accounting 5

develop such data which reflects false image of the entity. The objective of preparing financial

information is to assess the true position or situation of the company, to determine the amount of

return it could offer to its potential investors and others. In order to accomplish such motives, it

is very important for the managers to regulate its financial reporting procedure on periodic basis

and in an appropriate manner (Faulkender, Hankins and Petersen, 2018). It will bring

harmonization and uniformity in the function by applying the various accounting standards that

are relevant for the business as per its size and nature. The consistency in financial reporting will

eventually help the stakeholders to understand the data easily and compare the same with the

competitors. It will avoid the manipulation of the figures and misstatement of the financial

statements. Voluntary disclosure and regulation will help the managers and company to avoid the

possibility of falsification of accounts and will result in desirable and reliable results (Collins,

Hribar and Tian, 2014)

Accounting standard setting

Question 2

Accounting standards are the authoritative standards applied at time of preparing financial

reports. They are the primary source of Generally Accepted Accounting Principles (GAAP).

Such standards lay down the procedures for conducting an accounting treatment of some specific

business transactions and events. Australian Accounting Standard Board is a government agency

formulated with an objective to develop and maintain the financial reporting standards that will

be applicable to all the private and public entities operating in Australia. AASB has played a

vital role in process of setting global accounting standards. The authorized body responsible for

setting the global standards is the international accounting standard board (IASB) and it has

develop such data which reflects false image of the entity. The objective of preparing financial

information is to assess the true position or situation of the company, to determine the amount of

return it could offer to its potential investors and others. In order to accomplish such motives, it

is very important for the managers to regulate its financial reporting procedure on periodic basis

and in an appropriate manner (Faulkender, Hankins and Petersen, 2018). It will bring

harmonization and uniformity in the function by applying the various accounting standards that

are relevant for the business as per its size and nature. The consistency in financial reporting will

eventually help the stakeholders to understand the data easily and compare the same with the

competitors. It will avoid the manipulation of the figures and misstatement of the financial

statements. Voluntary disclosure and regulation will help the managers and company to avoid the

possibility of falsification of accounts and will result in desirable and reliable results (Collins,

Hribar and Tian, 2014)

Accounting standard setting

Question 2

Accounting standards are the authoritative standards applied at time of preparing financial

reports. They are the primary source of Generally Accepted Accounting Principles (GAAP).

Such standards lay down the procedures for conducting an accounting treatment of some specific

business transactions and events. Australian Accounting Standard Board is a government agency

formulated with an objective to develop and maintain the financial reporting standards that will

be applicable to all the private and public entities operating in Australia. AASB has played a

vital role in process of setting global accounting standards. The authorized body responsible for

setting the global standards is the international accounting standard board (IASB) and it has

Corporate and financial accounting 6

collaborated with many other national accounting setting bodies to bring harmonization and

consistency in the international standards (AASB. 2018).

AASB has created strategies to determine its role as a standard setter in the dynamic

environment. The board has formulated its strategies in such a manner that a proper alignment

can be maintained with IASB and its requirement. AASB assist IASB in identifying technical

issues and it also receives the feedback from many of the Australian companies which are taken

into consideration by IASB while setting the accounting standards. It submits some formal

documents and statement in order to get the feedback and seek comments from IASB for getting

the authority to develop such accounting standards.

Despite the worldwide acceptance, there are some countries where complying with IFRS is not

mandatory and the standards are not applicable. For instance, United States was one of the

original members of IASC and later IASB and many of the accounting standards are set in

accordance with the input of United States. The acceptance of GAAP and IFRS is a controversial

action and there are some reasons why US has not yet move towards IFRS. The foremost reason

was IFRS is costly and switching to it from GAAP will be costly for the country. Another reason

was that US will face the problem of comparability of financial statements and there will be no

common ground for making a comparison between the companies operating in different

countries. Apart from this, the IFRS standards do not have quality as the GAAP have and the

statements prepared will lack that quality factor. All such are the reasons why some members of

IASB have not yet applied IFRS in their process of financial reporting (Lam, 2015).

collaborated with many other national accounting setting bodies to bring harmonization and

consistency in the international standards (AASB. 2018).

AASB has created strategies to determine its role as a standard setter in the dynamic

environment. The board has formulated its strategies in such a manner that a proper alignment

can be maintained with IASB and its requirement. AASB assist IASB in identifying technical

issues and it also receives the feedback from many of the Australian companies which are taken

into consideration by IASB while setting the accounting standards. It submits some formal

documents and statement in order to get the feedback and seek comments from IASB for getting

the authority to develop such accounting standards.

Despite the worldwide acceptance, there are some countries where complying with IFRS is not

mandatory and the standards are not applicable. For instance, United States was one of the

original members of IASC and later IASB and many of the accounting standards are set in

accordance with the input of United States. The acceptance of GAAP and IFRS is a controversial

action and there are some reasons why US has not yet move towards IFRS. The foremost reason

was IFRS is costly and switching to it from GAAP will be costly for the country. Another reason

was that US will face the problem of comparability of financial statements and there will be no

common ground for making a comparison between the companies operating in different

countries. Apart from this, the IFRS standards do not have quality as the GAAP have and the

statements prepared will lack that quality factor. All such are the reasons why some members of

IASB have not yet applied IFRS in their process of financial reporting (Lam, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and financial accounting 7

Owners’ equity

Four ASX listed companies are selected that operates in consumer staples sector of Australia.

They are named as A2 Milk Company, Bega Cheese Limited, Wesfarmers Limited and

Woolworths Group Limited. All of them are listed on Australian Securities Exchange and

operate in the same industry. The items of equity for each company is analysed for the past four

years in the below sections. The data is derived from the annual reports of the selected

companies and on the basis of that the analysis has been done.

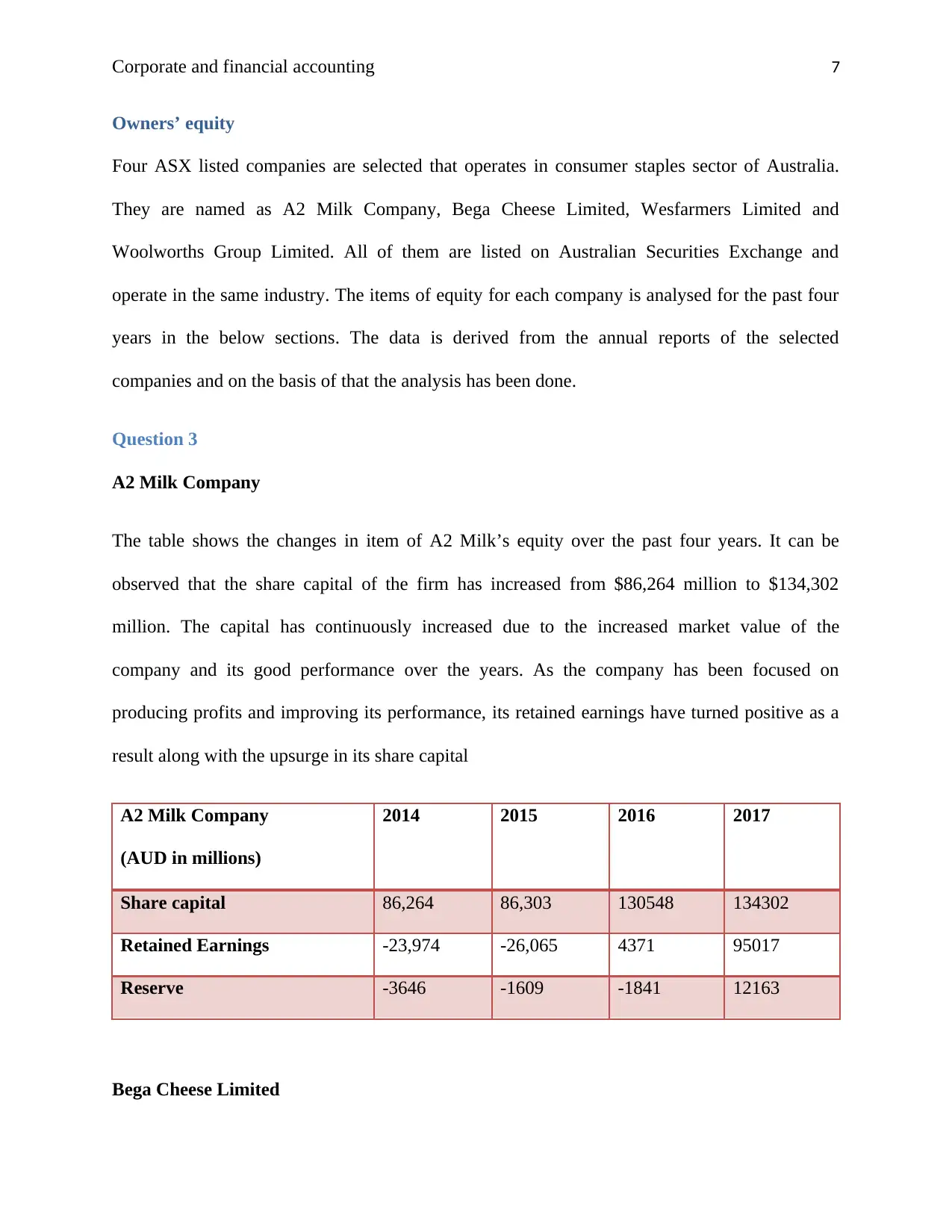

Question 3

A2 Milk Company

The table shows the changes in item of A2 Milk’s equity over the past four years. It can be

observed that the share capital of the firm has increased from $86,264 million to $134,302

million. The capital has continuously increased due to the increased market value of the

company and its good performance over the years. As the company has been focused on

producing profits and improving its performance, its retained earnings have turned positive as a

result along with the upsurge in its share capital

A2 Milk Company

(AUD in millions)

2014 2015 2016 2017

Share capital 86,264 86,303 130548 134302

Retained Earnings -23,974 -26,065 4371 95017

Reserve -3646 -1609 -1841 12163

Bega Cheese Limited

Owners’ equity

Four ASX listed companies are selected that operates in consumer staples sector of Australia.

They are named as A2 Milk Company, Bega Cheese Limited, Wesfarmers Limited and

Woolworths Group Limited. All of them are listed on Australian Securities Exchange and

operate in the same industry. The items of equity for each company is analysed for the past four

years in the below sections. The data is derived from the annual reports of the selected

companies and on the basis of that the analysis has been done.

Question 3

A2 Milk Company

The table shows the changes in item of A2 Milk’s equity over the past four years. It can be

observed that the share capital of the firm has increased from $86,264 million to $134,302

million. The capital has continuously increased due to the increased market value of the

company and its good performance over the years. As the company has been focused on

producing profits and improving its performance, its retained earnings have turned positive as a

result along with the upsurge in its share capital

A2 Milk Company

(AUD in millions)

2014 2015 2016 2017

Share capital 86,264 86,303 130548 134302

Retained Earnings -23,974 -26,065 4371 95017

Reserve -3646 -1609 -1841 12163

Bega Cheese Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and financial accounting 8

An increasing trend has been noticed in all the items of Bega Cheese owners’ equity. Along with

its share capital, the reserves and retained earnings of the company has also increased over the

period of past five years. In 2014, it had capital worth $103,642 million and earnings amounted

to $188,356 million which rise to $224,692 million and $326,326 million in 2017 respectively.

This reflected that company has enhanced its market value and is focused on keeping its

financial risk low by issuing more and more capital.

Bega Cheese Limited

(AUD in millions)

2014 2015 2016 2017

Share capital 103,642 103,942 103,942 224,692

Retained Earnings 188,356 187,793 202,838 326,326

Reserve 22,390 20,931 21,058 21,656

Wesfarmers Limited

The share capital of Wesfarmers has increased in 2017 as compare to the past years. In 2014, it

was $22,708 million which reduced to $21,937 in 2016. Later on the capital again increased to

$22,268 million last year (Wesfarmers. 2017). The same fluctuating trend has been noticed in the

value of company’s retained earnings. The issue of shares under the dividend investment plan

resulted in the increased share capital of the firm (Wesfarmers. 2015).

Wesfarmers Limited

(AUD in millions)

2014 2015 2016 2017

Share capital 22,708 21,844 21,937 22,268

An increasing trend has been noticed in all the items of Bega Cheese owners’ equity. Along with

its share capital, the reserves and retained earnings of the company has also increased over the

period of past five years. In 2014, it had capital worth $103,642 million and earnings amounted

to $188,356 million which rise to $224,692 million and $326,326 million in 2017 respectively.

This reflected that company has enhanced its market value and is focused on keeping its

financial risk low by issuing more and more capital.

Bega Cheese Limited

(AUD in millions)

2014 2015 2016 2017

Share capital 103,642 103,942 103,942 224,692

Retained Earnings 188,356 187,793 202,838 326,326

Reserve 22,390 20,931 21,058 21,656

Wesfarmers Limited

The share capital of Wesfarmers has increased in 2017 as compare to the past years. In 2014, it

was $22,708 million which reduced to $21,937 in 2016. Later on the capital again increased to

$22,268 million last year (Wesfarmers. 2017). The same fluctuating trend has been noticed in the

value of company’s retained earnings. The issue of shares under the dividend investment plan

resulted in the increased share capital of the firm (Wesfarmers. 2015).

Wesfarmers Limited

(AUD in millions)

2014 2015 2016 2017

Share capital 22,708 21,844 21,937 22,268

Corporate and financial accounting 9

Retained Earnings 2,901 2,742 874 1,509

Reserve 408 226 166 190

Woolworths Group Limited

The items of equity of Woolworths have shown an upward trend in respect of share capital

whereas the retained earnings have reduced in the past four years. The reason for reduced

earnings is the payment of high dividends to the shareholders. The company have declared high

dividends and also issued shares which ultimately increased its capital.

Woolworths Group Limited

(AUD in millions)

2014 2015 2016 2017

Share capital 4850 5065 5252 5615

Retained Earnings 5423 5830 3125 3797

Reserve 198 95 93.9 113.8

(Woolworths. 2017).

Items of equity are explained as follows:

Ordinary share capital: It is the equity capital which is invested by the shareholders in the

company. It is known as the issued capital of the entity which comprises of other

elements also such as retained earnings, reserves and accumulated profit.

Among the four selected companies, Bega Cheese has the highest share capital with $224,692

million followed by A2 Milk Company with $134,302. Both the companies have higher share

capital than Wesfarmers and Woolworths and in comparison to their past data also. When

Retained Earnings 2,901 2,742 874 1,509

Reserve 408 226 166 190

Woolworths Group Limited

The items of equity of Woolworths have shown an upward trend in respect of share capital

whereas the retained earnings have reduced in the past four years. The reason for reduced

earnings is the payment of high dividends to the shareholders. The company have declared high

dividends and also issued shares which ultimately increased its capital.

Woolworths Group Limited

(AUD in millions)

2014 2015 2016 2017

Share capital 4850 5065 5252 5615

Retained Earnings 5423 5830 3125 3797

Reserve 198 95 93.9 113.8

(Woolworths. 2017).

Items of equity are explained as follows:

Ordinary share capital: It is the equity capital which is invested by the shareholders in the

company. It is known as the issued capital of the entity which comprises of other

elements also such as retained earnings, reserves and accumulated profit.

Among the four selected companies, Bega Cheese has the highest share capital with $224,692

million followed by A2 Milk Company with $134,302. Both the companies have higher share

capital than Wesfarmers and Woolworths and in comparison to their past data also. When

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and financial accounting 10

analysed, it is interpreted that Woolworth is growing at low rate in terms of share capital and

may have to face high financial leverage.

Retained earnings: The other element of owner’s equity is retained earnings which show

the amount of profits retained by the company after paying all the amounts and

obligations. It is that amount which is utilized for making dividend payments to the

shareholders (Reid and Myddelton, 2017). Bega Cheese has the highest retained earnings

among the four companies in the past four years. Its retained profits have been constantly

increased over the years.

Reserves: It reflects the amount set aside by the entities for a specific purpose. The

reserve maintained by A2 Milk was $12163 million and by Bega Cheese the amount was

$21656 million. The other two companies Wesfarmers and Woolworths have maintained

low value of reserves.

Question 4

The debt and equity are the parts of company’s capital structure and are required to be

maintained in an appropriate proportion. All the four selected companies have maintained their

debt and equity elements by keeping in mind the profitability and financial risk factor.

A2 Milk Company

(AUD in millions)

2014 2015 2016 2017

Total equity 58644 58629 133078 241482

Total Liabilities 17999 30238 77074 102448

The debt of A2 Milk has increased constantly from the past four years. However, along with the

upsurge in debt the equity also increased which keeps the ratio stable.

analysed, it is interpreted that Woolworth is growing at low rate in terms of share capital and

may have to face high financial leverage.

Retained earnings: The other element of owner’s equity is retained earnings which show

the amount of profits retained by the company after paying all the amounts and

obligations. It is that amount which is utilized for making dividend payments to the

shareholders (Reid and Myddelton, 2017). Bega Cheese has the highest retained earnings

among the four companies in the past four years. Its retained profits have been constantly

increased over the years.

Reserves: It reflects the amount set aside by the entities for a specific purpose. The

reserve maintained by A2 Milk was $12163 million and by Bega Cheese the amount was

$21656 million. The other two companies Wesfarmers and Woolworths have maintained

low value of reserves.

Question 4

The debt and equity are the parts of company’s capital structure and are required to be

maintained in an appropriate proportion. All the four selected companies have maintained their

debt and equity elements by keeping in mind the profitability and financial risk factor.

A2 Milk Company

(AUD in millions)

2014 2015 2016 2017

Total equity 58644 58629 133078 241482

Total Liabilities 17999 30238 77074 102448

The debt of A2 Milk has increased constantly from the past four years. However, along with the

upsurge in debt the equity also increased which keeps the ratio stable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and financial accounting 11

Bega Cheese Limited

(AUD in millions)

2014 2015 2016 2017

Total equity 314388 312666 327838 572674

Total Liabilities 234249 239753 258836 483586

In case of Bega Cheese, the debt did not increased to a great extent from 2014 to 2015 as

compare to the changes in its equity. However, after 2016, the ratio of the company increased to

38% from 14% showing high financial risk.

Wesfarmers Limited

(AUD in millions)

2014 2015 2016 2017

Total equity 25987 24781 22949 23941

Total Liabilities 13740 15621 17834 16174

Wesfarmers’s debt portion has increased continuously till 2016 and after that it falls in 2017. The

ratio was 25% in 2016 which declined to 17% in 2017. This was due to the payments of

company’s net debt.

Woolworths Limited

(AUD in millions)

2014 2015 2016 2017

Total equity 10253 10,834 8782 9876

Total Liabilities 13611 14204 14,720 13039

Same fluctuations is observed in case of Woolworths as its debt increased in 2015 and 2016 but

reduced in 2017. However, company faces high financial leverage as the amount of its equity

Bega Cheese Limited

(AUD in millions)

2014 2015 2016 2017

Total equity 314388 312666 327838 572674

Total Liabilities 234249 239753 258836 483586

In case of Bega Cheese, the debt did not increased to a great extent from 2014 to 2015 as

compare to the changes in its equity. However, after 2016, the ratio of the company increased to

38% from 14% showing high financial risk.

Wesfarmers Limited

(AUD in millions)

2014 2015 2016 2017

Total equity 25987 24781 22949 23941

Total Liabilities 13740 15621 17834 16174

Wesfarmers’s debt portion has increased continuously till 2016 and after that it falls in 2017. The

ratio was 25% in 2016 which declined to 17% in 2017. This was due to the payments of

company’s net debt.

Woolworths Limited

(AUD in millions)

2014 2015 2016 2017

Total equity 10253 10,834 8782 9876

Total Liabilities 13611 14204 14,720 13039

Same fluctuations is observed in case of Woolworths as its debt increased in 2015 and 2016 but

reduced in 2017. However, company faces high financial leverage as the amount of its equity

Corporate and financial accounting 12

reduced in 2016 and 2017. This boosted up the ratio and increases the financial risk of the

company (Woolworths. 2015).

Conclusion

The above report concludes that the manager must disclose all the relevant accounting

information and regulating the financial reporting is very much necessary for avoiding errors and

mistakes. It also suggested that the Bega Cheese has the increased and highest share capital but

at the same time its financial risk is also high. While in comparison to it, the debt component of

Wesfarmers has reduced in 2017 making the company less risky.

reduced in 2016 and 2017. This boosted up the ratio and increases the financial risk of the

company (Woolworths. 2015).

Conclusion

The above report concludes that the manager must disclose all the relevant accounting

information and regulating the financial reporting is very much necessary for avoiding errors and

mistakes. It also suggested that the Bega Cheese has the increased and highest share capital but

at the same time its financial risk is also high. While in comparison to it, the debt component of

Wesfarmers has reduced in 2017 making the company less risky.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.