Comprehensive Financial Accounting Report: Principles and Application

VerifiedAdded on 2023/03/31

|38

|4678

|141

Report

AI Summary

This report provides a comprehensive analysis of financial accounting principles, regulations, and their practical applications. It begins by evaluating the role and regulations of financial accounting, including the influence of bodies like the FRC, ASB, FCA, IFRC, and IASB. The report then delves into accounting guidelines and principles such as economic entity, monetary unit, full disclosure, and revenue recognition. Through several client-based case studies, the report demonstrates the preparation of journal entries, ledger accounts, trial balances, income statements, and balance sheets. Furthermore, it explores concepts like consistency, material disclosure, depreciation methods, bank reconciliation statements, and the use of control, suspense, and clearing accounts, offering a detailed understanding of financial accounting practices. Desklib provides access to this and other solved assignments for students.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1) Evaluating financial accounting..............................................................................................3

2) Regulations regarding financial accounting............................................................................4

3 Accounting guideline and principles......................................................................................5

4 Convention and concepts w.r.t. consistency and material disclosure.......................................6

CLIENT 1........................................................................................................................................7

a. Journal entries..........................................................................................................................7

b. Ledger accounts.......................................................................................................................9

c. Trial balance...........................................................................................................................19

CLIENT 2......................................................................................................................................20

a. Preparing income statement...................................................................................................20

b. Framing statement of financial statement..............................................................................21

CLIENT 3......................................................................................................................................22

a. Profitability statement............................................................................................................22

b. balance sheet..........................................................................................................................23

c. Stating accounting principles and concepts...........................................................................24

d. Defining the concept of depreciation and related methods...................................................25

CLIENT 4......................................................................................................................................27

A. Explaining the purpose of preparing bank statement............................................................27

B. Listing the causes due to which record of bank and cash statement varies..........................27

c. Preparation of BRS................................................................................................................28

CLIENT 5......................................................................................................................................29

A) Prepare sales ledger control account and purchase ledger control account..........................29

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1) Evaluating financial accounting..............................................................................................3

2) Regulations regarding financial accounting............................................................................4

3 Accounting guideline and principles......................................................................................5

4 Convention and concepts w.r.t. consistency and material disclosure.......................................6

CLIENT 1........................................................................................................................................7

a. Journal entries..........................................................................................................................7

b. Ledger accounts.......................................................................................................................9

c. Trial balance...........................................................................................................................19

CLIENT 2......................................................................................................................................20

a. Preparing income statement...................................................................................................20

b. Framing statement of financial statement..............................................................................21

CLIENT 3......................................................................................................................................22

a. Profitability statement............................................................................................................22

b. balance sheet..........................................................................................................................23

c. Stating accounting principles and concepts...........................................................................24

d. Defining the concept of depreciation and related methods...................................................25

CLIENT 4......................................................................................................................................27

A. Explaining the purpose of preparing bank statement............................................................27

B. Listing the causes due to which record of bank and cash statement varies..........................27

c. Preparation of BRS................................................................................................................28

CLIENT 5......................................................................................................................................29

A) Prepare sales ledger control account and purchase ledger control account..........................29

B) Requirement to draw the control account. Explain the term 'control account'.....................29

CLIENT 6......................................................................................................................................30

A) Explain the term suspense account and its main features.....................................................30

B) Draft a Trial Balance............................................................................................................31

C) Prepare journal entries..........................................................................................................31

D) Differentiate between suspense account and Clearing Account...........................................31

CONCLUSION..............................................................................................................................31

CLIENT 6......................................................................................................................................30

A) Explain the term suspense account and its main features.....................................................30

B) Draft a Trial Balance............................................................................................................31

C) Prepare journal entries..........................................................................................................31

D) Differentiate between suspense account and Clearing Account...........................................31

CONCLUSION..............................................................................................................................31

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is highly concerned with the preparation of appropriate final

accounts which in turn presents the fair view of monetary information. In the business

organization, manager is highly concerned in relation to getting information about monetary

health and performance. In this regard, system of financial accounting enables manager to

record all the business transactions by following standardized rules or guidelines. Thus, by

following the concepts and rules of financial accounting business entity can prepare suitable

income and cash flow statement as well as balance sheet. This in turn helps business entity to

assess the extent to which financial performance is on right track or not. The present report is

based on different case situations which will provide deeper understanding about the manner in

which trial balance as well as adjusted balance sheet and income statement can be framed.

Further, report will also shed light on the concepts of suspense, clearing and control account. It

will also develop understanding about depreciation methods and its significance level.

PART A

1) Evaluating financial accounting

Financials accounting can be described as the records, reports and presentation of the data

in tabular form related to the finance performance of the organization. Such data occurs when

there is transaction related to the goods and services purchased, produced and sold. Making such

entities helps to understand the gain, expenses and revenue of the company during the period of

production and supply of the product. Such tasks are accomplished in the ledger which includes

the data related to the balance sheet, data related to collection of revenue, profit and loss

occurred in the company and income statements , asset accounts etc. Moreover, it may include

the data related to accounts, cash transaction, equipment cost, investment in capital, inventory

and other investment made by the organization. Obtained above data are used by the

organization in order to forecast the economic position of company in market and allows to make

further decision and strategies which are necessary and needs to be implemented for achieving

the goals and objectives of firm (Barth, 2015).

Furthermore, momentary performance details are prepared in the form of reports and

along with the data of previous years transaction. Various financial tools and optimum funds for

financial benefit can be achieved through the financial management. In order to complete the

Financial accounting is highly concerned with the preparation of appropriate final

accounts which in turn presents the fair view of monetary information. In the business

organization, manager is highly concerned in relation to getting information about monetary

health and performance. In this regard, system of financial accounting enables manager to

record all the business transactions by following standardized rules or guidelines. Thus, by

following the concepts and rules of financial accounting business entity can prepare suitable

income and cash flow statement as well as balance sheet. This in turn helps business entity to

assess the extent to which financial performance is on right track or not. The present report is

based on different case situations which will provide deeper understanding about the manner in

which trial balance as well as adjusted balance sheet and income statement can be framed.

Further, report will also shed light on the concepts of suspense, clearing and control account. It

will also develop understanding about depreciation methods and its significance level.

PART A

1) Evaluating financial accounting

Financials accounting can be described as the records, reports and presentation of the data

in tabular form related to the finance performance of the organization. Such data occurs when

there is transaction related to the goods and services purchased, produced and sold. Making such

entities helps to understand the gain, expenses and revenue of the company during the period of

production and supply of the product. Such tasks are accomplished in the ledger which includes

the data related to the balance sheet, data related to collection of revenue, profit and loss

occurred in the company and income statements , asset accounts etc. Moreover, it may include

the data related to accounts, cash transaction, equipment cost, investment in capital, inventory

and other investment made by the organization. Obtained above data are used by the

organization in order to forecast the economic position of company in market and allows to make

further decision and strategies which are necessary and needs to be implemented for achieving

the goals and objectives of firm (Barth, 2015).

Furthermore, momentary performance details are prepared in the form of reports and

along with the data of previous years transaction. Various financial tools and optimum funds for

financial benefit can be achieved through the financial management. In order to complete the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

above task various tools like accounting information system are used which are popularly used

by the manager, accountants, stakeholder and other accounts related persons. Various set of rules

and regulation are provided and needs to be followed in order to achieve accounting standards

and provide financials accountancy. Several calculation and transacting can be easily understood

through financial accounting. Actual business, financials and economical condition of the

organisation are mentioned through the report. Such values enhance and standards the

capabilities of the business orientation (Beatty and Liao, 2014).

2) Regulations regarding financial accounting

In UK financial accounting is governed through Financial Reporting Council (FRC)

which is developed by the Accounting Standards Board (ASB). Mainly there are various sets of

regulation which are needed to be followed in financial accounting such as Accounting Standard

Boards(ASB), Financial Conduct Authority (FCA). International Financial reporting Council

(IFRC) and International Accounting Standards Broad (IASB). These accounting standards

provide the set of rules, policies along with the obligations which are needed during time of

preparation and for maintenance of the financial records. Financial reporting Council board is

supported by the three committees which are codes and standards committee which provides the

advice to them for maintaining effective framework. Conduct committee which is needed to

support the high quality corporate reporting. In order to prepare the financial statements like

income statement, balance sheet and cash flow statement varied principles are followed like

GAAP general accepted accounting principles (Beaumont, 2015). The process includes the

discipline, overseeing the accountants, monitoring and checking of the quality.

International Financial Reporting Standards (IFRS):- For the accountancy profession,

IFRS is the international representative body. The organisation supports, promotes and

encourage public to protect the level of accountancy in the global world. They issues

standards which are required for assurance along with auditing, education, public sector

accounting, accounting ethics together with instruction regarding accountants working in

the financial sector. The organization was founded and developed by independent

society. The set of regulation made are adopted and followed internationally for

preparing Financials accountant.

by the manager, accountants, stakeholder and other accounts related persons. Various set of rules

and regulation are provided and needs to be followed in order to achieve accounting standards

and provide financials accountancy. Several calculation and transacting can be easily understood

through financial accounting. Actual business, financials and economical condition of the

organisation are mentioned through the report. Such values enhance and standards the

capabilities of the business orientation (Beatty and Liao, 2014).

2) Regulations regarding financial accounting

In UK financial accounting is governed through Financial Reporting Council (FRC)

which is developed by the Accounting Standards Board (ASB). Mainly there are various sets of

regulation which are needed to be followed in financial accounting such as Accounting Standard

Boards(ASB), Financial Conduct Authority (FCA). International Financial reporting Council

(IFRC) and International Accounting Standards Broad (IASB). These accounting standards

provide the set of rules, policies along with the obligations which are needed during time of

preparation and for maintenance of the financial records. Financial reporting Council board is

supported by the three committees which are codes and standards committee which provides the

advice to them for maintaining effective framework. Conduct committee which is needed to

support the high quality corporate reporting. In order to prepare the financial statements like

income statement, balance sheet and cash flow statement varied principles are followed like

GAAP general accepted accounting principles (Beaumont, 2015). The process includes the

discipline, overseeing the accountants, monitoring and checking of the quality.

International Financial Reporting Standards (IFRS):- For the accountancy profession,

IFRS is the international representative body. The organisation supports, promotes and

encourage public to protect the level of accountancy in the global world. They issues

standards which are required for assurance along with auditing, education, public sector

accounting, accounting ethics together with instruction regarding accountants working in

the financial sector. The organization was founded and developed by independent

society. The set of regulation made are adopted and followed internationally for

preparing Financials accountant.

Accounting Standard Board (ASB): The accounting standards set by ASB, various

enforcement and role about accounting are given for the financial details and provision.

Moreover, role of ASB can be understood through following:

1. Supports in preparing the financial standards (Bevis, 2013).

2. Various rules, laws and policies are recorded and mentioned regarding financial information.

3. For the own standard, related terms , guidelines and condition are mentioned. Financial Conduct Authority (FCA): Established in 2013 as UK conduct regulator for

organizational financial service by replacing Financial Services Authority.

International Accounting Standards Broad (IASB): The organisation is independent

and non profit private sector which is employed for the public interest in order to

develop high standards of accounting which can be globally accepted.

All the above mentioned accounting standards are required for establishing the rules and

regulation related to the financial accountancy. Such sets of rules are made through journals,

ledger, balance sheet, profit and loss of accounts. This sets and standards are made to prepare

statements and monetary performance of firm.

3 Accounting guideline and principles

FSAB in required for providing the provision related to guidelines and principle which

are related to mentioning the information and for making the future strategies regarding business

operation. Mentioned below are some of the guidelines and principles which are given by FASB

and are required to describe financial accountancy. These are:

Economic entity assumption: According to this assumption, proprietorship and its

owner are considered as the same entity. But in terms of accountancy these two are

considered as two different for maintaining the data sheets. Finally, making financial

records separately for the owner and company can make the Financial accountancy

efficiently(Bradshaw and et.al., 2013). Monetary unit assumption: Used for representing the cost in unit. For preparing it

organisation profit, loss related to sales are purchase are required for preparing the true

amount of the transaction for the further organisation strategies and operation. Full disclosure principles: the related principles is required for the income gained and

losses occurred which are required during the time of financial transaction. Such

enforcement and role about accounting are given for the financial details and provision.

Moreover, role of ASB can be understood through following:

1. Supports in preparing the financial standards (Bevis, 2013).

2. Various rules, laws and policies are recorded and mentioned regarding financial information.

3. For the own standard, related terms , guidelines and condition are mentioned. Financial Conduct Authority (FCA): Established in 2013 as UK conduct regulator for

organizational financial service by replacing Financial Services Authority.

International Accounting Standards Broad (IASB): The organisation is independent

and non profit private sector which is employed for the public interest in order to

develop high standards of accounting which can be globally accepted.

All the above mentioned accounting standards are required for establishing the rules and

regulation related to the financial accountancy. Such sets of rules are made through journals,

ledger, balance sheet, profit and loss of accounts. This sets and standards are made to prepare

statements and monetary performance of firm.

3 Accounting guideline and principles

FSAB in required for providing the provision related to guidelines and principle which

are related to mentioning the information and for making the future strategies regarding business

operation. Mentioned below are some of the guidelines and principles which are given by FASB

and are required to describe financial accountancy. These are:

Economic entity assumption: According to this assumption, proprietorship and its

owner are considered as the same entity. But in terms of accountancy these two are

considered as two different for maintaining the data sheets. Finally, making financial

records separately for the owner and company can make the Financial accountancy

efficiently(Bradshaw and et.al., 2013). Monetary unit assumption: Used for representing the cost in unit. For preparing it

organisation profit, loss related to sales are purchase are required for preparing the true

amount of the transaction for the further organisation strategies and operation. Full disclosure principles: the related principles is required for the income gained and

losses occurred which are required during the time of financial transaction. Such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

principles improves the business performance. For such accounting policies depreciated

values, loss and scrape value can be calculated. Going concern principles: Concerning the stakeholder, manager and other member are

required for the ongoing concerns which needed to be sorted out. Such principles are

required for the fame and name in the market. Through above rules company

performance and reputation can enhanced.

1. Revenue recognition principles: Mainly requires the actual data needed like income,

revenue rates which show the good reputation of organisation and losses to be ethical. To

understand more clearly following illustration is taken: Suppose company A collected

10000 for selling goods and in the data sheet mentioned 20000 which is illegal as per

business operation. Taking this, different problems are recorded which involves business

activities (Bushman, 2014).

4 Convention and concepts w.r.t. consistency and material disclosure

Convention and concepts are the methods which are required for the providing different

set of rules and guidelines to accountant for prepare financial information. Using the above

mentioned methods the financial accountancy for disclosing the sales and purchase of the

transaction. Moreover, they can be evaluate as:

Conventions in terms of consistency: This concepts comprises of recording all the terms

and values of the business operation. The business values needs to be true and fair for

recording accountancy. Moreover, other implication can be applied during after studying

the accountancy. Financial transaction can be made after evaluating the studies. Hence,

consistency is required to be expressive for recoding and writing financial transactions.

Convention in respect to materiality: Liability of accountant is to mention the business

operation and hence they must make the financial transactions in appropriate ways and in

proper format. Recording wrong details may affect the business operation(Dutta and

Patatoukas, 2016).

values, loss and scrape value can be calculated. Going concern principles: Concerning the stakeholder, manager and other member are

required for the ongoing concerns which needed to be sorted out. Such principles are

required for the fame and name in the market. Through above rules company

performance and reputation can enhanced.

1. Revenue recognition principles: Mainly requires the actual data needed like income,

revenue rates which show the good reputation of organisation and losses to be ethical. To

understand more clearly following illustration is taken: Suppose company A collected

10000 for selling goods and in the data sheet mentioned 20000 which is illegal as per

business operation. Taking this, different problems are recorded which involves business

activities (Bushman, 2014).

4 Convention and concepts w.r.t. consistency and material disclosure

Convention and concepts are the methods which are required for the providing different

set of rules and guidelines to accountant for prepare financial information. Using the above

mentioned methods the financial accountancy for disclosing the sales and purchase of the

transaction. Moreover, they can be evaluate as:

Conventions in terms of consistency: This concepts comprises of recording all the terms

and values of the business operation. The business values needs to be true and fair for

recording accountancy. Moreover, other implication can be applied during after studying

the accountancy. Financial transaction can be made after evaluating the studies. Hence,

consistency is required to be expressive for recoding and writing financial transactions.

Convention in respect to materiality: Liability of accountant is to mention the business

operation and hence they must make the financial transactions in appropriate ways and in

proper format. Recording wrong details may affect the business operation(Dutta and

Patatoukas, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CLIENT 1

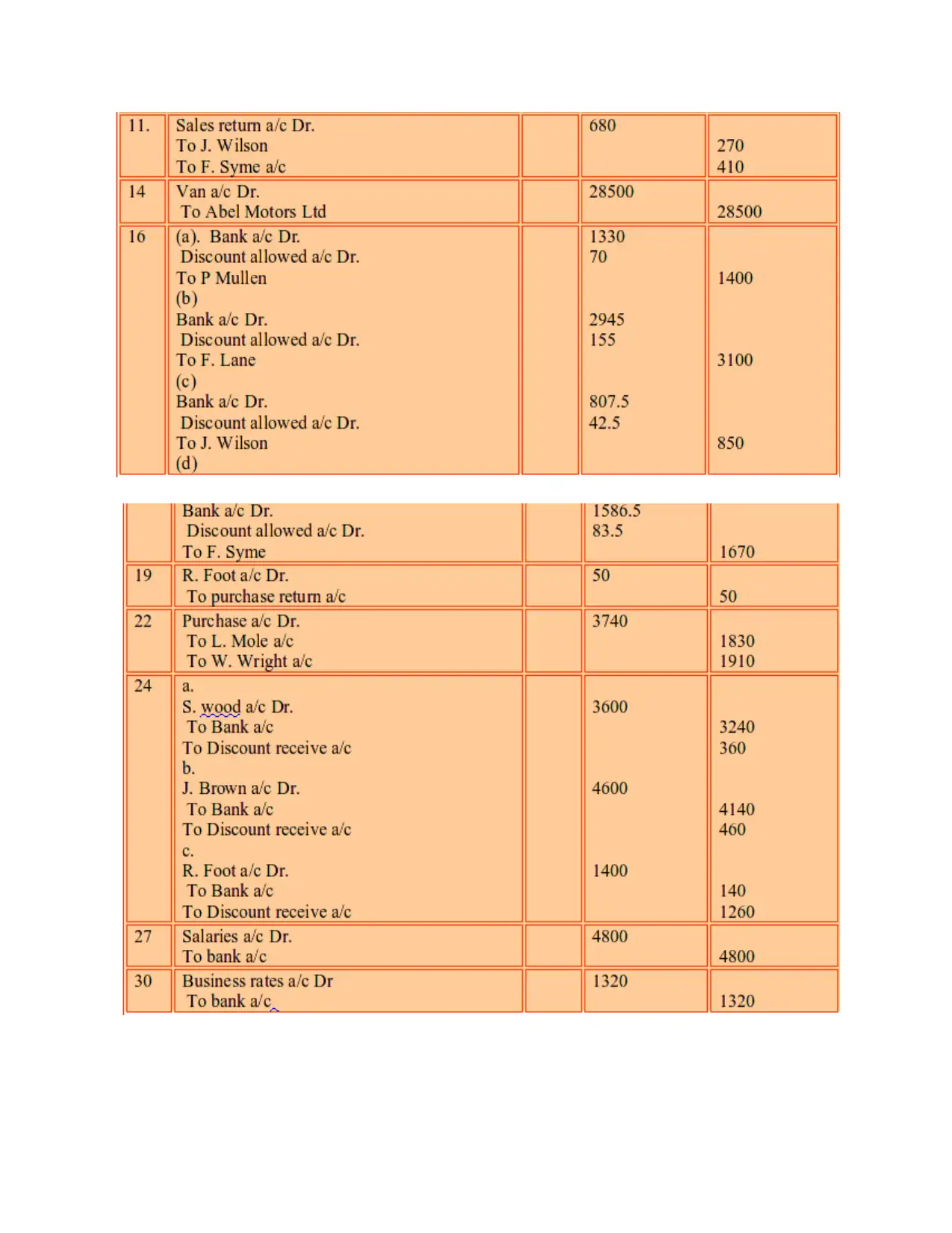

a. Journal entries

System of book keeping places high level of emphasis on recording financial

transactions in an effectual way. On the basis of double entry system, for every debit there must

be a credit. It assumes that each transaction has dual sided effects and helps in presenting the fair

view of monetary transactions (Oldroyd, Tyson and Fleischman, 2015). It helps business entity

in evaluating the transactions which are made during the year or specified time frame.

a. Journal entries

System of book keeping places high level of emphasis on recording financial

transactions in an effectual way. On the basis of double entry system, for every debit there must

be a credit. It assumes that each transaction has dual sided effects and helps in presenting the fair

view of monetary transactions (Oldroyd, Tyson and Fleischman, 2015). It helps business entity

in evaluating the transactions which are made during the year or specified time frame.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b. Ledger accounts

In ledger accounts, accounting personnel sorts and store the transactions pertaining to

income statement and balance sheet. Journals gives input for the preparation of ledger accounts

and thereby helps in preparing further final accounts (Pratt, 2013). Moreover, without preparing

journal accounting personnel is not in position to frame trial balance and thereby income

statement & balance sheet as well.

In ledger accounts, accounting personnel sorts and store the transactions pertaining to

income statement and balance sheet. Journals gives input for the preparation of ledger accounts

and thereby helps in preparing further final accounts (Pratt, 2013). Moreover, without preparing

journal accounting personnel is not in position to frame trial balance and thereby income

statement & balance sheet as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.