Financial Accounting: Financial Ratio Analysis and CGU Identification

VerifiedAdded on 2023/06/12

|13

|3035

|169

Report

AI Summary

This assignment provides solutions to questions related to financial accounting. It includes an analysis of cash-generating units (CGUs) according to AASB 136 for Wentnor Dairy Company Ltd, focusing on identifying CGUs within a vertically integrated structure. Additionally, it performs a financial ratio analysis of Woolworths Ltd, assessing profitability, capital structure, solvency, and efficiency using key ratios. The report interprets the implications of these ratios, particularly concerning liquidity and investment potential. Finally, it discusses the interpretation of foreign currency transactions in the context of Qantas Ltd's annual report, explaining the use of current rate processes and the impact of exchange rate variations.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question No 1................................................................................................................2

Requirement A.............................................................................................................................2

Requirement B.............................................................................................................................2

Requirement C.............................................................................................................................3

Answer to Question No 2................................................................................................................5

Requirement A.............................................................................................................................5

Requirement B.............................................................................................................................5

Requirement C.............................................................................................................................7

Answer to Question No 3................................................................................................................8

Answer to Question No 4..............................................................................................................10

Reference List................................................................................................................................12

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question No 1................................................................................................................2

Requirement A.............................................................................................................................2

Requirement B.............................................................................................................................2

Requirement C.............................................................................................................................3

Answer to Question No 2................................................................................................................5

Requirement A.............................................................................................................................5

Requirement B.............................................................................................................................5

Requirement C.............................................................................................................................7

Answer to Question No 3................................................................................................................8

Answer to Question No 4..............................................................................................................10

Reference List................................................................................................................................12

2

FINANCIAL ACCOUNTING

Answer to Question No 1

According to the scenario that has been provided in the case study, it is seen that Wentnor

Diary Company Ltd is associated with operating their business in the dairy farms and have

expanded their business by purchasing new factories that manufactures milk products. The Chief

Financial Officer of the organization is in the need of recognizing the units that are associated

with the creation of cash for the business in order to undertake the impairment of the assessment

according to AASB 136.

Requirement A

According to the paragraph 6 of the AASB 136, which has been disclosed by the

Australian Accounting Standards Board, the cash creating unit can be explained as the

recognition of the smallest asset groups, which are recognizable and which have the ability to

create cash and are even considered to be free from the other kinds of asset groups1.

Requirement B

According to the provisions that have been laid in the AASB 136, the investigations of

impairment of the assets are in need of the comparisons of the amount that is recoverable and

which has to be made with the value of the assets that is higher and which is in use and the fair

value subtracted by the disposal cost of the assets. The value that is in use according to the

required standard is explained as follows:

1 Wagner, Dominik, et al. "A meta-analysis of the financial performance of family firms:

Another attempt." Journal of Family Business Strategy 6.1 (2015): 3-13.

FINANCIAL ACCOUNTING

Answer to Question No 1

According to the scenario that has been provided in the case study, it is seen that Wentnor

Diary Company Ltd is associated with operating their business in the dairy farms and have

expanded their business by purchasing new factories that manufactures milk products. The Chief

Financial Officer of the organization is in the need of recognizing the units that are associated

with the creation of cash for the business in order to undertake the impairment of the assessment

according to AASB 136.

Requirement A

According to the paragraph 6 of the AASB 136, which has been disclosed by the

Australian Accounting Standards Board, the cash creating unit can be explained as the

recognition of the smallest asset groups, which are recognizable and which have the ability to

create cash and are even considered to be free from the other kinds of asset groups1.

Requirement B

According to the provisions that have been laid in the AASB 136, the investigations of

impairment of the assets are in need of the comparisons of the amount that is recoverable and

which has to be made with the value of the assets that is higher and which is in use and the fair

value subtracted by the disposal cost of the assets. The value that is in use according to the

required standard is explained as follows:

1 Wagner, Dominik, et al. "A meta-analysis of the financial performance of family firms:

Another attempt." Journal of Family Business Strategy 6.1 (2015): 3-13.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL ACCOUNTING

The evaluation of the future cash flows that the organization forecasts to attain from the

usage of the asset

Anticipation about the cash flow timing

The price for taking into account the asset uncertainty

There are several assets, which have been utilized in some of the organizations, which does

not have their own and individual cash flows and these assets can only establish cash flows when

they are considered together within an asset group that are similar in nature. In accordance to the

case study of Wentnor Diary Ltd, the tools and the machines that are utilized for the purification

and the extraction of the milk by the firm, does not have the ability to construct their own cash

flow statements. The significant cash flow creating product for the firm has been milk that is

initially extracted and then purified from the help of the machines. The equipment when utilized

together can be regarded to a cash generating mechanism2. The tools and the machines which is

utilized by the organizations is a blend that is useful for the creation of inflow of cash for the

companies.

Requirement C

There are numerous factors that needs to be considered by the Chief Financial Officer

prior to recognizing the cash creating units of the assets. The Chief Financial Officer of the

organization requires to initially gain knowledge that the cash generating units are the minimum

value of the assets, which can by their own create cash flows for the companies. The reasons and

2 Karna, Amit, Ansgar Richter, and Eberhard Riesenkampff. "Revisiting the role of the

environment in the capabilities–financial performance relationship: A meta‐analysis." Strategic

Management Journal 37.6 (2016): 1154-1173.

FINANCIAL ACCOUNTING

The evaluation of the future cash flows that the organization forecasts to attain from the

usage of the asset

Anticipation about the cash flow timing

The price for taking into account the asset uncertainty

There are several assets, which have been utilized in some of the organizations, which does

not have their own and individual cash flows and these assets can only establish cash flows when

they are considered together within an asset group that are similar in nature. In accordance to the

case study of Wentnor Diary Ltd, the tools and the machines that are utilized for the purification

and the extraction of the milk by the firm, does not have the ability to construct their own cash

flow statements. The significant cash flow creating product for the firm has been milk that is

initially extracted and then purified from the help of the machines. The equipment when utilized

together can be regarded to a cash generating mechanism2. The tools and the machines which is

utilized by the organizations is a blend that is useful for the creation of inflow of cash for the

companies.

Requirement C

There are numerous factors that needs to be considered by the Chief Financial Officer

prior to recognizing the cash creating units of the assets. The Chief Financial Officer of the

organization requires to initially gain knowledge that the cash generating units are the minimum

value of the assets, which can by their own create cash flows for the companies. The reasons and

2 Karna, Amit, Ansgar Richter, and Eberhard Riesenkampff. "Revisiting the role of the

environment in the capabilities–financial performance relationship: A meta‐analysis." Strategic

Management Journal 37.6 (2016): 1154-1173.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL ACCOUNTING

the factors that have been disclosed in Paragraph 69 and continues till Paragraph 71 of the AASB

136, explains how the management administers the functions and the activities of the

organization, which is inclusive of the product lines, specific locations and the regional and the

district locations3. The Chief Financial Officer looks to gain an understanding of how he would

be able to recognize the units that are generating cash of the organizations by making use of the

precise standards, which have been disclosed by the AASB.

The cash generating units of the organizations requires to be identified from a specific

time frame to the other unfailingly for any kind of assets unless there are observations that there

are several alterations related to the asset. The identification of the cash generating units is need

of precise verdicts on the section of the management and even by following the AASB 136,

which is based on the impairment of the assets of the organizations4.

Answer to Question No 2

Requirement A

According to the scenario that is provided in the question, the essential ratios that needs

to be calculated and which are reliant on the profitability, capital structure, solvency and

3 Ongore, Vincent O., et al. "Board composition and financial performance: Empirical analysis of

companies listed at the Nairobi Securities Exchange." International Journal of Economics and

Financial Issues 5.1 (2015): 23.

4 Flammer, Caroline. "Does corporate social responsibility lead to superior financial

performance? A regression discontinuity approach." Management Science 61.11 (2015): 2549-

2568.

FINANCIAL ACCOUNTING

the factors that have been disclosed in Paragraph 69 and continues till Paragraph 71 of the AASB

136, explains how the management administers the functions and the activities of the

organization, which is inclusive of the product lines, specific locations and the regional and the

district locations3. The Chief Financial Officer looks to gain an understanding of how he would

be able to recognize the units that are generating cash of the organizations by making use of the

precise standards, which have been disclosed by the AASB.

The cash generating units of the organizations requires to be identified from a specific

time frame to the other unfailingly for any kind of assets unless there are observations that there

are several alterations related to the asset. The identification of the cash generating units is need

of precise verdicts on the section of the management and even by following the AASB 136,

which is based on the impairment of the assets of the organizations4.

Answer to Question No 2

Requirement A

According to the scenario that is provided in the question, the essential ratios that needs

to be calculated and which are reliant on the profitability, capital structure, solvency and

3 Ongore, Vincent O., et al. "Board composition and financial performance: Empirical analysis of

companies listed at the Nairobi Securities Exchange." International Journal of Economics and

Financial Issues 5.1 (2015): 23.

4 Flammer, Caroline. "Does corporate social responsibility lead to superior financial

performance? A regression discontinuity approach." Management Science 61.11 (2015): 2549-

2568.

5

FINANCIAL ACCOUNTING

efficiency. The ratios are an essential requirement equipment, which is utilized in order to assess

the financial activities and the performance of Woolworths Ltd. The computation of the various

ratios, which have been explained in the appendix portion signifies the significant ratios which

explains the overall financial performance of the organization.

Requirement B

The current ratio of the organization addresses that the liquidity scenario of the firm is

not at all effective as the forecast has been explained to be lower than 1. The acid test ratio,

which is provided in the calculation within the appendix part even addresses the fact that the

organizations are going through liquidity problems. The acid test ratio and the current ratio of the

company has been found to be 0.330 and 0.793. The ratio even discloses the fact that the

forecasts of the current ratio and the acid test ratio has fallen from the forecasts of the last year,

which makes it pertinent that the organization has limited liquid cash, which can be discovered

be a problem. The gross profit margin of the company has risen from the last year, which

recommends that the organization is developing and expanding with respect to their

profitability5. The rise in the level of gross profit of the firm is even regarded to be a financial

gauge of the organization. The company has essentially enhanced with respect to the gross profit

margin of the organization. It is seen that the receivable turnover ratio of the firm has even

indicated a rise, which is regarded to be a positive and significant sign for the organization and

this is shown with the help of the ratios that have been constructed. The receivable turnover ratio

5 Saeidi, Sayedeh Parastoo, et al. "How does corporate social responsibility contribute to firm

financial performance? The mediating role of competitive advantage, reputation, and customer

satisfaction." Journal of Business Research 68.2 (2015): 341-350.

FINANCIAL ACCOUNTING

efficiency. The ratios are an essential requirement equipment, which is utilized in order to assess

the financial activities and the performance of Woolworths Ltd. The computation of the various

ratios, which have been explained in the appendix portion signifies the significant ratios which

explains the overall financial performance of the organization.

Requirement B

The current ratio of the organization addresses that the liquidity scenario of the firm is

not at all effective as the forecast has been explained to be lower than 1. The acid test ratio,

which is provided in the calculation within the appendix part even addresses the fact that the

organizations are going through liquidity problems. The acid test ratio and the current ratio of the

company has been found to be 0.330 and 0.793. The ratio even discloses the fact that the

forecasts of the current ratio and the acid test ratio has fallen from the forecasts of the last year,

which makes it pertinent that the organization has limited liquid cash, which can be discovered

be a problem. The gross profit margin of the company has risen from the last year, which

recommends that the organization is developing and expanding with respect to their

profitability5. The rise in the level of gross profit of the firm is even regarded to be a financial

gauge of the organization. The company has essentially enhanced with respect to the gross profit

margin of the organization. It is seen that the receivable turnover ratio of the firm has even

indicated a rise, which is regarded to be a positive and significant sign for the organization and

this is shown with the help of the ratios that have been constructed. The receivable turnover ratio

5 Saeidi, Sayedeh Parastoo, et al. "How does corporate social responsibility contribute to firm

financial performance? The mediating role of competitive advantage, reputation, and customer

satisfaction." Journal of Business Research 68.2 (2015): 341-350.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL ACCOUNTING

even recommends that the credit plans and policies of the firm is very much effective and strong,

which is an outcome of the fact that the receivable turnover ratio of the firm is positive and

encouraging. The return on the net sales and the return on assets of the firm has terribly enhanced

with respect to their business activities from the values that have been attained in the last year

and the figures that have been attained have been shown in the appendix section. In the year

2016, the outcome of the return on equity and the return on sales have indicated the fact that the

company Woolworths Ltd indicates returns that have been negative from which the functions of

the business has enhanced essentially and thereby have made the returns which are received by

the organization suitable and vital. The return on equity is looked upon to be a financial gauge,

which is assesses the probable business investors in order to undertake decisions, with respect to

whether they are going to undertake investments in the company shares or not6. Furthermore, the

return on equity that has been looked upon to be encouraging even addresses the fact that the

organization is able to satisfy the requirements of the shareholders and thereby gaining precise

and suitable returns for the same. The dividend payout ratio of the organization has even

developed vitally from the last year and this indicates that the organization is currently associated

with the principle of wealth maximization for the shareholders who are related to the

organization7. In the year 2017, the dividend payout ratio for the firm has been 70.35% and the

6 Rani, Neelam, Surendra S. Yadav, and P. K. Jain. "Financial performance analysis of mergers

and acquisitions: evidence from India." International Journal of Commerce and

Management 25.4 (2015): 402-423.

7 O’Neill, Peter, Amrik Sohal, and Chih Wei Teng. "Quality management approaches and their

impact on firms׳ financial performance–An Australian study." International Journal of

Production Economics 171 (2016): 381-393.

FINANCIAL ACCOUNTING

even recommends that the credit plans and policies of the firm is very much effective and strong,

which is an outcome of the fact that the receivable turnover ratio of the firm is positive and

encouraging. The return on the net sales and the return on assets of the firm has terribly enhanced

with respect to their business activities from the values that have been attained in the last year

and the figures that have been attained have been shown in the appendix section. In the year

2016, the outcome of the return on equity and the return on sales have indicated the fact that the

company Woolworths Ltd indicates returns that have been negative from which the functions of

the business has enhanced essentially and thereby have made the returns which are received by

the organization suitable and vital. The return on equity is looked upon to be a financial gauge,

which is assesses the probable business investors in order to undertake decisions, with respect to

whether they are going to undertake investments in the company shares or not6. Furthermore, the

return on equity that has been looked upon to be encouraging even addresses the fact that the

organization is able to satisfy the requirements of the shareholders and thereby gaining precise

and suitable returns for the same. The dividend payout ratio of the organization has even

developed vitally from the last year and this indicates that the organization is currently associated

with the principle of wealth maximization for the shareholders who are related to the

organization7. In the year 2017, the dividend payout ratio for the firm has been 70.35% and the

6 Rani, Neelam, Surendra S. Yadav, and P. K. Jain. "Financial performance analysis of mergers

and acquisitions: evidence from India." International Journal of Commerce and

Management 25.4 (2015): 402-423.

7 O’Neill, Peter, Amrik Sohal, and Chih Wei Teng. "Quality management approaches and their

impact on firms׳ financial performance–An Australian study." International Journal of

Production Economics 171 (2016): 381-393.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ACCOUNTING

percentage has improved drastically from the assessments that have been made in the last year.

Therefore, from the explanations that have been made earlier, it is pertinent that the organization

is favorable in order to undertake investments and therefore the shareholders has to undertake

investments in the shares of the firm. On the other hand, the organization has to enhance and

maintain their liquidity scenario and accordingly make sure that the organization does not go

through any kind of crisis related to liquidity8. Therefore, it can be explained that the investors

need to undertake investments in the company shares.

Requirement C

According to the ratios that have been calculated and is explained in Requirement A, the

acid test and the current ratio of the firm have explained that the firm does not have ratio values

that are encouraging in the year 2017 and the values have been 0.330 ad 0.793. The ratio, which

have been computed for the firm does not have any similarity with the precise standards and the

value has been 2:1 for a current ratio and the ideal ratio for acid test ratio has been 1.5:1.

According to the ratio of the concerned organization, it can be stated that the attained values are

not in line with the ideal standards and therefore this explains that the firm may be going through

liquidity issues which is essential to rectify from the normal mind set of the organization9.

8 Ozkan, Nasif, Sinan Cakan, and Murad Kayacan. "Intellectual capital and financial

performance: A study of the Turkish Banking Sector." Borsa Istanbul Review 17.3 (2017): 190-

198.

9 Waworuntu, Stephanus Remond, Michelle Dewi Wantah, and Toto Rusmanto. "CSR and

financial performance analysis: evidence from top ASEAN listed companies." Procedia-Social

and Behavioral Sciences 164 (2014): 493-500.

FINANCIAL ACCOUNTING

percentage has improved drastically from the assessments that have been made in the last year.

Therefore, from the explanations that have been made earlier, it is pertinent that the organization

is favorable in order to undertake investments and therefore the shareholders has to undertake

investments in the shares of the firm. On the other hand, the organization has to enhance and

maintain their liquidity scenario and accordingly make sure that the organization does not go

through any kind of crisis related to liquidity8. Therefore, it can be explained that the investors

need to undertake investments in the company shares.

Requirement C

According to the ratios that have been calculated and is explained in Requirement A, the

acid test and the current ratio of the firm have explained that the firm does not have ratio values

that are encouraging in the year 2017 and the values have been 0.330 ad 0.793. The ratio, which

have been computed for the firm does not have any similarity with the precise standards and the

value has been 2:1 for a current ratio and the ideal ratio for acid test ratio has been 1.5:1.

According to the ratio of the concerned organization, it can be stated that the attained values are

not in line with the ideal standards and therefore this explains that the firm may be going through

liquidity issues which is essential to rectify from the normal mind set of the organization9.

8 Ozkan, Nasif, Sinan Cakan, and Murad Kayacan. "Intellectual capital and financial

performance: A study of the Turkish Banking Sector." Borsa Istanbul Review 17.3 (2017): 190-

198.

9 Waworuntu, Stephanus Remond, Michelle Dewi Wantah, and Toto Rusmanto. "CSR and

financial performance analysis: evidence from top ASEAN listed companies." Procedia-Social

and Behavioral Sciences 164 (2014): 493-500.

8

FINANCIAL ACCOUNTING

Answer to Question No 3

According to the concerned question, which comprises of a paragraph that is disclosed in

the annual report of “Qantas Ltd”, which is associated to the interpretation of the foreign

currency in the domestic currency. The company has been associated with transactions that have

been made foreign in the year during which the company received income and in order to record

these revenues in the financial statements, it is essential for the firm to translate this kind of

transactions. The technique that is utilized frequently by most of the firms in order to undertake

the translations has been the current rate process.

The factor due to which the transactions related to foreign exchange takes place is

because of the variations that takes place in the foreign currency rate with respect to the domestic

currency10. This arises because of several factors like the inflation rate in the domestic and the

foreign countries, the policies that have been constructed by the government and several other

factors. The variation that is discovered in the comprehensive income statement and any kind of

gains is transported to the “foreign currency translation reserve account”.

10 Lunardi, Guilherme Lerch, et al. "The impact of adopting IT governance on financial

performance: An empirical analysis among Brazilian firms." International Journal of

Accounting Information Systems 15.1 (2014): 66-81.

FINANCIAL ACCOUNTING

Answer to Question No 3

According to the concerned question, which comprises of a paragraph that is disclosed in

the annual report of “Qantas Ltd”, which is associated to the interpretation of the foreign

currency in the domestic currency. The company has been associated with transactions that have

been made foreign in the year during which the company received income and in order to record

these revenues in the financial statements, it is essential for the firm to translate this kind of

transactions. The technique that is utilized frequently by most of the firms in order to undertake

the translations has been the current rate process.

The factor due to which the transactions related to foreign exchange takes place is

because of the variations that takes place in the foreign currency rate with respect to the domestic

currency10. This arises because of several factors like the inflation rate in the domestic and the

foreign countries, the policies that have been constructed by the government and several other

factors. The variation that is discovered in the comprehensive income statement and any kind of

gains is transported to the “foreign currency translation reserve account”.

10 Lunardi, Guilherme Lerch, et al. "The impact of adopting IT governance on financial

performance: An empirical analysis among Brazilian firms." International Journal of

Accounting Information Systems 15.1 (2014): 66-81.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL ACCOUNTING

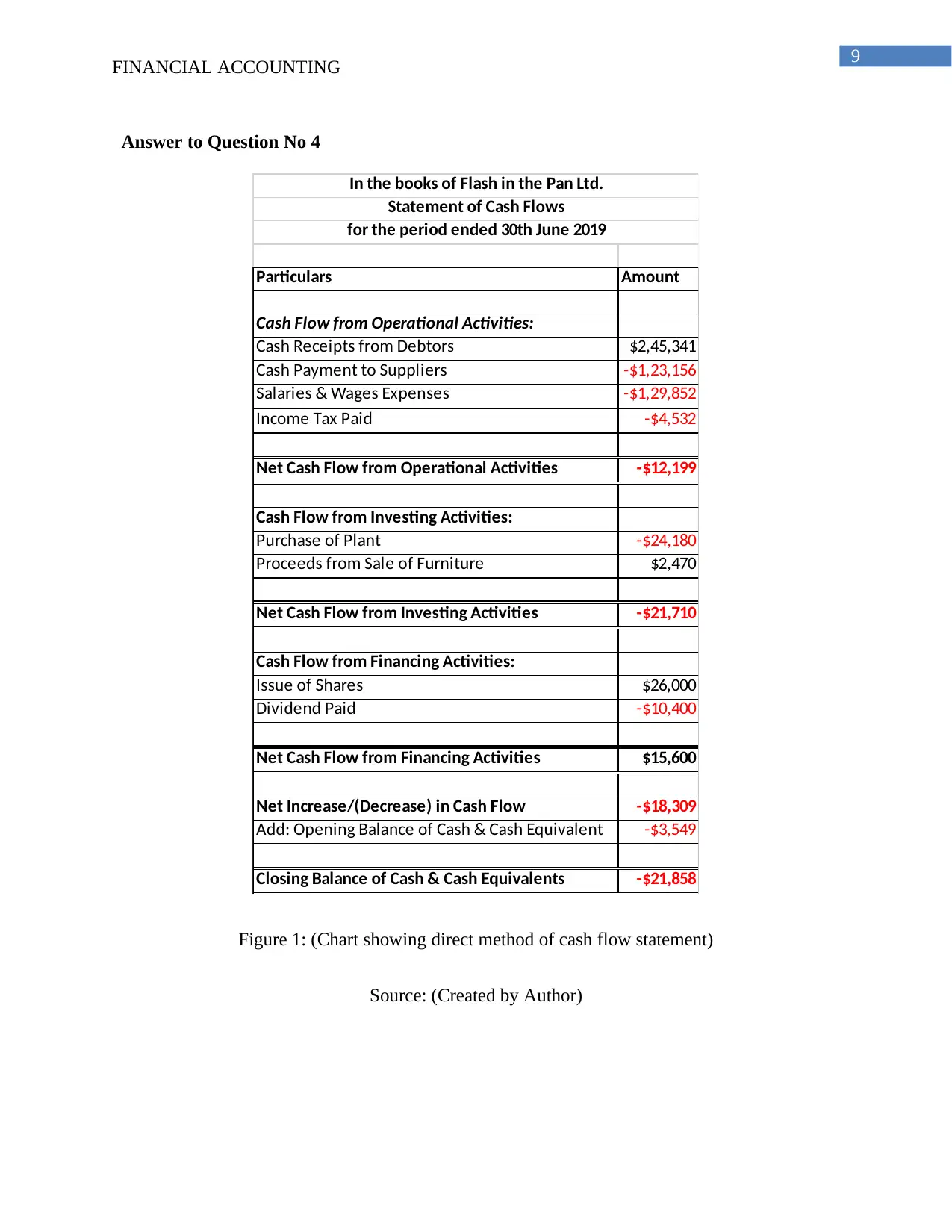

Answer to Question No 4

Particulars Amount

Cash Flow from Operational Activities:

Cash Receipts from Debtors $2,45,341

Cash Payment to Suppliers -$1,23,156

Salaries & Wages Expenses -$1,29,852

Income Tax Paid -$4,532

Net Cash Flow from Operational Activities -$12,199

Cash Flow from Investing Activities:

Purchase of Plant -$24,180

Proceeds from Sale of Furniture $2,470

Net Cash Flow from Investing Activities -$21,710

Cash Flow from Financing Activities:

Issue of Shares $26,000

Dividend Paid -$10,400

Net Cash Flow from Financing Activities $15,600

Net Increase/(Decrease) in Cash Flow -$18,309

Add: Opening Balance of Cash & Cash Equivalent -$3,549

Closing Balance of Cash & Cash Equivalents -$21,858

In the books of Flash in the Pan Ltd.

Statement of Cash Flows

for the period ended 30th June 2019

Figure 1: (Chart showing direct method of cash flow statement)

Source: (Created by Author)

FINANCIAL ACCOUNTING

Answer to Question No 4

Particulars Amount

Cash Flow from Operational Activities:

Cash Receipts from Debtors $2,45,341

Cash Payment to Suppliers -$1,23,156

Salaries & Wages Expenses -$1,29,852

Income Tax Paid -$4,532

Net Cash Flow from Operational Activities -$12,199

Cash Flow from Investing Activities:

Purchase of Plant -$24,180

Proceeds from Sale of Furniture $2,470

Net Cash Flow from Investing Activities -$21,710

Cash Flow from Financing Activities:

Issue of Shares $26,000

Dividend Paid -$10,400

Net Cash Flow from Financing Activities $15,600

Net Increase/(Decrease) in Cash Flow -$18,309

Add: Opening Balance of Cash & Cash Equivalent -$3,549

Closing Balance of Cash & Cash Equivalents -$21,858

In the books of Flash in the Pan Ltd.

Statement of Cash Flows

for the period ended 30th June 2019

Figure 1: (Chart showing direct method of cash flow statement)

Source: (Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

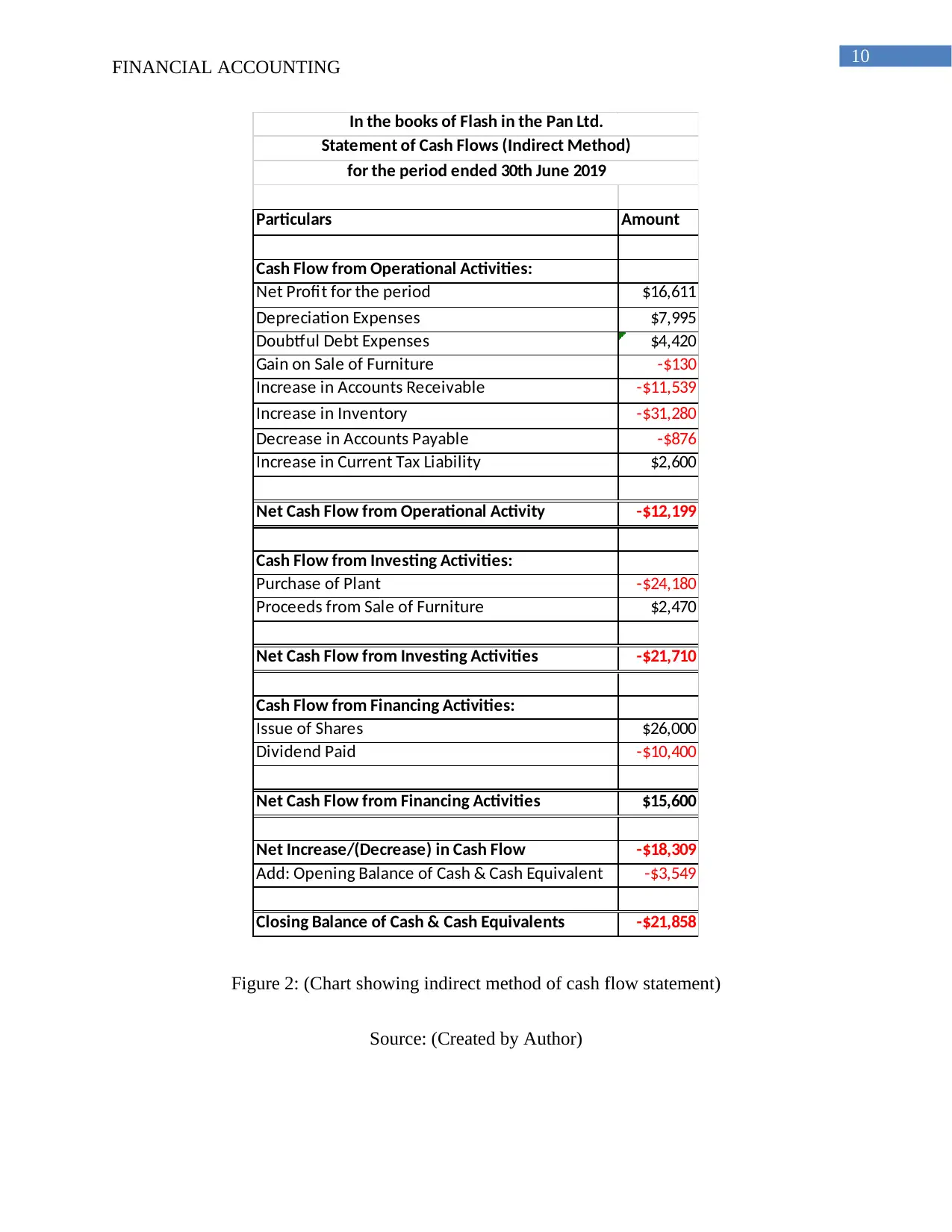

FINANCIAL ACCOUNTING

Particulars Amount

Cash Flow from Operational Activities:

Net Profit for the period $16,611

Depreciation Expenses $7,995

Doubtful Debt Expenses $4,420

Gain on Sale of Furniture -$130

Increase in Accounts Receivable -$11,539

Increase in Inventory -$31,280

Decrease in Accounts Payable -$876

Increase in Current Tax Liability $2,600

Net Cash Flow from Operational Activity -$12,199

Cash Flow from Investing Activities:

Purchase of Plant -$24,180

Proceeds from Sale of Furniture $2,470

Net Cash Flow from Investing Activities -$21,710

Cash Flow from Financing Activities:

Issue of Shares $26,000

Dividend Paid -$10,400

Net Cash Flow from Financing Activities $15,600

Net Increase/(Decrease) in Cash Flow -$18,309

Add: Opening Balance of Cash & Cash Equivalent -$3,549

Closing Balance of Cash & Cash Equivalents -$21,858

In the books of Flash in the Pan Ltd.

Statement of Cash Flows (Indirect Method)

for the period ended 30th June 2019

Figure 2: (Chart showing indirect method of cash flow statement)

Source: (Created by Author)

FINANCIAL ACCOUNTING

Particulars Amount

Cash Flow from Operational Activities:

Net Profit for the period $16,611

Depreciation Expenses $7,995

Doubtful Debt Expenses $4,420

Gain on Sale of Furniture -$130

Increase in Accounts Receivable -$11,539

Increase in Inventory -$31,280

Decrease in Accounts Payable -$876

Increase in Current Tax Liability $2,600

Net Cash Flow from Operational Activity -$12,199

Cash Flow from Investing Activities:

Purchase of Plant -$24,180

Proceeds from Sale of Furniture $2,470

Net Cash Flow from Investing Activities -$21,710

Cash Flow from Financing Activities:

Issue of Shares $26,000

Dividend Paid -$10,400

Net Cash Flow from Financing Activities $15,600

Net Increase/(Decrease) in Cash Flow -$18,309

Add: Opening Balance of Cash & Cash Equivalent -$3,549

Closing Balance of Cash & Cash Equivalents -$21,858

In the books of Flash in the Pan Ltd.

Statement of Cash Flows (Indirect Method)

for the period ended 30th June 2019

Figure 2: (Chart showing indirect method of cash flow statement)

Source: (Created by Author)

11

FINANCIAL ACCOUNTING

Reference List

Flammer, Caroline. "Does corporate social responsibility lead to superior financial performance?

A regression discontinuity approach." Management Science 61.11 (2015): 2549-2568.

Karna, Amit, Ansgar Richter, and Eberhard Riesenkampff. "Revisiting the role of the

environment in the capabilities–financial performance relationship: A meta‐analysis." Strategic

Management Journal 37.6 (2016): 1154-1173.

Lunardi, Guilherme Lerch, et al. "The impact of adopting IT governance on financial

performance: An empirical analysis among Brazilian firms." International Journal of

Accounting Information Systems 15.1 (2014): 66-81.

O’Neill, Peter, Amrik Sohal, and Chih Wei Teng. "Quality management approaches and their

impact on firms׳ financial performance–An Australian study." International Journal of

Production Economics 171 (2016): 381-393.

Ongore, Vincent O., et al. "Board composition and financial performance: Empirical analysis of

companies listed at the Nairobi Securities Exchange." International Journal of Economics and

Financial Issues 5.1 (2015): 23.

Ozkan, Nasif, Sinan Cakan, and Murad Kayacan. "Intellectual capital and financial performance:

A study of the Turkish Banking Sector." Borsa Istanbul Review 17.3 (2017): 190-198.

Rani, Neelam, Surendra S. Yadav, and P. K. Jain. "Financial performance analysis of mergers

and acquisitions: evidence from India." International Journal of Commerce and

Management 25.4 (2015): 402-423.

FINANCIAL ACCOUNTING

Reference List

Flammer, Caroline. "Does corporate social responsibility lead to superior financial performance?

A regression discontinuity approach." Management Science 61.11 (2015): 2549-2568.

Karna, Amit, Ansgar Richter, and Eberhard Riesenkampff. "Revisiting the role of the

environment in the capabilities–financial performance relationship: A meta‐analysis." Strategic

Management Journal 37.6 (2016): 1154-1173.

Lunardi, Guilherme Lerch, et al. "The impact of adopting IT governance on financial

performance: An empirical analysis among Brazilian firms." International Journal of

Accounting Information Systems 15.1 (2014): 66-81.

O’Neill, Peter, Amrik Sohal, and Chih Wei Teng. "Quality management approaches and their

impact on firms׳ financial performance–An Australian study." International Journal of

Production Economics 171 (2016): 381-393.

Ongore, Vincent O., et al. "Board composition and financial performance: Empirical analysis of

companies listed at the Nairobi Securities Exchange." International Journal of Economics and

Financial Issues 5.1 (2015): 23.

Ozkan, Nasif, Sinan Cakan, and Murad Kayacan. "Intellectual capital and financial performance:

A study of the Turkish Banking Sector." Borsa Istanbul Review 17.3 (2017): 190-198.

Rani, Neelam, Surendra S. Yadav, and P. K. Jain. "Financial performance analysis of mergers

and acquisitions: evidence from India." International Journal of Commerce and

Management 25.4 (2015): 402-423.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.