Financial Accounting and Principles: Detailed Company Report

VerifiedAdded on 2020/07/23

|37

|2902

|88

Report

AI Summary

This comprehensive financial accounting report begins with an introduction to the importance of financial accounting in business, emphasizing its role in recording transactions and preparing financial statements. The report then provides a detailed analysis of various accounting concepts and regulations, including financial accounting principles, legal frameworks, and accounting standards. It explores the preparation of reports for a line manager, including journal entries, ledger accounts, and trial balances for multiple clients. The report also delves into the creation and interpretation of income statements and balance sheets, alongside discussions on accounting concepts such as consistency, prudence, and depreciation methods. Furthermore, the report covers bank statements, cash books, reconciliation processes, and various accounting methods, providing a complete overview of financial accounting practices. The report concludes with a summary of key concepts and principles, highlighting their significance in assessing the overall financial performance of organizations.

Financial Accounting &

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A) Preparation of report for Line Manager............................................................................1

CLIENT 1........................................................................................................................................4

1. Passing journal entries........................................................................................................4

2. Preparation of ledger accounts...........................................................................................8

................................................................................................................................................9

................................................................................................................................................9

................................................................................................................................................9

..............................................................................................................................................10

..............................................................................................................................................10

..............................................................................................................................................11

3. Trial balance.....................................................................................................................18

M1. Purchase and sale transactions......................................................................................19

D1 Trial balance...................................................................................................................19

CLIENT 2......................................................................................................................................19

A) Income statement.............................................................................................................19

B) Balance sheet...................................................................................................................20

CLIENT 3......................................................................................................................................22

A) Income statement for the company.................................................................................22

..............................................................................................................................................23

B) Balance sheet...................................................................................................................24

..............................................................................................................................................27

..............................................................................................................................................28

..............................................................................................................................................28

C) Concepts of accounting...................................................................................................28

D) Methods of deprecation...................................................................................................29

M2 Income statement, balance sheet and cash flow statements...........................................29

D2 Calculations in producing final accounts........................................................................29

CLIENT 4......................................................................................................................................29

INTRODUCTION...........................................................................................................................1

A) Preparation of report for Line Manager............................................................................1

CLIENT 1........................................................................................................................................4

1. Passing journal entries........................................................................................................4

2. Preparation of ledger accounts...........................................................................................8

................................................................................................................................................9

................................................................................................................................................9

................................................................................................................................................9

..............................................................................................................................................10

..............................................................................................................................................10

..............................................................................................................................................11

3. Trial balance.....................................................................................................................18

M1. Purchase and sale transactions......................................................................................19

D1 Trial balance...................................................................................................................19

CLIENT 2......................................................................................................................................19

A) Income statement.............................................................................................................19

B) Balance sheet...................................................................................................................20

CLIENT 3......................................................................................................................................22

A) Income statement for the company.................................................................................22

..............................................................................................................................................23

B) Balance sheet...................................................................................................................24

..............................................................................................................................................27

..............................................................................................................................................28

..............................................................................................................................................28

C) Concepts of accounting...................................................................................................28

D) Methods of deprecation...................................................................................................29

M2 Income statement, balance sheet and cash flow statements...........................................29

D2 Calculations in producing final accounts........................................................................29

CLIENT 4......................................................................................................................................29

A) Bank statement................................................................................................................29

B) Outlining causes for preparing bank statements..............................................................29

C) Cash books.......................................................................................................................30

M3 Reconciliation process...................................................................................................31

D3 BRS.................................................................................................................................31

CLIENT 5......................................................................................................................................31

A) Sales and purchase ledger...............................................................................................31

B) Control account...............................................................................................................31

CLIENT 6......................................................................................................................................32

A) Suspense account and explaining features......................................................................32

B) Trial balance....................................................................................................................32

C) Journal entries..................................................................................................................32

D) Distinguishing between clearing and suspense account..................................................33

M4 Various accounts and reconciliation..............................................................................33

D4 Outlining accounting methods for the organisation.......................................................33

CONCLUSION..............................................................................................................................33

REFERENCES..............................................................................................................................34

B) Outlining causes for preparing bank statements..............................................................29

C) Cash books.......................................................................................................................30

M3 Reconciliation process...................................................................................................31

D3 BRS.................................................................................................................................31

CLIENT 5......................................................................................................................................31

A) Sales and purchase ledger...............................................................................................31

B) Control account...............................................................................................................31

CLIENT 6......................................................................................................................................32

A) Suspense account and explaining features......................................................................32

B) Trial balance....................................................................................................................32

C) Journal entries..................................................................................................................32

D) Distinguishing between clearing and suspense account..................................................33

M4 Various accounts and reconciliation..............................................................................33

D4 Outlining accounting methods for the organisation.......................................................33

CONCLUSION..............................................................................................................................33

REFERENCES..............................................................................................................................34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is quite important in the business as it helps to record every

transaction which occurs in the organisation. This is required so that final accounts can be

prepared with much ease. Present report deals with various companies which requires following

accounting regulations and concepts in the best possible manner. Moreover, various accounting

concepts and relevant terms are discussed in this report. Financials of the company such as

balance sheet, cash flow statement and income statements are prepared for assessing overall

financial performance of organisations in effective way.

A) Preparation of report for Line Manager

To: Line Manager of Firm

From: Junior Accountant

Subject: Accounting terms and regulations useful for the company

Respected Sir,

Accounting principles and regulations play crucial role in the company so that may be

able to prepare various financial statements in the best possible manner. This is quite important

so that effective financials may be prepared in consideration of various regulations implemented

by accounting bodies. In relation to this, financials of company are income statement and cash

flow statement and balance sheet which are three statements which provides clarity about the

financial health of organisation quite easily. Accounting concepts are required to be followed by

the company so that error free and true financial statements may be prepared exhibiting real

financial position of the organisation.

Financial accounting

The term financial accounting is the major branch of accounting which deals with

recording, summarizing of business transactions held over particular time frame. This is quite

essential for the business so that it may be able to analyse various transactions. Once financial

transactions are recorded and summarized, final accounts can be easily prepared. The final

accounts are then provided to various stakeholders such as investors, creditors so that they may

be able to take effective and better decisions with much ease. Thus, financial accounting is

1

Financial accounting is quite important in the business as it helps to record every

transaction which occurs in the organisation. This is required so that final accounts can be

prepared with much ease. Present report deals with various companies which requires following

accounting regulations and concepts in the best possible manner. Moreover, various accounting

concepts and relevant terms are discussed in this report. Financials of the company such as

balance sheet, cash flow statement and income statements are prepared for assessing overall

financial performance of organisations in effective way.

A) Preparation of report for Line Manager

To: Line Manager of Firm

From: Junior Accountant

Subject: Accounting terms and regulations useful for the company

Respected Sir,

Accounting principles and regulations play crucial role in the company so that may be

able to prepare various financial statements in the best possible manner. This is quite important

so that effective financials may be prepared in consideration of various regulations implemented

by accounting bodies. In relation to this, financials of company are income statement and cash

flow statement and balance sheet which are three statements which provides clarity about the

financial health of organisation quite easily. Accounting concepts are required to be followed by

the company so that error free and true financial statements may be prepared exhibiting real

financial position of the organisation.

Financial accounting

The term financial accounting is the major branch of accounting which deals with

recording, summarizing of business transactions held over particular time frame. This is quite

essential for the business so that it may be able to analyse various transactions. Once financial

transactions are recorded and summarized, final accounts can be easily prepared. The final

accounts are then provided to various stakeholders such as investors, creditors so that they may

be able to take effective and better decisions with much ease. Thus, financial accounting is

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

required in the organisation and should be adhered to accounting concepts and policies

governed by professional bodies. Moreover, when financials of the company are prepared then,

it is available for various stakeholders to take effective and better decisions whether to provide

funds to organisation or not.

Financial accounting regulations

Accounting regulations are required to be abide by the company so that accurate

financial statements can be prepared having transparency in the best possible way. This is

required to be followed by accountant so that he may formulate financials of the company in

effectual way and that too error and mistake free. In relation to this, UK's corporate governance

professional body such as FRC (Financial Reporting Council) has provided legal framework to

be followed by the company while preparing financial statements of the organisation in the best

possible way. These legal frameworks help accountants to prepare financials in quite effective

manner.

Legal frameworks

FRC : It is a professional body limited by guarantee and regulates entire organisations of UK so

that financials may be prepared in the best possible way. Moreover, government departments

are also regulated by it (Financial Reporting Council, 2017). The main objective of FRC is to

adequately foster investment in UK and as such, benefiting whole economy in effective way.

IASB : It is abbreviated as IASB (International Accounting Standards Board) which regulates

organisations so that adequate financial statements may be prepared. It provides guidelines

which help accountants to prepare financials so that true and fair view may be extracted out of

the statements in the best possible manner.

IFRS :It is abbreviated as IFRS (International Financial Reporting Standards) which is another

accounting body facilitating accountants to prepare fair financial statements exhibiting true

financial health of the company.

Principles of accounting

Principles of accounting are provided by GAAP (Generally Accepted Accounting

Principles) which are as follows-

2

governed by professional bodies. Moreover, when financials of the company are prepared then,

it is available for various stakeholders to take effective and better decisions whether to provide

funds to organisation or not.

Financial accounting regulations

Accounting regulations are required to be abide by the company so that accurate

financial statements can be prepared having transparency in the best possible way. This is

required to be followed by accountant so that he may formulate financials of the company in

effectual way and that too error and mistake free. In relation to this, UK's corporate governance

professional body such as FRC (Financial Reporting Council) has provided legal framework to

be followed by the company while preparing financial statements of the organisation in the best

possible way. These legal frameworks help accountants to prepare financials in quite effective

manner.

Legal frameworks

FRC : It is a professional body limited by guarantee and regulates entire organisations of UK so

that financials may be prepared in the best possible way. Moreover, government departments

are also regulated by it (Financial Reporting Council, 2017). The main objective of FRC is to

adequately foster investment in UK and as such, benefiting whole economy in effective way.

IASB : It is abbreviated as IASB (International Accounting Standards Board) which regulates

organisations so that adequate financial statements may be prepared. It provides guidelines

which help accountants to prepare financials so that true and fair view may be extracted out of

the statements in the best possible manner.

IFRS :It is abbreviated as IFRS (International Financial Reporting Standards) which is another

accounting body facilitating accountants to prepare fair financial statements exhibiting true

financial health of the company.

Principles of accounting

Principles of accounting are provided by GAAP (Generally Accepted Accounting

Principles) which are as follows-

2

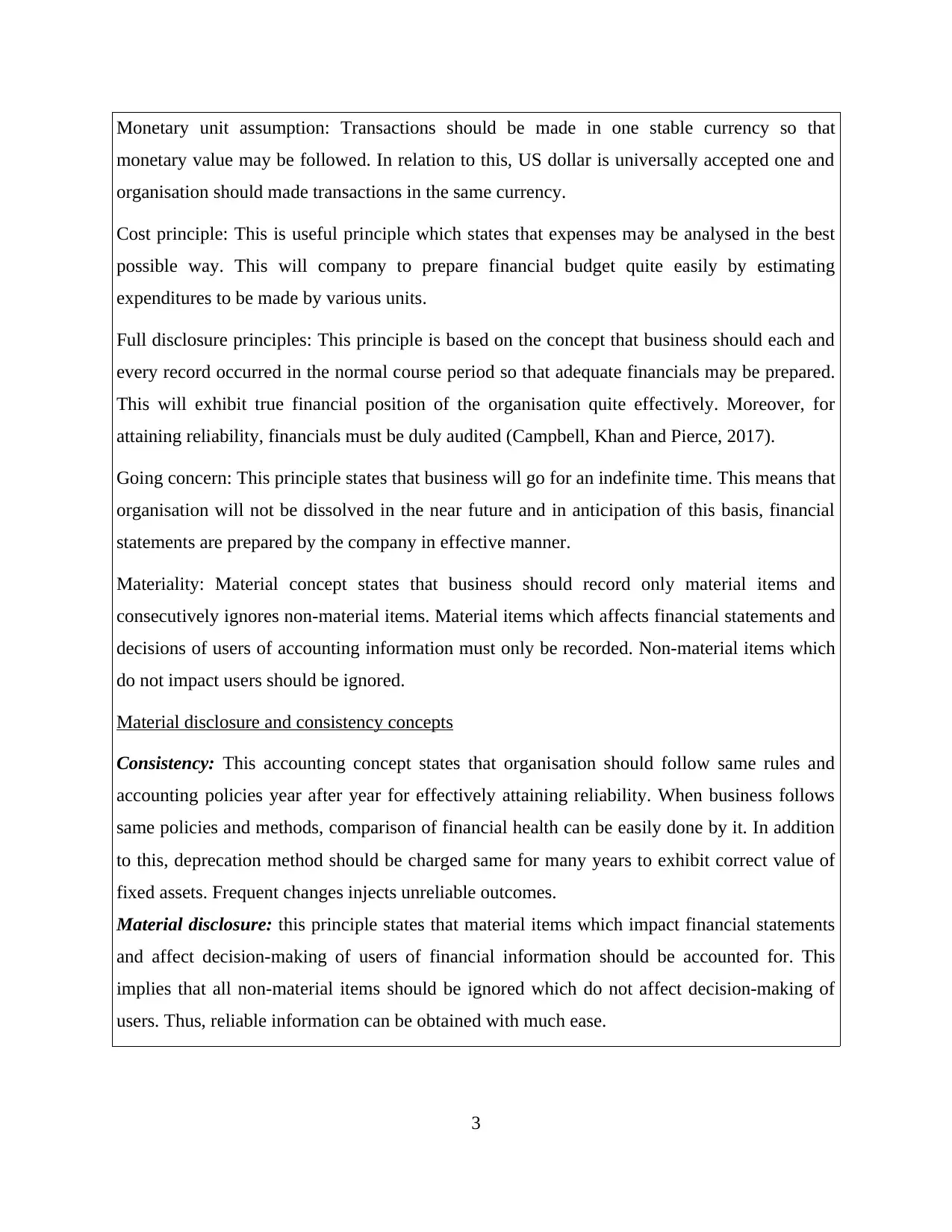

Monetary unit assumption: Transactions should be made in one stable currency so that

monetary value may be followed. In relation to this, US dollar is universally accepted one and

organisation should made transactions in the same currency.

Cost principle: This is useful principle which states that expenses may be analysed in the best

possible way. This will company to prepare financial budget quite easily by estimating

expenditures to be made by various units.

Full disclosure principles: This principle is based on the concept that business should each and

every record occurred in the normal course period so that adequate financials may be prepared.

This will exhibit true financial position of the organisation quite effectively. Moreover, for

attaining reliability, financials must be duly audited (Campbell, Khan and Pierce, 2017).

Going concern: This principle states that business will go for an indefinite time. This means that

organisation will not be dissolved in the near future and in anticipation of this basis, financial

statements are prepared by the company in effective manner.

Materiality: Material concept states that business should record only material items and

consecutively ignores non-material items. Material items which affects financial statements and

decisions of users of accounting information must only be recorded. Non-material items which

do not impact users should be ignored.

Material disclosure and consistency concepts

Consistency: This accounting concept states that organisation should follow same rules and

accounting policies year after year for effectively attaining reliability. When business follows

same policies and methods, comparison of financial health can be easily done by it. In addition

to this, deprecation method should be charged same for many years to exhibit correct value of

fixed assets. Frequent changes injects unreliable outcomes.

Material disclosure: this principle states that material items which impact financial statements

and affect decision-making of users of financial information should be accounted for. This

implies that all non-material items should be ignored which do not affect decision-making of

users. Thus, reliable information can be obtained with much ease.

3

monetary value may be followed. In relation to this, US dollar is universally accepted one and

organisation should made transactions in the same currency.

Cost principle: This is useful principle which states that expenses may be analysed in the best

possible way. This will company to prepare financial budget quite easily by estimating

expenditures to be made by various units.

Full disclosure principles: This principle is based on the concept that business should each and

every record occurred in the normal course period so that adequate financials may be prepared.

This will exhibit true financial position of the organisation quite effectively. Moreover, for

attaining reliability, financials must be duly audited (Campbell, Khan and Pierce, 2017).

Going concern: This principle states that business will go for an indefinite time. This means that

organisation will not be dissolved in the near future and in anticipation of this basis, financial

statements are prepared by the company in effective manner.

Materiality: Material concept states that business should record only material items and

consecutively ignores non-material items. Material items which affects financial statements and

decisions of users of accounting information must only be recorded. Non-material items which

do not impact users should be ignored.

Material disclosure and consistency concepts

Consistency: This accounting concept states that organisation should follow same rules and

accounting policies year after year for effectively attaining reliability. When business follows

same policies and methods, comparison of financial health can be easily done by it. In addition

to this, deprecation method should be charged same for many years to exhibit correct value of

fixed assets. Frequent changes injects unreliable outcomes.

Material disclosure: this principle states that material items which impact financial statements

and affect decision-making of users of financial information should be accounted for. This

implies that all non-material items should be ignored which do not affect decision-making of

users. Thus, reliable information can be obtained with much ease.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

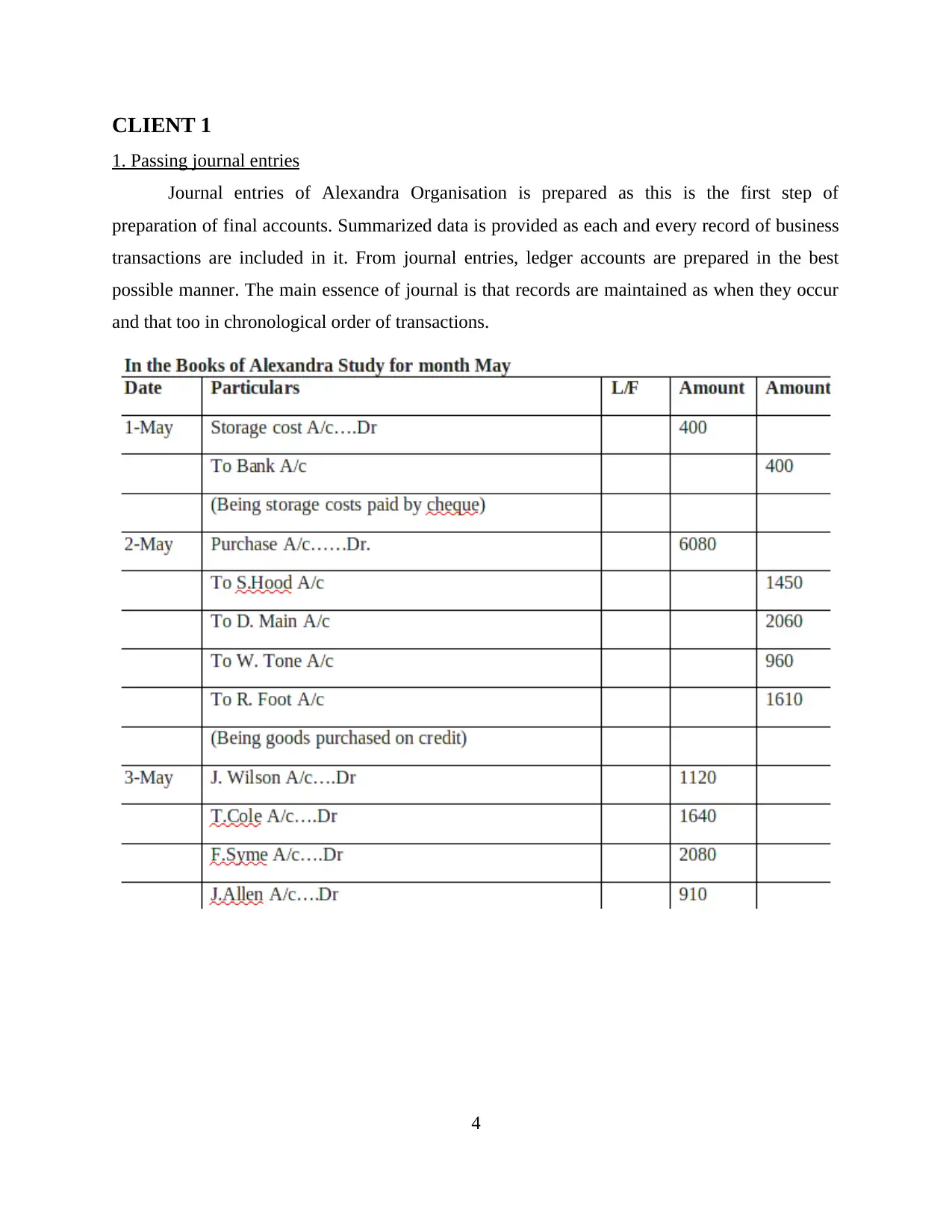

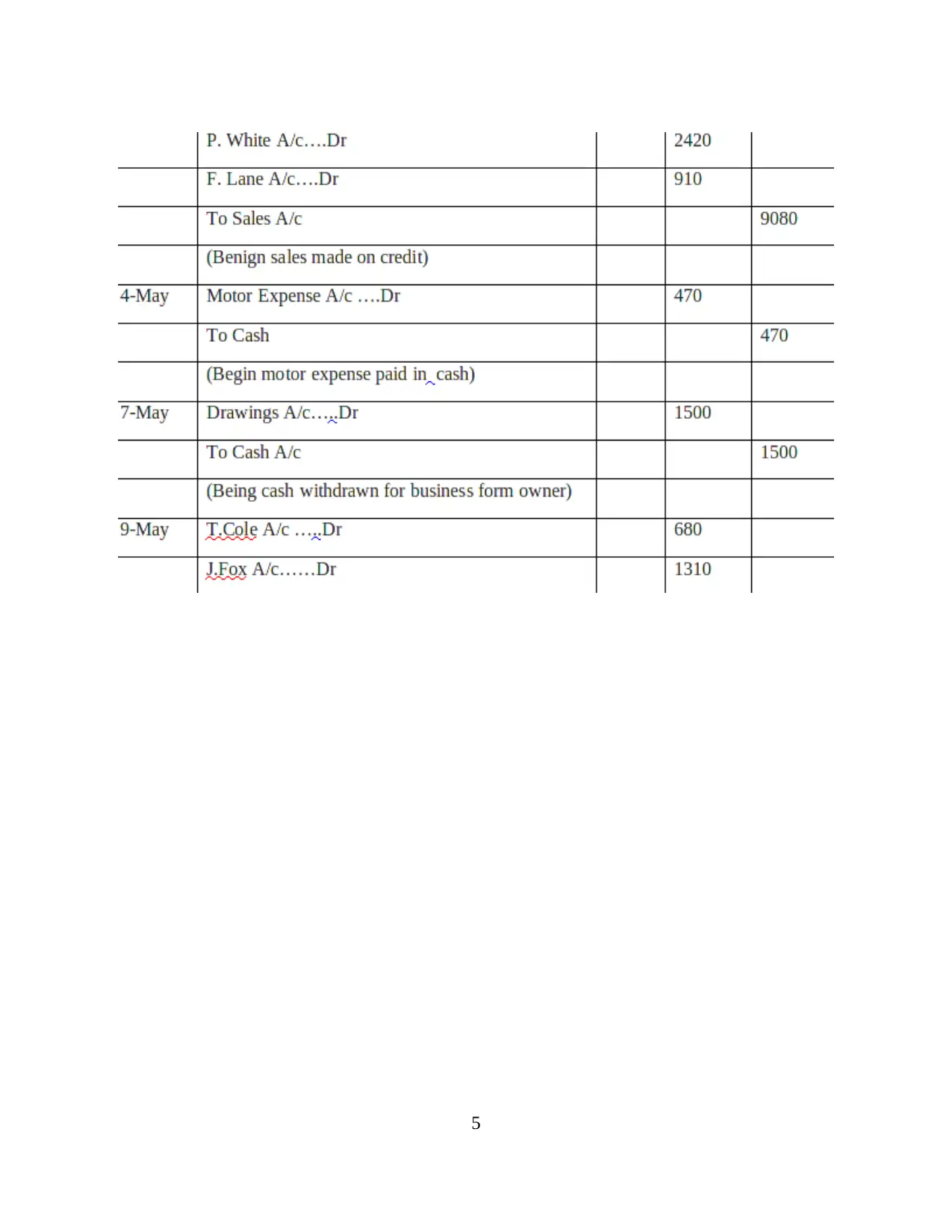

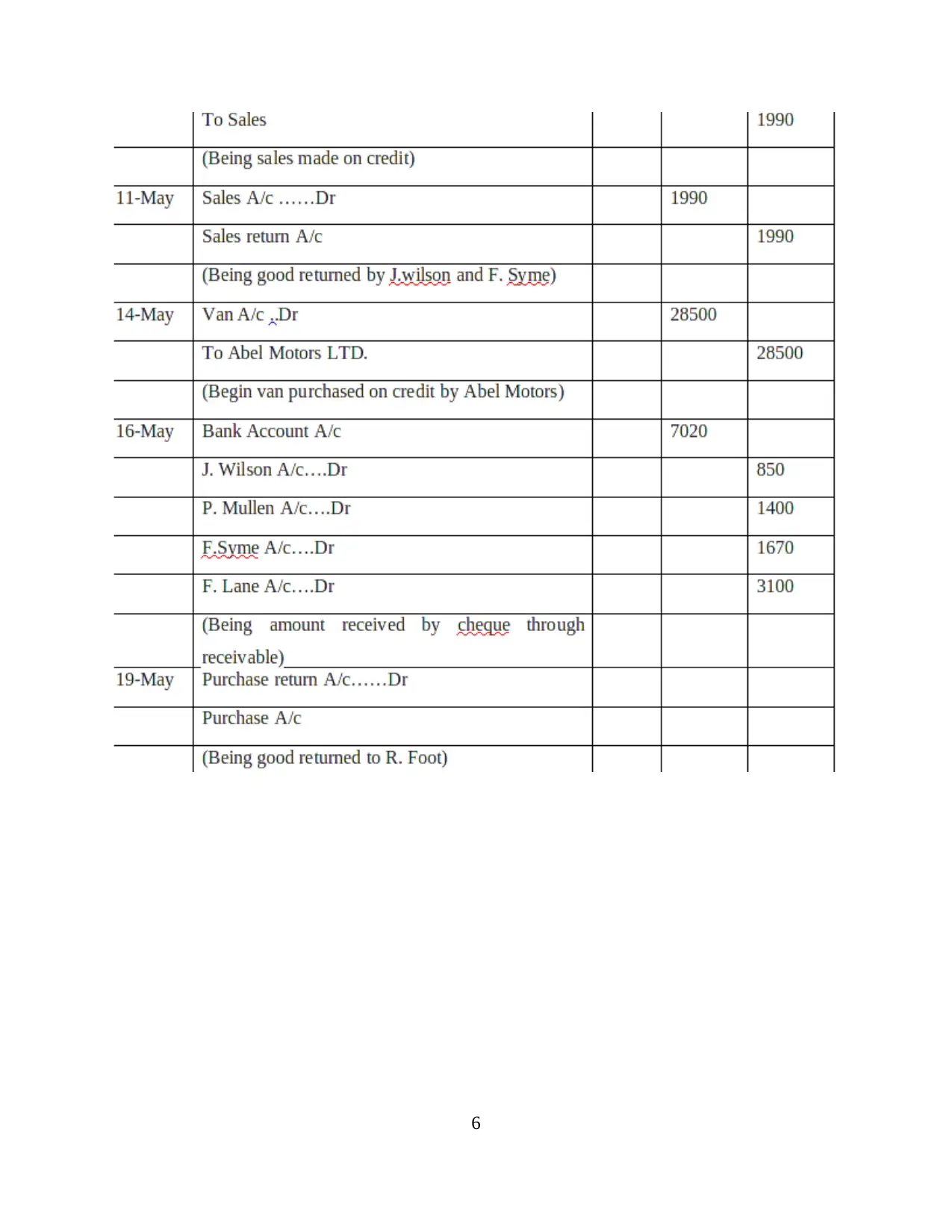

CLIENT 1

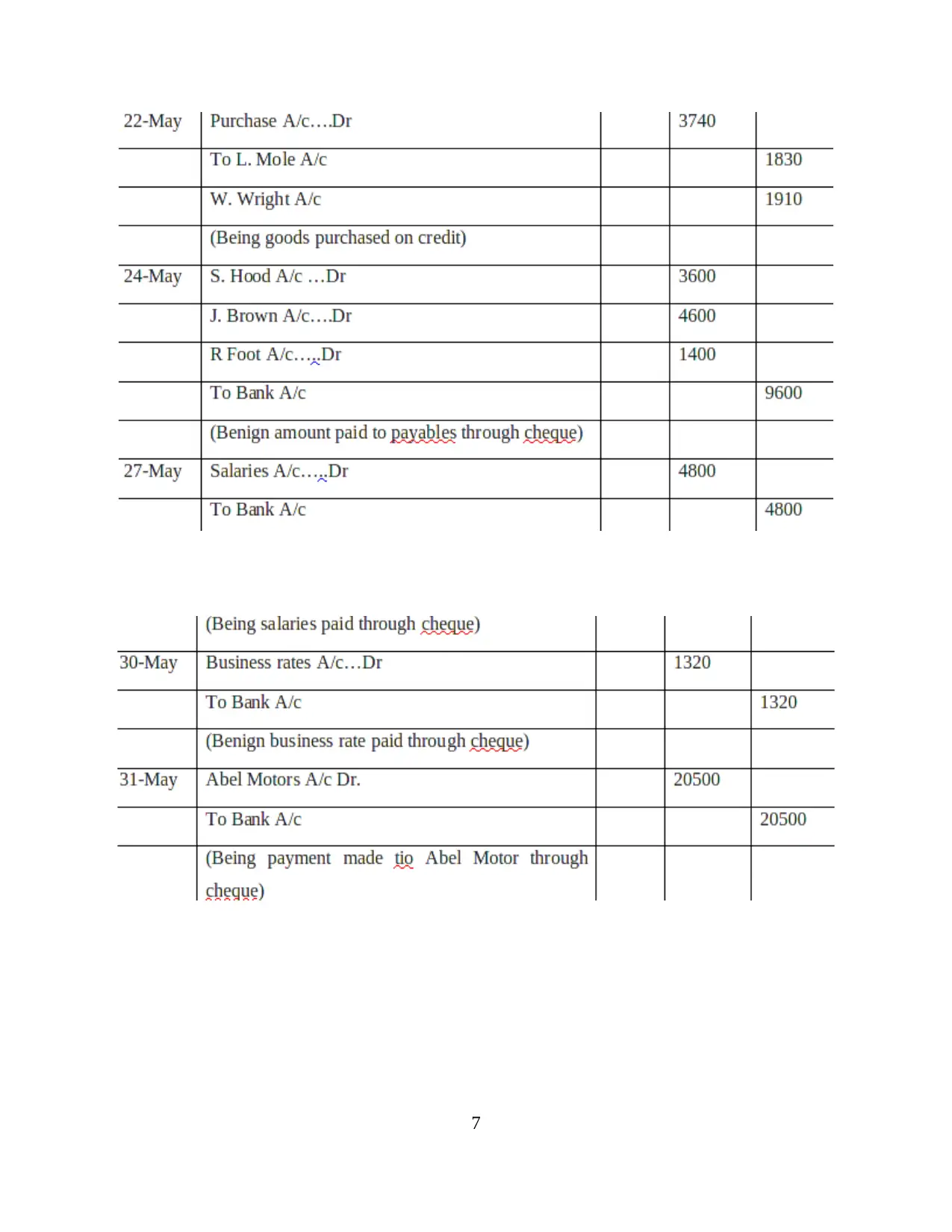

1. Passing journal entries

Journal entries of Alexandra Organisation is prepared as this is the first step of

preparation of final accounts. Summarized data is provided as each and every record of business

transactions are included in it. From journal entries, ledger accounts are prepared in the best

possible manner. The main essence of journal is that records are maintained as when they occur

and that too in chronological order of transactions.

4

1. Passing journal entries

Journal entries of Alexandra Organisation is prepared as this is the first step of

preparation of final accounts. Summarized data is provided as each and every record of business

transactions are included in it. From journal entries, ledger accounts are prepared in the best

possible manner. The main essence of journal is that records are maintained as when they occur

and that too in chronological order of transactions.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

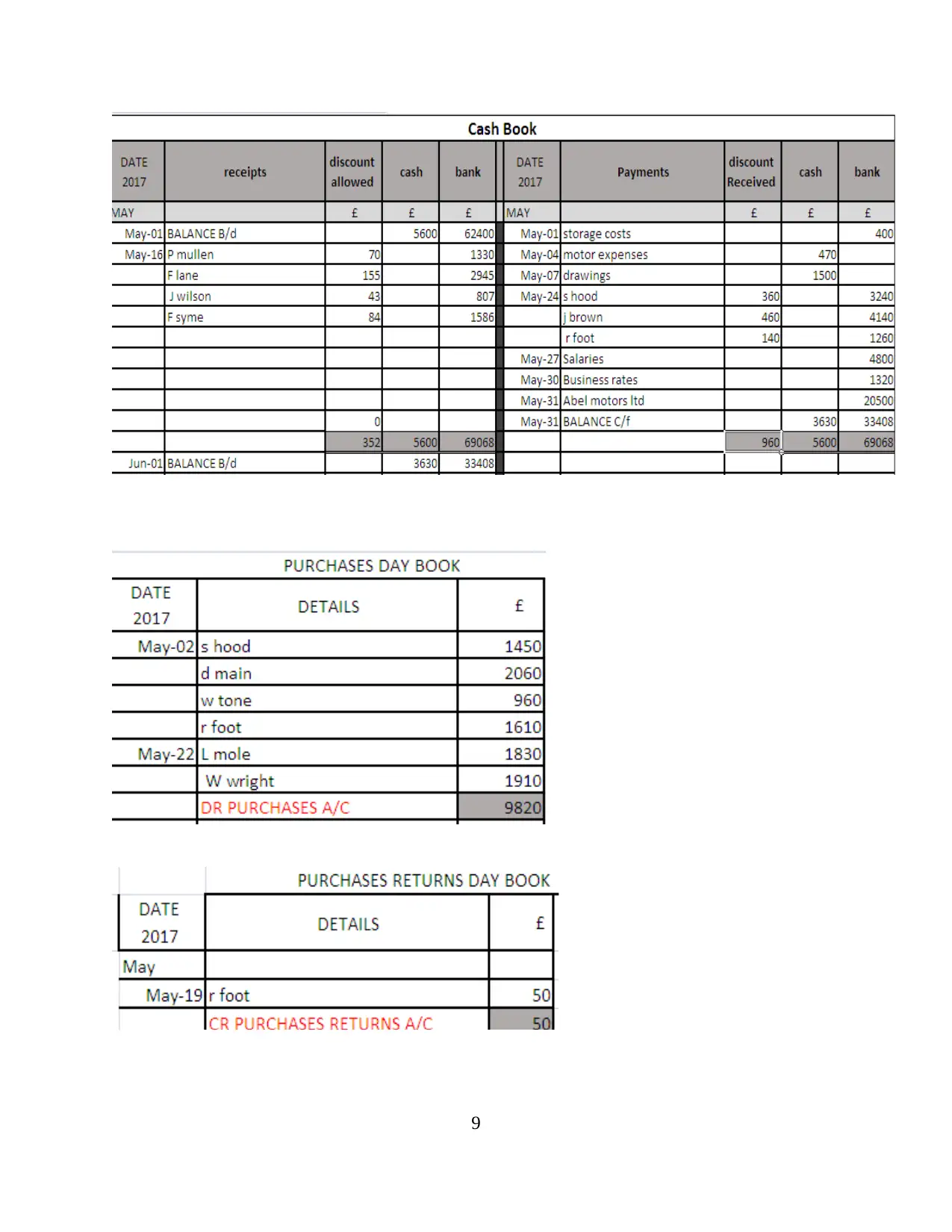

2. Preparation of ledger accounts

Ledger accounts are further bifurcation of the entries passed in journal. This means that

individual accounts are maintained by the business. This provides clarity to organisation

regarding various costs and income earned as every transaction is evaluated in it. This help

management to analyse expenditures and as such, control can be easily initiated on the same.

8

Ledger accounts are further bifurcation of the entries passed in journal. This means that

individual accounts are maintained by the business. This provides clarity to organisation

regarding various costs and income earned as every transaction is evaluated in it. This help

management to analyse expenditures and as such, control can be easily initiated on the same.

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 37

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.