FNSACC301 & BSBFIA401: Financial Accounting Portfolio, Term 2, 2018

VerifiedAdded on 2023/06/11

|48

|8266

|258

Portfolio

AI Summary

This portfolio assessment for the FNSACC301 (Process Financial Transactions and Extract Interim Reports) and BSBFIA401 (Prepare Financial Reports) units of competency includes a range of activities designed to assess the student's understanding and application of financial accounting principles. The assessment covers verifying supporting documentation, processing banking and petty cash documents, preparing invoices, posting journals to ledgers, entering data into systems, managing deposit facilities, extracting trial balances and interim reports, maintaining asset registers, recording general journal entries for balance day adjustments, and preparing final general ledger accounts and end-of-period financial reports. The assessment includes questions and tasks related to source documents, tax invoices, computerized accounting systems, internal controls, and compliance with accounting standards and regulations. The student's performance is evaluated based on competence in each element, with feedback provided to identify areas for improvement.

T-1.8.1

Details of Assessment

Term and Year 2, 2018 Time allowed Week 1, 2, 3, 4, 6, 7

Assessment No 1 Assessment Weighting 35%

Assessment Type Portfolio of Activities

Due Date Week No. 8 Room 609

Details of Subject

Qualification FNS40615 Certificate IV in Accounting

Subject Name Financial Accounting

Details of Unit(s) of competency

Unit Code (s) and

Names

FNSACC301 Process financial transactions and extract interim reports

BSBFIA401 Prepare financial reports

Details of Student

Student Name

College Student ID

Student Declaration: I declare that the work

submitted is my own, and has not been copied or

plagiarised from any person or source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Kaneez Selim

Assessment Outcome

Results Competent Not yet competent Marks / 35

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

________________________________________________________________________________________________

________________________________________________________________________________________________

________________________________________________________________________________________________

________________________________________________________

Student Declaration: I declare that I have been assessed

in this unit, and I have been advised of my result. I also

am aware of my appeal rights and reassessment

procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this

student, and I have provided appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/___ / 2018

Purpose of the Assessment FNSACC301

Financial Transactions & Interim Reports, Assessment No. 1 Page 1

v2.0, Last updated on 06/07/2015

Details of Assessment

Term and Year 2, 2018 Time allowed Week 1, 2, 3, 4, 6, 7

Assessment No 1 Assessment Weighting 35%

Assessment Type Portfolio of Activities

Due Date Week No. 8 Room 609

Details of Subject

Qualification FNS40615 Certificate IV in Accounting

Subject Name Financial Accounting

Details of Unit(s) of competency

Unit Code (s) and

Names

FNSACC301 Process financial transactions and extract interim reports

BSBFIA401 Prepare financial reports

Details of Student

Student Name

College Student ID

Student Declaration: I declare that the work

submitted is my own, and has not been copied or

plagiarised from any person or source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Kaneez Selim

Assessment Outcome

Results Competent Not yet competent Marks / 35

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

________________________________________________________________________________________________

________________________________________________________________________________________________

________________________________________________________________________________________________

________________________________________________________

Student Declaration: I declare that I have been assessed

in this unit, and I have been advised of my result. I also

am aware of my appeal rights and reassessment

procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this

student, and I have provided appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/___ / 2018

Purpose of the Assessment FNSACC301

Financial Transactions & Interim Reports, Assessment No. 1 Page 1

v2.0, Last updated on 06/07/2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

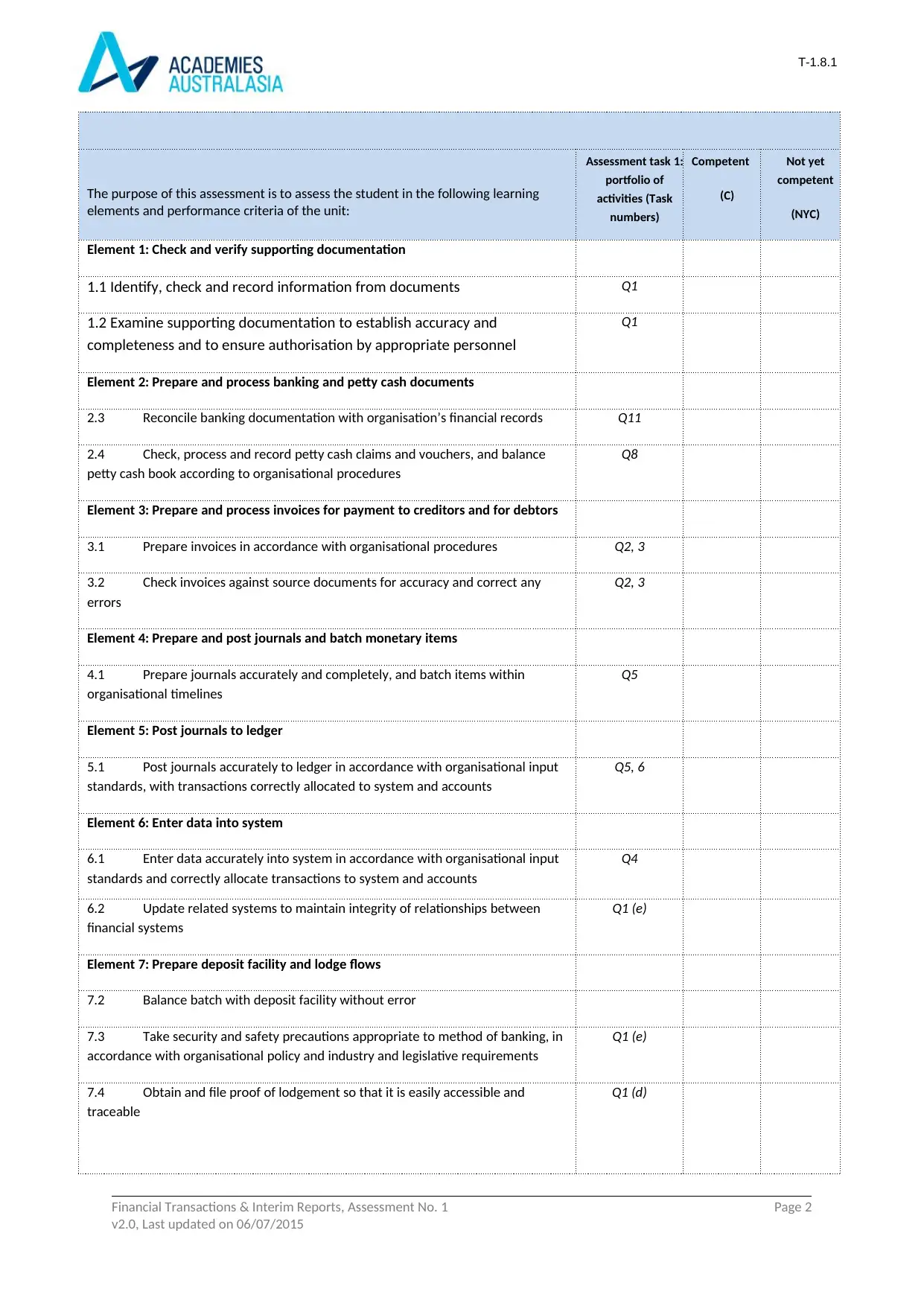

The purpose of this assessment is to assess the student in the following learning

elements and performance criteria of the unit:

Assessment task 1:

portfolio of

activities (Task

numbers)

Competent

(C)

Not yet

competent

(NYC)

Element 1: Check and verify supporting documentation

1.1 Identify, check and record information from documents Q1

1.2 Examine supporting documentation to establish accuracy and

completeness and to ensure authorisation by appropriate personnel

Q1

Element 2: Prepare and process banking and petty cash documents

2.3 Reconcile banking documentation with organisation’s financial records Q11

2.4 Check, process and record petty cash claims and vouchers, and balance

petty cash book according to organisational procedures

Q8

Element 3: Prepare and process invoices for payment to creditors and for debtors

3.1 Prepare invoices in accordance with organisational procedures Q2, 3

3.2 Check invoices against source documents for accuracy and correct any

errors

Q2, 3

Element 4: Prepare and post journals and batch monetary items

4.1 Prepare journals accurately and completely, and batch items within

organisational timelines

Q5

Element 5: Post journals to ledger

5.1 Post journals accurately to ledger in accordance with organisational input

standards, with transactions correctly allocated to system and accounts

Q5, 6

Element 6: Enter data into system

6.1 Enter data accurately into system in accordance with organisational input

standards and correctly allocate transactions to system and accounts

Q4

6.2 Update related systems to maintain integrity of relationships between

financial systems

Q1 (e)

Element 7: Prepare deposit facility and lodge flows

7.2 Balance batch with deposit facility without error

7.3 Take security and safety precautions appropriate to method of banking, in

accordance with organisational policy and industry and legislative requirements

Q1 (e)

7.4 Obtain and file proof of lodgement so that it is easily accessible and

traceable

Q1 (d)

Financial Transactions & Interim Reports, Assessment No. 1 Page 2

v2.0, Last updated on 06/07/2015

The purpose of this assessment is to assess the student in the following learning

elements and performance criteria of the unit:

Assessment task 1:

portfolio of

activities (Task

numbers)

Competent

(C)

Not yet

competent

(NYC)

Element 1: Check and verify supporting documentation

1.1 Identify, check and record information from documents Q1

1.2 Examine supporting documentation to establish accuracy and

completeness and to ensure authorisation by appropriate personnel

Q1

Element 2: Prepare and process banking and petty cash documents

2.3 Reconcile banking documentation with organisation’s financial records Q11

2.4 Check, process and record petty cash claims and vouchers, and balance

petty cash book according to organisational procedures

Q8

Element 3: Prepare and process invoices for payment to creditors and for debtors

3.1 Prepare invoices in accordance with organisational procedures Q2, 3

3.2 Check invoices against source documents for accuracy and correct any

errors

Q2, 3

Element 4: Prepare and post journals and batch monetary items

4.1 Prepare journals accurately and completely, and batch items within

organisational timelines

Q5

Element 5: Post journals to ledger

5.1 Post journals accurately to ledger in accordance with organisational input

standards, with transactions correctly allocated to system and accounts

Q5, 6

Element 6: Enter data into system

6.1 Enter data accurately into system in accordance with organisational input

standards and correctly allocate transactions to system and accounts

Q4

6.2 Update related systems to maintain integrity of relationships between

financial systems

Q1 (e)

Element 7: Prepare deposit facility and lodge flows

7.2 Balance batch with deposit facility without error

7.3 Take security and safety precautions appropriate to method of banking, in

accordance with organisational policy and industry and legislative requirements

Q1 (e)

7.4 Obtain and file proof of lodgement so that it is easily accessible and

traceable

Q1 (d)

Financial Transactions & Interim Reports, Assessment No. 1 Page 2

v2.0, Last updated on 06/07/2015

T-1.8.1

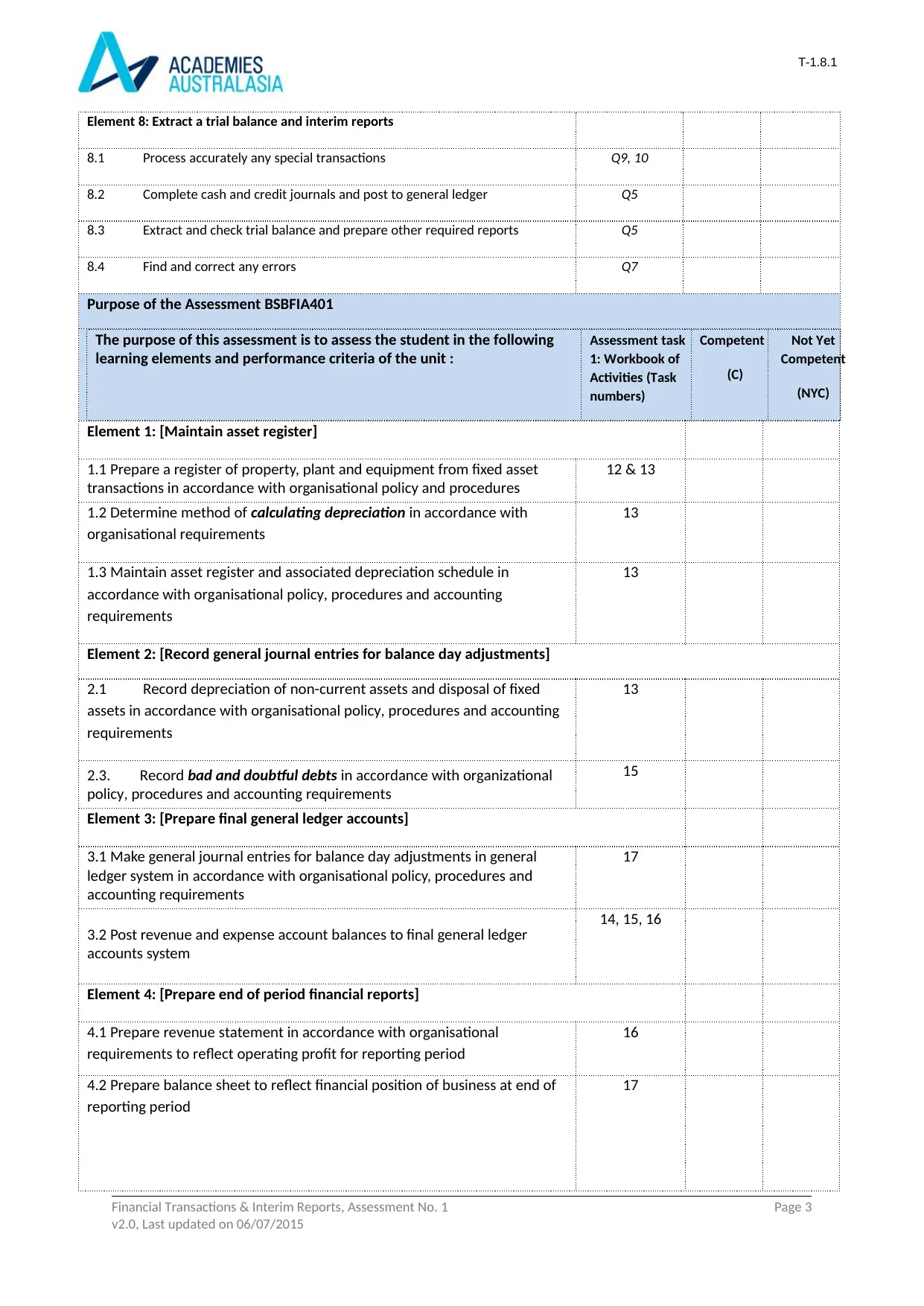

Element 8: Extract a trial balance and interim reports

8.1 Process accurately any special transactions Q9, 10

8.2 Complete cash and credit journals and post to general ledger Q5

8.3 Extract and check trial balance and prepare other required reports Q5

8.4 Find and correct any errors Q7

Purpose of the Assessment BSBFIA401

The purpose of this assessment is to assess the student in the following

learning elements and performance criteria of the unit :

Assessment task

1: Workbook of

Activities (Task

numbers)

Competent

(C)

Not Yet

Competent

(NYC)

Element 1: [Maintain asset register]

1.1 Prepare a register of property, plant and equipment from fixed asset

transactions in accordance with organisational policy and procedures

12 & 13

1.2 Determine method of calculating depreciation in accordance with

organisational requirements

13

1.3 Maintain asset register and associated depreciation schedule in

accordance with organisational policy, procedures and accounting

requirements

13

Element 2: [Record general journal entries for balance day adjustments]

2.1 Record depreciation of non-current assets and disposal of fixed

assets in accordance with organisational policy, procedures and accounting

requirements

13

2.3. Record bad and doubtful debts in accordance with organizational

policy, procedures and accounting requirements

15

Element 3: [Prepare final general ledger accounts]

3.1 Make general journal entries for balance day adjustments in general

ledger system in accordance with organisational policy, procedures and

accounting requirements

17

3.2 Post revenue and expense account balances to final general ledger

accounts system

14, 15, 16

Element 4: [Prepare end of period financial reports]

4.1 Prepare revenue statement in accordance with organisational

requirements to reflect operating profit for reporting period

16

4.2 Prepare balance sheet to reflect financial position of business at end of

reporting period

17

Financial Transactions & Interim Reports, Assessment No. 1 Page 3

v2.0, Last updated on 06/07/2015

Element 8: Extract a trial balance and interim reports

8.1 Process accurately any special transactions Q9, 10

8.2 Complete cash and credit journals and post to general ledger Q5

8.3 Extract and check trial balance and prepare other required reports Q5

8.4 Find and correct any errors Q7

Purpose of the Assessment BSBFIA401

The purpose of this assessment is to assess the student in the following

learning elements and performance criteria of the unit :

Assessment task

1: Workbook of

Activities (Task

numbers)

Competent

(C)

Not Yet

Competent

(NYC)

Element 1: [Maintain asset register]

1.1 Prepare a register of property, plant and equipment from fixed asset

transactions in accordance with organisational policy and procedures

12 & 13

1.2 Determine method of calculating depreciation in accordance with

organisational requirements

13

1.3 Maintain asset register and associated depreciation schedule in

accordance with organisational policy, procedures and accounting

requirements

13

Element 2: [Record general journal entries for balance day adjustments]

2.1 Record depreciation of non-current assets and disposal of fixed

assets in accordance with organisational policy, procedures and accounting

requirements

13

2.3. Record bad and doubtful debts in accordance with organizational

policy, procedures and accounting requirements

15

Element 3: [Prepare final general ledger accounts]

3.1 Make general journal entries for balance day adjustments in general

ledger system in accordance with organisational policy, procedures and

accounting requirements

17

3.2 Post revenue and expense account balances to final general ledger

accounts system

14, 15, 16

Element 4: [Prepare end of period financial reports]

4.1 Prepare revenue statement in accordance with organisational

requirements to reflect operating profit for reporting period

16

4.2 Prepare balance sheet to reflect financial position of business at end of

reporting period

17

Financial Transactions & Interim Reports, Assessment No. 1 Page 3

v2.0, Last updated on 06/07/2015

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Satisfactory (NS). A student can only achieve

competence when all assessment components listed under Purpose of the assessment section are Satisfactory. Your

trainer will give you feedback after the completion of each assessment. A student who is assessed as NS (Not

Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

Upon completion, submit the assessment copy to your trainer along with assessment coversheet.

Refer to the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer, if needed

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will

be provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student handbook).

Financial Transactions & Interim Reports, Assessment No. 1 Page 4

v2.0, Last updated on 06/07/2015

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Satisfactory (NS). A student can only achieve

competence when all assessment components listed under Purpose of the assessment section are Satisfactory. Your

trainer will give you feedback after the completion of each assessment. A student who is assessed as NS (Not

Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

Upon completion, submit the assessment copy to your trainer along with assessment coversheet.

Refer to the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer, if needed

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will

be provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student handbook).

Financial Transactions & Interim Reports, Assessment No. 1 Page 4

v2.0, Last updated on 06/07/2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

Part A: Financial Transaction (50 Marks)

Week 1:

Question 1 (2 marks)

Answer the following questions in the given space:

a. Explain what source document is. Give some examples.

Source document is the basic document evidencing the transaction or the document on

the basis of which the transaction can be recorded in the books.

The examples of source document includes Invoices, bank statement, cheque, debit

notes, credit notes, etc.

b. List different procedures employees can follow when they go to the bank to deposit

money for their business to ensure security and safety while banking.

To ensure security and safety they should properly deposit the money to the bankers only

and not to anybody else.

They should take deposit receipt properly stamped and signed by the bankers and keep

them in safe custody.

They should cross check the details filled on deposit slip to ensure that the amount is going

to credit in the correct account.

c. When you are filing documents, what factors should be considered when deciding the

filing order?

While filling the documents, it should be ensured that the documents are complete,

properly authorised and in the correct sequences.

The complete set should be filed along with necessary documents. These documents

includes, journal voucher, invoice, supporting to the invoices, etc.

All these documents should be properly signed and stamped.

Financial Transactions & Interim Reports, Assessment No. 1 Page 5

v2.0, Last updated on 06/07/2015

Part A: Financial Transaction (50 Marks)

Week 1:

Question 1 (2 marks)

Answer the following questions in the given space:

a. Explain what source document is. Give some examples.

Source document is the basic document evidencing the transaction or the document on

the basis of which the transaction can be recorded in the books.

The examples of source document includes Invoices, bank statement, cheque, debit

notes, credit notes, etc.

b. List different procedures employees can follow when they go to the bank to deposit

money for their business to ensure security and safety while banking.

To ensure security and safety they should properly deposit the money to the bankers only

and not to anybody else.

They should take deposit receipt properly stamped and signed by the bankers and keep

them in safe custody.

They should cross check the details filled on deposit slip to ensure that the amount is going

to credit in the correct account.

c. When you are filing documents, what factors should be considered when deciding the

filing order?

While filling the documents, it should be ensured that the documents are complete,

properly authorised and in the correct sequences.

The complete set should be filed along with necessary documents. These documents

includes, journal voucher, invoice, supporting to the invoices, etc.

All these documents should be properly signed and stamped.

Financial Transactions & Interim Reports, Assessment No. 1 Page 5

v2.0, Last updated on 06/07/2015

T-1.8.1

d. How do you ensure that the clerical officer deposited the

money to the bank? What would be the possible proof of lodgements?

On deposit of the money to the bank, the clerical officer will stamp and sign the deposit slip

and return one portion of deposit slip to the depositor.

The possible proof of lodgements is the deposit slip.

e. Name the popular accounting software that are in use in Australia. How do you ensure

that the data is entered into the accounting software accurately? How do you ensure the

currency of the accounting software? Describe the key purposes of Accounting reporting.

The popular accounting software used in Australia is MYOB.

To ensure that the data entered in software is accurate the parking and posting system is

used.

Under this system, the transactions are parked by the one person and those transactions

are cross checked by the other person. It is done to ensure that the mistakes done by one

person is corrected by the other.

The currency is ensured by checking the currency factor in the system.

The key purpose of accounting reporting is to record the transactions,

To maintain accounting records and to prepare the financials at time.

To provide the management information system, and provide the requisite details to the

management on time.

f. Money transfer via internet is a popular practice these days. To ensure that there is no

fraudulent activity in place, authorising the transfer is a common practice. This authorisation

process also ensures sound internal control system of a business.

Explain an authorisation process that a business can follow to ensure that the internal

control system is working properly.

The money transfer through internet generally involves two stage process.

Firstly, the transfer details and the beneficiary details are added through the net banking

Then these details are reviewed and authorised by other person or authorised signatory.

This two stage process reduces the chances of error and hence increases the security and

safety of online transactions.

Financial Transactions & Interim Reports, Assessment No. 1 Page 6

v2.0, Last updated on 06/07/2015

d. How do you ensure that the clerical officer deposited the

money to the bank? What would be the possible proof of lodgements?

On deposit of the money to the bank, the clerical officer will stamp and sign the deposit slip

and return one portion of deposit slip to the depositor.

The possible proof of lodgements is the deposit slip.

e. Name the popular accounting software that are in use in Australia. How do you ensure

that the data is entered into the accounting software accurately? How do you ensure the

currency of the accounting software? Describe the key purposes of Accounting reporting.

The popular accounting software used in Australia is MYOB.

To ensure that the data entered in software is accurate the parking and posting system is

used.

Under this system, the transactions are parked by the one person and those transactions

are cross checked by the other person. It is done to ensure that the mistakes done by one

person is corrected by the other.

The currency is ensured by checking the currency factor in the system.

The key purpose of accounting reporting is to record the transactions,

To maintain accounting records and to prepare the financials at time.

To provide the management information system, and provide the requisite details to the

management on time.

f. Money transfer via internet is a popular practice these days. To ensure that there is no

fraudulent activity in place, authorising the transfer is a common practice. This authorisation

process also ensures sound internal control system of a business.

Explain an authorisation process that a business can follow to ensure that the internal

control system is working properly.

The money transfer through internet generally involves two stage process.

Firstly, the transfer details and the beneficiary details are added through the net banking

Then these details are reviewed and authorised by other person or authorised signatory.

This two stage process reduces the chances of error and hence increases the security and

safety of online transactions.

Financial Transactions & Interim Reports, Assessment No. 1 Page 6

v2.0, Last updated on 06/07/2015

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1

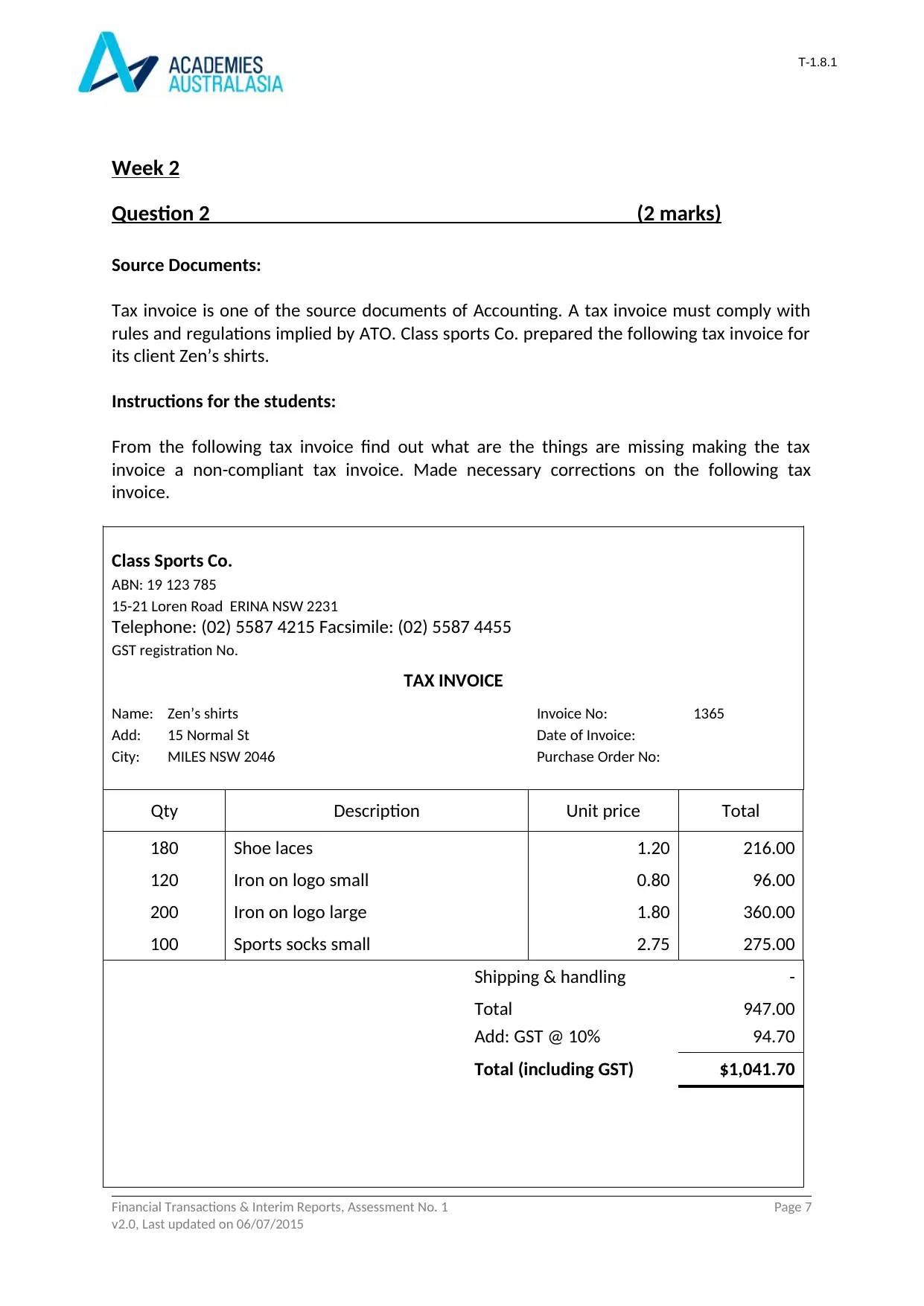

Week 2

Question 2 (2 marks)

Source Documents:

Tax invoice is one of the source documents of Accounting. A tax invoice must comply with

rules and regulations implied by ATO. Class sports Co. prepared the following tax invoice for

its client Zen’s shirts.

Instructions for the students:

From the following tax invoice find out what are the things are missing making the tax

invoice a non-compliant tax invoice. Made necessary corrections on the following tax

invoice.

Class Sports Co.

ABN: 19 123 785

15-21 Loren Road ERINA NSW 2231

Telephone: (02) 5587 4215 Facsimile: (02) 5587 4455

GST registration No.

TAX INVOICE

Name: Zen’s shirts

Add: 15 Normal St

City: MILES NSW 2046

Invoice No: 1365

Date of Invoice:

Purchase Order No:

Qty Description Unit price Total

180 Shoe laces 1.20 216.00

120 Iron on logo small 0.80 96.00

200 Iron on logo large 1.80 360.00

100 Sports socks small 2.75 275.00

Shipping & handling -

Total

Add: GST @ 10%

947.00

94.70

Total (including GST) $1,041.70

Financial Transactions & Interim Reports, Assessment No. 1 Page 7

v2.0, Last updated on 06/07/2015

Week 2

Question 2 (2 marks)

Source Documents:

Tax invoice is one of the source documents of Accounting. A tax invoice must comply with

rules and regulations implied by ATO. Class sports Co. prepared the following tax invoice for

its client Zen’s shirts.

Instructions for the students:

From the following tax invoice find out what are the things are missing making the tax

invoice a non-compliant tax invoice. Made necessary corrections on the following tax

invoice.

Class Sports Co.

ABN: 19 123 785

15-21 Loren Road ERINA NSW 2231

Telephone: (02) 5587 4215 Facsimile: (02) 5587 4455

GST registration No.

TAX INVOICE

Name: Zen’s shirts

Add: 15 Normal St

City: MILES NSW 2046

Invoice No: 1365

Date of Invoice:

Purchase Order No:

Qty Description Unit price Total

180 Shoe laces 1.20 216.00

120 Iron on logo small 0.80 96.00

200 Iron on logo large 1.80 360.00

100 Sports socks small 2.75 275.00

Shipping & handling -

Total

Add: GST @ 10%

947.00

94.70

Total (including GST) $1,041.70

Financial Transactions & Interim Reports, Assessment No. 1 Page 7

v2.0, Last updated on 06/07/2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

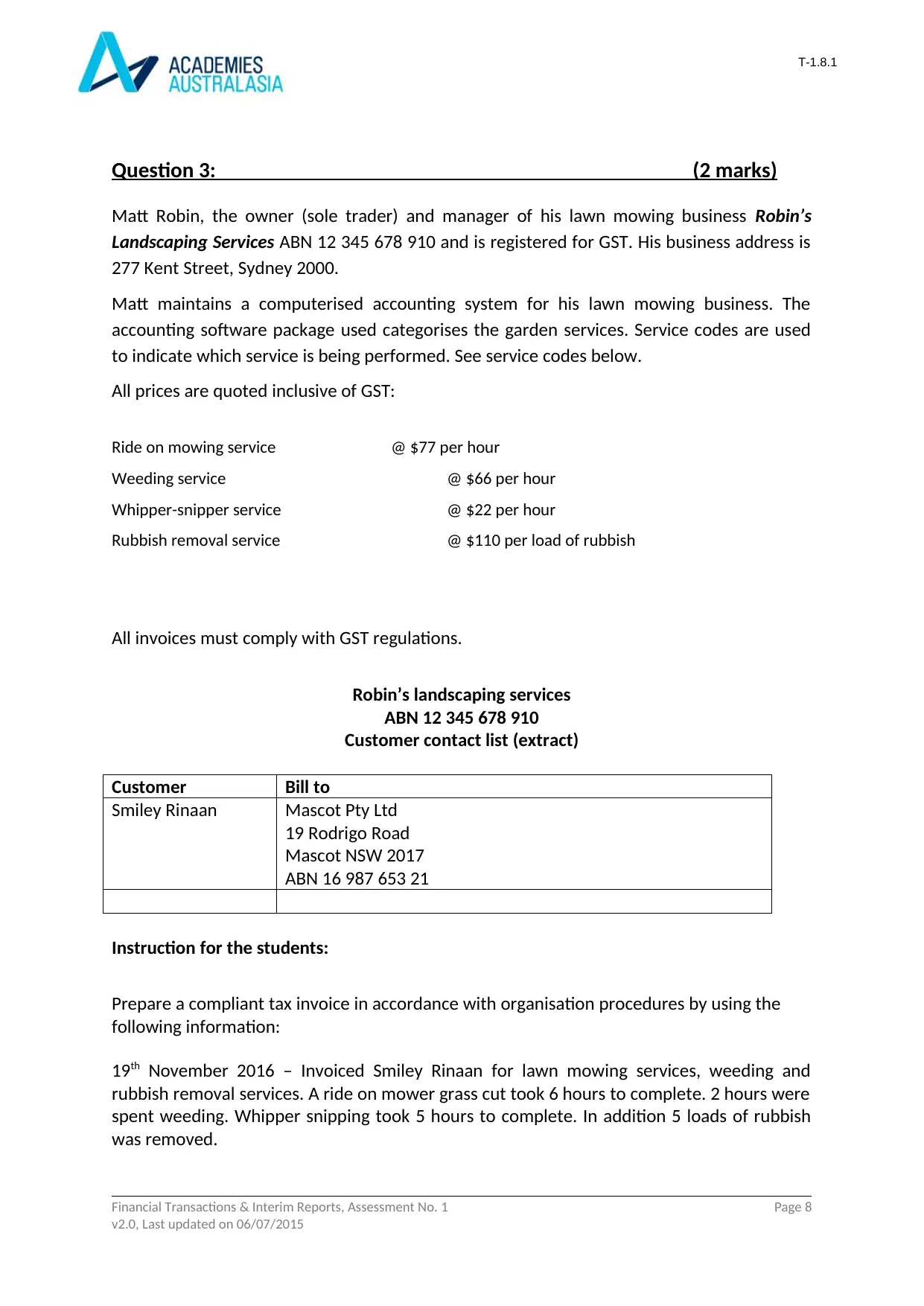

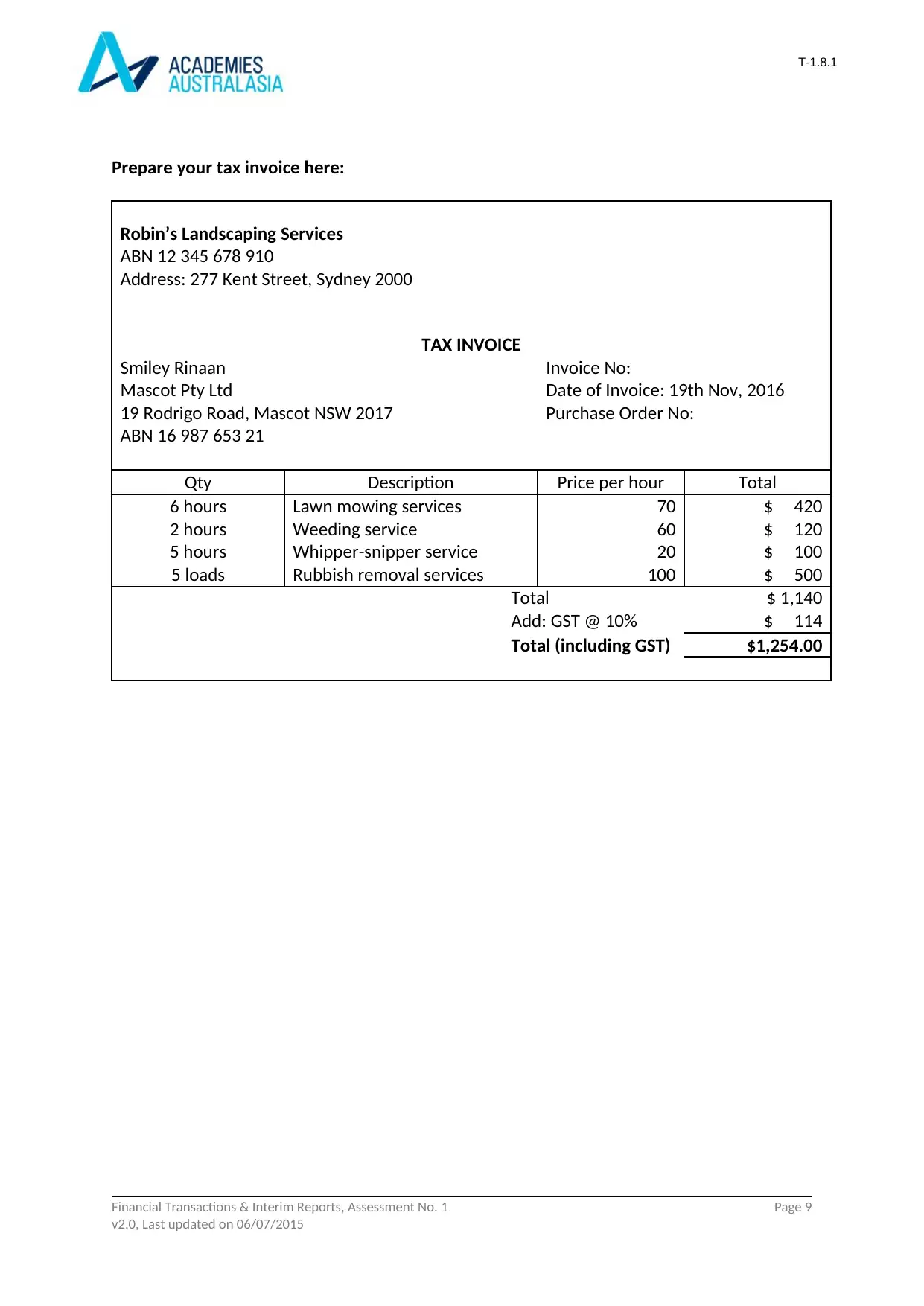

Question 3: (2 marks)

Matt Robin, the owner (sole trader) and manager of his lawn mowing business Robin’s

Landscaping Services ABN 12 345 678 910 and is registered for GST. His business address is

277 Kent Street, Sydney 2000.

Matt maintains a computerised accounting system for his lawn mowing business. The

accounting software package used categorises the garden services. Service codes are used

to indicate which service is being performed. See service codes below.

All prices are quoted inclusive of GST:

Ride on mowing service @ $77 per hour

Weeding service @ $66 per hour

Whipper-snipper service @ $22 per hour

Rubbish removal service @ $110 per load of rubbish

All invoices must comply with GST regulations.

Robin’s landscaping services

ABN 12 345 678 910

Customer contact list (extract)

Customer Bill to

Smiley Rinaan Mascot Pty Ltd

19 Rodrigo Road

Mascot NSW 2017

ABN 16 987 653 21

Instruction for the students:

Prepare a compliant tax invoice in accordance with organisation procedures by using the

following information:

19th November 2016 – Invoiced Smiley Rinaan for lawn mowing services, weeding and

rubbish removal services. A ride on mower grass cut took 6 hours to complete. 2 hours were

spent weeding. Whipper snipping took 5 hours to complete. In addition 5 loads of rubbish

was removed.

Financial Transactions & Interim Reports, Assessment No. 1 Page 8

v2.0, Last updated on 06/07/2015

Question 3: (2 marks)

Matt Robin, the owner (sole trader) and manager of his lawn mowing business Robin’s

Landscaping Services ABN 12 345 678 910 and is registered for GST. His business address is

277 Kent Street, Sydney 2000.

Matt maintains a computerised accounting system for his lawn mowing business. The

accounting software package used categorises the garden services. Service codes are used

to indicate which service is being performed. See service codes below.

All prices are quoted inclusive of GST:

Ride on mowing service @ $77 per hour

Weeding service @ $66 per hour

Whipper-snipper service @ $22 per hour

Rubbish removal service @ $110 per load of rubbish

All invoices must comply with GST regulations.

Robin’s landscaping services

ABN 12 345 678 910

Customer contact list (extract)

Customer Bill to

Smiley Rinaan Mascot Pty Ltd

19 Rodrigo Road

Mascot NSW 2017

ABN 16 987 653 21

Instruction for the students:

Prepare a compliant tax invoice in accordance with organisation procedures by using the

following information:

19th November 2016 – Invoiced Smiley Rinaan for lawn mowing services, weeding and

rubbish removal services. A ride on mower grass cut took 6 hours to complete. 2 hours were

spent weeding. Whipper snipping took 5 hours to complete. In addition 5 loads of rubbish

was removed.

Financial Transactions & Interim Reports, Assessment No. 1 Page 8

v2.0, Last updated on 06/07/2015

T-1.8.1

Prepare your tax invoice here:

Robin’s Landscaping Services

ABN 12 345 678 910

Address: 277 Kent Street, Sydney 2000

TAX INVOICE

Smiley Rinaan Invoice No:

Mascot Pty Ltd Date of Invoice: 19th Nov, 2016

19 Rodrigo Road, Mascot NSW 2017 Purchase Order No:

ABN 16 987 653 21

Qty Description Price per hour Total

6 hours Lawn mowing services 70 $ 420

2 hours Weeding service 60 $ 120

5 hours Whipper-snipper service 20 $ 100

5 loads Rubbish removal services 100 $ 500

Total $ 1,140

Add: GST @ 10% $ 114

Total (including GST) $1,254.00

Financial Transactions & Interim Reports, Assessment No. 1 Page 9

v2.0, Last updated on 06/07/2015

Prepare your tax invoice here:

Robin’s Landscaping Services

ABN 12 345 678 910

Address: 277 Kent Street, Sydney 2000

TAX INVOICE

Smiley Rinaan Invoice No:

Mascot Pty Ltd Date of Invoice: 19th Nov, 2016

19 Rodrigo Road, Mascot NSW 2017 Purchase Order No:

ABN 16 987 653 21

Qty Description Price per hour Total

6 hours Lawn mowing services 70 $ 420

2 hours Weeding service 60 $ 120

5 hours Whipper-snipper service 20 $ 100

5 loads Rubbish removal services 100 $ 500

Total $ 1,140

Add: GST @ 10% $ 114

Total (including GST) $1,254.00

Financial Transactions & Interim Reports, Assessment No. 1 Page 9

v2.0, Last updated on 06/07/2015

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1

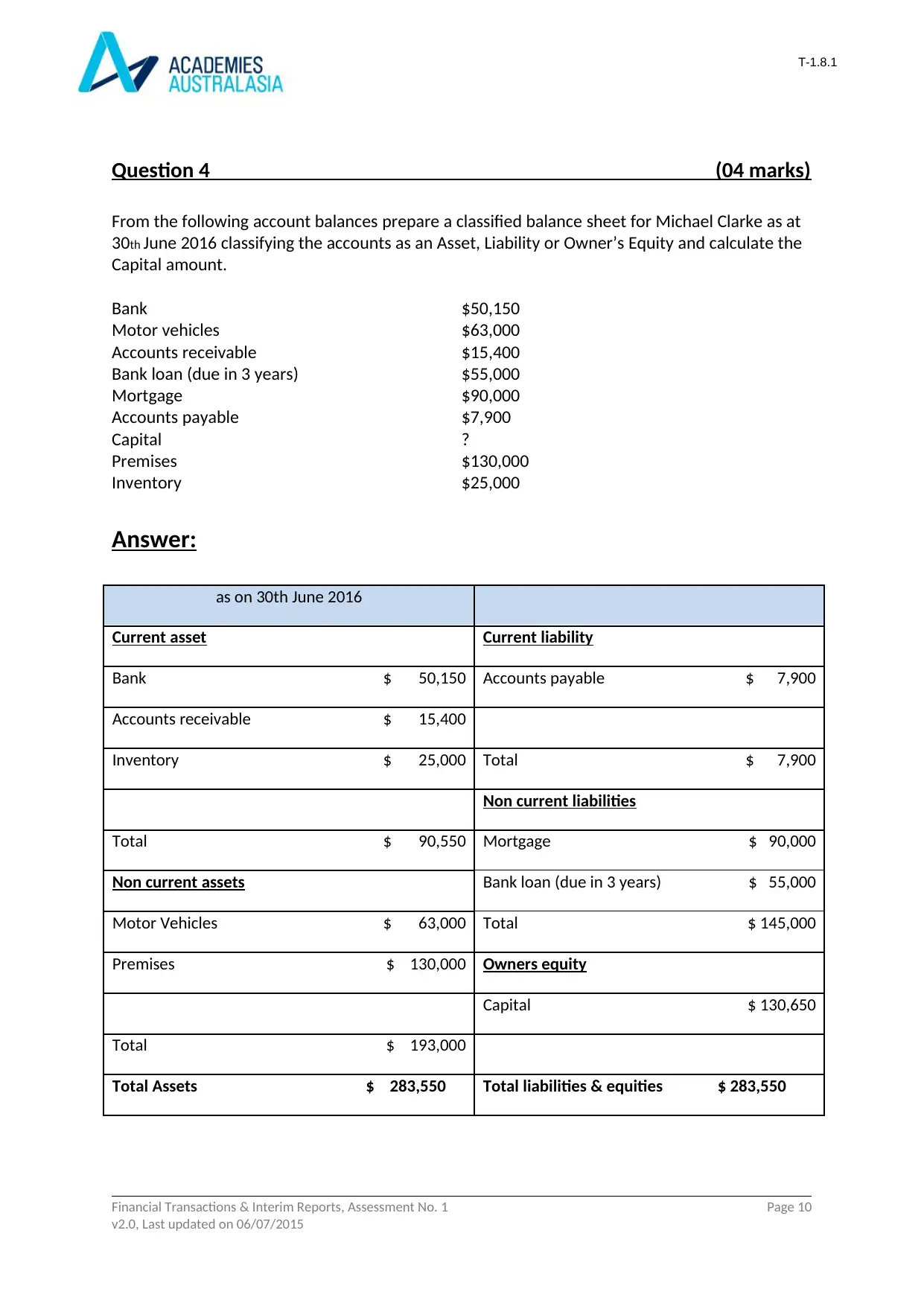

Question 4 (04 marks)

From the following account balances prepare a classified balance sheet for Michael Clarke as at

30th June 2016 classifying the accounts as an Asset, Liability or Owner’s Equity and calculate the

Capital amount.

Bank $50,150

Motor vehicles $63,000

Accounts receivable $15,400

Bank loan (due in 3 years) $55,000

Mortgage $90,000

Accounts payable $7,900

Capital ?

Premises $130,000

Inventory $25,000

Answer:

as on 30th June 2016

Current asset Current liability

Bank $ 50,150 Accounts payable $ 7,900

Accounts receivable $ 15,400

Inventory $ 25,000 Total $ 7,900

Non current liabilities

Total $ 90,550 Mortgage $ 90,000

Non current assets Bank loan (due in 3 years) $ 55,000

Motor Vehicles $ 63,000 Total $ 145,000

Premises $ 130,000 Owners equity

Capital $ 130,650

Total $ 193,000

Total Assets $ 283,550 Total liabilities & equities $ 283,550

Financial Transactions & Interim Reports, Assessment No. 1 Page 10

v2.0, Last updated on 06/07/2015

Question 4 (04 marks)

From the following account balances prepare a classified balance sheet for Michael Clarke as at

30th June 2016 classifying the accounts as an Asset, Liability or Owner’s Equity and calculate the

Capital amount.

Bank $50,150

Motor vehicles $63,000

Accounts receivable $15,400

Bank loan (due in 3 years) $55,000

Mortgage $90,000

Accounts payable $7,900

Capital ?

Premises $130,000

Inventory $25,000

Answer:

as on 30th June 2016

Current asset Current liability

Bank $ 50,150 Accounts payable $ 7,900

Accounts receivable $ 15,400

Inventory $ 25,000 Total $ 7,900

Non current liabilities

Total $ 90,550 Mortgage $ 90,000

Non current assets Bank loan (due in 3 years) $ 55,000

Motor Vehicles $ 63,000 Total $ 145,000

Premises $ 130,000 Owners equity

Capital $ 130,650

Total $ 193,000

Total Assets $ 283,550 Total liabilities & equities $ 283,550

Financial Transactions & Interim Reports, Assessment No. 1 Page 10

v2.0, Last updated on 06/07/2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

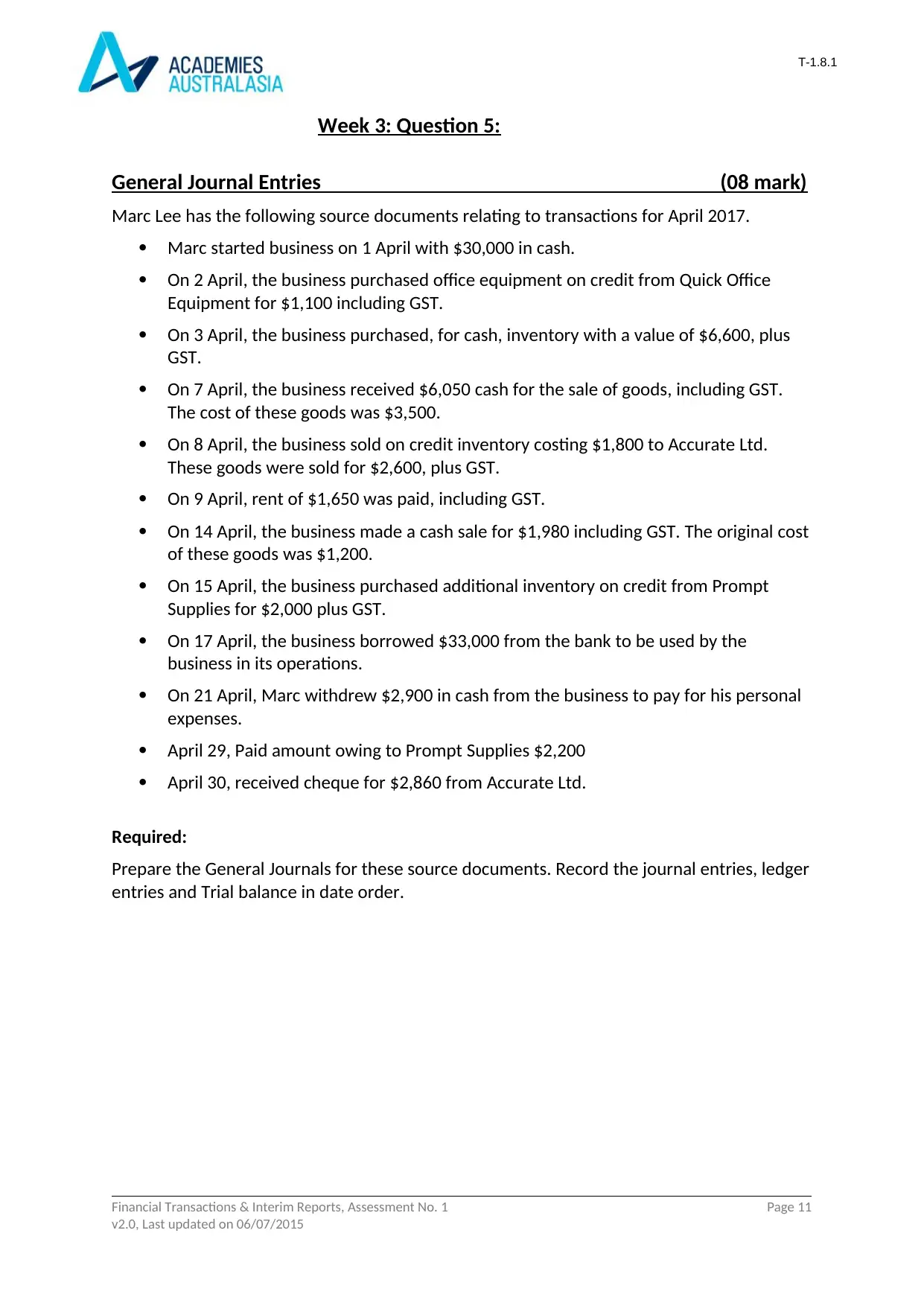

Week 3: Question 5:

General Journal Entries (08 mark)

Marc Lee has the following source documents relating to transactions for April 2017.

Marc started business on 1 April with $30,000 in cash.

On 2 April, the business purchased office equipment on credit from Quick Office

Equipment for $1,100 including GST.

On 3 April, the business purchased, for cash, inventory with a value of $6,600, plus

GST.

On 7 April, the business received $6,050 cash for the sale of goods, including GST.

The cost of these goods was $3,500.

On 8 April, the business sold on credit inventory costing $1,800 to Accurate Ltd.

These goods were sold for $2,600, plus GST.

On 9 April, rent of $1,650 was paid, including GST.

On 14 April, the business made a cash sale for $1,980 including GST. The original cost

of these goods was $1,200.

On 15 April, the business purchased additional inventory on credit from Prompt

Supplies for $2,000 plus GST.

On 17 April, the business borrowed $33,000 from the bank to be used by the

business in its operations.

On 21 April, Marc withdrew $2,900 in cash from the business to pay for his personal

expenses.

April 29, Paid amount owing to Prompt Supplies $2,200

April 30, received cheque for $2,860 from Accurate Ltd.

Required:

Prepare the General Journals for these source documents. Record the journal entries, ledger

entries and Trial balance in date order.

Financial Transactions & Interim Reports, Assessment No. 1 Page 11

v2.0, Last updated on 06/07/2015

Week 3: Question 5:

General Journal Entries (08 mark)

Marc Lee has the following source documents relating to transactions for April 2017.

Marc started business on 1 April with $30,000 in cash.

On 2 April, the business purchased office equipment on credit from Quick Office

Equipment for $1,100 including GST.

On 3 April, the business purchased, for cash, inventory with a value of $6,600, plus

GST.

On 7 April, the business received $6,050 cash for the sale of goods, including GST.

The cost of these goods was $3,500.

On 8 April, the business sold on credit inventory costing $1,800 to Accurate Ltd.

These goods were sold for $2,600, plus GST.

On 9 April, rent of $1,650 was paid, including GST.

On 14 April, the business made a cash sale for $1,980 including GST. The original cost

of these goods was $1,200.

On 15 April, the business purchased additional inventory on credit from Prompt

Supplies for $2,000 plus GST.

On 17 April, the business borrowed $33,000 from the bank to be used by the

business in its operations.

On 21 April, Marc withdrew $2,900 in cash from the business to pay for his personal

expenses.

April 29, Paid amount owing to Prompt Supplies $2,200

April 30, received cheque for $2,860 from Accurate Ltd.

Required:

Prepare the General Journals for these source documents. Record the journal entries, ledger

entries and Trial balance in date order.

Financial Transactions & Interim Reports, Assessment No. 1 Page 11

v2.0, Last updated on 06/07/2015

T-1.8.1

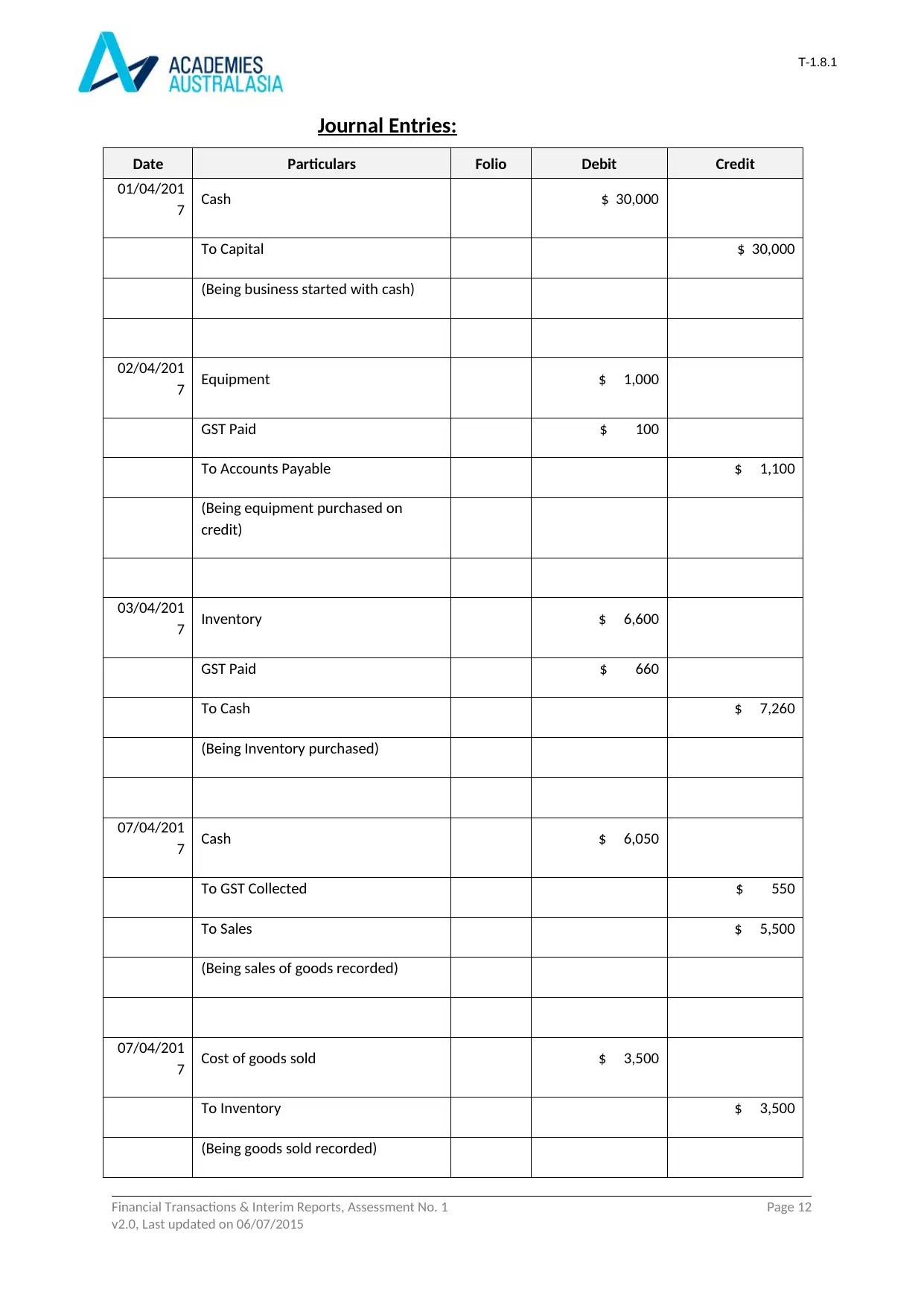

Journal Entries:

Date Particulars Folio Debit Credit

01/04/201

7 Cash $ 30,000

To Capital $ 30,000

(Being business started with cash)

02/04/201

7 Equipment $ 1,000

GST Paid $ 100

To Accounts Payable $ 1,100

(Being equipment purchased on

credit)

03/04/201

7 Inventory $ 6,600

GST Paid $ 660

To Cash $ 7,260

(Being Inventory purchased)

07/04/201

7 Cash $ 6,050

To GST Collected $ 550

To Sales $ 5,500

(Being sales of goods recorded)

07/04/201

7 Cost of goods sold $ 3,500

To Inventory $ 3,500

(Being goods sold recorded)

Financial Transactions & Interim Reports, Assessment No. 1 Page 12

v2.0, Last updated on 06/07/2015

Journal Entries:

Date Particulars Folio Debit Credit

01/04/201

7 Cash $ 30,000

To Capital $ 30,000

(Being business started with cash)

02/04/201

7 Equipment $ 1,000

GST Paid $ 100

To Accounts Payable $ 1,100

(Being equipment purchased on

credit)

03/04/201

7 Inventory $ 6,600

GST Paid $ 660

To Cash $ 7,260

(Being Inventory purchased)

07/04/201

7 Cash $ 6,050

To GST Collected $ 550

To Sales $ 5,500

(Being sales of goods recorded)

07/04/201

7 Cost of goods sold $ 3,500

To Inventory $ 3,500

(Being goods sold recorded)

Financial Transactions & Interim Reports, Assessment No. 1 Page 12

v2.0, Last updated on 06/07/2015

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 48

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.