Financial Accounting: AASB and International Standards

VerifiedAdded on 2020/01/28

|10

|1414

|54

Homework Assignment

AI Summary

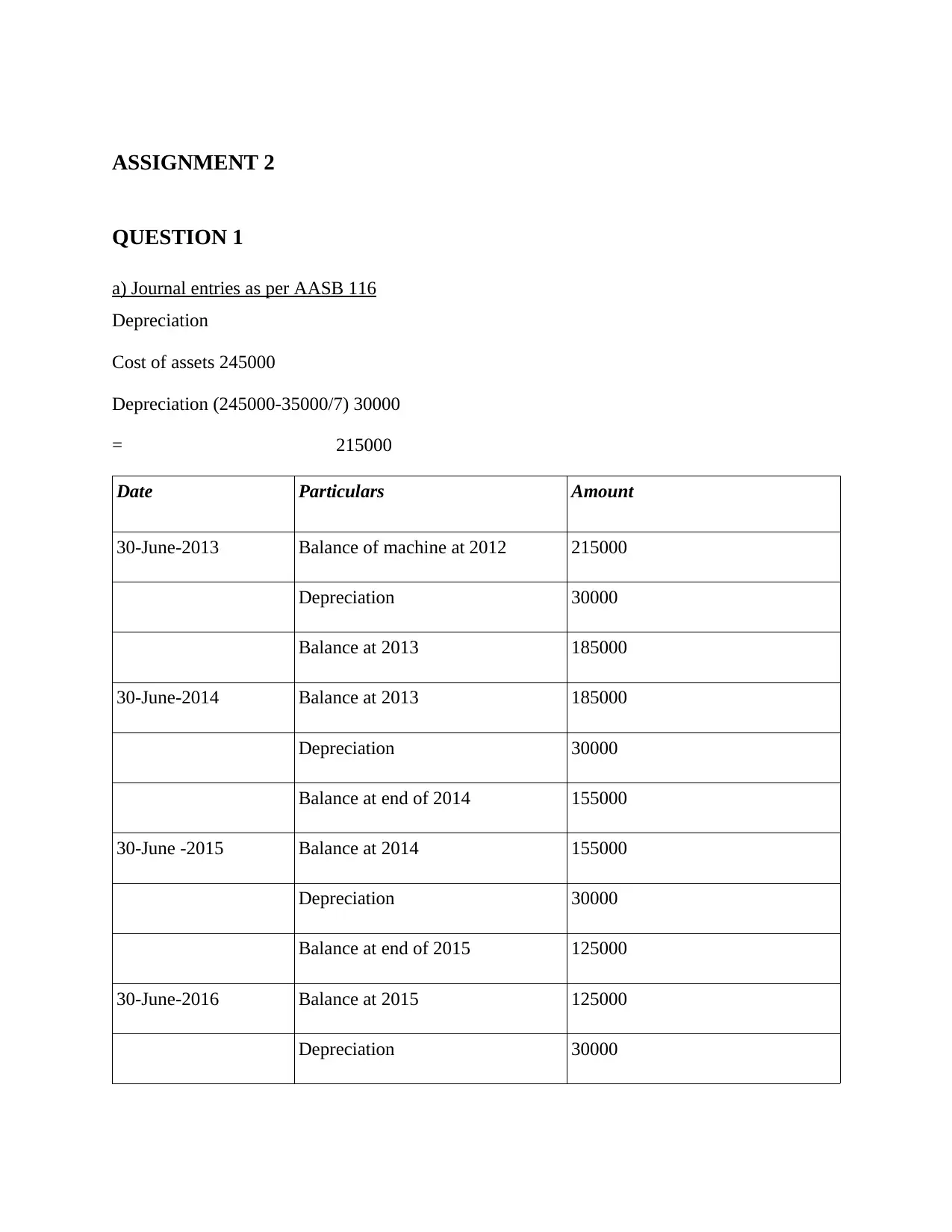

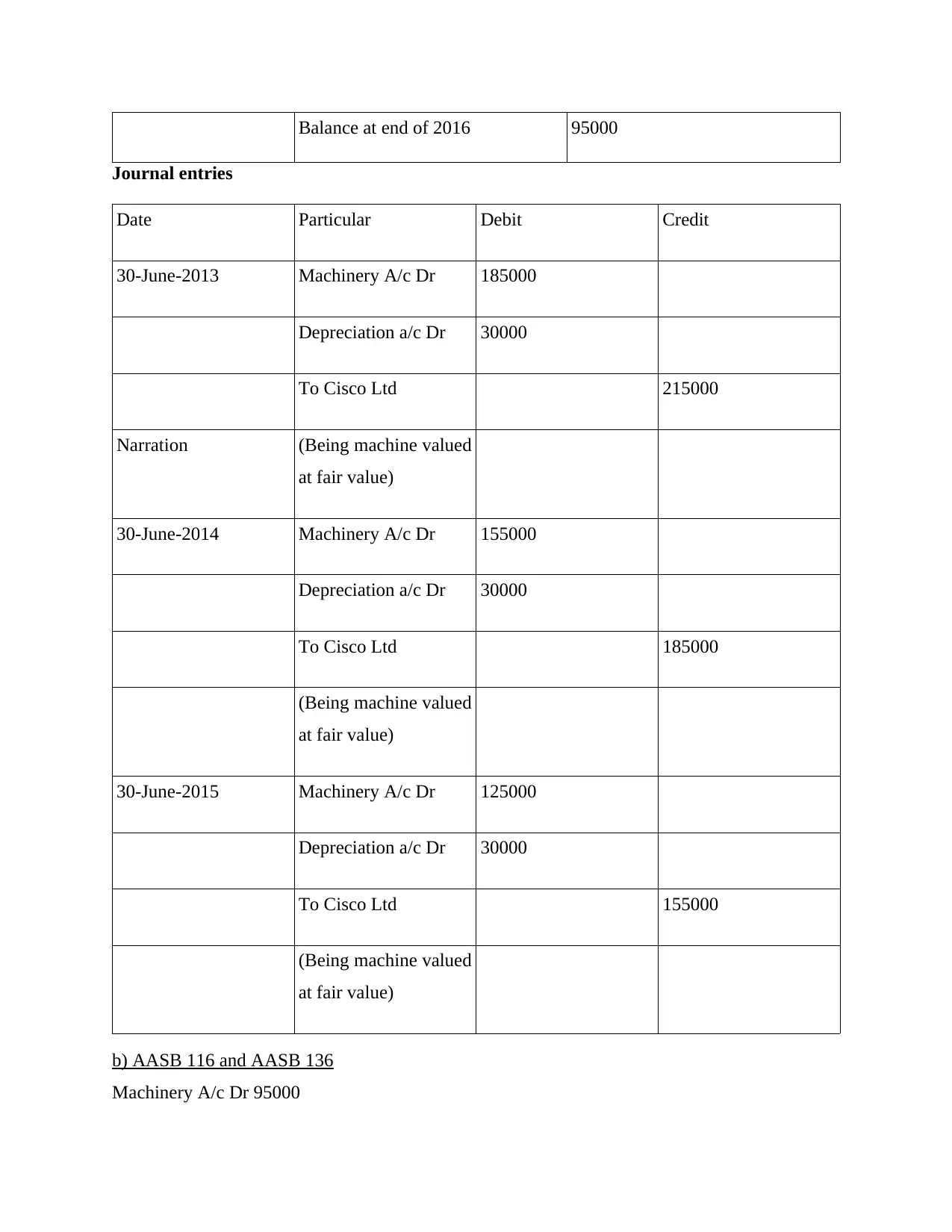

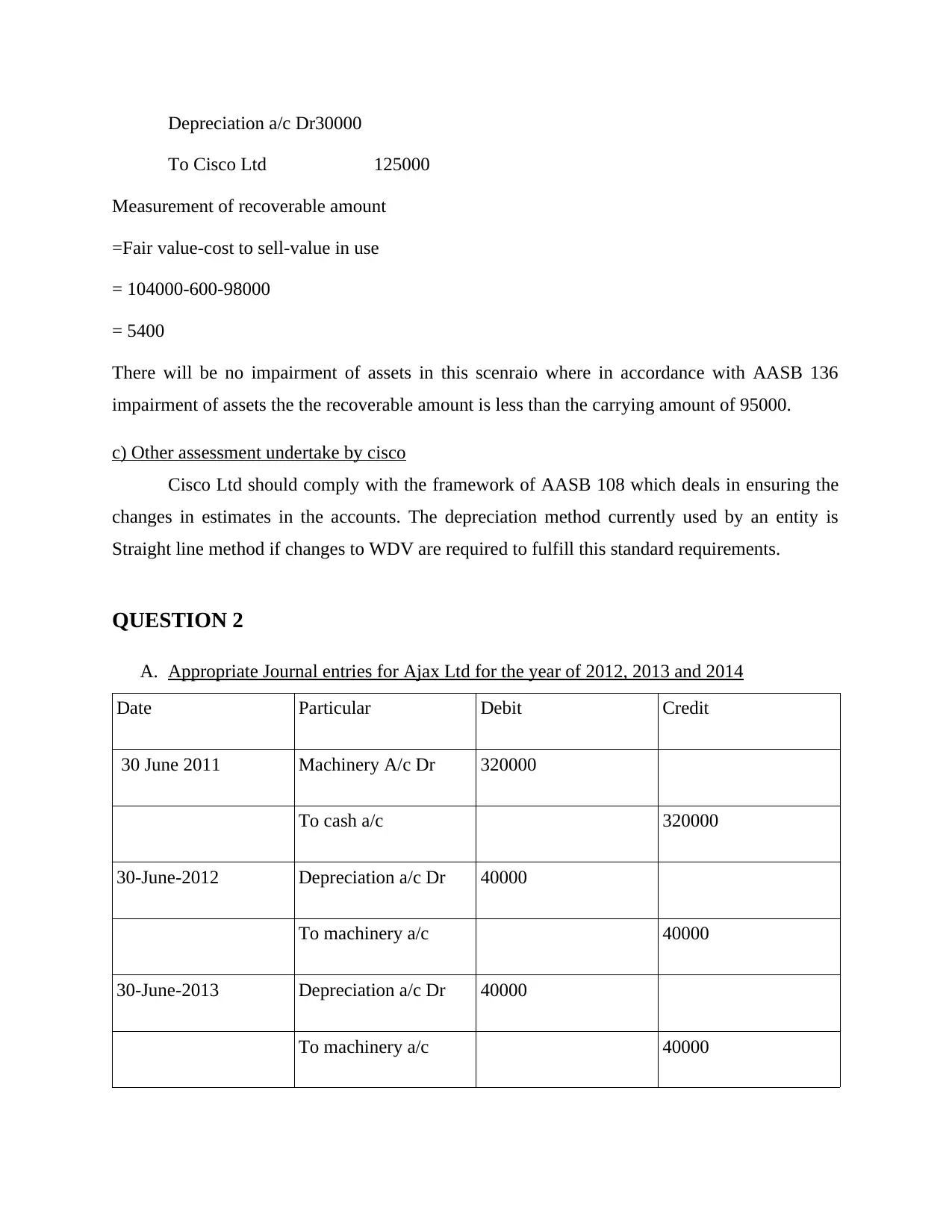

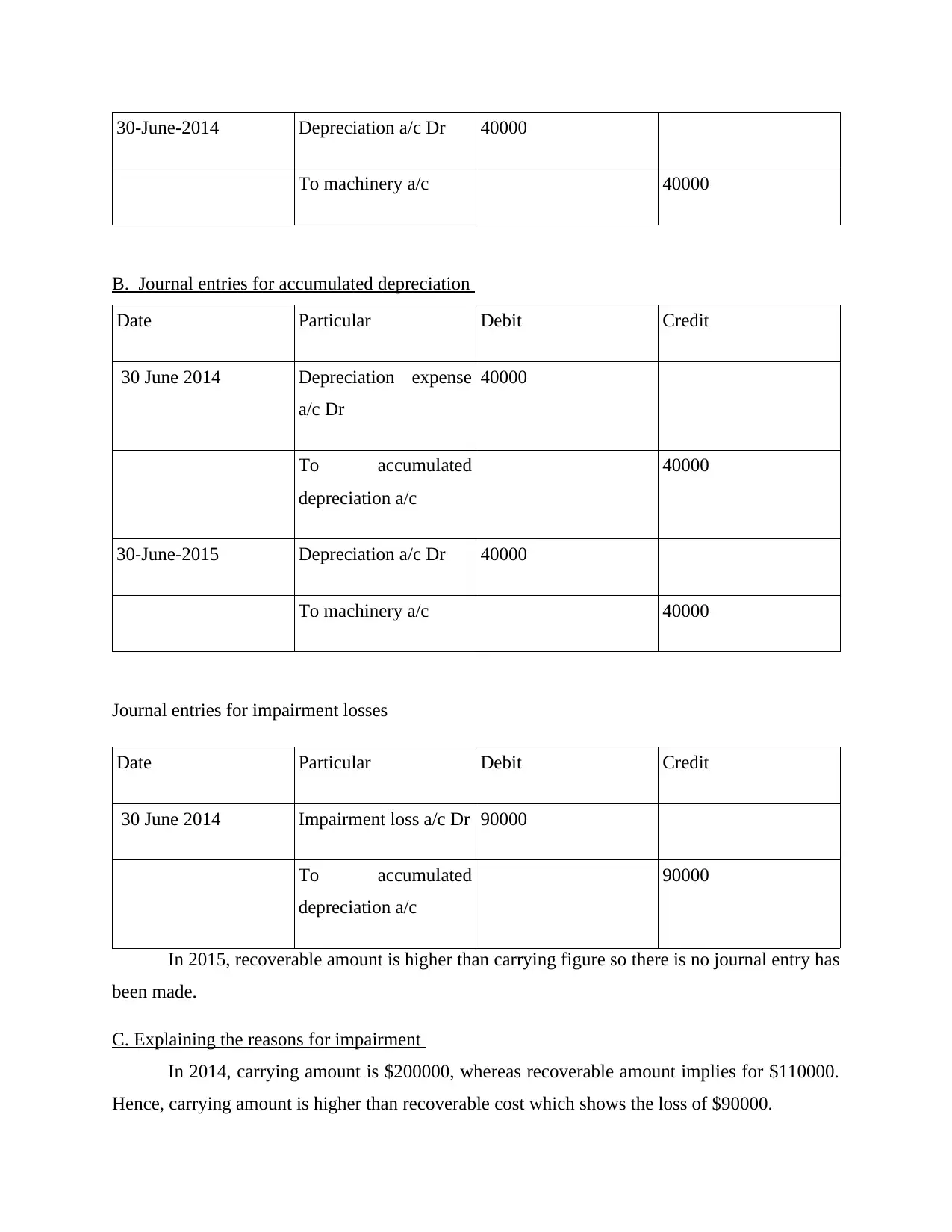

This financial accounting assignment addresses key concepts including depreciation, impairment of assets, and the application of accounting standards. The solution begins with journal entries related to asset depreciation under AASB 116, demonstrating the calculation and recording of depreciation expense over several years. It then explores the relationship between AASB 116 and AASB 136, specifically focusing on the impairment of assets and providing a scenario where no impairment occurs. The assignment further examines other assessments Cisco Ltd should undertake, referencing AASB 108 for changes in accounting estimates. Question 2 presents journal entries for Ajax Ltd from 2012 to 2014, including the initial purchase of machinery and subsequent depreciation entries. It also includes journal entries for accumulated depreciation and impairment losses, along with an explanation of the reasons for impairment, and the presentation of plant and equipment in the balance sheet. Finally, Question 3 interprets the technical requirements and importance of international accounting standards, highlighting the significance of transparency and standardization in financial reporting, and the need for technical knowledge to deal with IFRS, deferred tax assets and liabilities, and retirement plans.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.