Financial Accounting: Client Statements and Accounting Concepts

VerifiedAdded on 2020/10/23

|33

|5035

|191

Homework Assignment

AI Summary

This assignment delves into the core principles and practices of financial accounting. It begins by defining financial accounting, outlining its purpose, and explaining relevant regulations, including GAAP and IFRS. The document then explores various accounting rules, principles, and concepts such as the business entity concept, money measurement, dual aspect, going concern, cost, and matching concepts. The concepts of consistency and material disclosure are also discussed. The assignment further provides practical applications through client examples, including journal entries, profit and loss statements, balance sheets, bank reconciliation statements, control accounts, and suspense accounts. The document also covers depreciation methods and the accounting concepts of consistency and prudence. Overall, the assignment provides a comprehensive understanding of financial accounting principles and their practical application in preparing financial statements and analyzing financial data.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

A.1). Defining financial accounting and its different purpose....................................................1

A.2). Explaining the regulations relating to the financial accounting.........................................2

A. 3). Describing different accounting rules and principles.......................................................2

A. 4). Explaining the conventions and concepts relating to consistency and material

disclosure....................................................................................................................................4

CLIENT 1........................................................................................................................................4

Trail balance as of 31st may:.........................................................................................................13

CLIENT 2......................................................................................................................................15

A). The statement for Profit and loss of Peter Hampau............................................................15

B). Financial Statement.............................................................................................................16

........................................................................................................................................................17

CLIENT 3......................................................................................................................................17

A). Preparing the statement of profit and loss account.............................................................17

...................................................................................................................................................18

...................................................................................................................................................18

B). financial position of Bowling Ltd. For the year ending 31st July 2018..............................18

C). Explaining the accounting concepts of Consistency and Prudency....................................19

D). Describing the purpose and methods of Depreciation........................................................20

CLIENT 4......................................................................................................................................22

A). Explaining the purpose of preparing Bank Reconciliation Statements and its essential of

preparing it on monthly basis....................................................................................................22

B). Explaining the areas which may cause the bank records to vary. ......................................23

C). Preparing accounts through cash-flow statements..............................................................23

CLIENT 5......................................................................................................................................25

A). Preparing Control accounts.................................................................................................25

B). The need and purpose of preparing Control Account.........................................................26

CLIENT 6......................................................................................................................................26

A). Explaining Suspense account and the main features of it...................................................26

INTRODUCTION...........................................................................................................................1

A.1). Defining financial accounting and its different purpose....................................................1

A.2). Explaining the regulations relating to the financial accounting.........................................2

A. 3). Describing different accounting rules and principles.......................................................2

A. 4). Explaining the conventions and concepts relating to consistency and material

disclosure....................................................................................................................................4

CLIENT 1........................................................................................................................................4

Trail balance as of 31st may:.........................................................................................................13

CLIENT 2......................................................................................................................................15

A). The statement for Profit and loss of Peter Hampau............................................................15

B). Financial Statement.............................................................................................................16

........................................................................................................................................................17

CLIENT 3......................................................................................................................................17

A). Preparing the statement of profit and loss account.............................................................17

...................................................................................................................................................18

...................................................................................................................................................18

B). financial position of Bowling Ltd. For the year ending 31st July 2018..............................18

C). Explaining the accounting concepts of Consistency and Prudency....................................19

D). Describing the purpose and methods of Depreciation........................................................20

CLIENT 4......................................................................................................................................22

A). Explaining the purpose of preparing Bank Reconciliation Statements and its essential of

preparing it on monthly basis....................................................................................................22

B). Explaining the areas which may cause the bank records to vary. ......................................23

C). Preparing accounts through cash-flow statements..............................................................23

CLIENT 5......................................................................................................................................25

A). Preparing Control accounts.................................................................................................25

B). The need and purpose of preparing Control Account.........................................................26

CLIENT 6......................................................................................................................................26

A). Explaining Suspense account and the main features of it...................................................26

B). Preparing trail balance.........................................................................................................27

C). Trail balance with suspense account...................................................................................27

D). Differentiate between suspense account and clearing account...........................................28

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................29

C). Trail balance with suspense account...................................................................................27

D). Differentiate between suspense account and clearing account...........................................28

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................29

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is the specialised branch of the accounting which helps in gathering

and tracking the financial transaction of a company. It helps in analysed and classifying the

transactions in order to prepare the financial statements of the company. Financial accounting

mainly focuses on preparing and presenting the monetary statements that are useful for the

external users like investors and creditors. The present report is based on Zync Solutions Limited

which is a small accountancy firm. This report will help in understand the different aspects of

financial accounting and preparing financial statements. Report will define the purpose of

financial accounting with its regulations (Nobes, 2014). Different rules, principle and concepts of

accounting will also be discussed. Further, report will include preparation of financial accounting

using double entry book keeping. The final accounts of sole trader, partnership will also

presented. Report will than, discuss the methods of depreciation with examples. Furthermore, the

Bank reconciliation statement also discuss with appropriate calculation of cash-book.

A.1). Defining financial accounting and its different purpose.

It can be defined as specialised branch of accounting which indulge in keeping track of

company's financial transactions. It helps in classifying, analysing, summarizing and recording

of all the financial transaction in a manner that can be well utilised by external users. Financial

accounting mainly focuses on preparing the financial accounts on providing external users the

information regarding the company's financial position and financial performance over a specific

time period (What is Financial Accounting?, 2019). These external users are the investors and

creditors, who uses the financial information of the company in order to make decisions for

further investment in company. They use the financial information from the financial statement

that are being prepared from the financial information.

Financial accounting is an important method in order to prepare the financial reporting

through financial statements. The main purpose of financial accounting is:

To provide the fair and relevant information of company's financial performance to the

outside users.

To prepare financial statements of the company which reflects the financial transactions

of the company.

1

Financial accounting is the specialised branch of the accounting which helps in gathering

and tracking the financial transaction of a company. It helps in analysed and classifying the

transactions in order to prepare the financial statements of the company. Financial accounting

mainly focuses on preparing and presenting the monetary statements that are useful for the

external users like investors and creditors. The present report is based on Zync Solutions Limited

which is a small accountancy firm. This report will help in understand the different aspects of

financial accounting and preparing financial statements. Report will define the purpose of

financial accounting with its regulations (Nobes, 2014). Different rules, principle and concepts of

accounting will also be discussed. Further, report will include preparation of financial accounting

using double entry book keeping. The final accounts of sole trader, partnership will also

presented. Report will than, discuss the methods of depreciation with examples. Furthermore, the

Bank reconciliation statement also discuss with appropriate calculation of cash-book.

A.1). Defining financial accounting and its different purpose.

It can be defined as specialised branch of accounting which indulge in keeping track of

company's financial transactions. It helps in classifying, analysing, summarizing and recording

of all the financial transaction in a manner that can be well utilised by external users. Financial

accounting mainly focuses on preparing the financial accounts on providing external users the

information regarding the company's financial position and financial performance over a specific

time period (What is Financial Accounting?, 2019). These external users are the investors and

creditors, who uses the financial information of the company in order to make decisions for

further investment in company. They use the financial information from the financial statement

that are being prepared from the financial information.

Financial accounting is an important method in order to prepare the financial reporting

through financial statements. The main purpose of financial accounting is:

To provide the fair and relevant information of company's financial performance to the

outside users.

To prepare financial statements of the company which reflects the financial transactions

of the company.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To ensures that external information will be able to have quality information to make

their financial decisions on (Edwards, 2013).

The main purpose is to showcase an accurate picture and fair picture of financial affairs

of the company.

A.2). Explaining the regulations relating to the financial accounting.

The financial reporting is the process of preparing and presenting the financial statements

of the company to the external users. In order to prepare the company's monetary statements that

can be understandable to the users, there are some guidelines and regulations has been set. All

the listed company has to prepare their statements as per the guidelines set (Horngren and et.al.,

2012). The following are the regulation related to the financial accounting: GAAP: It is the collection of the rules and standards that are commonly formed in

preparing financial reporting. It provides general guidelines, accepted accounting

principles and procedures that companies has to follow at the time of preparing financial

statements (Barth and et.al., 2012). GAAP has set the rules based on some basic

underlying principles and concepts such as matching principles, relevance, reliability etc. IFRS: International financial reporting standards are designed as a common global

language for the business transaction so that the accounting standards if the company can

be understandable and comparable across the international boundaries (Weygandt,

Kimmel and Kieso, 2015). IFRS helps in facilitating the comparability between

enterprises operating in different jurisdictions.

IASB: The International Accounting Standard Board is the independent standard setting

body of the IFRS foundation (Hansen, 2011). The main mission of the board is to

develop and enforce the globally accepted International Financial Reporting Standard.

A. 3). Describing different accounting rules and principles.

Accounting practices can be termed as the uniform practices which entities follow in

order to record, prepare and present the financial statements (Weil, Schipper and Francis, 2013).

All the companies have to prepare its financial statements as per the rules and principles which is

essential in order to present the true and fair view of business. Following are the basic

accounting principles and concepts:

2

their financial decisions on (Edwards, 2013).

The main purpose is to showcase an accurate picture and fair picture of financial affairs

of the company.

A.2). Explaining the regulations relating to the financial accounting.

The financial reporting is the process of preparing and presenting the financial statements

of the company to the external users. In order to prepare the company's monetary statements that

can be understandable to the users, there are some guidelines and regulations has been set. All

the listed company has to prepare their statements as per the guidelines set (Horngren and et.al.,

2012). The following are the regulation related to the financial accounting: GAAP: It is the collection of the rules and standards that are commonly formed in

preparing financial reporting. It provides general guidelines, accepted accounting

principles and procedures that companies has to follow at the time of preparing financial

statements (Barth and et.al., 2012). GAAP has set the rules based on some basic

underlying principles and concepts such as matching principles, relevance, reliability etc. IFRS: International financial reporting standards are designed as a common global

language for the business transaction so that the accounting standards if the company can

be understandable and comparable across the international boundaries (Weygandt,

Kimmel and Kieso, 2015). IFRS helps in facilitating the comparability between

enterprises operating in different jurisdictions.

IASB: The International Accounting Standard Board is the independent standard setting

body of the IFRS foundation (Hansen, 2011). The main mission of the board is to

develop and enforce the globally accepted International Financial Reporting Standard.

A. 3). Describing different accounting rules and principles.

Accounting practices can be termed as the uniform practices which entities follow in

order to record, prepare and present the financial statements (Weil, Schipper and Francis, 2013).

All the companies have to prepare its financial statements as per the rules and principles which is

essential in order to present the true and fair view of business. Following are the basic

accounting principles and concepts:

2

Business entity concept: This concept states that the business and its owner will be

treated as different from his company (Collins, Pasewark and Riley, 2012). All the

financial transaction of owner will be treated differently with company's transaction. Money measurement concepts: As per this concepts, the business transaction that can be

expressed in term of money or currency will be taken in accounting and other types of

transaction will be kept separately (Trotman and Carson, 2018). Dual aspect concept: This concept is based on the basic accounting rule, that for every

credit a corresponding debit will made (Donelson, McInnis and Mergenthaler, 2012). The

transaction with dual aspects will be considered and will recorded in accounting. Going concern Concept: In accounting, a business is expected to continue for a longer

period in order to carry out its obligation and activities (Henderson and et.al., 2015). Cost concept: This concepts states that, all the fixed assets of the business will be

recorded at their actual cost in the first year of the business. After that, the assets will

recorded after deducting their annual depreciation (Peytcheva, Wright and Majoor, 2014).

As per this concept, the price of fixed assets will not be change on the basis of the cost

change in market. Accounting year concept: This concept states that, every company has to choose a

specific time period in order to complete its accounting process cycle (McEnroe and

Sullivan, 2012). This time period could be monthly, quarterly, annually as per the fiscal

year. Matching concept: This concepts said that for entry of revenue that will be recorded in

an accounting period, an equal amount of expense entry has to be made in order to

correctly calculate profit and loss for a given period (Beatty and Liao, 2014).

Realisation concept: As per this concept, the profit will be realised only when it is

actually earned (Bailey and Sawers, 2018). Advance of any type of fee will not be treated

as profit until the good and service will be delivered to the buyer.

The three rules of accounting are:

Debit the receiver, credit the giver. This rule is used in case of personal account.

3

treated as different from his company (Collins, Pasewark and Riley, 2012). All the

financial transaction of owner will be treated differently with company's transaction. Money measurement concepts: As per this concepts, the business transaction that can be

expressed in term of money or currency will be taken in accounting and other types of

transaction will be kept separately (Trotman and Carson, 2018). Dual aspect concept: This concept is based on the basic accounting rule, that for every

credit a corresponding debit will made (Donelson, McInnis and Mergenthaler, 2012). The

transaction with dual aspects will be considered and will recorded in accounting. Going concern Concept: In accounting, a business is expected to continue for a longer

period in order to carry out its obligation and activities (Henderson and et.al., 2015). Cost concept: This concepts states that, all the fixed assets of the business will be

recorded at their actual cost in the first year of the business. After that, the assets will

recorded after deducting their annual depreciation (Peytcheva, Wright and Majoor, 2014).

As per this concept, the price of fixed assets will not be change on the basis of the cost

change in market. Accounting year concept: This concept states that, every company has to choose a

specific time period in order to complete its accounting process cycle (McEnroe and

Sullivan, 2012). This time period could be monthly, quarterly, annually as per the fiscal

year. Matching concept: This concepts said that for entry of revenue that will be recorded in

an accounting period, an equal amount of expense entry has to be made in order to

correctly calculate profit and loss for a given period (Beatty and Liao, 2014).

Realisation concept: As per this concept, the profit will be realised only when it is

actually earned (Bailey and Sawers, 2018). Advance of any type of fee will not be treated

as profit until the good and service will be delivered to the buyer.

The three rules of accounting are:

Debit the receiver, credit the giver. This rule is used in case of personal account.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debit what comes in, credit what goes out (Macve, 2015). This principle is applied in

case of real account.

Debit all expenses and losses, credit all incomes and gains.

A. 4). Explaining the conventions and concepts relating to consistency and material disclosure.

The following are the concepts and conventions that are related to:

Consistency Concepts

This concepts states that, a company once adopted a method to treat a transaction or

events should use the same accounting method. It is important for a company to use a same

accounting method for every year. If a company will change its accounting method every year it

will be difficult for user to compare between different year's statements (Edmonds and et.al.,

2013). It does not mean that a company can never change its accounting method, a company can

change its method on some reasonable ground and has to disclose the nature of change and new

method adopted and its effect on the financial statements.

Material disclosure Concepts

This concepts states that, the financial information of a company is the material of the

financial statements as long it would change or affect the view of the person (McEnroe and

Sullivan, 2012). It can also be said that, all the important financial information that can make a

change in the monetary statements users has to be included in the financial statements of

company.

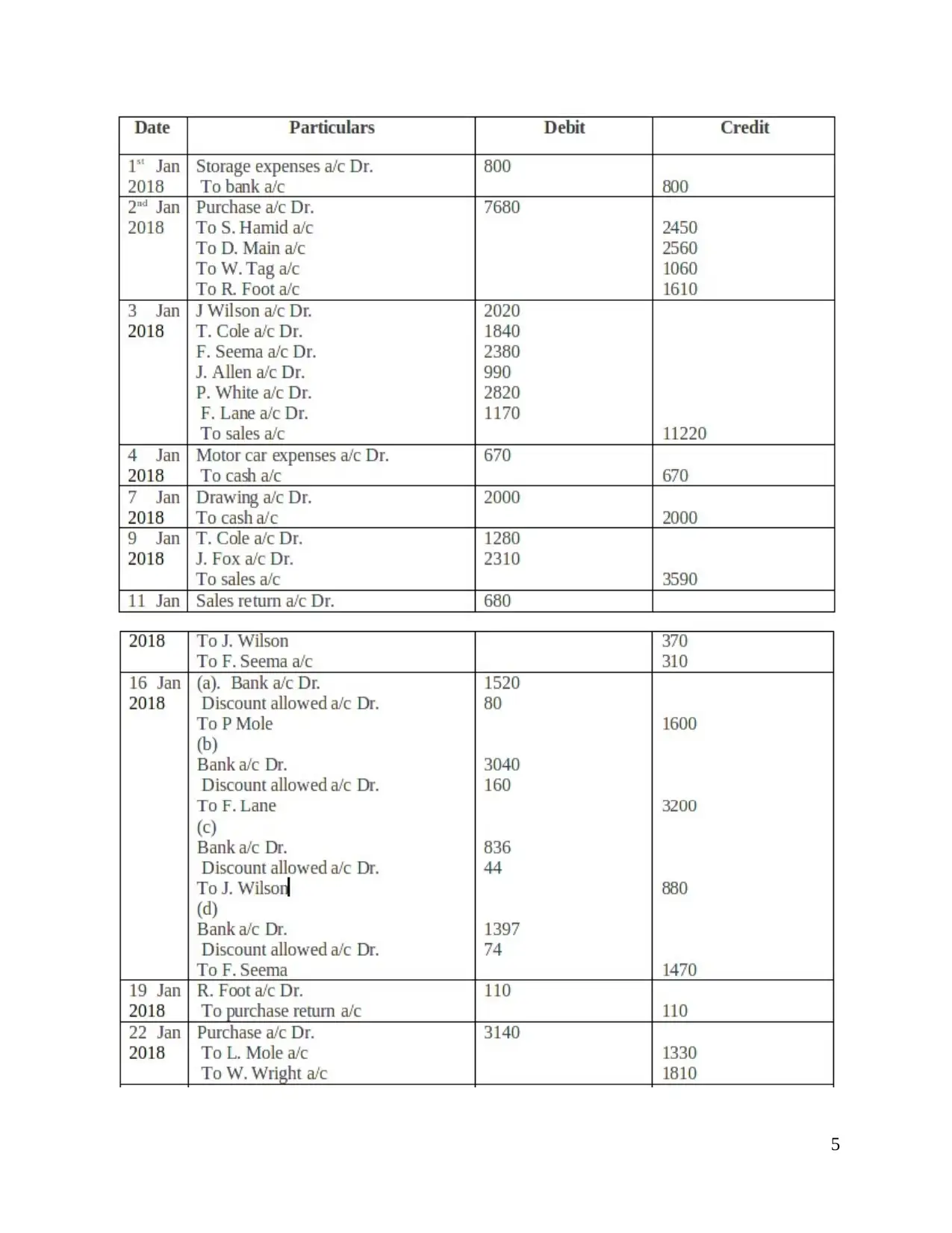

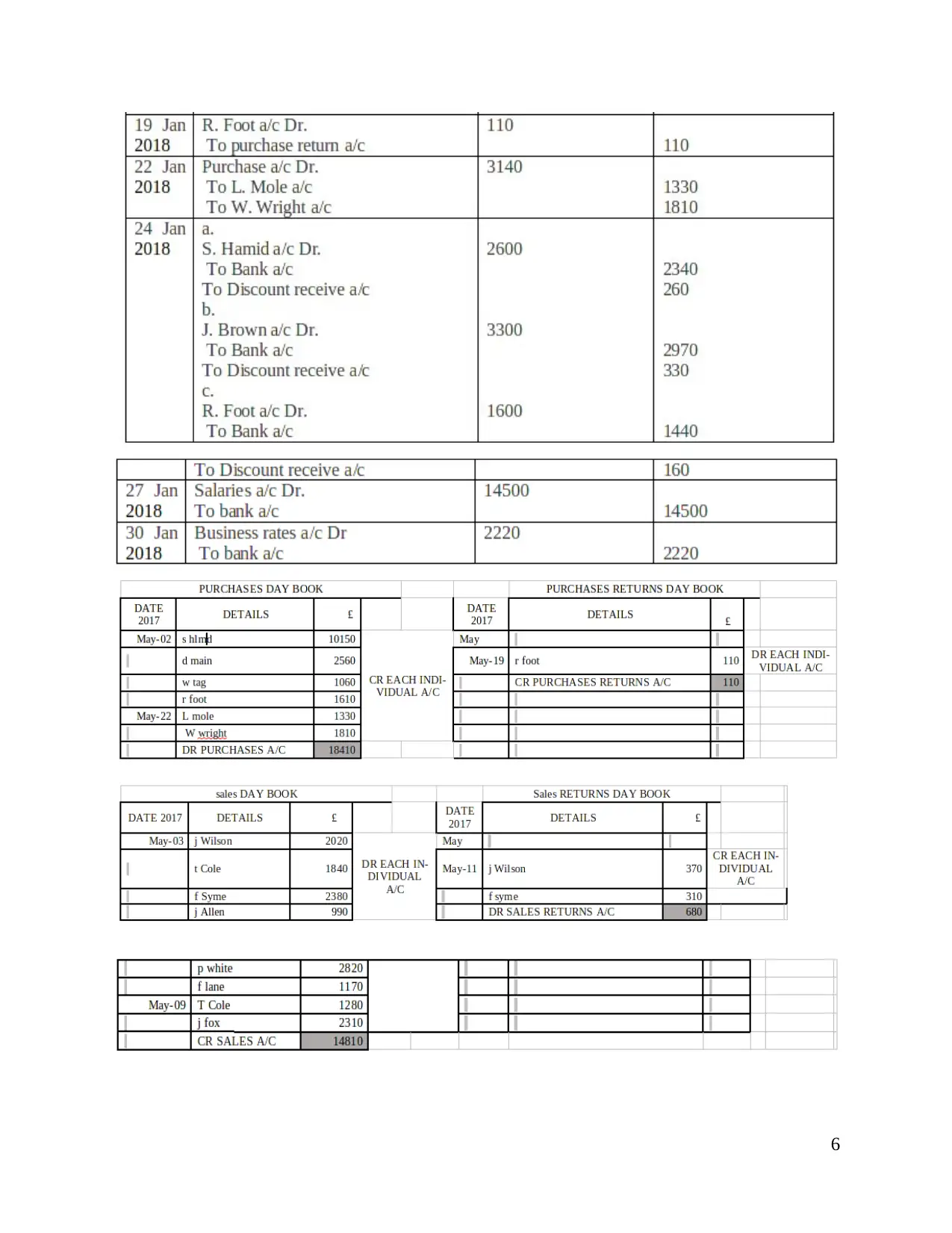

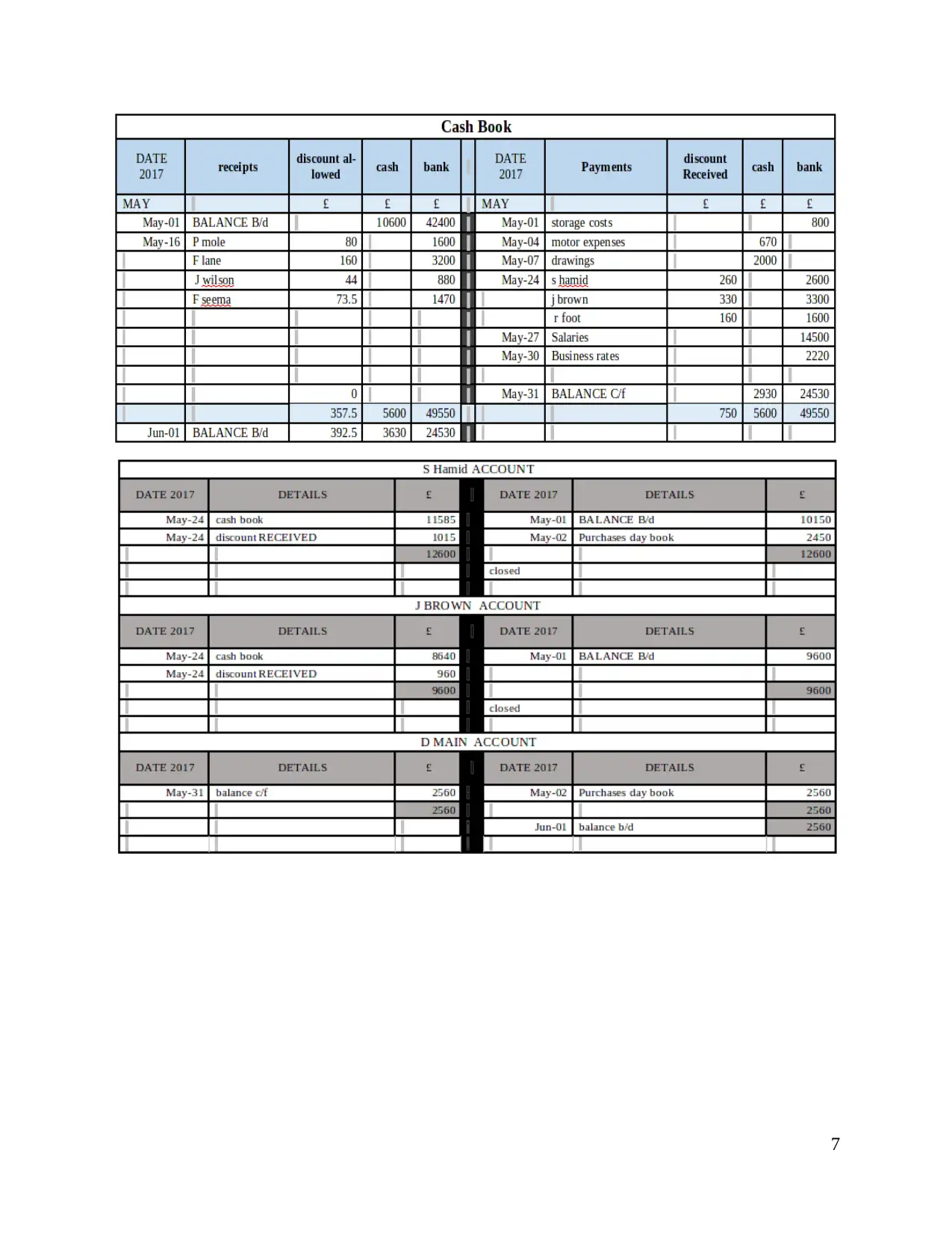

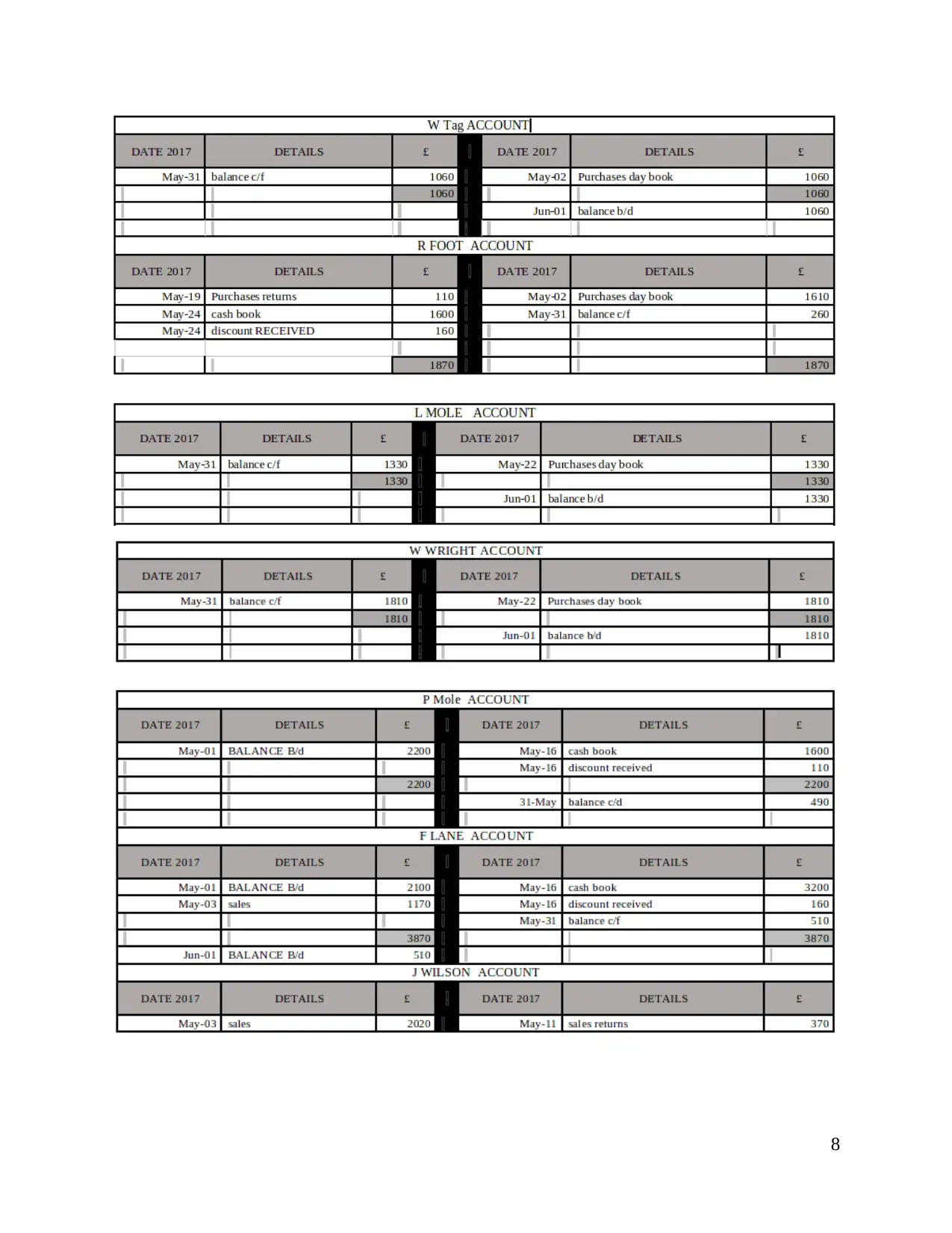

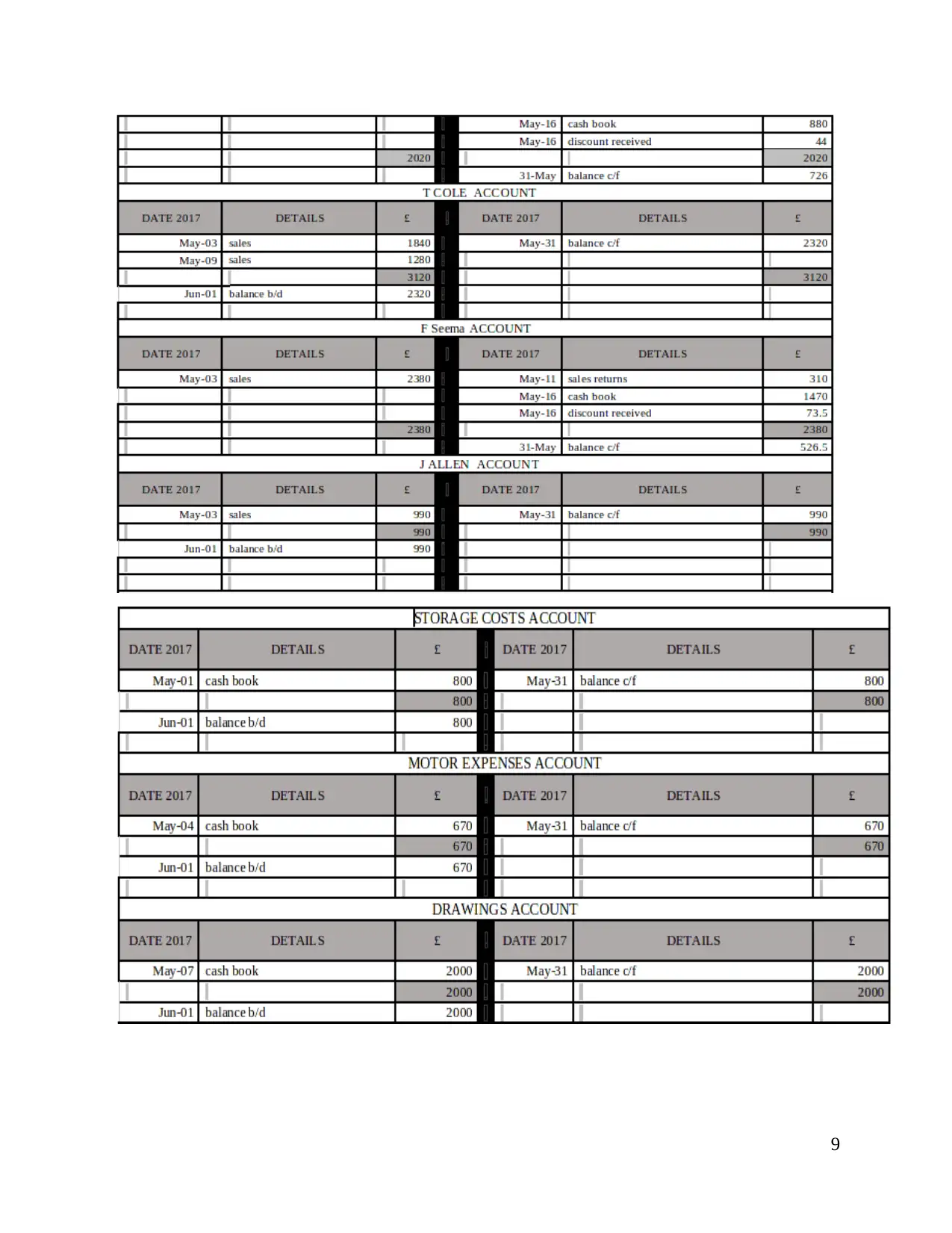

CLIENT 1

Journal entries in the book of David Study’s for the month of January are as follows:

4

case of real account.

Debit all expenses and losses, credit all incomes and gains.

A. 4). Explaining the conventions and concepts relating to consistency and material disclosure.

The following are the concepts and conventions that are related to:

Consistency Concepts

This concepts states that, a company once adopted a method to treat a transaction or

events should use the same accounting method. It is important for a company to use a same

accounting method for every year. If a company will change its accounting method every year it

will be difficult for user to compare between different year's statements (Edmonds and et.al.,

2013). It does not mean that a company can never change its accounting method, a company can

change its method on some reasonable ground and has to disclose the nature of change and new

method adopted and its effect on the financial statements.

Material disclosure Concepts

This concepts states that, the financial information of a company is the material of the

financial statements as long it would change or affect the view of the person (McEnroe and

Sullivan, 2012). It can also be said that, all the important financial information that can make a

change in the monetary statements users has to be included in the financial statements of

company.

CLIENT 1

Journal entries in the book of David Study’s for the month of January are as follows:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.