Financial Accounting Assignment: AASB 138 & Defined Benefit Plan

VerifiedAdded on 2020/03/23

|11

|3052

|94

Homework Assignment

AI Summary

This financial accounting assignment comprehensively addresses key concepts in financial reporting. It begins by exploring fair value measurement techniques, contrasting residential and industrial land valuations, and highlighting the significance of market value. The assignment then presents detailed journal entries for Peewee Ltd over two years, including depreciation, revaluation of assets, and the sale of an asset. Furthermore, it provides an in-depth analysis of internally generated intangible assets under AASB 138/IAS 38, differentiating them from acquired intangibles and discussing companies' reluctance to change accounting practices. Finally, the assignment delves into a defined benefit plan for Wattle Ltd, calculating surpluses/deficits, net liabilities, net interest, and providing a reconciliation of the net defined benefit liability, along with the necessary journal entries. The assignment provides a practical application of accounting standards and principles.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

1

Table of Contents

Question 1: Depicting the different measures used in identifying fair values...........................2

Question 2:.................................................................................................................................3

1. Depicting the journal entries of Peewee Ltd for the year ended 30 June 2017:.....................3

2. Depositing the journal entries of Peewee Ltd for the year ended 30 June 2018:...................4

Question 3:.................................................................................................................................6

1. Providing relevant explanation regarding internally generated intangible assets in AASB

138/IAS 38:................................................................................................................................6

2. Mentioning about the difference between accounting for internally generated intangible

assets and acquired intangible assets in AASB 138/IAS 38:.....................................................7

3. Depicting why companies might be reluctant to change in AASB 138/IAS 38:...................7

Question 4:.................................................................................................................................8

1. Mentioning the surplus or deficit of Wattle Ltd’s defined benefit plan at 31 December

2016:...........................................................................................................................................8

2. Depicting net defined benefit asset or liability at 31 December 2016:..................................9

3. Depicting net interest and the return on plan assets in 31 December 2016:..........................9

4. Providing reconciliation regarding opening balance and closing balance of the net defined

benefit liability:..........................................................................................................................9

5. Drafting journal entry to defined benefit superannuation plan in the books of Wattle Ltd for

the year ended 31 December 2016:..........................................................................................10

Reference and Bibliography:....................................................................................................12

1

Table of Contents

Question 1: Depicting the different measures used in identifying fair values...........................2

Question 2:.................................................................................................................................3

1. Depicting the journal entries of Peewee Ltd for the year ended 30 June 2017:.....................3

2. Depositing the journal entries of Peewee Ltd for the year ended 30 June 2018:...................4

Question 3:.................................................................................................................................6

1. Providing relevant explanation regarding internally generated intangible assets in AASB

138/IAS 38:................................................................................................................................6

2. Mentioning about the difference between accounting for internally generated intangible

assets and acquired intangible assets in AASB 138/IAS 38:.....................................................7

3. Depicting why companies might be reluctant to change in AASB 138/IAS 38:...................7

Question 4:.................................................................................................................................8

1. Mentioning the surplus or deficit of Wattle Ltd’s defined benefit plan at 31 December

2016:...........................................................................................................................................8

2. Depicting net defined benefit asset or liability at 31 December 2016:..................................9

3. Depicting net interest and the return on plan assets in 31 December 2016:..........................9

4. Providing reconciliation regarding opening balance and closing balance of the net defined

benefit liability:..........................................................................................................................9

5. Drafting journal entry to defined benefit superannuation plan in the books of Wattle Ltd for

the year ended 31 December 2016:..........................................................................................10

Reference and Bibliography:....................................................................................................12

FINANCIAL ACCOUNTING

2

Question 1: Depicting the different measures used in identifying fair values

Using the highest value of the plot for the valuation:

The highest valuation of the premises is mainly identified, if the plot is used for

residential purposes. The residential valuation directly includes only the plot value and

excludes the value of factory. Therefore, the demolition cost for the factory is estimated to be

$100,000, which directly helps in reducing the overall value of the land from $1,000,000 to

$900,000. The overall value of the plot is identified to be $900,000 under the residential

valuation. However, the second valuation technique that could be used for identifying the

value of a plot includes the factory outlet, where relevant cost of around $780,000 will be

included for setting up new factory. However, the existing factory plant if used will only cost

around $390,000 for the factory work. There are many other low budget plots in which the

factory could be built for reducing cost of factory. The evaluation of the overall land for

residential purposes is relatively higher and could directly allow the company to generate

high return from investment (Abbott & Tan‐Kantor, 2017).

Depicting the significance of selling the plot in market value:

The overall case directly indicates that selling the land for residential purpose could

directly provide higher returns from investment Maple Ltd.

Identifying the overall asset that is subject to measurement:

From the evaluation it could be identified that there are two different types of

valuation that needs to be conducted identifying the actual value of the asset. The first

valuation needs to be conducted for the overall plot and the second valuation is to be

conducted on the factory (Malone, Tarca & Wee, 2016). However, the overall is it could also

be valued as a single unit for deriving the actual value of the plot and actually.

Adequately using valuation techniques:

2

Question 1: Depicting the different measures used in identifying fair values

Using the highest value of the plot for the valuation:

The highest valuation of the premises is mainly identified, if the plot is used for

residential purposes. The residential valuation directly includes only the plot value and

excludes the value of factory. Therefore, the demolition cost for the factory is estimated to be

$100,000, which directly helps in reducing the overall value of the land from $1,000,000 to

$900,000. The overall value of the plot is identified to be $900,000 under the residential

valuation. However, the second valuation technique that could be used for identifying the

value of a plot includes the factory outlet, where relevant cost of around $780,000 will be

included for setting up new factory. However, the existing factory plant if used will only cost

around $390,000 for the factory work. There are many other low budget plots in which the

factory could be built for reducing cost of factory. The evaluation of the overall land for

residential purposes is relatively higher and could directly allow the company to generate

high return from investment (Abbott & Tan‐Kantor, 2017).

Depicting the significance of selling the plot in market value:

The overall case directly indicates that selling the land for residential purpose could

directly provide higher returns from investment Maple Ltd.

Identifying the overall asset that is subject to measurement:

From the evaluation it could be identified that there are two different types of

valuation that needs to be conducted identifying the actual value of the asset. The first

valuation needs to be conducted for the overall plot and the second valuation is to be

conducted on the factory (Malone, Tarca & Wee, 2016). However, the overall is it could also

be valued as a single unit for deriving the actual value of the plot and actually.

Adequately using valuation techniques:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING

3

Two different types of approaches are used for evaluating the fair value of the land,

which is determined under the residential purposes as $900,000. The highest value of the land

needs to be identified, which could directly allow the organisation to generate higher returns

from investment. The first valuation is mainly conducted for only the plot, where no inclusion

is conducted on factory outlet. Furthermore, the second valuation is conducted on the factory

outlet, which is for industrial purposes. The second valuation does not provide the adequate

returns, as the first valuation of residential plots. Therefore, the use of the plot for residential

purpose could directly allow the organisation to generate higher returns from investment

(Wang, 2016).

Question 2:

1. Depicting the journal entries of Peewee Ltd for the year ended 30 June 2017:

1st July

2016

Machine A...........................................................Dr

Machine B...........................................................Dr

Cash........................................................Cr

100,000

60,000

160,000

30th June

2017

Depreciation-Machine A................................................Dr

Accumulated Depreciation............................Cr

(1/5 * $100,000 = $20,000)

20,000

20,000

Depreciation-Machine B................................................Dr

Accumulated Depreciation.............................Cr

(1/3 * $60,000 = $20,000)

20,000

20,000

Accumulated Depreciation Machine A..........................Dr

Machine A...................................................Cr

20,000

20,000

3

Two different types of approaches are used for evaluating the fair value of the land,

which is determined under the residential purposes as $900,000. The highest value of the land

needs to be identified, which could directly allow the organisation to generate higher returns

from investment. The first valuation is mainly conducted for only the plot, where no inclusion

is conducted on factory outlet. Furthermore, the second valuation is conducted on the factory

outlet, which is for industrial purposes. The second valuation does not provide the adequate

returns, as the first valuation of residential plots. Therefore, the use of the plot for residential

purpose could directly allow the organisation to generate higher returns from investment

(Wang, 2016).

Question 2:

1. Depicting the journal entries of Peewee Ltd for the year ended 30 June 2017:

1st July

2016

Machine A...........................................................Dr

Machine B...........................................................Dr

Cash........................................................Cr

100,000

60,000

160,000

30th June

2017

Depreciation-Machine A................................................Dr

Accumulated Depreciation............................Cr

(1/5 * $100,000 = $20,000)

20,000

20,000

Depreciation-Machine B................................................Dr

Accumulated Depreciation.............................Cr

(1/3 * $60,000 = $20,000)

20,000

20,000

Accumulated Depreciation Machine A..........................Dr

Machine A...................................................Cr

20,000

20,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

4

(being writing down the carrying amount)

Machine A.................................................................Dr

Gain on revaluation of Machine A (OCI)........Cr

(being revaluation of increment $80,000 to $84,000)

4,000

4,000

Gain on revaluation of Machine A (OCI)........................Dr

Asset revaluation surplus Machine A..............Cr

(being increase in net revaluation gain in equity)

4,000

4,000

Accumulated Depreciation Machine B..........................Dr

Machine B...................................................Cr

(being writing down the carrying amount)

20,000

20,000

Loss on revaluation-Machine B....................................Dr

Machine B...................................................Cr

(being revaluation to fair value at 30-06-17)

2,000

2,000

2. Depositing the journal entries of Peewee Ltd for the year ended 30 June 2018:

1st

January

2018

Machine C..................................................................Dr

Cash...............................................................Cr

(being acquisition of machine C)

80,000

80,000

Depreciation expense-Machine B.................................Dr

Accumulated Depreciation............................Cr

(1/2 * 1/2 * $38,000 = $9,500)

9,500

9,500

Cash..........................................................................Dr

Proceeds from sale of Machine B....................Cr

(being received cash flow sale of Machine B)

29,000

29,000

4

(being writing down the carrying amount)

Machine A.................................................................Dr

Gain on revaluation of Machine A (OCI)........Cr

(being revaluation of increment $80,000 to $84,000)

4,000

4,000

Gain on revaluation of Machine A (OCI)........................Dr

Asset revaluation surplus Machine A..............Cr

(being increase in net revaluation gain in equity)

4,000

4,000

Accumulated Depreciation Machine B..........................Dr

Machine B...................................................Cr

(being writing down the carrying amount)

20,000

20,000

Loss on revaluation-Machine B....................................Dr

Machine B...................................................Cr

(being revaluation to fair value at 30-06-17)

2,000

2,000

2. Depositing the journal entries of Peewee Ltd for the year ended 30 June 2018:

1st

January

2018

Machine C..................................................................Dr

Cash...............................................................Cr

(being acquisition of machine C)

80,000

80,000

Depreciation expense-Machine B.................................Dr

Accumulated Depreciation............................Cr

(1/2 * 1/2 * $38,000 = $9,500)

9,500

9,500

Cash..........................................................................Dr

Proceeds from sale of Machine B....................Cr

(being received cash flow sale of Machine B)

29,000

29,000

FINANCIAL ACCOUNTING

5

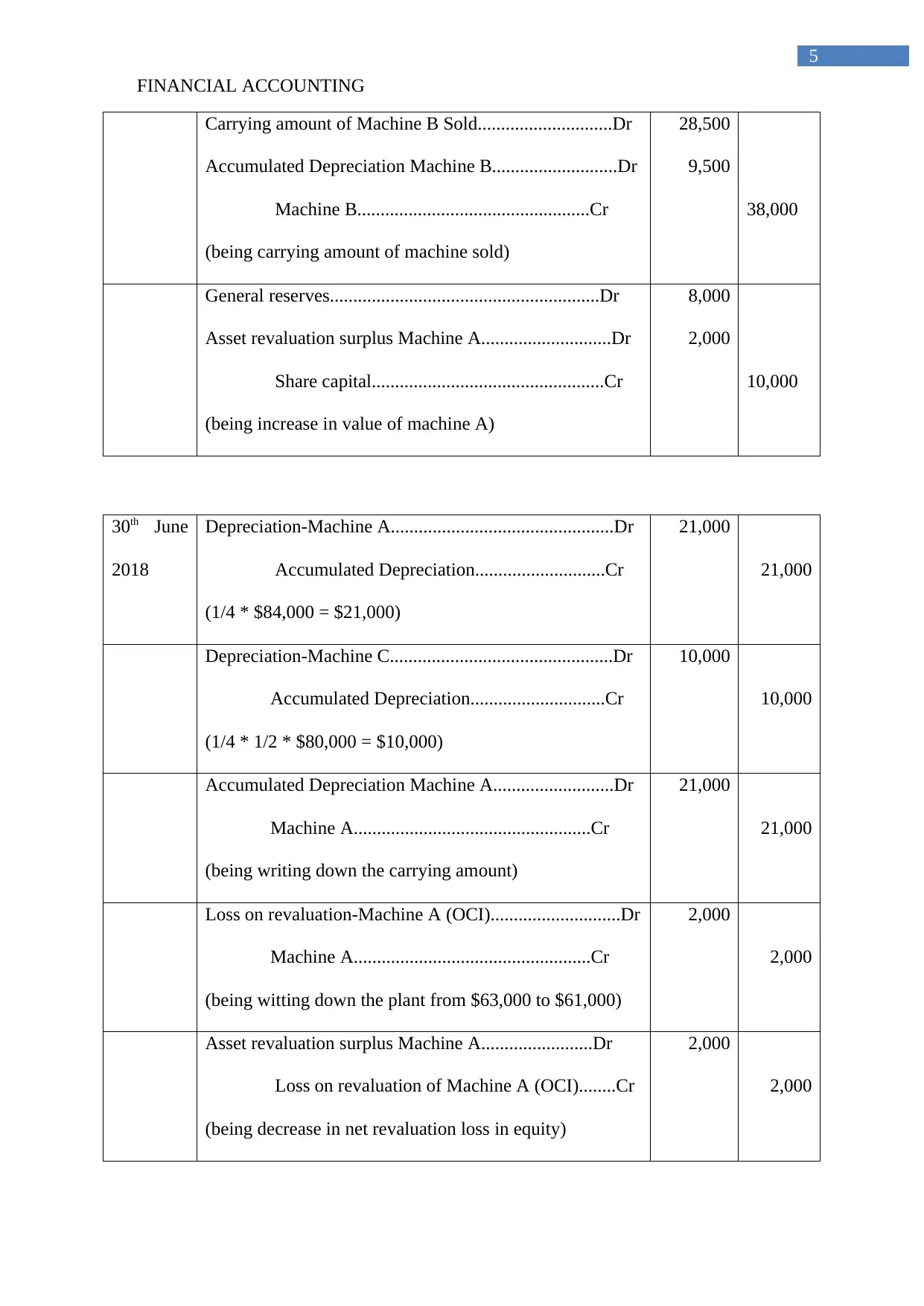

Carrying amount of Machine B Sold.............................Dr

Accumulated Depreciation Machine B...........................Dr

Machine B..................................................Cr

(being carrying amount of machine sold)

28,500

9,500

38,000

General reserves..........................................................Dr

Asset revaluation surplus Machine A............................Dr

Share capital..................................................Cr

(being increase in value of machine A)

8,000

2,000

10,000

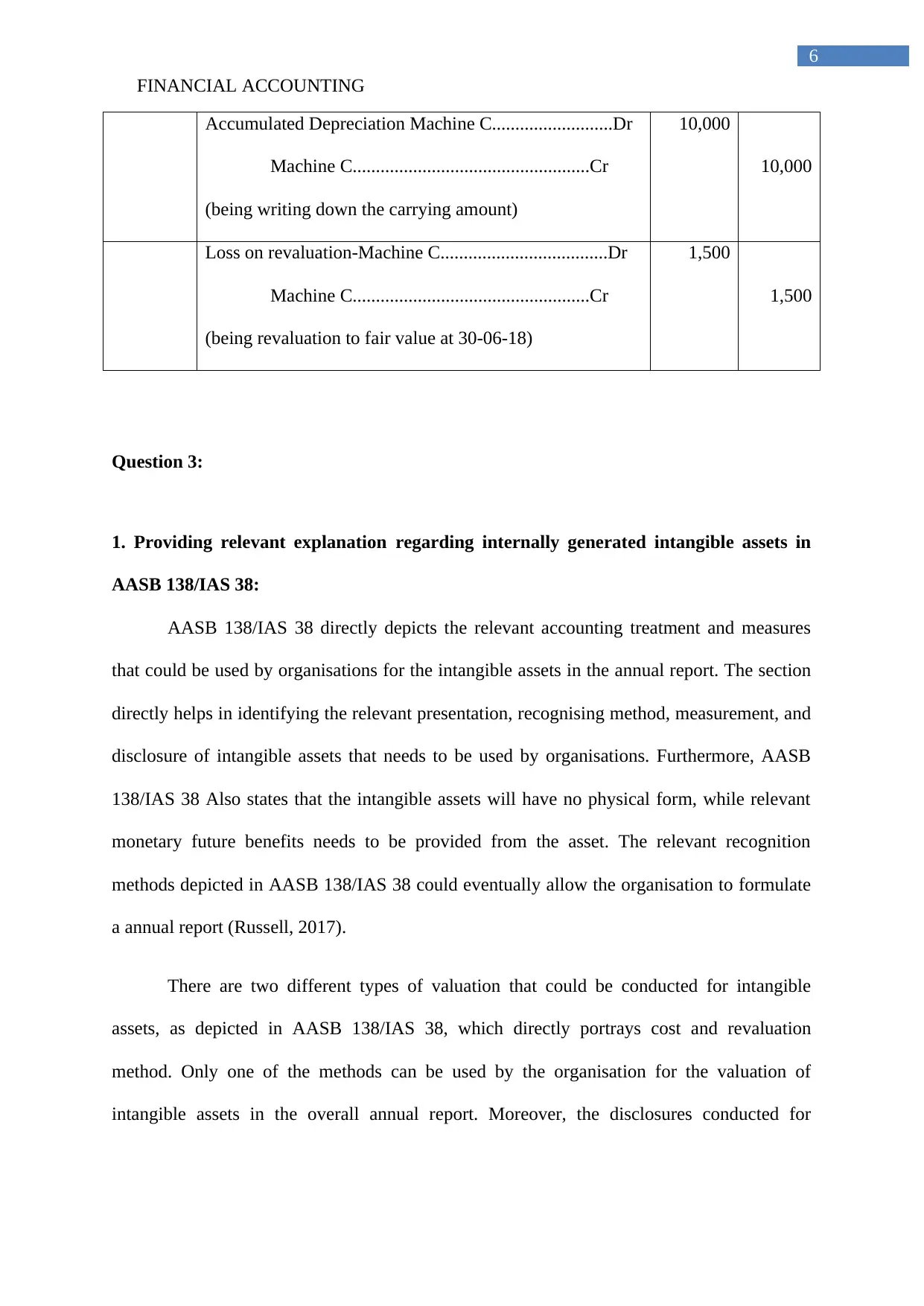

30th June

2018

Depreciation-Machine A................................................Dr

Accumulated Depreciation............................Cr

(1/4 * $84,000 = $21,000)

21,000

21,000

Depreciation-Machine C................................................Dr

Accumulated Depreciation.............................Cr

(1/4 * 1/2 * $80,000 = $10,000)

10,000

10,000

Accumulated Depreciation Machine A..........................Dr

Machine A...................................................Cr

(being writing down the carrying amount)

21,000

21,000

Loss on revaluation-Machine A (OCI)............................Dr

Machine A...................................................Cr

(being witting down the plant from $63,000 to $61,000)

2,000

2,000

Asset revaluation surplus Machine A........................Dr

Loss on revaluation of Machine A (OCI)........Cr

(being decrease in net revaluation loss in equity)

2,000

2,000

5

Carrying amount of Machine B Sold.............................Dr

Accumulated Depreciation Machine B...........................Dr

Machine B..................................................Cr

(being carrying amount of machine sold)

28,500

9,500

38,000

General reserves..........................................................Dr

Asset revaluation surplus Machine A............................Dr

Share capital..................................................Cr

(being increase in value of machine A)

8,000

2,000

10,000

30th June

2018

Depreciation-Machine A................................................Dr

Accumulated Depreciation............................Cr

(1/4 * $84,000 = $21,000)

21,000

21,000

Depreciation-Machine C................................................Dr

Accumulated Depreciation.............................Cr

(1/4 * 1/2 * $80,000 = $10,000)

10,000

10,000

Accumulated Depreciation Machine A..........................Dr

Machine A...................................................Cr

(being writing down the carrying amount)

21,000

21,000

Loss on revaluation-Machine A (OCI)............................Dr

Machine A...................................................Cr

(being witting down the plant from $63,000 to $61,000)

2,000

2,000

Asset revaluation surplus Machine A........................Dr

Loss on revaluation of Machine A (OCI)........Cr

(being decrease in net revaluation loss in equity)

2,000

2,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING

6

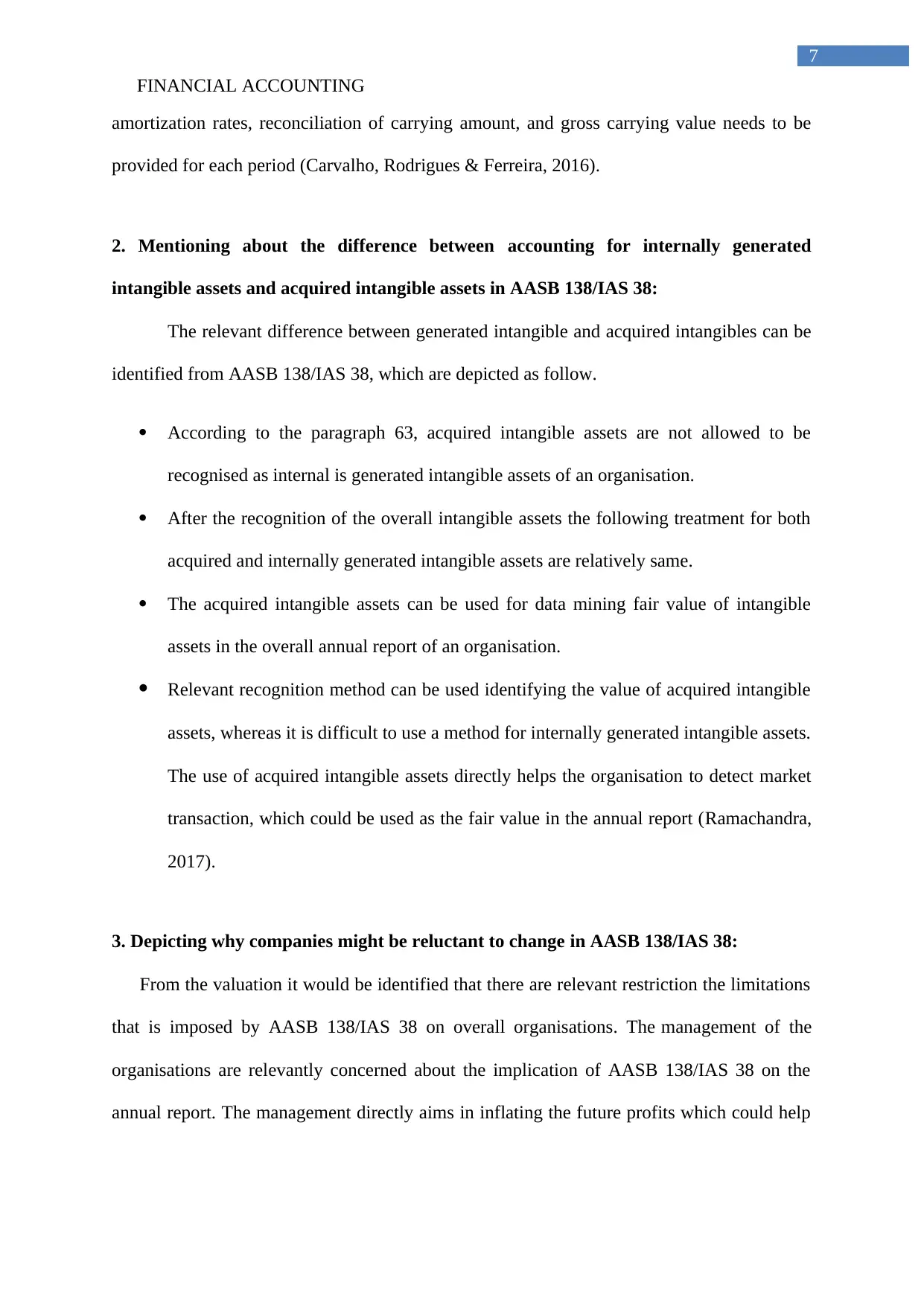

Accumulated Depreciation Machine C..........................Dr

Machine C...................................................Cr

(being writing down the carrying amount)

10,000

10,000

Loss on revaluation-Machine C....................................Dr

Machine C...................................................Cr

(being revaluation to fair value at 30-06-18)

1,500

1,500

Question 3:

1. Providing relevant explanation regarding internally generated intangible assets in

AASB 138/IAS 38:

AASB 138/IAS 38 directly depicts the relevant accounting treatment and measures

that could be used by organisations for the intangible assets in the annual report. The section

directly helps in identifying the relevant presentation, recognising method, measurement, and

disclosure of intangible assets that needs to be used by organisations. Furthermore, AASB

138/IAS 38 Also states that the intangible assets will have no physical form, while relevant

monetary future benefits needs to be provided from the asset. The relevant recognition

methods depicted in AASB 138/IAS 38 could eventually allow the organisation to formulate

a annual report (Russell, 2017).

There are two different types of valuation that could be conducted for intangible

assets, as depicted in AASB 138/IAS 38, which directly portrays cost and revaluation

method. Only one of the methods can be used by the organisation for the valuation of

intangible assets in the overall annual report. Moreover, the disclosures conducted for

6

Accumulated Depreciation Machine C..........................Dr

Machine C...................................................Cr

(being writing down the carrying amount)

10,000

10,000

Loss on revaluation-Machine C....................................Dr

Machine C...................................................Cr

(being revaluation to fair value at 30-06-18)

1,500

1,500

Question 3:

1. Providing relevant explanation regarding internally generated intangible assets in

AASB 138/IAS 38:

AASB 138/IAS 38 directly depicts the relevant accounting treatment and measures

that could be used by organisations for the intangible assets in the annual report. The section

directly helps in identifying the relevant presentation, recognising method, measurement, and

disclosure of intangible assets that needs to be used by organisations. Furthermore, AASB

138/IAS 38 Also states that the intangible assets will have no physical form, while relevant

monetary future benefits needs to be provided from the asset. The relevant recognition

methods depicted in AASB 138/IAS 38 could eventually allow the organisation to formulate

a annual report (Russell, 2017).

There are two different types of valuation that could be conducted for intangible

assets, as depicted in AASB 138/IAS 38, which directly portrays cost and revaluation

method. Only one of the methods can be used by the organisation for the valuation of

intangible assets in the overall annual report. Moreover, the disclosures conducted for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

7

amortization rates, reconciliation of carrying amount, and gross carrying value needs to be

provided for each period (Carvalho, Rodrigues & Ferreira, 2016).

2. Mentioning about the difference between accounting for internally generated

intangible assets and acquired intangible assets in AASB 138/IAS 38:

The relevant difference between generated intangible and acquired intangibles can be

identified from AASB 138/IAS 38, which are depicted as follow.

According to the paragraph 63, acquired intangible assets are not allowed to be

recognised as internal is generated intangible assets of an organisation.

After the recognition of the overall intangible assets the following treatment for both

acquired and internally generated intangible assets are relatively same.

The acquired intangible assets can be used for data mining fair value of intangible

assets in the overall annual report of an organisation.

Relevant recognition method can be used identifying the value of acquired intangible

assets, whereas it is difficult to use a method for internally generated intangible assets.

The use of acquired intangible assets directly helps the organisation to detect market

transaction, which could be used as the fair value in the annual report (Ramachandra,

2017).

3. Depicting why companies might be reluctant to change in AASB 138/IAS 38:

From the valuation it would be identified that there are relevant restriction the limitations

that is imposed by AASB 138/IAS 38 on overall organisations. The management of the

organisations are relevantly concerned about the implication of AASB 138/IAS 38 on the

annual report. The management directly aims in inflating the future profits which could help

7

amortization rates, reconciliation of carrying amount, and gross carrying value needs to be

provided for each period (Carvalho, Rodrigues & Ferreira, 2016).

2. Mentioning about the difference between accounting for internally generated

intangible assets and acquired intangible assets in AASB 138/IAS 38:

The relevant difference between generated intangible and acquired intangibles can be

identified from AASB 138/IAS 38, which are depicted as follow.

According to the paragraph 63, acquired intangible assets are not allowed to be

recognised as internal is generated intangible assets of an organisation.

After the recognition of the overall intangible assets the following treatment for both

acquired and internally generated intangible assets are relatively same.

The acquired intangible assets can be used for data mining fair value of intangible

assets in the overall annual report of an organisation.

Relevant recognition method can be used identifying the value of acquired intangible

assets, whereas it is difficult to use a method for internally generated intangible assets.

The use of acquired intangible assets directly helps the organisation to detect market

transaction, which could be used as the fair value in the annual report (Ramachandra,

2017).

3. Depicting why companies might be reluctant to change in AASB 138/IAS 38:

From the valuation it would be identified that there are relevant restriction the limitations

that is imposed by AASB 138/IAS 38 on overall organisations. The management of the

organisations are relevantly concerned about the implication of AASB 138/IAS 38 on the

annual report. The management directly aims in inflating the future profits which could help

FINANCIAL ACCOUNTING

8

in luring in more investors. The overall restriction that is been imposed on organisation by

AASB 138/IAS 38 are depicted as follows.

In paragraph 63 there is relevant instructions regarding intangible assets recognition

method as internally generated publishing titles, customer list, mastheads, and brand

is restricted from being listed in the intangible assets criteria.

The paragraph 57 directly states that internally generated intangible assets valuation

does not allow upper limit of capitalisation.

Relevant limitations are also imposed on identifying or defining the intangible assets,

as reputation, labour relations, customer relationship, and human resource are not

considered to be intangible assets that could be listed by the organisation in the annual

report.

AASB 138/IAS 38 directly indicates the overall intangible assets can be valued under

the revaluation method which could help in identifying the fair value conditions of an

asset (Aasb.gov.au, 2017).

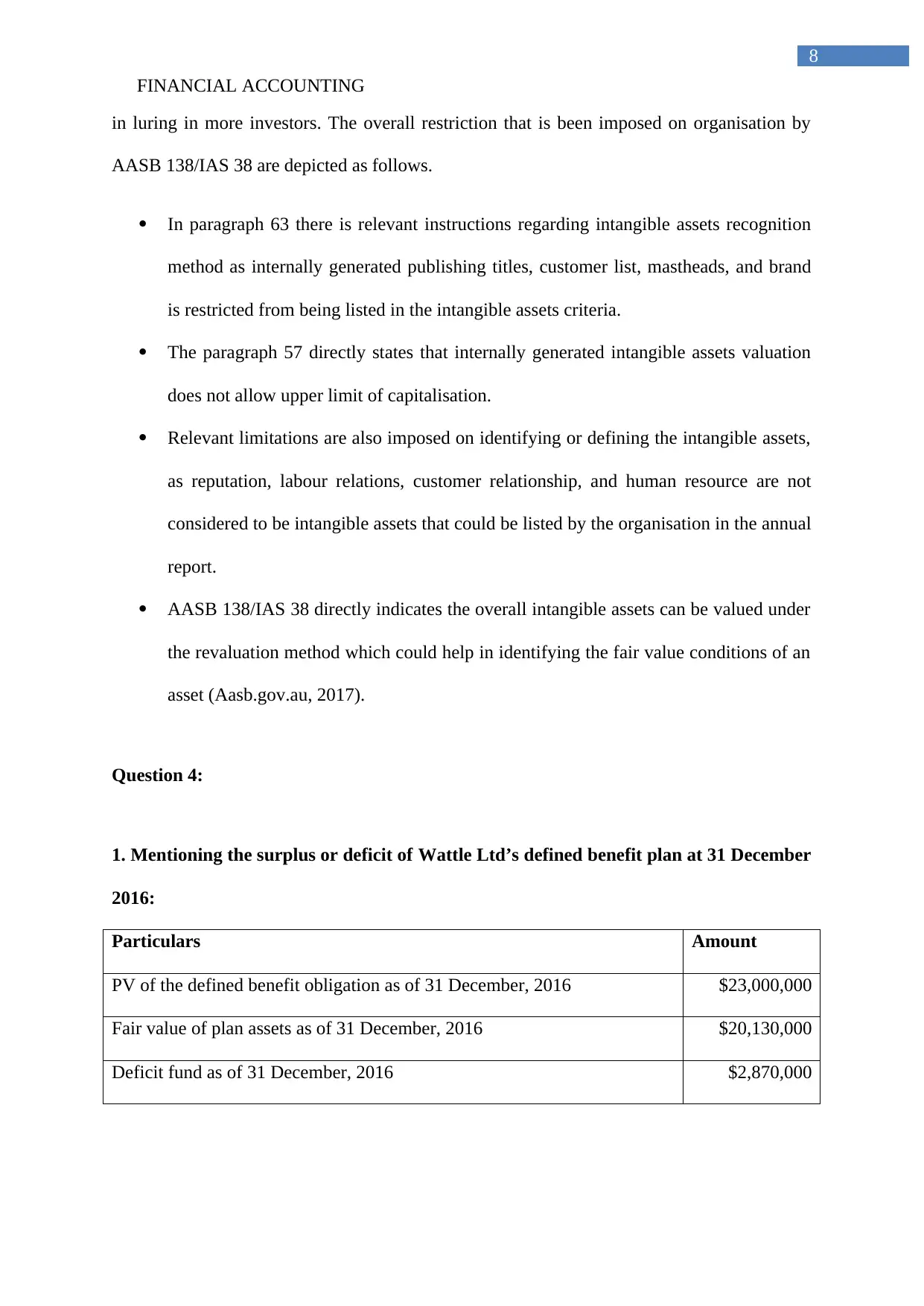

Question 4:

1. Mentioning the surplus or deficit of Wattle Ltd’s defined benefit plan at 31 December

2016:

Particulars Amount

PV of the defined benefit obligation as of 31 December, 2016 $23,000,000

Fair value of plan assets as of 31 December, 2016 $20,130,000

Deficit fund as of 31 December, 2016 $2,870,000

8

in luring in more investors. The overall restriction that is been imposed on organisation by

AASB 138/IAS 38 are depicted as follows.

In paragraph 63 there is relevant instructions regarding intangible assets recognition

method as internally generated publishing titles, customer list, mastheads, and brand

is restricted from being listed in the intangible assets criteria.

The paragraph 57 directly states that internally generated intangible assets valuation

does not allow upper limit of capitalisation.

Relevant limitations are also imposed on identifying or defining the intangible assets,

as reputation, labour relations, customer relationship, and human resource are not

considered to be intangible assets that could be listed by the organisation in the annual

report.

AASB 138/IAS 38 directly indicates the overall intangible assets can be valued under

the revaluation method which could help in identifying the fair value conditions of an

asset (Aasb.gov.au, 2017).

Question 4:

1. Mentioning the surplus or deficit of Wattle Ltd’s defined benefit plan at 31 December

2016:

Particulars Amount

PV of the defined benefit obligation as of 31 December, 2016 $23,000,000

Fair value of plan assets as of 31 December, 2016 $20,130,000

Deficit fund as of 31 December, 2016 $2,870,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING

9

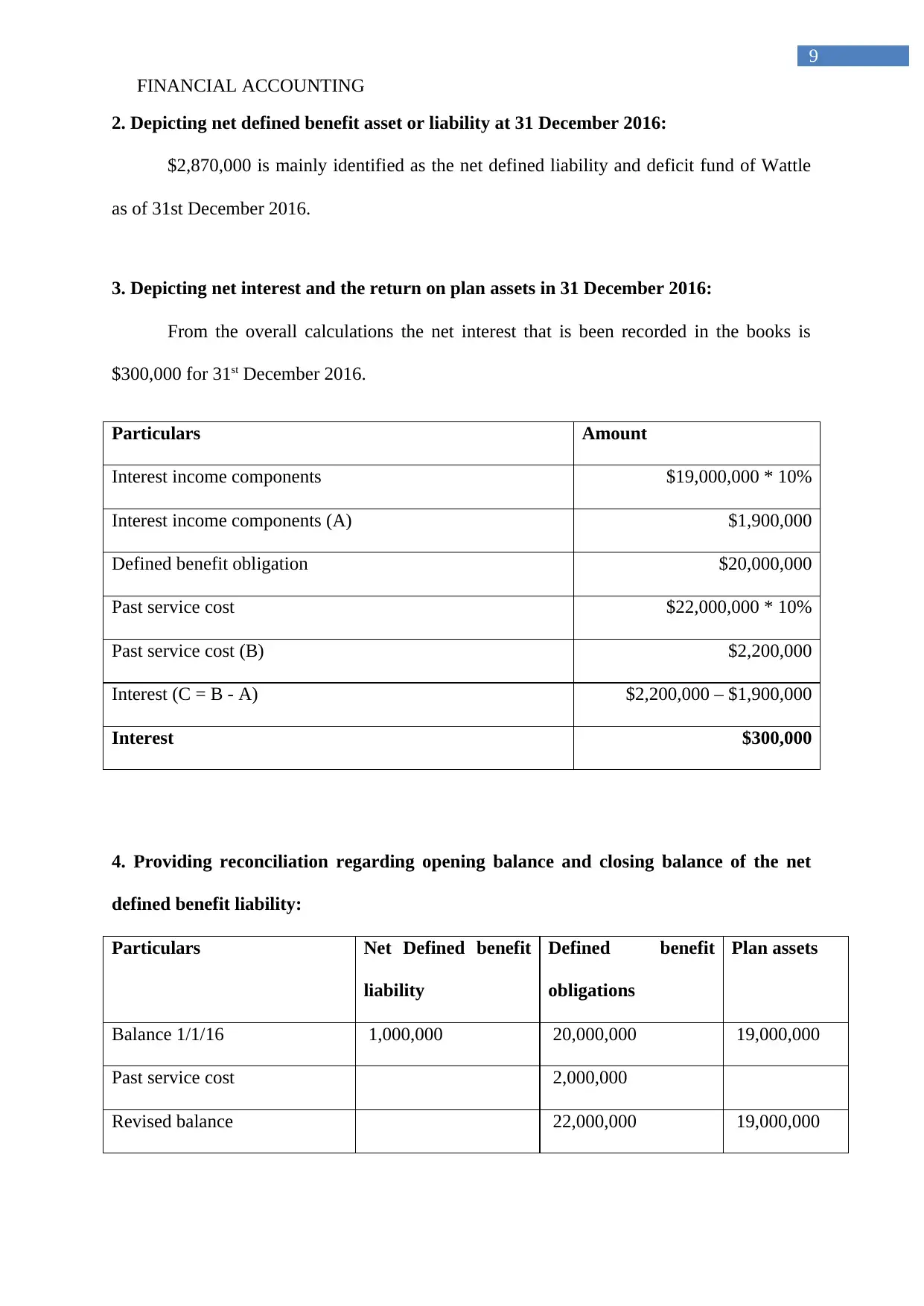

2. Depicting net defined benefit asset or liability at 31 December 2016:

$2,870,000 is mainly identified as the net defined liability and deficit fund of Wattle

as of 31st December 2016.

3. Depicting net interest and the return on plan assets in 31 December 2016:

From the overall calculations the net interest that is been recorded in the books is

$300,000 for 31st December 2016.

Particulars Amount

Interest income components $19,000,000 * 10%

Interest income components (A) $1,900,000

Defined benefit obligation $20,000,000

Past service cost $22,000,000 * 10%

Past service cost (B) $2,200,000

Interest (C = B - A) $2,200,000 – $1,900,000

Interest $300,000

4. Providing reconciliation regarding opening balance and closing balance of the net

defined benefit liability:

Particulars Net Defined benefit

liability

Defined benefit

obligations

Plan assets

Balance 1/1/16 1,000,000 20,000,000 19,000,000

Past service cost 2,000,000

Revised balance 22,000,000 19,000,000

9

2. Depicting net defined benefit asset or liability at 31 December 2016:

$2,870,000 is mainly identified as the net defined liability and deficit fund of Wattle

as of 31st December 2016.

3. Depicting net interest and the return on plan assets in 31 December 2016:

From the overall calculations the net interest that is been recorded in the books is

$300,000 for 31st December 2016.

Particulars Amount

Interest income components $19,000,000 * 10%

Interest income components (A) $1,900,000

Defined benefit obligation $20,000,000

Past service cost $22,000,000 * 10%

Past service cost (B) $2,200,000

Interest (C = B - A) $2,200,000 – $1,900,000

Interest $300,000

4. Providing reconciliation regarding opening balance and closing balance of the net

defined benefit liability:

Particulars Net Defined benefit

liability

Defined benefit

obligations

Plan assets

Balance 1/1/16 1,000,000 20,000,000 19,000,000

Past service cost 2,000,000

Revised balance 22,000,000 19,000,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

10

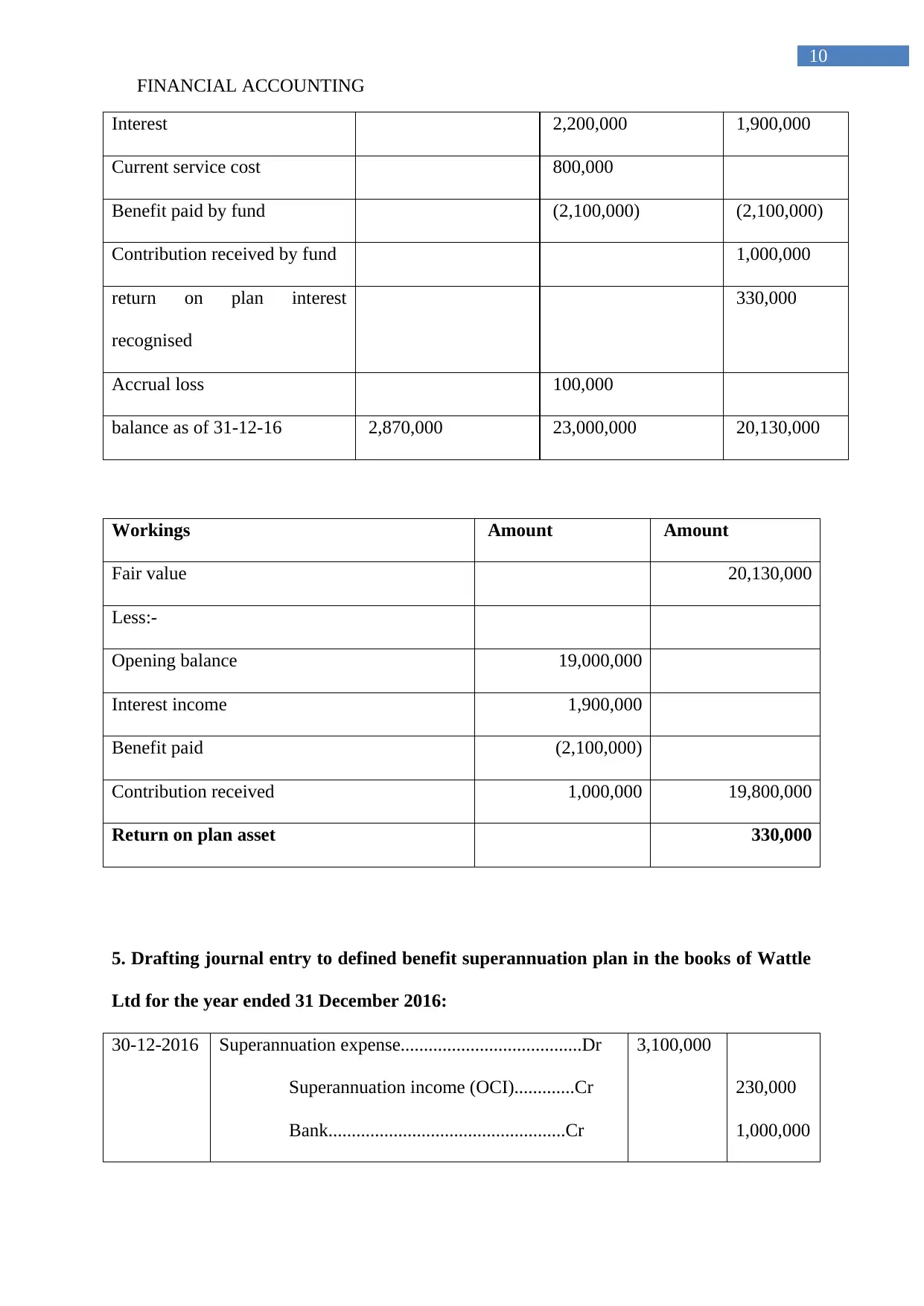

Interest 2,200,000 1,900,000

Current service cost 800,000

Benefit paid by fund (2,100,000) (2,100,000)

Contribution received by fund 1,000,000

return on plan interest

recognised

330,000

Accrual loss 100,000

balance as of 31-12-16 2,870,000 23,000,000 20,130,000

Workings Amount Amount

Fair value 20,130,000

Less:-

Opening balance 19,000,000

Interest income 1,900,000

Benefit paid (2,100,000)

Contribution received 1,000,000 19,800,000

Return on plan asset 330,000

5. Drafting journal entry to defined benefit superannuation plan in the books of Wattle

Ltd for the year ended 31 December 2016:

30-12-2016 Superannuation expense.......................................Dr

Superannuation income (OCI).............Cr

Bank...................................................Cr

3,100,000

230,000

1,000,000

10

Interest 2,200,000 1,900,000

Current service cost 800,000

Benefit paid by fund (2,100,000) (2,100,000)

Contribution received by fund 1,000,000

return on plan interest

recognised

330,000

Accrual loss 100,000

balance as of 31-12-16 2,870,000 23,000,000 20,130,000

Workings Amount Amount

Fair value 20,130,000

Less:-

Opening balance 19,000,000

Interest income 1,900,000

Benefit paid (2,100,000)

Contribution received 1,000,000 19,800,000

Return on plan asset 330,000

5. Drafting journal entry to defined benefit superannuation plan in the books of Wattle

Ltd for the year ended 31 December 2016:

30-12-2016 Superannuation expense.......................................Dr

Superannuation income (OCI).............Cr

Bank...................................................Cr

3,100,000

230,000

1,000,000

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.