University Financial Accounting Assignment Solution and Analysis

VerifiedAdded on 2020/05/11

|13

|1589

|45

Homework Assignment

AI Summary

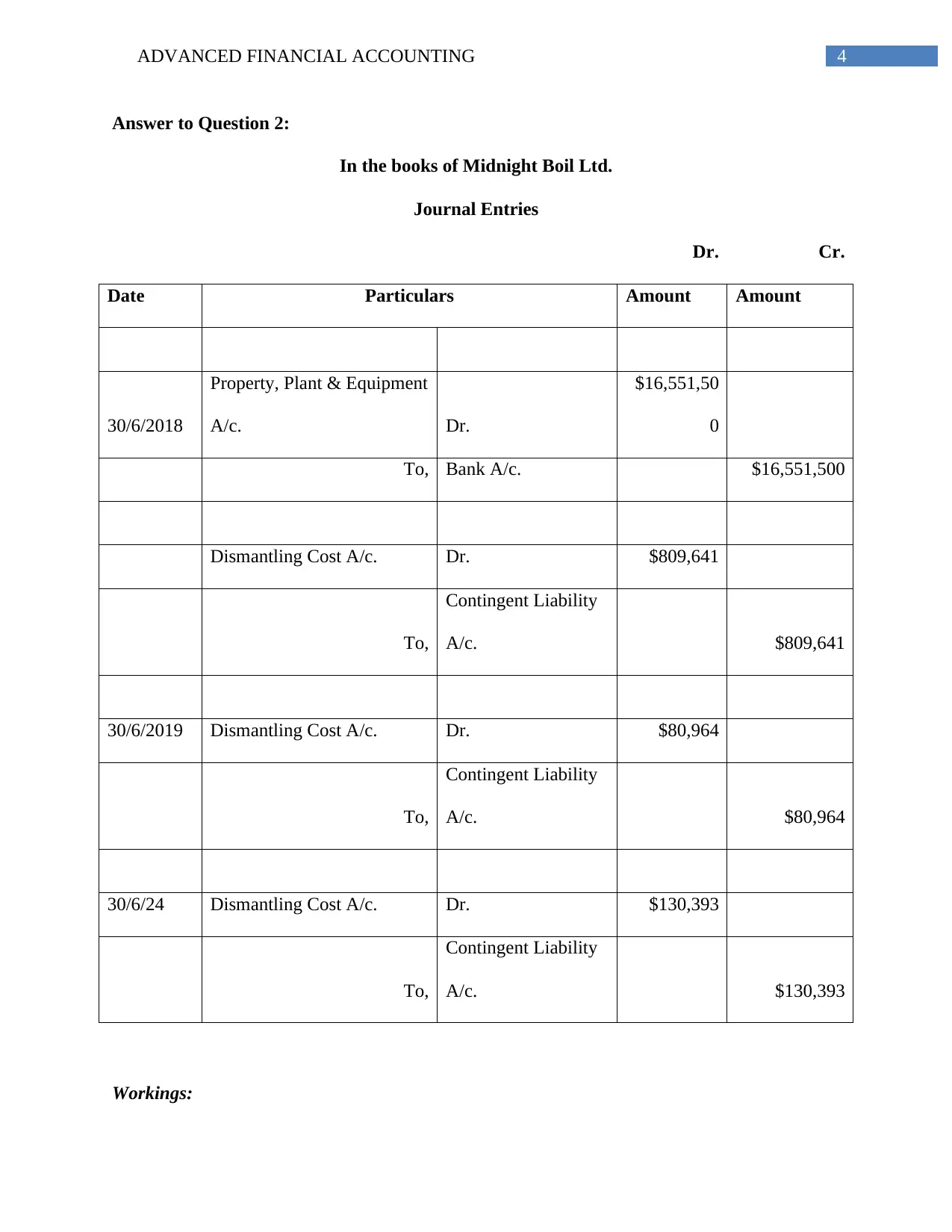

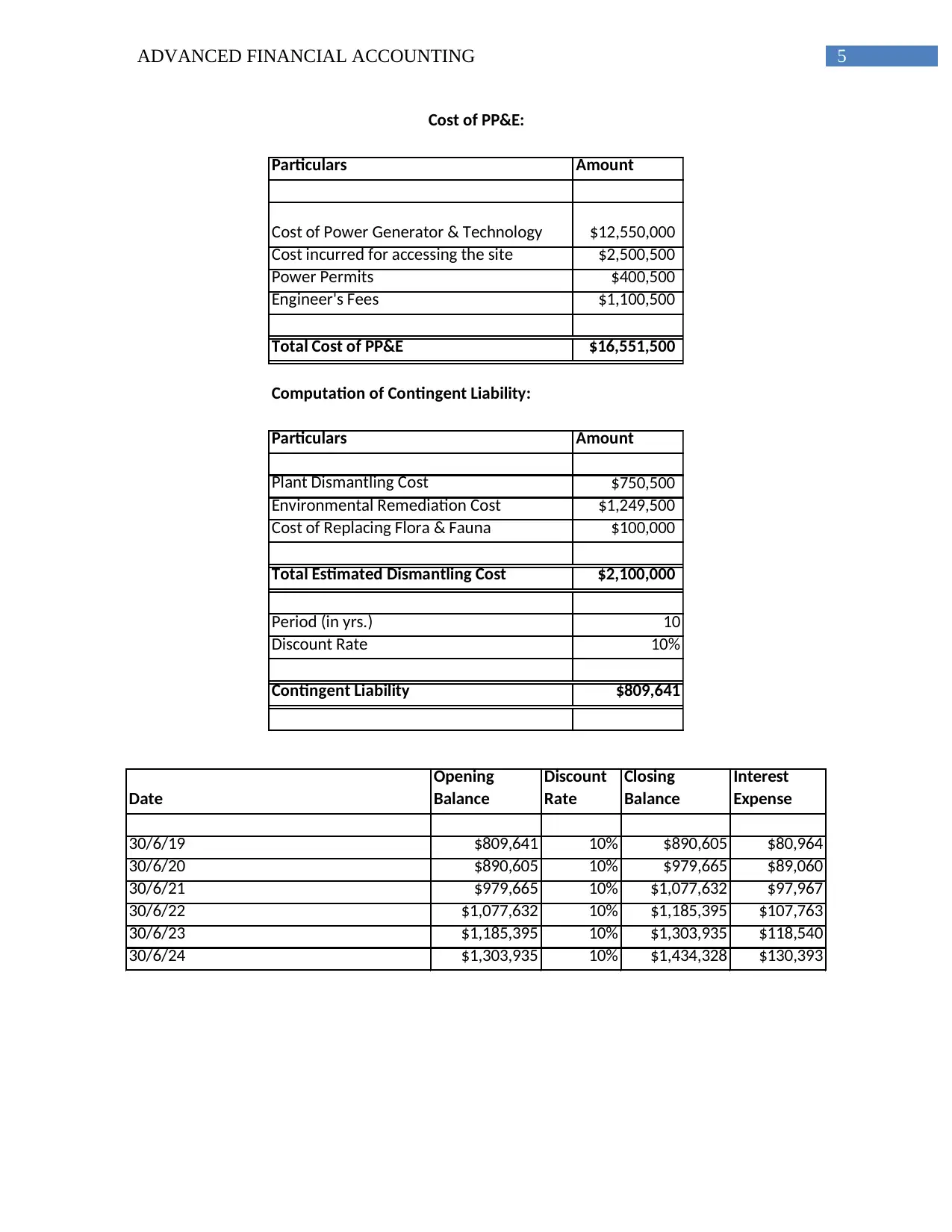

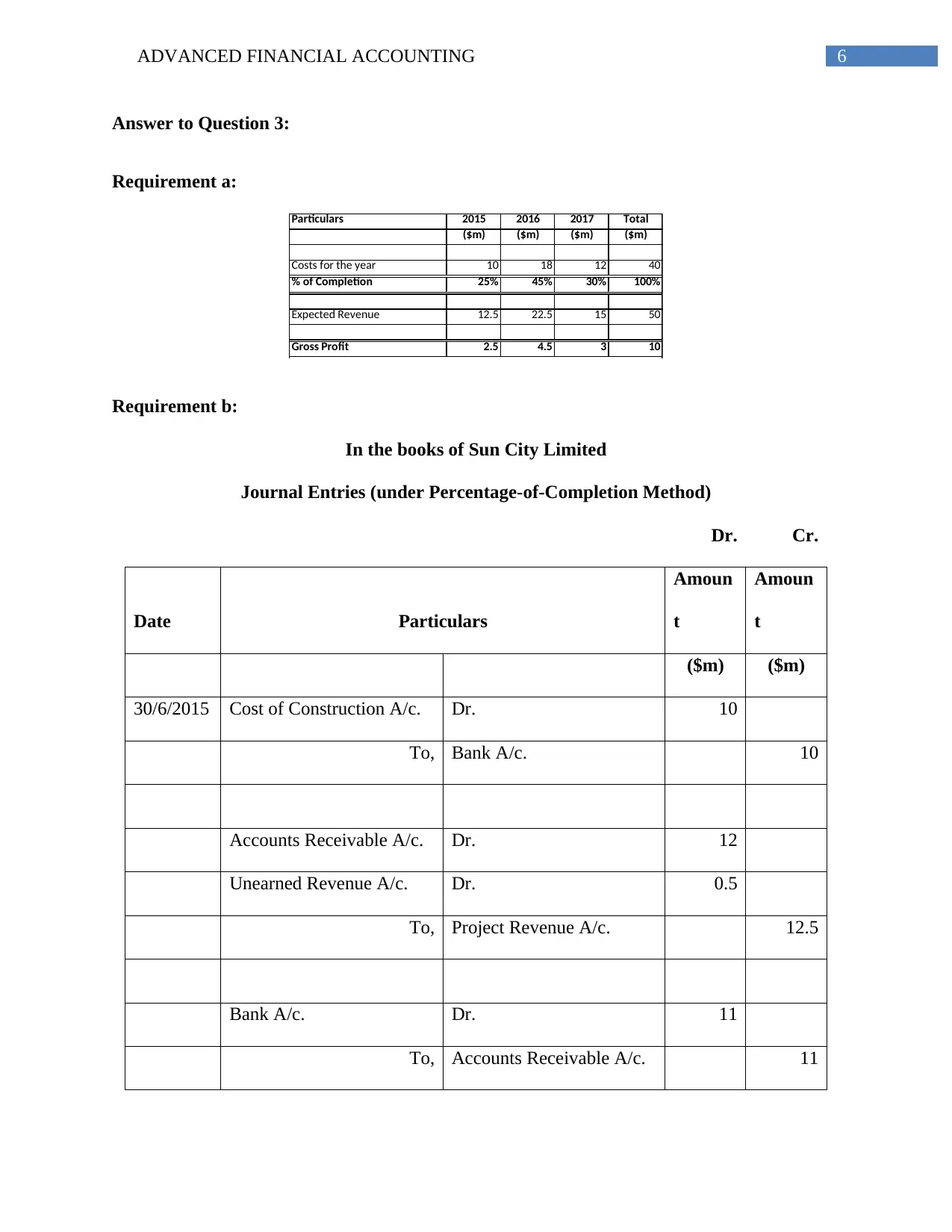

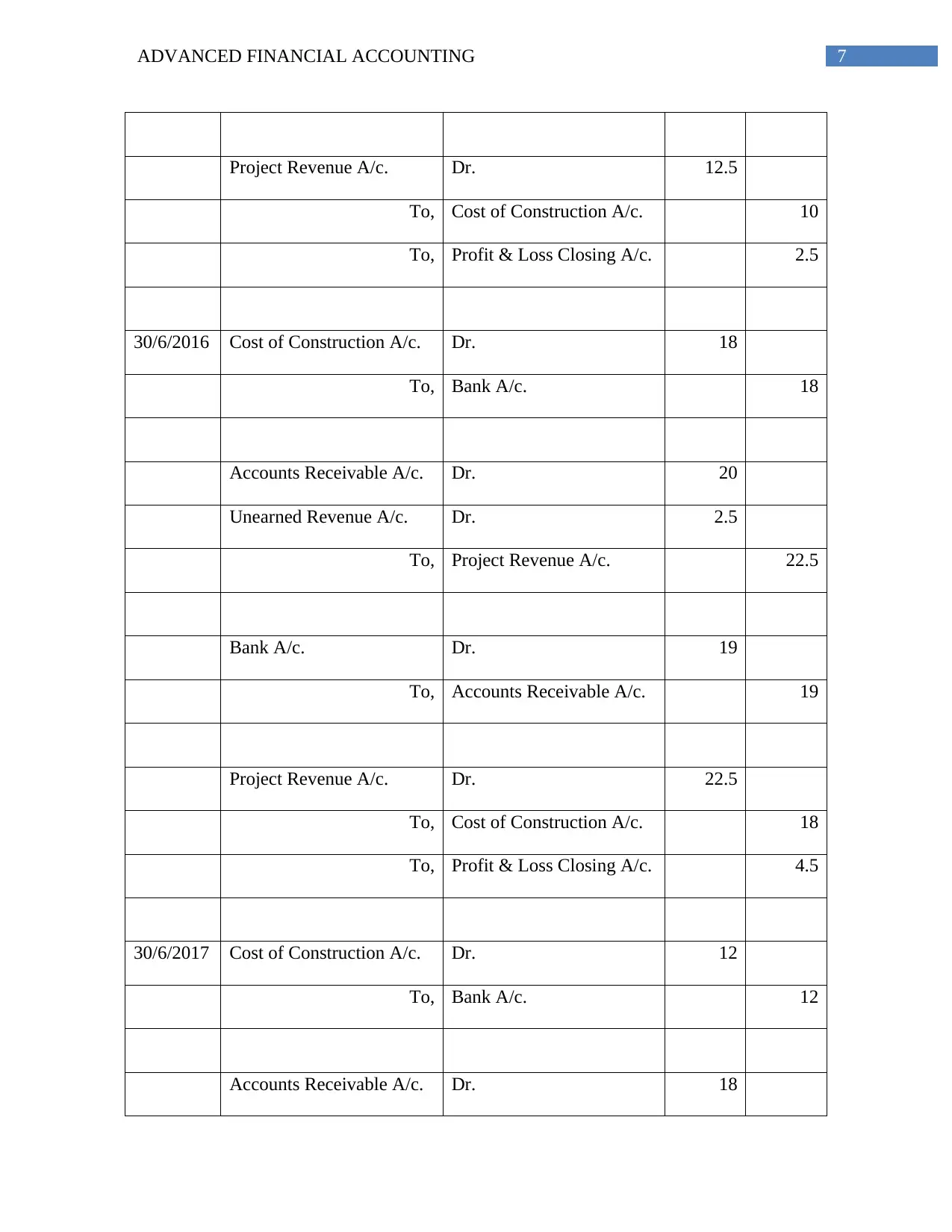

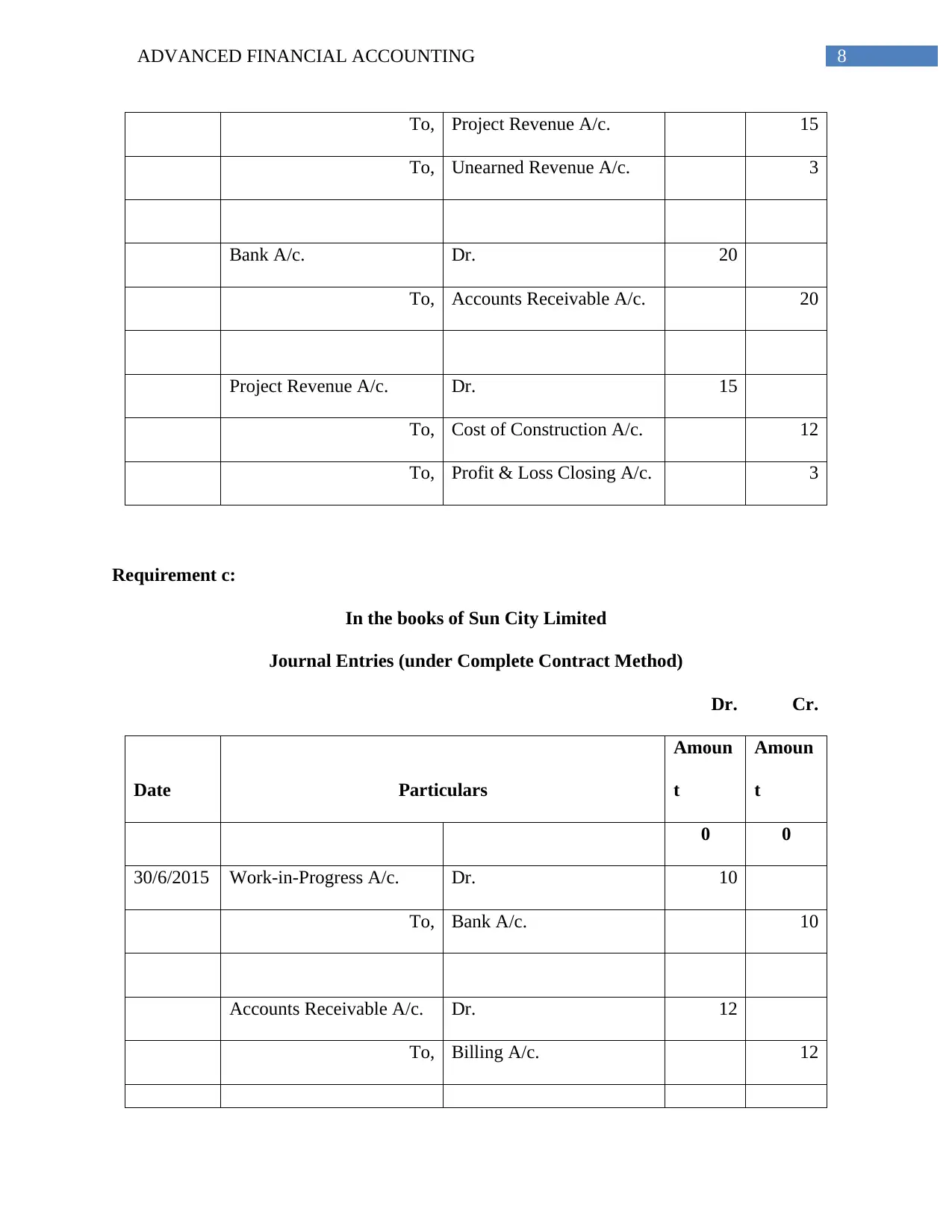

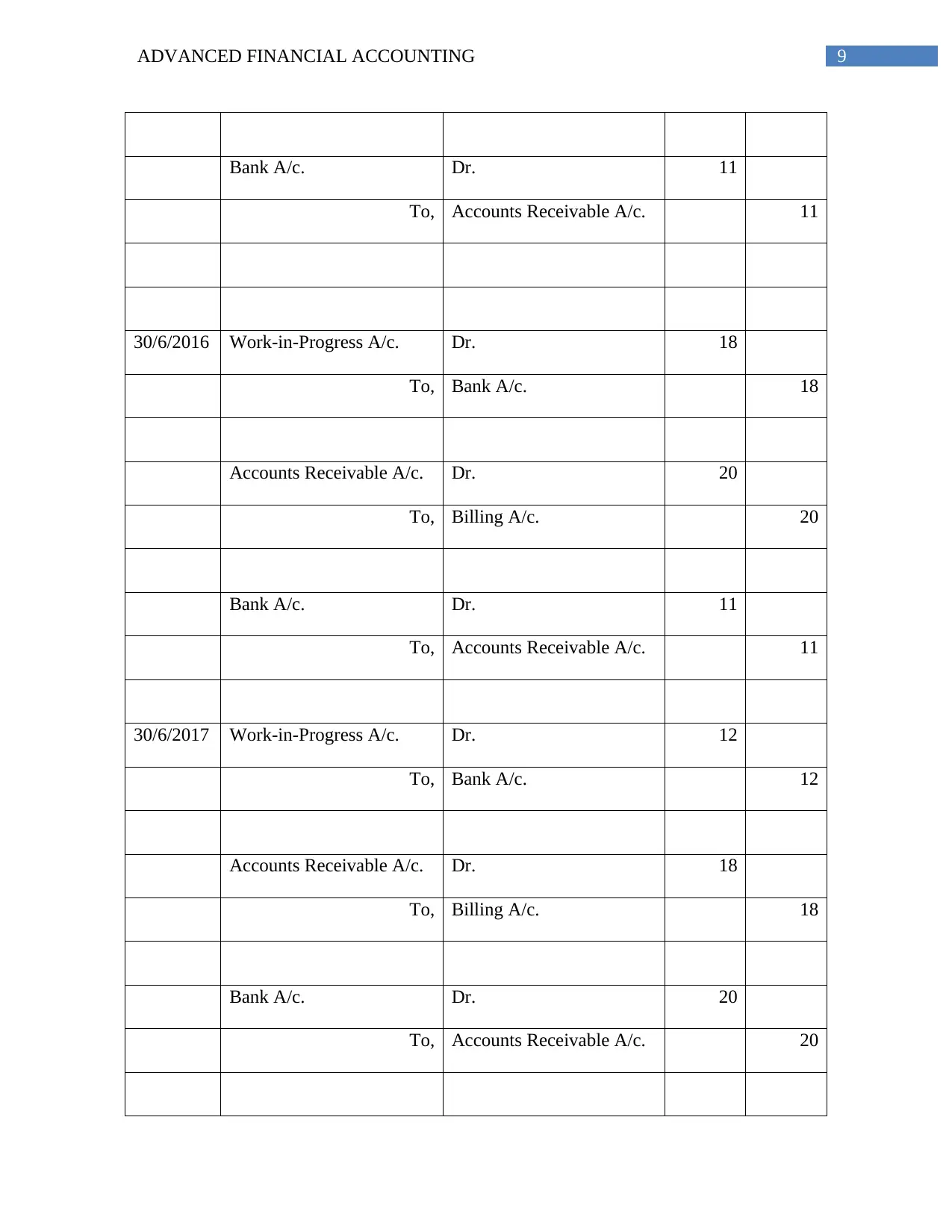

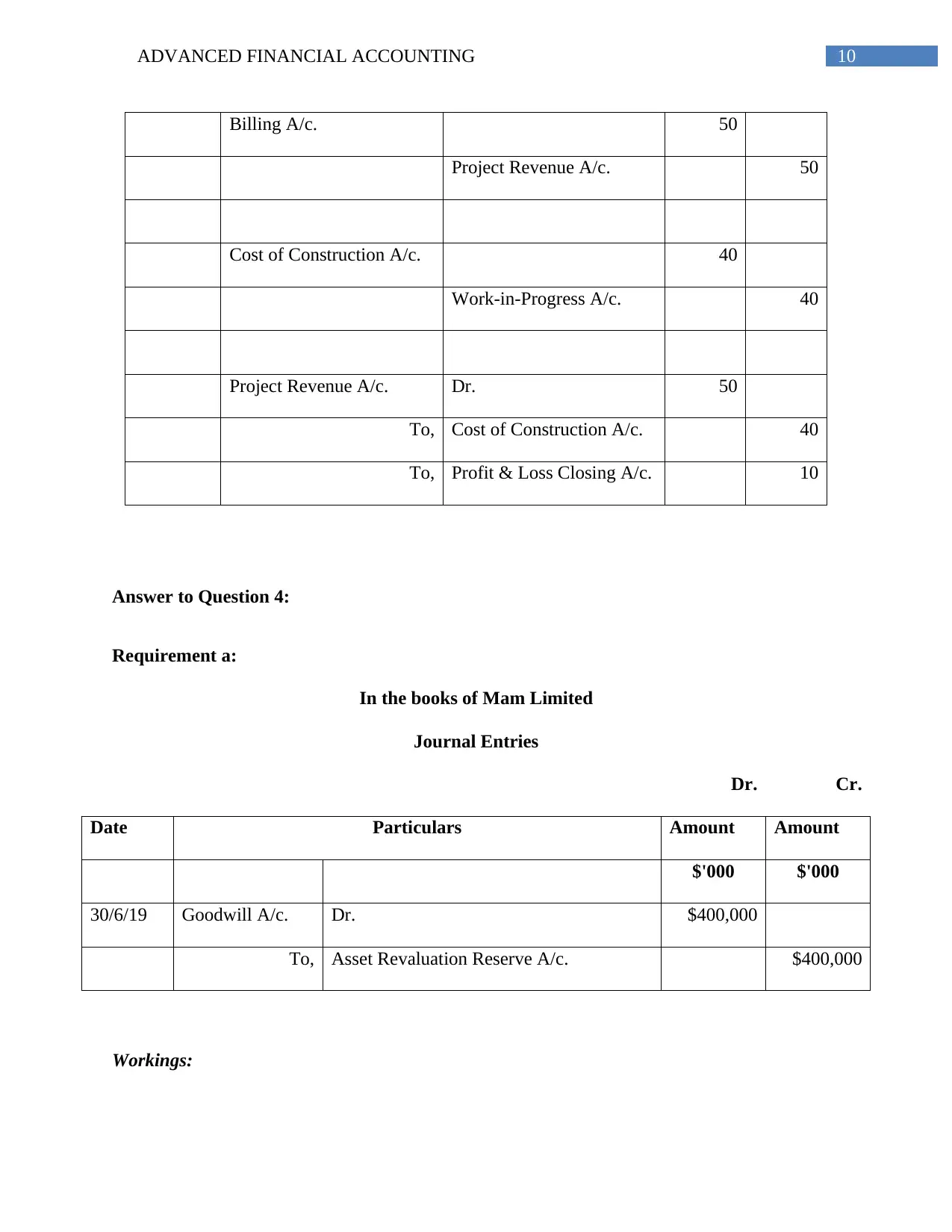

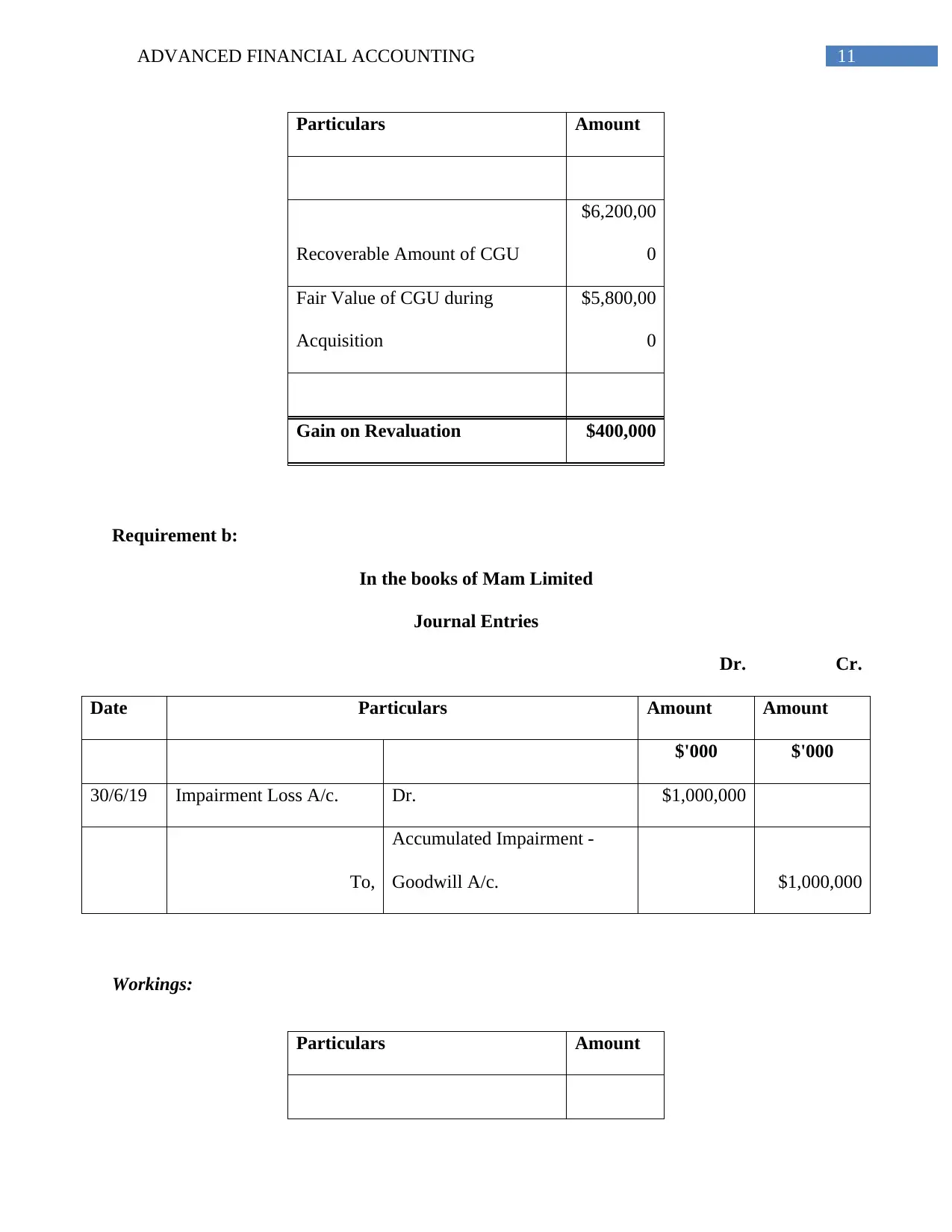

This document presents a comprehensive solution to an advanced financial accounting assignment. It begins by addressing depreciation, outlining the necessary information for a new accountant to compute it, including date placed in service, acquisition value, salvage value, estimated useful life, and depreciation methods. The assignment then proceeds with detailed journal entries for specific scenarios involving property, plant, and equipment, followed by an in-depth analysis of contract accounting, comparing the percentage-of-completion method and the completed contract method. The solution further explores goodwill and impairment losses, providing journal entries and calculations. The assignment incorporates various financial accounting concepts and principles, offering a complete and practical guide to solving complex financial accounting problems.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.