Financial Accounting Assignment Solution for Students

VerifiedAdded on 2020/06/03

|31

|2925

|245

Homework Assignment

AI Summary

This financial accounting assignment provides a comprehensive overview of key concepts and principles. It begins with a definition of financial accounting and its regulations, followed by an explanation of accounting rules and principles, including consistency and material disclosure. The assignment delves into practical applications, including the preparation of books of prime entry, ledger postings, and trial balances. It also includes profit and loss statements, balance sheets, and bank reconciliation statements for different clients. Furthermore, it explores depreciation methods, control accounts, and suspense accounts. The assignment concludes with journal entries and a discussion of the concepts of consistency and prudence, providing a solid foundation in financial accounting for students.

FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Assignment A...................................................................................................................................1

1. Defining Financial Accounting...............................................................................................1

2. Regulations of financial accounting........................................................................................2

3. Accounting rules and principles..............................................................................................2

4. Consistency and material disclosure with respect to concepts and conventions.....................3

ASSIGNMENT B............................................................................................................................4

CLIENT 1........................................................................................................................................4

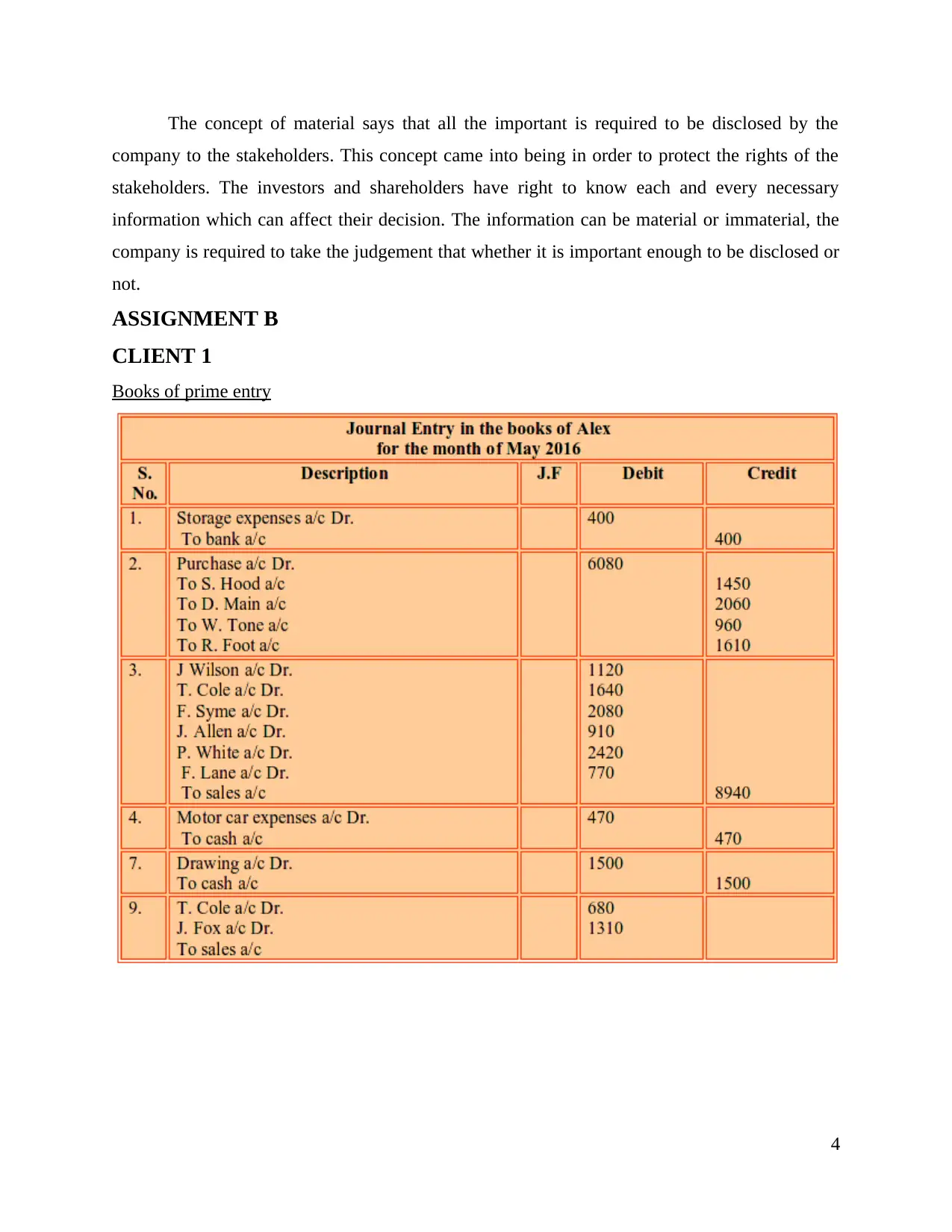

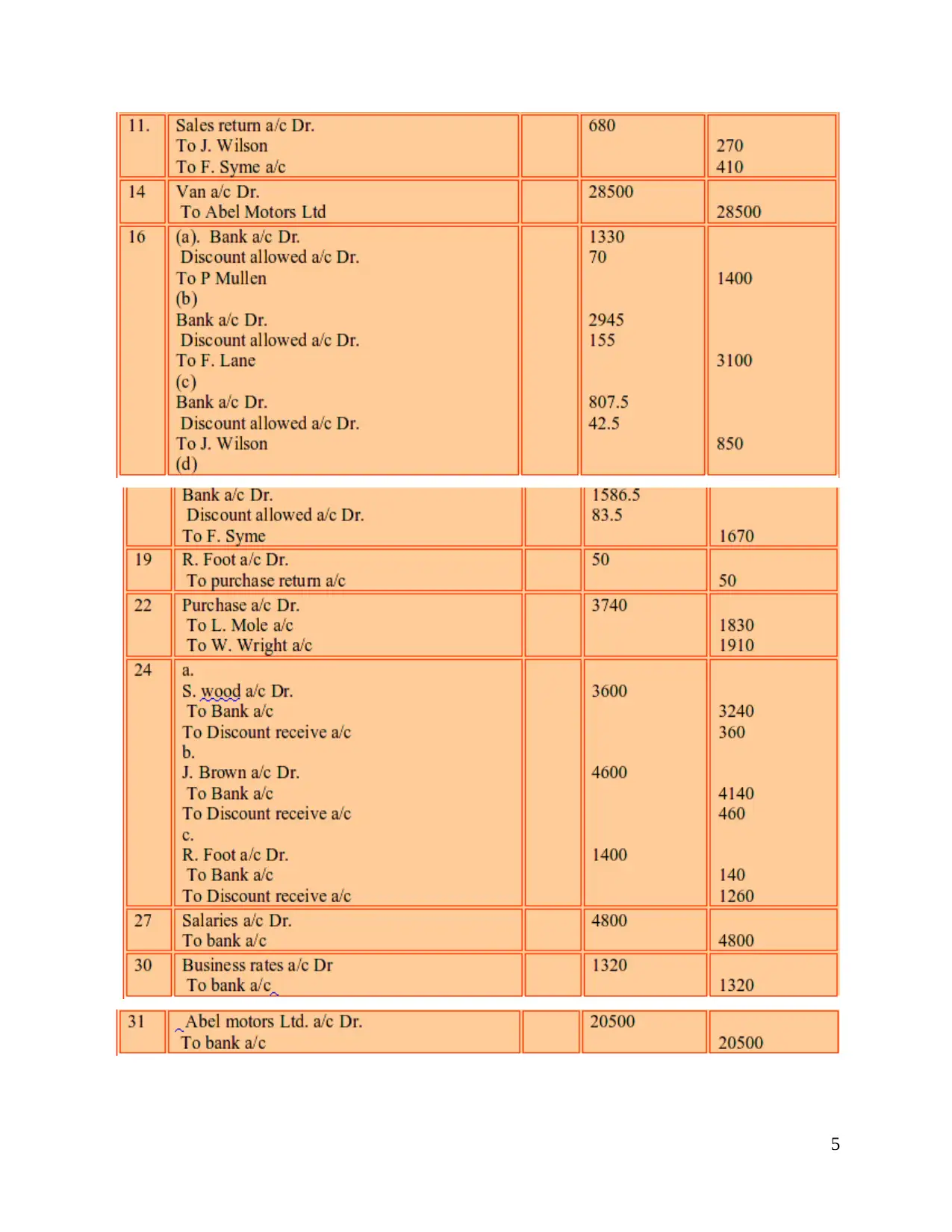

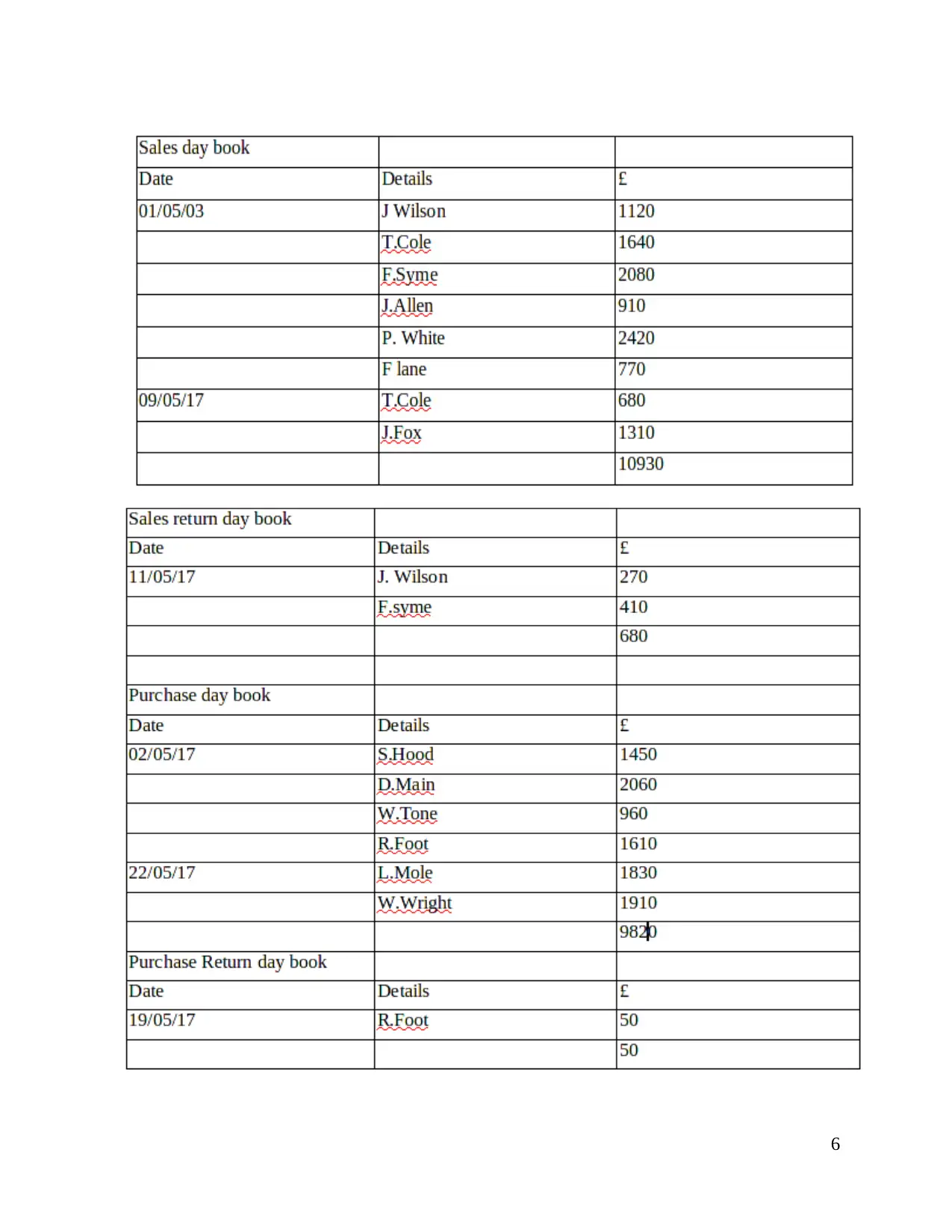

Books of prime entry...................................................................................................................4

Ledger book posting....................................................................................................................7

Trial balance..............................................................................................................................12

CLIENT 2......................................................................................................................................13

Profit and Loss Statement for Peter Piper as on 31st December 2016......................................14

Balance Sheet for Peter Piper as at 31st December 2016.........................................................15

CLIENT 3......................................................................................................................................16

Balance Sheet for Raintree ltd. As on 30 September 2016.......................................................17

c) Consistency and Prudence concepts.....................................................................................19

d) Purpose and methods of depreciation in formulating accounting statements.......................19

CLIENT 4......................................................................................................................................20

a) Reason of preparation for Bank reconciliation statement.....................................................20

b) Areas causing discrepancy in records...................................................................................20

c) BRS as on 1st December 2016..............................................................................................20

Cash book .................................................................................................................................21

BRS...........................................................................................................................................21

CLIENT 5......................................................................................................................................22

a) Books of Henderson for May 2016.......................................................................................22

Sales Ledger account.................................................................................................................22

Purchase ledger control Account..............................................................................................23

b) Describing 'Control Account'................................................................................................24

INTRODUCTION...........................................................................................................................1

Assignment A...................................................................................................................................1

1. Defining Financial Accounting...............................................................................................1

2. Regulations of financial accounting........................................................................................2

3. Accounting rules and principles..............................................................................................2

4. Consistency and material disclosure with respect to concepts and conventions.....................3

ASSIGNMENT B............................................................................................................................4

CLIENT 1........................................................................................................................................4

Books of prime entry...................................................................................................................4

Ledger book posting....................................................................................................................7

Trial balance..............................................................................................................................12

CLIENT 2......................................................................................................................................13

Profit and Loss Statement for Peter Piper as on 31st December 2016......................................14

Balance Sheet for Peter Piper as at 31st December 2016.........................................................15

CLIENT 3......................................................................................................................................16

Balance Sheet for Raintree ltd. As on 30 September 2016.......................................................17

c) Consistency and Prudence concepts.....................................................................................19

d) Purpose and methods of depreciation in formulating accounting statements.......................19

CLIENT 4......................................................................................................................................20

a) Reason of preparation for Bank reconciliation statement.....................................................20

b) Areas causing discrepancy in records...................................................................................20

c) BRS as on 1st December 2016..............................................................................................20

Cash book .................................................................................................................................21

BRS...........................................................................................................................................21

CLIENT 5......................................................................................................................................22

a) Books of Henderson for May 2016.......................................................................................22

Sales Ledger account.................................................................................................................22

Purchase ledger control Account..............................................................................................23

b) Describing 'Control Account'................................................................................................24

CLIENT 6......................................................................................................................................24

a) Meaning and features of suspense account...........................................................................24

b) Computation of Trial Balance...............................................................................................24

c) Preparation Journal entries....................................................................................................25

d) Difference in Suspense account and Clearing account.........................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

a) Meaning and features of suspense account...........................................................................24

b) Computation of Trial Balance...............................................................................................24

c) Preparation Journal entries....................................................................................................25

d) Difference in Suspense account and Clearing account.........................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial accounting analyses, summarises and records the financial statement. Financial

statement can be classified into 3 types, statement of cash flow, statement of profit and loss and

statement of financial position. It is an important to tool assess the growth of the organisation

and evaluate the financial performance of the company (Edwards, 2013). The statements can be

analysed by the financial analysts to prepare growth strategies for the company. The report

covers various regulations and principles of financial accounting. Also, accounting concepts such

as the concept of prudence and consistency are being discussed in detail. Further, written down

and straight line method of depreciation are focussed upon. In the end, financial statement of

different companies including journal entries and trial balance are also prepared.

Assignment A

1. Defining Financial Accounting

Financial accounting helps to record financial transactions of the company. By using set

guidelines, transactions are recorded, outlined proposed in as financial report like income

statement or balance sheet. Issuing financial statement is routine work of an organisation. It

Facilitates rational decision making, planning and control operations, agreement with legal

requirements, evidence in court in case of dispute (Horngren and et. al, 2012). This is considered

as both external internal factors of the company, information by financial report is basically used

for decision making by externals like investors, suppliers, borrowers, tax authorities and

stockholders, who decides buying and selling of shares, to give loan to entity, and to impose

taxation amount and internals like management and managers of operations who helps in

analysing the profits incurred by products and operational units, to decide buying and selling

business segments, to evaluate new production facilities and to decide the need for cash flows to

support companies operations (Weygandt and et. al 2010). The information of financial

statements is also circulated to company's secondary beneficiaries like competitors, employees,

buyers, labour organisation and investment analysts. It is important for every company to prepare

financial report regularly not because company need to know its value rather it is to provide

enough information to others for evaluation of value of the company themselves. The

organisation is required to keep systematic records in order to protect business and find out profit

and loss operations. It further helps to evaluate company's financial standing, to uncover hidden

liabilities, to forecast future financials of the company.

1

Financial accounting analyses, summarises and records the financial statement. Financial

statement can be classified into 3 types, statement of cash flow, statement of profit and loss and

statement of financial position. It is an important to tool assess the growth of the organisation

and evaluate the financial performance of the company (Edwards, 2013). The statements can be

analysed by the financial analysts to prepare growth strategies for the company. The report

covers various regulations and principles of financial accounting. Also, accounting concepts such

as the concept of prudence and consistency are being discussed in detail. Further, written down

and straight line method of depreciation are focussed upon. In the end, financial statement of

different companies including journal entries and trial balance are also prepared.

Assignment A

1. Defining Financial Accounting

Financial accounting helps to record financial transactions of the company. By using set

guidelines, transactions are recorded, outlined proposed in as financial report like income

statement or balance sheet. Issuing financial statement is routine work of an organisation. It

Facilitates rational decision making, planning and control operations, agreement with legal

requirements, evidence in court in case of dispute (Horngren and et. al, 2012). This is considered

as both external internal factors of the company, information by financial report is basically used

for decision making by externals like investors, suppliers, borrowers, tax authorities and

stockholders, who decides buying and selling of shares, to give loan to entity, and to impose

taxation amount and internals like management and managers of operations who helps in

analysing the profits incurred by products and operational units, to decide buying and selling

business segments, to evaluate new production facilities and to decide the need for cash flows to

support companies operations (Weygandt and et. al 2010). The information of financial

statements is also circulated to company's secondary beneficiaries like competitors, employees,

buyers, labour organisation and investment analysts. It is important for every company to prepare

financial report regularly not because company need to know its value rather it is to provide

enough information to others for evaluation of value of the company themselves. The

organisation is required to keep systematic records in order to protect business and find out profit

and loss operations. It further helps to evaluate company's financial standing, to uncover hidden

liabilities, to forecast future financials of the company.

1

2. Regulations of financial accounting

Financial accounting is an important aspect of defining the financial position of the

company. The ultimate aim of financial accounting are as follows:

Identifying: To identify the information which is required to be recorded in the books.

Measuring: The extracted information is measured to evaluate the performance and take

further decisions (Beatty and Liao, 2014).

Communicating: The information is communicated and presented in such a way that it is

understandable to the users.

There are various regulations that are required to be adopted by the companies while dealing in

the business within the country or across the geographical boundaries. Some of them are listed

below:

The International Financial Reporting Standards (IFRS): IFRS are the standards

issued by IFRS foundation and International Accounting Standard Boards (IASB) to have

set goals of understanding and comparing accounts. It is an important regulation for the

companies dealing across international boundaries (Carvalho and Salotti, 2012). The

accountants have to maintain financial books which are comparable, understandable,

reliable and relevant while analysing the accounts.

Generally Accepted Privacy Principles (GAPP): It assists Chartered Accountants

(CA) and Certified Public Accountants in managing and preventing privacy risk. It

covers the compliances over collection, use, retain, disclose and dispose personal

information of an individual.

3. Accounting rules and principles

It is important to understand the rules and regulations, in order to follow set standard of

accounting. There are three basic golden rules on accounting. They are:

Debit the party who receive the fund and credit the party who give the funds

Debit what is coming in the business and credit what is or will go out of the business

Debit all expenses incurred and losses and credit all incomes incurred and gains

There are various principles of accounting that are required to be followed when maintaining

accounts. Some important principles are discussed below:

2

Financial accounting is an important aspect of defining the financial position of the

company. The ultimate aim of financial accounting are as follows:

Identifying: To identify the information which is required to be recorded in the books.

Measuring: The extracted information is measured to evaluate the performance and take

further decisions (Beatty and Liao, 2014).

Communicating: The information is communicated and presented in such a way that it is

understandable to the users.

There are various regulations that are required to be adopted by the companies while dealing in

the business within the country or across the geographical boundaries. Some of them are listed

below:

The International Financial Reporting Standards (IFRS): IFRS are the standards

issued by IFRS foundation and International Accounting Standard Boards (IASB) to have

set goals of understanding and comparing accounts. It is an important regulation for the

companies dealing across international boundaries (Carvalho and Salotti, 2012). The

accountants have to maintain financial books which are comparable, understandable,

reliable and relevant while analysing the accounts.

Generally Accepted Privacy Principles (GAPP): It assists Chartered Accountants

(CA) and Certified Public Accountants in managing and preventing privacy risk. It

covers the compliances over collection, use, retain, disclose and dispose personal

information of an individual.

3. Accounting rules and principles

It is important to understand the rules and regulations, in order to follow set standard of

accounting. There are three basic golden rules on accounting. They are:

Debit the party who receive the fund and credit the party who give the funds

Debit what is coming in the business and credit what is or will go out of the business

Debit all expenses incurred and losses and credit all incomes incurred and gains

There are various principles of accounting that are required to be followed when maintaining

accounts. Some important principles are discussed below:

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Full disclosure principle: It is important to disclose all the information that is required

by the investor within the statements or in the notes of the statements(Freeman and et.al.,

2014).

Going concern principle: According to this principle, it is assumed that the functioning

of the company will be continued for a longer period to achieve its objectives and it will

not wind up in near future. If it is certain by the company's performance that it will

liquidate in coming years then it is required to be disclosed it in its assessment.

Matching principle: The companies are suggested to use accrual basis of accounting

where expenses should match with the revenues. All the future benefits are not

considered in the current year. However, all the future expenses are taken into

consideration.

Materiality principle: The basic principles are allowed to be violate in case some other

accounting principle is ideal for the situation. It is based on the judgement of the

company that whether the amount is insignificant or immaterial.

Conservatism: In situation of two available alternatives of reporting, the principle

suggest which alternative should be chosen by the accountant which results to less net

income or less net asset. Accountants are required to be unbiased while taking this

decision and anticipate or disclose potential losses while reporting financial statements.

4. Consistency and material disclosure with respect to concepts and conventions.

Consistency is the principle which says that same management accounting principles

should be followed by the company while preparing financial statements over period. It helps the

management to draw important conclusion by doing comparative analysis of financial statements

over the years. If the company will use different principle in different years then it will be

difficult to evaluate and compare the performance on different postulates. If the company wants

to change its principles then it important to disclose the new principle and reason for the change

to all the stakeholders in annual general meeting of the company (Cuckston, 2013). For instance,

if the company is using written down method for depreciation then it is advised to continue the

same method of depreciation for upcoming years as well. However, to change the method and

convert it to straight line method, it is advised to make proper disclosure with the stated reason to

all the stakeholders of the company.

3

by the investor within the statements or in the notes of the statements(Freeman and et.al.,

2014).

Going concern principle: According to this principle, it is assumed that the functioning

of the company will be continued for a longer period to achieve its objectives and it will

not wind up in near future. If it is certain by the company's performance that it will

liquidate in coming years then it is required to be disclosed it in its assessment.

Matching principle: The companies are suggested to use accrual basis of accounting

where expenses should match with the revenues. All the future benefits are not

considered in the current year. However, all the future expenses are taken into

consideration.

Materiality principle: The basic principles are allowed to be violate in case some other

accounting principle is ideal for the situation. It is based on the judgement of the

company that whether the amount is insignificant or immaterial.

Conservatism: In situation of two available alternatives of reporting, the principle

suggest which alternative should be chosen by the accountant which results to less net

income or less net asset. Accountants are required to be unbiased while taking this

decision and anticipate or disclose potential losses while reporting financial statements.

4. Consistency and material disclosure with respect to concepts and conventions.

Consistency is the principle which says that same management accounting principles

should be followed by the company while preparing financial statements over period. It helps the

management to draw important conclusion by doing comparative analysis of financial statements

over the years. If the company will use different principle in different years then it will be

difficult to evaluate and compare the performance on different postulates. If the company wants

to change its principles then it important to disclose the new principle and reason for the change

to all the stakeholders in annual general meeting of the company (Cuckston, 2013). For instance,

if the company is using written down method for depreciation then it is advised to continue the

same method of depreciation for upcoming years as well. However, to change the method and

convert it to straight line method, it is advised to make proper disclosure with the stated reason to

all the stakeholders of the company.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The concept of material says that all the important is required to be disclosed by the

company to the stakeholders. This concept came into being in order to protect the rights of the

stakeholders. The investors and shareholders have right to know each and every necessary

information which can affect their decision. The information can be material or immaterial, the

company is required to take the judgement that whether it is important enough to be disclosed or

not.

ASSIGNMENT B

CLIENT 1

Books of prime entry

4

company to the stakeholders. This concept came into being in order to protect the rights of the

stakeholders. The investors and shareholders have right to know each and every necessary

information which can affect their decision. The information can be material or immaterial, the

company is required to take the judgement that whether it is important enough to be disclosed or

not.

ASSIGNMENT B

CLIENT 1

Books of prime entry

4

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

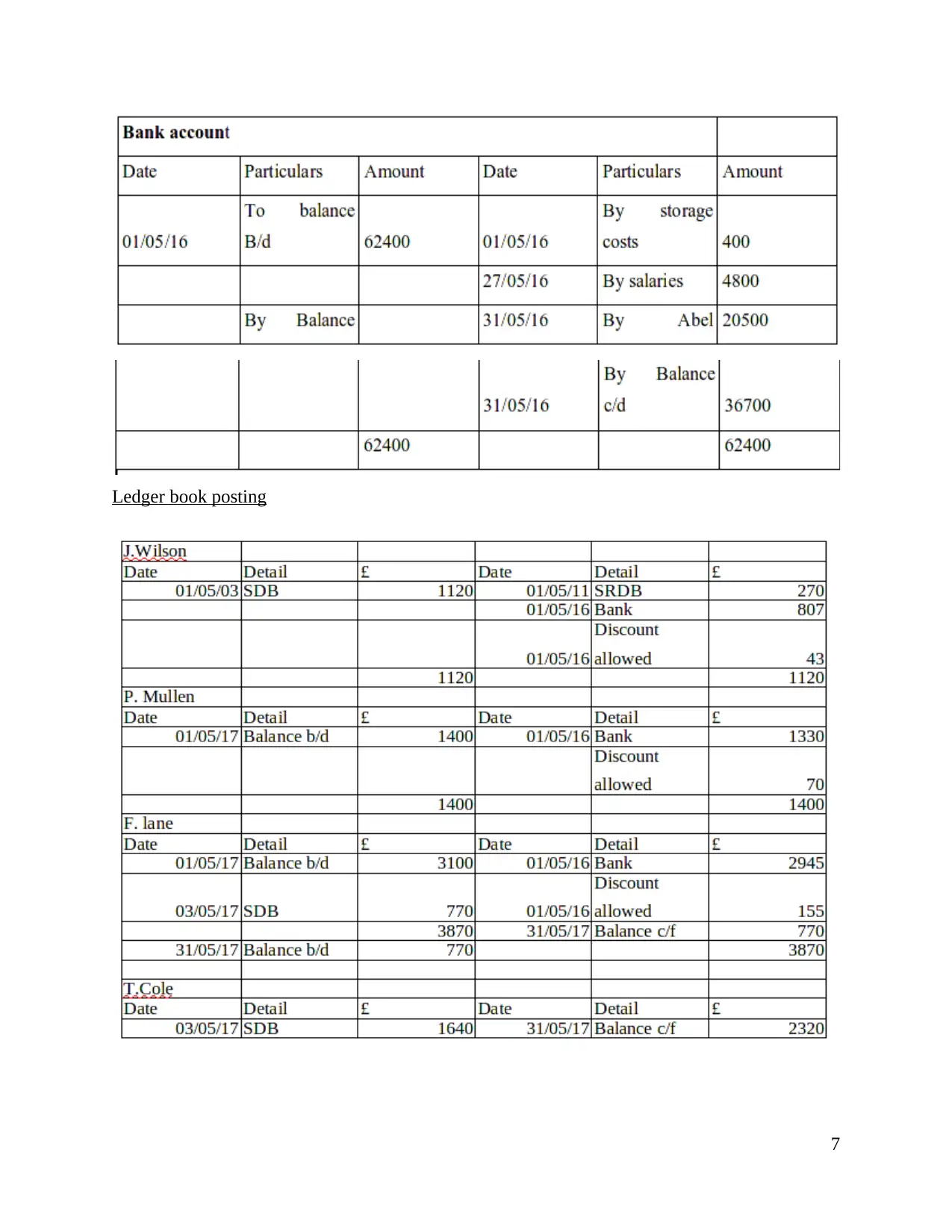

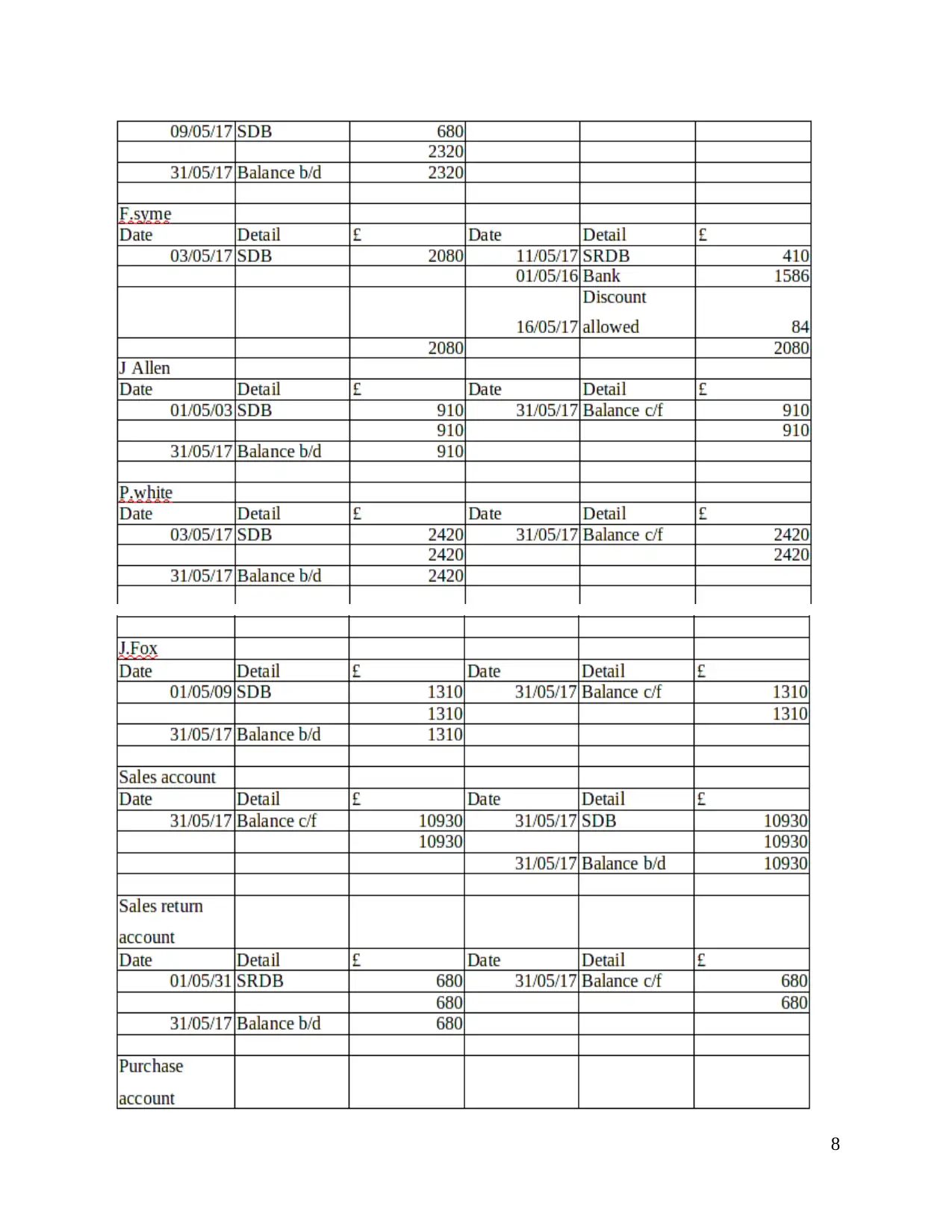

Ledger book posting

7

7

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.