Financial Accounting Principles and Practical Application

VerifiedAdded on 2020/02/03

|37

|6586

|40

Homework Assignment

AI Summary

This document presents a detailed solution to a financial accounting assignment, encompassing various aspects of the subject. It begins with an introduction to financial accounting, including regulations, rules, and principles like consistency, material disclosure, and cost concepts. The assignment then progresses through several client-based scenarios, starting with primary book entries and journal entries, including computations of capital. It covers double-entry recording systems, trial balance preparation, and the creation of financial reports, including profit and loss accounts and statements of financial position. The solution also explores depreciation methods (WDM and SLM), bank reconciliation statements, control accounts, and suspense accounts. Furthermore, it includes examples like balance book preparation, sales and purchase ledger control accounts, and journal entries. The assignment concludes with a discussion on the differences between suspense and clearing accounts and provides references for further study. Overall, the document serves as a comprehensive guide to understanding and applying financial accounting principles through practical examples and case studies.

Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1Financial accounting...................................................................................................................4

1.2 Regulations related to the financial accounting.........................................................................4

1.3 Accounting Rule and principles.................................................................................................5

1.4 Convention and cost concept related to consistency and material disclosure...........................6

Client 1.................................................................................................................................................7

Primary Book Entry.........................................................................................................................7

1 Journal Entries with computation of capital.................................................................................7

A) Book of primary entry frame work.............................................................................................7

B) Completing Double entry recording System..............................................................................9

B) Trial balance preparation..........................................................................................................18

Client 2...............................................................................................................................................19

A) Framing Financial report Profit and Loss account...................................................................19

B) Making Financials statement for getting current position........................................................22

CLIENT 3.............................................................................................................................................1

A) Organization like Raintree limited and preparation of Gain and loss account ........................1

B) Preparation of statement of financial position or balance sheet for Raintree limited.................1

C) Description of two accounting principles used for preparing financial statements....................2

D) Explanation of WDM and SLM in order to derive amount of depreciation...............................3

CLIENT 4.............................................................................................................................................4

A) Bank reconciliation statement (BRS) along with its purposes...................................................4

B) Determining the causes which lead to create difference among bank records and cash book.. .5

C) Bank Reconciliation Statement for December 2016..................................................................5

Updated cash book...........................................................................................................................6

Bank Reconciliation Statement dated on the 21st December.........................................................6

Client 5.................................................................................................................................................7

A) balance book preparation of Henderson for May 2016 .............................................................7

Sales ledge control account.............................................................................................................7

Purchase ledge control account preparation....................................................................................7

B) Control account and requirements for preparing this account....................................................8

Client 6.................................................................................................................................................9

A) Suspense account and its key features........................................................................................9

B) Trial balance with the help of control account.........................................................................10

C) Journal entries...........................................................................................................................10

D) Difference between Suspense and clearing account.................................................................10

Conclusion..........................................................................................................................................11

References..........................................................................................................................................13

2

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1Financial accounting...................................................................................................................4

1.2 Regulations related to the financial accounting.........................................................................4

1.3 Accounting Rule and principles.................................................................................................5

1.4 Convention and cost concept related to consistency and material disclosure...........................6

Client 1.................................................................................................................................................7

Primary Book Entry.........................................................................................................................7

1 Journal Entries with computation of capital.................................................................................7

A) Book of primary entry frame work.............................................................................................7

B) Completing Double entry recording System..............................................................................9

B) Trial balance preparation..........................................................................................................18

Client 2...............................................................................................................................................19

A) Framing Financial report Profit and Loss account...................................................................19

B) Making Financials statement for getting current position........................................................22

CLIENT 3.............................................................................................................................................1

A) Organization like Raintree limited and preparation of Gain and loss account ........................1

B) Preparation of statement of financial position or balance sheet for Raintree limited.................1

C) Description of two accounting principles used for preparing financial statements....................2

D) Explanation of WDM and SLM in order to derive amount of depreciation...............................3

CLIENT 4.............................................................................................................................................4

A) Bank reconciliation statement (BRS) along with its purposes...................................................4

B) Determining the causes which lead to create difference among bank records and cash book.. .5

C) Bank Reconciliation Statement for December 2016..................................................................5

Updated cash book...........................................................................................................................6

Bank Reconciliation Statement dated on the 21st December.........................................................6

Client 5.................................................................................................................................................7

A) balance book preparation of Henderson for May 2016 .............................................................7

Sales ledge control account.............................................................................................................7

Purchase ledge control account preparation....................................................................................7

B) Control account and requirements for preparing this account....................................................8

Client 6.................................................................................................................................................9

A) Suspense account and its key features........................................................................................9

B) Trial balance with the help of control account.........................................................................10

C) Journal entries...........................................................................................................................10

D) Difference between Suspense and clearing account.................................................................10

Conclusion..........................................................................................................................................11

References..........................................................................................................................................13

2

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is the filed or branch of accounting business concern with the summary

,investigation and reporting of financial transaction refer to an enterprise and reports of all the

transaction. Companies issue fiscal statement on a routeing basis like quarterly, half-yearly and

annually as per the business requirement. So this project is about the business transaction using

book keeping, trial balance. Sole trade, partnership, limited company in accordance with the

appropriate principle. Bank reconciliation statement and bank records, Regulations of the financial

accounting, Accounting rules and principles are explained.

TASK 1

1.1Financial accounting

This is the branch of company's accounting which deals with the tracking of financial

concepts of the company. (Deegan, C., 2013). According to its standard criteria the transactions are

summarised, presented and recorded in reporting of financial income statement and balance sheet.

Companies issue financial statement on routine basis(Francis, J., 2013). The statement that consider

external because they are issued and given to outside of the company for people, investors,

stakeholder as well as certain leaders. Other financial reporting and statements are broadly

calculated if a corporation stokes are traded publicaly, it helps to provide information to outside

sources such as customers, employees, labour, competitors and other investment analysts. In US

Financial Accounting Standard Board can be referred as a process of financial accounting which

contains process of transcription, summarising and reporting that varied of transaction resulting

from business operation over a period of time.

1.2 Regulations related to the financial accounting

Some accounting bodies like FASB (Financial accounting standard board) set different

standards by accepting principles of accounting. Talking about the FASB is private non profit

organisation established in US to set general accepted accounting principles in public interest. In

UK Financial reporting standards (FRS) and financial Reporting Exposure draft are followed.

Studying how other standard reflects in financial accounting and the different particular starting of

transactions are governed by International Accounting Standards (IAS). Earlier before, international

standards of accounting were developed by IASC (Board of International Accounting Standards)

but from 2001, the new set for accounting was launched which is International Financials Reporting

standards and issued by IASB. The Basis of fundamental principles in accounting are cost

principles, full disclosure principles, matching principles, revenue recognition principles, economic

4

Financial accounting is the filed or branch of accounting business concern with the summary

,investigation and reporting of financial transaction refer to an enterprise and reports of all the

transaction. Companies issue fiscal statement on a routeing basis like quarterly, half-yearly and

annually as per the business requirement. So this project is about the business transaction using

book keeping, trial balance. Sole trade, partnership, limited company in accordance with the

appropriate principle. Bank reconciliation statement and bank records, Regulations of the financial

accounting, Accounting rules and principles are explained.

TASK 1

1.1Financial accounting

This is the branch of company's accounting which deals with the tracking of financial

concepts of the company. (Deegan, C., 2013). According to its standard criteria the transactions are

summarised, presented and recorded in reporting of financial income statement and balance sheet.

Companies issue financial statement on routine basis(Francis, J., 2013). The statement that consider

external because they are issued and given to outside of the company for people, investors,

stakeholder as well as certain leaders. Other financial reporting and statements are broadly

calculated if a corporation stokes are traded publicaly, it helps to provide information to outside

sources such as customers, employees, labour, competitors and other investment analysts. In US

Financial Accounting Standard Board can be referred as a process of financial accounting which

contains process of transcription, summarising and reporting that varied of transaction resulting

from business operation over a period of time.

1.2 Regulations related to the financial accounting

Some accounting bodies like FASB (Financial accounting standard board) set different

standards by accepting principles of accounting. Talking about the FASB is private non profit

organisation established in US to set general accepted accounting principles in public interest. In

UK Financial reporting standards (FRS) and financial Reporting Exposure draft are followed.

Studying how other standard reflects in financial accounting and the different particular starting of

transactions are governed by International Accounting Standards (IAS). Earlier before, international

standards of accounting were developed by IASC (Board of International Accounting Standards)

but from 2001, the new set for accounting was launched which is International Financials Reporting

standards and issued by IASB. The Basis of fundamental principles in accounting are cost

principles, full disclosure principles, matching principles, revenue recognition principles, economic

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

entity principles, monetary assumption principle are, time period principles, going concern concept,

materiality and conservatism principles are included. Last two principles are constrains.

1.3 Accounting Rule and Principles

For any business, full disclosure Principle requires a company to provide all the necessary

information to those people who are engaged in finance related decision making in the company

(Beatty, A. and Lios, S., 2014). The company's Financial statements include any supplementary

schedule and notes. However, management analysis and discussions are included in publicly traded

corporation annual report to U.S. security exchange commission.

Ten basic Principles that make the accounting rules as describes by GAAP are:

Separate Legal Entity: Legally a business is a separate and legal entity. The activities been

carried out in the business remain separated from its owner. Legally it is said that a business

can survive longer till the existence of promoters and owners.

Currency specified principle: A currency must be specified for the over all business

transactions. Like in U.S. all currency is represented in dollars and companies who conduct

their business outside their home country then they need to convert their transaction into

USD and they have to use the current exchange rate while reporting the financial statements.

Specific time period principle: Financial statement always refers to a specific time. All the

income statements have a start and an end date. So, that the readers can identified the

transaction period and business transactions would be carried out.

Historical Cost: This principle is used for valuing the items. The price at which the items are

bought and sold can be used for valuation. The Real value of the items changes during the

course of time because of inflation, recession, depreciation on assets over time.

Full disclosure principle: Full disclosure principle is always in keen focus on all accounting

standards in today's world. It states that every company disclose every aspect of financial

statement to their related outsiders.

Recognition: It states that the company reveal its income and expenses in the same period in

which they have been occur.

No death principle: It states that business will continue to function eternally and have no

end.

Matching principle: It states that accrual accounting system to be used and for every debit

there should be a credit and vice-versa.

Principle of materiality: It states that if there is any error in book keeping then the way to

rectify the error is need to be followed by the organisation. Because there are few principles

which requires the book keeping to use their judgement rather than short tricks.

5

materiality and conservatism principles are included. Last two principles are constrains.

1.3 Accounting Rule and Principles

For any business, full disclosure Principle requires a company to provide all the necessary

information to those people who are engaged in finance related decision making in the company

(Beatty, A. and Lios, S., 2014). The company's Financial statements include any supplementary

schedule and notes. However, management analysis and discussions are included in publicly traded

corporation annual report to U.S. security exchange commission.

Ten basic Principles that make the accounting rules as describes by GAAP are:

Separate Legal Entity: Legally a business is a separate and legal entity. The activities been

carried out in the business remain separated from its owner. Legally it is said that a business

can survive longer till the existence of promoters and owners.

Currency specified principle: A currency must be specified for the over all business

transactions. Like in U.S. all currency is represented in dollars and companies who conduct

their business outside their home country then they need to convert their transaction into

USD and they have to use the current exchange rate while reporting the financial statements.

Specific time period principle: Financial statement always refers to a specific time. All the

income statements have a start and an end date. So, that the readers can identified the

transaction period and business transactions would be carried out.

Historical Cost: This principle is used for valuing the items. The price at which the items are

bought and sold can be used for valuation. The Real value of the items changes during the

course of time because of inflation, recession, depreciation on assets over time.

Full disclosure principle: Full disclosure principle is always in keen focus on all accounting

standards in today's world. It states that every company disclose every aspect of financial

statement to their related outsiders.

Recognition: It states that the company reveal its income and expenses in the same period in

which they have been occur.

No death principle: It states that business will continue to function eternally and have no

end.

Matching principle: It states that accrual accounting system to be used and for every debit

there should be a credit and vice-versa.

Principle of materiality: It states that if there is any error in book keeping then the way to

rectify the error is need to be followed by the organisation. Because there are few principles

which requires the book keeping to use their judgement rather than short tricks.

5

The conservative principle of accounting: It states that every expenses must be recorded

immediately, but incomes are need to be recorded when the actual income has been

received.

1.4 Convention and cost concept related to consistency and material disclosure

Accounting convention consist of guidelines that arises from practice applications of

accounting principles. It is not legal bound practice but is generally accepted convention based on

customs and design to help accountants and overcoming problem that arises at the time of

preparation of financial statement(Benjamin, M., 2015). If an organisations like Safety and

securities of exchange commission (SEC) or financial accounting Standards board (FASB) set a

guidelines that address the same accounting convention, convention is applicable for longer period.

Accounting Property principle: Consistence principle states that ones an adopted accounting

rules, method or time period then need to be followed consistently in future accounting

period(Board, A.P., 2015). Any business can changes accounting principles if Accounting bodies

circulates necessary changes and principles to make change in particular accounting technique.

Accounting audits activities follows the consistency rule so that reports results from period to

period are comparable. An observer may refuse to provide financial views is on a client fiscal

statement if there are clear-cut and unwarrantable violation of rules.

Materiality concept in accounting: It states that an accountancy modular board can be

neglected the gross effect of doing something so has such a little impact on financial statement that

the reader of the financial statement would not be confused. under GAAPS no demand to

implement the provisions of explanation standard if item is incorporeal. Safety and Legal

instrument exchange commission has recommended for the presentation purpose that an item

correspond at least 5% of total assets should be separately disclosed in balance sheet. Smaller or

larger item who have an impact on net profit or loss need to be considered in financial accounting

and is considered as material. A transaction would also be considered as material if that cost change

the ratio and impact on profitability.

CLIENT 1

Primary Book Entry

There are separate journals for recording different type of entries and book keeping and are

collectively known as Book of primary entries, Book of original entries and subsidiary book. All

transaction are recorded in Primary books and original entries (Sangster, A., 2015). Counselling to

programme and system evaluable multiple GAAPS in accounting information systems). The third

6

immediately, but incomes are need to be recorded when the actual income has been

received.

1.4 Convention and cost concept related to consistency and material disclosure

Accounting convention consist of guidelines that arises from practice applications of

accounting principles. It is not legal bound practice but is generally accepted convention based on

customs and design to help accountants and overcoming problem that arises at the time of

preparation of financial statement(Benjamin, M., 2015). If an organisations like Safety and

securities of exchange commission (SEC) or financial accounting Standards board (FASB) set a

guidelines that address the same accounting convention, convention is applicable for longer period.

Accounting Property principle: Consistence principle states that ones an adopted accounting

rules, method or time period then need to be followed consistently in future accounting

period(Board, A.P., 2015). Any business can changes accounting principles if Accounting bodies

circulates necessary changes and principles to make change in particular accounting technique.

Accounting audits activities follows the consistency rule so that reports results from period to

period are comparable. An observer may refuse to provide financial views is on a client fiscal

statement if there are clear-cut and unwarrantable violation of rules.

Materiality concept in accounting: It states that an accountancy modular board can be

neglected the gross effect of doing something so has such a little impact on financial statement that

the reader of the financial statement would not be confused. under GAAPS no demand to

implement the provisions of explanation standard if item is incorporeal. Safety and Legal

instrument exchange commission has recommended for the presentation purpose that an item

correspond at least 5% of total assets should be separately disclosed in balance sheet. Smaller or

larger item who have an impact on net profit or loss need to be considered in financial accounting

and is considered as material. A transaction would also be considered as material if that cost change

the ratio and impact on profitability.

CLIENT 1

Primary Book Entry

There are separate journals for recording different type of entries and book keeping and are

collectively known as Book of primary entries, Book of original entries and subsidiary book. All

transaction are recorded in Primary books and original entries (Sangster, A., 2015). Counselling to

programme and system evaluable multiple GAAPS in accounting information systems). The third

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

books indicate that these are subsidiaries of journal. There are 8 type of subsidiary book. Petty cash

book, day to day transactions and journal entries are recorded in this book.

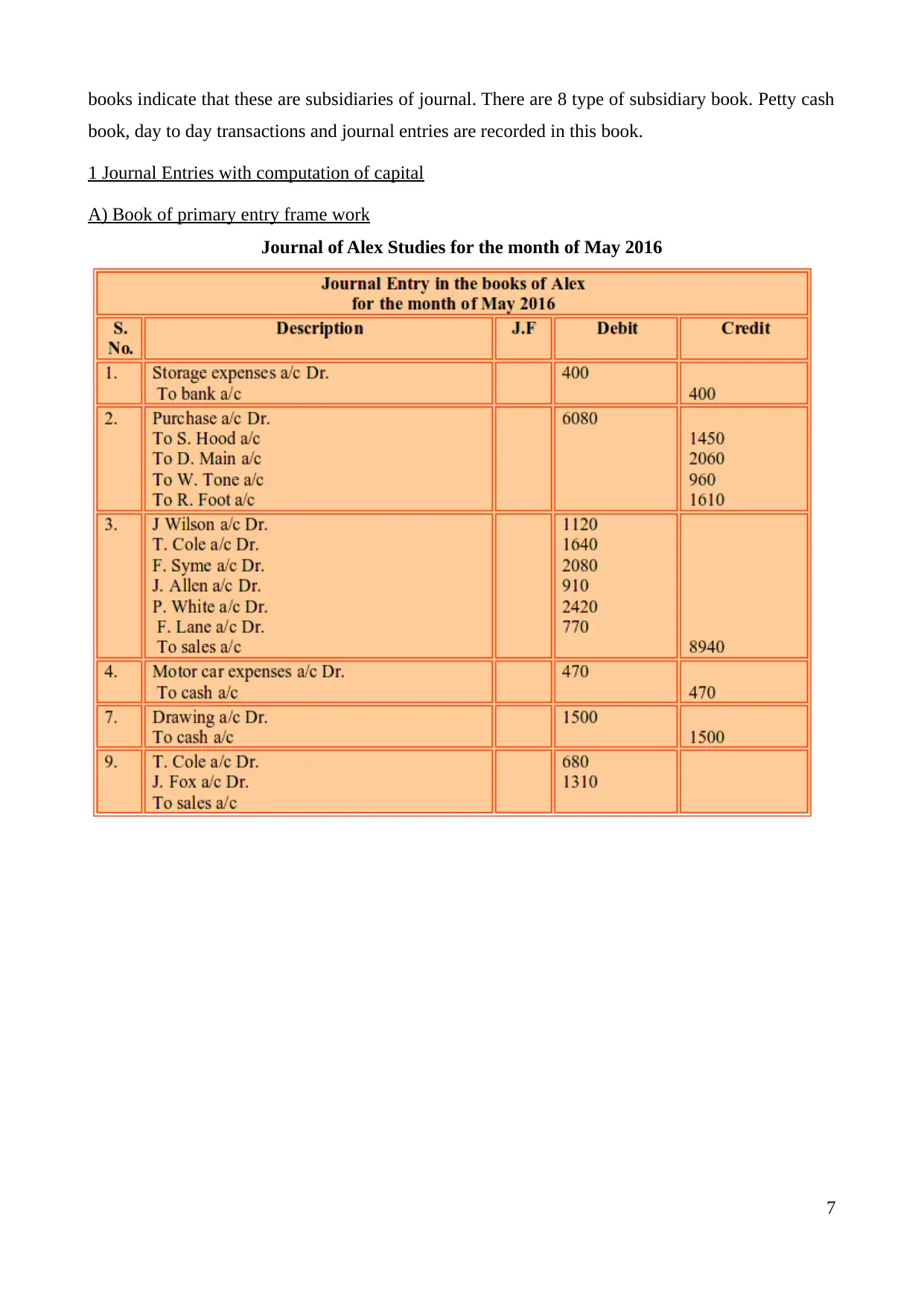

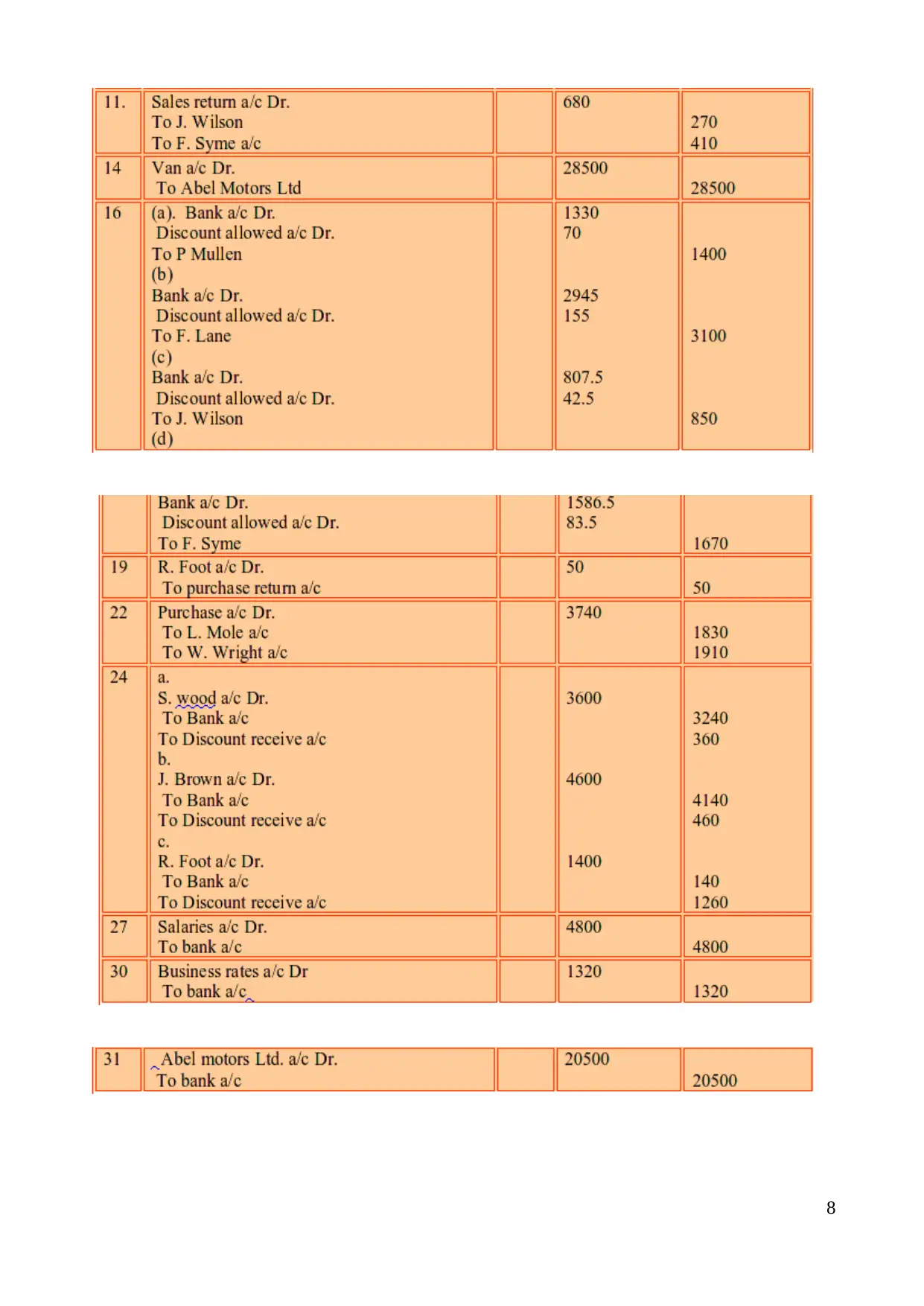

1 Journal Entries with computation of capital

A) Book of primary entry frame work

Journal of Alex Studies for the month of May 2016

7

book, day to day transactions and journal entries are recorded in this book.

1 Journal Entries with computation of capital

A) Book of primary entry frame work

Journal of Alex Studies for the month of May 2016

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

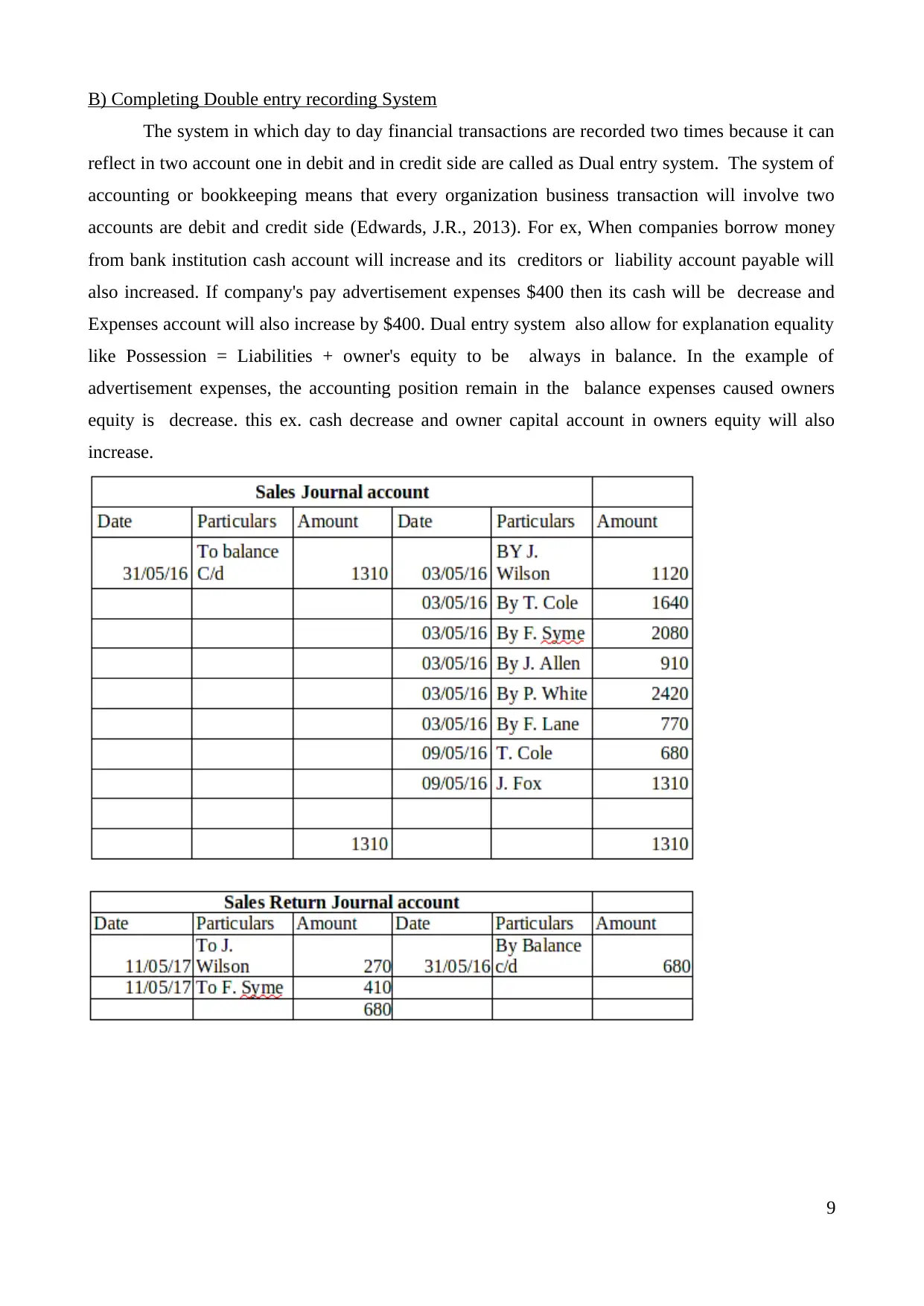

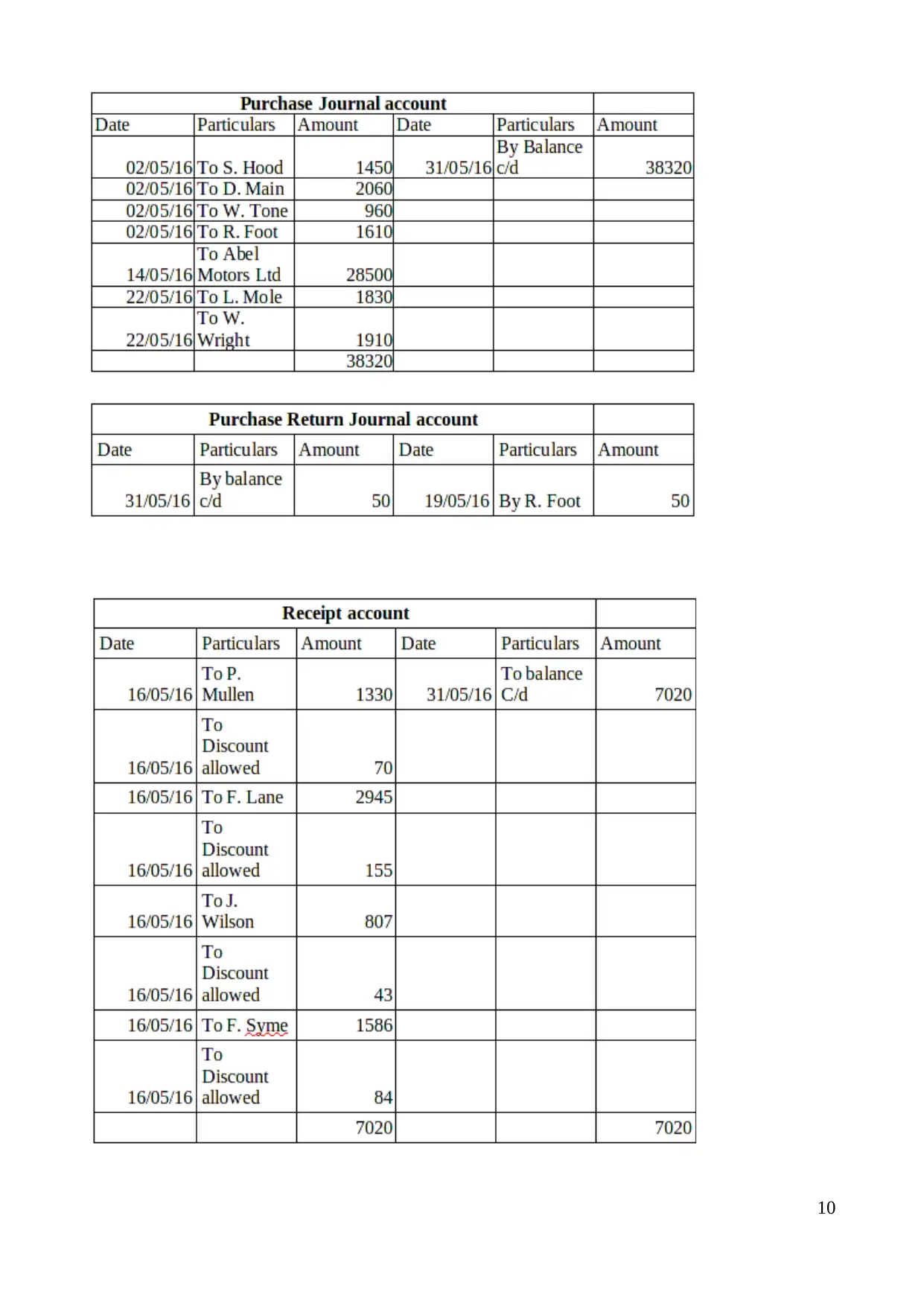

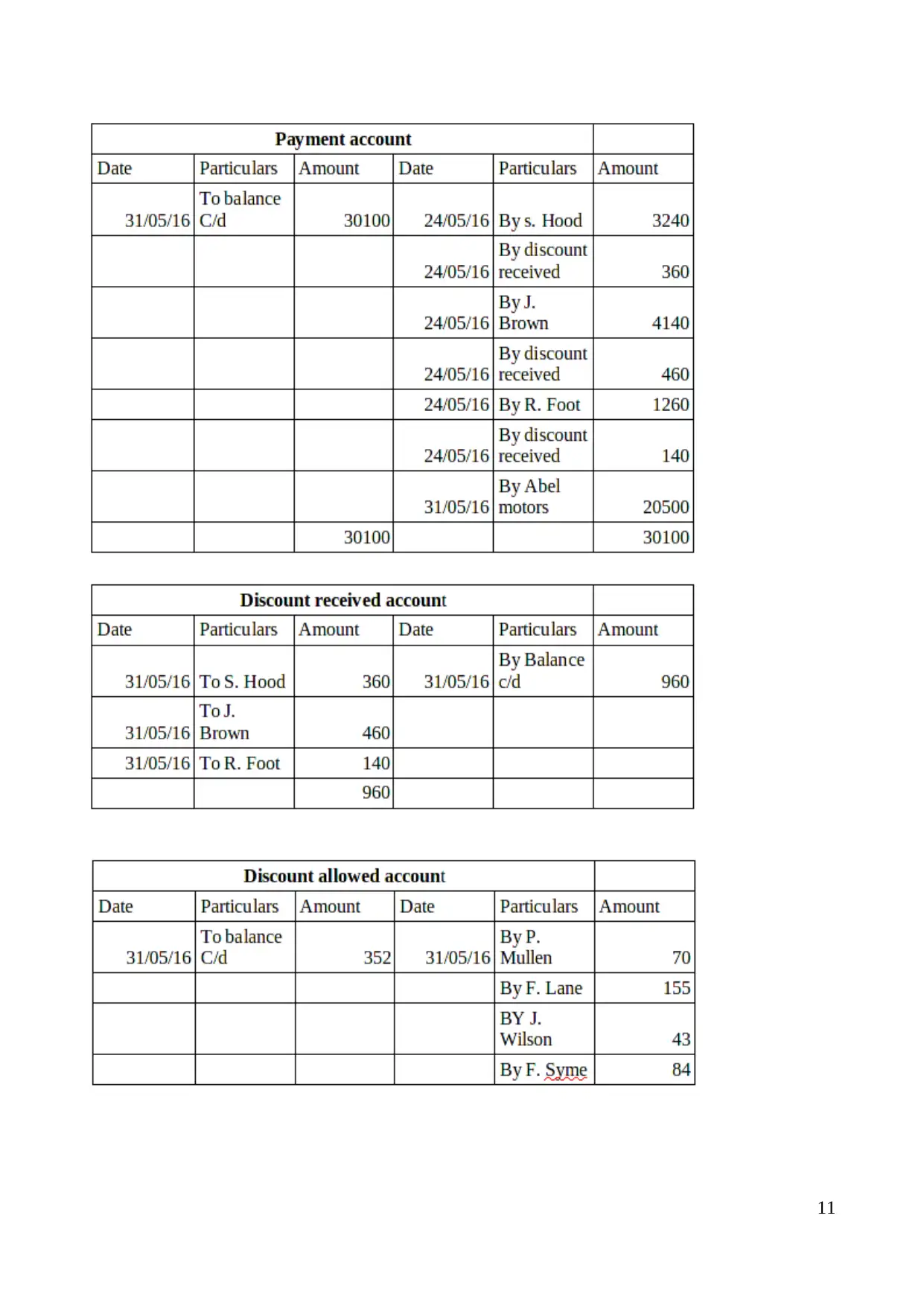

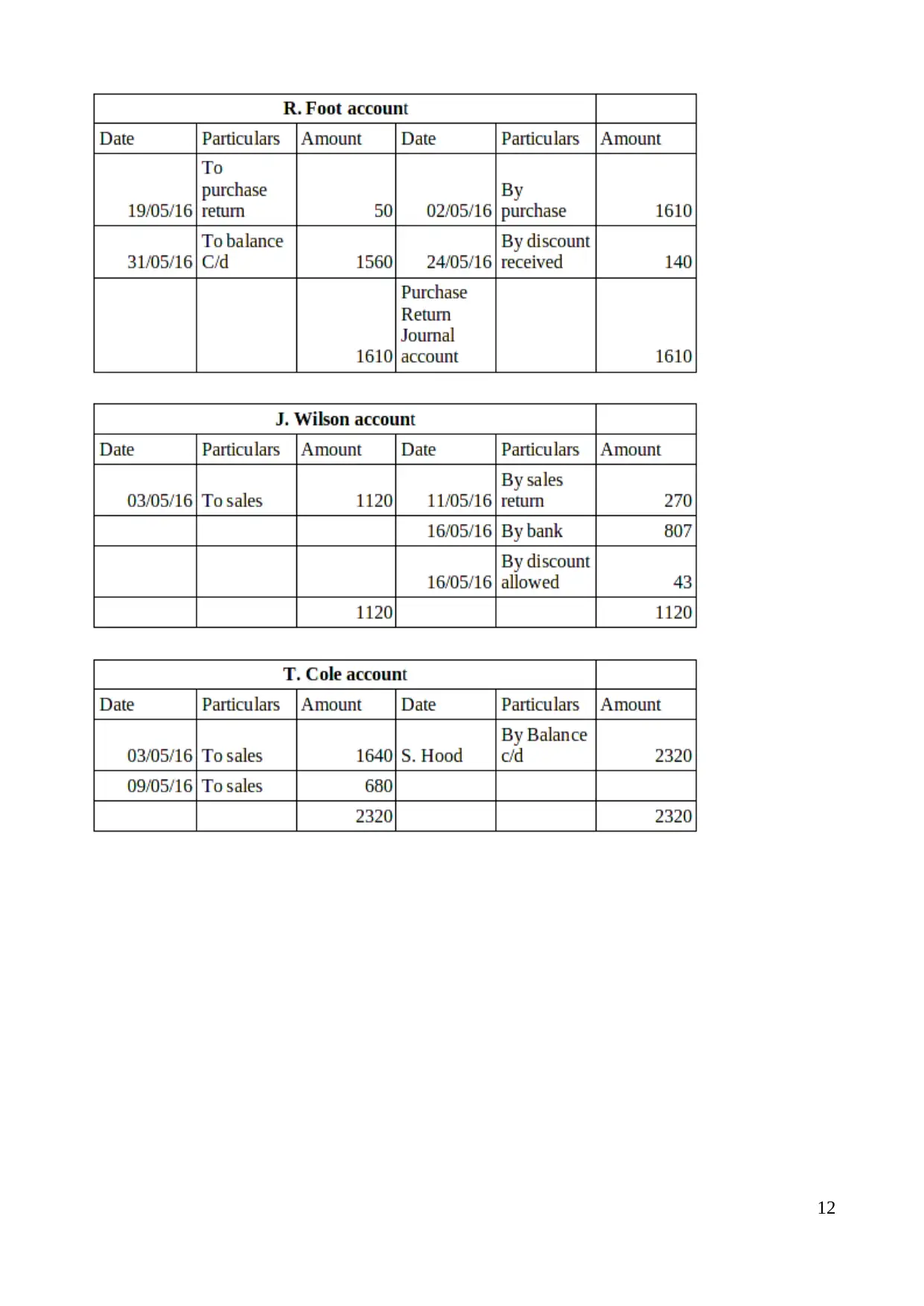

B) Completing Double entry recording System

The system in which day to day financial transactions are recorded two times because it can

reflect in two account one in debit and in credit side are called as Dual entry system. The system of

accounting or bookkeeping means that every organization business transaction will involve two

accounts are debit and credit side (Edwards, J.R., 2013). For ex, When companies borrow money

from bank institution cash account will increase and its creditors or liability account payable will

also increased. If company's pay advertisement expenses $400 then its cash will be decrease and

Expenses account will also increase by $400. Dual entry system also allow for explanation equality

like Possession = Liabilities + owner's equity to be always in balance. In the example of

advertisement expenses, the accounting position remain in the balance expenses caused owners

equity is decrease. this ex. cash decrease and owner capital account in owners equity will also

increase.

9

The system in which day to day financial transactions are recorded two times because it can

reflect in two account one in debit and in credit side are called as Dual entry system. The system of

accounting or bookkeeping means that every organization business transaction will involve two

accounts are debit and credit side (Edwards, J.R., 2013). For ex, When companies borrow money

from bank institution cash account will increase and its creditors or liability account payable will

also increased. If company's pay advertisement expenses $400 then its cash will be decrease and

Expenses account will also increase by $400. Dual entry system also allow for explanation equality

like Possession = Liabilities + owner's equity to be always in balance. In the example of

advertisement expenses, the accounting position remain in the balance expenses caused owners

equity is decrease. this ex. cash decrease and owner capital account in owners equity will also

increase.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 37

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.