Financial Accounting Assignment - Client Transaction Analysis Report

VerifiedAdded on 2020/10/04

|29

|5463

|298

Homework Assignment

AI Summary

This financial accounting assignment delves into various aspects of financial accounting through the analysis of multiple client scenarios. It begins with an introduction covering the core purposes, regulations, accounting rules, and principles, including conventions like consistency and material disclosure. The assignment then presents several client cases (Client1 to Client 6), each requiring the preparation of journal entries, ledger accounts, trial balances, profit and loss statements, and balance sheets. The tasks involve applying accounting concepts to real-world transactions, such as purchases, sales, expenses, and capital adjustments. Specific requirements include preparing journal entries, creating ledger accounts, constructing trial balances, and generating financial statements like the statement of profit and loss and the balance sheet. Additionally, the assignment addresses specific topics like bank reconciliation statements and suspense accounts, and the differences between them, along with the application of accounting concepts such as consistency and prudency. The assignment aims to provide a comprehensive understanding of financial accounting practices and their application in diverse business contexts. The document includes references to academic sources to support the concepts discussed.

FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

(a) 1. Examining the Financial Accounting and it's purposes......................................................1

(a) 2. Examining the regulations relating to financial accounting ..............................................2

(a) 3. Describing the Accounting rules and principles.................................................................3

(a) 4. Explaining the conventions and concepts relating to the consistency and material

disclosure.....................................................................................................................................4

CLIENT1.........................................................................................................................................5

(a) Journal Entry in the books of David Study...........................................................................5

(b) LEDGER ACCOUNTS .........................................................................................................8

(c) Trial Balance as at 31st January, 2018................................................................................14

CLIENT 2......................................................................................................................................16

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 .............16

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ...................17

CLIENT 3......................................................................................................................................17

....................................................................................................................................................18

(b) Balance Sheet of Bowling Limited......................................................................................19

(c) Accounts concepts such as consistency and prudency.........................................................19

Client 4...........................................................................................................................................21

(i) Purpose of bank reconciliation statement ............................................................................21

CLIENT 5......................................................................................................................................22

(a) Books of Henderson.............................................................................................................22

CLIENT 6......................................................................................................................................23

(a) Suspense Account.................................................................................................................23

(b) Drafting of Trail Balance:....................................................................................................24

(c) Trial balance have credit balance of £ 330 as suspense account..........................................24

(d) Difference between a Suspense A/c and Clearing A/c.........................................................25

CONCLUSION..............................................................................................................................25

REFERENCES..............................................................................................................................27

INTRODUCTION...........................................................................................................................1

(a) 1. Examining the Financial Accounting and it's purposes......................................................1

(a) 2. Examining the regulations relating to financial accounting ..............................................2

(a) 3. Describing the Accounting rules and principles.................................................................3

(a) 4. Explaining the conventions and concepts relating to the consistency and material

disclosure.....................................................................................................................................4

CLIENT1.........................................................................................................................................5

(a) Journal Entry in the books of David Study...........................................................................5

(b) LEDGER ACCOUNTS .........................................................................................................8

(c) Trial Balance as at 31st January, 2018................................................................................14

CLIENT 2......................................................................................................................................16

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 .............16

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ...................17

CLIENT 3......................................................................................................................................17

....................................................................................................................................................18

(b) Balance Sheet of Bowling Limited......................................................................................19

(c) Accounts concepts such as consistency and prudency.........................................................19

Client 4...........................................................................................................................................21

(i) Purpose of bank reconciliation statement ............................................................................21

CLIENT 5......................................................................................................................................22

(a) Books of Henderson.............................................................................................................22

CLIENT 6......................................................................................................................................23

(a) Suspense Account.................................................................................................................23

(b) Drafting of Trail Balance:....................................................................................................24

(c) Trial balance have credit balance of £ 330 as suspense account..........................................24

(d) Difference between a Suspense A/c and Clearing A/c.........................................................25

CONCLUSION..............................................................................................................................25

REFERENCES..............................................................................................................................27

INTRODUCTION

In modern times the financial accounting plays an integral part in managing and

ascertaining the operational activities of the business entity also ascertain it's performance.

Financial accounting refers to the process of preparation of annual or financial statements that

are used to record and depicts the financial performance as well as the operational experiences of

the organisation(Weil, Schipper and Francis, 2013). These statements forms a financial or

annual report of the organisation of the organisation which are mainly useful for the internal as

well as the external parties of the business entity. Besides this, the report pertain the knowledge

and evaluation regarding the financial statements of the small accountancy organisation like Taj

Accountants (UK).

(a) 1. Examining the Financial Accounting and it's purposes

Financial Accounting refers to the process of recording, summarising and reporting the

myriad of business operational activities over an accounting era(Schaltegger and Burritt, 2017).

These operational transactions are summarized in the preparation of the financial statements,

involves balance sheet, income statements and cash flow statement that depicts the operating as

well as the financial performance of the business organisation like Taj Accountancy over a

specific accounting era.

There are some purposes of the financial accounting for the business organisation, which are

mentioned underneath.

Financial Accounting used for maintaining the systematic records: The financial

accounting refers to the systematic record of the systematic record of the financial

transactions of the organisation. The financial accounting helps in maintaining the

systematic record of the business transactions by recording them on the accrual basis.

It is used for the purpose of protecting the business properties: The accounting also

used for the purpose of protecting the properties or assets of the business organisation for

unreasonable or unwarrantable use(Zeff, 2016).

Financial accounting is specialized for completing the purpose of ascertainment of

operational profit or loss: Among all the purpose the main purpose of adapting the

1

In modern times the financial accounting plays an integral part in managing and

ascertaining the operational activities of the business entity also ascertain it's performance.

Financial accounting refers to the process of preparation of annual or financial statements that

are used to record and depicts the financial performance as well as the operational experiences of

the organisation(Weil, Schipper and Francis, 2013). These statements forms a financial or

annual report of the organisation of the organisation which are mainly useful for the internal as

well as the external parties of the business entity. Besides this, the report pertain the knowledge

and evaluation regarding the financial statements of the small accountancy organisation like Taj

Accountants (UK).

(a) 1. Examining the Financial Accounting and it's purposes

Financial Accounting refers to the process of recording, summarising and reporting the

myriad of business operational activities over an accounting era(Schaltegger and Burritt, 2017).

These operational transactions are summarized in the preparation of the financial statements,

involves balance sheet, income statements and cash flow statement that depicts the operating as

well as the financial performance of the business organisation like Taj Accountancy over a

specific accounting era.

There are some purposes of the financial accounting for the business organisation, which are

mentioned underneath.

Financial Accounting used for maintaining the systematic records: The financial

accounting refers to the systematic record of the systematic record of the financial

transactions of the organisation. The financial accounting helps in maintaining the

systematic record of the business transactions by recording them on the accrual basis.

It is used for the purpose of protecting the business properties: The accounting also

used for the purpose of protecting the properties or assets of the business organisation for

unreasonable or unwarrantable use(Zeff, 2016).

Financial accounting is specialized for completing the purpose of ascertainment of

operational profit or loss: Among all the purpose the main purpose of adapting the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial is to find out or quantify the accurate values of the profits or losses incurred

from the business operational activities of the organisation(Edwards, 2013).

It is used for the purpose of ascertaining the financial performance of the business:

The accounting also used for the purpose of ascertaining the the financial performance of

the business organisations. As accounting helps in keeping the systematic record of the

past accounting years that renders a base or the comparative basis that is utilised by the

organisation to compare and ascertain the profit margin as well as the probability(Khan,

2015).

It is used to ensure effective decision making within the organisation: The financial

reporting helps the managers to make further futuristic decision regarding the business

operational activities of the organisations. With the help of accurate financial records

regarding the business activities it helps the managers to quantify the actual output from

the business activities and take further actions for ensuring more betterment and attaining

the more favourable outcomes(May, 2013).

(a) 2. Examining the regulations relating to financial accounting

There are some regulations for guiding the process of accounting in order to perform it

prominently and effectively. Some regulations are mentioned below.

The procedure pertains some rules, standards and procedures of Generally Accepted

Accounting Principles (GAAP) which are designed as regulatory body for the prominent

and accurate preparation financial statement. The GAAP pertains several regulations like

Principle of Regularity, Consistency, Precedence and Periodicity etc.

Regulations regarding the International Financial reporting Standards are also required to

be follow by the accountants of the organisations like Taj accountancy firm (UK) as due

to it depicts the appropriate manner for reporting of particular transactions and events in

financial statements(Broadbent and Cullen, 2012).

Regulations regarding Financial Accounting like debit and credit rules of accounts and

their treatment in accounting are required to be follow by the accountant of organisation

like Taj accountancy firm (UK). So appropriate and accurate information reported in

financial statements.

Accordance with the Companies Act it becomes compulsory to produce the Books of

accounts for developing the knowledge of general public for enhancing their observations

2

from the business operational activities of the organisation(Edwards, 2013).

It is used for the purpose of ascertaining the financial performance of the business:

The accounting also used for the purpose of ascertaining the the financial performance of

the business organisations. As accounting helps in keeping the systematic record of the

past accounting years that renders a base or the comparative basis that is utilised by the

organisation to compare and ascertain the profit margin as well as the probability(Khan,

2015).

It is used to ensure effective decision making within the organisation: The financial

reporting helps the managers to make further futuristic decision regarding the business

operational activities of the organisations. With the help of accurate financial records

regarding the business activities it helps the managers to quantify the actual output from

the business activities and take further actions for ensuring more betterment and attaining

the more favourable outcomes(May, 2013).

(a) 2. Examining the regulations relating to financial accounting

There are some regulations for guiding the process of accounting in order to perform it

prominently and effectively. Some regulations are mentioned below.

The procedure pertains some rules, standards and procedures of Generally Accepted

Accounting Principles (GAAP) which are designed as regulatory body for the prominent

and accurate preparation financial statement. The GAAP pertains several regulations like

Principle of Regularity, Consistency, Precedence and Periodicity etc.

Regulations regarding the International Financial reporting Standards are also required to

be follow by the accountants of the organisations like Taj accountancy firm (UK) as due

to it depicts the appropriate manner for reporting of particular transactions and events in

financial statements(Broadbent and Cullen, 2012).

Regulations regarding Financial Accounting like debit and credit rules of accounts and

their treatment in accounting are required to be follow by the accountant of organisation

like Taj accountancy firm (UK). So appropriate and accurate information reported in

financial statements.

Accordance with the Companies Act it becomes compulsory to produce the Books of

accounts for developing the knowledge of general public for enhancing their observations

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and knowledge regarding the financial statements of any organisation and make their own

regarding the investment or disinvestment(Beatty and Liao, 2014).

(a) 3. Describing the Accounting rules and principles

Financial Accounting requires and pertain assorted set of rules and principles which are

required to be follow by each accountant of organisations like Taj Accountancy Firm (UK) while

the preparation of the financial statements which are mentioned underneath:

Debit the receiver, credit the giver: This principle mainly applied for the treatment of

Personal accounts. Some examples of personal account are debtors, banks, creditors, capital

account etc. when the organisation received something in form of cash raw material or anything

from other organisation or individual then in case of personal account the it must be crucial to

debit the account of that organisation or individual and if the organisation gives some cash or

anything to other organisation or person then it the account of that individual or organisation

must be credit(Edwards, 2013).

Debit all expenses and losses, credit all incomes and gains: This rule is applicable

while the treatment of Nominal accounts. Under the treatment of nominal account, all the

expenses and losses of the organisation are to be debited in the books of accounts and all the

incomes or gains of the organisations are to be credited(Needles, Powers and Crosson, 2013).

Debit what comes in, credit what goes out: This principle is mainly applicable while the

treatment of the real accounts. The real account pertain the machineries, land and buildings etc.

For example, an organisation acquire furniture of $ 30000 by cash, then the furniture comes

under the real account and furniture account is required to be debited by $ 30000 and cash

account must be credited by $ 30000.

Some principles of the Financial accounting are mentioned underneath:

Dual aspect concept: Dual aspect concept defines that the organisations are required to

record their business transactions accordance with the dual reporting concepts, it states

that every transaction has its double effects or must be recorded twice in the books of

accounts as double on both debit and credit side of books. As in case of Single entry

system every transactions are to be recorded once and it has only one aspect of the

transaction which leads to recording of relevant informational data in books of accounts

an inappropriate manner. That is why, in order to prevent such kind of problem the dual

3

regarding the investment or disinvestment(Beatty and Liao, 2014).

(a) 3. Describing the Accounting rules and principles

Financial Accounting requires and pertain assorted set of rules and principles which are

required to be follow by each accountant of organisations like Taj Accountancy Firm (UK) while

the preparation of the financial statements which are mentioned underneath:

Debit the receiver, credit the giver: This principle mainly applied for the treatment of

Personal accounts. Some examples of personal account are debtors, banks, creditors, capital

account etc. when the organisation received something in form of cash raw material or anything

from other organisation or individual then in case of personal account the it must be crucial to

debit the account of that organisation or individual and if the organisation gives some cash or

anything to other organisation or person then it the account of that individual or organisation

must be credit(Edwards, 2013).

Debit all expenses and losses, credit all incomes and gains: This rule is applicable

while the treatment of Nominal accounts. Under the treatment of nominal account, all the

expenses and losses of the organisation are to be debited in the books of accounts and all the

incomes or gains of the organisations are to be credited(Needles, Powers and Crosson, 2013).

Debit what comes in, credit what goes out: This principle is mainly applicable while the

treatment of the real accounts. The real account pertain the machineries, land and buildings etc.

For example, an organisation acquire furniture of $ 30000 by cash, then the furniture comes

under the real account and furniture account is required to be debited by $ 30000 and cash

account must be credited by $ 30000.

Some principles of the Financial accounting are mentioned underneath:

Dual aspect concept: Dual aspect concept defines that the organisations are required to

record their business transactions accordance with the dual reporting concepts, it states

that every transaction has its double effects or must be recorded twice in the books of

accounts as double on both debit and credit side of books. As in case of Single entry

system every transactions are to be recorded once and it has only one aspect of the

transaction which leads to recording of relevant informational data in books of accounts

an inappropriate manner. That is why, in order to prevent such kind of problem the dual

3

aspect principle requires that every and each transaction is required to be recorded on

both debit and credit side of accounts.

Cost principle: This principles examines that costs of business assets are required to be

recorded at accurate acquiring cost (costs price+installation charges). It means that

business assets must be recorded by the organisation at their costs of acquisition, as they

are obliged to evaluate the assets balances while preparing the several accounts and final

accounts such as depreciation accounting and balance sheet(Taipaleenmäki and

Ikäheimo, 2013).

Matching principle: This principle examines that the all the relevant expenses incurred

by the organisations are required to be charged to the income statement in an accounting

era in which revenues are earned. Furthermore, the expenses are required to be record in

the same period as the income to which it is associated(Parker and Fleischman, 2017).

(a) 4. Explaining the conventions and concepts relating to the consistency and material disclosure

Financial accounting framework comprises with the conventions which acts as the

guidelines that are required to follow while applying the principles of accounting practically.

The mandatory accepted conventions depends on practical facts and it renders the prominent

method or techniques to accountant for solving practical issues which are faced while preparing

the financial statements of business entity. Some conventions of Financial accounting are

mentioned underneath:

Convention of consistency: It is mandatory for the organisation to follow the concepts

and conventions continuously and on consistent basis. As it is crucial for the final

accounts, it is essential for ascertainment of the organisation to analyse the performances

on the basis of comparative analysis. Besides this, it is also essential for the comparative

of different organisation of different countries, if all organisations follows the same

conventions an d concepts. As from the point of view of investors it is also beneficiary

for the investors to make comparative analysis of the organisation which follows same

accounting methodology and concepts(Collier, 2015). So it can be termed as

indispensable to precede accounting principles and rules in a familiar manner and on

consistently and continuously basis. As it ensure the reliability to the financial report. For

example, if an organisation adapted the method of Straight line method for depreciating

the fixed assets but after some years the organisation changes the method and follows the

4

both debit and credit side of accounts.

Cost principle: This principles examines that costs of business assets are required to be

recorded at accurate acquiring cost (costs price+installation charges). It means that

business assets must be recorded by the organisation at their costs of acquisition, as they

are obliged to evaluate the assets balances while preparing the several accounts and final

accounts such as depreciation accounting and balance sheet(Taipaleenmäki and

Ikäheimo, 2013).

Matching principle: This principle examines that the all the relevant expenses incurred

by the organisations are required to be charged to the income statement in an accounting

era in which revenues are earned. Furthermore, the expenses are required to be record in

the same period as the income to which it is associated(Parker and Fleischman, 2017).

(a) 4. Explaining the conventions and concepts relating to the consistency and material disclosure

Financial accounting framework comprises with the conventions which acts as the

guidelines that are required to follow while applying the principles of accounting practically.

The mandatory accepted conventions depends on practical facts and it renders the prominent

method or techniques to accountant for solving practical issues which are faced while preparing

the financial statements of business entity. Some conventions of Financial accounting are

mentioned underneath:

Convention of consistency: It is mandatory for the organisation to follow the concepts

and conventions continuously and on consistent basis. As it is crucial for the final

accounts, it is essential for ascertainment of the organisation to analyse the performances

on the basis of comparative analysis. Besides this, it is also essential for the comparative

of different organisation of different countries, if all organisations follows the same

conventions an d concepts. As from the point of view of investors it is also beneficiary

for the investors to make comparative analysis of the organisation which follows same

accounting methodology and concepts(Collier, 2015). So it can be termed as

indispensable to precede accounting principles and rules in a familiar manner and on

consistently and continuously basis. As it ensure the reliability to the financial report. For

example, if an organisation adapted the method of Straight line method for depreciating

the fixed assets but after some years the organisation changes the method and follows the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Written down value method (WDV) , then it becomes necessary for the organisation to

follow the WDV method consistently and continuously.

Convention of material disclosure: Accordance with this convention, it is also required

that the organization must disclose all relevant informational data for the betterment of

the accounting procedure. Therefore the accounts are prepared in most prominent manner

that all material facts or information are required to disclose. It is also crucial for the

business entity to render all informational data in financial reports so that the investors,

creditors and owners becomes able to know about relevant business information related

to material. As it helps them in taking the further futuristic decisions and investment

decisions(Porter and Norton, 2012).

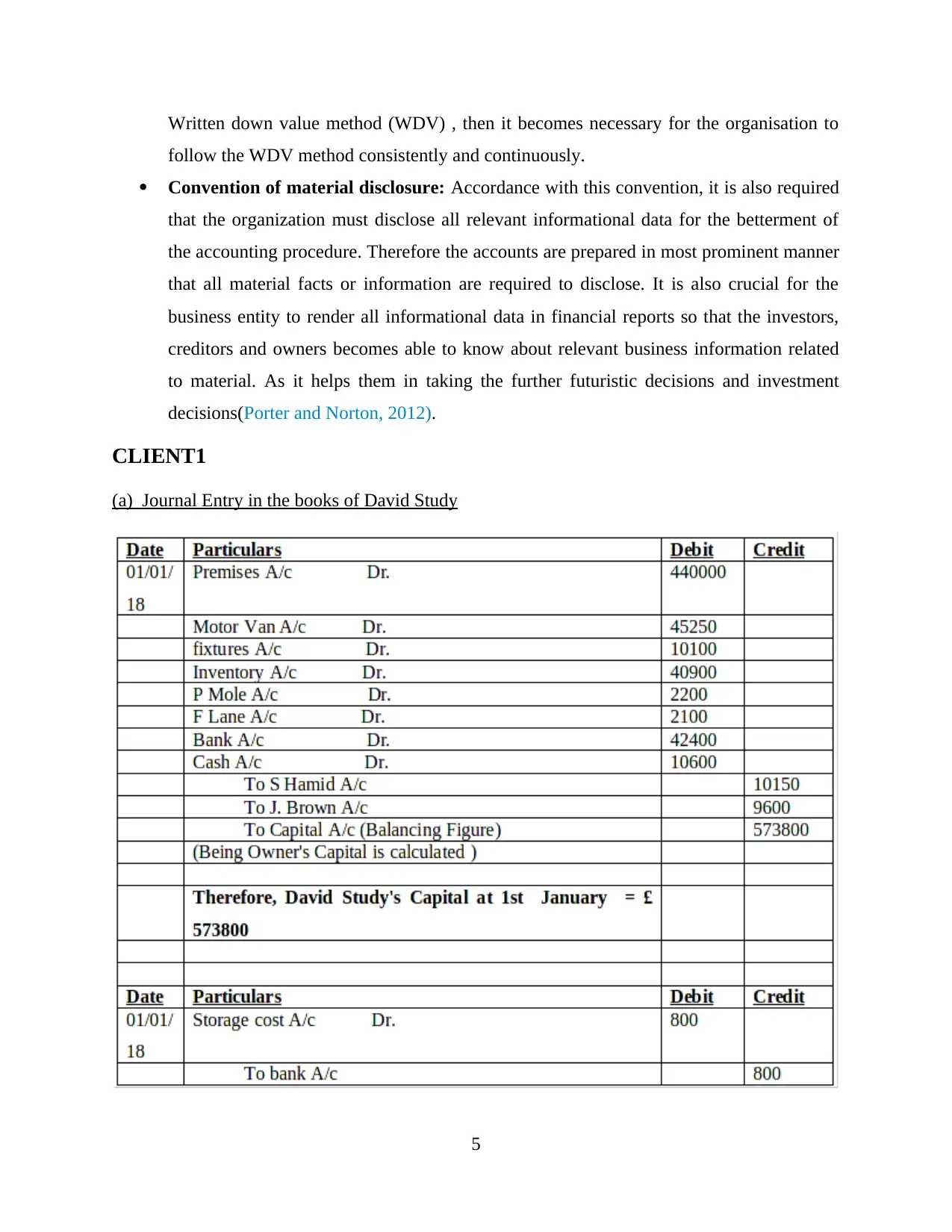

CLIENT1

(a) Journal Entry in the books of David Study

5

follow the WDV method consistently and continuously.

Convention of material disclosure: Accordance with this convention, it is also required

that the organization must disclose all relevant informational data for the betterment of

the accounting procedure. Therefore the accounts are prepared in most prominent manner

that all material facts or information are required to disclose. It is also crucial for the

business entity to render all informational data in financial reports so that the investors,

creditors and owners becomes able to know about relevant business information related

to material. As it helps them in taking the further futuristic decisions and investment

decisions(Porter and Norton, 2012).

CLIENT1

(a) Journal Entry in the books of David Study

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

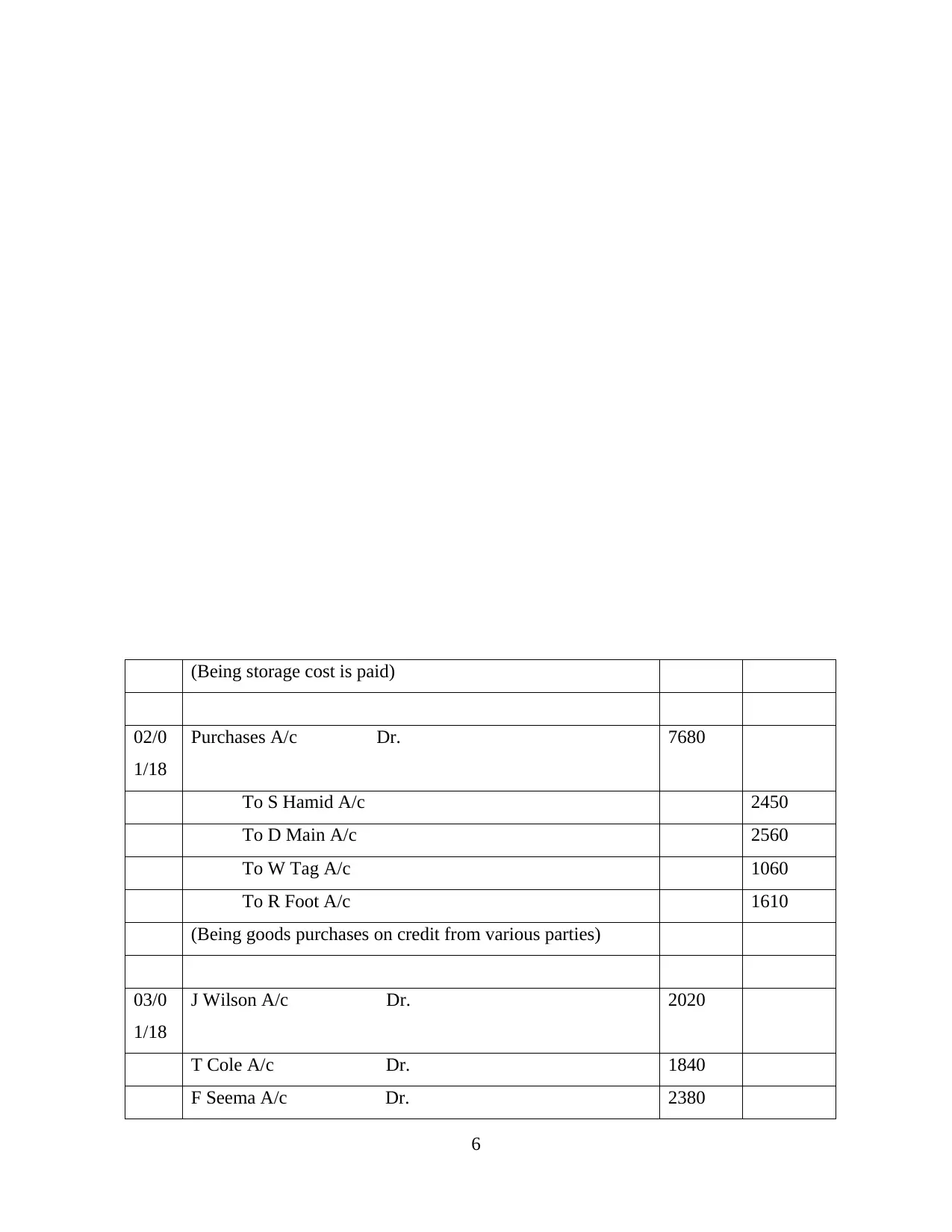

(Being storage cost is paid)

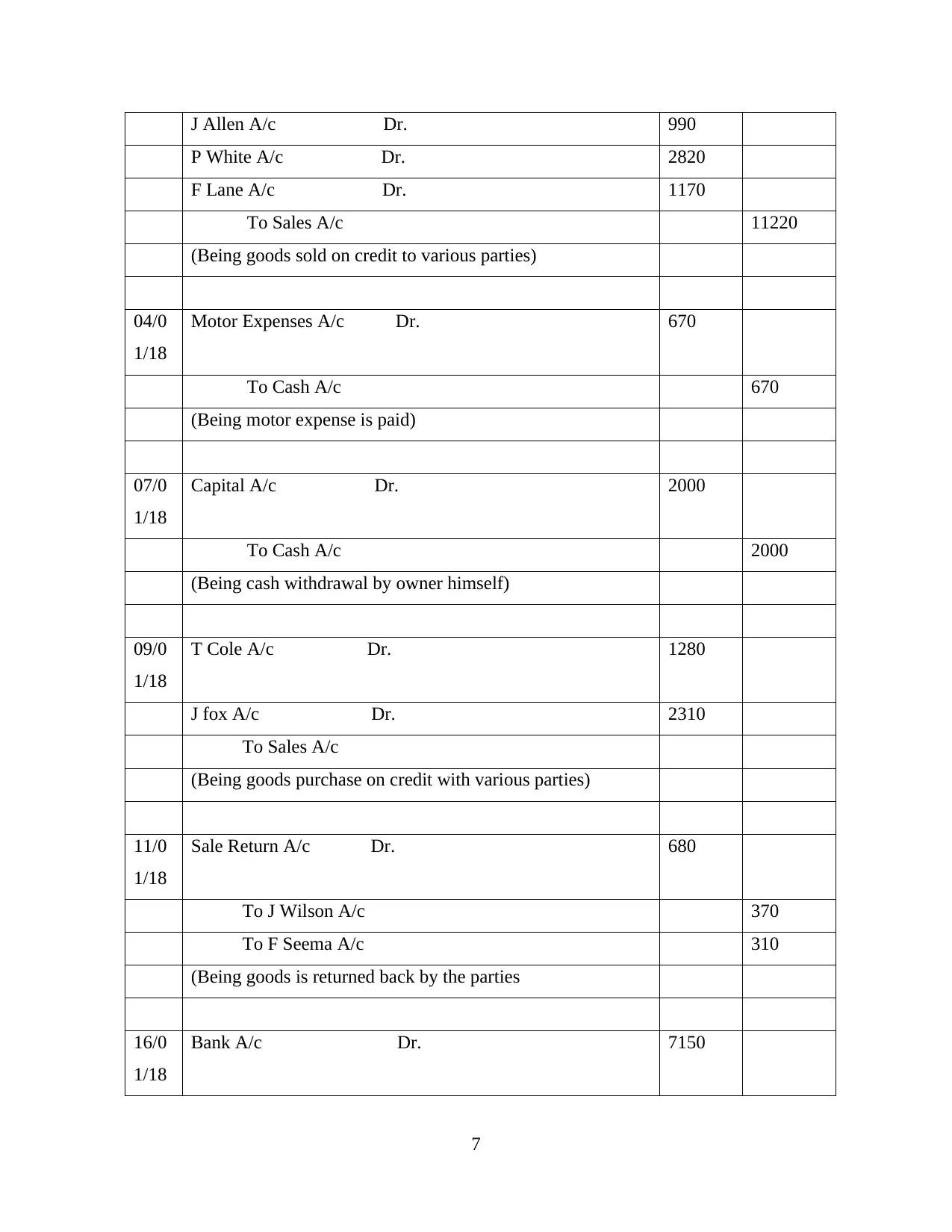

02/0

1/18

Purchases A/c Dr. 7680

To S Hamid A/c 2450

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/0

1/18

J Wilson A/c Dr. 2020

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

6

02/0

1/18

Purchases A/c Dr. 7680

To S Hamid A/c 2450

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/0

1/18

J Wilson A/c Dr. 2020

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

6

J Allen A/c Dr. 990

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c 11220

(Being goods sold on credit to various parties)

04/0

1/18

Motor Expenses A/c Dr. 670

To Cash A/c 670

(Being motor expense is paid)

07/0

1/18

Capital A/c Dr. 2000

To Cash A/c 2000

(Being cash withdrawal by owner himself)

09/0

1/18

T Cole A/c Dr. 1280

J fox A/c Dr. 2310

To Sales A/c

(Being goods purchase on credit with various parties)

11/0

1/18

Sale Return A/c Dr. 680

To J Wilson A/c 370

To F Seema A/c 310

(Being goods is returned back by the parties

16/0

1/18

Bank A/c Dr. 7150

7

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c 11220

(Being goods sold on credit to various parties)

04/0

1/18

Motor Expenses A/c Dr. 670

To Cash A/c 670

(Being motor expense is paid)

07/0

1/18

Capital A/c Dr. 2000

To Cash A/c 2000

(Being cash withdrawal by owner himself)

09/0

1/18

T Cole A/c Dr. 1280

J fox A/c Dr. 2310

To Sales A/c

(Being goods purchase on credit with various parties)

11/0

1/18

Sale Return A/c Dr. 680

To J Wilson A/c 370

To F Seema A/c 310

(Being goods is returned back by the parties

16/0

1/18

Bank A/c Dr. 7150

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

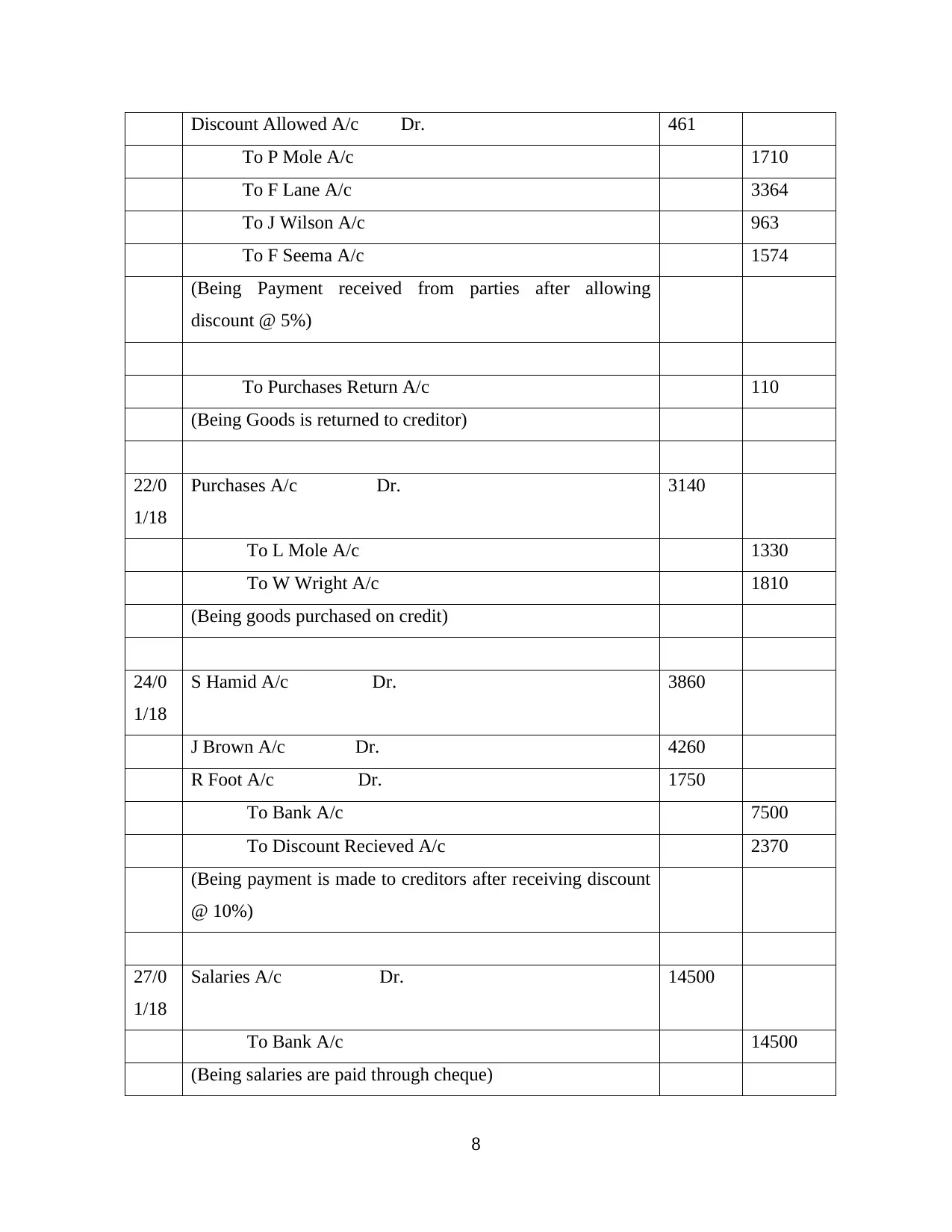

Discount Allowed A/c Dr. 461

To P Mole A/c 1710

To F Lane A/c 3364

To J Wilson A/c 963

To F Seema A/c 1574

(Being Payment received from parties after allowing

discount @ 5%)

To Purchases Return A/c 110

(Being Goods is returned to creditor)

22/0

1/18

Purchases A/c Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/0

1/18

S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors after receiving discount

@ 10%)

27/0

1/18

Salaries A/c Dr. 14500

To Bank A/c 14500

(Being salaries are paid through cheque)

8

To P Mole A/c 1710

To F Lane A/c 3364

To J Wilson A/c 963

To F Seema A/c 1574

(Being Payment received from parties after allowing

discount @ 5%)

To Purchases Return A/c 110

(Being Goods is returned to creditor)

22/0

1/18

Purchases A/c Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/0

1/18

S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors after receiving discount

@ 10%)

27/0

1/18

Salaries A/c Dr. 14500

To Bank A/c 14500

(Being salaries are paid through cheque)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

30/0

1/18

Business Rates A/c Dr. 2220

To Bank A/c 2220

(Being business rates are paid through cheque)

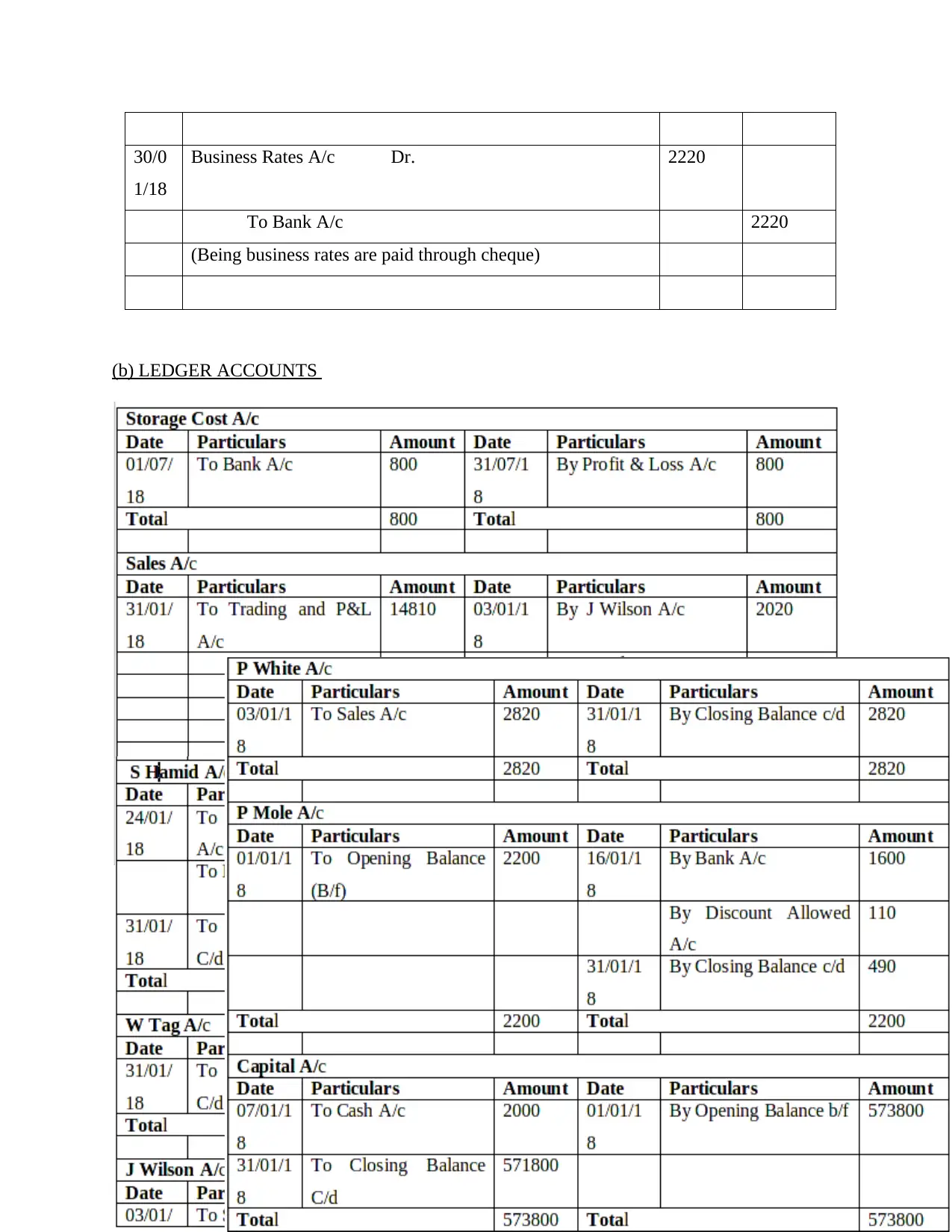

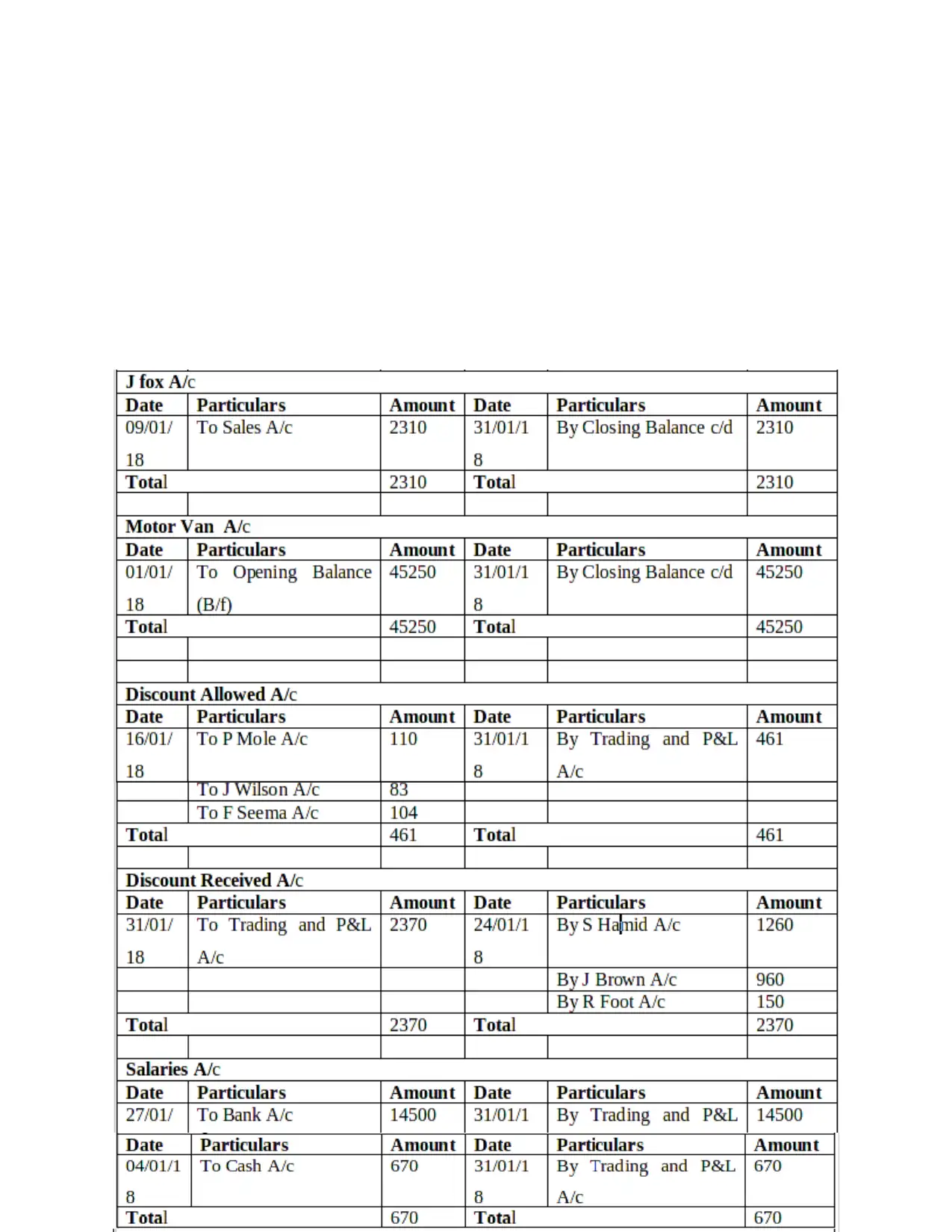

(b) LEDGER ACCOUNTS

9

1/18

Business Rates A/c Dr. 2220

To Bank A/c 2220

(Being business rates are paid through cheque)

(b) LEDGER ACCOUNTS

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.