Financial Accounting Assignment: FNSACC504 Assessment 2 Solution

VerifiedAdded on 2020/02/05

|15

|3277

|205

Homework Assignment

AI Summary

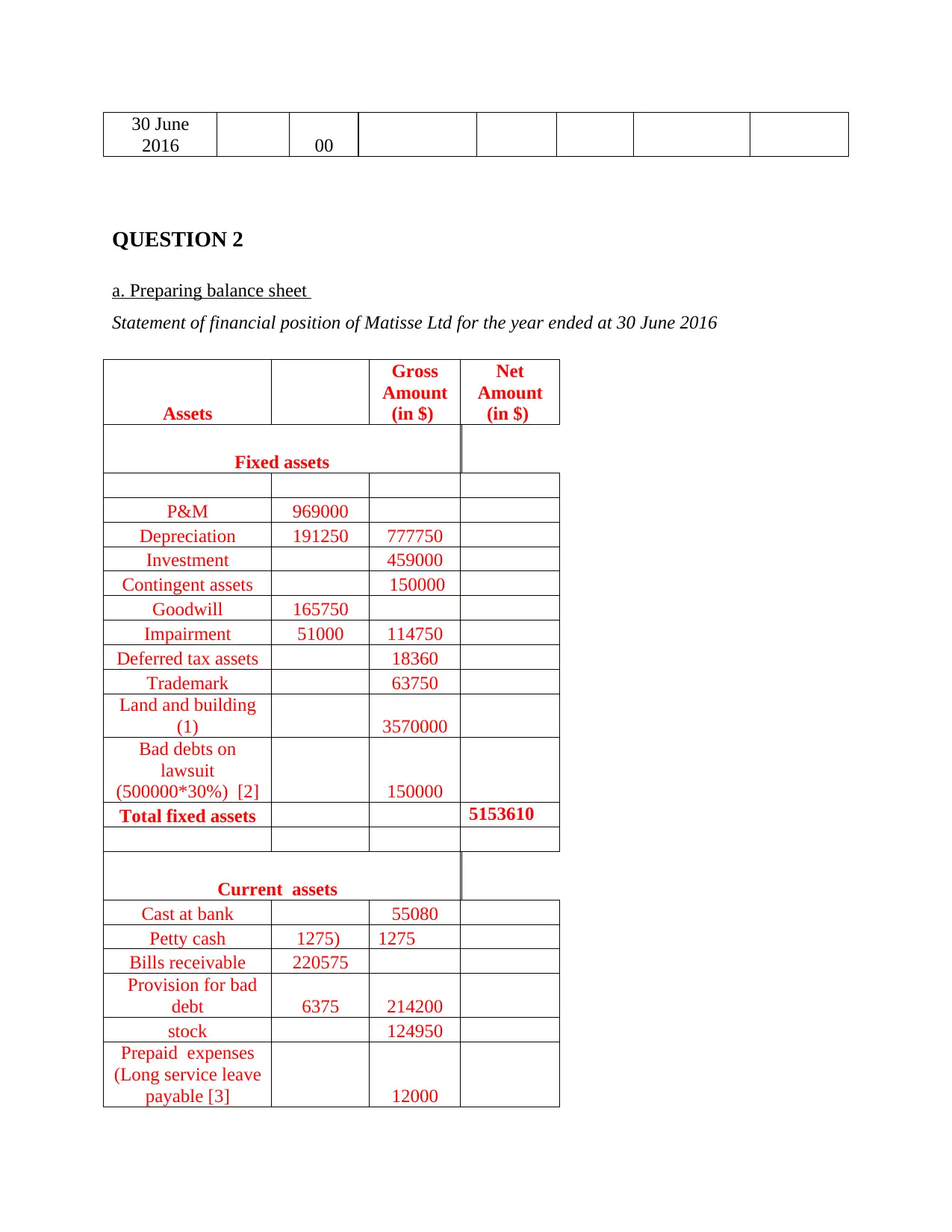

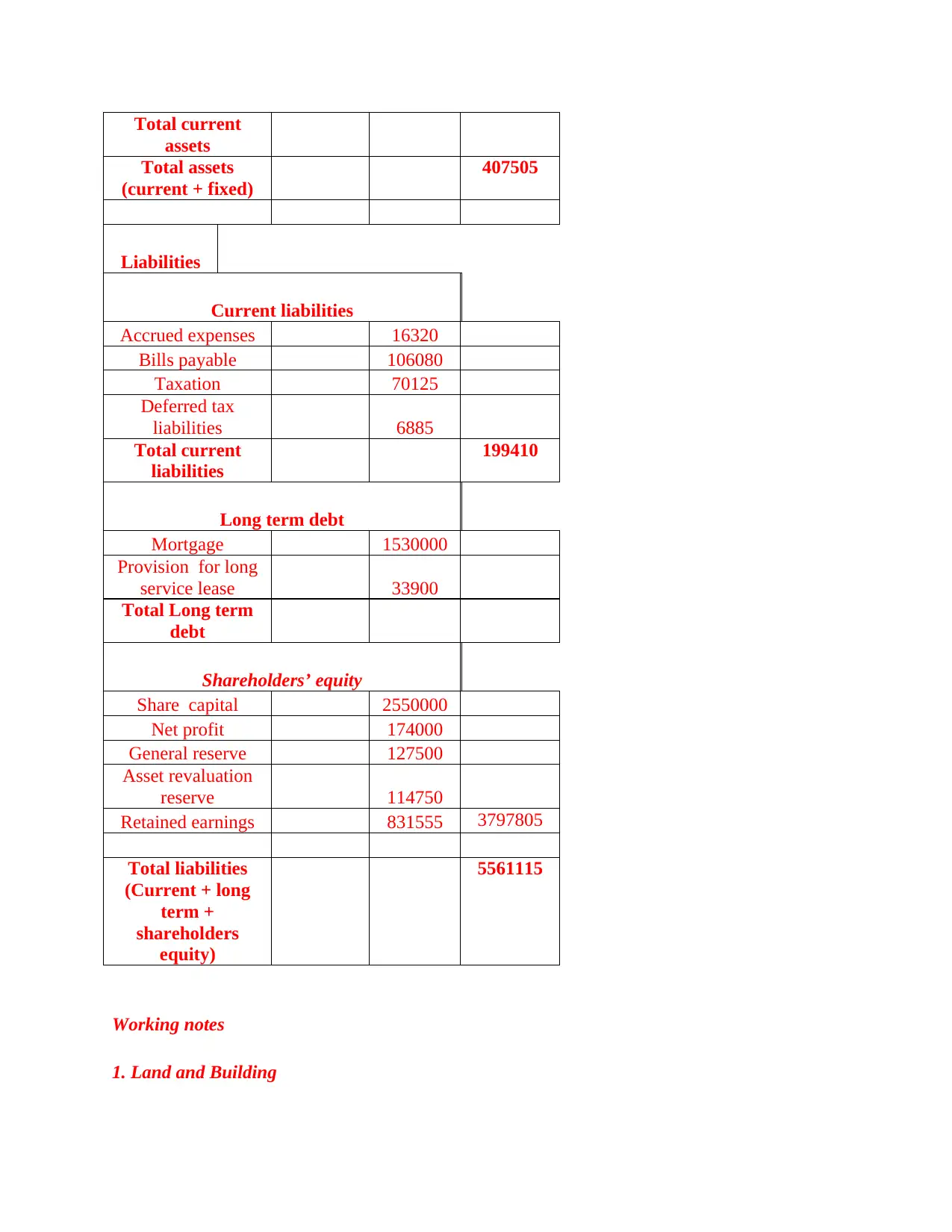

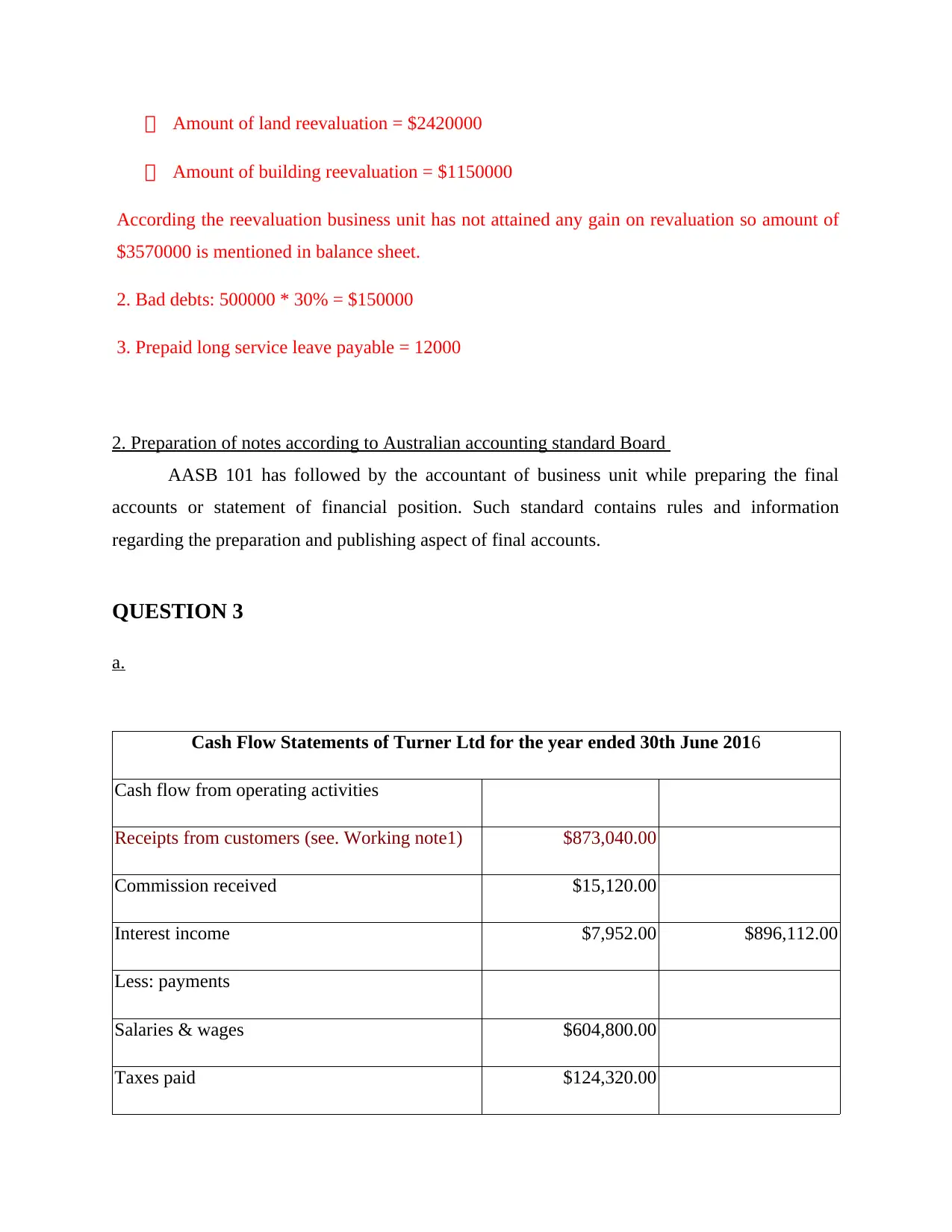

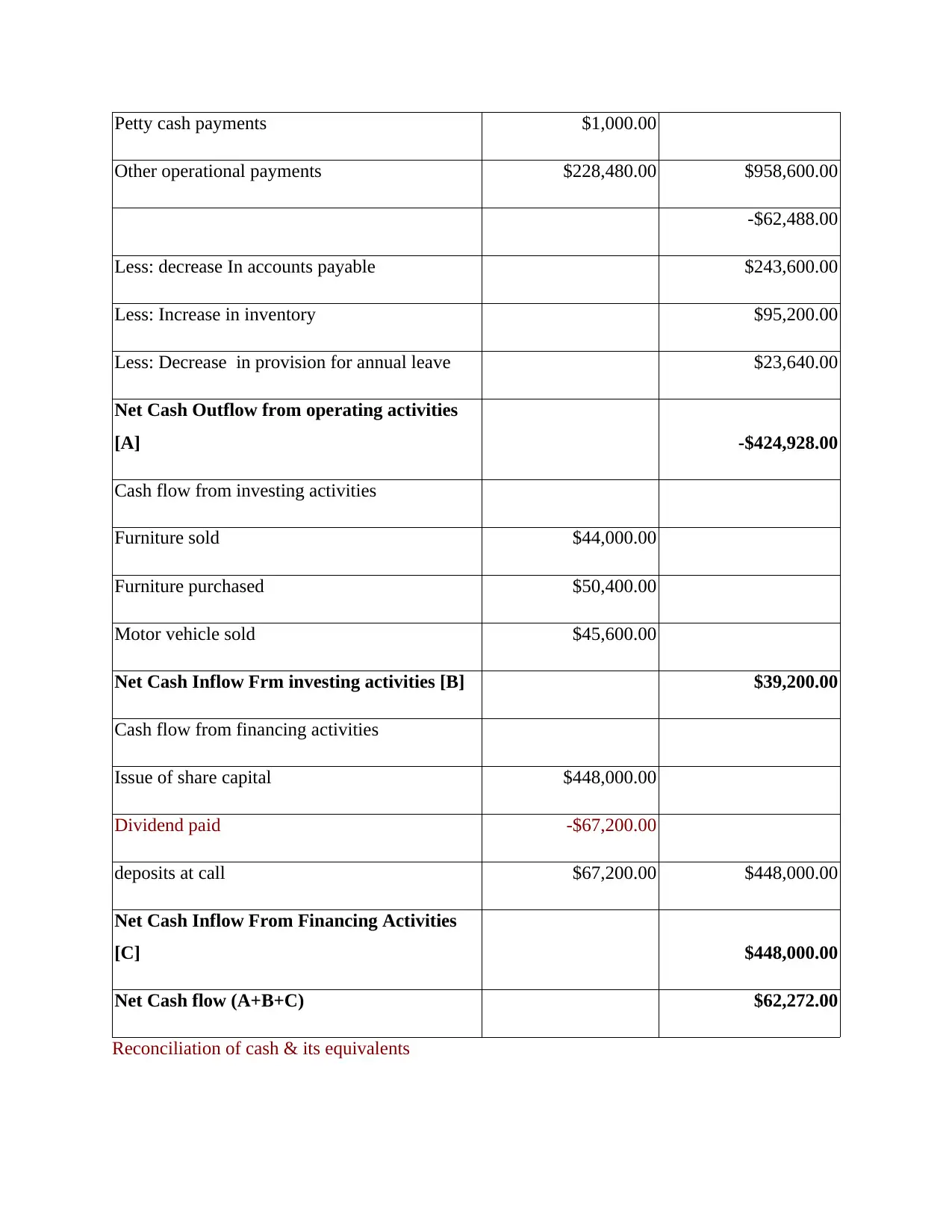

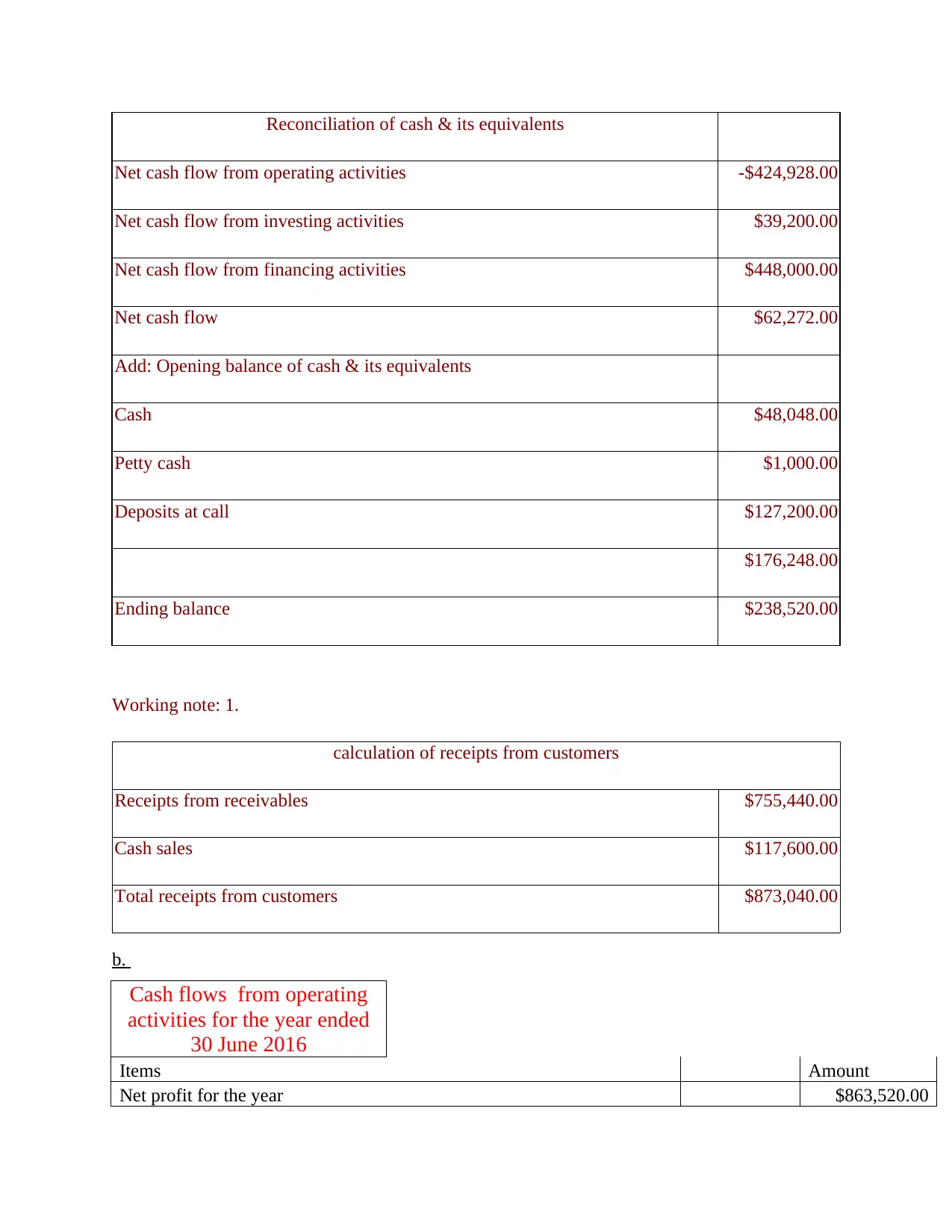

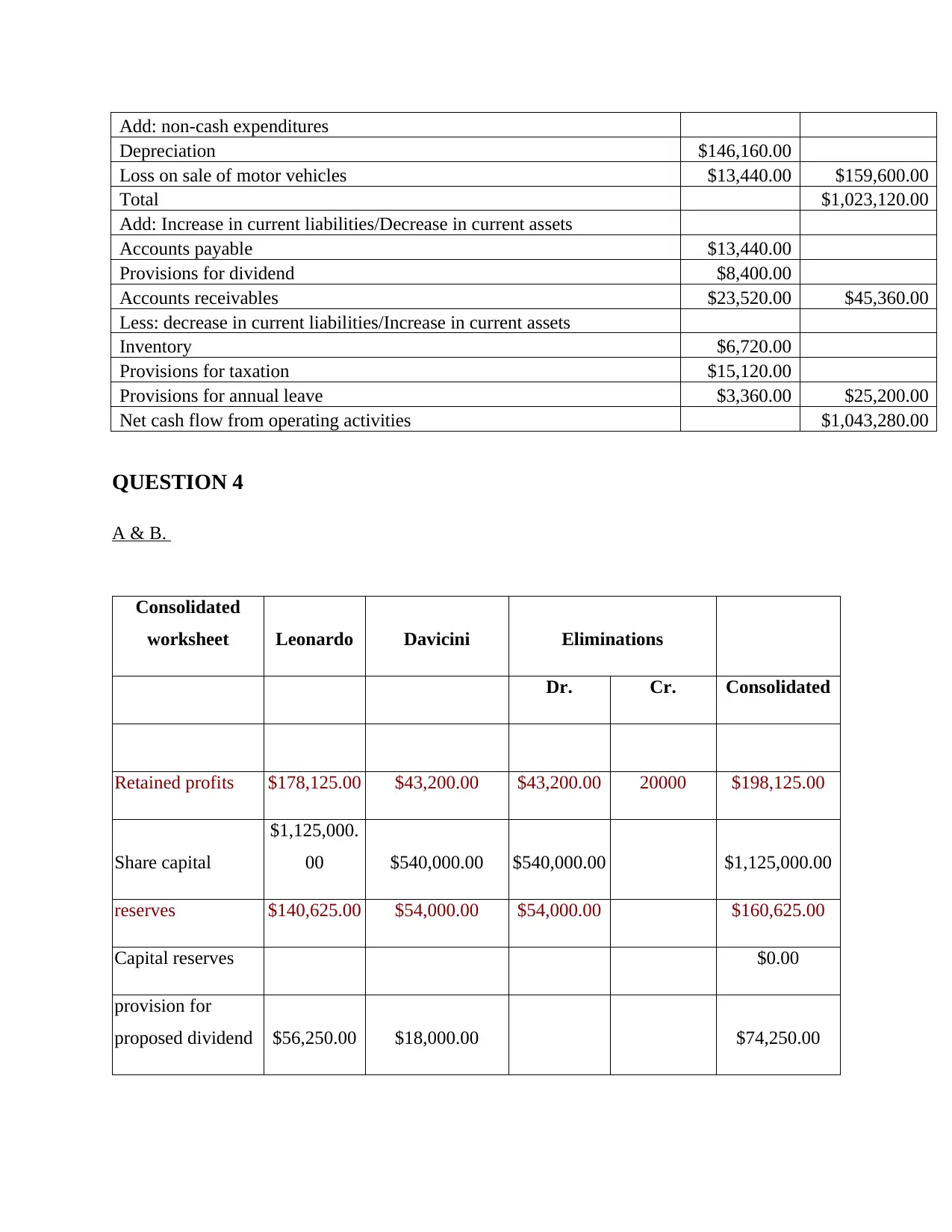

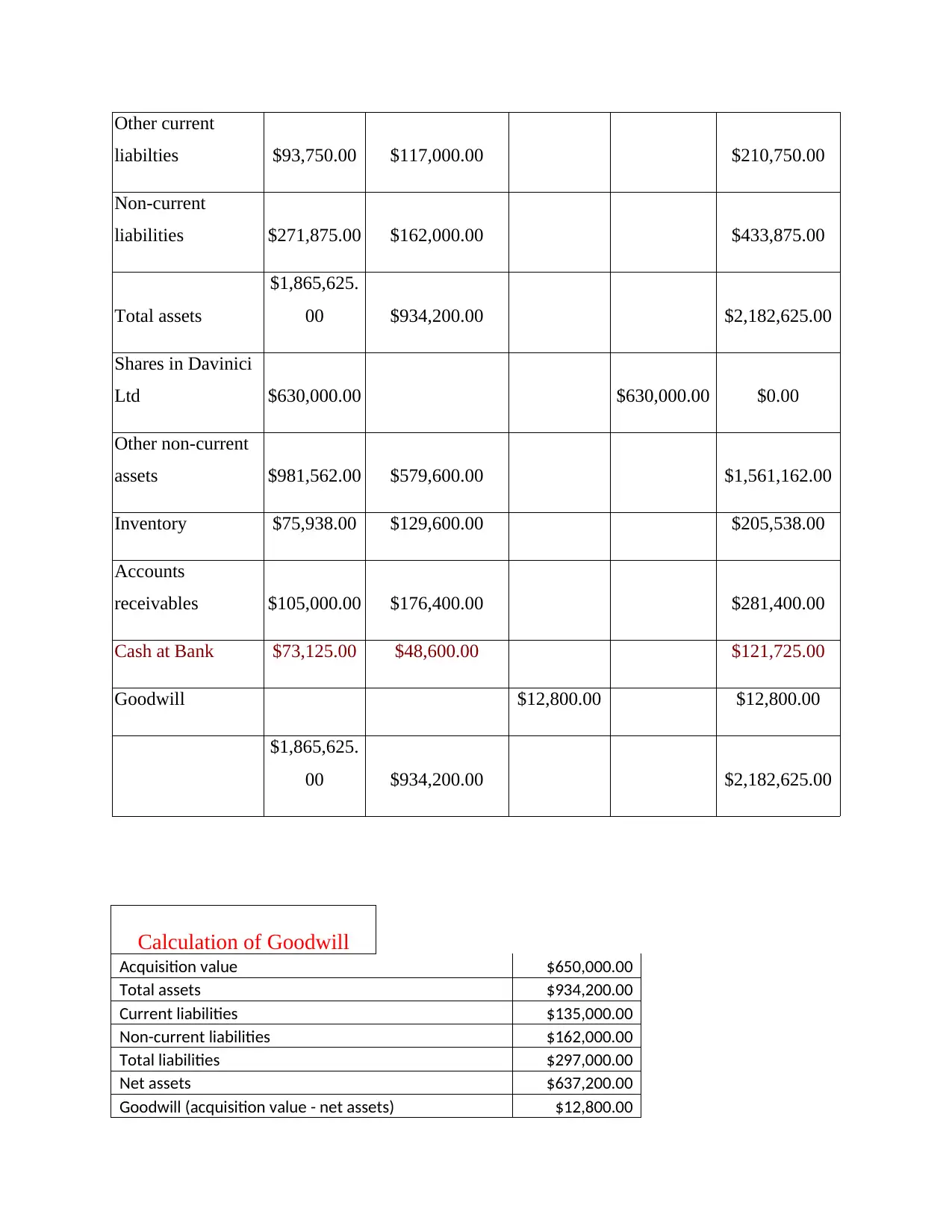

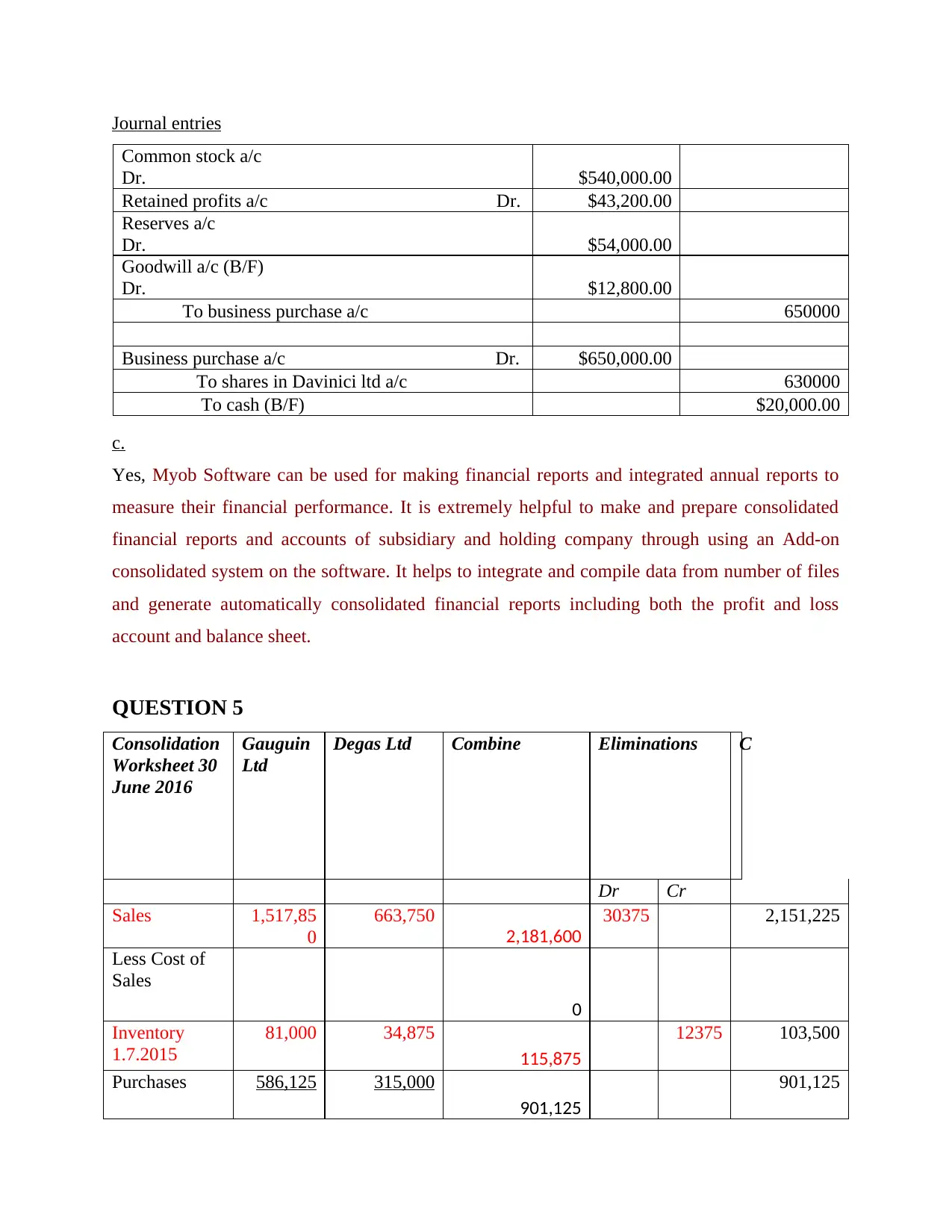

This document presents a comprehensive solution to a financial accounting assignment, specifically addressing the requirements of FNSACC504 Assessment 2. The solution includes detailed preparation of a Profit and Loss (P&L) account, along with supporting notes and illustrations of expenses. It covers the preparation of a statement of changes in equity, a balance sheet with accompanying notes according to Australian accounting standards, and a cash flow statement. Furthermore, the assignment delves into consolidation, providing consolidated worksheets, journal entries, and an overview of the use of accounting software like MYOB. The solution encompasses all five questions outlined in the assignment brief, offering a thorough understanding of financial accounting principles and practices.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.